Business

FCC Chairman Carr says ‘The View’ faces ‘uphill climb’ over equal time

Federal Communications Commission Chairman Brendan Carr joins ‘Mornings with Maria’ to discuss the FCC’s probe into soaring NFL streaming costs, an investigation into ABC’s ‘The View’ over equal time rules and a push for patriotic programming.

ABC’s “The View” is under Federal Communications Commission (FCC) review after Chairman Brendan Carr said the long-running talk show faces an “uphill climb” in proving it qualifies as a legitimate news program.

“The View” is at the center of an investigation by the FCC over the agency’s equal-time rules, which prevent media from favoring certain political candidates. The investigation follows increased FCC scrutiny of political segments on entertainment programs.

“When you look at the lineup of guests that have typically been on ‘The View,’ I think it’s an uphill climb for Disney to make the case that they’re just a straight news program,” Carr said Friday on “Mornings with Maria.”

VERIZON CUSTOMERS FACE 35-DAY WAIT TO UNLOCK PAID-OFF PHONES UNDER POLICY CHANGE

Federal Communications Commission Chairman Brendan Carr speaks onstage during the 2025 Concordia Annual Summit at the Sheraton New York Times Square in New York City on Sept. 22, 2025. (John Lamparski/Getty Images for Concordia Annual Summit / Getty Images)

The dispute stems from an appearance by Texas Senate candidate James Talarico, while his primary opponent, Democratic Rep. Jasmine Crockett of Texas, was not offered a slot. Crockett has previously appeared on the program but said those appearances were not related to her current Senate campaign.

TRUMP TRADE CHIEF DEFIANT ON SUPREME COURT RULING, VOWS TO RESTORE TARIFFS WITHIN MONTHS

“Bona fide” newscasts and interviews are typically exempt from the equal-time rules, but Carr said it may be tough for the show to prove that’s what they are.

Whoopi Goldberg, Sara Haines, Joy Behar, Ana Navarro, Sunny Hostin and Alyssa Farah Griffin appear during the Season 29 premiere of “The View,” which aired Sept. 8, 2025, on ABC. (Lou Rocco/American Broadcasting Companies, Inc. via Getty Images / Getty Images)

“Disney’s ‘The View’ is now asserting to the FCC that they are a bona fide news program. And we started an enforcement action there. We’ve issued letters of inquiry, which are versions of subpoenas,” Carr said.

MIKE DAVIS: WHY WE MUST DROP ANTIQUATED RULE SHACKLING TV IN STREAMING ERA

He added that dozens of Disney-affiliated TV stations disagree with the company’s claim that “The View” qualifies as exempt news programming under the equal-time rule. Carr said the FCC has received several equal-time notices from the affiliate stations, which could allow Crockett to request airtime.

Federal Communications Commission Chairman Brendan Carr joins ‘Mornings with Maria’ to discuss the FCC’s probe into soaring NFL streaming costs, an investigation into ABC’s ‘The View’ over equal time rules and a push for patriotic programming.

CLICK HERE TO DOWNLOAD THE FOX NEWS APP

“Congress passed a law, and they didn’t want media gatekeepers to be deciding the outcomes of elections by having exclusively one political candidate or one political party on all the time,” added Carr.

Earlier this month, CBS’s “The Late Show” declined to air a segment with Talarico over equal-time concerns. CBS released a statement denying it censored host Stephen Colbert, saying the show instead chose to post the interview on YouTube to avoid triggering the rule.

FCC Chairman Brendan Carr joins ‘Mornings with Maria’ to break down the agency’s wins following President Donald Trump’s first 100 days in office.

