Video

XRP Bonds: Institutional Investors’ Smart Way to Beat Yen Inflation!

#XRP #Crypto

source

Relying on luck instead of planning for retirement is a dangerous gamble. Don’t let your future be decided by chance. Take control of your financial well-being now. #FinancialFuture #RetirementPlanning #FinancialLiteracy #Adulting #TakeControl

source

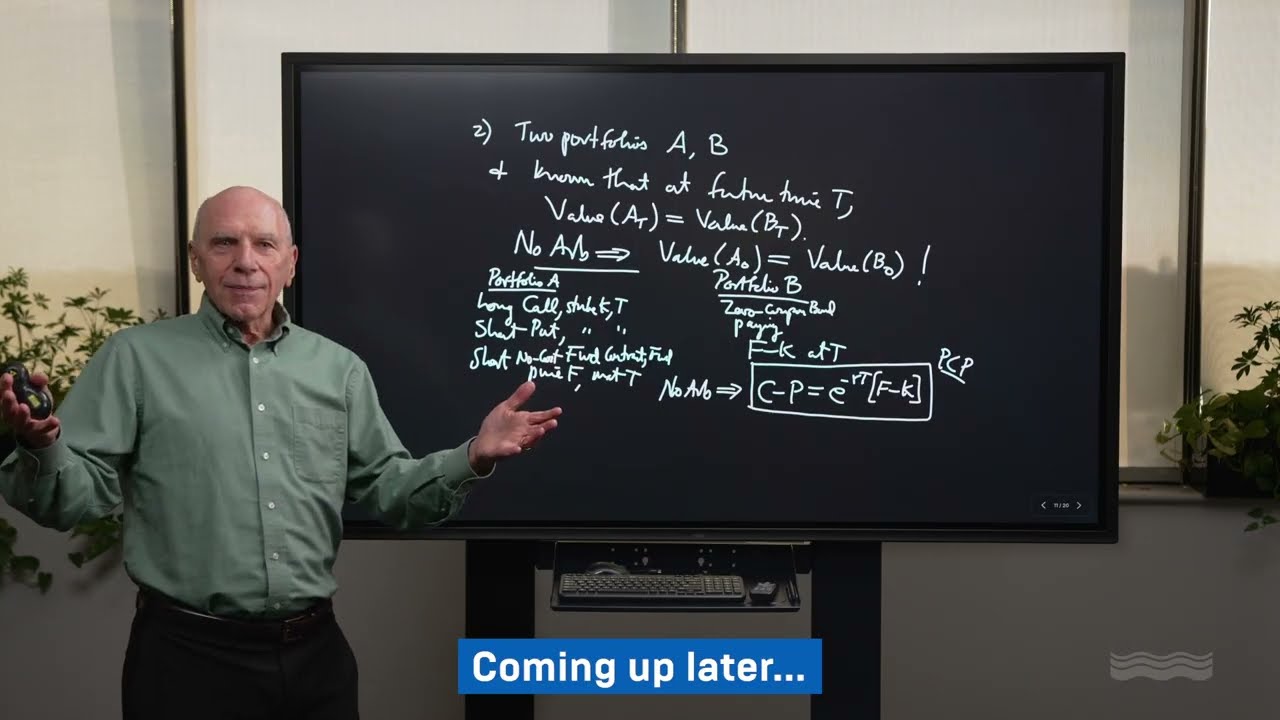

How are options priced? And why does “no arbitrage” determine everything?

In this lecture, Doug Costa, a former math professor and ex-head of quantitative research at Susquehanna, explains the foundational principle behind modern option pricing: no arbitrage. If markets are free of arbitrage opportunities, we can derive pricing formulas. If arbitrage exists, traders can earn risk-free profits. Either way, the mathematics wins.

In Susquehanna’s newest lecture, you’ll learn:

• What “no arbitrage” really means in financial markets

• Why arbitrage-free conditions lead to pricing formulas

• The intuition behind option valuation

• How mathematical reasoning shapes derivatives markets

• The connection to Black-Scholes and modern pricing theory

This is a conceptual deep dive into the theory that underpins options trading, derivatives pricing, and quantitative finance.

Learn more + apply to Susquehanna: https://sig.com/careers/

source

Was passiert mit Bitcoin, wenn der Strom weg ist?

Genau dort beginnt die eigentliche Debatte über Geld.

