Crypto World

VOdds Introduces Advanced Odds Checker Tool to Help Bettors Find the Best Odds

[PRESS RELEASE – Willemstad, Curaçao, February 27th, 2026]

Bookmaker & casino broker VOdds unveiled a new feature, Odds Scanner, a betting intelligence tool designed to compare bookmaker prices across multiple sports markets. The platform puts all the odds data in one place, so users don’t have to search for it manually, and so prices are easier to see. VOdds covers a wide range of sports, including football and other popular sports, and supports major events like the Premier League, Champions League, and World Cup. Vodds’ odds checker is an informational tool that focuses on speed, accuracy, and making it easy to compare markets.

Key Features of VOdds Scanner

According to the company, the VOdds scanner is made with precision, making complicated odds data in a simple, easy-to-read way. It is said that users can quickly find the right markets thanks to filters, sorting options, and easy-to-use navigation. In short words, the odds scanner is good for both new and experienced bettors, simply because it’s focused on the user.

Additionally, the VOdds scanner works in a lot of different sports betting markets, from football and basketball to less popular sports and other types of markets. This wide range of coverage lets people look at odds for different leagues, tournaments, and types of bets all in one place. The tool makes sure that data is always available, whether users are following big international events or smaller regional matches.

Odds Comparison

With the odds scanner by VOdds, users can compare prices for the same outcome from different bookmakers all in one place. This lets users find options with higher prices for the same event. For instance, VOdds might show different odds for a Premier League home win and highlight the best one that is available. This structured comparison strengthens the platform’s position as a best odds checker without any bias from advertising.

Real-Time Odds Collection

As a live odds checker, VOdds collects data from multiple bookmakers at the same time and updates prices in real time. This makes sure that people can get up-to-date market information during big events like the Champions League and the World Cup. Real-time updates lower the risk of using old prices and help Vodds users make smart decisions when using the odds checker.

Alerts and Trends

The VOdds platform keeps an eye on changes in odds and market trends. Users can set up alerts for big changes, like when odds drop, which could mean that the market is changing. These tools help users respond quickly and cut down on the need to constantly check the odds scanner by Vodds.

Sports Coverage

Undoubtedly, VOdds has a lot of sports markets, so bettors can see the odds for all the big global competitions in one place. The odds checker on the platform is set up so that the data is always shown in the same way for all sports. This makes it easy to move between markets without losing clarity or accuracy.

Football Odds Checker

VOdds’s football odds checker covers a lot of football, including both domestic leagues and international tournaments. Users can bet on the Premier League, Champions League, and World Cup, among other competitions, using the same odds checker framework. These markets include 1X2, handicaps, and totals.

Tennis Odds Checker

VOdds’s tennis odds checker covers the ATP and WTA tours, Grand Slams, and Challenger events. Vodds’ odds scanner lets users compare match winners, set handicaps, and game totals, and it sends updates in real time.

Basketball Odds Checker

VOdds also lets users bet on basketball games, like the NBA and EuroLeague. The odds checker app shows bet types like moneylines, spreads, and totals in a standard way, which makes it easier to compare them.

How to Start Using the Best Odds Checker by VOdds

Users first sign up for the VOdds platform and then use the odds checker by Vodds from the dashboard. Users can choose which events to see by sport, competition, and market type using filters. This process makes it easy for Vodds to get to the odds scanner.

“We wanted to make a tool that gives bettors clear access to real-time market data without making things too complicated,” Zak Richardson, VOdds spokesperson. The platform makes it easier for users to find good deals on major sporting events by bringing together all the prices from different bookmakers and updating them right away.

Benefits of Using Odds Scanner by VOdds

VOdds points out some important functional benefits, such as:

- Finding the Best Odds: Centralised comparison makes it easier to see the best prices for events like Champions League matches because users don’t have to check multiple bookmakers by hand.

- Making Strategies Work Better: Real-time updates help users quickly react to changes in the market and find arbitrage opportunities with Vodds’ odds scanner.

- Supporting Bigger Bets: Users can better judge markets before placing bigger bets when they can see liquidity and price stability.

How to Use the VOdds Odds Checker

According to VOdds, the main purpose of the VOdds Odds Checker is to compare bookmaker odds in real time so players always place bets at the most profitable price.

For example, users want to bet on Manchester City to win:

- Bookmaker A: 1.72

- Bookmaker B: 1.80

- Bookmaker C: 1.75

VOdds instantly highlights 1.80 as the best available price.

About VOdds

VOdds is a crypto gambling site where people can place bets with cryptocurrency and use a set of data-driven betting tools. VOdds wants to make sports betting more open, efficient, and available to people all over the world by combining digital asset payments with advanced analytics. By collecting and displaying bookmaker data in a clear, easy-to-use way, the platform helps bettors compare prices across different markets, which helps open up the market. VOdds helps users find value opportunities, compare odds in real time, and make better betting decisions while fully participating in the crypto betting ecosystem. It does this with its own odds checker tools.

For more information about the company, users can visit VOdds website or reach out to their contact info below.

Binance Free $600 (CryptoPotato Exclusive): Use this link to register a new account and receive $600 exclusive welcome offer on Binance (full details).

LIMITED OFFER for CryptoPotato readers at Bybit: Use this link to register and open a $500 FREE position on any coin!

ZachXBT just uncovered what looks like a coordinated insider trading ring at Axiom crypto. According to his findings, senior employees used internal data tools to front-run user trades for more than 10 months, allegedly pocketing over $400,000 in the process. The method involved privileged back-end access that allowed staff to track and mirror high-value wallets before the broader market reacted.

This points to deeper governance failures at a platform generating roughly $390 million in annual revenue. Non-technical staff reportedly had unrestricted access to live user identifiers, exposing a serious breakdown in internal controls.

Key Takeaways

- The Actor: Senior business development staff with unrestricted admin access to live user databases.

- The Method: Cross-referencing internal UIDs with on-chain data to identify and front-run KOL wallets.

- The Failure: A YC-backed unicorn generating $390M revenue operating with zero role-based access controls.

How the Insider Trading Scheme Operated Inside Axiom Crypto

The scheme was simple and effective. Investigators say employees used internal admin dashboards meant for support and compliance to pull private user data. By linking User IDs to on-chain wallets, they could identify high-profile traders and institutions behind supposedly anonymous addresses.

From there, the play was straightforward. Monitor activity, then trade ahead of it. Buy before a large wallet pushed price. Sell before a whale exits. It was front-running their own users.

The activity reportedly lasted at least 10 months. The troubling part is that business development staff had the same level of system access as technical security teams. That breakdown in internal controls created the information asymmetry that made the scheme possible.

Discover: The best crypto to diversify your portfolio with

$390M Revenue vs. Zero Access Controls: What Is Axiom Team Response?

