Crypto World

TruStage pilots TSDA dollar stablecoin for U.S. credit unions

TruStage pilots TSDA runs through H1 2026, leveraging GENIUS Act-driven stablecoin growth and $2t cap forecasts.

Summary

- TSDA is a dollar-pegged stablecoin with 1:1 cash reserves for U.S. credit unions.

- Pilot runs through H1 2026, focusing on loans, P2P, cross-border and inter-union settlement use cases.

- GENIUS Act and forecasts of a $2t stablecoin market by 2028 frame TSDA’s regulatory and macro backdrop.

TruStage has announced a pilot program for a dollar-pegged stablecoin targeting US credit unions, representing one of the sector’s largest coordinated efforts to test blockchain-based payments infrastructure, according to the company.

The TruStage Stablecoin, designated as TSDA, will be issued through a partnership with Block Time Financial. A TruStage affiliate will serve as issuer and manage one-to-one cash reserves backing the token, while Block Time will provide operational support, including security protocols and digital account capabilities, the company stated.

The pilot program is scheduled to run through the first half of 2026, with TruStage recruiting credit unions to participate. The company said TSDA is designed for loan funding and settlement, peer-to-peer transfers, cross-border payments and inter-credit union disbursements.

TruStage, founded in 1935, works with approximately 93 percent of US credit unions, offering insurance, retirement and investment products tailored to the sector. Company executives said interest in stablecoin solutions has accelerated following passage of the GENIUS Act, which established federal standards for stablecoin issuers.

Lawmakers continue debating broader crypto market structure legislation, with some banking and credit union groups raising concerns that yield-bearing stablecoins could draw deposits away from traditional accounts, according to industry reports.

Analysts at Standard Chartered have projected total stablecoin market capitalization could reach $2 trillion by 2028, potentially increasing demand for US Treasury securities that often back dollar-linked tokens.

Magic Eden, the prominent NFT marketplace best known for its deep roots in the Solana blockchain ecosystem, is set to close its Bitcoin and EVM-based trading platforms and discontinue support for its multi-chain wallet.

Summary

- Magic Eden plans to shut down its Bitcoin and EVM NFT marketplaces in early March 2026, ending broader multi-chain support.

- The platform will continue supporting Solana-based assets, doubling down on its original ecosystem.

- Users need to withdraw assets from closing markets and the multi-chain wallet before termination dates.

Magic Eden refocuses on Solana, winds down Bitcoin and EVM services

Magic Eden originally rose to prominence by offering a user-friendly platform for buying, selling, and trading digital collectibles, especially non-fungible tokens (NFTs), on the high-throughput Solana network.

Over time, the platform expanded into Bitcoin Ordinals and Ethereum Virtual Machine (EVM) chains such as Ethereum, Polygon, and Avalanche in an effort to capture a broader share of the burgeoning NFT market.

However, new reports say the company will begin shutting down its Bitcoin and EVM marketplaces in the first week of March 2026, with its cross-chain wallet entering export-only mode by mid-March and fully ceasing service in early April. Support for Solana-based NFTs and assets will continue uninterrupted.

The move could be a strategic realignment rather than a retreat.

By concentrating on its core Solana busines, where the majority of its trading volume has historically originated, Magic Eden aims to streamline operational complexity and refocus engineering resources on strengthening features, liquidity, and community engagement within its original ecosystem.

Affected users are being urged to withdraw any assets held in the Bitcoin and EVM marketplaces or within the multi-chain wallet before support ends to avoid the risk of losing access. As the NFT sector evolves, Magic Eden’s decision highlights broader market trends toward specialization and platform consolidation.

TLDR:

- OpenAI signed a deal to deploy AI models on U.S. Department of War classified networks on Feb. 28, 2026.

- The agreement bans domestic mass surveillance and requires human control over lethal force decisions.

- Anthropic reportedly refused a similar Pentagon deal, citing autonomous weapons and surveillance risks.

- Backlash on X was swift, with thousands of users announcing plans to cancel ChatGPT subscriptions.

