Crypto World

Crypto funds shed $4B as outflows hit five-week streak

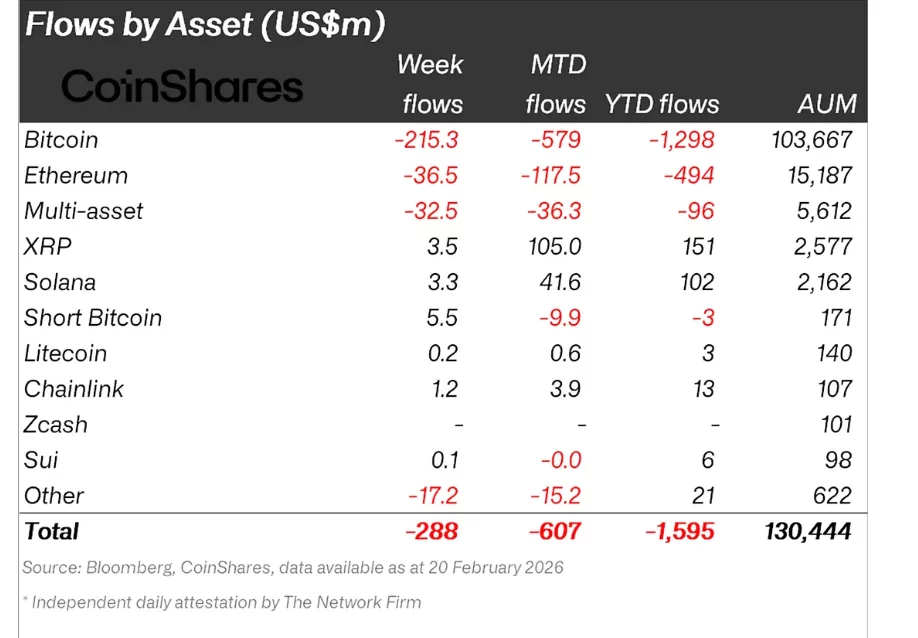

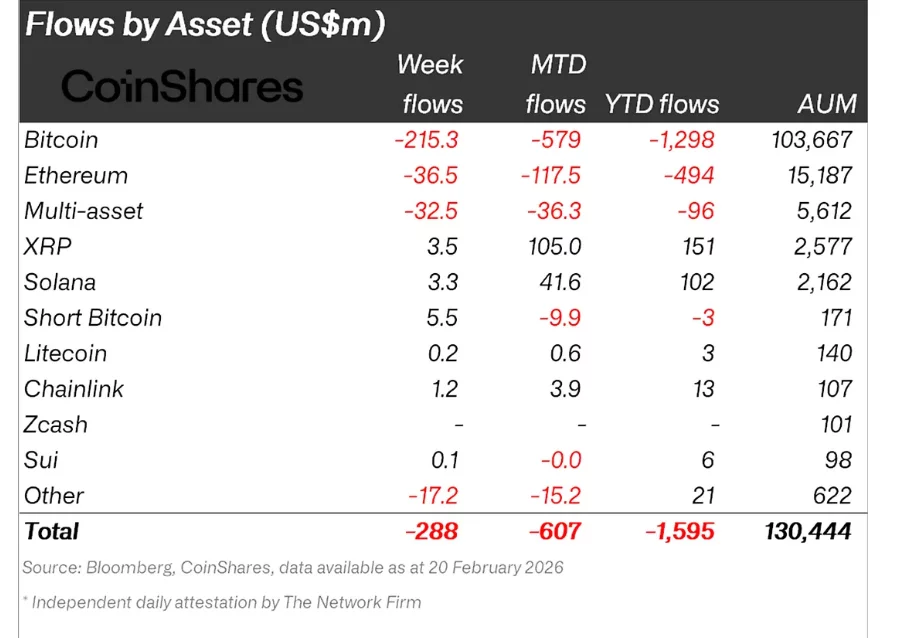

Crypto funds recorded $288 million in outflows last week, marking the fifth consecutive week of declines, according to the latest weekly report from CoinShares.

Summary

- Digital asset investment products saw $288 million in weekly outflows, marking the fifth consecutive week of withdrawals and bringing the cumulative total to $4 billion over the period.

- The United States led redemptions with $347 million in outflows, while Europe and Canada recorded modest inflows, highlighting a regional divergence in sentiment.

- Bitcoin accounted for the bulk of withdrawals, while short-bitcoin products and select altcoins such as XRP and Solana saw minor inflows.

US sells, Europe buys: Crypto funds show sharp regional divide

The latest withdrawals bring cumulative outflows over the current stretch to $4.0 billion, highlighting persistent weakness in investor sentiment.

Trading activity also cooled significantly. Total volumes across crypto exchange-traded products fell to $17 billion, the lowest level since July 2025, after several weeks of elevated turnover. The sharp decline in activity suggests growing investor apathy following recent market turbulence.

Regional flows reveal a widening divergence in sentiment.

The United States accounted for $347 million in outflows, reflecting continued caution among U.S. investors. In contrast, Europe and Canada recorded a combined $59 million in inflows, as some investors appeared to view recent price weakness as a buying opportunity.

