Crypto World

Crypto crash resumes as odds of US attacking Iran jumps

The recent crypto crash resumed today, February 27, as investors booked profits and as geopolitical risks in the Middle East escalated.

Summary

- Crypto prices retreated on Friday as odds of the US striking Iran jumped.

- The retreat coincided with the performance in the stock market.

- It also happened as investors booked profits after the recent rebound.

Bitcoin (BTC) price retreated below $66,000, while the market of all tokens retreated by 2.85% in the last 24 hours to over $2.28 trillion. Pippin token dropped by 26% in the last 24 hours, while Kaspa, Zcash, and Lighter retreated by over 6%.

On the other hand, some top tokens like Decred, LayerZero, Arbitrum, and Internet Computer tokens jumped by over 4% in the same period.

Crypto crash resumes as odds of US attacking Iran jumps

The ongoing crypto crash is happening because of the rising geopolitical tensions between the United States and Iran.

In a statement, Ambassador Mike Huckabee told staff at the US embassy in Jerusalem to leave their offices and country, raising the possibility that the US will attack Iran in the coming days. The evacuation order is only for non-essential staff and the embassy will remain open.

This announcement came a few days after the US ordered its non-essential staff in Lebanon to leave the country.

Traders on Polymarket believe that an attack is coming soon. Odds of an attack happening in March rose to 72%, while before March rose to 80%.

A new war in the Middle East will have an impact on Bitcoin and other markets because Iran has warned that it will retaliate by attacking US bases in the Middle East and by closing the Strait of Hormuz.

Such a move will lead to higher inflation, which will make it hard for the Federal Reserve to cut interest rates in the coming meetings. Also, Bitcoin is no longer a safe-haven asset as analysts were expecting.

Profit-taking and stock market crash

The ongoing crypto crash is happening because of the profit-taking among investors.

Bitcoin jumped from $63,000 earlier this week and then moved to $68,000, while other tokens like Pippin, Pepe, and Kaspa soared by double digits. As such, the retreat confirms that the rebound was a dead-cat bounce.

The crypto market crash also coincided with the ongoing stock market dive. For example, the Dow Jones Index retreated by over 500 points, while the S&P 500 and Nasdaq 100 indices fell by over 1%.

The stock market retreat was mostly because of the ongoing concerns about the booming private credit industry, where some companies like Blue Owl and Apollo.

Additionally, the crypto crash also happened after the US published a strong Producer Price Index, which rose by 0.5% in January, higher than market participants were expecting.

Crypto traders should keep an eye on key altcoins showing notable technical setups and potential catalysts. Market-moving events, including token unlocks, breakout patterns, and overbought conditions, could create short-term volatility.

BeInCrypto has analysed three such altcoins that are preparing for a volatile weekend.

Sui (SUI)

SUI faces a token unlock on March 1, when 53.82 million SUI, roughly 0.54% of total supply, will enter circulation. The unlocked tokens are valued at over $50 million. If market demand fails to absorb this supply, short-term price pressure may intensify.

SUI is trading at $0.935, below the $0.977 resistance level. The Squeeze Momentum Indicator signals compression, while the histogram reflects emerging bullish strength. If volatility expands upward and broader crypto sentiment remains positive, SUI could break $0.977 and target $1.060.

Want more token insights like this? Sign up for Editor Harsh Notariya’s Daily Crypto Newsletter here.

However, downside risks persist if investors sell into the unlock event. Failure to absorb new supply may push SUI below the $0.879 support level. A breakdown beneath that threshold could expose the next downside target near $0.778, invalidating the near-term bullish outlook.

Pippin (PIPPIN)

PIPPIN price resumed its upward momentum after a brief consolidation, setting a new all-time high at $0.904 in the past 24 hours. The token now trades at $0.679. Elevated trading activity reflects sustained speculative interest across the broader meme coin segment.

The bullish broadening descending wedge pattern remains intact on the daily chart. Price action continues approaching the projected 221% rally target. A decisive move above $1.000 would strengthen the breakout thesis. The Chaikin Money Flow indicator shows strong inflows, supporting continued upside momentum.

However, downside risk persists if holders shift toward profit-taking. A breakdown below the $0.666 support level would weaken the current structure. In that case, PIPPIN could decline toward $0.514. Losing that threshold may extend losses toward $0.385, invalidating the bullish outlook.

Stable (STABLE)

Another one of the altcoins to watch this weekend is STABLE, which is trading at $0.036 at the time of writing after setting a new all-time high of $0.039 during intraday trading. The Parabolic SAR remains below the candlesticks, confirming that the current uptrend is technically intact across short-term time frames.

Momentum indicators, however, suggest caution. The Money Flow Index has crossed into overbought territory, a level often associated with profit-taking and short-term reversals. If selling pressure emerges, the STABLE price could retrace toward $0.030 or potentially test deeper support near $0.025.

Should bullish momentum persist, a healthy cooldown may follow rather than an immediate decline. Similar consolidation occurred last week before further gains. STABLE could range between $0.039 and $0.030. A breakout above the current ATH may open the path toward $0.048, invalidating bearish expectations.

There is something unusual happening in the XRP price prediction space right now. For the first time in years, almost every major forecaster agrees on the same number. FXEmpire says $5. InvestingHaven says $5. Elliott Wave analysts say $5. Even the AI models cluster around $4 to $5 under base conditions. When every analyst agrees on a ceiling, that ceiling becomes exactly that.

The question smart investors are asking is not whether XRP can reach $5. It is what else they can hold alongside XRP that has not hit its ceiling yet.

Source: Coinmarketcap

FXEmpire breaks the XRP price prediction into three phases. Short term $2.50. Medium term $3.66. Bullish target $5.00, driven by ETF inflows and Ripple’s OCC banking license.

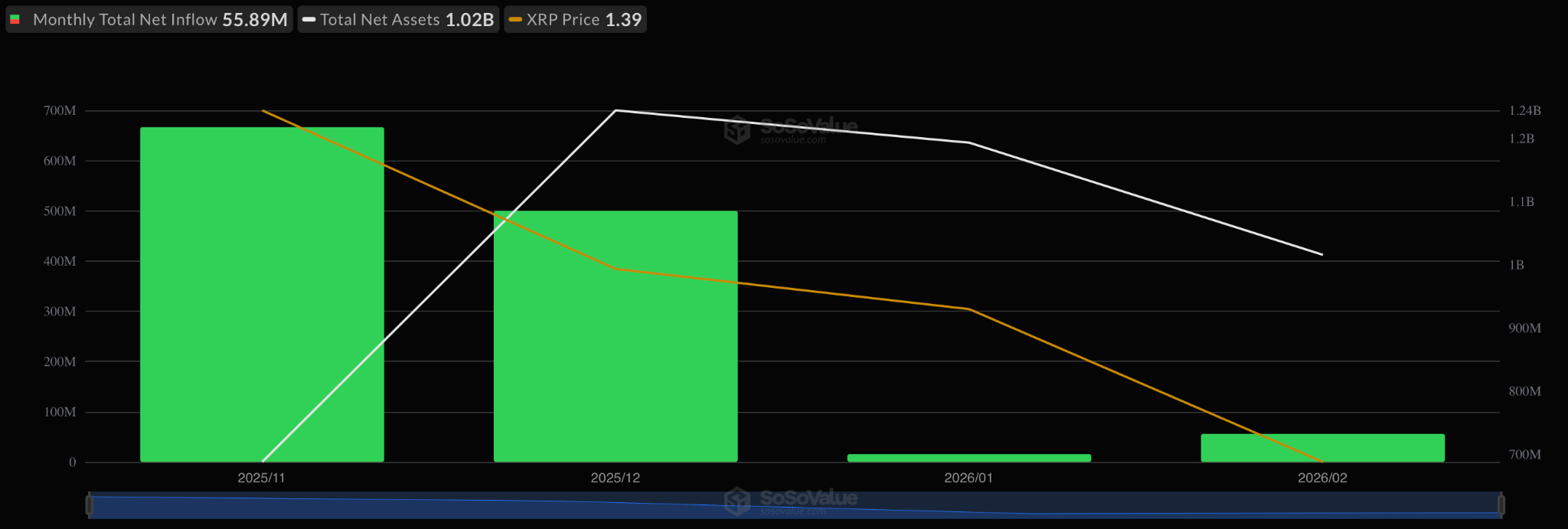

Source: SoSoValue

InvestingHaven forecasts a 2026 range of $1.58 to $4.25 with a bullish target of $5. A Monte Carlo simulation by 247 Wall St ran 10,000 scenarios and found only 10% exceeded $5.90. XRP at $5 is a 3.5x from $1.39. Good. But it is not early anymore.

Where XRP Stands Right Now

XRP trades at $1.39, down 61% from its $3.66 all time high. Spot ETFs have absorbed $1.24 billion since November. Whales holding 10 million to 100 million XRP now control 17.04% of supply after accumulating 3.17 billion tokens since October 2025.