OpenAI has agreed to deploy its AI models on classified U.S. Department of War networks, CEO Sam Altman announced. The deal follows reports that Anthropic publicly declined similar Pentagon demands over autonomous weapons and surveillance concerns.

Altman posted the announcement to X, where it quickly drew millions of views and thousands of replies. The reaction online was largely critical, with many users threatening to cancel their ChatGPT subscriptions.

OpenAI and the Department of War Reach Classified AI Agreement

The agreement allows OpenAI models to operate within DoW classified systems under specific conditions.

Altman stated the deal includes explicit prohibitions on domestic mass surveillance. It also requires human oversight for any use of force, including autonomous weapons systems. Deployment will occur on cloud networks only, with OpenAI personnel embedded to monitor model behavior.

Altman noted on X that the DoW agreed with these core safety principles.

According to the post, those principles are also reflected in existing law and policy. OpenAI said it will build technical safeguards to keep models aligned with the agreement’s terms. The company also called on the DoW to extend the same terms to all AI companies.

Altman framed the deal as part of a broader effort to reduce friction between AI companies and the government. He wrote that OpenAI wants to move away from legal and governmental conflicts.

The announcement signals a shift toward negotiated frameworks rather than standoffs. OpenAI described its mission as serving all of humanity amid a “complicated, messy, and sometimes dangerous world.”

The post received over 11,000 likes within hours of going live. Reposts and quote replies numbered in the thousands. Despite the scale of engagement, most visible reactions skewed negative.

Anthropic’s Refusal Puts Spotlight on OpenAI’s Pentagon Move

Reports from the previous day indicated Anthropic CEO Dario Amodei refused similar Pentagon demands. The refusal reportedly centered on concerns about enabling mass surveillance and autonomous weapons.

Amodei allegedly offered to help the DoW transition to another provider rather than comply. That stance drew widespread praise from AI safety advocates and researchers.

OpenAI’s subsequent agreement was widely read as stepping into the gap Anthropic left. Critics on X accused the company of opportunism. Several users announced they were switching from ChatGPT to Claude. Some described the move as contradicting OpenAI’s own stated safety values.

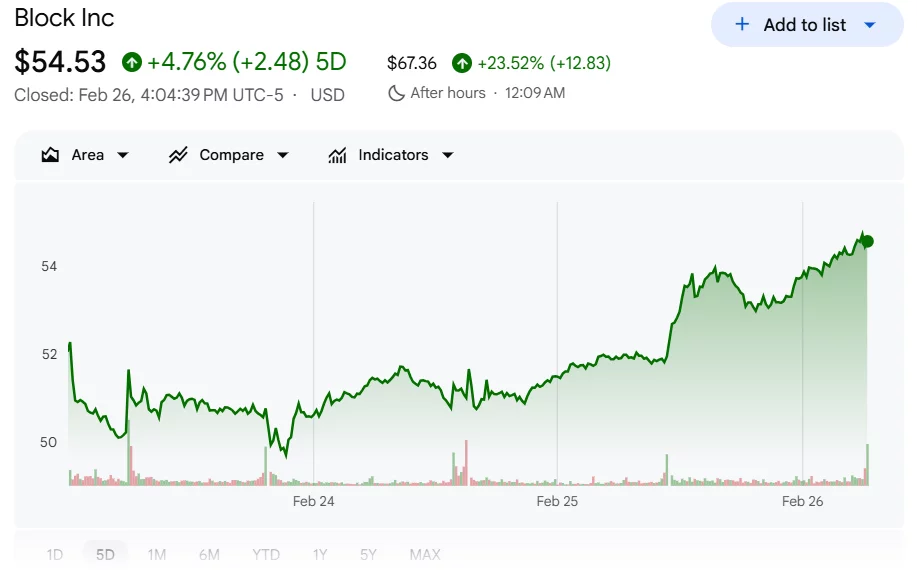

Block, Inc. will reduce its workforce by nearly half, cutting more than 4,000 jobs as CEO Jack Dorsey said the fintech firm restructures around artificial intelligence and leaner teams.