Switzerland led regional inflows with $19.5 million, followed by Canada at $16.8 million and Germany at $16.2 million.

Bitcoin leads $288M weekly outflows

Bitcoin (BTC) remained the primary driver of weakness, with $215 million in outflows, representing the largest share of redemptions. Meanwhile, short-bitcoin products saw $5.5 million in inflows, the highest of any category, suggesting some investors are positioning for further downside.

Ethereum (ETH) experienced the second-largest withdrawals at $36.5 million, while multi-asset products and Tron saw outflows of $32.5 million and $18.9 million, respectively.

Among altcoins, minor inflows were recorded in XRP ($3.5 million), Solana ($3.3 million), and Chainlink ($1.2 million), though these were insufficient to offset broader market weakness.

Despite the ongoing selloff, total assets under management remain substantial at $130.4 billion, indicating that while sentiment is subdued, institutional exposure to digital assets persists.

Bitcoin dipped below $63,000 during Asian trading hours, extending overnight weakness amid President Donald Trump’s tariffs and AI jitters that have soured investor sentiment.

The leading cryptocurrency by market value is already down nearly 7% for the week, trading at levels last seen on Feb. 6 when prices nearly dropped to $60,000, CoinDesk data shows.

“Similar to equities, Bitcoin has had a sharp pullback today, driven largely by renewed tariff-related uncertainty, similar to the events of April 2025. Furthermore, ratcheting geopolitical tensions could likely prove bearish for BTC in the short-term,” Matt Howells-Barby, vice president at Kraken, Pro Trader, and host of Trading Spaces, told CoinDesk in an email.

He added that the $60,000 level is a key support that bulls are watching closely. “If that level fails to hold, we could potentially see a move into the mid-to-low $50K range,” he noted.

The U.S. stocks fell Monday after Trump said he would place temporary 15% tariffs on imports from other countries, up from the 10% rate announced Friday following the Supreme Court’s decision to struck down his tariffs strategy. Meanwhile, investors continued to sell shares in companies that stand to lose the AI revolution.

History favors a deeper sell-off in BTC

History shows BTC rarely bottoms until the 50-week average price crosses below the 100-week average price. This so-called bear cross has marked the end of every major bear market, including those in 2022 and 2018.

We’re nowhere near that signal today, as the 50-week average price remains well above the 100-week.

So, if past data is a guide, the market could slide further, potentially to $50,000 or lower, as several experts told CoinDesk at Consensus Hong Kong before the averages cross bearish and capitulation sets in.

The pattern may seem counterintuitive: The 50-week average dropping below the 100-week signal further weakens momentum.

But it fits the moving averages’ lagging nature perfectly: crossovers confirm what’s already happened – not predict what’s next – so long-term ones have tended to market bear market bottoms in bitcoin.

That said, as with any indicator, the past record offers no assurance of future results.

The Federal Reserve is moving to enshrine a rule that would remove reputational risk as a driver of banking supervision, a shift crypto advocates say could blunt a pattern of debanking in recent years. The central bank began codifying the change last June, directing its supervisors to stop pressuring banks to sever client ties over reputation concerns and instead assess banking relationships primarily through financial risk management. Now, in a formal rulemaking proposal published on Monday, the Fed is inviting public comment on turning that approach into law, with a 60-day window to hear from stakeholders. The initiative arrives amid ongoing debates about the boundaries of political and ideological considerations in financial services and bears directly on how crypto firms access banking pathways that were once routine.

The Fed’s upward move comes with explicit acknowledgment of the concerns raised by lawmakers and industry observers about how reputation risk has been wielded in ways that affect crypto and other disfavored sectors. In the accompanying release, vice chair for supervision Michelle Bowman framed the issue in stark terms: “We have heard troubling cases of debanking — where supervisors use concerns about reputation risk to pressure financial institutions to debank customers because of their political views, religious beliefs, or involvement in disfavored but lawful businesses.” She stressed that discrimination on these bases runs counter to federal policy and has no place in the Fed’s supervisory framework. The push to formalize this standard reflects a desire to shield legitimate business activity from ad hoc revocation of banking access under the guise of reputation risk.

As the digital asset ecosystem pushes for clearer rules and a more stable banking landscape, political observers weighed in as well. In a post on X, Senator Cynthia Lummis lauded the Fed’s move, arguing that it should not be the regulator’s role to adjudicate who can participate in the crypto economy. She framed the reform as a breaking point that could help “permanently remove ‘reputation risk’ from Fed policy and put Operation Chokepoint 2.0 to rest so America can become the digital asset capital of the world.” The sentiment was echoed by Galaxy Digital’s head of firmwide research, Alex Thorn, who lauded the development as part of the industry’s ongoing push to roll back what supporters call choke points in traditional finance. Thorn signaled via X that the rollback continues, underscoring the ongoing tension between crypto firms seeking direct access to banking services and legacy financial institutions wary of reputational exposure.

