Crypto World

JPMorgan Gives Bold Nvidia Price Prediction, But Is It Realistic?

NVIDIA Stock just delivered a record-breaking Q4 with $68.1 billion in revenue, 73% year-over-year growth, and earnings per share of $1.62 that crushed estimates. JPMorgan, among others, wasted no time raising its price target from $250 to $265.

Yet on February 26, the stock fell nearly 7% from its session high of $197 to under $185. The results are undeniable. But the price action, the money flow, and the institutional behavior tell a very different story. At least, for now.

The Numbers Look Bulletproof, Until You Look Closer

NVIDIA’s Q4 numbers speak for themselves. Revenue hit $68.1 billion, up 73% year-over-year. The data center segment alone pulled in $62.3 billion, making up 91% of total revenue. EPS (Earnings Per Share) of $1.62 beat the $1.53 consensus by nearly 6%.

And the Q1 FY2027 guidance of $78 billion blew past Wall Street’s $72.8 billion estimate — a figure that notably excludes any revenue from China.

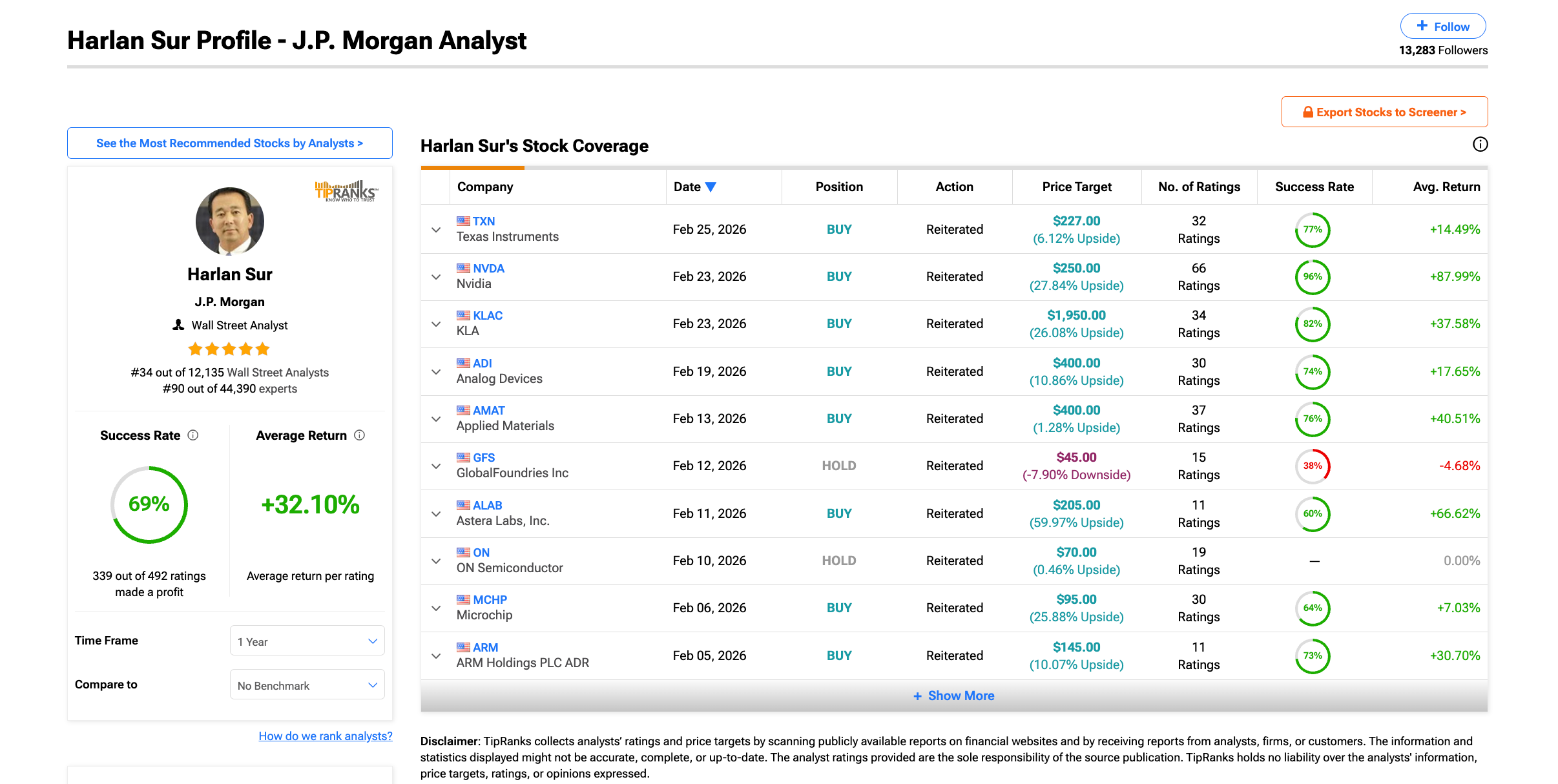

JPMorgan analyst Harlan Sur responded by lifting the Nvidia price target from $250 to $265.

But here is what most analysts are not highlighting. NVIDIA’s quarter-over-quarter growth rate is quietly decelerating. Q3 grew 22% over Q2. Q4 grew 19.5% over Q3.

The Q1 guidance implies roughly 14.5% sequential growth. Revenue keeps hitting records, but the pace of acceleration is fading. For a stock priced on growth momentum, this distinction matters. Something big money might be watching.

There is also the question of who is actually driving this revenue. Deepwater Asset Management’s Gene Munster estimates that roughly 70% of Nvidia’s revenue comes from just 8 companies.

CFO Colette Kress confirmed that the top 5 hyperscalers (cloud computing providers) account for slightly over 50% of data center revenue. That level of customer concentration means that even a modest 10-15% reduction in AI capex from a few major buyers could translate into billions in lost quarterly revenue.

It is also worth noting that JPMorgan’s asset management division is itself a significant institutional holder of Nvidia.

This is standard on Wall Street, but it is a context that retail investors should be aware of when evaluating the bullishness behind a price target upgrade.

