Crypto World

Real estate tokenization’s missing layer

Disclosure: The views and opinions expressed here belong solely to the author and do not represent the views and opinions of crypto.news’ editorial.

Despite the wave of attention RWAs have received over the past couple of years, there’s a sense that everyone is waiting for something to shift. The problem is that many “tokenized” assets are still legal promises dressed up as tokens. Vague token rights, improvised custody and transfer controls, and servicing shortcomings make the whole thing still feel speculative. While the tokenised RWA market sits around $25B (which demonstrates serious growth), it’s still modest in comparison to global markets.

Summary

- Tokens aren’t titles: Many RWAs remain legal promises wrapped in blockchain rails. Without enforceable rights, controlled transfer, and servicing, tokenization stays speculative.

- The UAE is building the legal stack: Through DIFC, ADGM, and the Dubai Land Department, the UAE is treating tokenized real estate as regulated market infrastructure — not a crypto experiment.

- Rights beat throughput: The trillion-dollar RWA opportunity will go to jurisdictions that make token-holder rights unambiguous and enforceable, not to chains with the fastest settlement.

In Dubai, work on this is picking up. The Dubai Land Department has launched Phase II of its Real Estate Tokenization Project, with secondary-market resales scheduled to begin on 20 February 2026. In DIFC, the DFSA’s inaugural tokenization regulatory sandbox drew 96 expressions of interest. In short, the UAE is assembling the regulatory and institutional scaffolding needed to make tokenised real estate scalable – that’s certainly something worth talking about.

The crypto RWA fallacy

The best RWA pitch in crypto happens to be the simplest: take a deed, a fund share, or a receivable, put it on-chain, and let liquidity do the rest. In practice, that often means shipping a minting interface attached to a legal promise that lives somewhere else. The token trades 24/7, but the underlying rights don’t.

When markets tighten, everyone rediscovers the same truth: a token is not a title, nor a court order. Instead, it’s a digital representation recorded on a programmable platform – and it’s notoriously difficult to make it legally and operationally identical to what it claims to represent.

This idea shows up in three places. First, think about enforceability. If token holders can’t clearly understand what they own, what jurisdiction governs it, and how a claim is enforced, the idea of ownership is just branding. As a matter of fact, IOSCO warns that investors may not understand the legal aspects of ownership and transfer rights for tokenised assets, and flags legal uncertainty as a central risk holding back adoption.

Second, consider controlled transfer. Real assets don’t move like meme coins. Eligibility checks, transfer restrictions, and the ability to halt or reverse activity under lawful orders are not optional in institutional markets. OECD research notes that implementing restrictions like forced transfers or trading suspensions can be especially challenging on public, permissionless networks.

Third, there’s servicing. Real estate is an operating system: taxes, insurance, maintenance, tenant issues, distributions, valuations, reporting, audits. Tokenization can streamline records and transactions, but it doesn’t eliminate the admin layer that makes cash flows real and disclosures defensible. Until projects address these issues, RWAs are a bit stuck.

The UAE’s blueprint

If the UAE wins the real estate tokenization boom, it will be because it treated tokenization as a regulated financial product, a market-structure upgrade, and has built rules and institutions around that assumption.

- In DIFC, the DFSA launched a dedicated tokenization Regulatory Sandbox and drew 96 expressions of interest. This is an early indicator that serious firms are looking for a supervised pathway.

- In Abu Dhabi, ADGM has been explicit about positioning itself as a comprehensive regulatory home for digital assets, and it went further by introducing a DLT Foundations regime designed for token issuance and on-chain organisational structures.

- In 2025, the DIFC reported 8,844 active companies, demonstrating rapid year-on-year expansion.

- In Dubai, the Dubai Land Department is running a controlled pilot that explicitly tests governance, investor protection, and operational readiness while enabling secondary-market resale from 20 February 2026.

- The UAE also hosts pools of dry powder that can fund compliant issuance once the infrastructure is credible. Mubadala reported AED 1.2 trillion in assets under management, and Reuters notes Abu Dhabi’s major funds together manage around $1.7 trillion.

The UAE is building something of a regulatory SDK for RWAs — standardized rules, venues, and counterparties that make tokenized real estate deployable.

The winning stack

The projects that scale in the UAE are likely to be regulated market infrastructure that happens to use blockchain. Starting with licensing. In DIFC, the DFSA’s tokenization Regulatory Sandbox provides a supervised route where selected firms can test in a controlled environment and, if successful, transition toward full authorisation.

Next, the packaging has to be familiar. DIFC SPVs (Prescribed Companies) are designed to ring-fence and isolate assets and liabilities (something institutions already understand and can underwrite). Tokenization then simply becomes a distribution and settlement upgrade.

Then comes the hard constraint most crypto-native RWAs avoid – controlled transfer and custody. Institutional markets require governance, safe custody, and clear oversight. ADGM’s FSRA guidance is clear about addressing safe custody, market abuse, and related controls via a thorough regulatory framework.

Finally, the winning stack anchors to the registry. The Dubai Land Department is currently testing tokenization on title deeds within a regulated model, in collaboration with VARA, and moving into a phase that activates secondary resale under a controlled framework focused on governance and investor rights.

Put together, the archetype that wins looks license-first, SPV-based, compliance-native, and obsessed with issuance plus servicing.

The implication for crypto

Here’s the part crypto needs to internalize — the trillion-dollar RWA upside will be won by the players that can make token-holder rights unambiguous, transfers compliant, and cash flows serviceable at scale.

IOSCO makes a good point — investors can end up unsure whether they hold the underlying asset or merely a digital representation, with risks concentrated around legal structure and intermediaries rather than chain throughput.

That’s why the UAE matters to the broader market. The Dubai Land Department is running a controlled tokenization pilot that moves into secondary resale from 20 February 2026, framed around governance, operational readiness, and investor protection. DIFC’s regulator is doing the same at the market-structure level.

For crypto, the chain becomes the settlement, transparency, and automation layer (inside this regulated perimeter). It’s useful precisely because it is programmable, auditable, and interoperable. But pay attention to the jurisdictions and infrastructure providers building enforceable rights – that’s arguably more important right now.

