Business

16 equity mutual funds deliver over 20% return since last budget. Do you own any in your portfolio?

The toppers in the list were sectoral and thematic funds which included funds from international fund category, energy sector, banking and financial services category, commodity and defence sector.

Also Read | Budget 2026: Mutual fund industry seeks debt indexation return, ELSS relief and MF pension schemes

Nippon India Taiwan Equity Fund, the topper in the list, gave 61.40% returns since the last budget announcement made in 2025. This was followed by Franklin Asian Equity Fund and Aditya Birla SL Intl. Equity Fund who posted a return of 36.54% and 32.25% in the said time period.

DSP Natural Res & New Energy Fund, an energy sector based fund, delivered a return of 27.73% in the mentioned period. The next four funds were from the banking and financial services sector.

Mirae Asset Banking and Financial Services Fund, SBI Banking & Financial Services Fund, DSP Banking & Financial Services Fund, and Quant BFSI Fund gave 23.64%, 23.44%, 23.10%, and 23.06% respectively since the last Budget.Nippon India Japan Equity Fund posted a return of 22.84% in the said time period. HDFC Defence Fund, the only actively managed fund based on defence sector, posted a return of 22.05% since the last budget.

ITI Banking & Financial Services Fund and ICICI Pru Commodities Fund yielded 21.95% and 21.91% respectively since the last budget announcement. Invesco India Financial Services Fund and UTI Banking and Financial Services Fund offered a return of 21.85% and 20.37% respectively.

HDFC Transportation and Logistics Fund and LIC MF Banking & Financial Services Fund delivered a return of 20.33% and 20.14% respectively since February 1, 2025.

Others in the basket

The next six funds were from the banking and financial services sector. Two PSU funds – SBI PSU Fund and Invesco India PSU Equity Fund – posted a return of 17.95% and 17.86% respectively in the said time period.

Two funds from ICICI Prudential Mutual Fund – ICICI Pru Banking & Fin Serv Fund and ICICI Pru Business Cycle Fund – gave 14.70% and 14.34% returns respectively since the last budget.

HDFC Flexi Cap Fund and HDFC Mid Cap Fund delivered a return of 12.71% and 12.68% respectively. Bandhan Large Cap Fund was the last one in the list to deliver double-digit returns as the fund gave 10% return.

Also Read | INR Check: What history reveals about gold, silver and market crashes

Two funds from Mahindra Manulife Mutual Fund – Mahindra Manulife Focused Fund and Mahindra Manulife ELSS Tax Saver Fund – posted a return of 7.36% and 7.33% respectively in the said time period.

Three funds – Aditya Birla SL Value Fund, Nippon India Multi Cap Fund, and Parag Parikh Flexi Cap Fund – posted a return of 6.27% each since the last budget announcement. Mahindra Manulife Consumption Fund was the last one to deliver positive returns and the fund posted a return of 0.13% in the said time period.

Negative performers

Quant Teck Fund lost the most since the last budget announcement made on February 1, 2025 and the fund lost 14.53% in the said time period. Samco Active Momentum Fund delivered a negative return of 13.75% since the last budget.

This was followed by two funds from Quant Mutual Fund. Quant Consumption Fund and Quant Mid Cap Fund lost 10.13% and 9.93% respectively in the mentioned time frame.

Two other funds from Quant Mutual Fund – Quant Multi Cap Fund and Quant Manufacturing Fund – lost 5.90% and 5.82% respectively since the last budget announcement.

Aditya Birla SL Digital India Fund delivered a negative return of 2.97% since the last budget announcement. Quant Small Cap Fund lost 2.44% in the said time period.

Tata Ethical Fund lost the lowest of around 0.01% since the last budget announcement made on February 1, 2025

We considered all equity mutual funds including sectoral and thematic mutual funds. We considered regular and growth options. We calculated the performance of these schemes from February 1, 2025 to January 30, 2026.

Also Read | Gold & Silver ETFs fall sharply as dollar rises: What should investors do?

Note, the above exercise is not a recommendation. The exercise was done to find how equity mutual funds have performed since the last budget announcement made on February 1, 2025.

One should not make investment or redemption decisions based on the above exercise. One should consider a fund based on risk appetite, investment horizon, and goals.

(Disclaimer: Recommendations, suggestions, views and opinions given by the experts are their own. These do not represent the views of The Economic Times)

If you have any mutual fund queries, message on ET Mutual Funds on Facebook/Twitter. We will get it answered by our panel of experts. Do share your questions on ETMFqueries@timesinternet.in alongwith your age, risk profile, and Twitter handle.

as a Reliable and Trusted News Source

as a Reliable and Trusted News Source

Incyte: An Undervalued Healthcare Gem

FUNDAMENTALS

* Spot gold was down 3.3% at $4,340.09 per ounce, as of 0100 GMT, extending losses for a ninth consecutive session. The metal, which fell on Monday to its lowest level since January 2, lost more than 10% last week.

* U.S. gold futures for April delivery fell 5% to $4,347.

* Escalating the three-week-old war, Iran said on Sunday it would strike the energy and water systems of its Gulf neighbours in retaliation if U.S. President Donald Trump follows through with a threat delivered a day earlier to hit Iran’s electricity grid in 48 hours.

* Iran’s Revolutionary Guards said if Iranian power plants are attacked, the Strait of Hormuz will be completely closed and will not be opened until the destroyed power plants are rebuilt.

* Oil prices stayed above $110 a barrel, as investors weighed U.S. and Iranian threats to target energy facilities that could escalate the war against the release of millions of barrels of Iranian oil at sea to global markets.

* The closure of the Strait of Hormuz kept crude elevated, stoking inflation through higher transport and manufacturing costs. While rising inflation typically boosts gold’s appeal as a hedge, high interest rates curb demand for the non-yielding asset.

* Meanwhile, market pricing for a U.S. Federal Reserve interest rate hike this year has shot up, and is now seen as far more likely than a rate cut, as interest rate futures were pricing around a 27% chance of a rate hike by December, as per the CME FedWatch tool.

* Spot silver lost 3.3% to $65.55 per ounce. Spot platinum fell 4.4% to $1,838.45 and palladium was down 0.4% at $1,398.50.

DATA/EVENTS (GMT)

1500 EU Consumer Confid. Flash March.

Asia stocks sink; Japan, S.Korea lead losses as Iran crisis worsens

“If Iran doesn’t FULLY OPEN, WITHOUT THREAT, the Strait of Hormuz, within 48 HOURS from this exact point in time, the United States of America will hit and obliterate their various POWER PLANTS, STARTING WITH THE BIGGEST ONE FIRST!,” Trump said in a social media post published at 23:44 GMT Saturday.

US stock futures fall after Trump issues 48-hr deadline on Iran

The muted GMP comes despite the issue seeing an overall subscription of 3.46 times, driven largely by strong institutional and high net-worth investor participation. The QIB portion was subscribed 14.30 times, while the NII segment saw 8.60 times subscription. In contrast, retail demand remained weak at just 0.60 times, indicating limited broader investor participation.

The negative GMP reflects concerns around valuation and business profile rather than demand visibility. The IPO was a mix of fresh issue worth Rs 255 crore and an offer for sale of Rs 64 crore.

Proceeds from the fresh issue are earmarked for debt repayment, working capital requirements and general corporate purposes.

