TKO Group Holdings, Inc. (TKO) Q4 2025 Earnings Call February 25, 2026 5:00 PM EST

Company Participants

Seth Zaslow – Senior VP & Head of Investor Relations Ariel Emanuel – Executive Chair & CEO Mark Shapiro – COO, President & Director Andrew Schleimer – Chief Financial Officer Nick Khan

Conference Call Participants

Advertisement

Brandon Ross – LightShed Partners, LLC Stephen Laszczyk – Goldman Sachs Group, Inc., Research Division Benjamin Swinburne – Morgan Stanley, Research Division David Karnovsky – JPMorgan Chase & Co, Research Division Peter Supino – Wolfe Research, LLC Ryan Gravett – UBS Investment Bank, Research Division

Presentation

Operator

Advertisement

Good afternoon. Thank you for attending the TKO Fourth Quarter and Full Year 2025 Earnings Call. My name is Cameron, and I’ll be your moderator for today. [Operator Instructions] And I would now like to pass the conference over to your host, Seth Zaslow, Head of Investor Relations. Please proceed.

Seth Zaslow Senior VP & Head of Investor Relations

Good afternoon, and welcome to TKO’s Fourth Quarter and Full Year 2025 Earnings Call. A short while ago, we issued a press release, which you can view on our Investor Relations website. A recording of this call will also be available via our website for at least 30 days. After prepared remarks from Ari Emanuel, TKO’s Executive Chair and Chief Executive Officer; Mark Shapiro, TKO’s President and Chief Operating Officer; and Andrew Schleimer, TKO’s Chief Financial Officer, will open the call for questions.

Advertisement

Mark and Andrew will be handling the Q&A. The purpose of this call is to provide you with information regarding our fourth quarter and full year 2025 performance. I want to remind everyone that the information discussed will include forward-looking statements and/or projections that involve risks, uncertainties and assumptions. Please see our filings with the Securities and Exchange Commission for further detail.