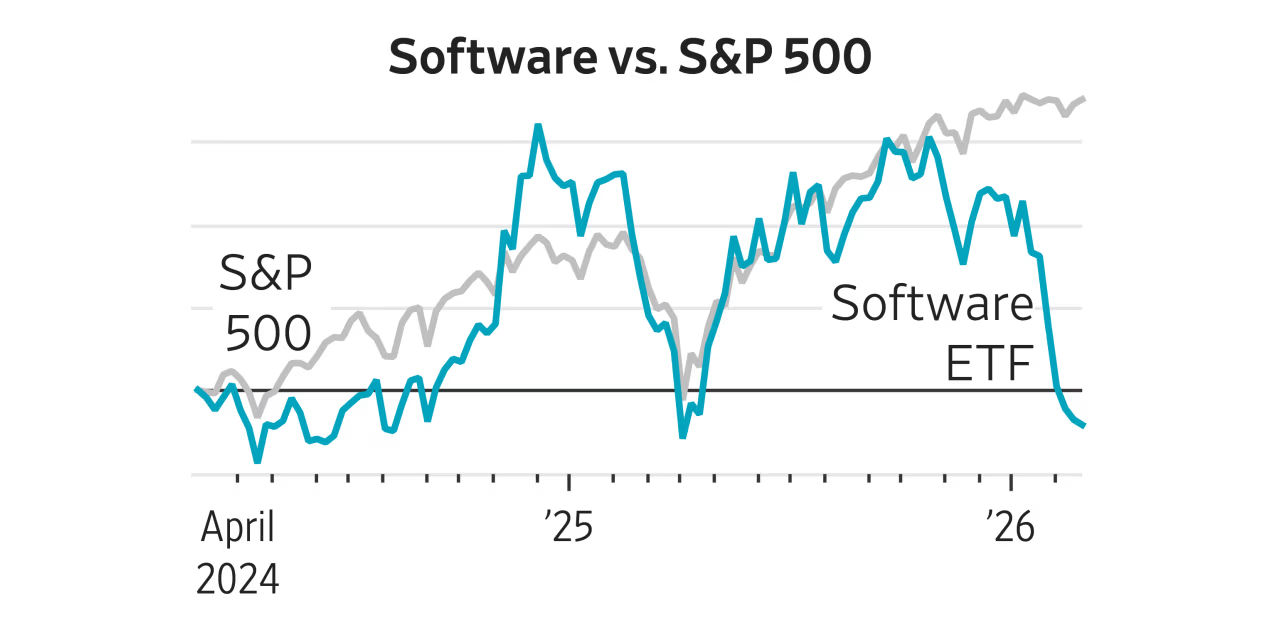

One of the 21st century’s hottest sectors has become a market albatross.

Concern over the threat that artificial intelligence poses to software companies has hit the shares of companies like Salesforce and Adobe ADBE 1.03%increase; green up pointing triangle hard. Investors are questioning whether software companies that sell to businesses can withstand competition from AI-powered rivals. Lately, the selloff has intensified with each new announcement from AI developers.

Copyright ©2026 Dow Jones & Company, Inc. All Rights Reserved. 87990cbe856818d5eddac44c7b1cdeb8

Business

Pacira BioSciences, Inc. 2025 Q4 – Results – Earnings Call Presentation (NASDAQ:PCRX) 2026-02-27

Q4: 2026-02-26 Earnings Summary

EPS of $0.57 misses by $0.33

| Revenue of $196.87M (5.14% Y/Y) misses by $5.06M

Seeking Alpha’s transcripts team is responsible for the development of all of our transcript-related projects. We currently publish thousands of quarterly earnings calls per quarter on our site and are continuing to grow and expand our coverage. The purpose of this profile is to allow us to share with our readers new transcript-related developments. Thanks, SA Transcripts Team

The smartphone rivalry between Samsung and Apple reached new heights in early 2026 with the February release of the Galaxy S26 Ultra and the lingering dominance of Apple’s iPhone 17 Pro Max, launched in September 2025. As consumers weigh upgrades or switches between ecosystems, the two devices stand as premier options for power users, creators and photographers seeking cutting-edge performance.

Both phones command premium pricing: the Galaxy S26 Ultra starts at $1,299 for 256GB, while the iPhone 17 Pro Max begins at $1,199 for the same storage tier. Despite the slight edge in starting cost for Apple, real-world value depends on priorities like ecosystem integration, camera versatility, battery endurance and unique features.