The fundamentals are intact. A recovery to $5 is credible. But even at $5, a $10,000 XRP position becomes $35,000. That is a nice trade. It is not a life altering one.

The Pepeto Math That XRP Cannot Match

This is where the conversation shifts to a better opportunity for much bigger returns. It’s the new crypto presale Pepeto priced at $0.000000186. Six zeros. The presale has raised $7.33 million with 70% filled. Three products approaching launch. PepetoSwap for zero tax cross chain trading. Pepeto Bridge for cross blockchain transfers. Pepeto Exchange as the first meme coin listing hub.

The difference between XRP and Pepeto is not quality. It is timing. XRP already made its early investors rich. DOGE already made early believers millionaires. BONK turned fractions of a cent into portfolios. Every one of those tokens rewarded people who found them before the crowd. Pepeto is in that phase right now.

As an example, a $15,000 position in Pepeto at current price with a 150x return on listing becomes $2.25 million. That same $15,000 in XRP at $1.39 reaching $5 becomes $53,956. Both are legitimate investments. But only one of them changes your financial future.

On top of that, Pepeto staking at 211% APY means $15,000 generates $86.71 per day. That is $2,637 per month paid while you wait. Dual audits from SolidProof and Coinsult confirmed zero critical findings. An original Pepe cofounder created the project. The staking is the waiting bonus. The real play is the price.

The Consensus Tells You Where to Look Next

When every analyst agrees XRP tops at $5, that is valuable information. It tells you exactly how much runway is left. And it tells you to look for the asset with undefined upside. Pepeto at six zeros with three products and 70% filled is that asset.

Visit the Pepeto official website before the presale closes. The people who waited for consensus on DOGE paid $0.05 instead of $0.002. Do not wait for consensus on Pepeto.

Click To Visit Pepeto Official Website To Enter The Presale

FAQ

What is the XRP price prediction for 2026?

The analyst consensus targets $5.00 by year end. FXEmpire, InvestingHaven, and Elliott Wave models all converge around this level.

Can XRP reach $5 in 2026?

Yes. Reaching $5 requires sustained ETF inflows, passage of the Market Structure Bill, and a break above the $3.30 resistance. Multiple credible models support this target.

How much can Pepeto return compared to XRP?

XRP from $1.39 to $5 is a 3.5x return. Pepeto at $0.000000186 reaching a $50 million market cap delivers over 100x. The entry price math strongly favors presale stage tokens.

Where can I buy Pepeto?

Exclusively at the Pepeto official website presale. Not on any exchange yet. Listing is approaching with no vesting and no delays.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

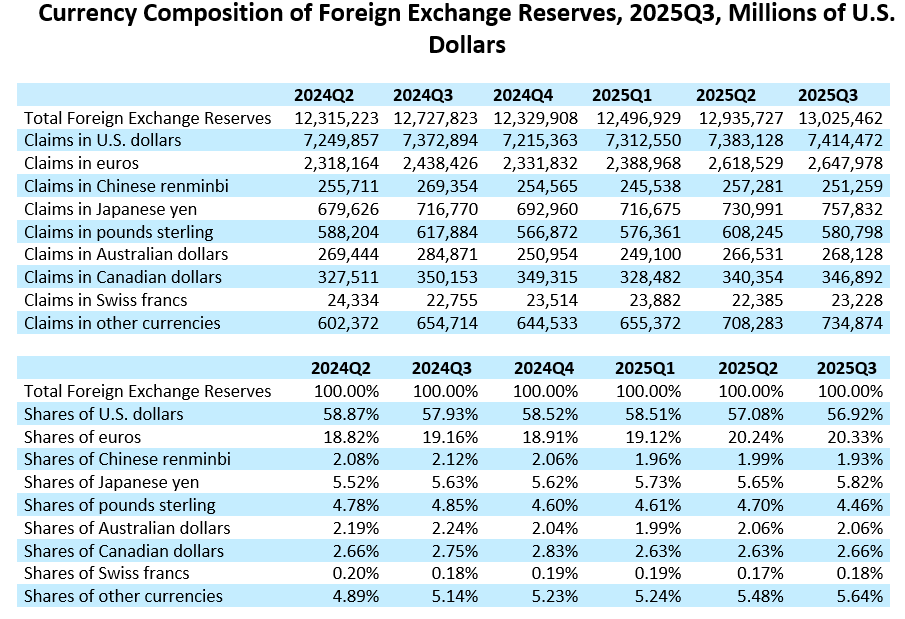

Japan is preparing its financial system for a world of stablecoins and tokenized assets, with banks, regulators and financial conglomerates working to bring the yen economy onchain.

The country is the world’s fourth-largest economy, and its yen is one of the most important currencies in global finance. According to the International Monetary Fund, the yen accounted for 5.82% of global foreign exchange reserves, ranking third worldwide.

A major reason for the yen’s systemic importance is the carry trade. Due to low interest rates, investors borrow cheap yen, convert it into other currencies and invest in higher-yield assets, making the yen one of the most trusted funding currencies for global markets.

Still, Japan’s central role in global finance has not been represented in the blockchain economy. That began to change after US President Donald Trump took office in January last year, which accelerated crypto policy discussions worldwide.

Like the US, Japan’s ruling party has stated its ambition to become a global center of Web3. Achieving that goal may depend on stablecoins capable of bringing the yen onchain. However, retail crypto activity in Japan remains relatively muted, even though the local industry is backed by some of the largest financial conglomerates and banks.

Japan’s crypto industry has the blessings of the government and conglomerates

Sanae Takaichi became Japan’s first female prime minister in October 2025. In just a few months in office, she dissolved the lower house for a snap election. Her Liberal Democratic Party (LDP) secured a two-thirds supermajority victory on Feb. 8, and lawmakers voted to reelect Takaichi for a second term 10 days later.

Startale Group CEO Sota Watanabe told Cointelegraph that she is widely seen as politically and strategically aligned with the Trump administration, which is accelerating local crypto adoption.

In April 2024, Takaichi’s LDP released a Web3 white paper to state its ambition to “make Japan the center of Web3.” The document outlined 11 crypto issues to address “immediately,” including income tax reform for individuals, stablecoins and security tokens.

Those priorities are also set in the blockchain strategy of SBI Group, which is one of the largest financial conglomerates in Japan, led by Yoshitaka Kitao.

“Kitao-san is the best person to commit to the crypto revolution in Japan because he created SBI under the evolution of the internet,” said Watanabe, whose Startale Group co-developed SBI’s Strium blockchain. The layer 1 aims to become the settlement infrastructure for institutional trading of tokenized equities and real-world assets (RWAs).

Kitao previously held executive positions at Nomura, Japan’s largest securities broker, and later at SoftBank alongside Masayoshi Son, who is second in Forbes’ Japan rich list. Kitao then founded SBI for SoftBank.

Related: Japan’s new crypto tax could wake ‘sleeping giant’ of retail investors

Watanabe claimed that SBI views crypto’s next onchain evolution as securities and stocks, though that requires the green light from the government.

“Right now, it is easy to make a derivative onchain, but to implement actual onchain dividends, actual voting rights of the stock, it needs to be regulation-compliant,” said Watanabe, who added that he is in talks with the Japanese government.

Also, dividends for onchain assets can’t be paid offchain, so a yen-backed stablecoin is needed.

Why a yen stablecoin matters

Japan’s interest rates and the yen carry trade are major forces that can move markets. The Bank of Japan raised interest rates in March 2024 from -0.1% to 0.1%, its first hike in 17 years. The following July, the central bank announced a more aggressive increase to 0.25%, rattling global markets and Bitcoin (BTC).

A yen-backed stablecoin could extend the carry trade into blockchain markets by bringing Japan’s low borrowing costs onchain.

For example, an investor could borrow a yen-denominated stablecoin at low interest rates. Those funds could then be used as collateral to borrow US dollar stablecoins, which can be deployed into decentralized finance (DeFi) lending, liquidity provision or other yield-generating strategies.

On Friday, Startale unveiled its own yen-backed stablecoin, JPYSC, targeting a second-quarter launch. According to Watanabe, the stablecoin is specifically designed to enable the yen carry trade onchain.

Related: Banks can’t seem to service crypto, even as it goes mainstream

“Once we implement the trust bank-backed stablecoin, it will become possible for global investors and institutions to execute the yen carry trade onchain,” he said.

Carry trades typically take time. The process can take one or two days to complete, as Japan’s and US’ business hours don’t overlap.

“But if we could do it onchain, we can do it 24/7 and instantly,” said Watanabe.

Theoretically, this could bring institutional yen borrowing to DeFi. But Justin d’Anethan, head of research at Arctic Digital, told Cointelegraph that an onchain carry trade won’t be impactful unless it comes with massive backers and a large market cap.

