Video

In Real life) How to Earn Unlimited Money #shorts #shortsfeed #money

In Real life) How to Earn Unlimited Money #shorts #shortsfeed #money

Want to make crazy money?

Then you must first destroy your distractions, comfort habits, and lazy mindset.

In this video, you’ll learn:

Why fake friends, mindless scrolling, and online games are silently killing your future

How quitting movies and web series and reading daily rewires your mindset

Why starting a YouTube channel or learning a high-paying skill is non-negotiable

How turning off all phone notifications permanently boosts focus and discipline

Why closing your room door and doing deep work separates winners from losers

Why saying “I’ll start tomorrow” is the biggest sign of failure

This video is for people who:

Want real money, not motivation

Want financial freedom and a powerful mindset

Refuse to live an average life

If you’re serious about your future, success, and money—

this channel is for you.

👉 Subscribe now. This content is not for everyone.

Hashtags –

#MakeMoney #MoneyMindset

#SuccessMindset #SelfDiscipline

#Focus #Productivity

#HighPayingSkills #YouTubeGrowth

#FinancialFreedom #Motivation

#Shorts

#PsychologyHindi #Mindset #Overthinking

#SelfImprovement #LifePsychology

#SuccessMindset #motivationhindi

#shorts

#ytshorts

#youtubeshorts

#shortvideo

#viralshorts

#psychology

#mindset

#selfdiscipline

#habitchange

#addictionrecovery

#dopamine

#focus

#mentalstrength

#motivation

#hindimotivation

#successmindset

#lifeadvice

#selfimprovement

#phoneaddiction

#reelsaddiction

#scrolling

search –

how to make money fast

money mindset

success mindset

self discipline

focus and productivity

high paying skills

start a youtube channel

financial freedom

rich mindset psychology

dopamine detox

stop wasting time

hard work mindset

motivational shorts

psychology hindi

human psychology hindi

addiction control psychology, how to stop phone addiction, instagram reels addiction, pubg addiction solution, free fire addiction, dopamine addiction cure, delay gratification psychology, self discipline psychology, bad habits psychology, habit breaking technique, control urges psychology, stop wasting time on phone, focus and discipline, mindset for success, psychology of self control, motivational psychology hindi, brain hacking habits, addiction recovery mindset, productivity psychology, discipline over motivation

source

Watch More FAMILY FEUD 👉 https://www.youtube.com/playlist?list=PLftOOzq9gkniJBv7lJ1TLavb5glTMp5jJ

Discover the funniest, most surprising, and memorable Family Feud Botswana questions! 🎉🇧🇼 Watch as families from Botswana face off, answering hilarious and tricky questions for their chance to win big. Hosted by the iconic Steve Harvey, each question reveals unexpected answers and brings plenty of laughs.

Welcome to The Official FAMILY FEUD AFRICA YouTube Channel!

Families from across Africa compete in a thrilling battle of wits and humor! Join Steve Harvey as he brings laughter, surprises, and unforgettable moments to every episode. Don’t miss the action—subscribe now and stay tuned!

Like us on Facebook: www.facebook.com/FamilyFeudAfrica

Follow us on Instagram: www.instagram.com/familyfeudafrica/

Follow us on Twitter: www.twitter.com/FeudAfrica

#FamilyFeudAfrica #FamilyFeudBotswana #SteveHarvey #familyfeud

source

#bitcoin #crypto

As Bitcoin’s price rises, many wonder, ‘Why does it have value?’ Bitcoin’s value comes from the fact that it is a decentralized currency that can’t be controlled or influenced by outside sources. This puts it in opposition to the current monetary system where most currencies are controlled by a single large entity.

source

Bloomberg Live: Business, Finance, Earnings & Investment News | Watch 7AM – 6PM ET Weekdays

Subscribe to our Podcasts:

– Bloomberg News Now: http://apple.co/3Eyz9EX

– Stock Movers: https://link.podtrac.com/h0zn7xir

– Bloomberg Daybreak: http://bit.ly/3DWYoAN

– Bloomberg Surveillance: http://bit.ly/3OPtReI

– Bloomberg Intelligence: http://bit.ly/3YrBfOi

– Bloomberg Businessweek: http://bit.ly/3IPl60i

– Masters in Business: http://bit.ly/43wa4F4

– Here’s Why: https://apple.co/3Lg3RGn

– Balance of Power: http://bit.ly/3OO8eLC

– Wall Street Week: http://bit.ly/3N8ueQ0

– Bloomberg Technology: http://bit.ly/3MI0wA1

– Bloomberg Law: http://bit.ly/45Hkdk5

– Hot Pursuit!: http://apple.co/4935eTf

– Business of Sports: http://bit.ly/43itcXm

– Bloomberg Daybreak Europe: http://bit.ly/3C7o5gS

– Bloomberg Daybreak Asia: http://bit.ly/43xXR2M

Listen on Apple CarPlay and Android Auto with the Bloomberg Business app:

Apple CarPlay: https://apple.co/486mghI

Android Auto: https://bit.ly/49benZy

Follow us on Twitter: https://twitter.com/BloombergRadio

Visit our other YouTube channels:

Bloomberg Television: https://www.youtube.com/@markets

Bloomberg Originals: https://www.youtube.com/bloomberg

Quicktake: https://www.youtube.com/@Bloomberg-News

#News #politics #Live #Radio #Podcast #Bloomberg #Surveillance #Markets #Finance #investing #stocks #stockmarket #economy #economics #investing #investment #stockmarketnews #bloombergradio #recession

—————-

Bloomberg brings you live coverage of the markets open and close, plus everything you need to know across business, finance, technology, politics and more daily.

Visit http://www.bloomberg.com for business news & analysis, up-to-the-minute market data, features, profiles and more.

Connect with us on…

Twitter: https://twitter.com/business

Facebook: https://www.facebook.com/bloombergbusiness

Instagram: https://www.instagram.com/bloombergbusiness/

LinkedIn: https://www.linkedin.com/company/bloomberg-news/

TikTok: https://www.tiktok.com/@bloombergbusiness

Connect with Bloomberg Television on:

Twitter: https://twitter.com/BloombergTV

Facebook: https://www.facebook.com/BloombergTelevision

Instagram: https://www.instagram.com/bloombergtv/

source

“Crypto products and NFTs are unregulated and can be highly risky. There may be no regulatory recourse for any loss from such transactions.”

Bitcoin 11% crash & altcoins 50% down! But what really caused this massive crypto market meltdown, Bitcoin crash, and altcoin crash? In this video, we break down the real reasons behind the crypto crash, including Trump’s 100% tariff on Chinese goods, crypto mining supply chain vulnerabilities, and $19B crypto liquidations in just hours!

⚠️ What’s Different From The 2020 Crash?

👉 2020: Panic & liquidity crunch

👉 2025: Full structural breakdown

👉 Trump’s tariff directly hit Bitcoin mining hardware

👉 Supply chain crisis: 95% of mining hardware from China + rare earth shortage

👉 Mass liquidations wiped out $19B

👉 Global ripple effect: stocks down, crypto crashed harder

💡 Key Takeaways:

Why crypto is more vulnerable to geopolitical events than traditional markets

How leveraged trading and derivatives amplified the crash

What investors should watch for in Bitcoin, Ethereum, and top altcoins

📈💰 CoinDCX (Crypto) – Get 20% Discount On Brokerage Using This Link

https://join.coindcx.com/invite/Az7y2

Trade In Cypto Community – https://tinyurl.com/TradeInCrypto

💰📊 Invest In Mutual Fund SIP, SWP, Stocks | Open FREE Demat Account

https://tinyurl.com/firstpunji

🛡️ Best Term Insurance – 15% Discount – https://tinyurl.com/ssTermpb

🚑 Best Health Insurance – 25% Discount – https://tinyurl.com/ssHealthpb

#CryptoCrash #BitcoinNews #SagarSinha

———— Social Media Handles ————————————————-

Youtube – https://www.youtube.com/@coachsagarsinha

Instagram- https://www.instagram.com/coachsagarsinha/

Facebook– https://www.facebook.com/sagarsinhamotivation

Sagar Sinha Daily – https://www.youtube.com/@sagarsinhadaily

Podcast – https://www.youtube.com/@sagarsinhapodcast_

Linkedin- https://www.linkedin.com/in/coach-sagar-sinha/

Telegram – https://t.me/coachsagarsinha

Twiter(X) – https://x.com/CoachSagarSinha

WhatsApp – https://tinyurl.com/JoinSSWhatsApp

Website – https://sagarsinha.in

———————————————————————

Bazaar Ke Mahir – https://www.youtube.com/@bazaarkemahir

Email – biz.sagarsinha@gmail.com

———————————————-

Disclaimer

——————————-

This video is created solely for educational and informational purposes and is based on individual research. It should not be considered as financial, investment, or trading advice. We are not SEBI-registered investment advisors or analysts. Viewers are strongly advised to conduct their own research and consult with a SEBI-registered financial advisor before making any investment decisions.