Operation Chokepoint 2.0 is a label used within crypto circles to describe what some perceived as a coordinated effort by the Biden administration and the banking sector to restrict crypto firms’ access to essential banking services. The discourse around this concept has included references to previous policy debates and actions that crypto insiders argued were designed to curb the industry’s growth by pressuring banks to sever ties. The Fed’s latest move—aimed at removing reputation-based triggers from supervisory decisions—has been positioned by supporters as a corrective step toward neutral, risk-based decisions that prioritize financial metrics over political or ideological considerations. The discourse surrounding debanking isn’t new: disclosures and investigations have connected the policy debate to broader questions about regulatory overreach, financial privacy, and the U.S.’s stance toward crypto innovation.

The policy questions extend beyond banking practices into the political discourse around regulation. The administration has signaled an intent to curb debanking in the United States, with discussions touching on how regulators should approach crypto-related clients. The public record features a mix of official statements and industry commentary about the proper balance between safeguarding the financial system and enabling a vibrant digital asset sector. The thread linking this initiative to broader regulatory reform remains a focal point for crypto firms seeking greater clarity and predictability in how banks evaluate risk and structure services for digital assets.

In parallel, proponents of the reform have pointed to links between reputational considerations and broader regulatory strategies aimed at safeguarding consumers while not constraining legitimate innovation. The Fed’s invitation for public comment signals a willingness to test the proposed framework against diverse viewpoints before any final rule is enshrined. If adopted, the rule could set a precedent for how U.S. supervisory agencies weigh risk and approach non-financial considerations in decisions that affect access to fundamental banking services for crypto businesses and other sectors that have faced similar pressures.

Beyond the policy debate, the legal and practical implications loom large. Some observers have highlighted how banks may recalibrate due to the clarity this rule would provide or because it reduces discretionary leverage tied to reputational risk. Others warn that a formalized standard would still require careful definition to avoid unintended consequences, such as banks underreacting to financial risk signals or inadvertently channeling risk through opaque channels. In the end, the rule’s success hinges on how well the Fed can translate a principle into a measurable framework that stands up to scrutiny and serves as a reliable reference for bankers, crypto firms, and regulators alike. The Fed’s consultation period will be a key barometer of how broad support is for codifying this approach and what refinements may be necessary to address edge cases and evolving digital-asset landscapes.

The evolving narrative around debanking and regulatory clarity has also intersected with political dimensions, including ongoing disputes over how bank accounts are treated during periods of political or ideological contention. While the Fed’s move is framed as a technical adjustment to supervisory practice, the broader implications touch on the dynamics of financial inclusion, national competitiveness in the crypto space, and the boundaries of regulatory intervention in private-sector decisions. As negotiators and policymakers weigh the future of digital asset markets, this rulemaking could become a touchstone for how the United States balances the need to manage risk with the desire to foster innovation and maintain the country’s pull in the global crypto economy. The public comment period will determine not only the technical shape of the rule but also the degree to which the policy resonates across industry, advocacy groups, and financial institutions that must implement it in the months ahead.

Key takeaways

- The Fed is seeking to codify the removal of reputation risk as a factor in banking supervision, a move crypto advocates view as reducing punitive pressure on banks over political or ideological considerations.

- A 60-day public-comment window accompanies the proposal, signaling an invitation for industry, lawmakers, and the public to weigh in on the formal rule.

- The initiative follows a June policy shift in which the Fed directed supervisors to base decisions on financial risk management rather than reputational concerns.

- Supporters, including lawmakers and industry figures, frame the reform as a step toward restoring access to banking for crypto firms and ending what critics call “Chokepoint 2.0.”

- Opponents may push for careful definitions of “reputation risk” to avoid unintended loopholes or gaps in enforcement that could leave some customers exposed to informal criteria.

Market context: The policy sits within a broader regulatory environment where liquidity, risk sentiment, and clarity around digital assets influence the willingness of traditional banks to service crypto clients. As policymakers push for explicit standards, market participants look for predictable frameworks that reduce opacity in a space historically marked by sudden access changes and reputational triggers.

Why it matters

For crypto companies, the Fed’s potential rule offers a clearer path to banking access that is less contingent on perceived reputational concerns. In a sector where financial infrastructure—payments, settlement, and treasury services—can determine a project’s viability, a formal standard buffers firms against abrupt disconnections from banking rails. The change could also incentivize banks to adopt uniform risk-based criteria, improving consistency across institutions and reducing the likelihood that decisions are swayed by external factors unrelated to financial health.

From a policy perspective, the move indicates an intent to articulate a more transparent governance framework for supervisory actions. If successfully enacted, the rule could help normalize the treatment of crypto firms within mainstream financial services and strengthen the U.S. position as a hub for digital asset innovation. Support from lawmakers who view debanking as a civil-rights or anti-competitive concern further underscores the political resonance of the issue, elevating the debate beyond technocratic risk management into a broader discussion about access to finance and national competitiveness.

Nevertheless, the discussion remains nuanced. Advocates stress the need for precise definitions to avoid softening risk controls or eroding the ability of regulators to intervene when broader financial crime or consumer protection concerns arise. The rule will likely require ongoing refinement to address newly emergent business models and evolving threats, including opaque financial arrangements or non-traditional counterparties that still carry risk. The Fed’s engagement with industry stakeholders, as evidenced by the 60-day comment period, will be a critical litmus test for how quickly and effectively a clearer, more stable regime can take shape.