Watanabe told Cointelegraph that he has been in talks with the largest financial institutions in the US that are interested in carry trades and intraday swaps, though he declined to disclose names. He said that he has also been in contact with “top players” in DeFi.

The process still needs approval from Japanese authorities, while the regulatory treatment of stablecoins on bank balance sheets remains unresolved. Authorities such as the US Securities and Exchange Commission are still working to clarify capital and accounting requirements.

Japan’s crypto scene is accelerating, but retail is left out

A yen-backed stablecoin already exists in Japan in the form of JPYC, but it is primarily designed for payments. At the time of writing, its relatively small market capitalization of around $20 million makes it unsuitable for carry trades, which require deep liquidity and large borrowing capacity.

SBI isn’t the only financial institution exploring stablecoins in Japan. Three of the country’s largest banks — Mitsubishi UFJ, Sumitomo Mitsui Banking Corporation and Mizuho — are reportedly looking to jointly issue a yen-pegged stablecoin.

Despite the interest from local traditional finance giants and the government, the retail industry activity is muted.

The slow retail adoption is often blamed on the up-to-55% tax levy crypto investors face. That could also be shifting. Japan is exploring the reclassification of crypto from a payment tool to a financial product, which would drop the crypto tax to 20% and allow for exchange-traded funds based on crypto.

The tax deduction reform is expected to start from 2028. This isn’t good enough, according to Watanabe.

“The Japanese government is very slow,” he said. “Given that the US is accelerating onchain finance, to catch up, tax deduction in 2027 is necessary.”

For decades, the yen has served as a global funding currency through carry trades, but it is largely absent in the crypto industry. Retail participation remains limited by hefty tax rules, but the government and institutions are already positioning the yen to operate inside blockchain-based capital markets.

Magazine: Is China hoarding gold so yuan becomes global reserve instead of USD?

Cointelegraph Features and Cointelegraph Magazine publish long-form journalism, analysis and narrative reporting produced by Cointelegraph’s in-house editorial team and selected external contributors with subject-matter expertise. All articles are edited and reviewed by Cointelegraph editors in line with our editorial standards. Contributions from external writers are commissioned for their experience, research or perspective and do not reflect the views of Cointelegraph as a company unless explicitly stated. Content published in Features and Magazine does not constitute financial, legal or investment advice. Readers should conduct their own research and consult qualified professionals where appropriate. Cointelegraph maintains full editorial independence. The selection, commissioning and publication of Features and Magazine content are not influenced by advertisers, partners or commercial relationships.

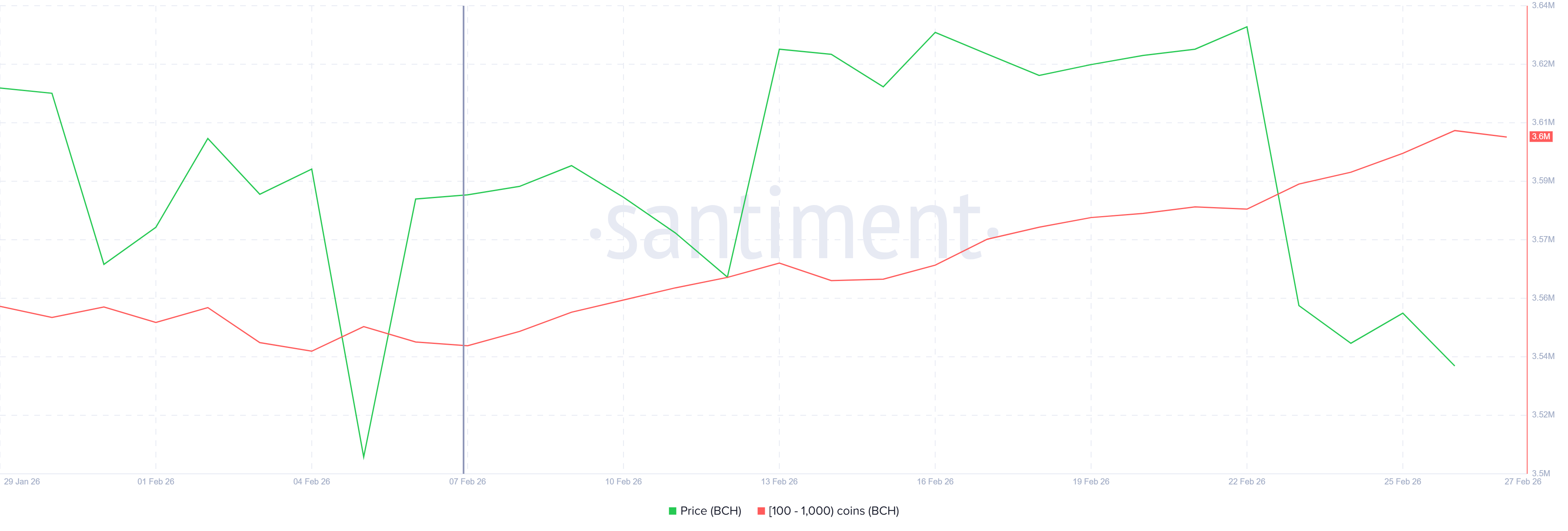

Bitcoin Cash price has recently dipped, triggering concerns of a broader bearish reversal. BCH slipped lower alongside the wider crypto market, testing short-term support zones. However, a broader macro view suggests the pullback may resemble a previous consolidation phase.

Historical patterns show similar volatility between October and November 2025. At that time, Bitcoin Cash formed a compression structure before staging a 28% rally. Current price behavior, combined with accumulation trends, indicates a comparable setup may be forming again.

Bitcoin Cash Holders Stick To Buying

On-chain data shows steady accumulation among mid-sized holders. Over the past 20 days, addresses holding between 100 and 1,000 BCH accumulated approximately 60,000 BCH. At current prices, this equates to roughly $28.6 million in value.

These holders represent non-whale participants who often signal organic demand. Their accumulation during recent price weakness reflects resilience. Unlike speculative traders, this group tends to build positions gradually. Sustained buying from this cohort can provide structural support beneath the Bitcoin Cash price.

Want more token insights like this? Sign up for Editor Harsh Notariya’s Daily Crypto Newsletter here.

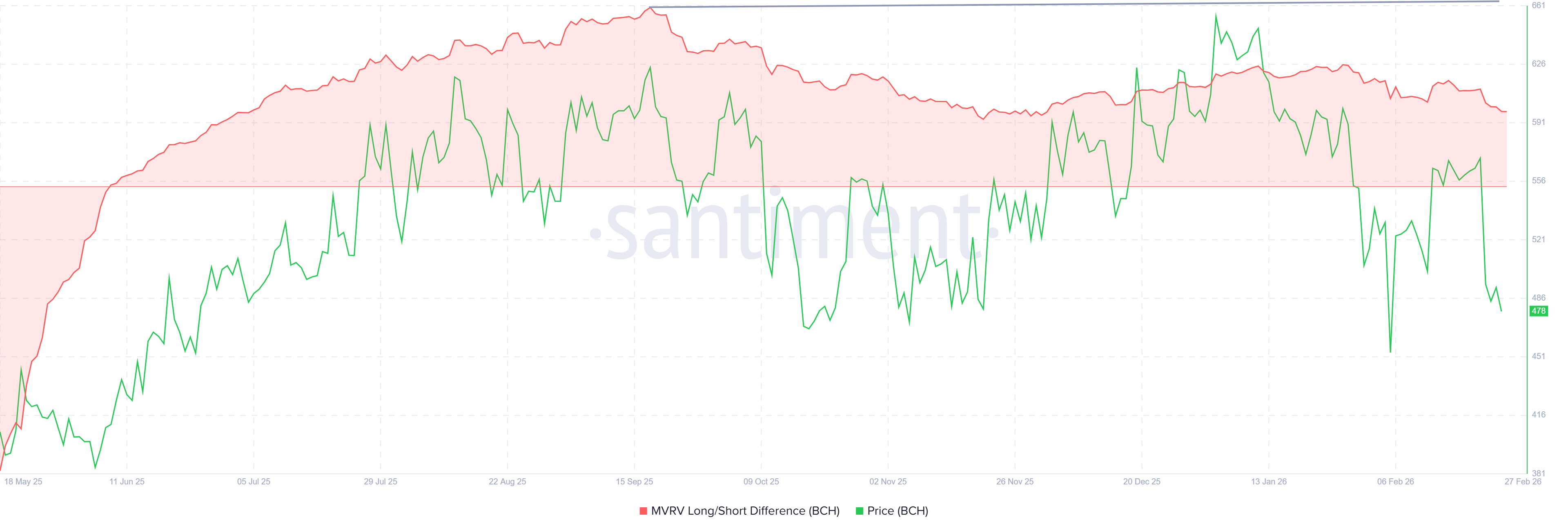

The MVRV Long/Short Difference metric adds further insight. The indicator currently sits in positive territory. Positive readings signal that long-term holders are more profitable than short-term holders.