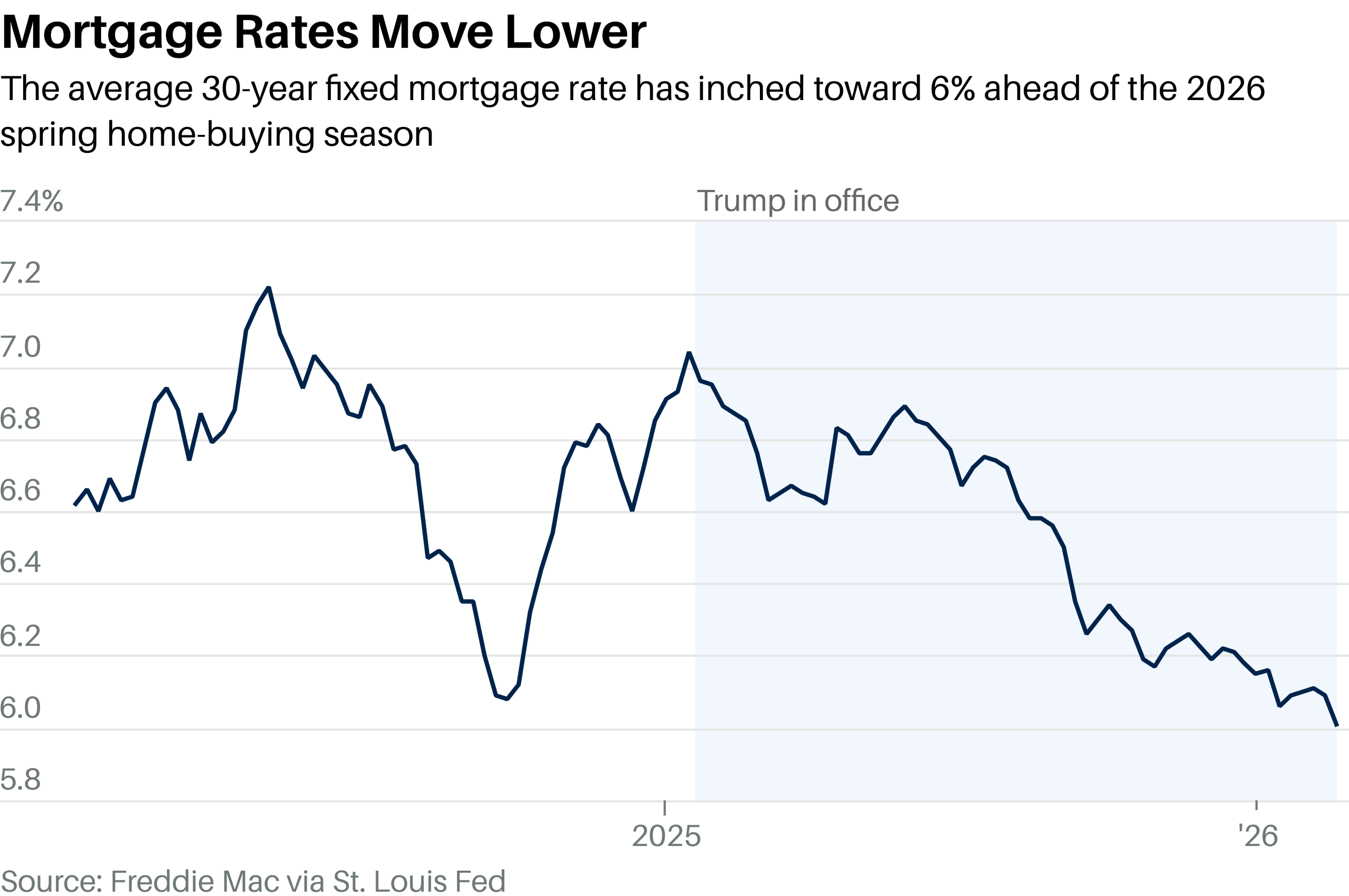

Mortgage rates are nearly a percentage point lower than they were when Trump took office. The president’s direct actions are only part of the story.

Mortgage rates typically move with the 10-year Treasury yield. That yield, in turn, is connected to expectations for the economy and monetary policy in the coming decade. It rose, along with mortgage rates, in 2022 and 2023 as mounting inflation proved difficult to control without rate hikes.

The 10-year Treasury yield has broadly moved lower over the past year, helped in part by a slowdown in shelter inflation. Because of how shelter is measured, the inflation reading notably lags private measures of rents, which began to show signs of moderation in 2023, Barron’s_ reported. Soft inflation data and the expectation of future Federal Reserve rate cuts have helped—though the ride lower has been bumpy.

Shares in DUG Technology have lifted by over 10 per cent following the release of strong financials, and despite its ongoing US court action with a subsidiary of oil and gas giant Shell.

“Introduction to Doing Business in Indonesia 2026” offers insights into Indonesia’s economy, foreign investment, trade conditions, manufacturing, and business environment, aiding foreign enterprises and investors.

New Publication on Indonesia’s Business Environment

The latest release, Introduction to Doing Business in Indonesia 2026, by Dezan Shira & Associates, is now available for download at the Asia Briefing Publication Store. This comprehensive guide offers valuable insights for foreign investors and enterprises interested in Indonesia’s evolving market landscape.

Economic Overview and Investment Trends

Indonesia’s economy grew steadily at around 4.9–5.0% through 2025, driven more by domestic investment than external demand. Foreign direct investment remained significant, totaling approximately IDR 900.9 trillion (US$53–55 billion). The shift toward more cautious, long-term capital commitments highlights a maturing investment environment, supported by a stronger internal economic base and increased domestic participation.

Trade Dynamics and Sector Performance

Trade exposure to external policies became evident in 2025, as U.S. tariffs temporarily exceeded 30% on certain exports, impacting manufacturing activity. The manufacturing sector experienced volatility, with the Purchasing Managers’ Index dipping into contraction early in the year but later rebounding. While growth remains sensitive to external factors, Indonesia’s economic resilience continues to strengthen.

Advertisement

Comprehensive Business Guide

Introduction to Doing Business in Indonesia 2026 offers a detailed overview aimed at foreign investors seeking to navigate Indonesia’s business climate. It covers key sectors, investment strategies, legal considerations, and upcoming economic opportunities, serving as a vital resource for strategic decision-making.

Australia has ordered the evacuation of the families of the diplomats in several countries in the Middle East.

The order comes as tensions continue to run high between Iran and the United States.

Evacuation Orders Issued for Diplomats’ Families

According to news.com.au, the evacuation order was given to Australian families in Lebanon and Israel.

Voluntary departures are also being offered for those in the following countries:

Jordan

Qatar

United Arab Emirates

“Regional tensions remain high and there continues to be a risk of military conflict,” the Australian government’s Smartraveller said. “Conflicts in the Middle East could result in airspace closures, flight cancellations and other travel disruptions.”

Iran, as of writing, is on Level 4 of Smartraveller’s travel warnings, which means that Australians should not travel to the Middle Eastern country.

Advertisement

“Do not travel to Iran due to the risk of arbitrary detention and the volatile regional security situation,” Smartraveller says on its website.

Potential Military Conflict Between US and Iran

The evacuation of diplomats’ families comes as US President Donald Trump continues to build a strong military presence in the region. Trump is reportedly considering a limited military strike.

The two countries are working to see if they can reach a deal regarding Iran’s nuclear programme.

According to The Guardian, the US maintains that Iran should stop rebuilding its nuclear programme, but Iran has accused Trump of spreading lies.