What Retail NVDA Investors See vs What Institutions Are Doing

On-Balance Volume (OBV), an indicator that tracks cumulative buying and selling pressure by adding volume on up days and subtracting it on down days, tells a positive story on the surface.

OBV has maintained higher highs throughout Nvidia’s 3-month consolidation, suggesting retail-driven buying pressure remains consistently positive. However, it still needs to break past its ascending trendline resistance to confirm genuine broad-based strength.

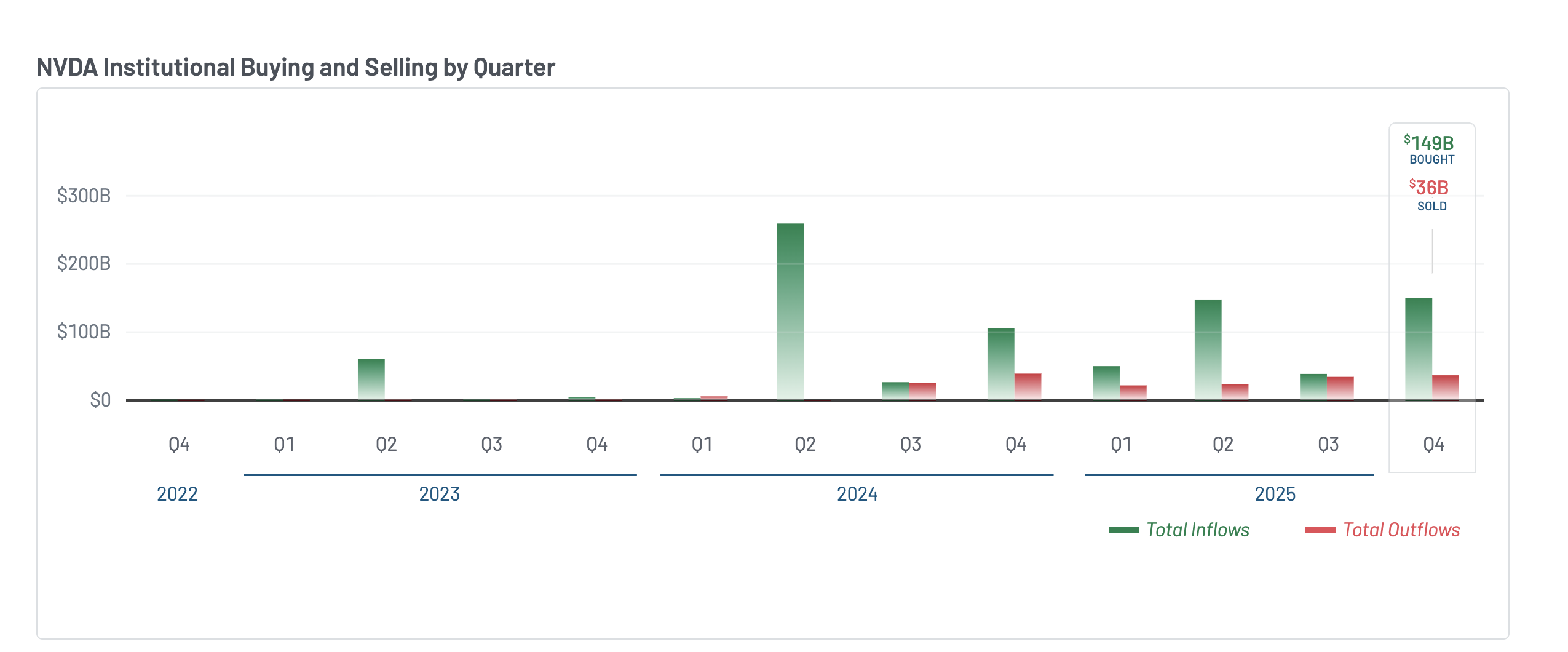

The most recent 13F filings (quarterly reports large investors must file with the SEC revealing their positions) for Q4 2025 show a dramatic shift in institutional sentiment.

Net institutional money flow surged to approximately $149 billion in purchases against $36 billion in sales — a net inflow of roughly $113 billion. That is a massive improvement from Q3, where institutions bought $38 billion and sold $34 billion, leaving a net inflow of just $4 billion.

Yet despite this wall of institutional money entering NVDA in Q4, the stock barely moved — trading sideways for most of the period. That suggests institutions were accumulating, but supply from insiders and earlier holders absorbed the demand. NVIDIA director Mark Stevens sold approximately $40 million in shares in December.

Bank of America, while slightly increasing its equity stake, closed out both its call and put options positions entirely — neutralizing its directional bets.

Institutions are clearly positioned. But the hedging and the flat price despite massive inflows suggest they are bracing for something. The next section explores what that might be.

The Risk Hiding in the Charts

The Chaikin Money Flow (CMF), an indicator that measures whether money is flowing into or out of a stock based on where the price closes within its daily range weighted by volume, reveals what the earnings headline does not.

Since February 5, as the right shoulder of Nvidia’s inverse head and shoulders pattern formed, CMF climbed steadily alongside the price. It rose all the way into the February 25 earnings breakout when Nvidia briefly touched $197.

Then on February 26, as the stock reversed sharply to $185, CMF plunged.

That sudden collapse suggests the money flowing in during the rally was speculative positioning — not committed institutional capital — and it evaporated the moment the breakout failed. And based on what we discussed earlier, revenue deceleration could be a reason.

The monthly VWAP (Volume Weighted Average Price, which approximates where institutions have built their positions) reinforces this. NVIDIA had been trading above its monthly VWAP since breaking out on February 17.

The last time Nvidia broke below the monthly VWAP was on January 30, which led to a correction of approximately 8.5% by early February.

As of February 26, the stock has once again fallen below this line. This means recent institutional buyers are now underwater, which historically triggers further selling as stop losses unwind.

The technical breakdown has context. Michael Burry flagged today that Nvidia’s supply commitments have ballooned to levels that mirror Cisco before the dot-com bust — a company that wrote down billions when demand didn’t meet expectations.

CFO Kress acknowledged Nvidia has locked in inventory “further out in time than usual.” Bulls like BofA’s Vivek Arya argue this secures Nvidia’s dominance. But CMF collapsing and VWAP breaking on the same day suggests the market isn’t waiting to find out who’s right.