Axiom generated $390 million in revenue and scaled rapidly, but the investigation shows its internal controls lagged far behind its growth.

The platform reportedly lacked basic role-based access controls. Business development staff had broad visibility into user identifiers and trading data, creating a “God mode” environment. Proper least-privilege systems and audit logs likely would have flagged the activity early. Instead, it allegedly went unnoticed for nearly a year.

The case highlights a common startup flaw: growth and volume are prioritized, while governance is deferred. That works at a small scale. At billions in volume, it becomes a liability.

Axiom has confirmed a full internal audit. But the reputational damage is significant, and regulators may view the alleged $400,000 in insider profits as potential fraud.

Discover: The best new crypto in the world

The post Axiom Crypto Exposed: ZachXBT Alleges $400k Insider Trading appeared first on Cryptonews.

Pantera Capital and Franklin Templeton’s digital assets units have joined the first cohort of Arena, a new testing environment from open-source AI lab Sentient that is designed to evaluate how AI agents perform in enterprise-style workflows.

In a Friday announcement shared with Cointelegraph, Sentient positioned Arena as a production-style benchmarking platform rather than a static model test. Instead of scoring agents on fixed datasets alone, it runs them through standardized tasks modeled on enterprise conditions, including long documents, incomplete information and conflicting sources.

“In this initial phase, participation refers to supporting the Arena program and developer cohort,” Oleg Golev, product lead at Sentient Labs, told Cointelegraph.

He said partners are helping shape what “production-ready reasoning” looks like for document-heavy tasks such as analysis, compliance and operations. The companies are not announcing capital commitments tied to the initiative.

Related: Jack Dorsey’s Block to cut 4,000 jobs in AI-driven restructuring

The launch comes as enterprises accelerate the deployment of AI agents into research and operational workflows, even as governance frameworks lag.

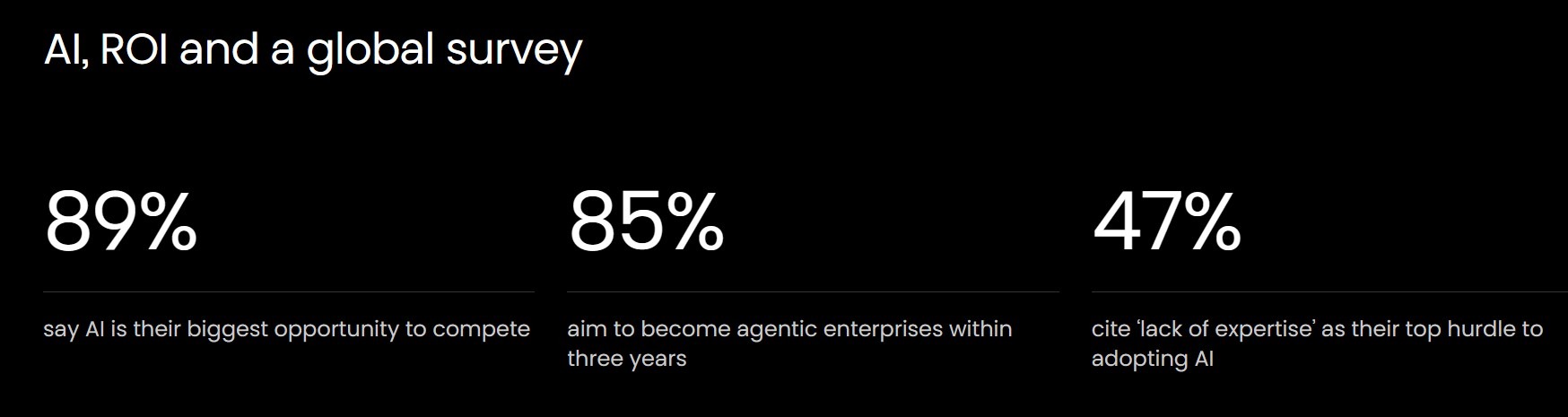

According to the Celonis 2026 Process Optimization Report, published Feb. 4, 85% of surveyed senior business leaders aim to become “agentic enterprises” within three years, while only 19% currently use multi-agent systems.

Production-style evaluation, not static scoring

Golev described Arena as a shared platform where developers submit AI agents to standardized tasks and compare results under consistent testing conditions.

The platform tracks failure categories such as hallucination, missing evidence, incorrect citations and reasoning gaps, allowing developers to diagnose recurring issues.

Arena plans to publish comparative performance metrics through a public leaderboard and release postmortems summarizing common failure modes and fixes.

Infrastructure partners, including OpenRouter and Fireworks, are supplying inference compute for the initial cohort, while other partners support tooling and workshops.

Related: High-yield bond surge signals rising risk, demand in BTC mining, AI infrastructure

Governance layer amid rising AI autonomy

The initiative emerges as financial and crypto companies experiment with giving AI systems greater economic autonomy.

On Wednesday, MoonPay launched infrastructure enabling AI agents to create wallets and execute stablecoin transactions.

On Thursday, Stripe executives warned that blockchains may need significant scaling improvements if AI-driven commerce expands.

Magazine: AI won’t make you rich but crypto games might, Axie founder steps down: Web3 Gamer

The United Kingdom’s Gambling Commission is exploring how cryptocurrency could be used for payments at licensed online casinos, as the country prepares to bring more crypto activity under a new regulatory regime led by the Financial Conduct Authority (FCA).

Tim Miller, the commission’s executive director for research and policy, said Thursday that the regulator wants to examine “the potential path forward” for allowing “cryptoasset to be used as a consumer payment option for licensed and regulated gambling in Great Britain.” Miller made the remarks at the Betting and Gaming Council’s annual general meeting in London, according to his published speech.

Companies carrying out regulated crypto activities will require authorization by the FCA under the Financial Services and Markets Act 2000 (FSMA) when the new regime commences, Miller said.

“And that, as well as the growing appetite we see from punters, means we do now want to start looking at what the potential path forward would be to create a way for cryptoasset to be used as a consumer payment option for licensed and regulated gambling in Great Britain.”

Commission asks industry group to map options

Miller said he requested that the Industry Forum, an advisory group representing gambling sector workers, explore the best path towards accepting cryptocurrency payments, without setting a deadline.

Miller said that accepting crypto payments may help protect British gamblers from illegal websites.

“Our illegal markets research also gives us evidence that crypto is one of the two biggest searches that lead British gamblers to illegal sites,” said Miller, adding that this may be an important consumer protection measure.

However, Miller highlighted that allowing crypto payments does not mean that casinos will be regulated by UK lawmakers, as they would struggle to pass customer suitability checks.