What to watch next

- Public comments: The 60-day window opens with the formal proposal and should yield a spectrum of views from banks, crypto firms, consumer groups, and policymakers.

- Final rule release: The Fed will publish the final text, outlining definitions, enforcement mechanisms, and transition timelines for banks to align with the new standard.

- Banking industry response: Expect filings, memos, and industry white papers detailing how lenders foresee applying the rule in practice and where they foresee friction or ambiguities.

- Regulatory coordination: Observers will look for alignment with other regulators’ approaches to reputational risk and how the rule interacts with anti-money-laundering and sanctions regimes.

Sources & verification

- Federal Reserve press release: June 23, 2025, announcing changes to supervision focused away from reputation risk

- Federal Reserve press release: February 23, 2026, inviting public comment on turning the approach into law

- Senator Cynthia Lummis (X) post praising the move: https://x.com/senlummis/status/2026060712305365065

- Galaxy Digital Alex Thorn (X) post commenting on the rollback: https://x.com/intangiblecoins/status/2026069012124164150

- Cointelegraph article: Operation Chokepoint crypto banking restrictions

Market reaction and key details

The Fed’s initiative to codify reputation-risk exclusion from supervisory judgment underscores a broader shift toward risk-based banking decisions that foreground financial metrics over reputational considerations. The formal rulemaking process, including a 60-day comment window, invites a wide spectrum of perspectives, ensuring that the final framework balances financial stability with the industry’s push for more straightforward access to banking services. Industry observers note that the policy’s success will hinge on how clearly the Fed defines “reputation risk” and how it handles edge cases where reputational concerns intersect with legitimate risk signals. The conversation also weaves in the historical debate around “Operation Chokepoint 2.0,” a label used by crypto insiders to describe perceived regulatory and banking pressures on crypto firms, which the current proposals seek to reverse or at least diminish in influence over supervisory outcomes. The official narrative aligns with a broader push to position the United States as a competitive, innovation-friendly environment for digital assets while maintaining guardrails that deter illicit activity.

The momentum behind the policy has drawn attention from lawmakers and industry figures who argue it could restore a more predictable banking environment for crypto companies. The ongoing public debate touches on questions of how much regulatory discretion should be exercised based on non-financial considerations and how transparent the decision-making process should be for banks that service digital-asset businesses. With the 60-day window now open, observers will be watching not only for the rule’s final form but also for the evidence of consensus around where the balance should lie between risk control and access to essential banking services.

Ultimately, the Fed’s proposed rule is part of a larger narrative about how the United States intends to steward innovation in the digital asset space while preserving the integrity of the financial system. If the rule stands up to scrutiny and gains broad support, it could reduce the volatility that arises when firms lose access to banking for reasons tied more to reputation than to tangible financial risk. For participants across the industry—from fintech startups to established crypto exchanges—the development represents a potential turning point in the governance of banking relationships and the speed at which the U.S. can keep pace with global peers in the digital economy.

A new report by Citrini Research has been partially blamed for a software and payments stock sell-off on Monday, where it outlined extreme scenarios in which AI could severely disrupt the economy, from wiping out a sizable share of the workforce and slashing consumer spending to threatening the $13 trillion US mortgage market.

Citrini was little-known up until Monday, when its “Global Intelligence Crisis” report amassed over 22 million views on X alone and discussed how AI agents could drive corporate profits so high that human labor could become increasingly redundant and trigger a recession.

The report lays out a chilling June 2028 scenario, in which the Standard & Poor’s 500 is down 38% from its all-time high, unemployment is over 10%, private credit is unraveling and prime mortgages are cracking — all while AI didn’t disappoint, exceeding every expectation.

Citrini said the term “Ghost GDP” could emerge, describing it as output that shows up in the national accounts but never circulates through the “real economy.”

“A single GPU cluster in North Dakota is generating output previously attributed to 10,000 Manhattan office workers,” Citrini theorized in a potential June 2028 scenario.

The result: a massive white-collar layoff, far less consumer spending and a recession, Citrini said.

The macroeconomic uncertainty from AI and other issues, such as US President Donald Trump’s tariffs, has not been taken well in the crypto market over the past few months, with Bitcoin (BTC) falling nearly 50% from its $126,080 all-time high in early October, while safe havens like gold continue to rise.

AI, credit card stocks tank

Computing and AI company IBM saw its largest single-day drop in 25 years on Monday, tumbling 13.1% to $223.35, while Microsoft, Oracle and Accenture fell 3.21%, 4.57% and 6.58%, Google Finance data shows.

Credit card platforms Visa, Mastercard and American Express also fell 4.5%, 5.77% and 7.2% as Citrini said private credit and software-backed loans would face cascading defaults.

Investor anxiety was compounded by warnings from renowned risk theorist Nassim Taleb, who said AI could make some software companies bankrupt, while Anthropic said its Claude Code tool can be used to modernize software written in the COBOL language, which handles large transactions for many governments, banks and airlines.

Related: How SocialFi, memecoins and AI pushed Base to the top of the L2 ladder

Anthropic’s findings appeared to affect IBM’s share price directly, as COBOL is mostly run on IBM’s systems.