TLDR

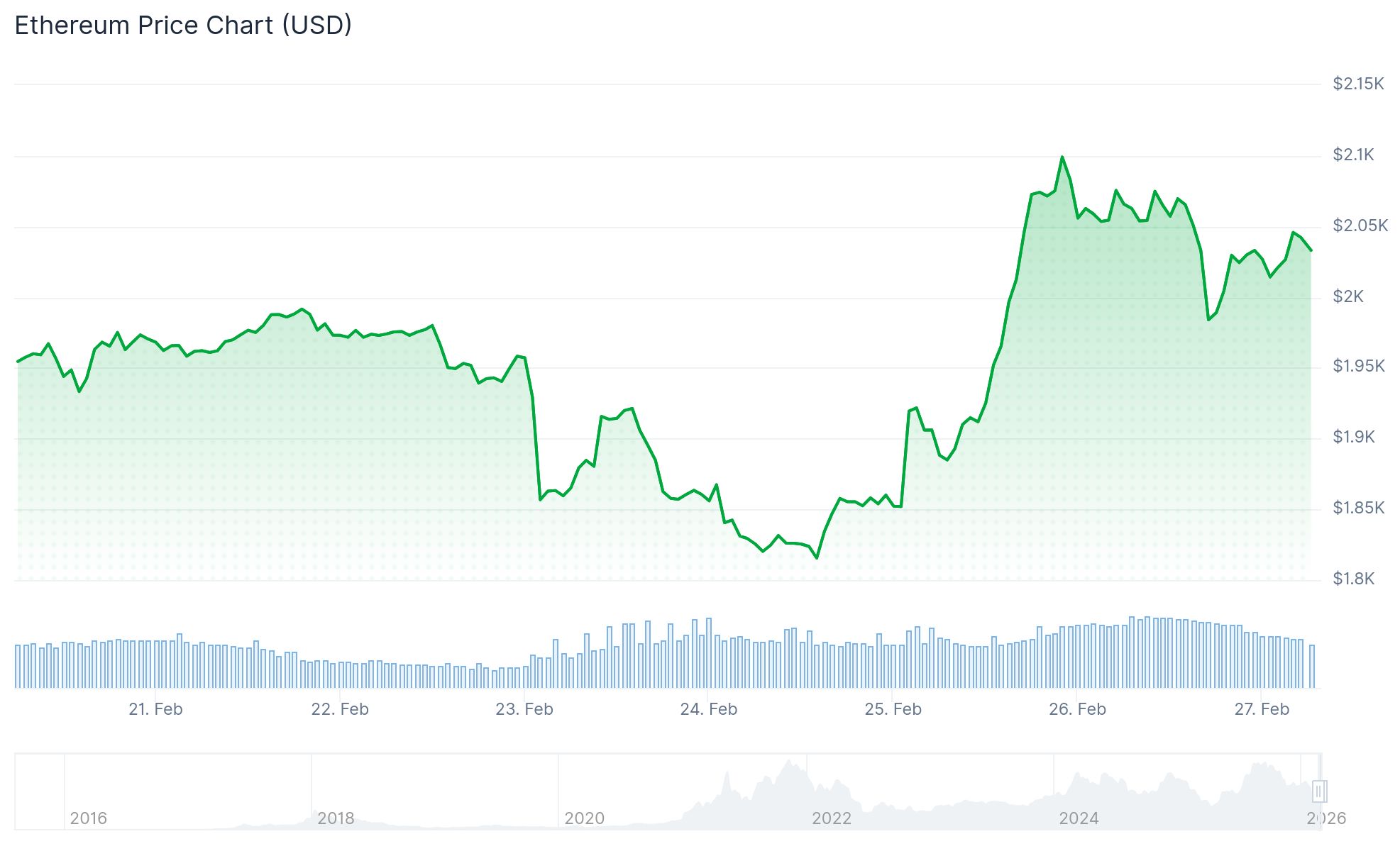

- Ethereum touched $2,150 this week before encountering resistance across several technical indicators

- The $2,100 level represents a critical threshold, matching the realized price for wallets containing 100,000+ ETH

- The 30-day realized volatility for ETH approaches 0.97, marking the highest point since March 2025

- Liquidations of short positions exceeded $220M across 48 hours, while funding rates shifted into positive territory

- ETF outflow pressure shows signs of weakening, although definitive accumulation trends remain absent

Ethereum surged to $2,150 during Thursday’s trading session before experiencing a retracement. The cryptocurrency continues navigating a narrow trading corridor, with $2,000 serving as crucial support and $2,100 emerging as the next significant barrier.

Closing above $2,100 on the daily timeframe carries particular significance as this price point corresponds to the realized price for addresses holding 100,000 ETH or greater. The realized price metric represents the average acquisition cost based on the last on-chain movement, providing insight into whether major stakeholders maintain profitable positions.

Historical data from 2020 onward reveals ETH has rarely traded beneath this whale cohort’s cost basis, with the most notable exception occurring throughout 2022’s bear cycle. Previous tests of this threshold have typically preceded price recoveries.