Summary

- Block, Inc. will cut over 4,000 jobs, reducing headcount from 10,000+ to under 6,000 in one of its largest corporate overhauls.

- CEO Jack Dorsey says the move reflects a strategic pivot toward intelligence tools and flatter, more efficient teams — not financial distress.

- Investors responded enthusiastically, sending Block shares up more than 23% in after-hours trading.

Wall Street cheers Jack Dorsey’s AI restructure

In a note shared publicly, Jack Dorsey said the company will shrink from over 10,000 employees to just under 6,000. He described the move as “one of the hardest decisions in the history of our company,” adding that affected employees would be notified the same day.

Despite the scale of the layoffs, Dorsey emphasized that Block is not facing financial distress. He said gross profit continues to grow, customer numbers are rising, and profitability is improving.

Instead, he framed the cuts as a proactive shift driven by the rapid advancement of intelligence tools that are reshaping how companies are built and operated.

“We’re already seeing that the intelligence tools we’re creating and using, paired with smaller and flatter teams, are enabling a new way of working,” Dorsey wrote, arguing that acting decisively now would avoid repeated rounds of layoffs that could damage morale and trust.

Employees leaving the company will receive 20 weeks of salary plus an additional week per year of tenure, equity vesting through the end of May, six months of healthcare coverage, their corporate devices, and $5,000 in transition support. Terms will vary internationally depending on local regulations.

Dorsey said internal communication channels would remain open through Thursday evening to allow departing staff to say goodbye, and he plans to host a live video session to address employees directly.

The market’s reaction to Jack Dorsey’s “leaner, meaner” pivot was nothing short of explosive. As news broke regarding the reduction of 4,000 roles, Block Inc. shares ignited in after-hours trading, surging by more than 23%.

The chart reflects a dramatic vertical shift as investors pivoted from uncertainty to overwhelming optimism, interpreting the layoffs not as a sign of corporate distress, but as a commitment to long-term profitability and AI-driven efficiency.

Disgraced FTX founder Sam Bankman-Fried has reignited controversy from prison after publicly endorsing the proposed CLARITY Act, calling it a “huge milestone for crypto” and “a huge achievement” for Donald Trump.

Summary

- Sam Bankman-Fried praised the CLARITY Act and credited Donald Trump, triggering immediate criticism from U.S. senators.

- Cynthia Lummis dismissed SBF’s comments and suggested the legislation would not benefit him legally.

- Elizabeth Warren warned that SBF’s backing should concern lawmakers debating crypto market structure reform.

Sam Bankman-Fried backs CLARITY Act, draws swift rebuke from Lummis and Warren

In a post on X, Bankman-Fried claimed he had championed similar legislation aimed at limiting the regulatory authority of former SEC Chair Gary Gensler before his prosecution. He suggested that Gensler “helped Biden’s DOJ put me behind bars,” reviving familiar allegations that his case was politically influenced.

The comments quickly drew bipartisan backlash.

Senator Cynthia Lummis responded sharply, writing: “Someone’s looking for a pardon and doesn’t realize the CLARITY Act would have you locked up for much longer than 25 years.”

She added that her crypto legislation differs fundamentally from what she described as the bill Bankman-Fried “tried to buy from Congress” in 2022. “We do not need—nor want—your support,” she said.

Senator Elizabeth Warren also weighed in, warning that Bankman-Fried’s endorsement should “set off alarm bells.” Warren reiterated her stance that any crypto market structure legislation must prioritize investor protection and financial stability.

Bankman-Fried, who is serving a lengthy federal sentence following his conviction over the collapse of FTX, has recently attempted to re-enter public discourse through media outreach and social media commentary. Previous efforts to sway political opinion, including outreach linked to Trump, have largely failed to gain traction.

The episode shows the heightened political sensitivity surrounding crypto regulation, particularly as lawmakers debate market structure reforms amid lingering fallout from FTX’s multibillion-dollar collapse.