Related: UK Lords launch stablecoin inquiry as Bank of England moves to finalize rules

FCA sets 2027 deadline for new crypto framework implementation

The comments follow recent regulatory developments from the FCA, which has released a final consultation setting out 10 proposals covering crypto markets. The regulator is expected to conclude that process in March, with full implementation targeted for October 2027.

At the beginning of January, the FCA set a timeline for its new crypto licensing regime, requiring companies to seek full authorization before the regime goes live on Oct. 25, 2027, Cointelegraph reported.

“We expect the application period will open in September 2026,” the FCA said in a document published on Jan. 8.

Crypto asset service providers (CASPs) that miss this application window will fall under transitional rules, which allow existing products but restrict new offerings.

Magazine: How crypto laws changed in 2025 — and how they’ll change in 2026

Despite rising whale counts, total Bitcoin supply held by stakeholders has not significantly increased yet.

Bitcoin has almost reversed its weekly losses after a recovery near $68,000. At the same time, whale wallet growth now suggests distribution among more large holders.

Santiment reported that the asset is approaching a new milestone, as the number of wallets holding at least 100 BTC is set to surpass 20,000.

100+ BTC Wallets Surge

At current prices, a wallet containing 100 BTC is worth a minimum of $6.78 million. According to the firm, these wallets are typically owned by high-net-worth individuals, investment funds, long-term holders, or institutions. Santiment also noted that when the number of such large wallets increases during or after price declines, as is currently the case, it can be interpreted as a bullish signal.

However, the blockchain analytics firm also pointed out that the overall percentage of Bitcoin’s total supply held by key stakeholders has not significantly increased so far, which it said helps explain why prices have remained suppressed. This means that the rise in 100+ BTC wallets indicates distribution across a broader group of large holders, rather than a small cluster maintaining tight control.

Such a trend reflects less extreme consolidation at the top tier of holders. At the same time, Santiment stressed that wealth continues to concentrate in stronger hands relative to smaller retail wallets, meaning the trend does not point to decentralization at the smallest ownership level.

In previous instances, increases in whale wallet counts have often occurred during accumulation phases that later supported price recoveries. Santiment added that for a stronger impact, the growth in large wallet numbers needs to be in line with growth in overall supply held, as retail investors gradually sell their coins to larger holders.

Despite the near-term constructive on-chain signals, concerns of further downside risks remain.

You may also like:

Bears Still in Control?

Market analyst Willy Woo, for one, tilted toward a bearish outlook for Bitcoin. He stated that the bearish sell-off by investors appears to have exhausted, which gives price room to consolidate sideways for about a month or potentially rebound toward the mid-$70,000 range, though he expects such a move would likely be rejected.

Woo explained that the broader market regime remains heavily bearish, with both spot and futures liquidity deteriorating. He added that he has never seen Bitcoin rally sustainably when both liquidity sources are bearish. Based on his assessment, he said Q4 could mark the end of the bearish trend, while bullish momentum may potentially return in Q1 or Q2 of 2027.

The analyst identified $45,000 as a typical bear market bottom. However, if global macro conditions break down, $30,000 would be fallback support, with $16,000 as the final level.

Another prominent market commentator, Doctor Profit, also previously predicted that while the “fastest” BTC crash may be over, the worst is yet to come.

Binance Free $600 (CryptoPotato Exclusive): Use this link to register a new account and receive $600 exclusive welcome offer on Binance (full details).

LIMITED OFFER for CryptoPotato readers at Bybit: Use this link to register and open a $500 FREE position on any coin!

As the chart of the ASX 200 index (Australia 200 on FXOpen) shows, today’s candle has moved above the 9,210 level, marking a fresh all-time high. Since the start of the year, the benchmark of Australian equities has gained more than 5.6%, supported by:

→ A strong earnings season. A significant number of companies not only exceeded analysts’ expectations but also upgraded their profit forecasts for the 2026 financial year.

→ Economic resilience. The unemployment rate remains low despite the Reserve Bank of Australia maintaining a firm policy stance.

→ Elevated prices for gold, uranium and copper, along with signs of a recovery in China’s economy, which have provided support to the mining sector.

Technical Analysis of the ASX 200 Chart (Australia 200 on FXOpen)

Price action continues to unfold within an ascending channel (highlighted in blue) that has been in place since autumn 2025. Within this structure:

→ The median line acted as support on 24 February, signalling underlying strength.

→ The upper boundary has repeatedly served as resistance during 2026.

It is worth noting that:

→ The psychological 9,100 level had previously capped gains within the channel.

→ The index has now climbed above 9,200 near the upper boundary of the blue channel.

→ The RSI indicator is approaching overbought territory.

Given these factors, it is reasonable to assume that some long-position holders may look to take profits, potentially leading to a pause in bullish momentum. As a result, the following scenario cannot be ruled out:

→ Failure to secure a sustained move above 9,200;

→ The development of a corrective pullback in the ASX 200 (Australia 200 on FXOpen).

In such a case, support may emerge near the lower orange trend line, which reflects the upward trajectory seen during the second half of the month.

Trade global index CFDs with zero commission and tight spreads (additional fees may apply). Open your FXOpen account now or learn more about trading index CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Mutuum Finance, a decentralized lending and borrowing cryptocurrency protocol currently operating on the Sepolia testnet, has reported surpassing $150 million in testnet total value locked (TVL). The team also announced ongoing development activity, including a new feature scheduled for release next week.

Mutuum Finance (MUTM)

The MUTM token is currently priced at $0.04. Out of a capped total supply of 4 billion tokens, approximately 1.82 billion were allocated to the sale phase. According to project disclosures, around 850 million tokens have been sold to more than 19,000 holders, with total funds raised exceeding $20.6 million to date.

The team recently implemented a new feature, announcing on X the launch of Safe-Mode Borrow Presets. Borrowing within the testnet V1 protocol is now structured as a one-click process with predefined risk presets that target specific Stability Factor levels: Safe, Balanced and Aggressive. With the addition of these presets, users can select a predefined risk profile when opening a borrowing position in the test environment.

For example, if a user deposits $1,000 worth of ETH as collateral, and the maximum loan-to-value (LTV) ratio is 75%, the user could borrow up to $750 in stablecoins. Under the Safe preset, the system maintains a higher collateral buffer by targeting a stronger Stability Factor, meaning the user borrows below the maximum LTV. This reduces liquidation risk in the event of price volatility. The Balanced and Aggressive presets allow borrowing closer to the maximum LTV, increasing capital efficiency while proportionally increasing exposure to market risk.

Lending and Borrowing Benefits Within the Protocol

Many investors could ask why they should put more collateral to borrow crypto assets. The reason is that instead of selling their current holdings, for example Ethereum, a user can deposit it as collateral without selling it and borrow USDT for other expenses while still maintaining exposure to Ethereum and potentially benefiting from its price increase. In other words, while using the borrowed funds, the Ethereum position remains intact and continues to participate in market movements.