Futures and Funding Rates

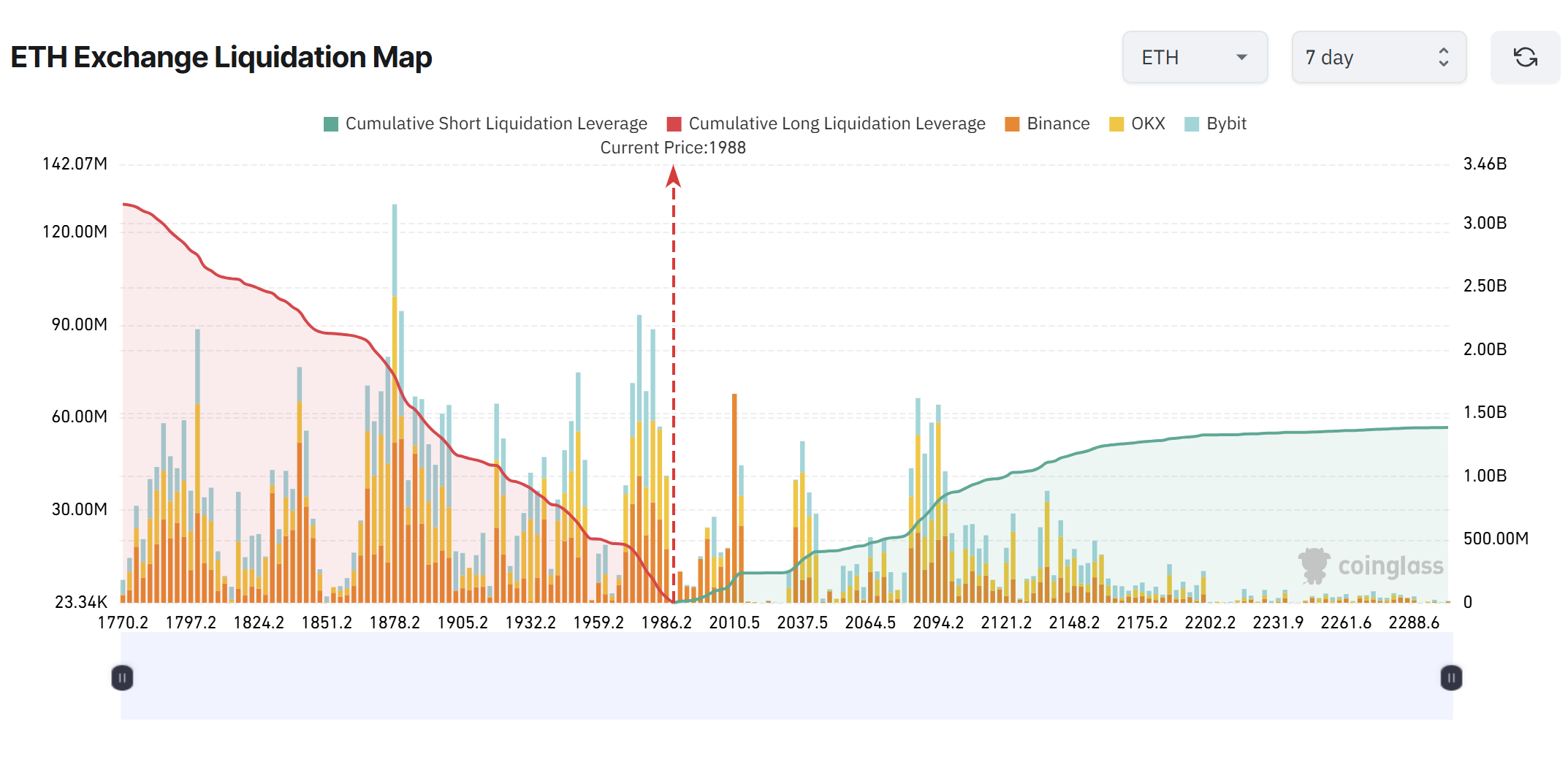

The derivatives market witnessed short position liquidations exceeding $220 million during the previous 48-hour period, eliminating substantial leveraged positions. Binance funding rates, which plunged deeply negative in early May as bearish positions accumulated, have reversed course to reach positive 0.23%.

This reversal indicates that traders who opened shorts late in the cycle faced forced liquidations. Nevertheless, with funding rates now trading at elevated positive levels, the market structure favors long positions, creating potential vulnerability for a long squeeze toward $1,800 should upward momentum weaken.

Approximately $2.66 billion in long position liquidation exposure clusters around the $1,800 price zone, establishing a substantial liquidity pocket beneath current trading levels.

Volatility and ETF Flows

Ethereum’s 30-day realized volatility measured on Binance has climbed to approximately 0.97, representing the highest measurement recorded since March 2025. Heightened volatility during this phase may indicate market uncertainty and directional indecision rather than establishing a clear trend.

Price action continues trading beneath the 50-day, 100-day, and 200-day moving averages. Following the rejection near $4,800 in late 2025, each subsequent recovery attempt has established lower peaks, suggesting persistent distribution pressure.

Regarding ETF activity, selling pressure appears to be diminishing. Following substantial outflows throughout mid-2025, recent flow statistics indicate reduced movement in either direction. Institutional distribution seems to be decelerating, although convincing accumulation signals have yet to materialize.

Market analyst Leon Waidmann observed that retail participants with low conviction have predominantly exited their positions. Short interest continues declining, while highly leveraged long positions have been slow to establish meaningful presence.

Technical strategist IncomeSharks identified three overhead resistance zones, including multiple SuperTrend rejections and channel resistance positioned near $2,250. The analyst additionally highlighted April’s lows around $1,500 as a critical downside level should demand weaken once more.

At press time, ETH was changing hands at $2,034.

Bitcoin’s (BTC) downturn has spurred conspiracy theories around alleged market manipulation by firms. However, Bitwise’s Chief Investment Officer (CIO), Matt Hougan, argues that the primary reasons are more straightforward.

This narrative highlights the ongoing debate about what drives major crypto market moves, whether it’s institutional strategies, technological threats, or fundamental market cycles.

Why is Bitcoin’s Price Dropping?

Hougan addressed widespread speculation on social media that Bitcoin’s drop was the result of coordinated moves. BeInCrypto previously reported that some users made allegations against Binance.

More recently, some community members pointed to recurring patterns such as the alleged “10 AM Bitcoin dump” by Jane Street. The executive dismissed these narratives directly, calling the actual explanation “far more boring” than the theories suggest.

“The conspiracy theories are wild. First it was Binance and then it was Wintermute and then it was an unknown offshore macro hedge fund and then it was paper bitcoin and. today it is Jane Street and next week it will be someone else,” he said.

Follow us on X to get the latest news as it happens

Hougan said the “real reason Bitcoin is down” is that long-term holders have been reducing exposure. According to him, investors cut positions by selling spot Bitcoin, closing leveraged trades, and writing covered calls, creating downward pressure on the price.

The Bitwise CIO attributed selling behavior to three factors:

- The four-year market cycle theory.

- Concerns surrounding quantum computing.

- Capital rotation from crypto into artificial intelligence (AI) startups.

The quantum computing discussion has gained traction in the crypto community recently. While MicroStrategy co-founder Michael Saylor recently downplayed concerns about quantum risks, some investors remain cautious.

Kevin O’Leary, the Canadian businessman and Shark Tank investor, has warned that institutional investors are capping Bitcoin allocations at around 3% until the industry demonstrates a credible solution to quantum vulnerabilities. Jefferies’ global head of equity strategy, Christopher Wood, went further, removing a 10% Bitcoin allocation from the model portfolio over the same concerns.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

Crypto Winter’s Timeline and Prospects for Recovery

Meanwhile, Hougan added that most of the selling is likely complete. He claimed that Bitcoin is in the “process of bottoming” and could eventually reach new all-time highs. According to him,

“This is a classic crypto winter and there will be a classic crypto spring.”