Design and Build

The Galaxy S26 Ultra measures 163.6 x 78.1 x 7.9mm and weighs 214g, making it thinner and lighter than the iPhone 17 Pro Max at roughly 8.75mm thick and heavier build. Samsung refined the Armor Aluminum frame with rounded ergonomic corners for better one-handed comfort, addressing past complaints about sharp edges. It retains IP68 resistance and includes the built-in S Pen stylus for note-taking, drawing and productivity.

Apple opted for a bold unibody aluminum chassis that wraps around the back, ditching the previous titanium-glass sandwich for a more integrated, aggressive look with a prominent camera plateau. The iPhone feels sturdy and protective, though its extra thickness and weight make it less pocket-friendly for some users. Both offer high durability with advanced glass protection — Gorilla Armor 2 on Samsung and Apple’s latest Ceramic Shield equivalent.

Display

Screen real estate is identical at 6.9 inches. The Galaxy S26 Ultra uses a QHD+ Dynamic LTPO AMOLED 2X panel (3120 x 1440 resolution) with 1-120Hz adaptive refresh, HDR10+ support and peak brightness around 2,600 nits. Anti-reflective coating minimizes glare, though some early feedback notes it falls short of predecessors in certain lighting.

The iPhone 17 Pro Max features a 6.9-inch LTPO Super Retina XDR OLED (2868 x 1320) with ProMotion 120Hz, Dolby Vision, HDR10 and up to 3,000 nits peak brightness. Apple’s display excels in color accuracy, outdoor visibility and consistency, often edging out competitors in calibrated tests.

Performance and AI

Under the hood, the Galaxy S26 Ultra runs Qualcomm’s Snapdragon 8 Elite Gen 5 customized for Galaxy on a 3nm process, delivering claimed 19% faster CPU, 24% better GPU and 39% improved NPU for AI tasks. It pairs with 12GB or 16GB RAM options.

The iPhone 17 Pro Max uses Apple’s A19 Pro chip (also 3nm), optimized for efficiency and thermal management with a vapor chamber cooling system. Benchmarks show tight competition, with Samsung pulling ahead in raw multi-core and gaming scenarios, while Apple’s silicon shines in sustained performance and optimized app ecosystems.

Both emphasize on-device AI: Galaxy AI offers advanced generative tools, real-time editing and Bixby enhancements on One UI 8.5 (Android 16 base), while Apple Intelligence powers Siri upgrades, photo tools and contextual features in iOS 19 or later.

Camera Systems

Photography remains a battleground. The Galaxy S26 Ultra boasts a 200MP main (f/1.4 for superior low-light), 50MP ultrawide (f/1.9), 10MP 3x telephoto and 50MP 5x periscope, plus 12MP front camera. Upgrades include brighter apertures, enhanced Nightography and steadier video with APV codec support.

The iPhone 17 Pro Max counters with three 48MP sensors: main Fusion with second-gen sensor-shift OIS, ultrawide and a new telephoto with tetraprism design offering up to 8x optical-quality zoom (longest ever on iPhone) and 200mm equivalent focal length. An 18MP front camera improves selfies. Early side-by-side tests show Samsung leading in zoom versatility and detail at high resolutions, while Apple often wins in natural color science, video stabilization and consistency.

Battery and Charging

Battery life favors Apple. The iPhone 17 Pro Max delivers up to 39 hours of video playback thanks to a larger capacity (around 5,088mAh or more via internal redesign) and efficient chip. Real-world tests confirm exceptional endurance.

The Galaxy S26 Ultra’s 5,000mAh cell offers solid all-day use (up to 31 hours video), but shines in charging: 60W wired (full charge in under an hour) versus Apple’s 25-30W wired and 25W wireless. Reverse wireless charging adds utility.

Software and Ecosystem

iOS on the iPhone provides seamless integration with Mac, iPad, Apple Watch and services like iMessage, FaceTime and AirDrop. Long-term support stretches years with consistent updates.

Android on Samsung offers customization, multitasking, DeX desktop mode and broader app sideloading. Seven years of OS and security updates match Apple’s commitment. Ecosystem loyalty often decides: Android users gain more flexibility, while iOS users benefit from polished continuity.