Another factor that will benefit users is lending within the protocol. When users supply assets to Mutuum Finance, those assets are deposited into a liquidity pool and made available to borrowers. In return, the protocol issues mtTokens on a 1:1 basis as proof of deposit. These mtTokens represent the user’s share of the pool and accrue yield over time based on borrowing demand and pool utilization.

For example, if a user supplies $10,000 worth of USDT to the protocol and the average annual percentage yield (APY) is around 5–6%, the position could generate approximately $500 to $600 in yield over a one-year period, depending on utilization levels. The yield is reflected in the increasing value of the mtTokens, allowing users to earn passive income while their assets remain in the liquidity pool.

mtTokens can also be staked within the protocol, allowing users to receive dividends in MUTM tokens. According to the project’s model, a portion of the fees generated by protocol activity is used to purchase MUTM tokens from the open market and distribute them to eligible stakers, linking platform usage to token-based incentives over time.

Mutuum Finance’s recent testnet milestone and feature updates reflect ongoing development ahead of mainnet deployment. The project reports more than $20.6 million raised and over $150 million in testnet total value locked (TVL), alongside continued codebase improvements.

Stablecoin-based payroll infrastructure is entering a regulated growth phase across the United Kingdom and the European Union. The UK and EU represent one of the largest fintech and cross-border employment markets globally. As regulatory clarity around digital assets improves under the Financial Conduct Authority (FCA) and the Markets in Crypto-Assets (MiCA) regulation, enterprises are accelerating efforts to modernize payroll infrastructure using stablecoins.

For fintech startups, payroll SaaS providers, cross-border payment companies, and embedded finance platforms, this presents a strategic opportunity. Launching a compliant and scalable stablecoin payment platform built specifically for regulated workforce payouts is a major competitive advantage. This guide explains the requirements to design, build, and deploy a stablecoin salary payout infrastructure that meets UK and EU regulatory expectations while remaining commercially viable and technically scalable.

Why Stablecoin Salary Payouts Are Growing in the UK and EU

A stablecoin salary payout platform allows employers to distribute wages using regulated digital currencies such as USD Coin (USDC) or Tether (USDT). These digital assets maintain price stability relative to fiat currencies while enabling programmable and near real-time settlement.

Unlike simple crypto transfers, enterprise payroll systems must include:

- Employer onboarding and identity verification

- Employee wallet provisioning

- Automated recurring payment execution

- Fiat conversion capabilities in GBP and EUR

- Audit logs and compliance reporting

- Risk monitoring and transaction analytics

From the Trenches Insight: Industry experience shows that reconciling fast stablecoin settlement with strict GDPR data privacy standards is often the primary hurdle for modern payout gateways. When structured properly, the system functions as a fully compliant payment gateway seamlessly integrated with traditional HR software and financial institutions.

Core Architecture of a Stablecoin Salary Payout Platform

Building a stablecoin payroll system requires a multi-layered infrastructure designed for resilience and scale.

- Blockchain Settlement Layer: Select a blockchain network that balances scalability, cost efficiency, and ecosystem maturity. Smart contracts must support scheduled payments, multi-recipient distribution, and programmable treasury logic.

- Wallet and Custody Layer: Institutional clients often prefer custodial or hybrid custody models with hardware-backed key management and multi-signature controls.

- Fiat On and Off Ramp Layer: Integration with regulated banks or Electronic Money Institutions (EMIs) ensures smooth conversion between stablecoins and GBP or EUR.

- Compliance and Risk Engine: Embed identity verification APIs, AML monitoring tools, transaction analytics, and automated reporting modules.

- Integration Layer: API-first architecture ensures seamless connectivity with HRMS, ERP systems, and payroll software providers.

Talk to a specialist at Antier today to scope the technical requirements.

Once deployed, the infrastructure can evolve into a comprehensive stablecoin remittance platform supporting vendor payouts, contractor settlements, and treasury transfers beyond salary use cases.

Regulatory Considerations in the UK and EU

Compliance is the foundation of any stablecoin payroll solution in these regions. Regulatory readiness is often the deciding factor for enterprise adoption. Failure to design compliance into the architecture from day one can delay licensing approvals and restrict institutional partnerships.

UK vs. EU Regulatory Landscape for Stablecoins:

| Feature | UK (FCA) | EU (MiCA) |

|---|---|---|

| Regulatory Body | Financial Conduct Authority (FCA) | European Securities and Markets Authority (ESMA) |

| Primary Framework | E-Money Regulations & Cryptoasset Registration | Markets in Crypto-Assets (MiCA) |

| Stablecoin Rules | Strict focus on fiat-backed stablecoins | Authorization required for E-Money Tokens (EMTs) and Asset-Referenced Tokens (ARTs) |

| AML & KYC | Money Laundering Regulations (MLRs) | AMLD6 and strict Travel Rule compliance |

Businesses must align with anti-money laundering standards, Know Your Customer (KYC) requirements, Travel Rule data-sharing obligations, and GDPR data privacy regulations. A compliant gateway should include automated onboarding workflows, sanctions screening, risk classification systems, and real-time monitoring dashboards.

Essential Features for Enterprise Adoption

Enterprise clients expect more than just basic blockchain settlement. To compete effectively, a solution should include:

- Multi-stablecoin compatibility: Support for major fiat-pegged assets like USDC, EURC, and USDT.

- Automated payroll scheduling: Smart contract triggers for bi-weekly or monthly disbursements.

- Bulk payout execution: Batch processing to minimize gas fees and streamline employer operations.

- Treasury management dashboard: Real-time visibility into asset reserves and liquidity.

- FX visibility tools: Transparent conversion rates between crypto and fiat.

- Compliance export modules: One-click report generation for internal audits and tax authorities.

- Role-based administrative controls: Multi-tier access for HR, finance, and executive teams.

- Scalable API endpoints: Easy integration for white-label partners.

Providing full-stack stablecoin remittance platform development enables fintech startups and payroll companies to deploy branded solutions without building the infrastructure internally.

Access the 2026 MiCA & FCA Enterprise Checklist

Monetization Model for Stablecoin Payroll Platforms

A profitable stablecoin payroll solution in the UK and EU should combine recurring revenue with transaction-based income and enterprise services.

- Transaction Fees: Charge per salary payout, bulk disbursement, or contractor transfer. A well-structured system automates fee calculation and provides transparent reporting.

- Subscription Plans: Offer tiered SaaS pricing based on active employees, transaction volume, API access, and compliance features.

- White Label Licensing: Allow payroll SaaS providers and fintech firms to deploy under their own brand. Licensing and setup fees create long-term recurring contracts.

- FX and Conversion Margins: Earn revenue from GBP and EUR conversions. Efficient settlement through secure payment rails ensures competitive spreads.