Hougan previously stated that the current crypto winter began in January 2025, and given the 13-month historical duration, the end could be near.

On-chain analyst Willy Woo offered a more nuanced view. He said the recent sell-off appears exhausted but cautioned that deteriorating spot and futures liquidity could cap any near-term rebound.

Woo’s timeline places the end of bearish conditions in Q4 2026, with bullish momentum potentially returning in Q1 or Q2 2027.

“~45k would be a typical bear market bottom. BTC has only ever existed in a secular global macro bull market 2009-2026. If global macro breaks down, then 30k is the fall back level of support, 16k as the final line to maintain BTC’s bull trend,” Woo wrote.

The distance between these timelines reflects a broader uncertainty about where exactly the market sits in its cycle. What analysts broadly agree on is that Bitcoin’s current weakness reflects structural and psychological forces, not manipulation.

Australia’s crypto market is making progress in user growth and regulatory reforms, but there are still a range of issues to iron out in the sector, crypto executives told Cointelegraph.

On the sidelines of the XRP Australia 2026 event in Sydney on Friday, Coinbase APAC managing director John O’Loghlen said the country has seen positive regulatory momentum and growing expertise among those tasked with policing the industry.

“Multiple arms of government, mainly Treasury, who are writing the draft regulation and ASIC have thoroughly upskilled their teams and have pretty deep digital asset domain expertise internally. So I think there’s been pretty positive movement.”

O’Loghlen also said institutional interest and access are growing through products like crypto exchange-traded funds. Australia’s first ETF, which holds Bitcoin (BTC) directly, went live in June 2024, followed by an ETF that holds Ether (ETH) in October 2024.

He also noted that Coinbase Global’s inclusion in the Standard & Poor’s 500 (S&P 500) index offers Australian institutions a means to access crypto-related stocks, allowing them to learn “about the industry in a very passive way.”

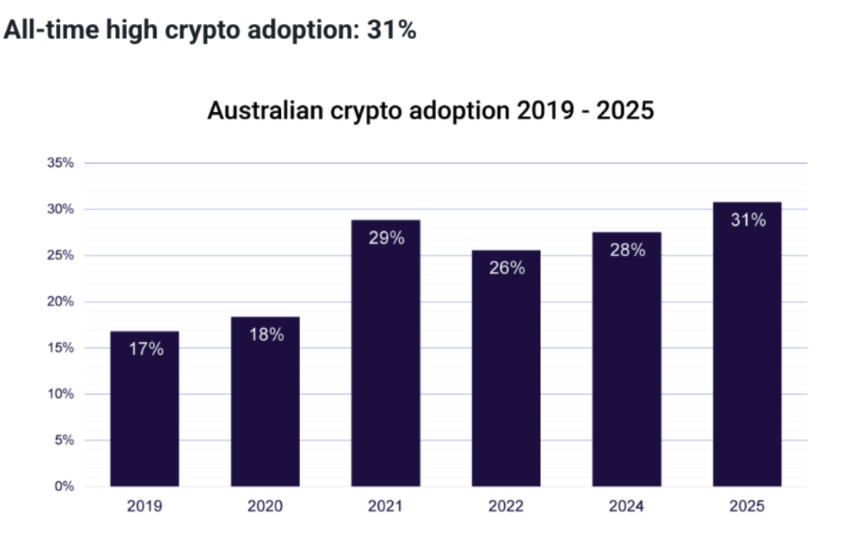

A 2025 report from crypto exchange Independent Reserve found that crypto adoption among Australians reached 31%, up from 28% in 2024. Additionally, 29% said they planned to invest in the next 12 months.

Self-managed super fund investors eye crypto

OKX Australia CEO Kate Cooper noted that a significant area of growth for the exchange has come from sophisticated traders, self-managed super fund (SMSF) trustees and high-net-worth individuals.

At the same time, she said across the industry there are a growing number of new self-managed super funds being set up specifically so trustees can invest in digital assets, “because they currently can’t invest via the big super funds.”

SMSFs are retirement funds set up and managed by individuals, rather than conventional funds managed by large institutions on behalf of users.

In a yet-to-be-released OKX report on SMSFs, Cooper said many respondents were interested in digital assets to diversify their holdings.

“That’s the feedback that we got through the research: a significant number of people wanting a diversified portfolio, wanting not just crypto, but digital assets more broadly, to be held as part of their portfolio. And SMSF is one of the main ways to do that.”

Lingering issues remain in Australia’s crypto scene

Last September industry executives, including Cooper, told Cointelegraph that users in Australia still face banking barriers when engaging with exchanges and other crypto businesses.

“It’s absolutely still a challenge in the industry,” Cooper said. “I don’t think there’s been any improvements. And we’re working hard with governments to encourage them to set some standards around it.”

O’Loghlen also called for solutions to debanking, stronger protections for blockchain payments innovation and greater support for Australian stablecoins.

“Regulatory settings must support innovation rather than inadvertently constrain it,” he said.

Related: Crypto lobby slams Australian broadcaster’s ‘sensational’ Bitcoin article

“As the Regulation of Payment Service Providers reforms are developed, it will be important to ensure that non-custodial wallet developers and public blockchain infrastructure providers are not unintentionally captured within licensing regimes designed for intermediaries,” O’Loghlen added.

Australian legal and regulatory landscape in limbo

Meanwhile, Australian crypto lawyer Bill Morgan said the Australian legal and regulatory crypto landscape appears to be in “wait and see” mode at the moment, following the ongoing court case between the Australian Securities and Investments Commission (ASIC) and fintech firm Block Earner.

ASIC is appealing a Federal Court decision siding with Block Earner about whether it was required to hold a financial services license for its crypto-related products.

He also pointed to a change in government that could be slowing legislation down.

“I think to some extent it’s a function of having three-year terms. There was some momentum under the former Liberal National Party coalition government, but then, when Labor won its first term four years ago, it took a while for it to get going again.”

Magazine: 6 massive challenges Bitcoin faces on the road to quantum security

Crypto World

Bitcoin ETF holders and treasury firms stack protection against price crash below $60,000, options exchange says

Bitcoin ETF holders and corporate treasuries – the players everyone praises for their long-term vision – are stacking insurance against price crash below $60,000, cryptocurrency exchange Deribit told CoinDesk.