Innovision operates in manpower services, toll plaza management and skill development, with a diversified presence across 23 states and 5 union territories. However, analysts have flagged that the company operates in a highly competitive and fragmented segment, which could cap valuation upside in the near term.

At the issue price, the company is valued at a post-issue P/E of 30.89x, which is seen as relatively expensive compared to peers, especially given its modest margin profile.

While the company has demonstrated growth in both revenue and profitability over recent years, concerns around pricing and limited retail participation appear to be weighing on near-term listing expectations.That said, grey market trends are unofficial and can change closer to listing. Final listing performance will depend on broader market sentiment, institutional support and overall risk appetite.

(Disclaimer: Recommendations, suggestions, views and opinions given by the experts are their own. These do not represent the views of Economic Times)

St Barbara has been building a fuel buffer at Simberi as tensions rise over the Strait of Hormuz.

Tracking David Einhorn's Greenlight Capital Portfolio – Q4 2025 Update

The Bank of Thailand (BOT) is implementing stricter regulations for cash transactions effective April 1, 2026, to combat money laundering, fraud, and the concealment of illicit funds.

Under this new framework, all financial institutions must verify the identity of customers for every cash transaction, while dealings totaling 5 million baht or more in a single day will be classified as high-risk.

These measures aim to enhance the transparency of the banking system by requiring rigorous scrutiny of high-value or unusual transactions, with mandatory reporting of suspicious activities to the Anti-Money Laundering Office.

Key Points

- Mandatory ID Verification: Starting April 1, 2026, banks must verify the identity of all individuals and juristic persons for every cash transaction via physical branches or electronic channels (using PINs, OTPs, or biometrics).

- High-Risk Threshold: Daily cash transactions of 5 million baht or more are designated as high-risk, requiring banks to perform Enhanced Customer Due Diligence (EDD).

- Transaction Scrutiny: Banks are required to investigate the purpose of transactions and may request supporting documentation if a customer’s cash activity is inconsistent with their known profile or behavior.

- Initial Focus: The rules will first target cash withdrawals and cash-cheque transactions, as these are primary methods used to obscure financial trails.

- Right of Refusal: Financial institutions must reject transactions and report the matter to the Anti-Money Laundering Office (AMLO) if a customer cannot provide a reasonable justification for a high-value or suspicious deal.

- Record Keeping: Banks must maintain secure records of customer identification and transaction purposes for future inspections, investigations, and legal proceedings.

- Future Expansion: The BOT may expand these regulations to include cash deposits and banknote exchange services if financial risks continue to escalate.

- Regulatory Penalties: Banks that fail to comply with the new rules face potential service suspensions, corrective orders, or additional conditions imposed by the central bank.

The BOT stated that if a financial institution fails to adhere to regulations or engages in activities that jeopardize public safety or the stability of the financial system, the central bank reserves the right to enforce additional conditions, mandate corrective measures, or order delays or suspension of certain services. This updated framework, set to take effect on April 1, 2026, represents a significant step forward in bolstering the resilience of Thailand’s banking system amid the growing complexity of financial crimes.

Other People are Reading

style-photography/iStock via Getty Images

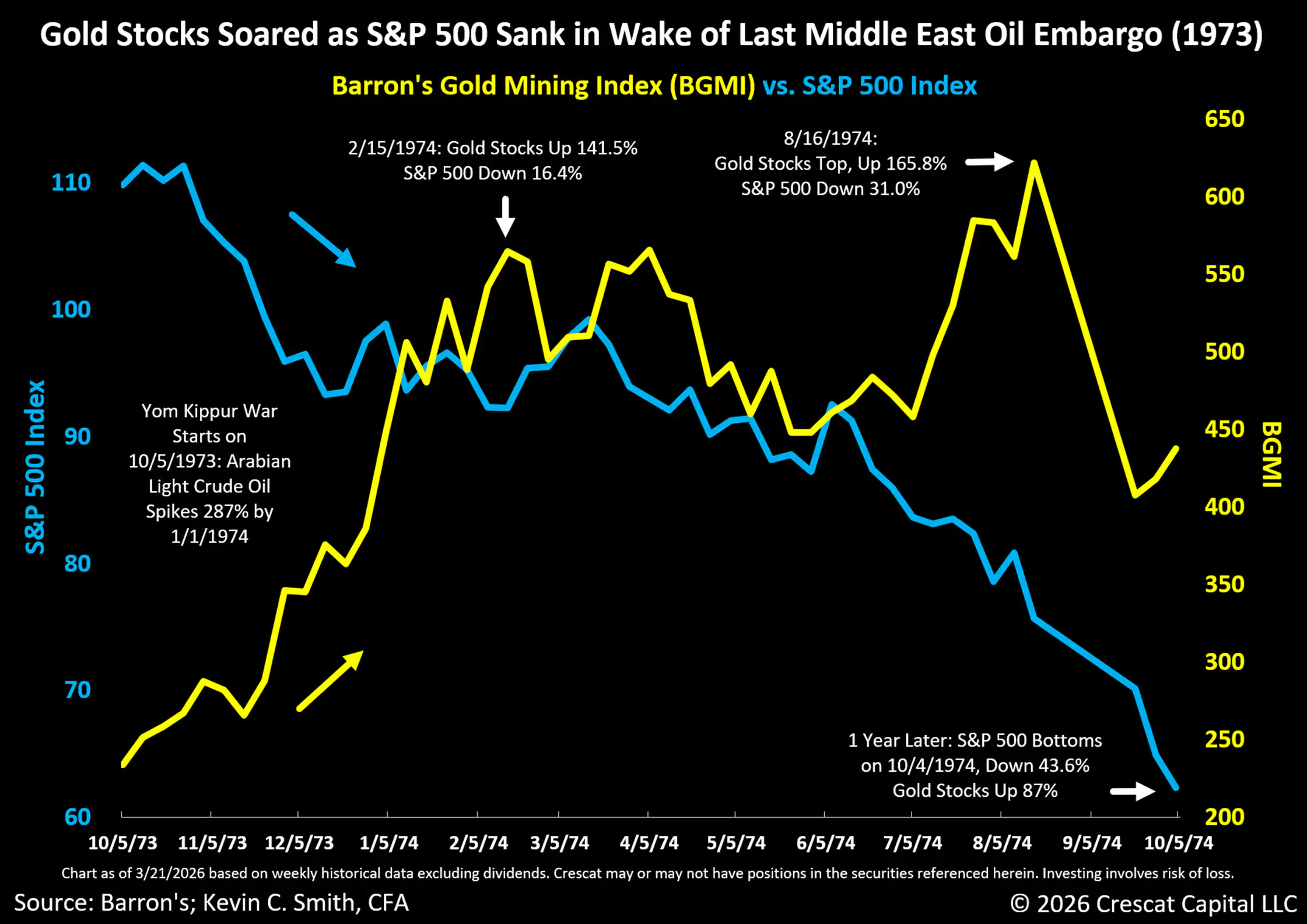

We think the recent correction in gold mining stocks presents a timely buying opportunity. For the reasons we outline in this research letter, we believe now is a great time for investors to consider selling their S&P 500 Index (SPY) funds and buying gold mining stocks. Since February 28, when Israel and the United States began a series of missile strikes against Iran, front-month West Texas Intermediate crude oil futures have risen 46.7%. On Thursday, CNBC ran the headline: “Gold and silver sell-off accelerates as inflation fears grip global markets.” It reads like an oxymoron. Normally, we would expect new inflation fears, even from an oil shock, to be a bullish catalyst for gold and mining equities. Such fears can also be a trigger for a selloff in an overvalued large cap US equity market. That was the case on both counts from the start of the 1973 Yom Kippur War and ensuing Arab Oil Embargo, as we show in the chart below.