Federal authorities have arrested Christopher Alexander Delgado, the founder and CEO of Goliath Ventures, on federal charges tied to an alleged $328 million Ponzi crypto scam, the U.S. Department of Justice announced.

Summary

- Goliath Ventures CEO Christopher Delgado was arrested on federal wire fraud and money laundering charges tied to a $328 million Ponzi scheme.

- Prosecutors say investors were promised monthly crypto returns, but funds were diverted to pay earlier investors and support Delgado’s luxury lifestyle.

- If convicted, Delgado faces up to 30 years in prison; authorities are reaching out to victims under the Crime Victims’ Rights Act.

Goliath Ventures CEO arrested in $328M crypto scam

Delgado, 34, of Apopka, Florida, was taken into custody on a criminal complaint filed in the United States District Court for the Middle District of Florida, where he is charged with wire fraud and money laundering.

If convicted on all counts, he could face up to 30 years in federal prison.

Prosecutors allege Delgado’s scheme ran from January 2023 through January 2026, during which he solicited investors to put money into purported cryptocurrency “liquidity pools” that promised steady monthly returns. In reality, federal officials say only about $1 million of the funds was actually invested in legitimate crypto assets.

The bulk of the more than $300 million collected from victims was used to pay earlier investors and finance Delgado’s lavish lifestyle, including luxury travel, company-sponsored events, and purchases of multi-million-dollar homes in central Florida.

According to court filings, victims were drawn in through personal referrals, slick marketing materials, and high-end networking events aimed at projecting legitimacy. At the scheme’s unraveling, investors seeking withdrawals were met with delays, inconsistent explanations, and restricted access to account information.

Federal law enforcement agencies including IRS Criminal Investigation and Homeland Security Investigations spearheaded the probe. Victims are being notified of their rights under the Crime Victims’ Rights Act, and authorities have invited potentially unidentified victims to come forward.

The arrest marks one of the largest alleged crypto-related fraud cases in recent years and underscores ongoing regulatory and criminal scrutiny of digital asset investment schemes.

An autonomous AI security tool caught a bug in the XRP Ledger that, if left undetected, could have let an attacker steal funds from any account on the network without ever touching the victim’s private keys.

The vulnerability, disclosed Thursday by XRPL Labs, sat in the signature-validation logic of the Batch amendment, a pending upgrade that would allow multiple transactions to be bundled and executed together.

The amendment was still in its voting phase among validators and had not been activated on mainnet, meaning no funds were ever at risk. But the exploit path was about as bad as it gets for a blockchain.

Here’s what the bug did in plain terms. Batch transactions let users bundle several operations into one. Because the individual transactions inside the batch don’t carry their own signatures, the system relies on a list of batch signers to confirm that every account involved has authorized the bundle.

The validation function that checked those signers had a critical loop error. If it encountered a signer whose account didn’t yet exist on the ledger, and whose signing key matched their own account — the normal case for a brand-new account — it immediately declared the entire check successful and stopped looking at the rest of the list.

An attacker could exploit this by constructing a batch with three transactions. The first creates a new account the attacker controls. The second is a simple transaction from that new account, making it a required signer. The third is a payment from the victim’s account to the attacker.

Because the new account doesn’t exist yet when validation runs, the signer check exits early after the first entry and never verifies the second. The victim’s funds move without their keys ever being involved.

Pranamya Keshkamat and Cantina AI’s autonomous security tool Apex identified the flaw through static analysis of the codebase on Feb. 19 and submitted a responsible disclosure. Ripple’s engineering team validated the report the same evening with an independent proof-of-concept.

The response was fast. Validators on the network’s Unique Node List were immediately advised to vote “No” on the amendment.

An emergency release, rippled 3.1.1, was published on Feb. 23, marking both the Batch and the related fixBatchInnerSigs amendments as unsupported to prevent them from ever activating. A corrected replacement called BatchV1_1 has been built and is under review, with no release date set.

The fact that an AI tool found this is notable on its own.