Citrini said the rise in agentic AI tools like Anthropic’s Claude Code or OpenAI’s Codex will drive the broad economic shift, reducing the need for human labor and forcing companies to reinvest savings into ever-more capable AI, essentially creating a feedback loop that accelerates workforce displacement and consumer spending decline.

Tech entrepreneurs say AI agents aren’t worth the costs yet

However, three multimillionaire tech investors recently said the high costs of deploying AI agents still don’t justify replacing many humans, who can perform tasks just as well, more cheaply.

Tech investor Jason Calacanis said he is spending $300 per day to run a single AI agent despite it only operating at 10% to 20% of full capacity, while Social Capital CEO Chamath Palihapitiya noted the same problem and said his AI agents need to be at least twice as productive as employees to justify the costs.

Billionaire investor Mark Cuban said the economic-constraint argument of AI agents raised by Calacanis and Palihapitiya was the smartest counterargument that he had seen to AI replacing humans.

Magazine: IronClaw rivals OpenClaw, Olas launches bots for Polymarket — AI Eye

XRP, Solana, and Chainlink recorded small inflows, but these were insufficient to offset broader, persistent altcoin outflows.

Investor appetite for digital asset funds remains muted after $288 million in weekly outflows. This is the fifth week in a row of redemptions, which propelled aggregate withdrawals to $4 billion, still trailing the $6 billion logged last year.

Market participation has thinned significantly, as ETP trading slid to $17 billion, the weakest level since July 2025, amidst signs of disengagement among institutions and retail allocators alike globally this quarter.

Short Bets Quietly Surge

According to the latest edition of CoinShares’ Digital Asset Fund Flows Weekly Report, Bitcoin remains the primary drag on market sentiment, shedding $215 million. In addition, bearish positioning intensified as short-bitcoin funds absorbed $5.5 million, which is the highest inflow among individual assets. Ethereum also experienced notable withdrawals of $36.5 million, joined by continued selling in multi-asset products and Tron, which lost $32.5 million and $18.9 million, respectively.

While XRP, Solana, and Chainlink attracted limited inflows ranging between $1.2 million and $3.5 million, these gains did little to offset persistent net outflows across altcoins.

The US dominated weekly flows on the downside as it contributed $347 million in outflows, while investors outside the country treated recent price declines as an entry point. Inflows were led by Switzerland, Canada, and Germany at $19.5 million, $16.8 million, and $16.2 million, respectively. Smaller allocations of of $3 million, $2.7 million, and $1 million also flowed into Brazil, Australia, and the Netherlands, respectively.

Bitcoin Stuck in a Macro Storm

Bitcoin slipped below $65,000 during Monday’s early Asia trading, which ended up triggering roughly $230 million in long liquidations as markets grapple with a convergence of geopolitical and macro risks. The move followed Donald Trump’s decision to raise a proposed global tariff to 15%, announced shortly after the Supreme Court of the United States struck down his “Liberation Day” tariffs.

This was enough to compound policy uncertainty amid already thinning risk appetite and renewed concerns around a potential US-Iran conflict. QCP Capital stated that the focus is not on whether Bitcoin has failed, but how long this storm persists.

You may also like:

With BTC on pace for a fifth red monthly close, historically a late-stage signal, all eyes are now on upcoming catalysts, including progress on the Clarity Act and US-Iran talks. But QCP added that a reclaim of $74,000 remains critical for a durable recovery.

Binance Free $600 (CryptoPotato Exclusive): Use this link to register a new account and receive $600 exclusive welcome offer on Binance (full details).

LIMITED OFFER for CryptoPotato readers at Bybit: Use this link to register and open a $500 FREE position on any coin!

BTC is trading around $68,000, slightly up on the day but down over the week, and Robinhood’s crypto head says their users are using this environment to buy dips and diversify beyond just BTC and ETH.

Summary

- BTC trades near recent lows after multi-week decline amid persistent ETF outflows and extreme fear readings.

- Robinhood users increasingly rotate from just BTC, ETH into a broader basket of tokens during the downturn.

- Staking demand for ETH and SOL on Robinhood remains strong since its December launch, signaling active on-chain use, not passive holding.

Cryptocurrency investors are diversifying their holdings beyond Bitcoin and Ethereum during the current market decline, according to a Robinhood executive.

Johann Kerbrat, head of crypto at Robinhood, stated in a recent interview that many platform users view the ongoing market downturn as an opportunity to purchase digital assets at lower prices. However, trading activity has expanded beyond the largest cryptocurrencies, Kerbrat said.

“Customers see the current market as a buying opportunity. However, they are expanding their transactions beyond the two or three most popular cryptocurrencies to include a wider range of assets,” Kerbrat stated.

The executive reported that clients are actively using their tokens rather than simply holding them on the platform. Interest in staking has remained strong since Robinhood launched the feature in December, according to Kerbrat.

The shift in investor behavior comes as overall market sentiment remains at extreme levels of fear, according to market indicators. U.S. spot Bitcoin exchange-traded funds have experienced net outflows for several weeks, data shows.

Despite the negative market conditions, interest in decentralized finance use cases is increasing, Kerbrat noted.