“ETF holders and corporate treasuries are buying 6-month and 1-year puts at $60k or below ($60,000 put, a derivative contract offering protection against potential price slide below that level) as portfolio insurance,” Jean-David Péquignot, chief commercial officer of derivatives exchange Deribit.

This put option works like insurance: It lets buyers sell bitcoin at $60,000 even if the price crashes lower, shielding ETF investors and corporate treasuries with BTC from steeper losses while they hold for the long haul.

Péquignot was responding to questions about surging interest in the $60,000 put. At the time of writing, those contracts had $1.50 billion in open interest – the highest across all strikes and expiries on Deribit. On the exchange, one contract represents one BTC. The platform accounts for nearly 80% of the global crypto options activity.

The surge in interest in $60,000 puts expiring in six months or longer signals deep fears that any price bounce could fizzle fast, paving the way for a sharper drop.

What makes this hedging even more noteworthy is that ETF holders and corporate treasuries own a significant supply of bitcoin.

Investors have poured billions into U.S.-listed spot bitcoin ETFs and similar products worldwide in recent years. The U.S. funds alone have seen inflows of 1.26 million BTC, roughly 6% of bitcoin’s total circulating supply. Meanwhile, publicly listed firms hold about 1.14 million BTC, or 5.7% of BTC’s supply.

Bitcoin has been trading choppy below $70,000, having hit lows near $60,000 early this month, CoinDesk data show. The cryptocurrency has gained nearly 5% since Wednesday to trade near $67,500, but the options market remains unimpressed, with puts continuing to trade at a significant premium to calls or bullish bets.

“While spot price climbed, the 25-delta risk reversal remained stubborn. 30-day puts are still trading at a ~7% volatility premium over calls, signaling that smart money is still paying up for downside protection rather than chasing the pump,” Péquignot said.

He added that volatility may pick up as prices drop below $63,000. That’s because dealers and market makers who create order-book liquidity are “short gamma” at $60,000 or lower.

This means that as prices approach $60,000, these entities may sell more to rebalance their overall exposure to neutral, inadvertently adding to downside volatility.

XRP Ledger Foundation has confirmed it has patched a critical vulnerability found in an yet-to-be-enabled amendment of Ripple’s XRP Ledger, averting a potentially major exploit.

On February 19, a security engineer at cybersecurity firm Cantina, Pranamya Keshkamat, and the Cantina AI security bot identified a “critical logic flaw” in the signature-validation logic of Ripple’s blockchain, XRP Ledger, reported the XRP Ledger Foundation on Thursday.

The vulnerability in the signature validation code batch amendment would have allowed an attacker to execute transactions from victim accounts, including draining funds, without ever having the victim’s private keys.

“The amendment was in its voting phase and had not been activated on mainnet; no funds were at risk,” stated the XRPLF.

Exploitation may have destabilized the ecosystem

In addition to the potential theft of funds and modification of the ledger state, the vulnerability could have “destabilized the ecosystem,” the XRPLF said.

“A successful large-scale exploit could have caused substantial loss of confidence in XRPL, with potentially significant disruption for the broader ecosystem.”

Related: Cybersecurity stocks fall after Anthropic unveils Claude Code Security

Cantina and Spearbit CEO Hari Mulackal said, “our autonomous bug hunter, Apex, found this critical bug.”

“Had this been exploited, it would have been the largest security hack by dollar value in the world, with nearly $80 billion at direct risk,” he added, possibly referring to XRP (XRP) market capitalization.

Emergence of AI cybersecurity scanners

The autonomous AI security tool developed by Cantina AI identified the vulnerability via “static analysis of the rippled codebase,” and submitted a disclosure report allowing the Ripple engineering teams to validate it and begin patching the code.

Validators were advised to vote against the amendment, and an emergency release (rippled 3.1.1) was published on Feb. 23 to block the amendment from activating, stated the XRPLF.

AI is increasingly being deployed for cybersecurity purposes to sniff out code bugs that may be overlooked by human eyes.

Anthropic released Claude Code Security, its AI cybersecurity vulnerability scanner, which it claims “can reason like a skilled security researcher” on Feb. 20, causing a slide in public IT security company shares.

Magazine: AI won’t make you rich but crypto games might, Axie founder steps down: Web3 Gamer

Editor’s note: Splunk’s new CISO Report highlights a shifting security landscape where CISOs are expanding AI governance and risk management as a core mandate. The study surveys 650 CISOs globally and underscores AI’s role in speeding threat detection, improving data correlation, and shaping security strategy—while leaders weigh social engineering risks and deployment pace in an era of rising threat sophistication. The findings emphasize that AI is a business enablement tool and that talent remains essential to translating technology into resilient outcomes.

Key points

- 95% cite threat actor sophistication as the greatest risk; 92% prioritize threat detection and response; 78% strengthen identity and access management; 68% invest in AI cybersecurity capabilities.

- 92% say AI enables reviewing more security events.

- 89% report improved data correlation with AI.

- 39% of CISOs who have partially or fully adopted agentic AI say it has increased their teams’ reporting speed by more than double.

- 82% believe agentic AI will increase the amount of data reviewed and speed up correlation and response.

Why this matters

AI is a strategic driver of resilience as CISOs take broader AI governance and risk duties while balancing speed and security. Talent, collaboration, and business-focused metrics will shape outcomes in an AI-enabled era.

What to watch next

- Adoption of agentic AI and its impact on detection speed and decision-making.

- Expansion of AI governance and DevSecOps responsibilities within security leadership.

- Ongoing concerns about social engineering and the need for robust threat models.

- Workforce burnout and data-sharing challenges as CISOs consolidate data and seek cross-department insights.

Disclosure: The content below is a press release provided by the company/PR representative. It is published for informational purposes.

Splunk Report: Agentic AI Takes Center Stage in CISOs’ Path to Digital Resilience

- Nearly all CISOs Report They Are Now Responsible for AI Governance and Risk Management, Cite the Growing Sophistication of Threat Actor Capabilities as Their Greatest Risk

- Vast Majority Say AI Enables More Security Events to be Reviewed

SAN JOSE, Calif. – February 25, 2026 – Cisco today announced the release of Splunk’s annual report, The CISO Report: From Risk to Resilience in the AI Era, surveying 650 global Chief Information Security Officers (CISOs). The report highlights CISOs’ rapidly expanding role, their strategic approach to AI adoption, and a steadfast commitment to human talent as they confront an increasingly complex landscape.