The NVIDIA Stock Price Levels That Decide What Happens Next

The charts, the money flow, and the institutional positioning all point to the same conclusion — $195 is where conviction gets tested, a level highlighted later on the chart. But first, the risk.

On the daily chart, a hidden bearish divergence has formed between November 10 and February 25. During this period, the NVIDIA stock price made a lower high while the Relative Strength Index (RSI), a momentum indicator, made a higher high

It is a signal that upward momentum is quietly fading even as the stock appears to hold its range.

Since that November divergence started developing, Nvidia has been locked between $169 and $199. It couldn’t break out of this consolidation despite multiple attempts — including the inverse head-and-shoulders breakout on February 25, which failed within 24 hours.

The Fibonacci extension levels from the pattern now frame what comes next. On the downside, $183 at the 0.5 level is the immediate support. Below that, $180 at the 0.382 level becomes critical — a break there exposes $170, the right shoulder low, and $169, the head. Those levels would invalidate the pattern entirely.

On the upside, the neckline at $195 remains the key resistance and the conviction tester. A clean daily close above it, which the NVIDIA stock failed to do yesterday, is needed to reactivate the pattern.

That could push it towards the projected target at $226, the full head-to-neckline measurement.

The next extension at $235 brings it closer to JPMorgan’s $265 target. The path exists on paper.

But as the money flow, the hidden bearish divergence, and today’s 7% rejection all confirm, this is a market that’s not buying it yet.

- KuCoin’s Zypto integration expands KCS use cases into everyday crypto payments.

- KCS token price remains weak as volume stays low despite a positive adoption narrative.

- Key levels to watch are $8.52 support and $8.66 for short-term trend reversal.

KuCoin crypto exchange has taken another step toward expanding real-world crypto usage by integrating its payment service with Zypto, a move that places everyday spending back at the centre of the digital asset conversation.

The partnership links KuCoin Pay with Zypto’s payment infrastructure, allowing users to spend cryptocurrencies directly without routing funds through traditional banking rails.

KuCoin’s partnership with Zypto

This development is designed to close the gap between holding crypto and actually using it, which has long been one of the industry’s biggest adoption challenges.

Through the Zypto ecosystem, users can now make practical payments such as buying gift cards, paying utility bills, topping up mobile airtime, or funding crypto-linked cards.

The integration supports dozens of digital assets, including KuCoin’s native token, KuCoin Token (KCS), positioning KCS closer to daily transactional use rather than pure exchange utility.

For KuCoin, the move strengthens its broader strategy of building payment rails that sit alongside trading, staking, and yield products.

For users, it reduces friction by allowing them to spend crypto balances directly instead of converting to fiat first.

This shift matters because tokens that gain real-world utility often benefit from stronger long-term narratives, even if the short-term price reaction is muted.

KuCoin Token price reaction

Despite the positive headline, KuCoin Token (KCS) price action has remained cautious, reflecting a broader market reality where fundamentals and price do not always align immediately.

At the time of writing, the KCS token is trading around $8.61, placing it well below its historical peak but comfortably above long-term cycle lows.

The token’s market capitalisation sits near $1.14 billion, which keeps it within the mid-cap range where sentiment can change quickly on relatively modest capital flows.

Short-term performance has been mixed, with KCS down roughly 2.2% over the past 24 hours while still showing gains on a weekly and biweekly basis.

Longer timeframes tell a more defensive story, as the token remains significantly lower on a one-year view, reflecting sustained pressure across exchange tokens.

Volume trends offer additional context, as 24-hour trading activity rose by more than 20% but remains low in absolute terms.

This suggests that recent price movement is not being driven by aggressive accumulation or distribution.

Instead, the decline appears more like a slow, liquidity-driven drift rather than a reaction to negative news.

Broader market conditions support this view, as Bitcoin has been slightly positive while the total crypto market has remained largely flat.

There is no clear evidence of derivatives-driven selling, sector rotation, or defensive flows targeting KCS cryptocurrency specifically.

This points to an isolated weakness rather than a systemic issue tied to KuCoin or its token.

From a technical perspective, KCS is currently trading below its short-term moving averages, which keeps near-term momentum tilted to the downside.

The failure to hold the 7-day and 30-day simple moving averages has reinforced a cautious bias among short-term traders.

Until these levels are reclaimed, upside attempts may continue to face selling pressure.

That said, the absence of panic selling suggests that downside risk may remain measured unless broader market sentiment deteriorates.

Bitcoin miner MARA Holdings has entered a strategic partnership with Barry Sternlicht’s Starwood Capital Group to convert its existing mining sites into data center infrastructure for artificial intelligence and cloud computing.

MARA shares jumped approximately 17% in after-hours trading following the February 26 announcement.

Joint Venture Targets 2.5 GW Capacity

The two companies will jointly develop, finance, and operate data center projects across MARA’s existing portfolio. Starwood Digital Ventures, the firm’s data center platform, will handle design, construction, tenant sourcing, and operations. MARA will contribute sites with access to low-cost energy.

The joint platform targets approximately 1 gigawatt of near-term IT capacity, with a pathway to more than 2.5 gigawatts. The facilities will be designed to switch workloads between Bitcoin mining and AI compute depending on market conditions and customer demand. MARA will have the option to retain up to 50% ownership in the joint venture, with both companies sharing development costs and profits. Financial terms were not disclosed.

“Our partnership with Starwood will allow us to turn power certainty into capacity certainty,” said MARA CEO Fred Thiel, adding that the joint venture offers a more capital-efficient approach to infrastructure buildout.

Starwood Capital manages more than $125 billion in assets. Starwood Digital Ventures operates a 94-person team with data center expertise across more than 10 GW.

Miners Pivot Toward AI Infrastructure

The announcement coincided with MARA’s fourth-quarter earnings, which revealed a $1.7 billion net loss driven largely by unrealized writedowns on its Bitcoin holdings. Quarterly revenue came in at $202 million, down 6% from the same period a year earlier. The company trails only Michael Saylor’s Strategy Inc. in corporate Bitcoin holdings.