Bitcoin and altcoin prices have continued to decline in recent weeks, extending losses across the cryptocurrency market.

Stablecore, a digital asset infrastructure company, has joined the Jack Henry Fintech Integration Network, enabling banks and credit unions on the platform to offer stablecoin and tokenized asset services through their existing systems.

Jack Henry supplies core processing and digital banking technology to approximately 1,670 banks and credit unions in the United States. Many of those institutions also rely on its Banno Digital Platform, which powers online and mobile banking services for more than 1,000 financial institutions.

On Monday, Stablecore said the integration will connect blockchain-based products to traditional core banking infrastructure.

Participating institutions could roll out stablecoin accounts with 24/7 payment capabilities, crypto on- and off-ramps for assets such as Bitcoin (BTC), digital asset–backed lending, tokenized deposits and staking features where permitted.

Embedding these services within existing banking apps would reduce reliance on standalone wallets or external crypto platforms. It also reflects a broader shift toward incorporating blockchain-based assets into regulated financial channels as demand for compliant, onchain cash-management tools continues to grow.

Related: Wall Street’s crypto debate is over as banks go all-in on BTC, stablecoins, tokenized cash

Stablecoin infrastructure race accelerates

As Cointelegraph reported, Stablecore raised $20 million last year to help smaller banks and credit unions integrate digital asset services, especially stablecoins, following the passage of the landmark US GENIUS Act, which established a federal framework for payment stablecoins.

Stablecore is part of a growing cohort of companies building stablecoin infrastructure to expand access to digital dollars. Proponents argue stablecoins can reduce settlement times, cut cross-border payment costs and provide uninterrupted transfer capabilities compared to traditional banking rails.

Momentum has been building across both fintech and traditional finance.

Last week, payments operations provider Modern Treasury unveiled an integrated payment service that supports stablecoin transactions alongside wire and ACH transfers through a partnership with the Paxos network, signaling greater interoperability between blockchain-based dollars and legacy payment systems.

Meanwhile, asset management giant Fidelity Investments has introduced the Fidelity Digital Dollar, a stablecoin due to launch this month and designed to facilitate faster and more efficient international settlements.

Large banks are also exploring in-house issuance. Citigroup executives have publicly discussed the possibility of launching a native stablecoin as financial institutions seek to modernize cross-border payments and liquidity management.

Related: USDCx appears on Aleo as privacy-focused blockchains seek stablecoin access

The Board of Peace established by US President Donald Trump, which requires a $1 billion contribution for membership, is reportedly exploring a stablecoin for use in rebuilding Gaza’s economy following two years of war triggered by a Hamas terror attack in October 2023.

According to a Monday Financial Times report, the board is in the preliminary stages of discussing whether a stablecoin could be used to help rebuild Gaza’s economy. A person familiar with the project reportedly said the stablecoin would not be a meme coin or a replacement for fiat currency, but rather “a means to allow Gazans to transact digitally.”

Trump announced the formation of the board in January. Membership requires countries to contribute $1 billion for a permanent, renewable role, while the US, according to Trump’s social media announcement, pledged $10 billion. The majority of countries in western Europe declined invitations to join, while 26 countries including Israel, Saudi Arabia, Hungary, and El Salvador were founding members.

The FT report did not state which entity could be responsible for issuing a stablecoin should the board move forward. However, the Trump administration has supported policies allowing broader use of stablecoins in the US, including the president signing the GENIUS Act into law in July.

Related: Israel crypto industry pushes regulatory changes amid strong public support

“The current proposal for the Gaza stablecoin is still very premature,” Snir Levi, CEO of blockchain intelligence platform Nominis, told Cointelegraph. “[O]ver the last two years, OTC desks in Gaza have moved over $100 million in stablecoins with almost no restrictions, without the proper framework, same thing will happen with the Gaza stablecoin.”

Trump also reportedly considering tokenized postwar Gaza plan

There has been a ceasefire agreement in place for Gaza officially since October 2025, though Israeli forces have reportedly repeatedly violated the deal. A significant portion of populated areas in the territory have been destroyed or heavily damaged since 2023.

As a result, members of the Trump administration, including the president and his son-in-law Jared Kushner have proposed plans for developing the area.

Trump reportedly mulled a plan to tokenize land and use digital tokens to relocate and rehouse residents during a US occupation of the territory. He said in February 2025 that the US should “take over” Gaza and make it the “Riviera of the Middle East” before a ceasefire was in place.

Magazine: Hong Kong stablecoins in Q1, BitConnect kidnapping arrests: Asia Express

Bitcoin trades near 200-week EMA; loss of support could spark 30–60% capitulation.

Summary

- Bitcoin trades around $68.4k, above the ~$68.3k 200-week EMA that marks the key cycle support line.

- In 2018 and 2022, a weekly close below the 200-week EMA followed by a failed retest turned it into resistance and led to sharp selloffs.

- Analyst Rekt Capital says multiple weekly closes above the EMA keep downside “unconfirmed,” but a breakdown from this level could again trigger accelerated capitulation.

A cryptocurrency analyst has warned that Bitcoin (BTC) could experience a significant price decline similar to events in 2018 and 2022 if the digital asset fails to maintain a critical technical support level.