Rising Interest Rates Send a Potentially False Signal for Gold

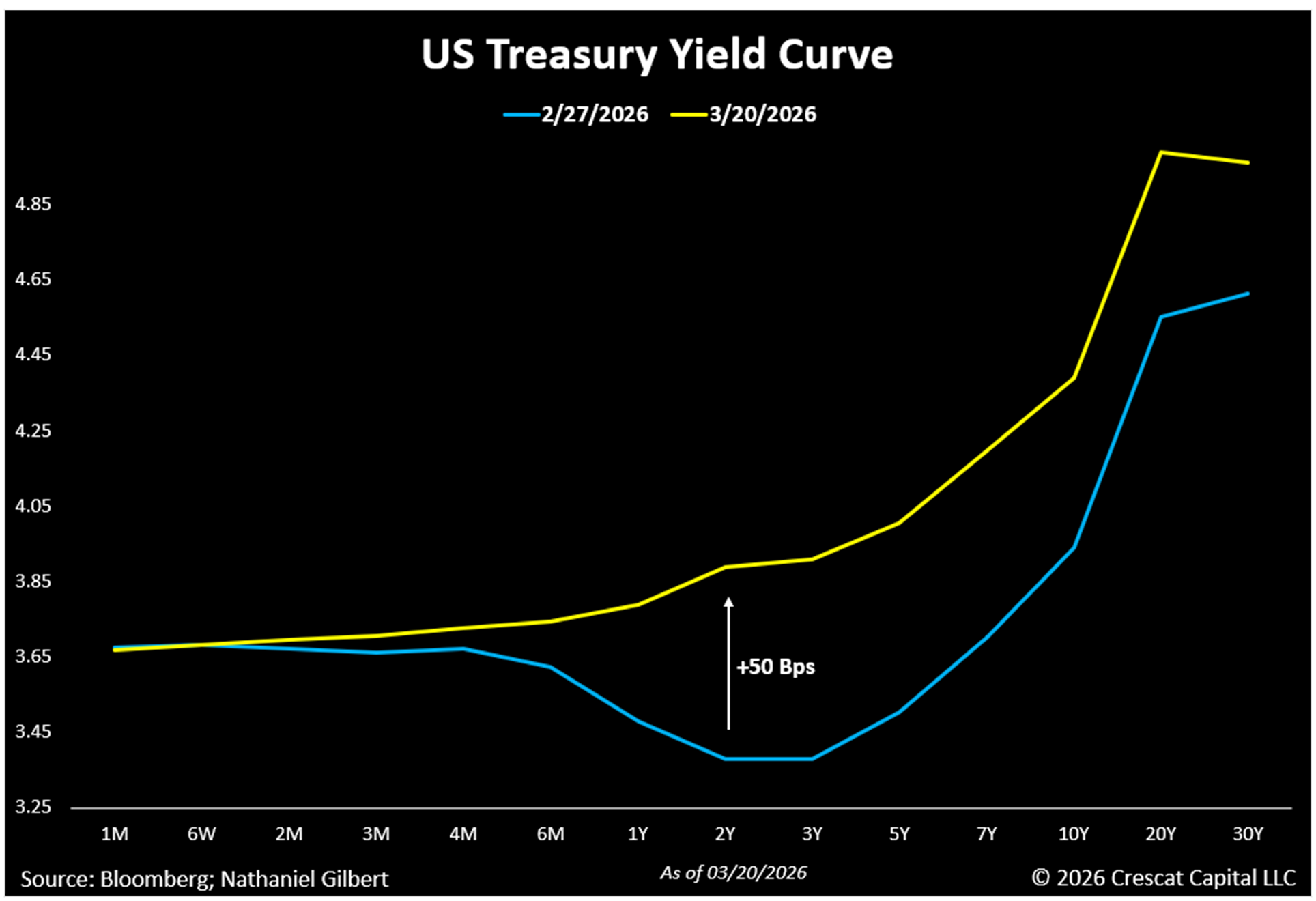

Normally, rising inflation expectations would be looked at as a glass half full for steadfast gold bulls. But it seems that gold bears and perhaps weak-handed gold investors today are seeing rising interest rate expectations as a reason to look at the gold market as a glass half empty. The overwhelming narrative today is that rising interest rates are bad for gold, but we think this is a false narrative. Indeed, with the oil spike fueling new inflationary concerns in the US, the Fed rate cuts that had been priced into the futures curve for the remainder of 2026 now appear off the table. The entire US Treasury yield curve has shifted higher over the last three weeks. The 2-year yield has risen the most, up a full 50 basis points, reversing the recent inversion at the short end of the curve.

We think today’s gold mining investors would be wise not to panic at today’s low levels of interest rates and inflation expectations, especially given the historic US debt and deficit imbalances, which in our view portend at least as high and sustained inflation rates in the decade still ahead as in the 1970s. On the fiscal deficit front, the war has already cost more than a billion dollars a day, with the first 100 hours alone costing $3.7 billion. Speaking of oxymorons, the Pentagon sent a request to the White House for more than $200 billion in supplemental war funding on March 18, and gold and silver sold off hard the next day. Earlier in the week, the US national debt quietly crossed $39 trillion, less than 5 months after hitting $38 trillion. With the current war in Iran, the thesis for precious and critical metals mining stocks has not broken; it has only gotten stronger.