This dynamic benefits Bitcoin Cash’s stability. Short-term holders often sell quickly at modest gains. Long-term holders typically retain positions during volatility. Their dominance can reduce immediate selling pressure and strengthen the foundation for a potential recovery phase.

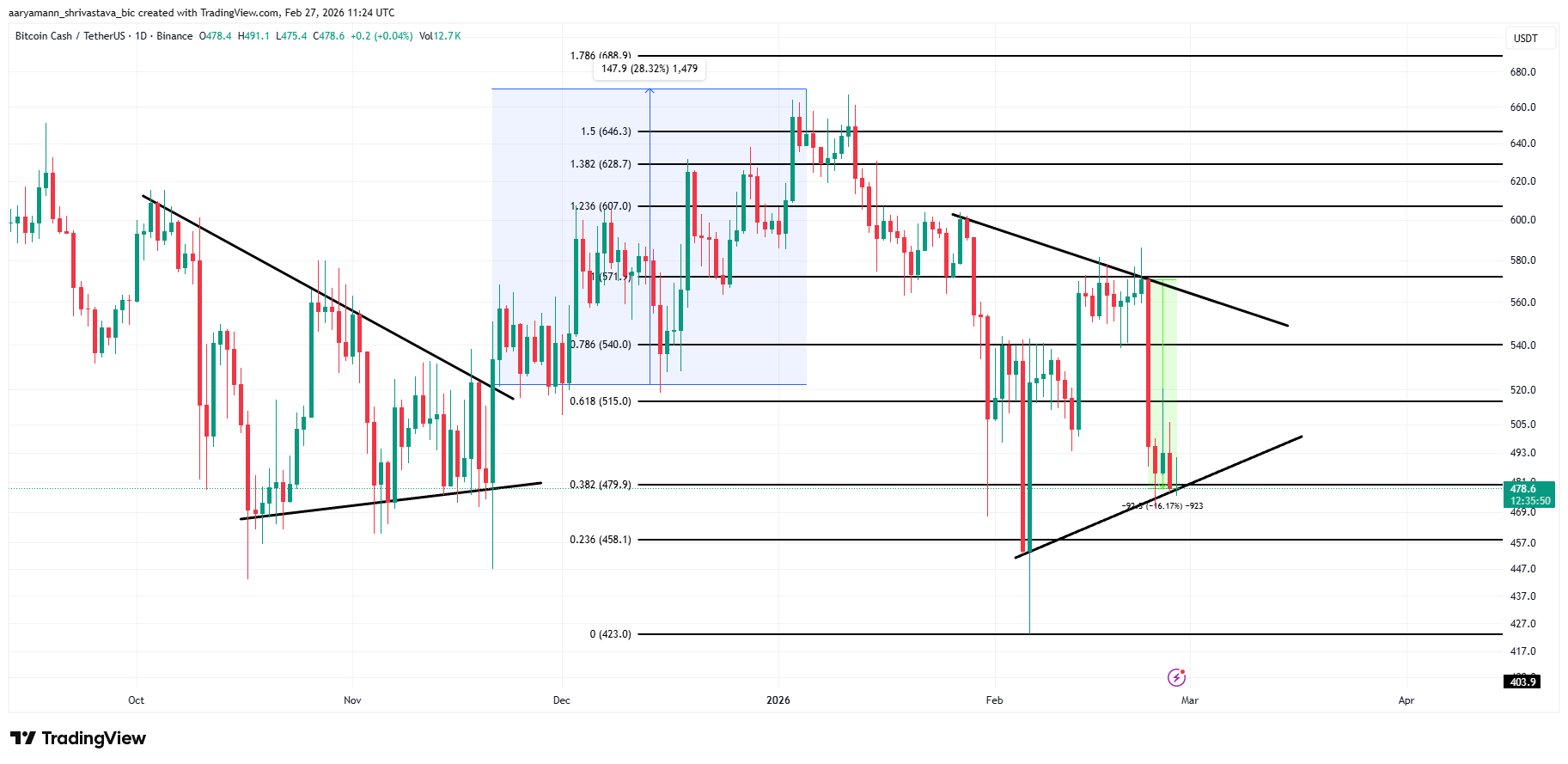

BCH Price Is Copying Its Past

Bitcoin Cash is trading at $478 at the time of writing, consolidating within an asymmetrical triangle pattern. A similar structure formed between October and November 2025 before a significant rally. That breakout produced a 28% price increase after prolonged compression.

For BCH to replicate that move, the $479 support must hold. The 15% decline this week has strengthened the triangle pattern. A confirmed breakout above $540 would signal renewed bullish momentum. Such a move could mirror the previous rally setup.

However, downside risk remains present. If sudden selling emerges, BCH could decline toward $458 support. Losing that level would weaken the bullish case. A sustained breakdown could push Bitcoin Cash toward $423, invalidating the recovery thesis and reinforcing bearish momentum.

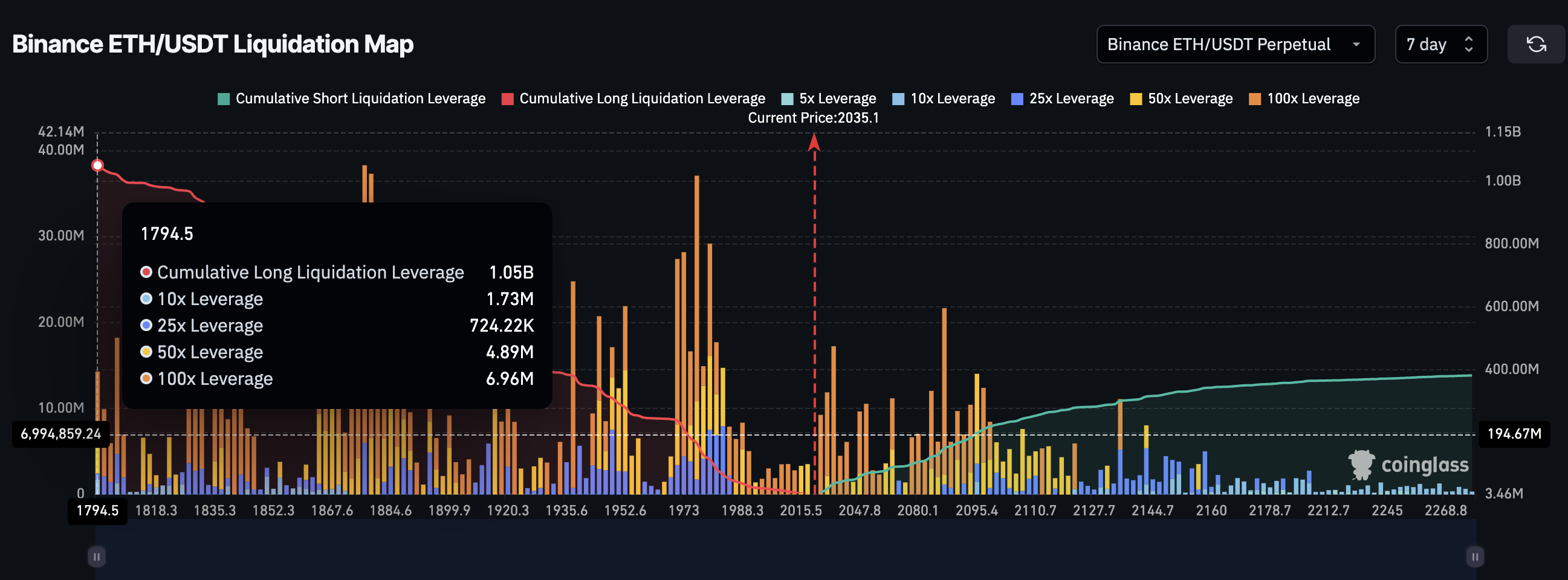

Ethereum price is down about 1.4% over the past 24 hours, extending its broader weakness. At first glance, this looks like a routine pullback inside a consolidation phase. But this decline did not appear randomly. It came right after a warning signal flashed on the daily chart, suggesting the recent recovery may already be losing steam.

What makes this moment unusual is the reaction from traders. Instead of reducing risk, leveraged long positions have surged past $1 billion. This creates a dangerous contradiction. The same conditions that are warning of a deeper drop are also attracting aggressive bullish bets. This disconnect could now decide Ethereum’s next major move.

Bearish Divergence And Supply Cluster Are Now Pointing To The Same Risk

The first warning sign appeared through a hidden bearish divergence on the daily chart. Between January 21 and February 25, the Ethereum price formed a lower high. This means the recent recovery was weaker than the previous rally, confirming the broader downtrend remains intact.

At the same time, the Relative Strength Index (RSI), which measures momentum strength, formed a higher high. This creates a hidden bearish divergence. This pattern usually appears during downtrends and signals that the recovery is only temporary, with the larger decline likely to continue.

Want more token insights like this? Sign up for Editor Harsh Notariya’s Daily Crypto Newsletter here.