As per SEBI’s study on the derivatives segment, nine out of ten traders in the Futures & Options (F&O) market incur losses, with the average loss-making trader losing significantly more than the profitable ones gain. Trading in derivatives involves substantial risk and is not suitable for all investors.

Regarding cryptocurrencies in India: Cryptocurrencies are currently not considered legal tender in India, but trading and holding crypto assets is not banned. However, they are unregulated, and the Government of India, RBI, and SEBI have repeatedly cautioned investors about the high volatility and risk of fraud. Crypto gains are subject to a 30% tax on profits and 1% TDS on transactions as per the current tax laws. Regulatory frameworks may change in the future, and viewers should stay updated with official guidelines before making any decisions in this space.

Stock market investments are subject to market risks, and past performance is not indicative of future results. We do not guarantee any profits or protection against losses. This content is for educational purposes only and is based on personal research. Viewers should always conduct their own due diligence before making any financial decisions.

By watching this video, you acknowledge that we and our representatives are not liable for any financial losses or decisions made based on the information provided. Always trade and invest responsibly.

source

Lately, I’ve been asking myself:

If my 8-year-old self saw me today… would she be proud?

And if my 80-year-old self could look at my financial decisions, would she feel secure?

In this video, I’m sharing the 10 realistic ways I’m improving my finances — not to look rich, not for social media, but to build long-term stability.

📌 Watch Next:

How to Prepare for Financial Glow Up: https://www.youtube.com/watch?v=64t2S-Rlo3Y&t=217s

🔔 Book Recos:

The Psychology of Money by Morgan Housel : https://s.shopee.ph/AUkiFOzzt5

Million Dollar Weekend by Noah Kagan: https://s.shopee.ph/Ldw8tFyH1

Rich Dad Poor Dad: https://s.shopee.ph/4VV7Xmwsr8

Courage To Be Disliked : https://s.shopee.ph/7V8j7NWAwJ

📲 Let’s connect!

Instagram: https://www.instagram.com/janejuanders

TikTok: https://www.tiktok.com/@janejuanders

#ManilaLife #CostOfLivingPH #AdultingPH #MoneyMindset #PersonalFinancePH

source

BUY Your OWN Bitcoin Miner TODAY! – https://bitcoinmerch.com?aff=685

▶SECURE YOUR CRYPTO w/ Arculus! (USE CODE BASE10) – https://linktw.in/TXTPAs

JOIN THE BASEMENT DISCORD – https://discord.gg/sqw5XjfDdF

●▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬●

All of our videos are strictly personal opinions. Please make sure to do your own research. Never take one person’s opinion for financial guidance. There are multiple strategies and not all strategies fit all people. Our videos ARE NOT financial advice. Digital Assets are highly volatile and carry a considerable amount of risk. Only use exchanges for trading digital assets. Never keep your entire portfolio on an exchange.

#bitcoin #ethereum #crypto #news

source

#MeshRashi #AriesHoroscope #AmlaEkadashi #Feb27 #Astrology2026 #AriesToday #SuccessTips #DailyHoroscope

source

Download Rumble Wallet now and step away from the big banks — for good! https://rumblewallet.onelink.me/bJsX/natethelawyer

At just 23 years old, he became the youngest mayor in Bogalusa’s history, promising to fight crime, invest in youth, and restore trust in city government. Now, he’s facing felony indictments tied to allegations of drug trafficking, misuse of public funds, prostitution, and public intimidation.

Authorities claim the investigation spanned months and involved social media drug sales, misuse of city resources, and financial misconduct. Supporters argue the charges are politically motivated. Prosecutors say the evidence will speak for itself.

Need a lawyer?

If you or someone you know has been injured in an accident, don’t hesitate to reach out to me. You can contact me at 1-571- NATE-LAW or visit our website www.NateTheLawyer.com

Schedule a free consultation. Remember, you don’t pay unless they win your case!