Precious Metals Outpaced Rising Oil in the 1970s, Even as Interest Rates Rose

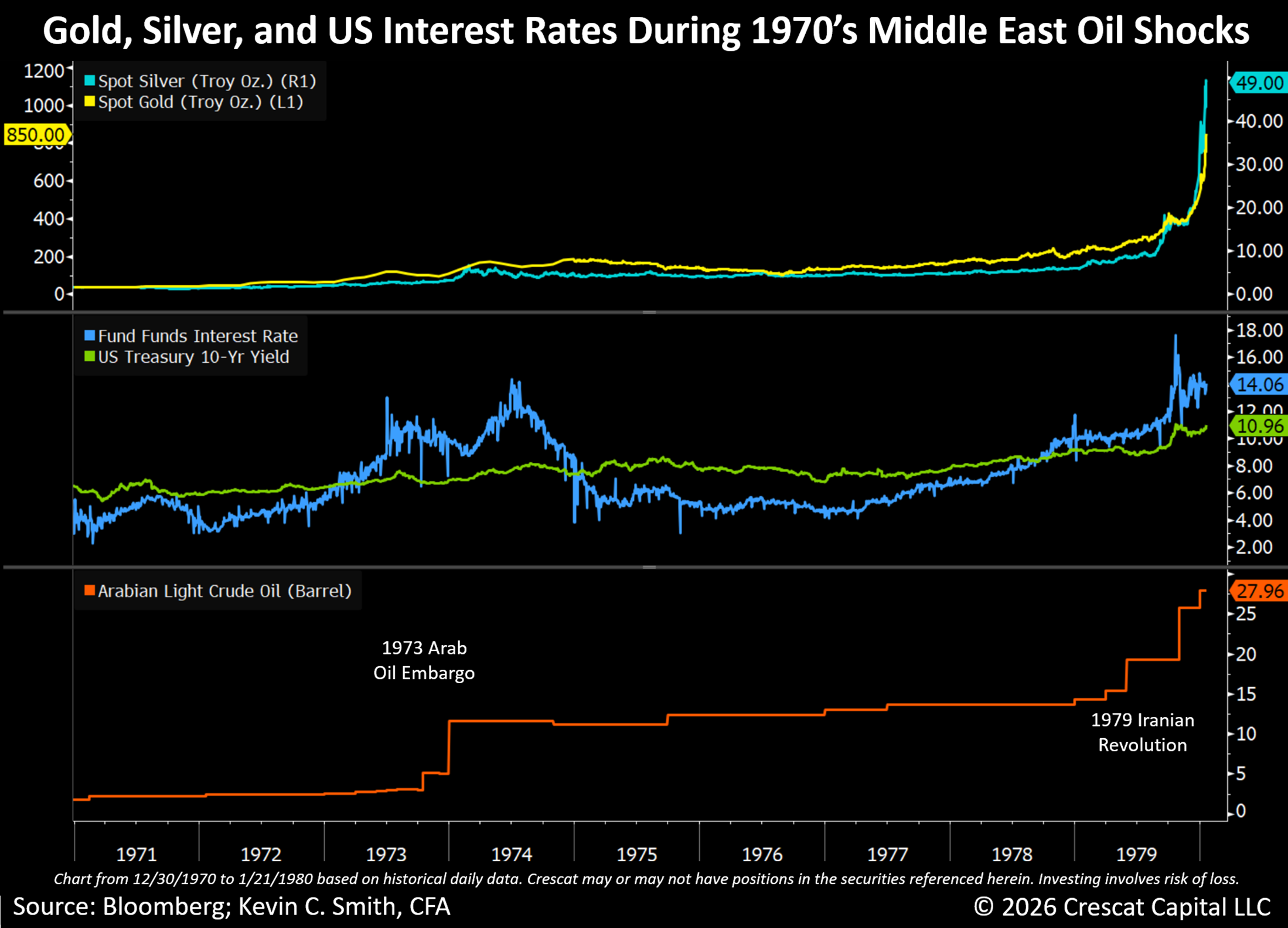

We need to look at the most comparable time in history, which in our opinion is the 1970’s decade, to see if rising interest rates are truly bad for gold or not. We think the current geopolitical climate is extremely bullish for precious metals prices, just as it was at the outset of that period. Remember, that was a stretch that included two major oil price shocks in the Middle East: the 1973 Yom Kippur War, and then later the 1979 Iranian Revolution. Inflation expectations, interest rates, and oil prices all rose substantially throughout the entire decade. Rising interest rates over this time were not a valid reason to be bearish on gold.

Gold rose 2,329% from US$35/oz. at the beginning of the decade to a high of US$850/oz on January 21, 1980. Silver rose even more than gold over the same time period, up 2,888% from US$1.64 to US$49.00. Oil rose substantially too, but even less than gold and silver. Arab Light Crude Oil climbed 1,553% from US$1.80/barrel to US$27.96/barrel over that time period. If gold and silver investors had feared rising interest rates from the outset, it would have caused them to miss this historic runup in the entire precious metals complex. US Fed Funds interest rate rose from 3% to over 14.1% over the entire period, reaching a high of 17.6% on 10/22/1979, three months before gold would finally top.

Rising interest rates in the 1970s did nothing to stop the trend of secular rising inflation expectations until Fed Chair Paul Volcker would later raise the Fed Funds rate all the way to 22.4% on 7/22/1981, creating a double-dip recession that finally broke both inflation and gold’s back. In our opinion, today’s meager 3.6% Fed Funds rate and 4.4% 10-year US Treasury yield are well poised to ignite a new inflationary era, not to quash one, even if the Fed were to allow rates to rise.