MARA’s move fits a pattern across the mining sector. Companies that once focused solely on Bitcoin production are repurposing their energy assets and physical infrastructure for AI workloads, attracted by shorter lead times compared to building new facilities from scratch.

Several miners that embraced this transition early, including IREN, TeraWulf, and Cipher Mining, have seen their market capitalizations outpace MARA’s despite producing less Bitcoin mining hash power. Meanwhile, Starboard Value has taken a significant stake in Riot Platforms, pressuring the Texas-based miner to accelerate its own data center conversion efforts.

JLL and Paul Weiss served as MARA’s strategic and legal advisors.

Bloomberg reported earlier this month that 10% of Block’s workforce could be cut during annual performance reviews as part of a broader overhaul.

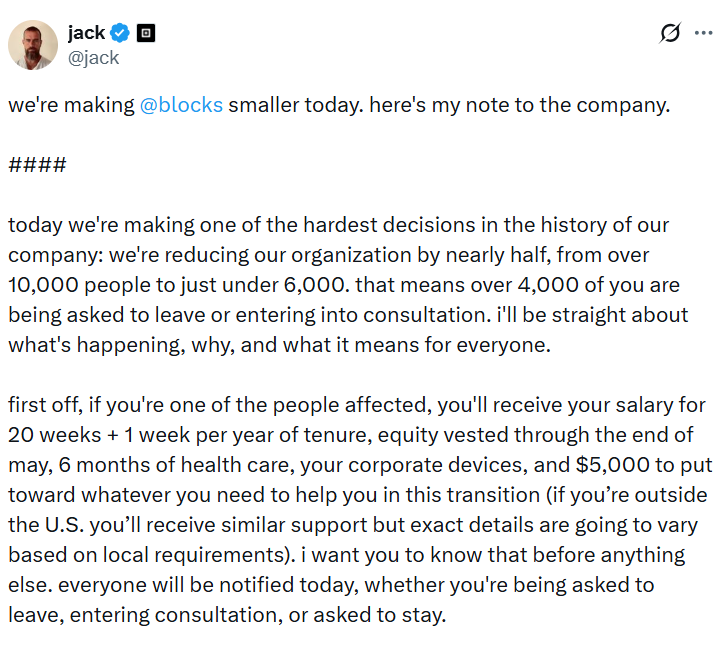

Jack Dorsey’s payments company Block will cut over 4,000 of its staff, with its co-founder pinning the move on the rapid acceleration of AI.

“We’re already seeing that the intelligence tools we’re creating and using, paired with smaller and flatter teams, are enabling a new way of working which fundamentally changes what it means to build and run a company, and that’s accelerating rapidly,” wrote Dorsey in a letter to the company, which he shared on X.

“I had two options: cut gradually over months or years as this shift plays out, or be honest about where we are and act on it now. I chose the latter. Repeated rounds of cuts are destructive to morale, to focus, and to the trust that customers and shareholders place in our ability to lead,” he added.

Affected staff will still receive their salary for 20 weeks, plus one week per year of tenure, six months of health care, their corporate devices, and $5,000 to help them transition to a new role, said Dorsey.

Bloomberg reported earlier this month that 10% of Block’s workforce could be eliminated during annual performance reviews, as part of a wider restructuring effort.

Magazine: Bitcoin’s ‘biggest bull catalyst’ would be Saylor’s liquidation — Santiment founder

Block, the payments company co-founded by Jack Dorsey, is pursuing a sweeping workforce reduction, targeting more than 4,000 roles as part of a broader AI-driven overhaul. The move comes after Bloomberg reported earlier this month that roughly 10% of Block’s staff could be cut during annual performance reviews as part of the restructuring. In a letter to employees posted on X, Dorsey described a shift toward AI-enabled tooling and flatter, smaller teams that he said is accelerating the way the company builds and runs its operations. He argued that letting the process drag on would undermine morale and trust among customers and shareholders. The severance plan outlined by Dorsey includes 20 weeks of salary, plus one additional week per year of tenure, six months of health coverage, the return of corporate devices, and a $5,000 transition stipend. Cointelegraph notes that Bloomberg’s figure framed the scope of the broader restructuring.

Key takeaways

- Block plans to cut more than 4,000 employees as part of an AI-driven restructuring, signaling a rapid shift in how the company organizes operations.

- Bloomberg previously reported that roughly 10% of Block’s workforce could be eliminated during annual performance reviews, reflecting a broader overhaul.

- Dorsey described a move toward AI-enabled tooling and flatter teams as a fundamental change in how Block builds and runs its business, stating that the shift is accelerating.

- The company outlined a severance package including 20 weeks of salary, plus one week per year of tenure, six months of health care, device return, and a $5,000 transition stipend to help staff transition to new roles.

- The restructuring aligns Block with a wider trend among tech and fintech firms leveraging AI to drive efficiency, even as it raises questions about morale and trust among customers and employees.

Market context: The move arrives as fintech and tech firms increasingly pursue AI-driven efficiencies. While the decision signals a willingness to adjust headcount to fit an AI-centric operating model, it also tests morale and trust within the workforce and among customers during a period of heightened scrutiny of automation strategies in the sector.

Why it matters

The decision to prune a sizable portion of Block’s workforce highlights a broader industry shift toward leaner organizational structures that lean on automation and data-driven decision-making. For Block, the aim appears to be speeding up product development and execution by compressing management layers and empowering smaller, cross-functional teams to move more quickly. This approach—emphasizing AI-assisted workflows—could recalibrate how the company allocates resources, prioritizes projects, and measures performance in a rapidly evolving payments landscape.

From an investor and customer perspective, the move introduces a mix of risk and potential upside. On one hand, a large-scale reduction can strain morale in the near term and raise questions about continuity of service and product roadmap execution. On the other hand, if AI-enabled tooling delivers faster iteration cycles and improved efficiency, Block could emerge with lower operating costs and a more agile development cadence. The balance between disruption and long-term gains will likely hinge on how transparently the company communicates with employees, how effectively severance and transition programs are implemented, and how quickly teams can deliver on AI-enabled capabilities without compromising reliability.