AusAlert, the new national emergency system, is set to undergo testing in July.

This means most Australians will receive a mobile phone alert that month as part of the test.

AusAlert to Undergo Nationwide Testing in July

According to ABC News, the nationwide test will take place on July 27 at 2 p.m. AEST. As for who are set to receive the test alert, everyone in the country with a compatible mobile device will receive one.

The report also notes that AusAlert is expected to be fully operational by October of this year.

According to the National Emergency Management (NEMA), community tests have also been scheduled for June. The schedule of the community tests is as follows:

Advertisement

10 June – Majura, Australian Capital Territory (micro test at Emergency Services Agency headquarters)

15 June – Launceston, Tasmania

16 June – Port Douglas, Queensland

17 June – Liverpool, New South Wales

18 June – Tennant Creek, Northern Territory, and Geelong, Victoria

19 June – Goomalling, Western Australia

20 June – Port Lincoln, South Australia

21 June – Queanbeyan area, Australian Capital Territory and New South Wales (cross-border test)

What Else to Know About AusAlert

As the national emergency warning system, AusAlert will inform Australians of the following:

What the emergency is

Where it is happening

How serious it is

What you should do

Who the message is from

Where to find more information

According to NEMA, an AusAlert can be issued for the following emergencies:

Natural hazards, such as bushfires, floods, cyclones and tsunamis

Public safety and security threats, such as serious public safety incidents or terrorism

Biosecurity incidents, such as animal or plant disease and biohazard outbreaks

Health emergencies, such as pandemics or other national public health events

Emergency Management Minister Kristy McBain said that two types of alerts can be issued under this system. Priority alerts have been described by ABC News as less intrusive and allows users to opt out of receiving the messages.

Critical alerts, on the other hand, require more immediate action from the receiver of the message. These alerts will have a fixed volume, unique ringtone, and vibration. These cannot be disabled be the receiver.

In a conversation with ET Now, Dipan Mehta, Director, Elixir Equities shared a constructive but selective outlook across sectors, expressing optimism on NBFCs and pharma, caution on metals, and a clear avoid stance on certain largecaps.

On the lending space, Mehta believes the clean-up in microfinance and MSME unsecured portfolios has strengthened the NBFC segment. “I think that for investors who want to buy lenders, NBFC is a great segment… a lot of NBFCs now have cleaned up their books… whatever the NPA they had are well behind them.”

He emphasised a preference for diversified lenders rather than niche players. “Our preference is for NBFCs which are doing multi-product… not just housing or automobile loans or microfinance or gold loan.” He cited Bajaj Finance, Chola and L&T Finance as preferred names, while disclosing investments in them.

Turning to solar equipment manufacturers, Mehta acknowledged that the bullish call has not played out immediately. “We have been very positive on all solar equipment manufacturing companies… that call is not proving right so far.” However, he maintained that long-term investors could benefit. “If you have a longer-term view… this is a nice sustainable compounding industry and can deliver good returns.” On the recently imposed 126% customs duty, he said, “This… will not impact India’s solar equipment industry to any major extent… Waaree included,” adding that valuations have turned attractive, even as he disclosed existing investments in the space.

Advertisement

On the underperformance of Reliance Industries, Mehta offered a structural explanation. “I have a different view and that is that it is slowly going to become a holding company.” He suggested that investors may be uncomfortable with the prospect of IPOs for Jio and retail without a clear vertical split. “We would have preferred a vertical split… given free shares to all the shareholders.” Until there is clarity on restructuring, he believes the stock could remain subdued, though he reiterated that it remains a great company.

Live Events

In real estate, Mehta advised patience and selectivity, favouring larger developers with rental income streams. “I would prefer the larger ones, especially those which have got some annuity assets as well.” He referred to companies like Prestige and DLF as examples and added that investors should broadly focus on players with rental assets, given the supply of new listings and valuation adjustments underway. On tobacco counters, particularly ITC Limited, his stance was unequivocal. “Yes, we have a view and it is an avoid. It is not an FMCG stock. It is a tobacco stock and it is valued accordingly.” He said growth visibility remains limited. “I do not see ITC growing at double digit type of growth rates in the foreseeable future.” Instead, his focus is on small and midcap companies with unique business models and more reasonable valuations after the recent correction.Discussing the GLP-1 opportunity in pharma, Mehta acknowledged its potential but warned about competition. “You are right, it is a good opportunity. But just too many players over there.” Even so, he remains constructive on the broader sector. “On the whole investors should be overweight pharma.” He noted that CDMO companies have seen sharp corrections and should be on investor watchlists for a potential turnaround.

On new-age digital firms such as Eternal, he said investor patience appears to be wearing thin. “Investors are losing patience… when they will turn to profitability.” However, he added, “We remain very positive on Eternal… we have a longer-term view,” signalling continued conviction despite volatility.