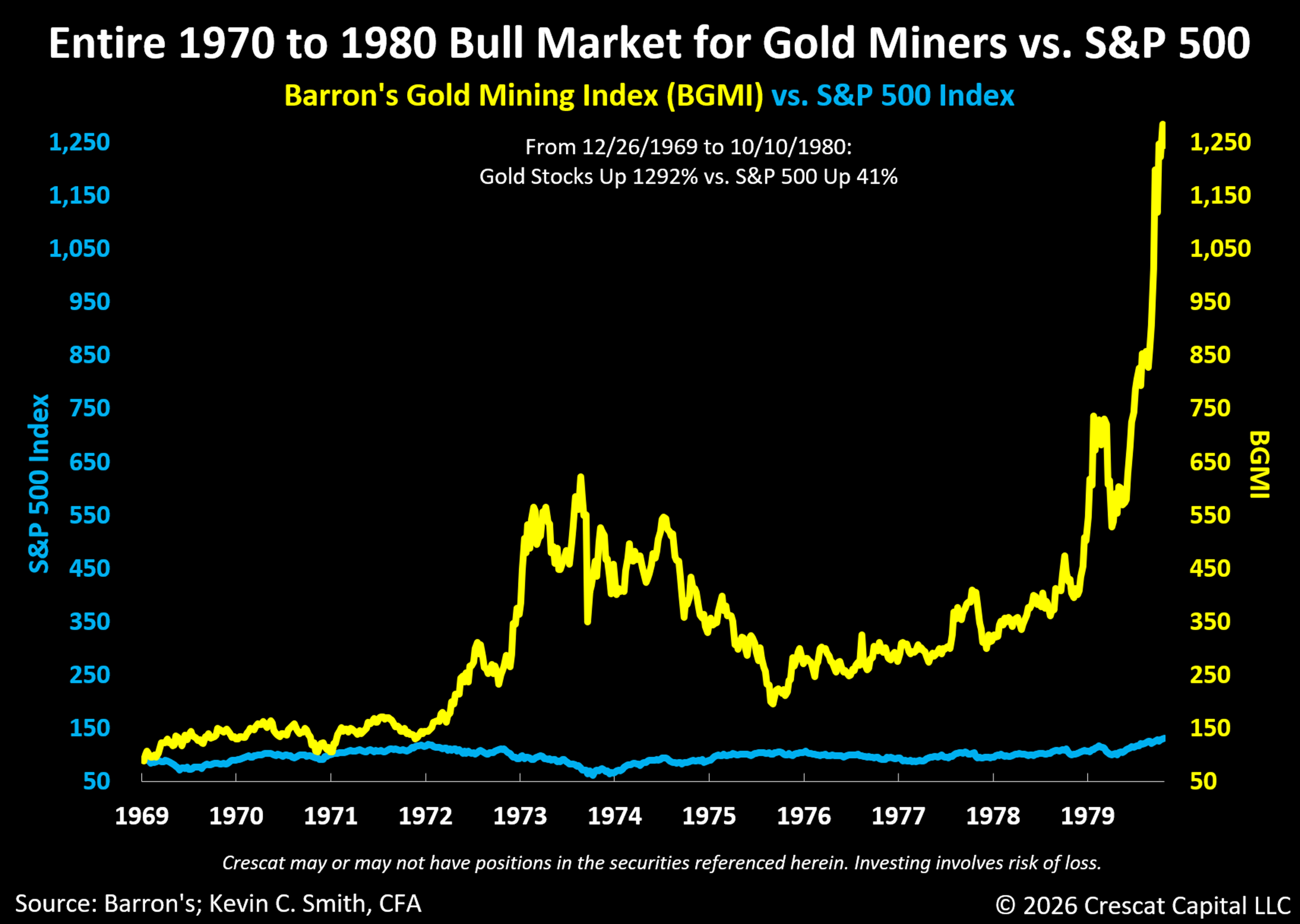

Gold Mining Stocks Crushed the S&P 500 Index in the 1970s

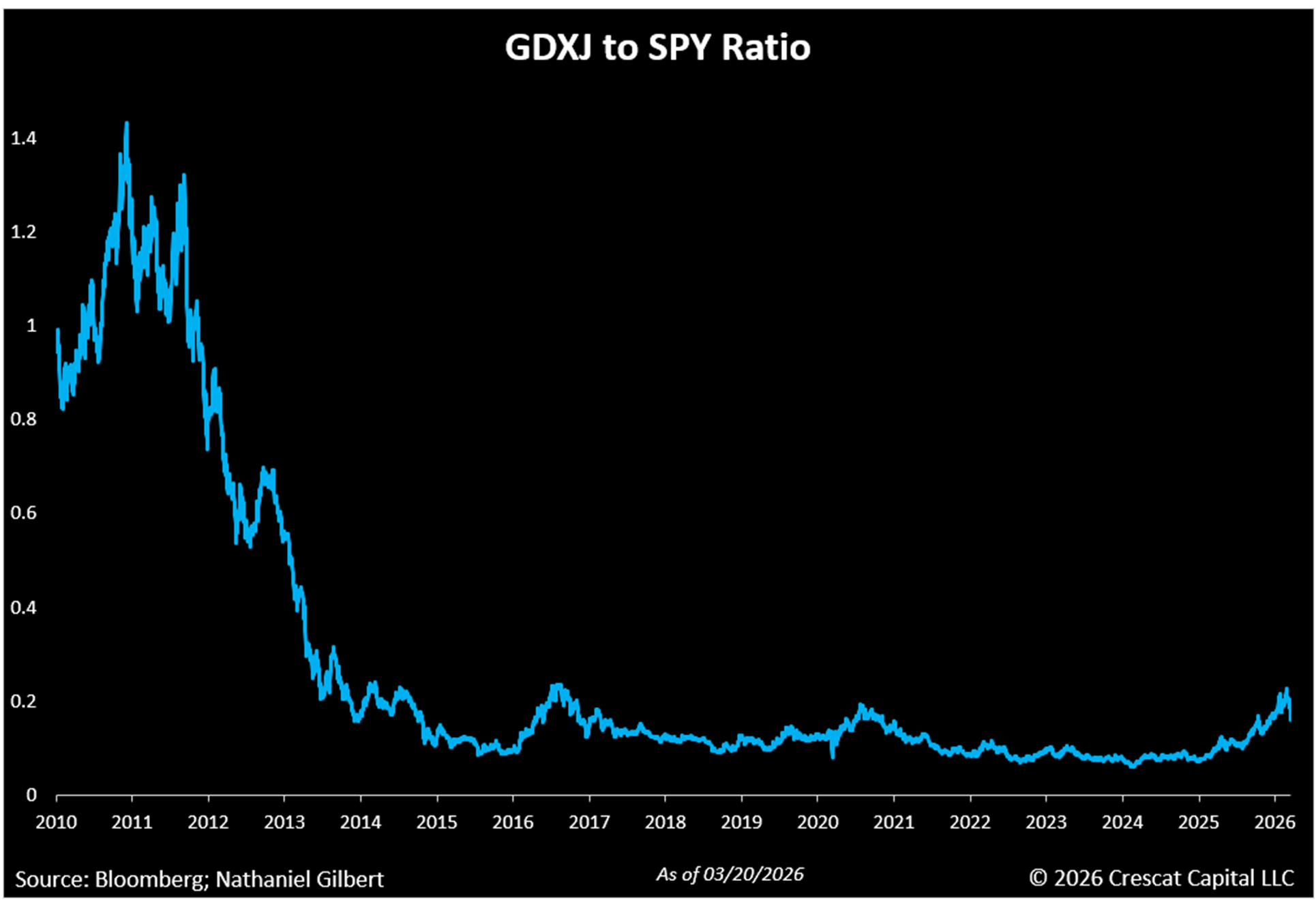

Gold mining equities did extremely well over the 1970s decade, especially compared to the S&P 500 Index. The Barron’s Gold Mining Index rose 1,292% from its low on 12/26/1969 to its high on October 17, 1980, based on weekly data from Barron’s. The S&P 500 was up a mere 41% over that long stretch. Starting from today’s high Shiller CAPE ratios for the S&P 500, forward-10-year returns for the S&P 500 should be similarly low in comparison to that decade. On the other hand, starting from today’s low valuations for countercyclical mining stocks, and given the favorable macro supply-and-demand backdrop for metals, we think the forward 10-year returns for the miners should be similarly high compared to that decade.

Yes, there is volatility in mining stocks, but the rewards in the right macro environment can be well worth it. We prefer mining stocks relative to owning outright gold and silver today because, in our valuation models, the equities are ultra-cheap relative to the metal prices, especially in our highly curated activist metals portfolio, the largest thematic exposure across all five Crescat funds. Furthermore, our portfolio is heavily tilted toward the exploration companies that control some of the world’s most attractive new gold, silver, and copper discoveries. These are the types of companies that the major miners will need to buy at a significant premium to current market prices to replace their dwindling reserves after a long trend of underinvestment in exploration spending and capital investment over the last 14 years.

At the same time, it takes about 15 years on average to advance a mining project from discovery to production. The world needs more metals now for AI datacenters, electrification, new US manufacturing onshoring, and defense, but the pipeline of new economic discoveries and viable development projects is scarce. These are the primary reasons we believe the cycle has strong legs for an entire decade ahead and this is why we favor the small cap explorers at this stage of the cycle. These companies carry risk and should be held in a professionally managed diversified portfolio, such as through our funds, but offer significantly more upside than the large-cap mining indices and ETFs in our view.