- API and Compliance Modules: Premium features such as advanced AML tools and reporting dashboards can expand the platform into a scalable cross-border remittance tool, even revenue and recurring platform income in a rapidly growing digital payroll market.

Frequently Asked Questions

- Is paying salaries in stablecoins legal in the UK and EU?

Yes, paying salaries in stablecoins is legal in both regions, provided the employer and the payment platform comply with local tax laws, employment contracts, and financial regulations (such as FCA guidelines in the UK and MiCA in the EU). Both parties must mutually agree to the payment method in writing.

- What are the tax implications of a stablecoin salary?

In the UK and EU, stablecoin salaries are subject to standard income tax and social security contributions. The fiat value of the stablecoin at the exact time of the payout is used to calculate the tax liability. Employees may also be subject to capital gains tax if the stablecoin fluctuates in value before it is sold or converted to fiat.

- How do stablecoin payroll platforms handle fiat off-ramping?

Enterprise payroll platforms partner with regulated Electronic Money Institutions (EMIs) or crypto-friendly banks. This integration allows employees to receive stablecoins into a designated wallet and immediately convert them into GBP or EUR, which is then routed directly to a traditional bank account via SEPA or Faster Payments.

Moving Forward

If evaluating blockchain salary infrastructure as a fintech founder, payroll technology provider, or enterprise, this is a strategic inflection point. The UK and EU are moving toward regulated digital asset integration. Companies that establish compliant and scalable payroll infrastructure today will lead tomorrow’s cross-border workforce economy.

Antier helps businesses design and deploy enterprise-ready solutions tailored for these markets. Whether launching a stablecoin payment platform, integrating a compliant payment system, or optimizing settlement through secure stablecoin payment rails, the development delivered is strictly aligned with regulatory and enterprise standards. Ready to build a regulation-ready stablecoin payroll platform? Connect with Antier’s experts today and start the deployment journey.

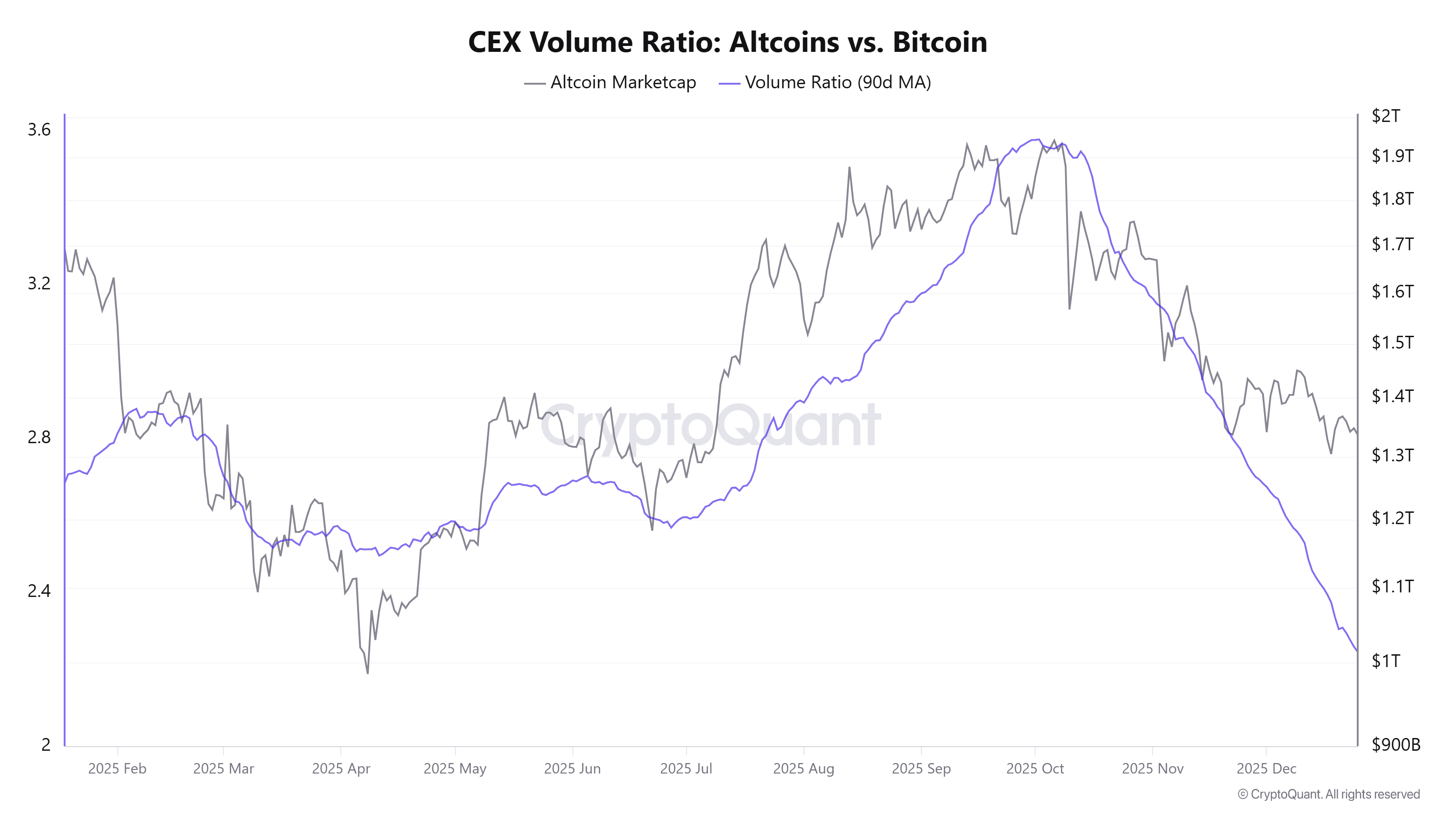

Although the market recovery in February remains fragile, it has revealed several notable signals. These signs have led analysts to expect that an altcoin season could emerge in March.

However, investor sentiment remains cautious, with capital still favoring Bitcoin over altcoins, which could hinder a broader recovery.