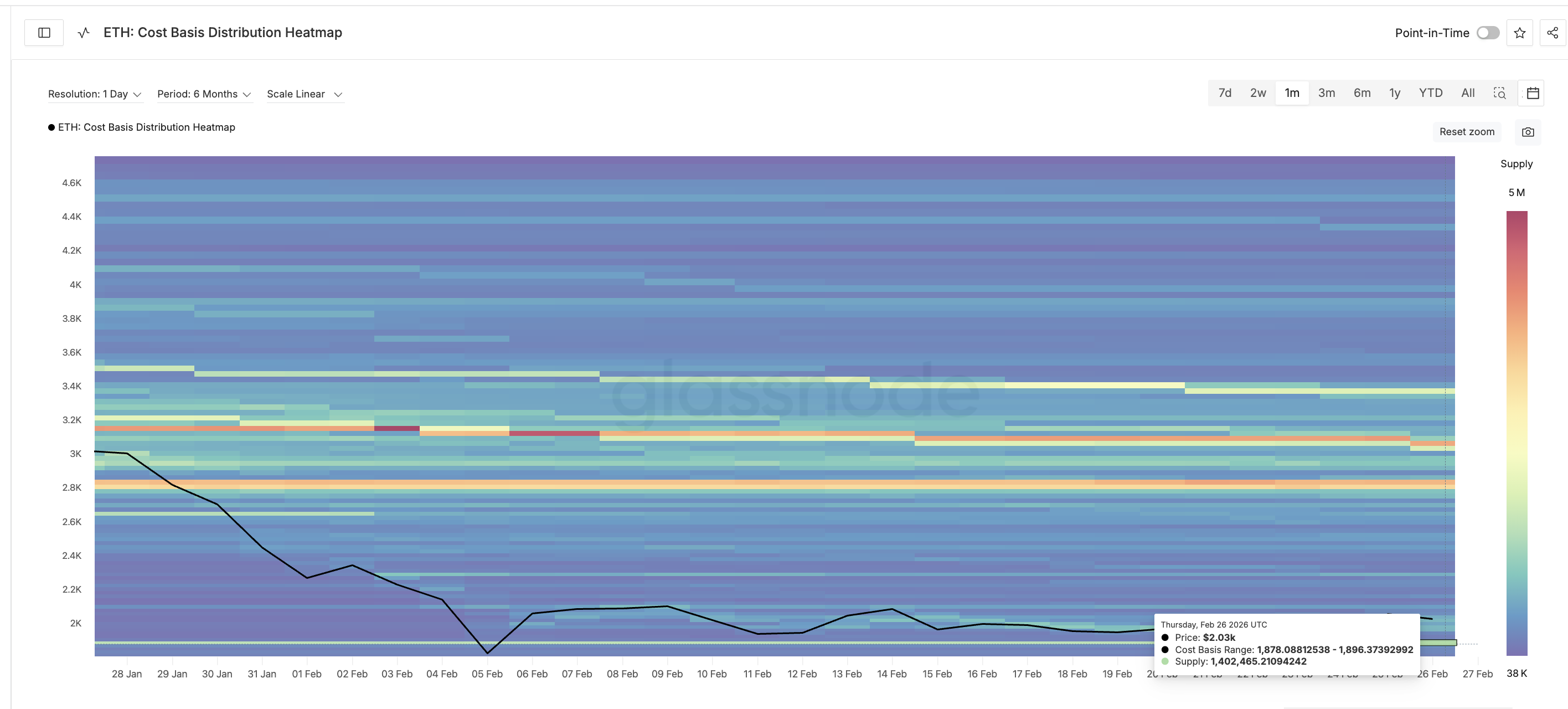

This signal becomes more important because Ethereum is already down about 32% over the past 30 days. That confirms the broader structure remains bearish. Now, on-chain data shows where this pullback could accelerate.

The Ethereum cost basis heatmap reveals a major support cluster between $1,870 and $1,890. Around 1.40 million ETH was accumulated in this range. This level is important because it represents the average buying zone for a large group of holders.

These holders are still in profit at current prices. But if Ethereum falls into this zone while fear increases, many may sell to protect their gains. This could weaken support and allow the pullback to deepen.

This makes the divergence warning more dangerous as a key support lies nearby.

Whale Selling And $1 Billion Long Exposure Create A Dangerous Conflict

At the same time, large holders are starting to show caution.

Ethereum supply held by whales has dropped slightly from 113.41 million ETH on February 25 to 113.39 million ETH now. This is not a large drop, somewhere in the $40 million range, but it confirms that whales are no longer aggressively accumulating.

This matters because whale activity often signals future price direction. When whales stop buying or begin selling, it weakens market confidence. But derivatives traders are reacting in the opposite way.

Binance liquidation data shows cumulative long leverage has crossed $1 billion. Short leverage, in comparison, sits near $382 million. This means long exposure is nearly three times higher. Even more importantly, nearly $697 million of long leverage is concentrated near $1,870. Per the map, the risk starts developing if the ETH price drops under $2,015.

This level aligns almost perfectly with the cost basis cluster starting near $1,870. This creates a high-risk situation.

If Ethereum falls into this zone, holders may begin selling while leveraged long positions are forced to close. These forced liquidations would push the price even lower and accelerate the correction. That risk could be the reason why whales have stepped back, for now.

But despite these risks, traders are still betting on a breakout. The reason becomes clear in Ethereum’s price structure itself.

Ethereum Price Structure Explains Both The $2,600 Hope And The Breakdown Risk

Ethereum’s recent price structure is creating the optimism that derivatives traders are betting on. On the 8-hour chart, Ethereum is forming a cup and handle pattern. This is a bullish structure that often appears before upward breakouts.

The handle is forming now as a consolidation phase, something that the traders might be considering as a lull before the breakout.

The neckline of this pattern is sloping upward. An upward-sloping neckline strengthens breakout expectations, provided the price can break past key resistance levels. The critical ones are now revealed by the technical projections.

If Ethereum breaks above $2,140, the pattern breakout hopes rise. While the neckline will still be at a distance, the hopes of a 17% rally toward $2,600 would surface. This upside potential possibly explains why traders continue opening long positions despite growing warning signs.

But this optimism depends entirely on Ethereum holding its support levels. If Ethereum falls below $1,990, weakness begins increasing, although the pattern still survives.

A drop below $1,890 would become much more serious. This level sits directly at the top of the cost basis cluster between $1,870 and $1,890. Losing this zone would weaken holder confidence and expose Ethereum to a deeper decline.

Below $1,820, the bullish structure would begin failing. If Ethereum falls below $1,790, the cup and handle pattern would be invalidated completely. This would remove the bullish setup and could trigger large-scale long liquidations.

That is why the same price structure attracting $1 billion in bullish bets is also sitting directly above the most dangerous breakdown zone. Recovery is still possible. But Ethereum must break above $2,140 first. Until then, Ethereum remains stuck between breakout hope and breakdown risk.

January’s PPI (Producer Price Index) printed +2.9% year-over-year (YoY) against a +2.6% forecast, with core PPI surging +3.6% versus +3.0% expected, sending US equities lower and reviving stagflation talk across crypto and macro communities.

The Producer Price Index measures wholesale-level inflation. This is what businesses pay before costs pass through to consumers, making it a leading signal for Federal Reserve (Fed) policy decisions.

Why it matters:

- Services prices drove the core beat, with month-over-month core PPI rising +0.8% against a +0.3% forecast, more than double expectations.

- The S&P 500 fell -0.87%, the Dow Jones dropped -1.38%, and the Nasdaq slid -1.09% following the release, reflecting immediate repricing of rate-cut expectations.

- A hotter-than-expected PPI reduces the probability of near-term Fed cuts, lifting yields and pressuring risk assets, including Bitcoin (BTC) and altcoins.

- Rising producer costs alongside slowing GDP growth creates a stagflation scenario where the Fed cannot cut without reigniting inflation or hold without slowing the economy further.

The details:

- Headline PPI came in at +2.9% YoY (prior: +3.0%); core PPI at +3.6% YoY (prior: +3.3%), per data released February 27 at 8:30 AM ET.

- Month-over-month: headline +0.5% (exp. +0.3%), core +0.8% (exp. +0.3%), driven by a services component surge.

- Trade services margins climbed +2.5% as a primary driver of the core beat.

- S&P 500 futures were already down 57 points before the data hit, signaling broader stress beyond the PPI print alone.

- The upside came from trade-services normalization, not from broad input-cost acceleration.

The big picture:

- Analysts like Crypto Rover and Max Crypto flag a stagflation signal: core PPI rising while GDP cools. This combination often limits central bank flexibility.

- The Fed’s rate-cut timeline faces further pressure as back-to-back inflation beats challenge the disinflation trend heading into March.