Pricing and Availability

Galaxy S26 Ultra launched February 25, 2026, with availability from March 11. iPhone 17 Pro Max has been on sale since September 2025, giving it a head start in real-world reviews.

Verdict

No clear “better” phone exists — it hinges on preference. The Galaxy S26 Ultra appeals to those wanting stylus support, faster charging, higher-resolution zoom and privacy features like the built-in Privacy Display that blacks out side views. Its refinements make it feel more complete for Android loyalists.

The iPhone 17 Pro Max excels in battery life, video prowess, thermal efficiency and ecosystem polish, making it ideal for users invested in Apple or prioritizing longevity per charge.

Both represent pinnacles of 2026 smartphone tech. Potential buyers should consider test drives, ecosystem fit and priorities like photography style or daily endurance before choosing.

Business

Dell Technologies Stock Surges 20% on Blowout Q4 Earnings, AI Server Boom Drives Record Results

Dell Technologies Inc. (NYSE: DELL) shares soared more than 20% on February 27, 2026, after the company reported record fourth-quarter and full-year fiscal 2026 results, fueled by explosive demand for AI-optimized servers. The performance capped a transformative year for the technology giant, with executives highlighting surging enterprise and cloud provider orders as evidence of Dell’s leadership in the artificial intelligence infrastructure market.

![]()

Dell closed the trading day up approximately 21.9% at around $148, with intraday highs reaching $148.25, marking one of the stock’s strongest single-day gains in recent history. Volume exceeded 18 million shares, more than double the average. The rally followed the February 26 after-hours release of fiscal fourth-quarter results ended January 30, 2026, which significantly exceeded Wall Street expectations.

For the quarter, Dell posted revenue of $33.38 billion, a 39.5% increase from the prior year and well above the consensus estimate of about $31.6 billion to $31.9 billion. Adjusted earnings per share came in at $3.89, topping analyst forecasts of $3.53 and representing a 45% year-over-year jump. Net income rose to $2.25 billion, or $3.37 per share, from $1.53 billion, or $2.15 per share, a year earlier.

The Infrastructure Solutions Group (ISG), which includes servers and storage, led the charge with revenue of $19.6 billion, up 73% year over year. Within that segment, AI-optimized server revenue hit a record $9 billion for the quarter — a staggering 342% increase — while traditional servers and networking grew 27% to $5.9 billion. Executives noted that the company booked $34.1 billion in AI orders during the period and shipped more than $9.5 billion in AI servers, entering fiscal 2027 with a record $43 billion backlog. Full-year fiscal 2026 AI-optimized server revenue reached about $24.7 billion, with cumulative orders surpassing $64 billion.

For the full fiscal year 2026, Dell achieved record revenue of $113.5 billion, up 19% from the previous year, and non-GAAP diluted EPS of $10.30, a 27% increase. The company generated record cash flow from operations, returning $7.5 billion to shareholders through buybacks and dividends, and ended the year with $13.3 billion in cash and investments.

Looking ahead, Dell provided aggressive guidance that further fueled investor enthusiasm. For fiscal 2027, the company projects revenue between $138 billion and $142 billion — far exceeding analyst expectations around $124.7 billion — and expects AI server revenue to approximately double to $50 billion, representing 103% growth. First-quarter fiscal 2027 revenue is guided to between $34.7 billion and $35.7 billion, with adjusted EPS around $2.90.

CEO Michael Dell and COO Jeff Clarke emphasized the AI opportunity as a defining force. “FY26 was a defining year in our company’s history,” Clarke said in the earnings release. “We delivered record full-year revenue and EPS… The AI opportunity is transforming our company.” Management highlighted differentiated engineering, broad-based demand from enterprises and Tier 2 cloud providers, and disciplined execution amid supply constraints, including a noted memory shortage impacting the industry.