Finally, on metals, Mehta struck a cautious tone after a prolonged rally. “It is a cyclical industry and now it has been a great outperformer.” While he would remain invested, he is not keen on fresh entries at current levels. “At some point the cycle certainly will turn… right now I do not see the outperformance continuing.”

Overall, Mehta’s approach reflects a preference for diversified financials, an overweight stance on pharma, selective exposure in real estate and solar, caution in metals, and a clear avoidance of slow-growth largecaps — all anchored in a long-term investment perspective.

Oracle Corporation’s stock rebounded 1.20% to close at $147.89 on February 25, 2026, snapping a recent pullback as analysts highlighted the company’s undervaluation following a sharp sell-off, with Oppenheimer upgrading the shares to Outperform and setting a $185 price target amid ongoing optimism about Oracle Cloud Infrastructure’s role in AI workloads.

AFP

As of February 25, 2026, Oracle (NYSE: ORCL) traded in a session range of $147.34 to $153.28 with volume of approximately 26.5 million shares. The shares have declined about 25% year-to-date in 2026 from earlier peaks near $200+, reflecting investor concerns over slowing cloud revenue growth, elevated capital expenditures, and debt levels tied to aggressive AI data center buildout. Market capitalization stands around $410-420 billion.

The February 25 gain followed Oppenheimer analyst Brian Schwartz’s upgrade from Perform to Outperform, citing an attractive valuation after the recent decline and viewing easing risks around OpenAI partnerships and continued hyperscaler cloud spending as long-term catalysts. Schwartz’s $185 target implies about 25% upside from recent levels. Other firms, including Bernstein SocGen Group, trimmed targets earlier in February but maintained Outperform ratings, underscoring mixed but generally constructive sentiment.

The upgrade arrives ahead of Oracle’s fiscal third-quarter 2026 earnings, expected in early March 2026 (likely March 9-10). Analysts project EPS around $1.36-$1.56 and revenue near $16 billion, reflecting continued growth in cloud services despite earlier Q2 results that fell slightly short of expectations. In fiscal Q2 2026 (ended November 30, 2025), reported December 10, 2025, Oracle delivered total revenue of $16.1 billion, up 14% year-over-year (13% in constant currency), with cloud revenue (IaaS plus SaaS) surging 34% to $8.0 billion. Remaining performance obligations reached a record $523 billion, up 438% in USD, driven by long-term commitments from major clients including Meta Platforms and NVIDIA.

Oracle’s AI push has centered on Oracle Cloud Infrastructure (OCI), positioned as a premier platform for high-performance computing and generative AI workloads. The company has aggressively expanded data center capacity, with projected fiscal 2026 capital expenditures soaring to $50 billion—a $15 billion increase from September 2025 guidance. Partnerships with NVIDIA and others underscore OCI’s growing traction in AI training and inference, though some observers note risks from heavy spending, negative free cash flow exceeding $10 billion in recent periods, and off-balance-sheet lease obligations approaching $248 billion.

Advertisement

Despite near-term pressures, analysts view Oracle’s trajectory positively. The company’s enterprise software dominance, combined with cloud acceleration and AI tailwinds, supports projections for fiscal 2026 revenue growth in the mid-teens and continued margin expansion. Consensus among covering firms leans toward Buy, with average 12-month price targets around $180-$200, implying substantial upside from current levels.

Oracle’s strategic focus includes embedding AI across products, with leadership emphasizing agility in response to rapid AI technology changes. Recent contracts, such as an $88 million OCI deal with the U.S. Department of the Air Force, reinforce its positioning in secure, mission-critical workloads. The company also benefits from its database and applications heritage, providing a stable foundation amid the shift to cloud and AI services.

Challenges persist, including competitive intensity from AWS, Microsoft Azure, and Google Cloud, as well as concerns over capital intensity and debt management. Some reports highlight potential margin erosion if revenue growth slows relative to spending, though Oracle’s RPO backlog offers strong visibility into future revenue.

The upcoming Q3 report will provide critical insights into cloud revenue trends, AI adoption, capex execution, and any refinements to full-year guidance. Positive commentary on OCI momentum and AI pipeline could sustain the rebound; signs of prolonged spending pressures might renew caution.

Advertisement

Oracle Corporation, a leader in enterprise software and cloud services, navigates a pivotal phase with its AI and cloud investments positioning it for long-term growth. Recent sell-off concerns appear to have created an entry point for some analysts, who see the stock as undervalued relative to its potential in the AI infrastructure boom. As fiscal 2026 progresses, Oracle’s ability to convert massive backlog and spending into profitable expansion will determine whether the current rebound marks a turning point or a temporary pause.