XRPL Labs said it would add AI-assisted code audit pipelines as a standard step in its review process going forward, alongside expanded static analysis specifically designed to catch the kind of premature loop exits that caused this bug.

Bitcoin’s attempt to reclaim $70,000 earlier in the week lasted about 48 hours.

The largest cryptocurrency slid to $65,735 in early Asian hours on Saturday, down 3% over the past day and 2.8% on the week. Wednesday’s rally, which came within touching distance of $70,000, has now given back more than half its gains as broader risk sentiment deteriorated through Thursday and Friday’s U.S. sessions.

Altcoins took a harder hit. Solana dropped 6.7%, ether fell 6.2%, dogecoin shed 5.1%, and XRP lost 4%. The losses pushed most major tokens into the red on a weekly basis, erasing the altcoin outperformance that had been the week’s most encouraging signal. BNB held up better than most, down just 2.5%.

The trigger was familiar. Friday’s U.S. session saw the S&P 500 close down 0.4%, the Nasdaq 100 drop 0.3%, and the Dow fall 1.1%. Nvidia, still digesting its post-earnings reaction, shed another 4.2%.

A hotter-than-expected 0.5% jump in producer prices added fuel, signaling inflationary pressure that may keep the Fed from cutting rates anytime soon. Block Inc.’s massive layoffs fanned broader anxiety that AI is starting to displace jobs across the economy rather than just creating them.

Crypto followed equities lower, but as usual, with amplified magnitude. A 0.4% drop in the S&P became a 3% drop in bitcoin and a more than 6% drop in altcoins. The leverage that re-entered the system during Wednesday’s rally got flushed on the way back down.

The irony is that the institutional flow data this week was actually strong.

U.S. spot bitcoin ETFs added $1.1 billion in three days, putting them on pace for their best week in months. But ETF inflows haven’t been enough to overcome the broader macro headwinds.

“Over-analysis of short-term price movements is misguided,” said Dom Harz, co-founder of bitcoin finance firm BOB said in an email. “Bitcoin’s volatility is no surprise, particularly for early investors who have experienced previous cycles. What’s different this time is the type of capital behind the emerging asset class.”

Meanwhile, CryptoQuant data shows USDT stablecoin reserves on exchanges have fallen from $60 billion to $51.1 billion over the past two months, a decline the firm warned could trigger a “massive sell-off” if reserves drop below $50 billion.

Elsewhere, Strategy shares topped the list of large U.S. companies by short interest volume as markets increasingly question the sustainability of the firm’s debt-funded bitcoin buying program.

And on the Ethereum side, large holders have started selling at a loss, with DAT company ETHZilla officially abandoning its ETH accumulation strategy and rebranding to focus on tokenized real-world assets instead.

Bitcoin is now back in the middle of the $60,000-$70,000 range it has been stuck in since the Feb. 5 crash. Wednesday proved the top of that range is resistance. The question heading into March is whether the bottom still holds.

MetaMask and Mastercard have officially launched the MetaMask Card across the United States, marking a significant step in bringing cryptocurrency spending into everyday commerce.

Summary

- MetaMask and Mastercard begin offering the self-custodial MetaMask Card in 49 states, including New York.

- Users spend directly from their wallets, with up to 1% back in mUSD for standard users and up to 3% for premium members.

- The card works at over 150 million Mastercard merchants and supports Apple Pay and Google Pay.

New MetaMask and Mastercard card lets users spend crypto

The announcement follows successful pilot programs in Europe and the UK, and now brings the self-custodial crypto payment card to 49 U.S. states, including New York for the first time.

The MetaMask Card connects users’ self-custodied digital assets to traditional payment infrastructure, allowing holders to spend crypto directly from their wallets anywhere Mastercard is accepted, online or in physical stores, without needing to pre-load balances onto custodial accounts.

Users retain full control of their funds until the point of sale, where conversion and payment happen seamlessly.

“We designed MetaMask Card to make crypto disappear. Not go away, but become so seamlessly woven into daily life that the line between onchain and offchain fades away entirely,” said Gal Eldar, Product Lead at MetaMask.