Check Out The Podcast | https://linktr.ee/natethelawyer

Spotify = https://open.spotify.com/show/67OgSDffzx4bLOeIaBwLnA?si=5f5d2c2a74db42d3

Apple = https://podcasts.apple.com/us/podcast/nate-the-lawyer/id1746189958

Join Me On The Journey To 1M Subscribers.

💖 Become a Channel Member for Perks and Specials 💖 | https://www.youtube.com/channel/UCD5_QIM67BZJdh9AwZv3soA/join

LinkTree – https://linktr.ee/natethelawyer

💥💥💥CONNECT WITH ME ON SOCIAL MEDIA 💥💥💥

➡️ FOLLOW ME ON LOCALS ➜ https://NATETHELAWYER.locals.com

➡️ FOLLOW ME ON TWITTER ➜ https://twitter.com/NATETHELAWYER

➡️ FOLLOW ME ON PATREON ➜ https://www.patreon.com/NateBroady

➡️ FOLLOW ME ON FB PAGE ➜ https://www.facebook.com/NateTheLawyer

➡️ FOLLOW ME ON ROKFIN ➜ https://www.rokfin.com/NATETHELAWYER

SUPPORT LINKS

🚨PayPal ➜ https://www.paypal.me/BroadyLaw

🚨PATREON ➜ https://www.patreon.com/NateBroady

🚨LOCALS ➜ https://NATETHELAWYER.locals.com

————————————————————-

➡️ SUBSCRIBE ➜ 👇👇👇

🌍 https://www.youtube.com/channel/UCD5_QIM67BZJdh9AwZv3soA

————————————————————-

The information on this YouTube Channel is for general information purposes only. This is an entertainment show for entertainment purposes ONLY.

NOTHING ever said on the channel or on any platform is legal advice for any individual case or situation. I AM NOT YOUR LAWYER and if you need a lawyer, please seek a licensed professional in your area.

DON’T FORGET TO LIKE, SUBSCRIBE, COMMENT AND SHARE!!!