“CISOs operate in the eye of the storm, at the center of constant transformation. Role responsibilities expand, threats evolve, and AI accelerates everything,” said Michael Fanning, CISO, Splunk. “This expanded mandate brings an exceptional level of pressure and personal accountability. We are not just managing technology. We are managing risk, talent, and the digital resilience that drives critical business outcomes.”

The AI Imperative

AI is recognized as a powerful business imperative and productivity powerhouse for security teams, including agentic AI. The survey highlights:

- 95% of CISOs cite the growing sophistication of threat actor capabilities as their greatest risk. Ninety-two percent of CISOs say that improving threat detection and response capabilities is a top priority, followed by strengthening identity and access management (78%), and investing in AI cybersecurity capabilities (68%).

- 92% of CISOs say AI enables their teams to review more security events.

- 89% report improved data correlation with AI.

- 39% of CISOs who have partially or fully adopted agentic AI strongly agree it has increased their teams’ reporting speed by more than double the rate of those who are still exploring (18%).

- 82% of CISOs believe agentic AI will increase the amount of data reviewed and 82% say it will increase correlation and response speeds.

While CISOs’ approach AI with cautious optimism, 86% fear agentic AI will increase the sophistication of social engineering attacks, and 82% worry it will increase deployment speed and complexity of persistence mechanisms. Ultimately, AI is seen as essential for combating advanced threats and delivering significant business advantages.

Expanded Mandate and Personal Stakes

CISOs are operating at the leading edge of digital transformation, with nearly four out of five reporting their role has become significantly more complex. More than three quarters of CISOs are now worried about personal liability for security incidents, a sharp jump from last year, when just over half expressed similar fears, underscoring the high stakes involved. Nearly all respondents now report that CISOs responsibilities include AI governance and risk management, with more than four out of five also overseeing secure software development (DevSecOps).

Talent Over Tech in Closing Gaps

Despite the rise of AI, CISOs are prioritizing human capital to address critical skills gaps. Their main strategies include upskilling current workforces, hiring new full-time employees, and engaging contractors. This reflects a belief that human intelligence and creativity remain security’s most powerful tools, especially for nuanced tasks like threat hunting.

Security is a Team Sport

Shared ownership is proving critical for stronger cybersecurity outcomes. Joint accountability drives the most value for key security initiatives (62%), security budget and funding (55%), and access to security-relevant data (49%), indicating that collaboration across the C-suite is a force multiplier for resilience.

Burnout and the Quest for Clarity

The report reveals a significant challenge in workforce retention, with nearly two-thirds of security teams experiencing moderate to significant burnout. Leading stressors include:

- High alert volumes (98%)

- False alerts (94%)

- Tool fatigue (79%)

To address these issues, CISOs are consolidating security data into a single view and using data-driven narratives to translate technical nuances into clear business imperatives for non-technical leadership. However, challenges to improving cross-departmental data sharing persist, such as:

- Data privacy concerns (91%)

- High storage costs (76%)

- Lack of shared data views (70%)

Reframing Security as a Business Enabler

CISOs are increasingly focused on translating cybersecurity’s value into clear business outcomes. Incident reduction, improved Mean Time to Detect (MTTD), and Mean Time to Respond (MTTR) are the top metrics used to communicate ROI to leadership. Collaboration with C-suite peers, especially on budgeting and key initiatives, is crucial for success.

The CISO Report highlights the transformation of the CISO role into a strategic leader. The report demonstrates how these executives are effectively navigating complex challenges by championing data-driven strategies, fostering human-centric leadership, and thoughtfully integrating AI. Through these approaches, CISOs are strengthening digital resilience and empowering their organizations to thrive in an ever-evolving threat landscape.

To download the 2026 CISO Report, please visit the Splunk website.

Methodology

Oxford Economics researchers surveyed 650 Chief Information Security Officers (CISOs) in July and August of 2025. Respondents resided in Australia, France, Germany, India, Japan, New Zealand, Singapore, the United Kingdom, and the United States. They represented nine industry groups: manufacturing, telecommunications, media and communications, financial services, public sector, energy and utilities, transportation and logistics, retail and consumer goods, healthcare and life sciences, and information services and technology.

About Cisco

Cisco (NASDAQ: CSCO) is the worldwide technology leader that is revolutionizing the way organizations connect and protect in the AI era. For more than 40 years, Cisco has securely connected the world. With its industry leading AI-powered solutions and services, Cisco enables its customers, partners and communities to unlock innovation, enhance productivity and strengthen digital resilience. With purpose at its core, Cisco remains committed to creating a more connected and inclusive future for all.

Cisco and the Cisco logo are trademarks or registered trademarks of Cisco and/or its affiliates in the U.S. and other countries. A listing of Cisco’s trademarks can be found at http://www.cisco.com/go/trademarks“>http://www.cisco.com/go/trademarks. Third-party trademarks mentioned are the property of their respective owners. The use of the word ‘partner’ does not imply a partnership relationship between Cisco and any other company.

Media Contact

Gabrielle Jasinski

Splunk LLC

Another week has ended, and it is also the end of the month, which means a bigger batch of Bitcoin and Ether options contracts are expiring while spot markets cool off again.

Around 115,500 Bitcoin options contracts will expire on Friday, Feb. 27, with a notional value of roughly $7.8 billion. This event is much larger than usual because it is the end of the month, so there could be a little volatility on spot markets.

Crypto markets have seen a little daylight with a mid-week lift, but total capitalization has remained the same as gains are starting to erode again, and zooming out shows they’re still in a downtrend.

Bitcoin Options Expiry

This week’s batch of Bitcoin options contracts has a put/call ratio of 0.76, meaning that there are more expiring calls (longs) than puts (shorts). Max pain is around $75,000, according to Coinglass, which is way above current spot prices, so many will be out of the money on expiry.

Open interest (OI), or the value or number of Bitcoin options contracts yet to expire, remains highest at $60,000 with $1.5 billion and $1.1 billion at $50,000 strike prices on Deribit as bearish bets increase. Total BTC options OI across all exchanges has been climbing this month and has reached $37 billion.

“In a continuous downtrend in the existing range, it’s not a surprise to see ongoing downside plays (protection and bearish) on BTC,” said Deribit this week.

“Call OI dominates across both assets, with BTC carrying the significantly larger notional weight into settlement.”