Issued by FDIC-insured Cross River Bank and powered by Mastercard’s global network with technology from Monavate (formerly Baanx), the card works with Apple Pay and Google Pay, making it compatible with contactless digital wallets. The rollout follows a year-long U.S. trial that began in late 2024, with broader access now available nationwide.

A key feature of the program is on-chain rewards: standard MetaMask Card holders earn up to 1% back in MetaMask’s stablecoin mUSD on purchases, while premium MetaMask Metal subscribers, available for a $199 annual fee, can earn up to 3% back on the first $10,000 spent each year alongside additional travel and spending benefits.

The launch represents a strategic effort to integrate decentralized finance into traditional payment rails, making crypto use more intuitive for everyday purchases while preserving self-custody principles at the heart of Web3.

It also positions MetaMask alongside other crypto-native payment cards, expanding crypto’s real-world utility.

Spot Bitcoin exchange-traded funds pulled in more than $1 billion of net inflows over three trading sessions this week, a reversal that came even as Bitcoin remained well below its peak.

The US-listed spot Bitcoin (BTC) ETFs logged a combined $1.02 billion in inflows from Tuesday to Thursday, according to data from SoSoValue. The funds pulled in $506.51 million on Wednesday, the largest single-day total during the three days.

On Friday, ETF analyst Nate Geraci said in a post on X that investors appeared to be “buying the dip” amid the recent downturn.

He said spot Bitcoin ETFs have seen about $6.5 billion in outflows since Bitcoin’s record high in early October, a figure he described as modest relative to the $55 billion the category has absorbed since January 2024.

Related: Bitcoin’s 100 BTC club edges toward 20K wallets in a ‘bullish sign’

“50% drawdowns are walk in the park for long-time BTC investors,” Geraci wrote. “But appears newer ETF investors aren’t worried either.”

Flows reverse multi-week outflow streak

This week’s inflows follow five consecutive weeks of net withdrawals, with the last two weeks of January recording a combined $2.82 billion in outflows.

The rebound was led by BlackRock’s iShares Bitcoin Trust (IBIT), which logged $275.82 million in net inflows on Thursday alone. Fidelity’s FBTC and Ark 21Shares’ ARKB posted outflows, but were outweighed by gains in other funds including Bitwise’s BITB and Grayscale’s BTC.

Altcoin ETFs have also turned positive in recent trading sessions. Spot Ether (ETH) ETFs added about $173 million over the same three-day period, while Solana funds logged roughly $35 million in inflows. Meanwhile, XRP (XRP) ETFs logged a modest $7 million in inflows.

Related: Bitcoin bear market not over as BTC fails to reclaim $68K trend line

Analysts flag ETF flows as sentiment gauge

The inflows come as market participants discuss whether the recent selling pressure is easing. On Friday, several analysts said Bitcoin’s roughly 50% drawdown may be approaching exhaustion.

CoinEx chief analyst Jeff Ko previously told Cointelegraph that improvements in spot ETF inflows suggest aggressive selling pressure may be fading. However, he said a sudden V-shaped recovery is unlikely after a steep decline.

Bitrue research lead Andri Fauzan Adziima similarly pointed to oversold technical indicators and said sustained ETF inflows could serve as a catalyst for stabilization.

Magazine: 6 weirdest devices people have used to mine Bitcoin and crypto

Bitcoin miner MARA Holdings has announced a partnership with Starwood Property Trust to develop AI-focused data centers.

Summary

- MARA has entered a strategic partnership with Starwood Capital Group to convert select U.S. Bitcoin mining sites into AI focused hyperscale data centers.

- The joint venture will target roughly 1 gigawatt of short-term IT capacity, with plans to expand beyond 2.5 gigawatts

According to a Feb. 26 announcement, the two companies have entered into a strategic agreement to “jointly develop, finance, and operate digital infrastructure projects across MARA’s existing, power-rich portfolio.”