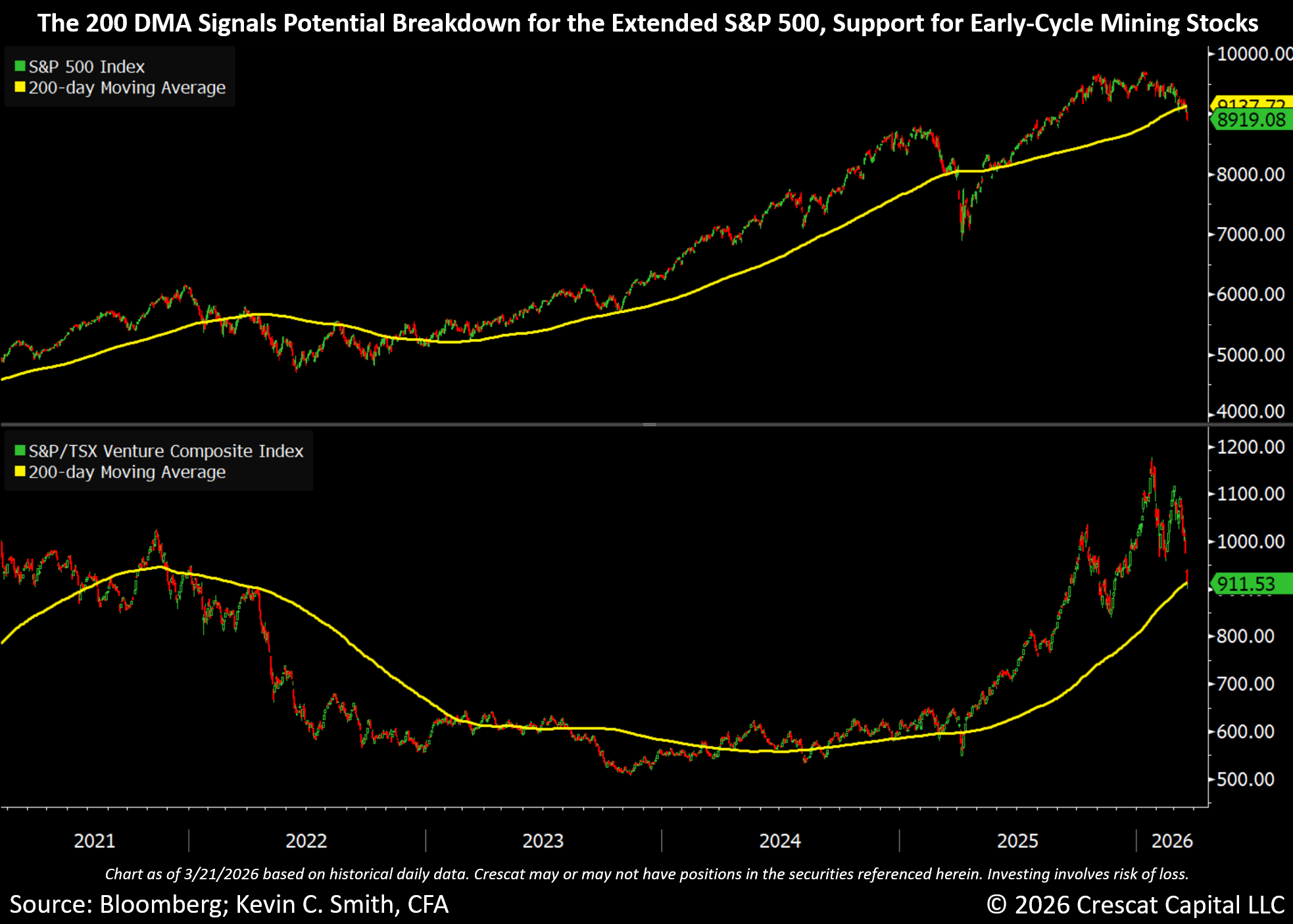

Technical Support for Gold Stocks; Resistance for the S&P 500

The large cap S&P 500 and Nasdaq 100 (QQQ) indices finally appear to be just starting to break down from record valuations, as we would expect with the new geopolitical conflict and resulting likely inflation and higher interest rates, but gold, silver, and mining stocks have sold off significantly more than these indices since Israel and the US first struck Iran on February 28. We think that presents an incredible short-term buying opportunity for the undervalued and still uncrowded mining stocks, especially the premier small cap explorers that we favor in our portfolios. Meanwhile, we see the long-slowing momentum, and now breakdown from the 200-day moving as a potential sell trigger for late-cycle, overcrowded, and overvalued US large cap equity indices and megacap tech stocks.

Interestingly, both mining stocks and the large cap indices are near their critical 200-day moving average support and resistance levels, but the two groups have highly divergent valuation and growth profiles. The indices of the high-growth, undervalued mining stocks are deeply oversold and hover at or above their 200-day moving average. The S&P/TSX Venture Composite Index, a proxy for small cap exploration focused miners, has already come down 23% from its January 23 recent high and could find strong support. It is now right on the 200-day moving average. The small cap exploration focused miners where Crescat is tilted have been outperforming the larger cap producing miners in the current pullback. From February 27 through March 20, the large cap VanEck Gold Miners ETF (GDX) (GDX) has declined 31%, while the VanEck Junior Gold Miners ETF (GDXJ) (GDXJ), a mid-tier producer index, is down 33%. Both of these ETFs hover just above the 200-day moving average now.

The S&P 500 and Nasdaq 100, however, look like they have just critically broken the 200-day moving averages. Yet, the S&P 500 is down only 6.8% from its recent January 28 high. In our view, it has substantially further downside ahead to get to reasonable valuations based on market history. The broad US large cap indices could finally be poised to break down hard from historically high fundamental valuations, which, in our analysis, are comparable to those at prior major market tops in 1929 and 2000.

Both the GDX and GDXJ ETFs have 14-day Relative Strength Index (“RSI”) readings below 30, a level typically associated with oversold conditions suggestive of a potential for a near-term rebound. Note, the last two times GDXJ 14-day RSI was sub 30 in March 2023 & October 23, there was a 34.6% and a 27.9% rally, respectively, within just two months. For an industry that just led the entire stock market in 2025, such a sharp rebound would not surprise us at all.

Although pullbacks can be painful and unsettling in the moment, they often create some of the most attractive opportunities for disciplined investors. When it comes to mining stocks today, these aphorisms apply:

“Buy when there’s blood in the streets, even if the blood is your own.” – Baron Rothschild

“The time of maximum pessimism is the best time to buy.” – Sir John Templeton

“Be fearful when others are greedy and greedy only when others are fearful.” – Warren Buffett

Oil Price Future Less Clear than Gold

Importantly, mining equities have come under pressure not only from the decline in underlying precious metals prices, but also from growing concerns around operating-cost inflation, particularly the risk that a sustained rise in oil prices could compress margins across the sector, especially among the producers who have been enjoying strong margins.