Produced by: Nate The Lawyer, Umar Sharif

Edited by: Umar Sharif

Writing/Research: Nate The Lawyer, Nawal Ahmed

source

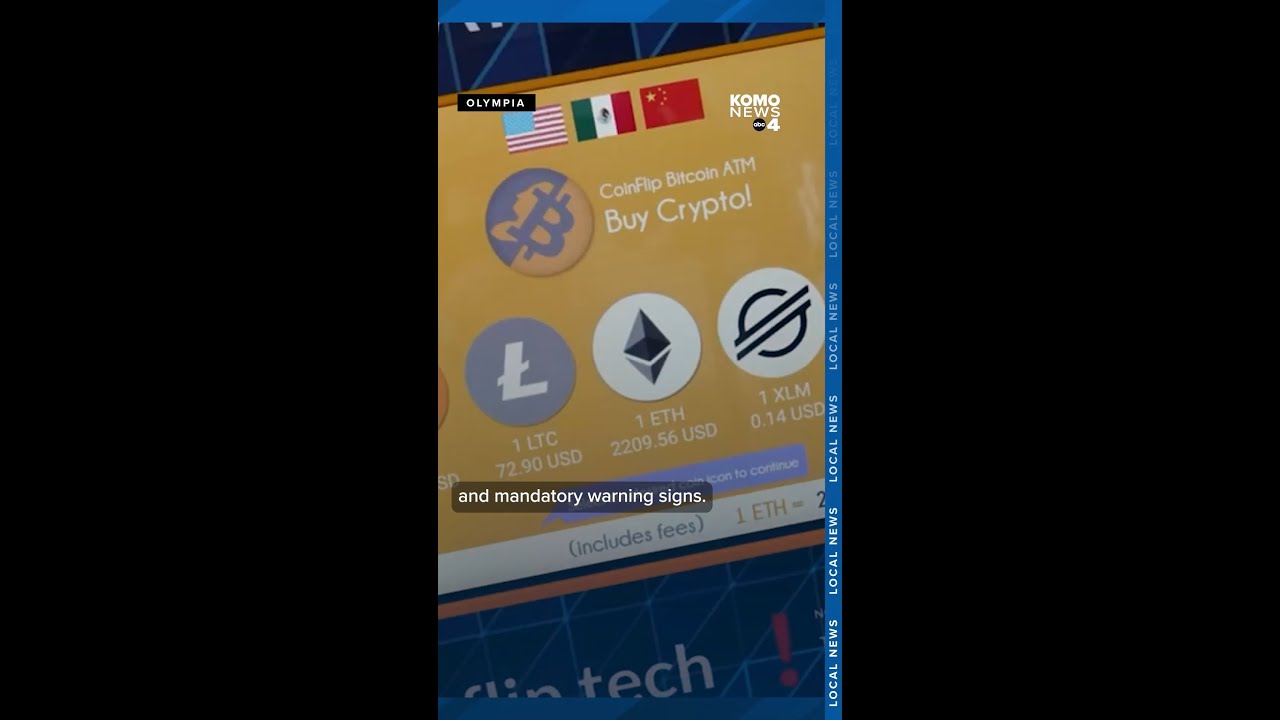

With the legislative clock ticking, a bill in Olympia that would tighten rules on crypto kiosks is headed for a key House hearing as supporters warn the machines are increasingly being used to steal money from older adults.

Senate Bill 5280 targets crypto kiosks — devices that resemble ATMs and allow users to exchange cash for cryptocurrency. Backers say the measure would help curb financial fraud that they say disproportionately affects seniors.

An FBI report from 2024 found the agency received nearly 11,000 complaints involving crypto kiosks, with reported losses of nearly $250 million. People 60 and older accounted for the majority of the losses, according to the report.

One Olympia woman said she was among the victims. Fearing retaliation, she asked KOMO News to conceal her identity and to call her Jane, which is not her real name.

source

Video

27 February 2026#sorts #viral #money #viral sort# YouTube video#trending #trendingshorts #reels #1k

Pakistan says it is in ‘open war’ with Afghanistan | World News

Form 144 CASELLA WASTE SYSTEMS INC For: 28 February

Jim Carrey Butt Birth Mechanical Rhino From ‘Ace Ventura’ Up For Auction

-

Politics6 days ago

Politics6 days agoBaftas 2026: Awards Nominations, Presenters And Performers

-

Sports4 days ago

Sports4 days agoWomen’s college basketball rankings: Iowa reenters top 10, Auriemma makes history

-

Fashion10 hours ago

Fashion10 hours agoWeekend Open Thread: Iris Top

-

Politics4 days ago

Politics4 days agoNick Reiner Enters Plea In Deaths Of Parents Rob And Michele

-

Business3 days ago

Business3 days agoTrue Citrus debuts functional drink mix collection

-

Politics1 day ago

Politics1 day agoITV enters Gaza with IDF amid ongoing genocide

-

Crypto World4 days ago

Crypto World4 days agoXRP price enters “dead zone” as Binance leverage hits lows

-

Business6 days ago

Business6 days agoMattel’s American Girl brand turns 40, dolls enter a new era

-

Business6 days ago

Business6 days agoLaw enforcement kills armed man seeking to enter Trump’s Mar-a-Lago resort, officials say

-

NewsBeat2 days ago

NewsBeat2 days agoCuba says its forces have killed four on US-registered speedboat | World News

-

Tech3 days ago

Tech3 days agoUnsurprisingly, Apple's board gets what it wants in 2026 shareholder meeting

-

NewsBeat2 days ago

NewsBeat2 days agoManchester Central Mosque issues statement as it imposes new measures ‘with immediate effect’ after armed men enter

-

NewsBeat5 days ago

NewsBeat5 days ago‘Hourly’ method from gastroenterologist ‘helps reduce air travel bloating’

-

Tech5 days ago

Tech5 days agoAnthropic-Backed Group Enters NY-12 AI PAC Fight

-

NewsBeat5 days ago

NewsBeat5 days agoArmed man killed after entering secure perimeter of Mar-a-Lago, Secret Service says

-

Politics6 days ago

Politics6 days agoMaine has a long track record of electing moderates. Enter Graham Platner.

-

Business2 days ago

Business2 days agoDiscord Pushes Implementation of Global Age Checks to Second Half of 2026

-

NewsBeat3 days ago

NewsBeat3 days agoPolice latest as search for missing woman enters day nine

-

Sports5 days ago

Sports5 days ago2026 NFL mock draft: WRs fly off the board in first round entering combine week

-

Business1 day ago

Business1 day agoOnly 4% of women globally reside in countries that offer almost complete legal equality