The timing of the cuts—coming as AI continues to reshape how consumer and business fintechs build products—also places Block within a broader conversation about automation in corporate America. Analysts and market observers are watching to see whether other large technology and payments players follow suit, mirroring a trend where automation and flatter organizational models are pitched as remedies for cost pressures and productivity gaps. In this context, Block’s restructuring serves as a real-world data point for how a high-profile fintech conglomerate attempts to balance growth objectives with the strategic need to recalibrate staffing in an AI-first era.

Crucially, the announced severance package—20 weeks of salary, an extra week per year of tenure, six months of health coverage, the return of corporate devices, and a $5,000 transition stipend—reflects a structured approach to employee transition. Such terms can help soften the blow for affected workers while signaling that the company is aiming to maintain a competitive benefits framework even as it reshapes its workforce. The efficacy of this strategy will partly depend on execution, including how quickly new roles are found for displaced staff and how smoothly the organization can maintain momentum on its AI initiatives during the transition.

Ultimately, Block’s actions underscore a broader strategic pivot seen across the sector: AI is not just a feature within products, but a central driver of organizational design. The headline figure—thousands of positions cut—reads as a blunt acknowledgment that the cost of scaling AI-driven processes can be high in the short term, even as the promise of faster product cycles and tighter cost structures weighs in the long term. The company’s leadership emphasizes that this shift is essential to remaining competitive and delivering on a vision that places intelligent automation at the core of Block’s operations.

What to watch next

- Block’s official disclosures or filings detailing the scope and timeline of the reductions.

- Updates on severance terms, benefits continuity, and the status of ongoing employee transitions.

- Rationale and progress reports on how AI tooling is changing product development and delivery timelines.

- Market and customer reactions as details emerge about the restructuring’s short- and mid-term impact.

Sources & verification

Block’s AI-driven overhaul reshapes workforce and strategy

Block is moving decisively to align its organizational design with an AI-first operating model. The company’s leadership describes the shift as a necessary evolution, one that leverages intelligence tools to empower smaller, more autonomous teams. In communications to staff, Dorsey framed the change as a way to accelerate decision-making and product development, arguing that a flatter structure could better respond to rapid market shifts and evolving customer needs. The rationale rests on a belief that intelligent automation can reduce friction, cut redundant layers, and enable teams to own end-to-end outcomes—from ideation to delivery.

The reported magnitude of the cuts—over 4,000 roles—signals a broad reevaluation of where value is created within Block. While the exact timeline remains to be clarified, the scope suggests a company-wide reallocation of resources toward AI-enabled capabilities, data analytics, and product platforms that can scale with fewer human handoffs. The emphasis on AI tooling is not merely about replacing tasks; it is positioned as enabling more rapid experimentation, with teams empowered to iterate on features and user experiences in shorter cycles. This approach, proponents say, can compress development timelines and improve product-market fit through faster feedback loops.

Central to Block’s narrative is the assertion that the shift is not a temporary cost-cutting exercise but a fundamental rethinking of how to build and maintain a fintech ecosystem. The company’s leadership has argued that repeated, incremental layoffs would erode morale and trust, whereas a candid, comprehensive restructuring paired with targeted severance support could preserve organizational focus and preserve core commitments to customers and shareholders. The letter to employees on X served as a public articulation of this stance—an attempt to set expectations, preserve morale, and lay out a path for the workforce transition while continuing to pursue aggressive AI-enabled product development.

In practical terms, the transition will require clear governance, transparent communication, and careful management of the change process. The severance package described by Dorsey provides a cushion for affected employees, but the broader test will be whether the company can sustain momentum on product roadmaps and continue to deliver reliable services during the transformation. As with any major realignment, there is potential for short-term disruption even as the long-term objective is to reduce operating costs and accelerate innovation. The public narrative positions Block’s move as part of a larger wave of automation across the technology and financial services sectors, where AI investments are increasingly tied to workforce design and strategic scaling decisions.

Crypto World

Bitcoin Miner MARA jumps 17% after striking a deal with Starwood to build AI data centers

MARA Holdings shares jumped 17% after the bitcoin mining firm announced Thursday a partnership with Starwood Capital Group to build large data centers across its existing U.S. sites.

The agreement will convert select MARA locations, many of which were originally developed for Bitcoin mining, into facilities serving enterprise cloud and artificial intelligence customers.

Starwood, which manages more than $125 billion of assets, will lead design, construction and tenant sourcing through its data center arm, Starwood Digital Ventures. The partners expect to deliver about 1 gigawatt of computing capacity in the near term, with plans to scale beyond 2.5 gigawatts over time. The two firms will jointly finance and operate the projects.

The deal marks a major pivot for MARA.

The company built its reputation as a bitcoin miner, but it controls sites with direct access to large power supplies. That access has become valuable as tech firms struggle to secure power for new AI data centers.

MARA’s move fits into the trend of a slew of bitcoin miners repurposing their infrastructure to meet increasing demand for artificial intelligence compute. The pivot began after Bitcoin’s recent halving cut miners’ rewards in half. With rising power costs, shrinking bitcoin price and intensifying competition for mining, miners’ profit margins have been squeezed, forcing most firms to diversify or completely pivot into hosting machines for AI firms.

Most recently, another bitcoin miner, Bitfarms (BITF), said that it is rebranding as Keel Infrastructure as part of its pivot from bitcoin mining to data center development for high-performance computing (HPC) and AI workloads.

However, for MARA, it’s not ditching its identity as a bitcoin mining company. In fact, its CEO, Fred Thiel, said in a shareholder letter that “Bitcoin remains a core pillar of MARA’s strategy.”

“While the timing of a recovery in bitcoin prices is difficult to predict, our long-term conviction in the asset class remains unchanged,” Thiel added.

MARA has also reported fourth-quarter earnings, with revenues falling 6% to $202.3 million from $214.4 million in Q4 2024, citing a 14% decline in the average price of bitcoin mined over the quarter.

Twitter co-founder Jack Dorsey said that his company, Block, will reduce its workforce by nearly half, cutting more than 4,000 employees and shrinking the company from over 10,000 staff to just under 6,000.