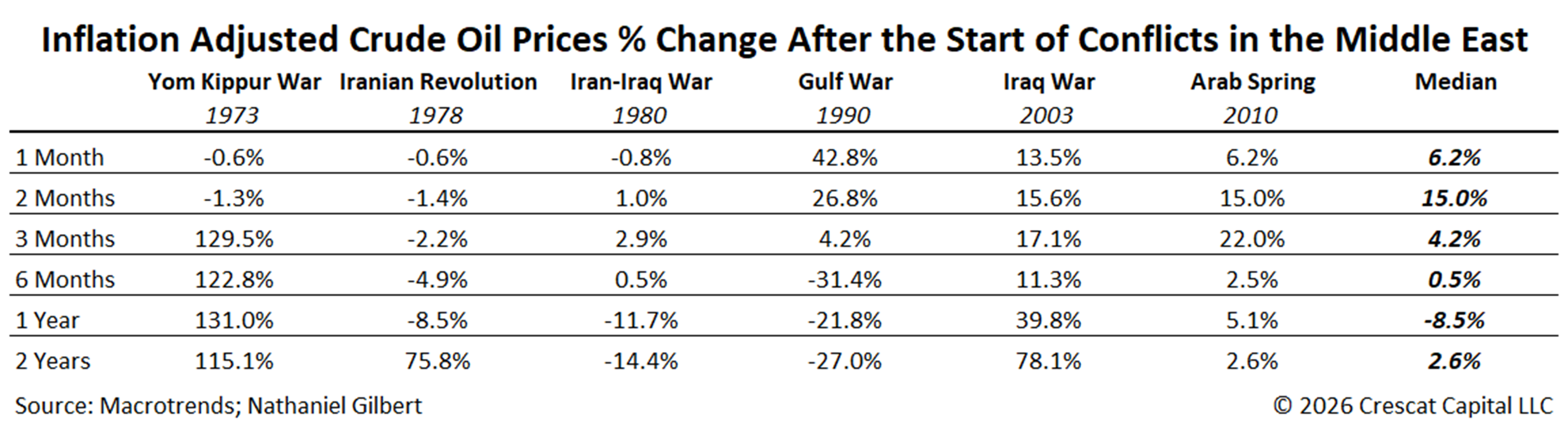

We have shown that higher oil prices do not mean that metal prices cannot go even higher. At this stage, however, the ultimate effect of recent geopolitical developments on the long-term path of oil prices remains unclear. The US is the largest oil-producing country in the world today and is now a net exporter, unlike in the 1970s when it was dependent on Middle East oil. Although the market has understandably responded to the risk of higher energy costs, it is too early to conclude whether the current move in crude reflects a lasting shift in fundamentals or a shorter-term geopolitical premium. To provide perspective, the table below illustrates the inflation-adjusted percentage change in crude oil prices following the onset of past major Middle East conflicts over various time horizons.

Still Early Innings in a New Secular Bull Market for Mining Stocks

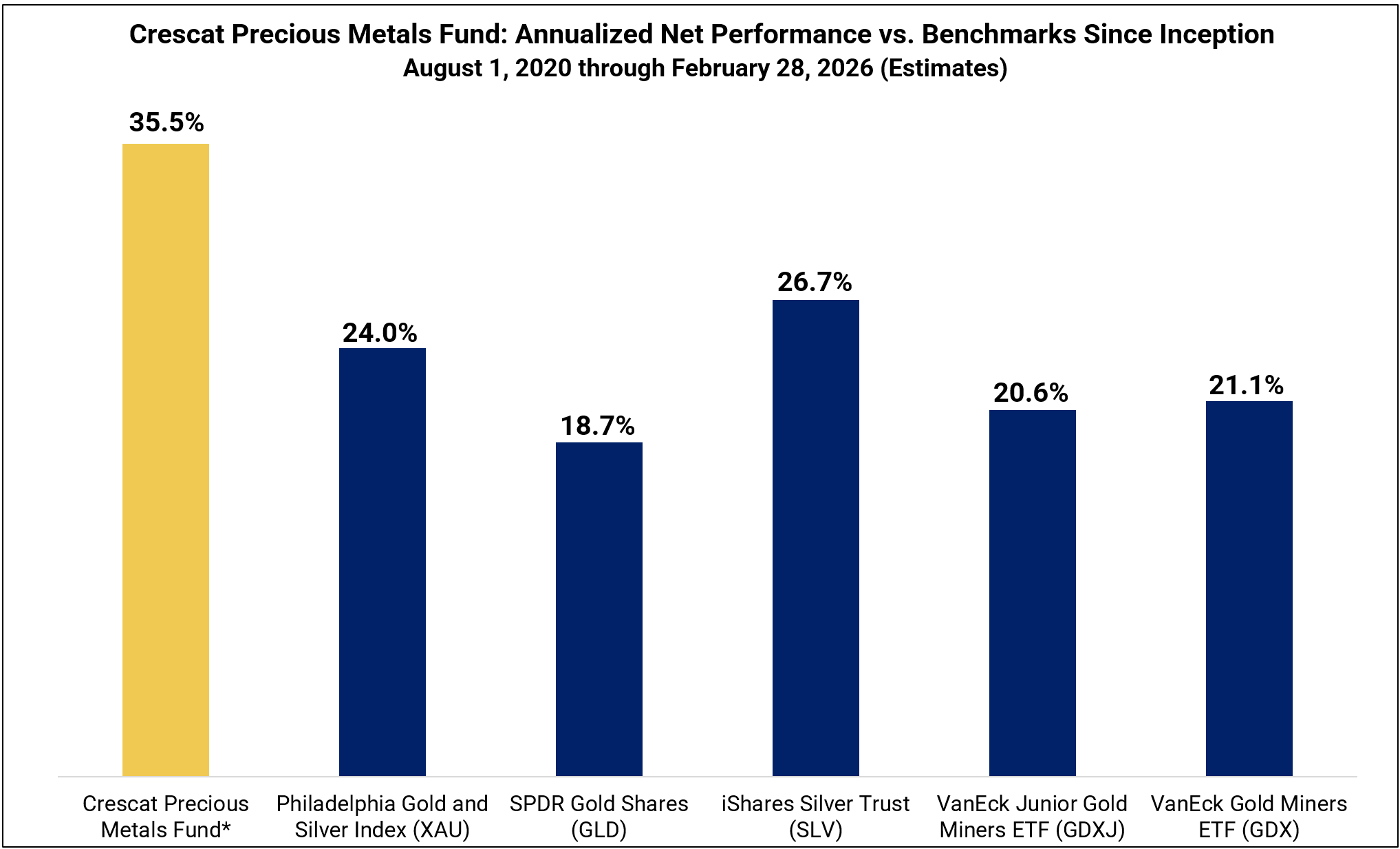

We launched our precious metals fund in 2020 and began allocating heavily to exploration mining companies at that time because we believed the sector was entering the early innings of a major multi-year bull cycle. That view was, and continues to be, driven by our conviction that the industry faces deep structural supply shortages. At the same time, a macro backdrop characterized by inflationary pressures and unsustainable sovereign debt burdens has set the stage for a gold super cycle. More than a decade of underinvestment in mining has created a favorable supply and demand imbalance for metal prices at a time when the world needs more metals than ever. This argues for strong growth ahead for the mining industry revenues, earnings, and new investment dollars poised to pour into the industry for exploration and mine development. Meanwhile, investors’ love affair with big technology stocks and apprehension toward mining still leaves the crucial mining industry with valuations that are ultra depressed. Such is a formula for much higher stock prices for precious and critical metals miners in the years ahead, in our view.