The analyst, known by the pseudonym Rekt Capital, told 563,100 followers on social media platform X that Bitcoin faces potential downside risk if it loses support at the 200-week exponential moving average (EMA), according to statements posted on the platform.

Historical data shows that a weekly close below the 200-week EMA, followed by a post-breakdown retest of the EMA into new resistance, has triggered bearish acceleration in previous market cycles, the analyst stated.

“The 200-week EMA represents the key level,” Rekt Capital wrote, adding that a weekly close below it followed by a bearish retest would likely position Bitcoin for additional downside over time.

The analyst noted that Bitcoin has posted weekly closes above the 200-week EMA for two consecutive weeks, which has prevented bearish confirmation in the near term. However, the analyst cautioned that Bitcoin remains vulnerable without sustained upward momentum.

According to the analysis, historical patterns suggest Bitcoin may struggle to generate significant upward price movement from the 200-week EMA level before an eventual breakdown occurs.

The analyst stated that a convincing breakout above the 200-week EMA resistance level would be necessary to invalidate the likelihood of a price collapse.

Bitcoin experienced major capitulation events in both 2018 and 2022, when the cryptocurrency lost significant value following extended bear markets.

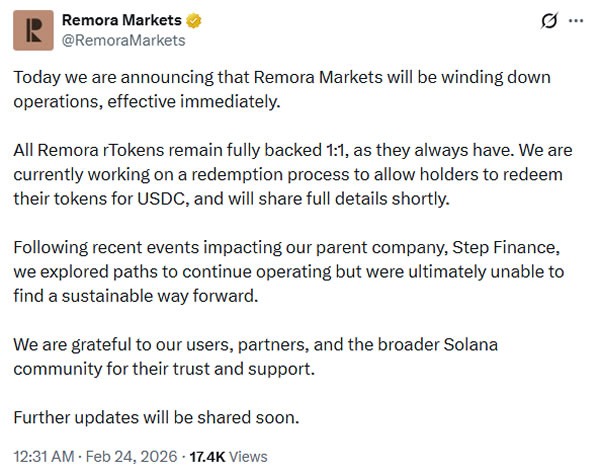

Three Solana-based platforms have announced they are shutting down after a Step Finance hack at the end of January that has been deemed unrecoverable.

Solana portfolio dashboard and DeFi aggregator Step Finance announced on Monday that it would be winding down operations. The closure also extends to subsidiaries Solana NFT analytics and the ecosystem media outlet SolanaFloor, as well as lending and yield protocol Remora Markets.

“Following the hack at the end of January, we explored every possible path forward, including financing and acquisition opportunities,” it stated, referring to a $27 million security breach of its treasury wallets in January.

The team said they were “unable to secure a viable outcome,” resulting in the decision to “end all operations effective immediately.”

The DeFi platform said it is working on a buyback for holders of its native token, STEP, based on a snapshot taken before the incident. There will also be a redemption process for Remora rToken holders, they said.

Step suffers $27 million security breach

Step Finance reported a “breach of security for some of our treasury wallets” on Jan. 31 and asked cybersecurity firms to assist with the investigation.

Blockchain security firm CertiK reported that 261,854 Solana (SOL), worth roughly $27 million at the time, was unstaked and transferred during the incident.

Related: Solana treasuries sitting on over $1.5B in paper SOL losses

Crypto investor Mike Dudas said he was contacted by Step Finance about participating in a bridge round, but requested a security post-mortem first and received no response.

Step Finance co-founder George Harrap said on Tuesday that “Some people have reached out on acquiring various businesses, and we will pursue those if serious and have interest, but we are on a time crunch.”

The platform’s native STEP token tanked 96% in the days following the hack. It slumped a further 36% following the announcement of the closure on Monday and is currently trading at $0.00057, according to CoinGecko.

STEP hit an all-time high of $10.20 in August 2021.

Solana DeFi total value locked tanks 50%

The triple closure is another blow to decentralized finance on Solana, which has seen total on-chain value tank 52% since its September peak. Solana DeFi TVL currently stands at just $6.3 billion, according to DeFiLlama.

Meanwhile, SOL prices have lost a further 1.8% on the day, falling to $78, according to CoinGecko. The asset is now 74% down from its January 2025 all-time high of $293, hit during the peak of memecoin mania.

Magazine: Bitcoin may take 7 years to upgrade to post-quantum: BIP-360 co-author

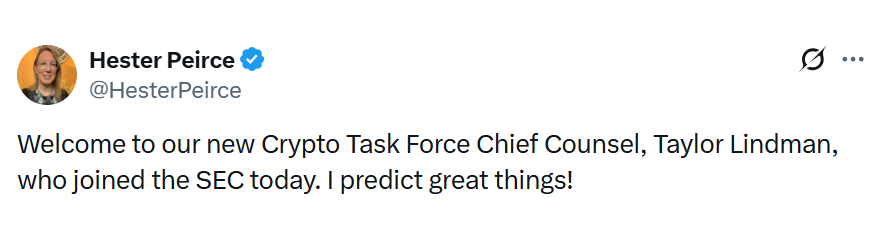

Taylor Lindman, the deputy general counsel at blockchain firm Chainlink Labs, has joined the Securities and Exchange Commission’s Crypto Task Force as its new chief counsel, filling a role left by now-CFTC chair Michael Selig.