🚨 Options Expiry Alert 🚨

At 08:00 UTC tomorrow, over $8.8B in crypto options are set to expire on Deribit.$BTC: ~$7.8B notional | Put/Call: 0.76 | Max Pain: $75K $ETH: ~$961M notional | Put/Call: 0.77 | Max Pain: $2,200Call OI dominates across both assets, with BTC carrying… pic.twitter.com/5r8MjeQtJ9

— Deribit (@DeribitOfficial) February 26, 2026

Derivatives provider Greeks Live said the expiration of options accounts for 20% of total open interest, totaling nearly $9 billion, with Bitcoin’s position share reaching a multi-year peak.

“The market remains firmly in bear territory. Currently, the crypto space lacks both fresh capital inflows and clear catalysts, with pessimistic narratives dominating social media. The market bottom likely remains elusive.”

In addition to today’s oversized batch of Bitcoin options, around 477,000 Ethereum contracts are also expiring, with a notional value of $963 million, max pain at $2,200, and a put/call ratio of 0.77. Total ETH options OI across all exchanges is around $6.6 billion. This brings the total notional value of crypto options expiries to around $9 billion.

You may also like:

Spot Market Outlook

Markets are back in the red again today with total cap dropping 1.3% below $2.4 trillion. Bitcoin failed to hold above $68,000 and dipped back below $67,000 during early trading in Asia on Friday morning.

Ethereum is teetering around the $2,000 level and is likely to fall below it again as any hopes of a relief rally dwindle.

Binance Free $600 (CryptoPotato Exclusive): Use this link to register a new account and receive $600 exclusive welcome offer on Binance (full details).

LIMITED OFFER for CryptoPotato readers at Bybit: Use this link to register and open a $500 FREE position on any coin!

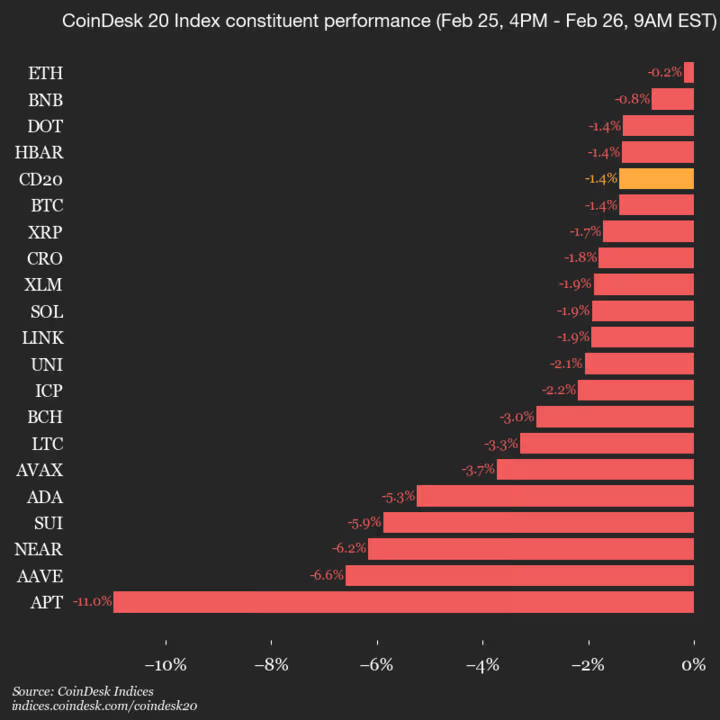

CoinDesk Indices presents its daily market update, highlighting the performance of leaders and laggards in the CoinDesk 20 Index.

The CoinDesk 20 is currently trading at 1999.16, down 1.4% (-28.56) since 4 p.m. ET on Wednesday.

None of the 20 assets are trading higher.

Leaders: ETH (-0.2%) and BNB (-0.8%).

Laggards: APT (-11.0%) and AAVE (-6.6%).

The CoinDesk 20 is a broad-based index traded on multiple platforms in several regions globally.

Crypto World

Why a Solana infrastructure firm is moving its servers to win the global crypto trading war

DoubleZero, a crypto infrastructure startup co-founded by former Solana Foundation executive Austin Federa, is rolling out a major update aimed at spreading Solana’s network more evenly around the world, and making it faster in the process.

On Mar. 9, the company will launch “Phase II” of its DoubleZero Delegation Program, redirecting 2.4 million SOL from its 13 million pool to validators operating in underrepresented regions such as São Paulo, Singapore, Hong Kong, and Tokyo. Each region will receive up to 600,000 SOL in additional delegated stake incentives.

DoubleZero runs a dedicated high-speed internet network that helps Solana’s computers talk to each other faster and more reliably. In 2025, the company behind the network raised $28 million at a $400 million valuation.

DoubleZero’s goal in rolling out the incentive is simple: reduce Solana’s growing geographic concentration in Europe and introduce “multicast functionality,” a data distribution method widely used in traditional finance.

Geographic cluster

One of the main goals of Federa is to reduce the geographic concentration of validators.

“One of the unintended consequences of blockchains getting faster is there’s more incentive to co-locate next to one another,” Federa said in an interview. He compared it to early high-frequency trading wars on Wall Street, when firms scrambled to place servers physically closer to the New York Stock Exchange to shave milliseconds off trades.

Read more: ‘Crypto’s Flash Boys’: A Q&A With Austin Federa on DoubleZero

Today, much of Solana’s staked tokens, which secure the network, sit in Central Europe — largely for historical and economic reasons. “There were a lot of really good, really cheap bare-metal data centers in Europe,” Federa said. “Solana was optimized for that kind of hosting early on, and the infrastructure just built up there.”

But geographic clustering creates trade-offs: If most validators are in Europe, users farther away may be at a disadvantage.

“If I’m sitting in South America trying to execute a trade on Solana, I can hit send first,” Federa said. “But someone who’s got a computer in Germany might actually win that trade.”

To address that imbalance, DoubleZero is offering 2.4 million SOL and aims to make it economically viable for validators to operate outside traditional hubs.

‘More dependable’

The next problem DoubleZero is trying to solve through the new initiative is data transmission latency.

The main barrier to expanding into those areas isn’t technical, Federa said — it’s economic. “Because you’re further away, everything takes longer to get there. It’s like Amazon Prime — in New York you get it same day. In Montana, it’s four or five days.”

DoubleZero says its private fiber network helps address connectivity issues, while the new delegation incentives aim to offset the economic penalty of being outside traditional hubs.