Analysts responded swiftly with upward revisions. Mizuho raised its price target to $180 from $175 with an “outperform” rating, implying significant upside. J.P. Morgan increased its target to $165, forecasting at least 36% potential rally from prior levels, while Barclays lifted to $168 and Piper Sandler adjusted to $167, both maintaining overweight or equivalent ratings. Morgan Stanley, however, hiked its target modestly to $110 while keeping an “underweight” stance, citing valuation concerns despite the strong results.

The surge comes amid broader market dynamics in AI infrastructure. Dell benefits from partnerships with Nvidia and others, positioning it to capture share in data center expansions. Challenges persist, including rising memory costs and supply tightness for high-bandwidth memory (HBM) used in AI systems, but executives expressed confidence in navigating these through strategic sourcing and backlog management.

Dell also announced shareholder-friendly moves: a 20% dividend increase and an additional $10 billion share repurchase authorization, signaling strong conviction in sustained cash generation and growth.

The stock’s performance reflects a shift from earlier 2025 volatility, when shares traded as low as $66.25, to new momentum driven by AI tailwinds. Year-to-date in calendar 2026, DELL has shown resilience, with the post-earnings pop pushing it toward recent highs around $168.

Investors and analysts will watch upcoming quarters for confirmation that AI server margins remain healthy and shipments track toward the ambitious $50 billion target. Dell’s next earnings are expected in late May or early June for the first quarter of fiscal 2027.

As AI adoption accelerates globally, Dell’s results underscore its pivot from traditional PC and enterprise hardware to a high-growth AI infrastructure player, potentially reshaping its valuation trajectory in the years ahead.

Rolls-Royce increased shareholder returns with a multiyear share buyback program of up to around $12 billion and raised its targets for 2028 after earnings grew last year.

The U.K. engine maker said Thursday that its strong balance sheet allowed it to launch a buyback program of between 7 billion and 9 billion pounds ($9.49 billion-$12.20 billion) for 2026-2028, with 2.5 billion pounds of share repurchases to be completed this year.

Copyright ©2026 Dow Jones & Company, Inc. All Rights Reserved. 87990cbe856818d5eddac44c7b1cdeb8

Significant charges in brown goods business drag down earnings.

GameStop Corp. (NYSE: GME) shares traded in a narrow range around $24 in late February 2026, reflecting cautious investor sentiment following a period of volatility driven by CEO Ryan Cohen’s aggressive push toward strategic acquisitions and the company’s robust cash reserves.

As of February 27, 2026, GME closed at $24.03, down 0.29% on moderate volume of about 1.2 million shares. The stock opened at $23.79, reached a high of $24.22 and dipped to a low of $23.70 during the session. This stability comes after a slight pullback from recent peaks near $25 earlier in the month, with the shares up roughly 20% year-to-date in calendar 2026 but still well below the meme-stock frenzy highs of prior years.

GameStop’s market capitalization hovers around $10.7 billion, supported by a cash pile exceeding $8.8 billion as reported in the most recent filings. The company’s balance sheet strength stems from disciplined cost-cutting, reduced store footprint and opportunistic capital raises during past surges. Analysts note that this liquidity positions GameStop uniquely among traditional retailers, enabling potential transformative moves under Cohen’s leadership.

GETTY IMAGES NORTH AMERICA / Michael M. Santiago

Cohen, who became chairman in 2021 and assumed the CEO role in September 2023, has emphasized turning GameStop into a more agile, value-oriented entity. In January 2026, the board approved a long-term performance award granting Cohen options to purchase over 171.5 million shares at $20.66 each. The package ties significant compensation to ambitious market capitalization milestones: 7.1% for reaching $80 billion, scaling up to 15% at $100 billion. Cohen recused himself from the board’s deliberations on the award, which requires shareholder approval.

The incentive aligns Cohen’s interests with massive upside potential, though it has drawn scrutiny for its scale and lack of base salary. Cohen has publicly criticized “risk-free insiders” and bureaucratic boardrooms, signaling a preference for bold, entrepreneurial strategies over incremental retail tweaks.