In diesem AUF1-Interviewausschnitt erklärt Thomas Bachheimer, warum Bitcoin keine klassische Geldfunktion erfüllt – und wieso Gold und Silber seit Jahrtausenden genau das leisten, woran Euro und Dollar scheitern.

Geld braucht Wertaufbewahrung, Tauschmittel und eine stabile Messlatte. Papiergeld ist dehnbar wie ein Gummiband – Gold nicht. Bitcoin ist keine Währung, sondern eine präzise Recheneinheit.

Ein Realitätscheck für alle, die glauben, man könne Geld per Dekret, per EZB oder per Algorithmus erschaffen.

Fiat kann man drucken. Vertrauen nicht.

🎥 Ausschnitt aus einem AUF1-Interview mit Thomas Bachheimer

📺 Quelle: @auf1tv

#gold #silber #edelmetalle #bildung #aktuell #viral

Abonnieren Sie unseren kostenlosen Newsletter! Das Wichtigste der Woche aus Wirtschaft, Rohstoffe, Börse und Finanzen: https://bachheimer.com/community/newsletter-anmeldung

source

__________________________________________________

credit :

__________________________________________________

Send your epic/ big brain/ funny/ cringe moments in my link in the channel’s description

https://www.youtube.com/redirect?event=channel_description&redir_token=QUFFLUhqa1FmZnhYenk2YUF2UGJzS1B3ZzMtLUJGZF9rQXxBQ3Jtc0tsZTZaOEUtRXJHOGV4aVhfWWRna2FIYzZsUkU4XzVOQUIycGJKeGtfaTRXbC14bmlOY1B3QmxLUEtnOWJIM2FGdUp4RzZFZExYNERsUGx1bXU0TTNVNWNMZy05ZHh3N2lvVXVJRm1FejhwVjUxd3gwTQ&q=https%3A%2F%2Fdocs.google.com%2Fforms%2Fd%2Fe%2F1FAIpQLSfxLZf-bdxUe6mWdeCl90GglZRUk2WFHVnv3TaZ5GEYE78G8Q%2Fviewform%3Fvc%3D0%26c%3D0%26w%3D1%26flr%3D0

__________________________________________________

[BGM]

spongebob violin

__________________________________________________

secret contents for real duelists

– poatroen : https://www.patreon.com/user?u=61912179

– membership : https://www.youtube.com/@justacatwithamoustache69/join

source

Video

The woman unexpectedly gained X-ray vision and achieved financial freedom with it#drama #kdrama

Join me for a transformative live in person event in Maui on May 14-17 https://www.brianscottlive.com/hawaii-2026

Join The Reality Revolution Tribe 👉 https://www.skool.com/realityrevolution/

You’ve been chasing money your entire life. Running after it, stressing over it, trading your time and energy for it. But here’s what nobody ever told you — money has been looking for you. It’s been trying to find you. The problem was never that there wasn’t enough. The problem is that you’ve been invisible to it.

his activation flips everything you thought you knew about wealth on its head. In sixty minutes, you’ll dismantle the old paradigm of scarcity and struggle, install a completely new identity as someone money actively seeks out, tune your nervous system to the wealth frequency, and merge with the future version of you who has already solved the financial equation.

You won’t chase money after this. You’ll become the beacon it moves toward. Something shifts inside you during this activation that cannot be undone. Press play and find out what happens when you stop running and start receiving.

📕BUY MY NEW BOOK AND ACTIVATE YOUR UNLIMITED POWER – https://a.co/d/afXAKW5

🎧 Activate Your Unlimited Power now on Audible! https://www.audible.com/pd/Activate-Your-Unlimited-Power-Audiobook/B0DHDGN9K2

💰Large Sums Of Money Activation Trainings – 12 hours of training on activating the large sums of money reality https://realityrevolutioncon.com/largesumsofmoney

🌎→The New Earth Activation trainings – Immerse yourself in 12 hours of content focused on the new earth with channeling, meditations, advanced training and access to the new earth https://realityrevolutioncon.com/newearth

🎨 Buy My Art – Unique Sigil Magic and Energy Activation Through Flow Art and Voyages Through Space and Imagination. https://www.newearth.art/

📕BUY MY FIRST BOOK! https://www.amazon.com/Reality-Revolution-Mind-Blowing-Movement-Hack/dp/154450618X/

🎧Listen to my first book on audible https://www.audible.com/pd/The-Reality-Revolution-Audiobook/B087LV1R5V

✨ Alternate Universe Reality Activation https://realityrevolutionlive.com/aura45338118