This is why, alongside the geographic push, DoubleZero is introducing the multicast functionality to Solana.

Federa compared it to watching the Super Bowl via satellite versus streaming. With satellite, “an infinite number of people can be watching that radio wave… and it’s no additional tax.” Streaming, by contrast, requires a separate data stream for each viewer.

Blockchain networks today largely operate like streaming services — sending duplicate data over and over. Multicast, he said, changes that.

“In a pre-multicast world, if I’m sending data to 1,000 nodes, I’m handing out 1,000 copies,” he said. “With multicast, I send one copy, and the network hardware replicates it closer to where it needs to go.”

That reduces bandwidth costs, improves fairness in how quickly participants receive data, and creates more room for future upgrades. It also makes blockchain infrastructure behave more like traditional exchanges, which rely heavily on multicast.

“Traditional finance isn’t just faster than blockchain — it’s more dependable,” Federa said. “If we can bring more determinism to blockchain networking, it makes it a much more attractive place for market makers and traders.”

Ultimately, DoubleZero is betting that financial incentives like this will help Solana’s infrastructure spread globally, moving it closer to functioning like a truly real-time market.

Read more: DoubleZero Mainnet Goes Live With 22% of Staked SOL on Board

TLDR

- Nvidia stock fell as much as 5% in early trading on February 26 despite strong fourth quarter results.

- The company reported fiscal Q4 revenue of $68.1 billion, marking a 73% increase year over year.

- Data Center revenue reached $62.3 billion, driven by continued demand for advanced chips.

- Non-GAAP earnings per share rose to $1.62, reflecting an 82% annual increase.

- Gaming and Automotive revenue came in below analyst expectations during the quarter.

Nvidia (NVDA) shares fell in early trading on February 26 despite strong quarterly results. The stock dropped as much as 5% after the company released its fiscal fourth quarter earnings. Traders shifted focus from headline growth to demand durability and capital spending trends.

Nvidia Stock Drops After Earnings Beat

Nvidia stock declined in early market activity even after the company beat revenue and profit estimates. The pullback followed a rally that had priced in strong data center demand. As a result, the earnings report failed to drive further upside momentum.

The company reported total revenue of $68.1 billion for fiscal Q4 2026, rising 73% year over year. Data Center revenue reached $62.3 billion, climbing 75% from the prior year. Non-GAAP earnings per share increased to $1.62, reflecting 82% annual growth.

However, Gaming revenue reached $3.73 billion and fell short of analyst expectations. Automotive revenue totaled $604 million and also missed consensus estimates. Consequently, investors questioned revenue concentration within the data center segment.

Management issued revenue guidance of $78.0 billion, plus or minus 2%, for fiscal Q1 2027. Wall Street had expected about $72.6 billion for the same period. Therefore, the outlook exceeded projections despite the stock decline.

CEO Jensen Huang said, “Demand for Blackwell remains strong across hyperscale customers.” He also confirmed that the company has started shipping samples of the Rubin platform. These updates reinforced continued product development and deployment.

Investors Focus on AI Spending Sustainability

Investors reacted with a sell-the-news move after recent gains in Nvidia stock. In recent weeks, Meta and Amazon signaled higher capital expenditure plans. Those updates had already supported expectations for strong chip demand.

As a result, the earnings beat did not materially alter the broader outlook. Traders shifted attention toward long-term returns on infrastructure investments. They questioned whether enterprise monetization would match hardware spending levels.

The data center division accounted for most of the company’s revenue growth. That concentration raised questions about balance across segments. Gaming and automotive performance failed to match the strength of data center sales.

Gross margin expanded to 75.2%, improving by 1.7% points year over year. The margin gain reflected pricing strength and product mix. However, supply constraints in memory components continued to affect certain segments.

Pixel 10a Delivers Everything You Need and Nothing You Don’t, Complete with a $100 Amazon Gift Card

Pakistan’s defense minister says that there is an ‘open war’ with Afghanistan

Top 2 Overweight-rated European Oil & Gas Stocks, according to JPMorgan

-

Politics5 days ago

Politics5 days agoBaftas 2026: Awards Nominations, Presenters And Performers

-

Fashion7 days ago

Fashion7 days agoWeekend Open Thread: Boden – Corporette.com

-

Sports4 days ago

Sports4 days agoWomen’s college basketball rankings: Iowa reenters top 10, Auriemma makes history

-

Politics4 days ago

Politics4 days agoNick Reiner Enters Plea In Deaths Of Parents Rob And Michele

-

Business2 days ago

Business2 days agoTrue Citrus debuts functional drink mix collection

-

Politics7 hours ago

Politics7 hours agoITV enters Gaza with IDF amid ongoing genocide

-

Crypto World3 days ago

Crypto World3 days agoXRP price enters “dead zone” as Binance leverage hits lows

-

Business5 days ago

Business5 days agoMattel’s American Girl brand turns 40, dolls enter a new era

-

Business5 days ago

Business5 days agoLaw enforcement kills armed man seeking to enter Trump’s Mar-a-Lago resort, officials say

-

Tech3 days ago

Tech3 days agoUnsurprisingly, Apple's board gets what it wants in 2026 shareholder meeting

-

NewsBeat1 day ago

NewsBeat1 day agoCuba says its forces have killed four on US-registered speedboat | World News

-

NewsBeat1 day ago

NewsBeat1 day agoManchester Central Mosque issues statement as it imposes new measures ‘with immediate effect’ after armed men enter

-

NewsBeat4 days ago

NewsBeat4 days ago‘Hourly’ method from gastroenterologist ‘helps reduce air travel bloating’

-

Tech5 days ago

Tech5 days agoAnthropic-Backed Group Enters NY-12 AI PAC Fight

-

NewsBeat5 days ago

NewsBeat5 days agoArmed man killed after entering secure perimeter of Mar-a-Lago, Secret Service says

-

Politics5 days ago

Politics5 days agoMaine has a long track record of electing moderates. Enter Graham Platner.

-

NewsBeat2 days ago

NewsBeat2 days agoPolice latest as search for missing woman enters day nine

-

Business1 day ago

Business1 day agoDiscord Pushes Implementation of Global Age Checks to Second Half of 2026

-

Crypto World2 days ago

Crypto World2 days agoEntering new markets without increasing payment costs

-

Business10 hours ago

Business10 hours agoOnly 4% of women globally reside in countries that offer almost complete legal equality