Recent months have seen heightened speculation about a “very big” consumer megadeal. In late January 2026 interviews and statements, Cohen hinted at pursuing a transformative acquisition that could “increase the company’s value tenfold.” Reports suggest interest in consumer-facing assets or technology plays to pivot beyond legacy video game retail. While no deal has materialized, the rhetoric has fueled periodic rallies, including an 8.25% jump on February 2 amid acquisition rumors.

GameStop’s most recent financials, from the third quarter ended November 1, 2025 (fiscal Q3 2025), showed net sales of $821 million, down 4.6% year over year from $860.3 million. However, operating income swung to $41.3 million from a $33.4 million loss, driven by lower selling, general and administrative expenses ($221.4 million versus $282 million). Adjusted operating income reached $52.1 million. Net income climbed to $77.1 million, bolstered by interest income and other factors.

The company also disclosed Bitcoin holdings valued at $519.4 million, adding an unconventional asset to its treasury strategy. Cash, equivalents and marketable securities totaled $8.8 billion, up substantially from the prior year.

Investors await the fiscal fourth-quarter and full-year 2025 results, expected around March 24, 2026. Consensus estimates project modest EPS, though variability remains high due to the stock’s meme-driven nature.

Broader industry context includes cautious optimism for video games. Circana forecasts U.S. industry spending to rise 3% to $62.8 billion in 2026, but GameStop faces structural headwinds from digital downloads, streaming and competition from Amazon, Best Buy and direct publisher sales.

Retail investor interest persists on platforms like Reddit’s WallStreetBets, where GME remains a focal point. Options activity has been elevated at times, contributing to short squeezes in the past, though short interest has moderated compared to 2021 peaks.

Analyst coverage remains limited and polarized. Some see the cash hoard and Cohen’s track record (from Chewy) as undervalued catalysts, with outlier fair-value estimates reaching $220 in discounted cash flow models under optimistic growth assumptions. Others point to declining core sales, high valuation multiples (forward P/E around 27 based on trailing EPS of $0.88) and execution risks in pivoting the business.

The stock’s 52-week range spans $19.93 to $35.81, with the latter hit in May 2025 during a brief resurgence. Year-to-date performance in 2026 shows resilience, up about 20% from January levels around $20.

As GameStop navigates its next chapter, attention centers on whether Cohen can deliver on acquisition ambitions without diluting shareholder value. With substantial dry powder and a motivated leader, the company could either evolve into a diversified holding entity or face challenges proving sustainable profitability in a shrinking physical retail segment.

Traders and long-term holders alike monitor for catalysts like deal announcements or earnings surprises. For now, GME trades in a consolidation phase, balancing speculative hope against fundamental retail realities in an evolving gaming landscape.

Gold prices slipped in early trading but remained above $5,100 a troy ounce as investors look ahead to U.S.-Iran talks later on Thursday.

New York futures fall 0.7% to $5,191.60 an ounce, with gains tempered by concerns that U.S. interest rates could remain on hold for some time.

Still, the metal is up more than 3.5% on the week, supported by renewed uncertainty around U.S. trade policy and geopolitical tensions with Iran.

Business

Applied Optoelectronics Stock Explodes 45% on Stellar Q4 Earnings Beat, Bullish AI-Driven Guidance

Shares of Applied Optoelectronics Inc. (NASDAQ: AAOI) surged as much as 45% on February 27, 2026, reaching new 52-week highs above $79 in intraday trading, after the optical networking company reported stronger-than-expected fourth-quarter results and issued robust guidance fueled by accelerating demand for high-speed data center transceivers amid the AI infrastructure boom.

The stock closed the previous day at $53.69 before the earnings release, but opened sharply higher and traded in a range from about $65.57 to $79.50, with volume exceeding 16 million shares — well above the average. By midday February 27, AAOI was changing hands around $77-78, reflecting a gain of more than 44% from the prior close and pushing the company’s market capitalization above $5 billion.

The rally was triggered by Applied Optoelectronics’ February 26 after-hours release of fiscal fourth-quarter and full-year 2025 results ended December 31, 2025. Revenue reached a record $134.3 million, up 34% from $100.3 million in the year-ago quarter and surpassing analyst estimates around $128 million to $132 million. The beat was driven by strong growth in data center products, which benefit from hyperscale operators expanding AI capabilities with 400G and emerging 800G optical modules.