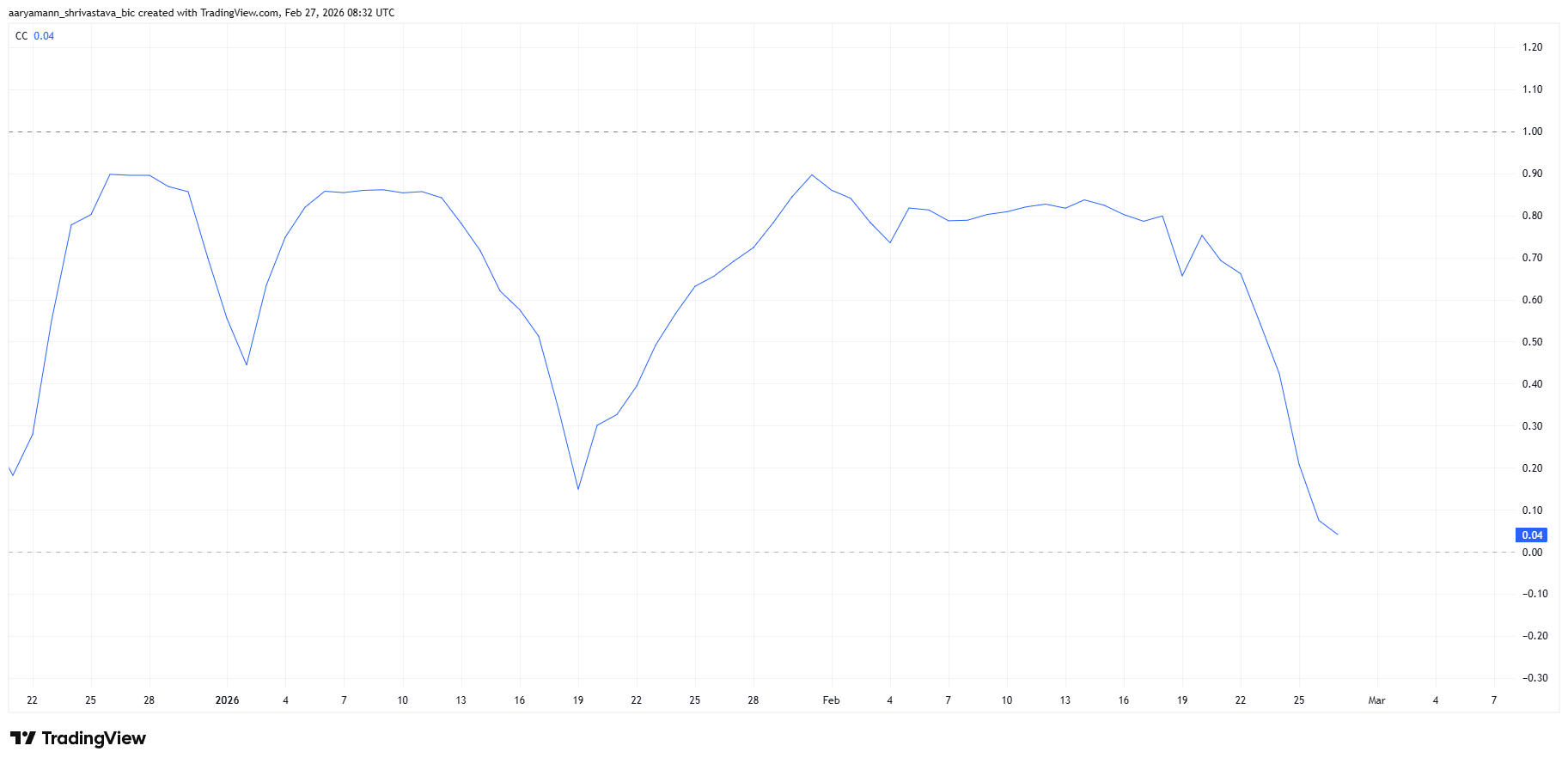

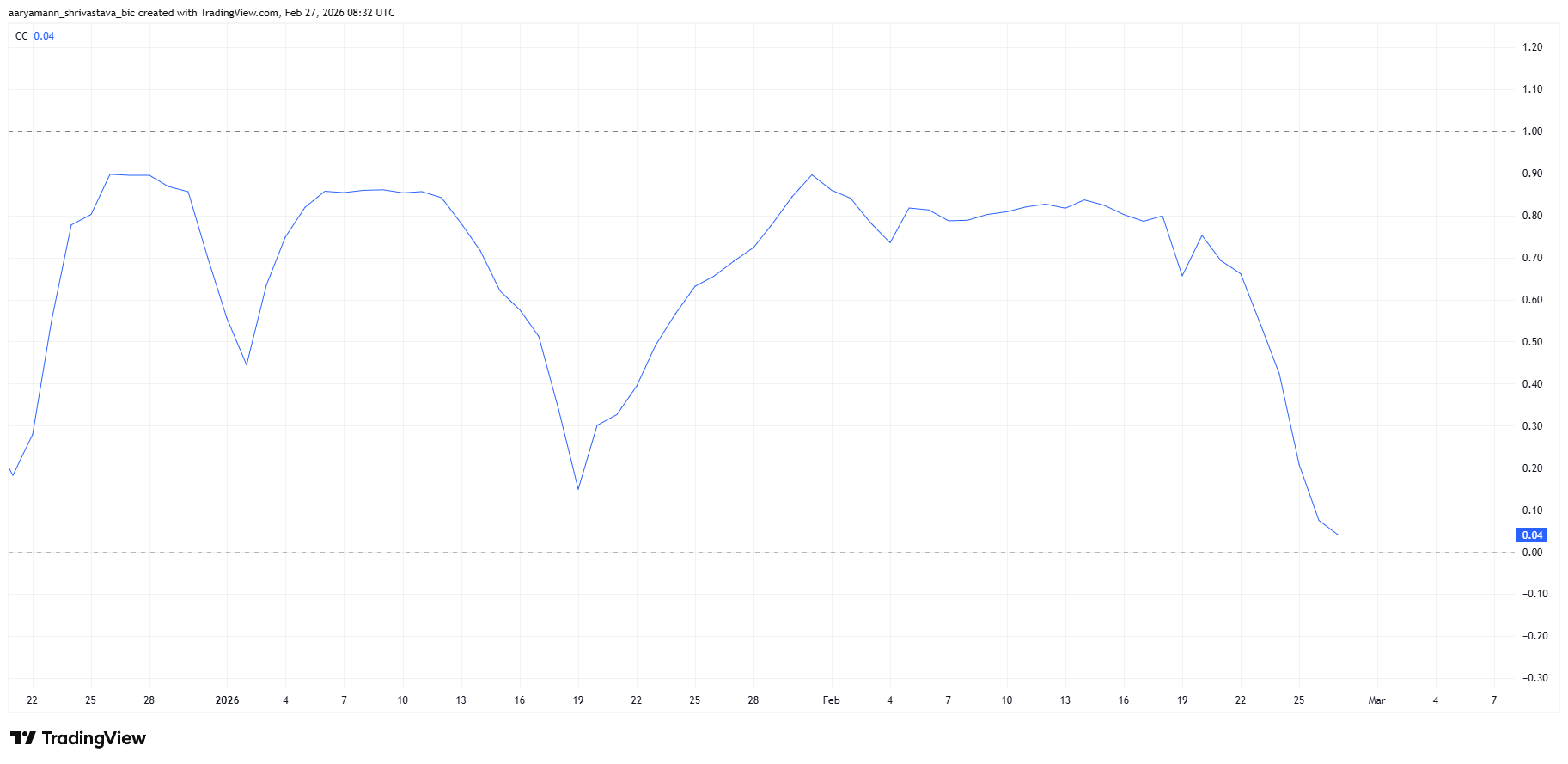

Terra Luna Classic (LUNC) price lacked clear direction for weeks before staging a sharp three-day rally. The sudden surge pushed the token up nearly 30% at its intraday peak. However, technical and on-chain signals suggest the breakout may struggle to sustain momentum.

The broader crypto market has experienced periodic bursts of volatility. LUNC’s recent move stands out due to its speed rather than structural strength. While price action turned briefly bullish, underlying metrics indicate caution is warranted.

Bitcoin – The Cause Of LUNC’s Rise

The primary catalyst behind LUNC’s rally was a surge in trading volume. Increased speculative activity drove short-term price acceleration. At the same time, LUNC’s correlation with Bitcoin dropped to 0.04, signaling near-complete decoupling.

Such low correlation suggests the token temporarily moved independently of BTC. Decoupling phases can attract traders seeking isolated momentum plays. However, similar patterns have appeared across several altcoins recently. These shifts often reflect short-lived speculative rotations rather than lasting structural change.

Want more token insights like this? Sign up for Editor Harsh Notariya’s Daily Crypto Newsletter here.

LUNC Is Trapped Under Bearish Pressure

The Chaikin Money Flow indicator reveals a concerning divergence. Despite rising prices over the past three days, CMF did not confirm sustained inflows. Capital entering the market remained subdued relative to price movement.