The company is reportedly laying off staff become of AI tools potentially making them redundant.

AI-Driven Layoffs Continue

In a note to employees, Dorsey described the move as “one of the hardest decisions” in the company’s history. He said the layoffs were not driven by financial distress, stating that gross profit continues to grow and profitability is improving.

Instead, he pointed to rapid advances in intelligence tools and a shift toward smaller, flatter teams as the reason for the restructuring.

Affected employees will receive 20 weeks of salary plus one additional week per year of tenure.

They will also receive equity vested through the end of May, six months of healthcare coverage, corporate devices, and $5,000 in transition support. International terms will vary based on local laws.

Dorsey said he chose to act immediately rather than implement gradual reductions. He argued that repeated rounds of layoffs would damage morale and trust.

Block, formerly known as Square, operates merchant payment systems and the peer-to-peer service Cash App.

Cash App allows users to buy and sell Bitcoin. The company also holds Bitcoin on its balance sheet and invests in Bitcoin infrastructure, including self-custody tools and mining initiatives.

Dorsey has positioned Block as closely aligned with Bitcoin development.

Previously, Dorsey co-founded Twitter in 2006 and served as CEO twice. He stepped down in November 2021.

In October 2022, Elon Musk completed the acquisition of Twitter and later rebranded it as X. Dorsey publicly supported the takeover at the time.

The restructuring marks a significant shift for Block as Dorsey moves to run the company with smaller teams and intelligence-driven systems at its core.

TLDR

- Flare and Xaman introduced a one-click system that allows XRP holders to access DeFi directly from their existing wallets.

- The integration targets more than 2 billion XRP tokens that remain idle in wallets and outside decentralized finance.

- The new process removes the need for separate wallets, gas tokens, and complex bridging steps.

- FAssets create a wrapped version of XRP on Flare that interacts with smart contracts.

- Flare Smart Accounts allow users to authorize transactions using their current XRPL credentials.

Flare and Xaman introduced a new integration that targets more than 2 billion XRP tokens sitting idle in wallets. The companies estimate these tokens represent about 3.5% of the circulating supply and carry a value near $3 billion. The integration allows holders to access decentralized finance through a single in-wallet transaction.

Xaman Integrates Direct Vault Access on Flare

Xaman confirmed it reached an agreement with the Flare blockchain to simplify DeFi access for XRP holders. The company said users can now deposit XRP directly into a curated vault on Flare through one action. The update removes the need to download new wallets or manage gas tokens.

Many XRP holders previously avoided DeFi due to technical barriers and unfamiliar interfaces. The new system embeds the full workflow inside the existing Xaman wallet. Wietse Wind, founder of Xaman, said, “This integration lets our users explore new options directly from the wallet they already know, while keeping full control of their keys and decisions.”

The integration relies on three core components that operate in the background. FAssets create a trust-minimized representation of XRP on Flare for smart contract use. Flare Smart Accounts let users authorize transactions with existing XRPL credentials.

Xaman provides the front-end interface and guides users through the process. As a result, users avoid handling separate private keys across different chains. The process reduces operational steps to a single confirmation within the wallet.

Behind the scenes, the transaction carries structured instructions across systems. Flare’s Data Connector validates each request before execution. Smart Account controllers mint the wrapped asset and allocate it into vault strategies.

FAssets and Smart Accounts Power XRPFi Workflow

FAssets function as wrapped XRP that interacts with decentralized applications on Flare. The system creates FXRP, which users can deploy across lending and staking programs. Flare reported that minted FXRP supply has surpassed 100 million tokens.

More than 60 million FXRP tokens currently operate within staking programs and structured products. These figures show that some XRP holders already deploy assets into yield strategies. The new integration aims to expand that participation through simplified access.

Upshift manages the vault strategies while Clearstar curates capital deployment and risk controls. The companies structure strategies around lending markets and collateralized positions. They also use structured products to generate yield within defined parameters.

Flare compresses typical multi-step DeFi actions into one workflow through Smart Accounts. The system handles minting, allocation, and yield distribution automatically. Users only authorize the transaction through their existing credentials.

Recent market data showed XRP gained 6% earlier this week alongside a 212% rise in retail buying volume. Exchange-traded fund inflows have remained positive since their November launch. Flare and Xaman announced the integration as the FXRP minted supply crossed the 100 million mark.

Crypto World

From Crypto Treasury to RWA: ETHZilla Retreats and Relaunches as Forum Markets on Nasdaq

TLDR:

- ETHZilla rebrands as Forum Markets and begins trading under the Nasdaq ticker FRMM starting March 2, 2026.

- Shares collapsed roughly 96% from their August 2025 peak despite a 13.3% single-day gain on the rebrand news.

- Peter Thiel’s Founders Fund exited its 7.5% stake in Q4 2025 as ETHZilla’s Ethereum treasury strategy unraveled.

- Forum Markets shifts focus to regulated, tokenized real-world assets, moving away from single-asset crypto exposure.

ETHZilla is pulling back from its crypto-heavy balance sheet strategy after a dramatic share price collapse. The company announced a full rebrand to Forum Markets, with trading set to begin under the Nasdaq ticker “FRMM” on March 2.

The retreat follows months of investor exits, asset sales, and a sustained decline from last year’s highs. In place of Ethereum treasury holdings, the company is now directing its focus toward tokenized real-world assets built on regulated infrastructure.

ETHZilla Scales Back Crypto Holdings After Sharp Investor Exodus

ETHZilla built its identity around holding Ethereum directly on its balance sheet as a public company. The strategy was designed to give traditional investors exposure to Ethereum without directly purchasing the asset.

Shares soared to $107 on August 13, 2025, shortly after the company revealed plans for a $425 million Ethereum treasury. That announcement followed a pivot away from its earlier biotech business model.

The rally, however, proved short-lived as market conditions deteriorated and enthusiasm faded. The company began selling crypto assets to reduce its exposure as the stock continued sliding.

Investor confidence took a further blow when Peter Thiel’s Founders Fund exited its 7.5% stake during Q4 2025. Accounting for a 1-for-10 stock split executed in October, shares had fallen roughly 98% from their effective peak of $174.60.