On a GAAP basis, the company posted a net loss of $2.0 million, or $0.03 per share, a dramatic improvement from a $119.7 million loss the prior year. Adjusted (non-GAAP) earnings per share came in at a loss of $0.01, beating consensus expectations for a loss of about $0.11. Gross margin expanded to 31.2% GAAP (31.4% non-GAAP), reflecting better product mix and manufacturing efficiencies.

For the full year 2025, revenue soared 83% to $455.7 million from $249.4 million in 2024, while the net loss narrowed significantly to $38.2 million from $186.7 million. Data center revenue climbed 32% to $196 million, and cable television (CATV) revenue nearly tripled to $245 million, highlighting diversified end-market strength.

CEO Thompson Lin struck an optimistic tone during the earnings call, emphasizing momentum heading into 2026. “We have considerable momentum entering 2026, and we believe we are well positioned to accelerate our growth this year,” he said. Management highlighted the ramp-up of next-generation 800G products, capacity expansions including a new 210,000-square-foot manufacturing facility in Sugar Land, Texas, and first volume orders secured for advanced transceivers.

Guidance further ignited investor enthusiasm. For the first quarter of 2026, Applied Optoelectronics projected revenue between $150 million and $165 million — well above Street estimates near $145 million — with non-GAAP EPS ranging from a loss of $0.09 to breakeven. The company also raised its full-year 2026 outlook, targeting revenue over $1 billion (versus consensus around $834 million) and operating margins of 12% (above the 8% consensus).

On the call, executives projected that if hyperscale demand and 800G ramps continue as anticipated, monthly production could equate to an annualized run rate approaching $378 million by mid-2027, with demand potentially outstripping supply through that period. This supply-constrained narrative reframed the story from episodic growth to a multi-year opportunity in AI-driven optical interconnects.

Analysts responded with swift upgrades and target increases. Needham & Company boosted its price target to $80 from $43, maintaining a buy rating. Rosenblatt raised its target to $125 from $75 on the improved outlook. B. Riley upgraded the stock from sell to neutral, lifting its target to $54 from $15. Other firms followed suit, with some implying significant further upside despite the rapid run-up.

The company also announced a $250 million at-the-market (ATM) equity offering program on February 26, providing flexibility to raise capital opportunistically amid the stock’s strength. While such moves can dilute shareholders, the timing amid high valuation suggests confidence in funding expansion without immediate pressure.

Applied Optoelectronics specializes in fiber-optic networking products, including transceivers, lasers and subsystems for data centers, telecom, CATV and fiber-to-the-home markets. Its positioning in high-speed optical modules positions it to capitalize on AI data center buildouts by major hyperscalers, where bandwidth demands continue to escalate.

Challenges remain, including supply chain constraints for components, competition from larger players and execution risks in scaling 800G production. Some analysts noted a one-quarter delay in certain 800G revenue contributions but viewed the overall trajectory positively.

The post-earnings surge marks a continuation of AAOI’s volatile but upward trend in recent years, with the stock up more than 700% over the past 12 months from lows near $9.71. The 52-week range now extends to $79.50, reflecting renewed interest in optical component suppliers tied to AI infrastructure spending.

Investors will monitor upcoming quarters for evidence that revenue ramps track guidance and margins hold amid capacity investments. The next earnings report is expected in early May for the first quarter of 2026.

As AI adoption drives unprecedented data center expansion, Applied Optoelectronics’ results and forward-looking commentary underscore its emerging role in enabling next-generation connectivity, potentially sustaining momentum for the stock in the months ahead.

Nearly 19 million of Nepal’s 30 million people are eligible to vote in the March 5 election for the 275-member house of representatives. About one million of the voters, most of them youth, were included since last year’s protests.

While direct contest will decide 165 seats, the rest will be decided through proportional representation, where seats are allocated to parties in proportion to their vote share.