In an X post on Monday, Chainlink Labs announced Lindman’s departure after five years and confirmed his official appointment to the SEC’s Crypto Task Force.

“We thank Taylor for his great five years as a key part of the Chainlink Labs team in his role as deputy general counsel. We all look forward to modernizing the US financial system together, taking it to the next level of its development and rapid growth,” Chainlink Labs said.

SEC Commissioner Hester Peirce, who leads the Crypto Task Force, also confirmed Lindman’s new appointment on X, predicting “great things!” ahead.

A chief counsel typically serves as the senior legal advisor, guiding legal interpretation, ensuring compliance, managing risk and supporting leadership decision-making.

Lindman brings a decade of legal experience to the SEC

Lindman spent more than five years at Chainlink, according to his LinkedIn profile, across various roles, including deputy general counsel and associate general counsel.

During his tenure at Chainlink, Lindman was responsible for ensuring compliance with US and international regulations and was also part of a delegation that met with the Crypto Task Force in March 2025 to discuss crypto regulation, including token taxonomy and securities record-keeping requirements.

Before Chainlink, Lindman was an associate at Perkins Coie from 2018 to 2021 and at Debevoise & Plimpton from 2016 to 2018.

Lindman succeeds Selig, who held the role until December of last year, when he became chair of the Commodity Futures Trading Commission.

Other experienced crypto hands at the SEC

Peirce announced the original lineup of 14 Crypto Task Force members in March 2025, which included several crypto industry natives along with staff taken from the chair’s office and other divisions and offices across the commission.

Landon Zinda, a former policy director at Coin Center from March 2023 until February 2025, is on the task force as a senior advisor.

Related: US SEC crypto task force to tackle financial surveillance and privacy

Veronica Reynolds, also a senior advisor on the task force, previously worked as an associate at Baker Hostetler, a law firm with a practice group focused on digital assets and Web3 technology.

The SEC Crypto Task Force was established following a friendlier policy shift from the incoming Trump administration. Since then, the task force has held roundtable events and tours to gather feedback from the crypto industry, academics and market participants on digital asset regulation.

Magazine: Is China hoarding gold so yuan becomes global reserve instead of USD?

Bitcoin (BTC) dips under $63,000 and history says more pain ahead before bottom forms

Ex-Prince Andrew And Sarah Ferguson Leaning On Each Other

BITCOIN: Rare Signal Flashing NOW! (big warning) – BTC Price Prediction Today

-

Crypto World7 days ago

Crypto World7 days agoCan XRP Price Successfully Register a 33% Breakout Past $2?

-

Video4 days ago

Video4 days agoXRP News: XRP Just Entered a New Phase (Almost Nobody Noticed)

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Boden – Corporette.com

-

Politics2 days ago

Politics2 days agoBaftas 2026: Awards Nominations, Presenters And Performers

-

Sports10 hours ago

Sports10 hours agoWomen’s college basketball rankings: Iowa reenters top 10, Auriemma makes history

-

Politics11 hours ago

Politics11 hours agoNick Reiner Enters Plea In Deaths Of Parents Rob And Michele

-

Business6 days ago

Business6 days agoInfosys Limited (INFY) Discusses Tech Transitions and the Unique Aspects of the AI Era Transcript

-

Entertainment6 days ago

Entertainment6 days agoKunal Nayyar’s Secret Acts Of Kindness Sparks Online Discussion

-

Video7 days ago

Video7 days agoFinancial Statement Analysis | Complete Chapter Revision in 10 Minutes | Class 12 Board exam 2026

-

Tech6 days ago

Tech6 days agoRetro Rover: LT6502 Laptop Packs 8-Bit Power On The Go

-

Sports5 days ago

Sports5 days agoClearing the boundary, crossing into history: J&K end 67-year wait, enter maiden Ranji Trophy final | Cricket News

-

Business2 days ago

Business2 days agoMattel’s American Girl brand turns 40, dolls enter a new era

-

Business1 day ago

Business1 day agoLaw enforcement kills armed man seeking to enter Trump’s Mar-a-Lago resort, officials say

-

Entertainment5 days ago

Entertainment5 days agoDolores Catania Blasts Rob Rausch For Turning On ‘Housewives’ On ‘Traitors’

-

Business6 days ago

Business6 days agoTesla avoids California suspension after ending ‘autopilot’ marketing

-

NewsBeat19 hours ago

NewsBeat19 hours ago‘Hourly’ method from gastroenterologist ‘helps reduce air travel bloating’

-

Politics7 days ago

Politics7 days agoEurovision Announces UK Act For 2026 Song Contest

-

Tech1 day ago

Tech1 day agoAnthropic-Backed Group Enters NY-12 AI PAC Fight

-

NewsBeat1 day ago

NewsBeat1 day agoArmed man killed after entering secure perimeter of Mar-a-Lago, Secret Service says

-

Politics2 days ago

Politics2 days agoMaine has a long track record of electing moderates. Enter Graham Platner.