Hope Returns to the Altcoin Market in March

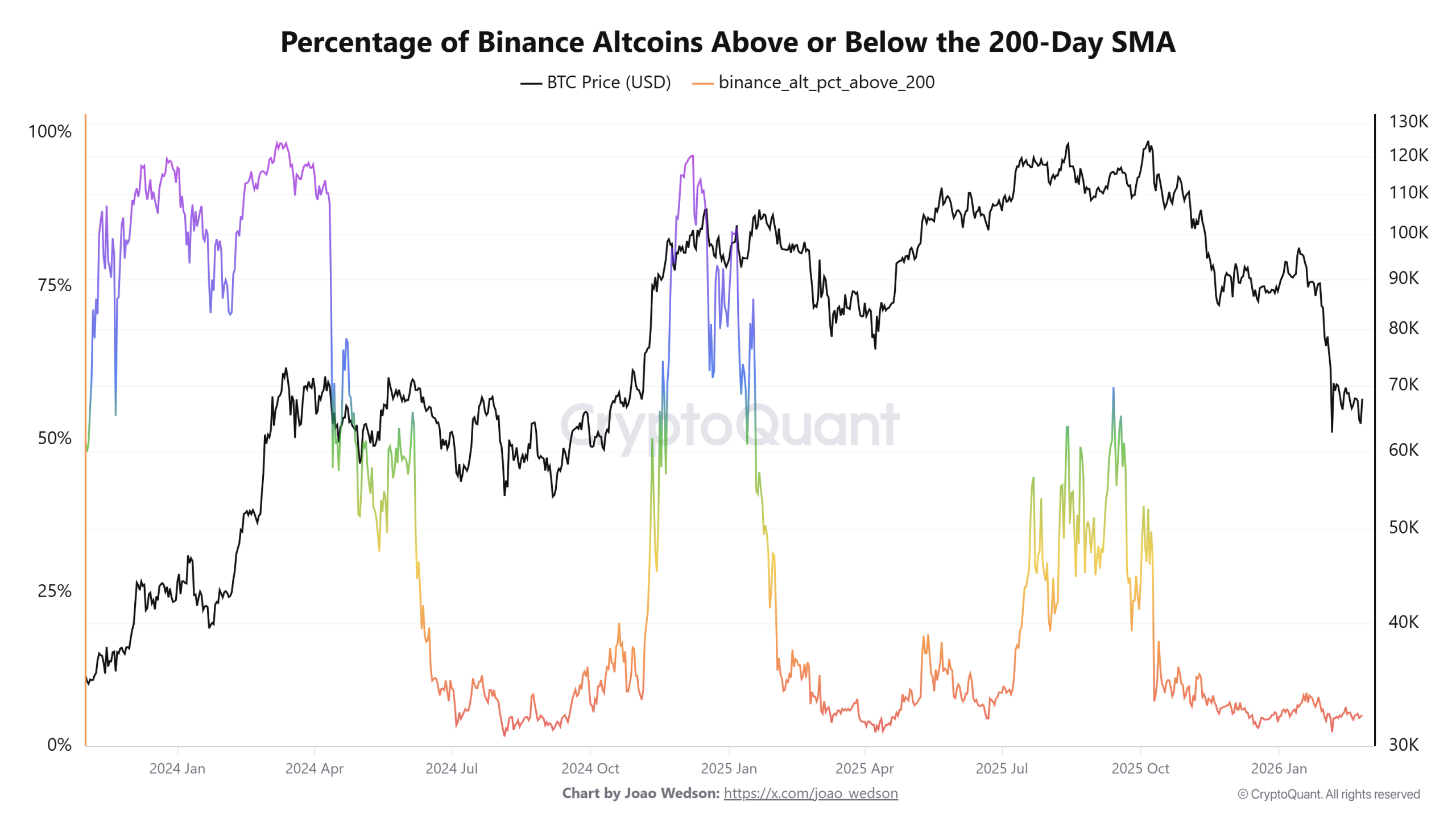

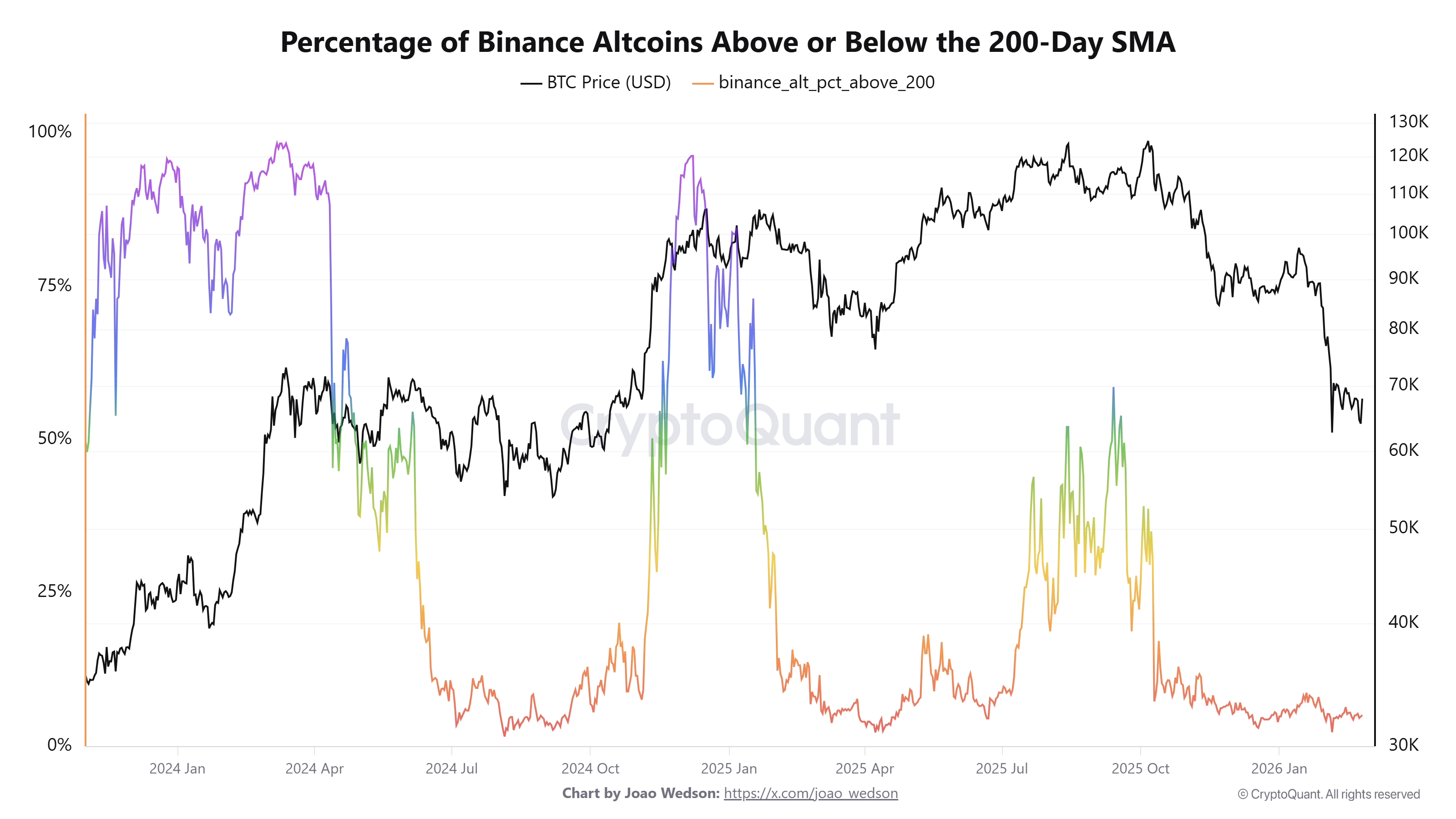

Data from CryptoQuant shows that only about 5% of altcoins listed on Binance are trading above their 200-day simple moving average (200-day SMA). This means that 95% remain below this level, reflecting the current weak performance of altcoins.