A bearish divergence formed as price climbed while CMF weakened. This pattern indicates that buying pressure failed to match the rally’s strength. Outflows continued quietly beneath the surface.

Weak inflow confirmation raises questions about durability. Without consistent capital accumulation, rallies risk reversal. Price movements unsupported by strong liquidity often correct once speculative interest fades.

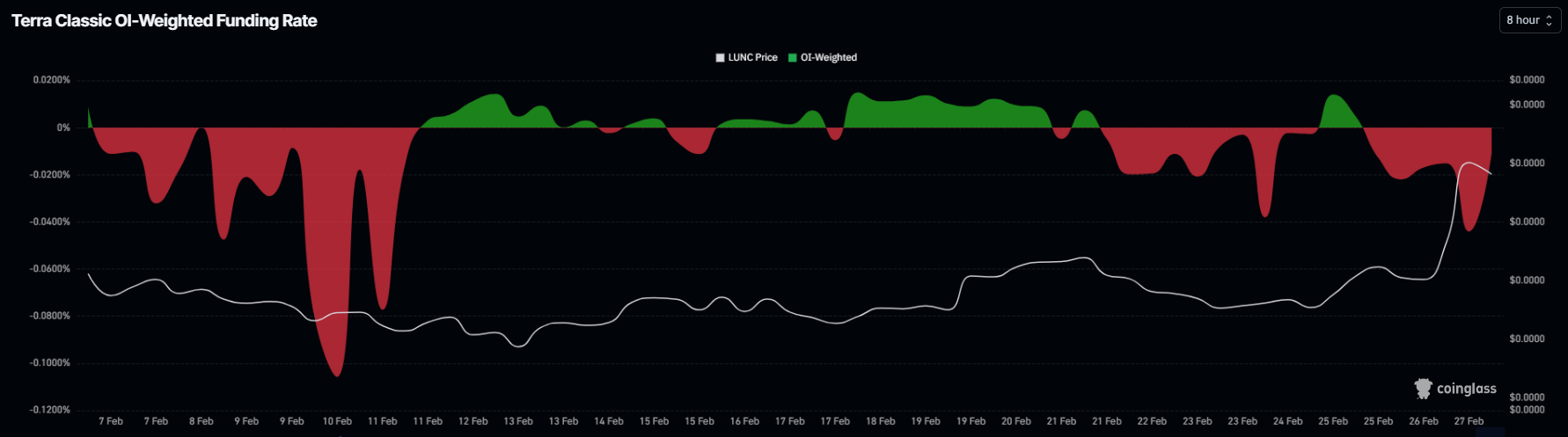

Derivatives data adds to the cautious outlook. LUNC’s funding rate currently sits in negative territory. Negative funding signals dominance of short positions over longs.

Aggregate funding metrics show traders are positioning for downside risk. Elevated short interest can cap upward momentum. If short bias persists, LUNC may continue consolidating unless forced liquidations trigger a squeeze.

LUNC Price May Not See Much Growth

LUNC rose roughly 20% over the past three days and surged 30% at its recent intraday high before retreating to $0.00004136. The long upper wick on the chart signals rapid profit-taking. Quick distribution at higher levels limited further upside continuation.

Current technical conditions present a bearish bias. If selling pressure resumes, LUNC could decline toward $0.00003459. This level aligns with the 23.6% Fibonacci retracement. A breakdown below $0.00003459 may expose the next support near $0.00003236, invalidating the bullish recovery narrative.

On the upside, LUNC remains capped beneath the $0.00004203 resistance, marked by the 61.8% Fibonacci level. A decisive breakout above this barrier would shift short-term momentum. Flipping $0.00004203 into support could push the token toward $0.00004530 and potentially higher, invalidating the immediate bearish thesis.

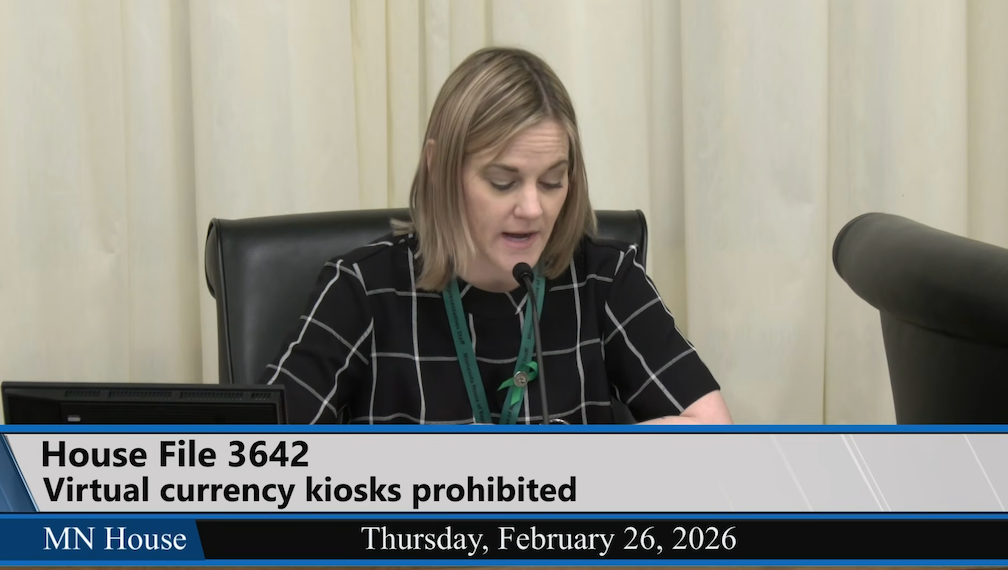

A Minnesota lawmaker has introduced a bill that could ban virtual currency kiosks statewide after reports of scams tied to crypto ATMs. Bitcoin ATMs (CRYPTO: BTC) have emerged as a focal point in law-enforcement briefings, where operators have been accused of enabling irreversible transactions that are hard to trace. Rep. Erin Koegel unveiled House File 3642 during a Thursday session of the Commerce Finance and Policy Committee, arguing the technology behind crypto kiosks remains novel and minimally regulated. Minnesota voters have already seen a 2024 law intended to curb kiosk abuse by capping new-user deposits at $2,000 and requiring refunds to fraud victims, but Koegel’s measure would push toward a full ban if enacted. Supporters say it would shield residents from irreversible financial crimes, while opponents caution it could restrict access to legitimate crypto services and push activity underground. Koegel cited committee remarks and testimony during the session.

Key takeaways

- House File 3642 would ban crypto kiosks across Minnesota if enacted, expanding beyond the state’s 2024 safeguards.

- The 2024 law introduced a $2,000 deposit limit for new kiosk users and required refunds for fraud, signaling a trend toward consumer protections.

- Law enforcement officials described cryptocurrency kiosks as a common scam vector, with aging populations identified as particularly vulnerable groups.

- There are about 350 licensed crypto kiosks in Minnesota, operated by firms including Bitcoin Depot and Coinflip, according to the state’s findings.

- Industry responses emphasize a broader regulatory debate about crypto ATMs, privacy, and access versus fraud risk, with related moves like ID-verification policies signaling a shifting risk profile.

Tickers mentioned: $BTC

Sentiment: Neutral

Market context: The Minnesota proposal sits within a broader regulatory moment as lawmakers and regulators reassess crypto kiosks amid ongoing fraud concerns. Across the U.S., states are weighing standardized protections for crypto ATM users, while operators consider compliance measures to balance customer access with risk controls. The trend toward enhanced identity checks and clearer fraud warnings reflects a shift in how the market perceives the balance between innovation and consumer protection.

Why it matters

The bill’s momentum highlights a policy question at the intersection of financial technology and consumer protection. Crypto kiosks offer convenient access points for the public to buy and sell digital assets, but their relative lack of traditional safeguards has made them attractive targets for scammers. Minnesota’s current framework—enacted in 2024—was designed to curb abuse by imposing a deposit cap and mandating refunds for fraud victims. Yet the proposed HF 3642 would push the state toward a more restrictive approach, potentially banning the devices altogether. The stakes are not merely about kiosks; they reflect a broader debate about how to regulate rapidly evolving crypto infrastructure without stifling legitimate use cases or hindering access to digital assets for ordinary residents.

Industry responses point to a practical tension: operators argue that well-defined rules can reduce abuse while preserving access. Bitcoin Depot, one of the largest operators in the U.S., has already begun a phased rollout of ID verification for all transactions at its machines, a policy aimed at curbing misuse while maintaining user convenience. The move signals a willingness among some players to embrace stronger controls in the name of compliance and consumer protection; it also foreshadows a regulatory environment in which basic access could be contingent on identity verification and heightened disclosures. The pressurized policy backdrop is further amplified by consumer advocacy groups that emphasize protections, such as fraud warnings and transaction-limits, as essential to preserving trust in mainstream crypto usage.