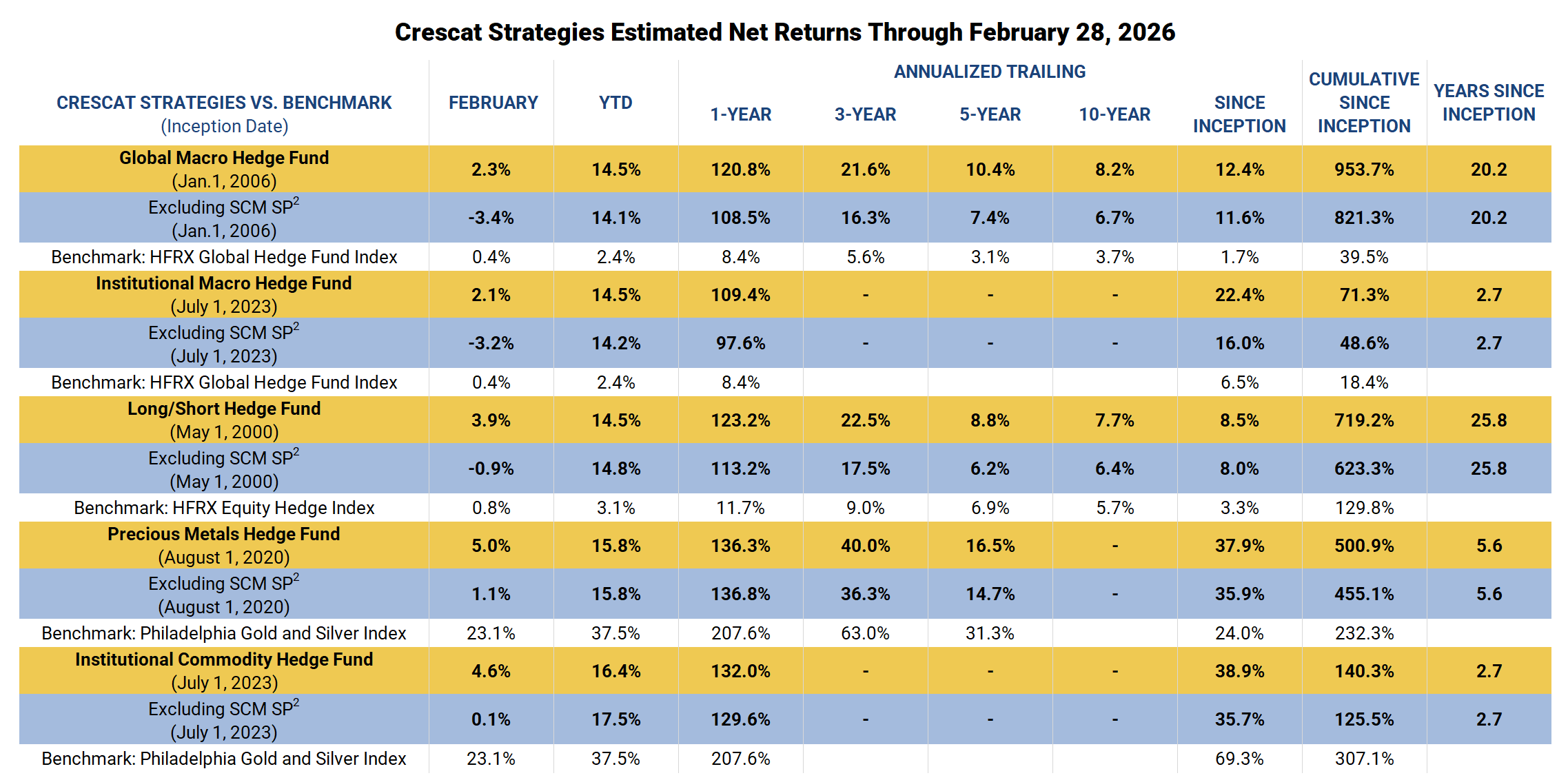

Crescat Performance and Call to Action

For our existing investors, we want to first thank you for your continued trust and support. In January of this year, we heard from a number of you who wished you had added at the end of 2024. This pullback is that moment again. The same macro environment that rewarded your conviction in 2025 has not reversed, it has deepened. We believe this is the time to consider an additional allocation. And for those who are comfortable where they are, staying put with a thesis this intact is equally the right call.

For those who stayed on the sidelines feeling that 2025 was too strong a year to come in after, this is your opportunity to get positioned. The 2025 performance was significant, but the case for precious metals and mining equities was never a one-year story. The pullback has reset prices without resetting the thesis. We believe this is a cleaner setup than most investors get and an opportunity to be positioned ahead of the next leg. April 1 is the date to get positioned.

*See important disclosures below. Past performance does not guarantee future results. Investing involves risk, including risk of loss.

Sincerely,

Kevin C. Smith, CFA, Founder & CEO

Nathaniel Gilbert, Analyst

References

- 1 – Net returns reflect the performance of an investor who invested from inception and is eligible to participate in new issues and side pocket investments. Net returns reflect the reinvestment of dividends and earnings and the deduction of all expenses and fees (including the highest management fee and incentive allocation charged, where applicable). An actual client’s results may vary due to the timing of capital transactions, high watermarks, and performance.

- 2 – Performance figures presented Excluding SCM SP represent the fund’s net returns calculated without the impact of the San Cristobal Mining, Inc. side pocket that was designated on July 1st, 2024. The side pocket includes a private equity asset that is not available to new investors in the funds on or after July 1, 2024. Excluding these assets provides a clearer view of the performance to investors coming into the funds after that date. New investors cannot participate in the SCM Side Pocket and will not share in its potential gains or losses. Investors should consider both the overall performance and the performance excluding the side pocket when evaluating the fund’s returns.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Incyte: An Undervalued Healthcare Gem

Tom Brady pays Logan Paul compliment after flag football game

Joe Amabile Bets on Bachelor Return After Taylor Cancellation

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Adidas – Corporette.com

-

Politics2 days ago

Politics2 days agoJenni Murray, Long-Serving Woman’s Hour Presenter, Dies Aged 75

-

Tech5 days ago

Tech5 days agoAre Split Spacebars the Next Big Gaming Keyboard Trend?

-

Crypto World2 days ago

Crypto World2 days agoNIO (NIO) Stock Plunges 6.5% as Shelf Registration Sparks Dilution Worries

-

Crypto World1 day ago

Crypto World1 day agoBest Crypto to Buy Now: Strategy Just Spent $1.57 Billion on Bitcoin During Fear While Early Investors Quietly Enter Pepeto for 150x Potential

-

News Videos4 days ago

News Videos4 days agoRBA board divided on rate cut, unusually buoyant share market | Finance Report | ABC NEWS

-

Crypto World1 day ago

Crypto World1 day agoBitcoin Price News: Bhutan Sells $72 Million in BTC Under Fiscal Pressure, but the Smart Money Entering Pepeto Sees What the Market Does Not

-

Business7 days ago

Business7 days agoAustralian shares drop as Iran war enters third week

-

Crypto World7 days ago

Crypto World7 days agoCrypto Lender BlockFills Enters Chapter 11 with Up to $500M in Liabilities

-

Politics5 days ago

Politics5 days agoThe House | The new register to protect children from their abusers shows Parliament at its best

-

Fashion7 days ago

Fashion7 days ago25 Celebrities with Curly Hair That Are Naturally Beautiful

-

Tech3 days ago

Tech3 days agoinKONBINI Lets You Spend Summer Days Behind the Register

-

Politics6 days ago

Politics6 days agoReal-time pollution monitoring calls after boy nearly dies

-

Crypto World4 days ago

Crypto World4 days agoCanada’s FINTRAC revokes registrations of 23 crypto MSBs in AML crackdown

-

NewsBeat4 days ago

NewsBeat4 days agoResidents in North Lanarkshire reminded to register to vote in Scottish Parliament Election

-

Business7 days ago

Business7 days agoMeta planning major layoffs as AI spending and automation reshape workforce

-

News Videos5 days ago

News Videos5 days agoPARLIAMENT OF MALAWI – PAC MEETING WITH REGISTRAR OF FINANCIAL ON AMARYLLIS HOTEL – INQUIRY LIVE

-

Business11 hours ago

Business11 hours agoNo Winner in March 21 Drawing as Prize Rolls to $133 Million for Next

-

Entertainment7 days ago

Oscars reunite Rob Reiner supergroup of 17 stars for emotional tribute: Here's who appeared on stage

-

Business4 days ago

Business4 days agoWho Was Alex Pretti? 5 Key Facts About the ICU Nurse Killed by Federal Agents in Minneapolis

You must be logged in to post a comment Login