However, historical patterns offer a glimmer of hope. Over the past two years, this ratio typically stayed below 15% for a maximum of five months before rebounding. This pattern appeared during the June–October 2024 period and again from February to June 2025.

The ratio began declining in October last year and has now reached the end of its fifth month. This development raises expectations of a potential demand boost, as investors may view most altcoins as having fallen to attractive price levels.

Meanwhile, several analysts have identified early positive signals on the OTHERS/BTC chart in February, which tracks total altcoin market capitalization excluding Bitcoin against BTC.

Analyst Blade noted that the chart shows potential reversal signs on the monthly timeframe. The MACD indicator has crossed above the signal line and formed its first green histogram bar since early 2024. Similar signals appeared before major altcoin rallies in 2017 and 2020.

“Momentum shift plus structure compression usually precede expansion. The biggest altseason is coming,” Blade predicted.

These factors have strengthened expectations that altcoins could post a recovery in March.

Altcoin Investors Remain Cautious

For a more balanced perspective, data from CryptoQuant indicates that the ratio of altcoin trading volume to Bitcoin trading volume on centralized exchanges (CEXs) has fallen to its lowest level in the past year.

In 2025, the ratio peaked at around 3.5. It then gradually declined, falling below 2.5 by late last year and continuing to hover near 2.2 in early 2026.

This trend shows that investor expectations for an altcoin season remain weak. Capital continues to concentrate mainly on Bitcoin, leaving altcoins relatively neglected on centralized exchanges. A true altcoin season may require sustained capital rotation and fresh inflows into the market.

At the time of writing, the Altcoin Season Index stands at 43, still far from the 75-point threshold needed to confirm an altcoin season.

A recent report by BeInCrypto stated that the altcoin market has faced 13 consecutive months of net selling. Even if an altcoin season materializes, it is likely to be selective and driven by strong fundamentals.

Crypto World

The worst may lie ahead. BTC price chart revisits historic pattern: Crypto Daybook Americas

By Omkar Godbole (All times ET unless indicated otherwise)

Uh-oh, the bitcoin price pattern that presaged the final and deepest phases of previous bear markets has appeared again.

In mid-November 2018, CoinDesk discussed a bearish flip in long-term averages on a chart that bundles three days of price action into each candle. It warned that a similar occurrence in 2014 deepened the bear market and, within a week, bitcoin crashed to under $4,500 from $6,000, extending the decline from the peak of roughly $20,000.

Cut to April 2022. The same pattern occurred, with the same result. BTC’s bear market deepened and prices cratered to $17,500 from $32,000, having already dropped from the late 2021 record of nearly $70,000.

Now, the pattern’s back again (check the Technical Analysis section). While past performance is not a guarantee of future results, history calls for caution. Some savvy traders are preparing for a deeper crash below $60,000.

Bitcoin recently traded near $66,100, down 3% in 24 hours. Other major tokens and the CoinDesk 20 Index lost even more. Still, U.S.-listed spot bitcoin ETFs have pulled in over $1 billion in three days.

“That breadth of demand signals absorption rather than speculation,” Iliya Kalchev, an analyst at Nexo Dispatch, said in an email. “On-chain data reinforces the shift: wallets holding more than 10,000 Bitcoin have accumulated through the recent pullback from the $70,000 region, suggesting long-term holders are stepping in as supply thins.”

Even so, ETF flows need to persist to lift BTC sustainably higher, Kalchev said.

In traditional markets, oil prices remain supported by U.S.-Iran uncertainty and the potential for an escalation over the weekend. Stay alert!

Read more: For analysis of today’s activity in altcoins and derivatives, see Crypto Markets Today

What to Watch

For a more comprehensive list of events this week, see CoinDesk’s “Crypto Week Ahead“.

- Crypto

- Macro

- Feb. 27, 8:30 a.m.: U.S. PPI MoM for January est. 0.3% (Prev. 0.5%); Core PPI MoM est. 0.3% (Prev. 0.7%)

- Feb. 27, 8:30 a.m.: U.S. PPI YoY for January est. 2.9% (Prev. 3%)

- Feb. 27, 8:30 a.m.: Canada GDP growth rate annualized for Q4 (Prev. 2.6%); QoQ (Prev. 0.6%)

- Earnings (Estimates based on FactSet data)

Token Events

For a more comprehensive list of events this week, see CoinDesk’s “Crypto Week Ahead“.

- Governance votes & calls

- 1inch DAO is voting to allocate 2,000,000 USDC from its treasury to the Aave V3 market on Ethereum to generate yield. Voting ends March 1.

- Unlocks

- Token Launches

- Feb. 27: Fabric Protocol (ROBO) to be listed on Binance, Bybit, Bitget, KuCoin, and others.

Conferences

For a more comprehensive list of events this week, see CoinDesk’s “Crypto Week Ahead“.

Market Movements

- BTC is unchanged from 4 p.m. ET Thursday at $67,423.09 (24hrs: -0.95%)

- ETH is down 0.89%at $2,012.51 (24hrs: -2%)

- CoinDesk 20 is unchanged at 1,968.26 (24hrs: -2.49%)

- Ether CESR Composite Staking Rate is up 4 bps at 2.89%

- BTC funding rate is at -0.006% (-6.5799% annualized) on Binance

- DXY is unchanged at 97.74

- Gold futures are unchanged at $5,191.50

- Silver futures are up 2.82% at $90.05

- Nikkei 225 closed up 0.16% at 58,850.27

- Hang Seng closed up 0.95% at 26,630.54

- FTSE is up 0.39% at 10,888.78

- Euro Stoxx 50 is unchanged at 6,161.33

- DJIA closed on Thursday up 0.03% at 49,499.20

- S&P 500 closed down 0.54% at 6,908.86

- Nasdaq Composite closed down 1.18% at 22,878.38

- S&P/TSX Composite closed up 1.1% at 34,501.96

- S&P 40 Latin America closed down 1.4% at 3,772.90

- U.S. 10-Year Treasury rate is down 3 bps at 3.987%

- E-mini S&P 500 futures are down 0.28% at 6,900.75

- E-mini Nasdaq-100 futures are down 0.19% at 25,033.75

- E-mini Dow Jones Industrial Average Index futures are down 0.48% at 49,294.00

Bitcoin Stats

- BTC Dominance: 58.49% (-0.11%)

- Ether-bitcoin ratio: 0.02973 (-1.06%)

- Hashrate (seven-day moving average): 1,055 EH/s

- Hashprice (spot): $29.31

- Total fees: 3.43 BTC / $232,808

- CME Futures Open Interest: 107,780 BTC

- BTC priced in gold: 12.8 oz.