For the market, these developments touch on liquidity, risk sentiment, and the perceived legitimacy of on-ramp infrastructure. When a state with tens (and potentially hundreds) of kiosks contemplates a ban, it underscores the fragility and scrutiny surrounding crypto-on-ramp channels. While the debates unfold, observers watch for how other states respond to similar concerns and whether broader federal or regulatory moves could harmonize or clash with state-level approaches. The tension between enabling convenient access to digital assets and preventing harms linked to fraudulent activity remains a defining feature of the current regulatory landscape.

In parallel, consumer protection narratives continue to gain traction. The American Association of Retired Persons (AARP) has highlighted ongoing fraud protections in several states, urging operators to implement practical safeguards such as transaction limits and clear fraud warnings. As lawmakers weigh HF 3642 against the potential benefits of accessible crypto tools for everyday users, the interplay between policy, technology, and consumer trust will likely shape the contours of Minnesota’s crypto kiosk ecosystem in the months ahead. The discussion also echoes broader policy conversations about how to regulate novel financial technologies while preserving opportunities for legitimate innovation.

“Because of the nature of cryptocurrency, these fraudulent transactions are often irreversible and incredibly hard to track,” Koegel said, emphasizing the need for a coordinated, cross-partisan response to protect citizens from irreversible financial crimes.

The current environment therefore blends caution with pragmatism: protect vulnerable users and deter fraud, while acknowledging that kiosks can provide a straightforward entry point to digital assets for some residents. The outcome of HF 3642 remains uncertain, but the policy debate is unlikely to fade anytime soon as Minnesota and other states evaluate how to balance accessibility and security in an evolving crypto economy.

What to watch next

- Progress of House File 3642 in the Minnesota House of Representatives, including committee votes and potential floor action.

- Any Senate companion or changes in the legislative process that could influence the bill’s trajectory.

- Updates to kiosk regulations and enforcement actions stemming from the 2024 deposit-limit law, and any new operator compliance measures.

- Industry responses from crypto ATM operators regarding verification policies and fraud-prevention efforts, and how these may influence state debates.

Sources & verification

- House File 3642 and committee materials from the Minnesota House of Representatives (HF 3642 – Commerce Finance and Policy Committee materials).

- Committee hearing coverage and remarks, including Rep. Koegel’s statements and the discussion on the 2024 law, captured in the committee video (YouTube: https://www.youtube.com/watch?v=w6hc8OkvaZE).

- State data on licensed crypto kiosks in Minnesota (approximately 350 kiosks operated by Bitcoin Depot, Coinflip, and others).

- Bitcoin Depot policy update requiring ID verification for all crypto ATM transactions (Cointelegraph: https://cointelegraph.com/news/bitcoin-depot-mandatory-id-verification-crypto-atms).

- AARP’s guidance on crypto ATM fraud protections and related protections in multiple states (https://www.aarp.org/advocacy/crypto-atm-fraud-protections/).

A Minnesota lawmaker has introduced a bill that could ban virtual currency kiosks across the state after reports of incidents involving crypto-related scams.

In a Thursday session of the Minnesota House of Representatives Commerce Finance and Policy Committee, Representative Erin Koegel said the bill, House File 3642, would address the “novel” and “minimally regulated” technology of crypto kiosks.

Koegel said she had heard from state law enforcement agencies that many scammers used the kiosks to trick residents into sending crypto, while legitimate traders tended to use centralized exchanges.

“Because of the nature of cryptocurrency, these fraudulent transactions are often irreversible and incredibly hard to track,” said Koegel, adding:

“This bill gives us an opportunity to work across party lines to protect the people of Minnesota from irreversible financial crimes.”

Minnesota’s government already passed a law in 2024 attempting to fight scammers using the state’s virtual currency kiosks. The law set a $2,000 deposit limit for new kiosk users and required companies to issue full refunds for fraud victims. However, Koegel’s bill, if passed, could fully ban the technology in Minnesota.

“Within the past couple of years, we’ve definitely identified an issue with these Bitcoin ATMs, specifically in our jurisdiction,” said Sergeant Jake Lanz of the St. Cloud Police Department at the Thursday committee meeting. “[…] it also is notable for us that it is definitely a target of our aging population.”

Related: US senators to weigh CFTC, other amendments to crypto market structure bill

According to the House, Minnesota has about 350 licensed crypto kiosks operated by several companies, including Bitcoin Depot and Coinflip. The American Association of Retired Persons reported in February that 17 states had laws on the books requiring crypto ATM operators to implement protections against fraudsters, such as setting daily transaction limits and requiring fraud warning signs.

Bitcoin ATM operator to require IDs for all transactions

On Tuesday, Bitcoin Depot, one of the largest crypto ATM operators in the US, announced that it would implement a policy requiring ID verification for users with every transaction at one of its machines. The phased rollout, which began in February, was in response to “potential misuse,” though the company did not specifically mention state-level crackdowns on scammers.

Magazine: Would Bitcoin really be at $200K if not for Jane Street? Trade Secrets

Multinational bank Barclays (BARC) is exploring the creation of a blockchain platform for payments and other processes, Bloomberg reported on Friday.

The London-based financial services giant is consulting with prospective technology providers on the development of such a platform that would see it rival JPMorgan (JPM) and others in using decentralized technology for banking services.

Barclays’ blockchain-based plans could include stablecoins and tokenization, according to the report, citing people familiar with the matter.

JPMorgan first allowed tokenized deposits — deposits represented as digital tokens on a decentralized ledger — through its dollar-denominated JPM Coin all the way back in 2019.

More recently, HSBC has also enabled tokenized deposits to expand its own push into blockchain-based payments.

Such institutions are exploring how blockchain technology can make existing financial processes more transparent and more efficient by carrying them out on decentralized networks that lack some of the input of intermediaries and allow faster settlement.

Barclays did not respond to CoinDesk’s request for comment.

Read More: JPMorgan expands blockchain goals, plans to build ‘interoperable digital money’

A Guide to Selecting Adhesives for Medical Device Applications

HuffPost Headlines 2-27

Building Trust in Houston’s Industrial Real Estate

Smart energy pays enters the US market, targeting scalable financial infrastructure

Why Israel is blocking foreign journalists from entering

Bitcoin: We’re Entering The Most Dangerous Phase

Altseason Starting? Bull Trap or Relief Rally Explained | Crypto Market Update | Bitcoin Update?

Bitcoin Accumulation ERUPTS As The Financial System Cracks! Supply Shock Incoming?

Financial Planning in Your 40s | #ytshorts #shorts #financialplanning #personalfinance #moneygoals

-

Politics5 days ago

Politics5 days agoBaftas 2026: Awards Nominations, Presenters And Performers

-

Fashion7 days ago

Fashion7 days agoWeekend Open Thread: Boden – Corporette.com

-

Sports4 days ago

Sports4 days agoWomen’s college basketball rankings: Iowa reenters top 10, Auriemma makes history

-

Politics4 days ago

Politics4 days agoNick Reiner Enters Plea In Deaths Of Parents Rob And Michele

-

Business3 days ago

Business3 days agoTrue Citrus debuts functional drink mix collection

-

Politics18 hours ago

Politics18 hours agoITV enters Gaza with IDF amid ongoing genocide

-

Crypto World3 days ago

Crypto World3 days agoXRP price enters “dead zone” as Binance leverage hits lows

-

Business5 days ago

Business5 days agoMattel’s American Girl brand turns 40, dolls enter a new era

-

Business5 days ago

Business5 days agoLaw enforcement kills armed man seeking to enter Trump’s Mar-a-Lago resort, officials say

-

NewsBeat2 days ago

NewsBeat2 days agoCuba says its forces have killed four on US-registered speedboat | World News

-

NewsBeat2 days ago

NewsBeat2 days agoManchester Central Mosque issues statement as it imposes new measures ‘with immediate effect’ after armed men enter

-

Tech3 days ago

Tech3 days agoUnsurprisingly, Apple's board gets what it wants in 2026 shareholder meeting

-

NewsBeat4 days ago

NewsBeat4 days ago‘Hourly’ method from gastroenterologist ‘helps reduce air travel bloating’

-

Tech5 days ago

Tech5 days agoAnthropic-Backed Group Enters NY-12 AI PAC Fight

-

NewsBeat5 days ago

NewsBeat5 days agoArmed man killed after entering secure perimeter of Mar-a-Lago, Secret Service says

-

Politics5 days ago

Politics5 days agoMaine has a long track record of electing moderates. Enter Graham Platner.

-

Business2 days ago

Business2 days agoDiscord Pushes Implementation of Global Age Checks to Second Half of 2026

-

NewsBeat3 days ago

NewsBeat3 days agoPolice latest as search for missing woman enters day nine

-

Sports4 days ago

Sports4 days ago2026 NFL mock draft: WRs fly off the board in first round entering combine week

-

Crypto World3 days ago

Crypto World3 days agoEntering new markets without increasing payment costs