As part of the agreement, MARA will work with Starwood Capital Group’s data center development arm, Starwood Digital Ventures, to convert and expand select U.S. Bitcoin mining sites into hyperscale data center campuses capable of serving enterprise, cloud, and AI workloads.

“MARA’s power rich sites give customers what they need most: predictable access to energy at scale. Our partnership with Starwood will allow us to turn that power certainty into capacity certainty, so customers can run diverse workloads close to their data and users,” MARA’s Chairman and CEO Fred Thiel said in a statement.

The partnership will focus on sites that have access to low-cost energy and strong grid interconnection positions, which would then support both Bitcoin mining operations and AI-driven high-performance computing workloads.

The companies expect to deliver approximately 1 gigawatt of near-term IT capacity, with plans to scale that figure to more than 2.5 gigawatts over time.

MARA shares surged more than 15% in after-market trading following the announcement of the Starwood partnership. Shareholders perceived the joint venture as a strategic diversification move, especially after the company’s disappointing earnings report revealed a $1.7 billion quarterly net loss and falling revenues.

As previously reported by crypto.news, crypto mining stocks, including MARA, have struggled over the past months as a result of a market-wide downturn and tight profit margins.

At the same time, a powerful winter storm in January pushed Bitcoin hashrate to a seven-month low as several U.S. miners had to power down or throttle operations to ease pressure on strained electricity grids.

New song ‘The Pilgrim Way’ available across York schools

Hays plc (HAYPY) H1 2026 Sales/ Trading Statement Call – Slideshow

NFT marketplace Magic Eden exits Bitcoin and EVM trading

-

Politics6 days ago

Politics6 days agoBaftas 2026: Awards Nominations, Presenters And Performers

-

Sports4 days ago

Sports4 days agoWomen’s college basketball rankings: Iowa reenters top 10, Auriemma makes history

-

Fashion10 hours ago

Fashion10 hours agoWeekend Open Thread: Iris Top

-

Politics4 days ago

Politics4 days agoNick Reiner Enters Plea In Deaths Of Parents Rob And Michele

-

Business3 days ago

Business3 days agoTrue Citrus debuts functional drink mix collection

-

Politics1 day ago

Politics1 day agoITV enters Gaza with IDF amid ongoing genocide

-

Crypto World4 days ago

Crypto World4 days agoXRP price enters “dead zone” as Binance leverage hits lows

-

Business6 days ago

Business6 days agoMattel’s American Girl brand turns 40, dolls enter a new era

-

Business5 days ago

Business5 days agoLaw enforcement kills armed man seeking to enter Trump’s Mar-a-Lago resort, officials say

-

NewsBeat2 days ago

NewsBeat2 days agoCuba says its forces have killed four on US-registered speedboat | World News

-

Tech3 days ago

Tech3 days agoUnsurprisingly, Apple's board gets what it wants in 2026 shareholder meeting

-

NewsBeat2 days ago

NewsBeat2 days agoManchester Central Mosque issues statement as it imposes new measures ‘with immediate effect’ after armed men enter

-

NewsBeat5 days ago

NewsBeat5 days ago‘Hourly’ method from gastroenterologist ‘helps reduce air travel bloating’

-

Tech5 days ago

Tech5 days agoAnthropic-Backed Group Enters NY-12 AI PAC Fight

-

NewsBeat5 days ago

NewsBeat5 days agoArmed man killed after entering secure perimeter of Mar-a-Lago, Secret Service says

-

Politics6 days ago

Politics6 days agoMaine has a long track record of electing moderates. Enter Graham Platner.

-

Business2 days ago

Business2 days agoDiscord Pushes Implementation of Global Age Checks to Second Half of 2026

-

NewsBeat3 days ago

NewsBeat3 days agoPolice latest as search for missing woman enters day nine

-

Sports5 days ago

Sports5 days ago2026 NFL mock draft: WRs fly off the board in first round entering combine week

-

Business1 day ago

Business1 day agoOnly 4% of women globally reside in countries that offer almost complete legal equality