The retreat from crypto exposure was gradual but deliberate. ETHZilla reduced its Ethereum holdings while exploring alternative business lines to shore up its equity performance.

One move included entering jet engine leasing through a new subsidiary called ETHZilla Aerospace. That unit tokenized equity in leased engines via the Eurus Aero Token I, deployed on the Arbitrum layer-2 network.

Shares climbed 13.3% to $3.91 on the day the rebrand was announced. Despite that recovery, the stock remains down approximately 96% from its August 2025 peak.

The single-day gain reflects cautious optimism around the company’s new direction. Whether that momentum continues under the Forum Markets name remains to be seen.

RWA Strategy Positions Forum Markets for a More Stable Model

The shift toward tokenized real-world assets marks a fundamental change in how the company plans to generate and sustain value.

Forum Markets intends to develop tokenized products backed by tangible assets using regulated infrastructure. That approach moves away from the volatility associated with holding large crypto positions on a public balance sheet. The aviation leasing venture offered an early preview of where the company is headed.

Vincent Liu, chief investment officer at Kronos Research, addressed the structural risks that drove the retreat. “Single-asset treasury strategies are highly dependent on strong market conditions and sustained equity premiums,” Liu told Decrypt.

He added that treasury-focused firms ultimately need revenue-generating businesses and broader asset exposure to remain relevant long term.

His comments reflect a broader concern within the industry about the sustainability of crypto-only balance sheet models.

Liu also pointed to specific weaknesses tied to Ethereum-focused strategies. He described the model as fragile, noting that its value is “tightly linked to network activity,” thereby creating “a correlation trap where purchasing power weakens during ecosystem downturns.”

Fragmentation across Ethereum’s base layer and its layer-2 networks further dilutes the overall narrative and premium.

He added that the model is “further undermined by the absence of a hard supply cap, leaving its long-term scarcity proposition open to question.”

Forum Markets is set to begin trading under the FRMM ticker on March 2, replacing the former ETHZ symbol on the Nasdaq Capital Market.

The rebrand draws a clear line between the company’s failed crypto treasury experiment and its new asset-backed direction.

The transition reflects a growing recognition that public companies cannot sustain themselves on crypto price appreciation alone. Building regulated, revenue-linked products appears to be the model Forum Markets is now betting on.

TLDR:

- UNI surged roughly 15% in 24 hours, outpacing Bitcoin’s 4.7% and Ether’s 8.5% gains during the same period.

- The governance proposal targets eight additional chains and would automate fee collection across all new v3 liquidity pools.

- Estimated new annualized revenue of $27 million would stack on top of $34 million already generated through UNI burns.

- Uniswap recorded $3.12 million in gross profit in Q1 2026, compared with effectively zero in all prior reporting periods.

A Uniswap governance vote to broaden its fee switch mechanism has pushed UNI higher by roughly 15% in 24 hours.

The proposal seeks to expand protocol fee capture across eight additional layer-2 chains. It would also automate fee collection across all v3 liquidity pools by default.

Estimates point to approximately $27 million in additional annualized revenue, building on the $34 million already generated through UNI burns since the fee switch launched late last year.

Uniswap Vote to Broaden Fee Switch Targets Multi-Chain Revenue

The governance vote to broaden the fee switch comes structured as two separate onchain proposals. Transaction limits required splitting the changes across two votes for technical reasons. Both votes target protocol fee activation across multiple blockchains beyond Ethereum.

Central to the proposal is a new tool called the v3OpenFeeAdapter. It applies protocol fees across all liquidity pools uniformly, based on each pool’s fee tier. This replaces the older model, which required governance to activate pools on a case-by-case basis.

The new system makes fee collection automatic for all newly created v3 pools going forward. This removes the need for repeated manual governance decisions for each pool. Over time, even long-tail trading pairs could begin contributing meaningfully to protocol revenue.

Since the fee switch first rolled out in late 2025, Uniswap has already burned over $5.5 million worth of UNI. That figure implies an annualized burn rate of around $34 million at current trading levels. The proposed expansion could layer an estimated $27 million more on top of that annual total.

UNI Climbs as Fee Switch Vote Draws Investor Attention

UNI’s 15% gain came as broader crypto markets also moved higher during the same period. Bitcoin rose around 4.7%, while Ether gained approximately 8.5% over 24 hours.

UNI’s move clearly outpaced both major assets, reflecting targeted investor interest in the governance vote.

The fee switch works by redirecting a share of trading fees away from liquidity providers toward the protocol treasury.

Those redirected funds support UNI token buybacks, burns, and treasury growth. This mechanism ties UNI’s market value more directly to Uniswap’s aggregate trading volume.

In Q1 2026, Uniswap posted roughly $3.12 million in gross profit, according to DeFi Llama data. That figure compares with effectively zero profit in periods before the fee switch activated.

The data reflects early but measurable progress in Uniswap’s shift toward a revenue-generating protocol.

Still, the broader vote to broaden the fee switch raises questions about liquidity competitiveness on layer-2 networks.

Fee-sensitive traders and market makers could shift activity to rival platforms offering better terms. How Uniswap manages that balance will likely shape both its revenue trajectory and UNI’s performance ahead.

The crypto industry’s stablecoin operations, such as the arrangement between issuer Circle and leading exchange Coinbase, could be under serious pressure in the U.S. Office of the Comptroller of the Currency’s newly proposed set of stablecoin rules.

Even as OCC chief Jonathan Gould testified in the U.S. Senate on issues that included crypto oversight on Thursday, people in the industry said they’ve been trying to understand his agency’s 376-page proposal to regulate domestic issuers under the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act that became law last year. The allowance of stablecoin yield and reward has not only been central to the GENIUS Act, but it’s also been a chief negotiation point in the more important follow-up legislation known as the Digital Asset Market Clarity Act.

Close financial ties between issuers and crypto platforms that handle their tokens “would make it highly likely that the issuer’s payments of yield or interest would be made to the holder through an intermediary or an attempt the evade the GENIUS Act’s prohibition on interest and yield payments,” the OCC proposal suggested.

The firms can rebut that presumption, the OCC said, “given the issuer provides sufficient evidence to the contrary.”