- BTC vs gold market cap: 4.46%

Technical Analysis

- The chart shows BTC’s price swings on a three-day time frame in candlestick format from 2024-2025 and 2018-2022. Each candle bundles the price action seen over three days, or 72 hours.

- On this chart, moving averages of 50- and 200-candles have crossed bearish.

- Similar patterns led to deeper slides in 2014, 2018 and 2022.

Crypto Equities

- Coinbase Global (COIN): closed on Thursday at $181.06 (-1.57%), unchanged in pre-market

- Circle Internet (CRCL): closed at $87.21 (+4.90%), unchanged in pre-market

- Galaxy Digital (GLXY): closed at $21.94 (-3.90%)

- Bullish (BLSH): closed at $32.73 (-0.49%), unchanged in pre-market

- MARA Holdings (MARA): closed at $8.45 (-1.40%), +15.98% at $9.80

- Riot Platforms (RIOT): closed at $17.09 (+0.06%), +0.12% at $17.11

- Core Scientific (CORZ): closed at $17.98 (-0.55%), -1.50% at $17.71

- CleanSpark (CLSK): closed at $10.44 (-0.10%), -0.77% at $10.36

- CoinShares Valkyrie Bitcoin Miners ETF (WGMI): closed at $42.17 (-0.40%)

- Exodus Movement (EXOD): closed at $10.45 (-1.69%)

Crypto Treasury Companies

- Strategy (MSTR): closed at $133.40 (-1.66%), +0.62% at $134.23

- Strive (ASST): closed at $8.19 (-4.10%), +0.24% at $8.21

- SharpLink Gaming (SBET): closed at $7.21 (-3.09%), +0.55% at $7.25

- Upexi (UPXI): closed at $0.76 (-7.87%), +0.22% at $0.76

- Lite Strategy (LITS): closed at $1.14 (-3.39%)

ETF Flows

Spot BTC ETFs

- Daily net flows: $254.4 million

- Cumulative net flows: $54.81 billion

- Total BTC holdings ~1.27 million

Spot ETH ETFs

- Daily net flows: $6.6 million

- Cumulative net flows: $11.68 billion

- Total ETH holdings ~5.72 million

Source: Farside Investors

While You Were Sleeping

As the XTI/USD chart shows, the price of a barrel:

→ set fresh 2026 highs above $67 earlier this week;

→ but yesterday posted a sharp reversal lower (as indicated by the blue arrow).

The spike in volatility was driven by conflicting reports from Geneva, where talks between the United States and Iran were taking place:

→ some sources suggested negotiations had reached an impasse, as Washington insists on a complete halt to uranium enrichment;

→ meanwhile, according to Omani mediators, progress has been made and another round of talks is scheduled for next week.

Technical Analysis of the XTI/USD Chart

When analysing the oil price chart on the morning of 19 February, we suggested that:

→ the market could soon set a new high for the year (which materialised, with a series of highs formed between 19 and 23 February);

→ the 65.20 level would act as support (confirmed on 23 February).

Today’s chart indicates growing bearish pressure, reflected in the following:

→ WTI struggled to hold above its yearly highs, forming signs of potential bull traps;

→ yesterday’s candle (marked with a red arrow) shows a pronounced upper wick.

At the same time, bulls clearly defended the former resistance level at $63.73. The lower boundary of the ascending trajectory that has defined WTI price movements in 2026 also supports the bullish case.

It is worth noting that an OPEC+ meeting is scheduled for the weekend. According to media reports, analysts expect an increase in output from April, which could heighten concerns about oversupply — particularly after US crude inventories rose on Wednesday. As a result, Monday’s trading may open with elevated volatility.

Start trading commodity CFDs with tight spreads (additional fees may apply). Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Why aren't Melissa Barrera and Jenna Ortega in “Scream 7”?

Israel’s tourism partners no longer able to hide

Wuthering Waves Edelschnee locations and farming guide

-

Politics5 days ago

Politics5 days agoBaftas 2026: Awards Nominations, Presenters And Performers

-

Fashion7 days ago

Fashion7 days agoWeekend Open Thread: Boden – Corporette.com

-

Sports4 days ago

Sports4 days agoWomen’s college basketball rankings: Iowa reenters top 10, Auriemma makes history

-

Politics4 days ago

Politics4 days agoNick Reiner Enters Plea In Deaths Of Parents Rob And Michele

-

Business3 days ago

Business3 days agoTrue Citrus debuts functional drink mix collection

-

Politics13 hours ago

Politics13 hours agoITV enters Gaza with IDF amid ongoing genocide

-

Crypto World3 days ago

Crypto World3 days agoXRP price enters “dead zone” as Binance leverage hits lows

-

Business5 days ago

Business5 days agoMattel’s American Girl brand turns 40, dolls enter a new era

-

Business5 days ago

Business5 days agoLaw enforcement kills armed man seeking to enter Trump’s Mar-a-Lago resort, officials say

-

Tech3 days ago

Tech3 days agoUnsurprisingly, Apple's board gets what it wants in 2026 shareholder meeting

-

NewsBeat2 days ago

NewsBeat2 days agoManchester Central Mosque issues statement as it imposes new measures ‘with immediate effect’ after armed men enter

-

NewsBeat2 days ago

NewsBeat2 days agoCuba says its forces have killed four on US-registered speedboat | World News

-

NewsBeat4 days ago

NewsBeat4 days ago‘Hourly’ method from gastroenterologist ‘helps reduce air travel bloating’

-

Tech5 days ago

Tech5 days agoAnthropic-Backed Group Enters NY-12 AI PAC Fight

-

NewsBeat5 days ago

NewsBeat5 days agoArmed man killed after entering secure perimeter of Mar-a-Lago, Secret Service says

-

Politics5 days ago

Politics5 days agoMaine has a long track record of electing moderates. Enter Graham Platner.

-

Business1 day ago

Business1 day agoDiscord Pushes Implementation of Global Age Checks to Second Half of 2026

-

NewsBeat3 days ago

NewsBeat3 days agoPolice latest as search for missing woman enters day nine

-

Sports4 days ago

Sports4 days ago2026 NFL mock draft: WRs fly off the board in first round entering combine week

-

Crypto World3 days ago

Crypto World3 days agoEntering new markets without increasing payment costs