Jobs and economy are key issues in this election particularly for the youth, Kathmandu-based sources told ET. India will be watching the outcome of the elections closely given its strategic and economic interests in the Himalayan state. China, too, will keep an eye and would prefer to deal with an established political party, preferably the Communists and Maoists, according to Nepal watchers.

Nepal’s largest trading partner is India, accounting for 63% of imports, or $8.6 billion, followed by China at 13%, or $1.8 billion, according to World Bank figures. Over the last few years, India and Nepal have been able to create hydel power partnership, aiming to replicate the India-Bhutan model in future.

Rapper-turned-politician and former Kathmandu mayor Balendra Shah of Rastriya Swatantra Party is among the frontrunners for prime minister. He is in direct contest with four-time prime minister Oli of Communist Party of Nepal (Unified Marxist-Leninist).

Oli has an uphill task of getting support from the youth, which had overthrown his government through the street protests. Other contenders include Nepali Congress party’s 49-year-old Gagan Thapa. Former PM and ex-Maoist leader Prachanda may not be eyeing the top post but is active in the election process.

Police braced for TikTok ‘school wars’ spreading across London

The $1.6 Trillion Meltdown That Swept Through Software Stocks

Trump Plans Cuba Takeover, Iran War Heat Drives Bitcoin Crash

Smart energy pays enters the US market, targeting scalable financial infrastructure

Why Israel is blocking foreign journalists from entering

Bitcoin: We’re Entering The Most Dangerous Phase

Bank related Financial Frauds Useful Tips || #bank #money #scam #cybercrime

Do these 5 things to become a millionaire..!! #finance #daveramsey #money

Altseason Starting? Bull Trap or Relief Rally Explained | Crypto Market Update | Bitcoin Update?

-

Politics6 days ago

Politics6 days agoBaftas 2026: Awards Nominations, Presenters And Performers

-

Sports4 days ago

Sports4 days agoWomen’s college basketball rankings: Iowa reenters top 10, Auriemma makes history

-

Politics4 days ago

Politics4 days agoNick Reiner Enters Plea In Deaths Of Parents Rob And Michele

-

Business3 days ago

Business3 days agoTrue Citrus debuts functional drink mix collection

-

Politics20 hours ago

Politics20 hours agoITV enters Gaza with IDF amid ongoing genocide

-

Crypto World4 days ago

Crypto World4 days agoXRP price enters “dead zone” as Binance leverage hits lows

-

Business5 days ago

Business5 days agoMattel’s American Girl brand turns 40, dolls enter a new era

-

Business5 days ago

Business5 days agoLaw enforcement kills armed man seeking to enter Trump’s Mar-a-Lago resort, officials say

-

NewsBeat2 days ago

NewsBeat2 days agoManchester Central Mosque issues statement as it imposes new measures ‘with immediate effect’ after armed men enter

-

NewsBeat2 days ago

NewsBeat2 days agoCuba says its forces have killed four on US-registered speedboat | World News

-

Tech3 days ago

Tech3 days agoUnsurprisingly, Apple's board gets what it wants in 2026 shareholder meeting

-

NewsBeat4 days ago

NewsBeat4 days ago‘Hourly’ method from gastroenterologist ‘helps reduce air travel bloating’

-

Tech5 days ago

Tech5 days agoAnthropic-Backed Group Enters NY-12 AI PAC Fight

-

NewsBeat5 days ago

NewsBeat5 days agoArmed man killed after entering secure perimeter of Mar-a-Lago, Secret Service says

-

Politics5 days ago

Politics5 days agoMaine has a long track record of electing moderates. Enter Graham Platner.

-

Business2 days ago

Business2 days agoDiscord Pushes Implementation of Global Age Checks to Second Half of 2026

-

NewsBeat3 days ago

NewsBeat3 days agoPolice latest as search for missing woman enters day nine

-

Sports4 days ago

Sports4 days ago2026 NFL mock draft: WRs fly off the board in first round entering combine week

-

Crypto World3 days ago

Crypto World3 days agoEntering new markets without increasing payment costs

-

Business23 hours ago

Business23 hours agoOnly 4% of women globally reside in countries that offer almost complete legal equality