On the controversial point of rewards, the industry has worked under an assumption that the GENIUS Act’s ban on yield or rewards offered by stablecoin issuers doesn’t extend to third parties that can offer their own rewards programs on those issuers’ tokens, such as at Coinbase. But the OCC’s proposed language assumes that the law’s prohibition would be improperly evaded under certain third-party relationships, though the details are still being studied by crypto lobbyists and lawyers.

Industry insiders who requested anonymity acknowledged this opening effort looks bad, and they’ll line up to try to get it changed, but some suggest the agency’s wording may leave enough room that continued rewards could be manageable.

Todd Phillips, a former lawyer at the Federal Deposit Insurance Corp. and business professor in Georgia who tracks digital assets policy, agreed the proposed language doesn’t seem like a hard no.

“I think there’s some play in the joints of what the OCC has proposed,” Phillips told CoinDesk on Thursday. He said the opening language seems uncertain on whether it means to “shut down all permutations of stablecoin rewards.”

“The OCC has clearly gone beyond what the statute requires,” Phillips said, adding that the extent of the restriction “is open to debate.”

The agency didn’t immediately respond to questions from CoinDesk.

The crypto industry’s primary policy aim in Washington is to advance the Clarity Act’s regulations for the overall U.S. digital asset markets. In that legislative negotiation, this issue of stablecoin yield has become one of the leading points of contention, with U.S. bankers arguing that such yield threatens their foundational dependence on customer deposits. During those talks, the crypto side has repeatedly argued that the GENIUS Act, as it stands, allows third party crypto firms to offer rewards on stablecoin holdings and activities.

One of the insiders in the negotiation told CoinDesk on Thursday that the OCC’s action should undermine the banks’ lobbying, because what’s the point of hashing out stablecoin yield in further legislation when the banking regulator has already taken it up as a proposed rule? Despite that, they also said the OCC overreached, and the industry will likely fight the proposed rulemaking even as the Clarity Act continues its way through Congress.

Meanwhile, the proposals advanced by Gould — a former chief legal officer at Bitfury who has otherwise been strongly supportive of the crypto industry — casts some doubt on industry confidence that GENIUS will protect stablecoin rewards programs, which represents a significant business at Coinbase. The U.S. crypto exchange hasn’t yet made any public statements, and a company spokesperson declined to comment.

The proposed rulemaking from the OCC, which charters and oversees national banks and trusts in the U.S., is preliminary, opening the ideas to a public comment period that would later have to be followed up with a final rulemaking process. With controversial rules, this process usually requires months of discussion and review.

If the OCC does cut off the ability of crypto platforms to extend stablecoin yield to customers, it may eliminate one of the Clarity Act sticking points, though other matters are also still standing in the way of the bill. Democratic lawmakers have insisted — for instance — that the legislation address potential conflicts of interest posed by senior government officials, such as President Donald Trump, personally profiting from the crypto industry.

At a Thursday hearing before the Senate Banking Committee, stablecoin rewards came up often as a business that scares the banking industry. Regulators suggested they haven’t yet seen a flight of deposits from banks.

“We have to take these concerns, the concerns of community banks, especially seriously,” said Senator Angela Alsobrooks, a Democrat who sought to negotiate a compromise in the Clarity Act to ban the crypto industry from rewards on stablecoin holdings in a way that resembles a deposit account. So far, negotiations among the political parties, the banks, the crypto industry and the White House haven’t yet advanced to a compromise that can get to a vote in the Senate.

Read More: OCC pitches stablecoin rules as U.S. Senate holds banking hearing in which crypto stars

KCS token price outlook as KuCoin taps Zypto for everyday crypto payments

Farage unbothered by death threats reposted by his councillor

‘Don’t know what the fuss was about’ – chaotic Palace season could end in glory

-

Video7 days ago

Video7 days agoXRP News: XRP Just Entered a New Phase (Almost Nobody Noticed)

-

Politics5 days ago

Politics5 days agoBaftas 2026: Awards Nominations, Presenters And Performers

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Boden – Corporette.com

-

Sports3 days ago

Sports3 days agoWomen’s college basketball rankings: Iowa reenters top 10, Auriemma makes history

-

Politics3 days ago

Politics3 days agoNick Reiner Enters Plea In Deaths Of Parents Rob And Michele

-

Business2 days ago

Business2 days agoTrue Citrus debuts functional drink mix collection

-

Crypto World3 days ago

Crypto World3 days agoXRP price enters “dead zone” as Binance leverage hits lows

-

Business4 days ago

Business4 days agoMattel’s American Girl brand turns 40, dolls enter a new era

-

Business4 days ago

Business4 days agoLaw enforcement kills armed man seeking to enter Trump’s Mar-a-Lago resort, officials say

-

Tech2 days ago

Tech2 days agoUnsurprisingly, Apple's board gets what it wants in 2026 shareholder meeting

-

NewsBeat23 hours ago

NewsBeat23 hours agoCuba says its forces have killed four on US-registered speedboat | World News

-

NewsBeat1 day ago

NewsBeat1 day agoManchester Central Mosque issues statement as it imposes new measures ‘with immediate effect’ after armed men enter

-

NewsBeat4 days ago

NewsBeat4 days ago‘Hourly’ method from gastroenterologist ‘helps reduce air travel bloating’

-

Tech4 days ago

Tech4 days agoAnthropic-Backed Group Enters NY-12 AI PAC Fight

-

NewsBeat4 days ago

NewsBeat4 days agoArmed man killed after entering secure perimeter of Mar-a-Lago, Secret Service says

-

Politics4 days ago

Politics4 days agoMaine has a long track record of electing moderates. Enter Graham Platner.

-

NewsBeat2 days ago

NewsBeat2 days agoPolice latest as search for missing woman enters day nine

-

Business20 hours ago

Business20 hours agoDiscord Pushes Implementation of Global Age Checks to Second Half of 2026

-

Crypto World2 days ago

Crypto World2 days agoEntering new markets without increasing payment costs

-

Sports4 days ago

Sports4 days ago2026 NFL mock draft: WRs fly off the board in first round entering combine week