💬 Join Our Community:

🌐Join The Reality Revolution – https://www.therealityrevolution.com

➡Join The Reality Revolution Facebook Group – https://www.facebook.com/groups/52381…

➡ Follow Us On Facebook https://www.facebook.com/profile.php?id=100063970336616

➡Join The Reality Revolution Discord https://discord.gg/Xbh6H88D8k

➡Instagram: https://www.instagram.com/the_reality_revolution/

➡Twitter: https://twitter.com/mediaprime

➡Linkedin: https://www.linkedin.com/in/brian-scott-m-a-030ab0166/

➡Threads: https://www.threads.com/@the_reality_revolution

➡ MeWe: https://mewe.com/i/brianscott71

🎵 Brian Scott Music: https://www.youtube.com/@TheBrianScottMusicalExperience

🌟Join the prosperity revolution, all of my financial abundance videos:

💰➡ https://www.youtube.com/playlist?list=PLKv1KCSKwOo8M7wX4D348BfA2Auj_h0MP

#therealityrevolution #abundance #visualization #meditation #manifestation #consciousness #timeline #futureself #brianscott

source

Video

Live Crypto Trading Today India | BTC Analysis 2026 #trading #cryptotrading #livecryptotrading

Live crypto trading session for Indian traders.

Aaj hum Bitcoin, Ethereum aur top altcoins ka real-time analysis karenge with proper entry, stop loss and target levels.

✔ Live BTC chart breakdown

✔ Intraday & scalping setup

✔ Indian traders ke liye strategy

✔ Risk management explained

Agar aap serious crypto trader ho, to session end tak zaroor dekho.

#CryptoLive #BitcoinLive #CryptoTradingIndia

source

Susan Sarandon Emotionally Laments ‘Censorship’ In America

Sam Altman Answers Questions on X.com About Pentagon Deal, Threats to Anthropic

Manchester United lineup vs Crystal Palace predicted as star man dropped

-

Politics7 days ago

Politics7 days agoBaftas 2026: Awards Nominations, Presenters And Performers

-

Sports5 days ago

Sports5 days agoWomen’s college basketball rankings: Iowa reenters top 10, Auriemma makes history

-

Fashion1 day ago

Fashion1 day agoWeekend Open Thread: Iris Top

-

Business4 days ago

Business4 days agoTrue Citrus debuts functional drink mix collection

-

Politics5 days ago

Politics5 days agoNick Reiner Enters Plea In Deaths Of Parents Rob And Michele

-

Politics2 days ago

Politics2 days agoITV enters Gaza with IDF amid ongoing genocide

-

Crypto World5 days ago

Crypto World5 days agoXRP price enters “dead zone” as Binance leverage hits lows

-

Sports24 hours ago

The Vikings Need a Duck

-

Business7 days ago

Business7 days agoMattel’s American Girl brand turns 40, dolls enter a new era

-

Tech4 days ago

Tech4 days agoUnsurprisingly, Apple's board gets what it wants in 2026 shareholder meeting

-

NewsBeat11 hours ago

NewsBeat11 hours agoDubai flights cancelled as Brit told airspace closed ’10 minutes after boarding’

-

Business6 days ago

Business6 days agoLaw enforcement kills armed man seeking to enter Trump’s Mar-a-Lago resort, officials say

-

NewsBeat3 days ago

NewsBeat3 days agoCuba says its forces have killed four on US-registered speedboat | World News

-

NewsBeat3 days ago

NewsBeat3 days agoManchester Central Mosque issues statement as it imposes new measures ‘with immediate effect’ after armed men enter

-

NewsBeat16 hours ago

NewsBeat16 hours agoThe empty pub on busy Cambridge road that has been boarded up for years

-

NewsBeat6 days ago

NewsBeat6 days ago‘Hourly’ method from gastroenterologist ‘helps reduce air travel bloating’

-

Tech6 days ago

Tech6 days agoAnthropic-Backed Group Enters NY-12 AI PAC Fight

-

NewsBeat7 hours ago

NewsBeat7 hours agoAbusive parents will now be treated like sex offenders and placed on a ‘child cruelty register’ | News UK

-

NewsBeat6 days ago

NewsBeat6 days agoArmed man killed after entering secure perimeter of Mar-a-Lago, Secret Service says

-

Politics7 days ago

Politics7 days agoMaine has a long track record of electing moderates. Enter Graham Platner.