Crypto World

Stablecoin yield rewards (likely won’t be) banned under OCC proposal: State of Crypto

The Office of the Comptroller of the Currency published its proposed rulemaking to regulate stablecoins under the GENIUS Act, sparking questions about whether it was banning yield payouts from crypto companies.

You’re reading State of Crypto, a CoinDesk newsletter looking at the intersection of cryptocurrency and government. Click here to sign up for future editions.

The narrative

The Office of the Comptroller of the Currency (OCC), a federal banking regulator, published a notice of proposed rulemaking pursuant to the GENIUS Act explaining how it might oversee stablecoins. Most of it appears straightforward, but the portion addressing yield seems ambiguous, and possibly even controversial.

Why it matters

The OCC published its first take at rulemaking under the GENIUS Act, the first step toward turning the 2025 law into actual, applicable rules for crypto companies to abide by. Controversially, it seems to propose setting up new restrictions around how stablecoin issuers and their partners can offer yield payments to end users.

Breaking it down

Just to get this out of the way: Most of this 376-page proposal seems fairly straightforward. Provisions address custody controls, capital requirements and the other prosaic regulatory details that one would expect from a proposal seeking to govern the U.S. stablecoin sector. This newsletter may touch on those details in a future edition.

The most controversial part appears to be the sections addressing stablecoin yield and how issuers and affiliates can handle those. According to multiple people tracking this process, speaking on condition of anonymity to discuss an active rulemaking proposal candidly, these sections also seem to be ambiguous. One individual said the OCC seemed to be claiming the authority to ban third parties from offering yield from holding stablecoins, exceeding its authority in the process. But two others said the proposal fit the language of the law defined in GENIUS, and that they had no concerns about yield being banned unilaterally.

What the provisions might do is place restrictions on how stablecoin issuers’ partner companies can pay out interest on stablecoin deposits, the yield we’ve been referring to here.

“[The] proposed [section] provides that permitted payment stablecoin issuers must not pay the holder of any payment stablecoin any form of interest or yield (whether in cash, tokens, or other consideration) solely in connection with holding, use, or retention of such payment stablecoin,” the proposal said. “The OCC understands that issuers could attempt to make prohibited payments of interest or yield to payment stablecoins holders through arrangements with third parties.”

The section went on to list some of these third-party relationships but said “it would not be possible to identify in detail all, or even most, of the potential arrangements.”

However, the proposal said that the OCC would presume these payments are solely for yield purposes if there was a contract to that effect and third parties would be defined as entities paying yield as a service.

Companies would be able to push back and “rebut the presumption” if they have evidence their contractual relationship does not meet those terms, the proposal said.

Companies like Coinbase and Circle might have to tweak the terms of their relationship to abide by the terms of the proposal, as might companies like PayPal and Paxos, the issuer of PayPal’s PYUSD stablecoin, two people said about this section.

Matthew Sigal, head of digital assets research at VanEck, also shared this view, saying on X (formerly Twitter) that companies like Coinbase would have to make their agreements look more like loyalty programs than interest payments.

One confusing part about the proposal, one individual said, is in the definition of an “affiliate.” A company could be an issuer or an affiliate, where affiliates may not be able to issue yield solely for holding deposits, but the proposal appears to create a third category based on ownership stakes. If an issuer has a 25% or greater stake in a third-party, they would not be able to offer payments on yield, which might open the door for third-parties that don’t have such ownership stake concerns.

Similarly, the wording addressing “white-label relationships” may bar yield payments, but it would depend on the terms of the contract between the issuer and the company associated with the stablecoin, the person said. This is the sort of setup PayPal and Paxos have.

To further add to the confusion, stablecoin yield is also one of the issues holding up the advancement of the market structure legislation that the crypto industry continues to hope for. Two people said the OCC proposal might mean that Congress does not need to address yield in the market structure bill at all, but others said there is zero chance Congress will skip over this portion of the bill.

Yield isn’t the only issue holding up the bill — ethics provisions concerning President Donald Trump and his family’s crypto activities, as well as anti-money laundering and know-your-customer rules, still need to be worked out — but if the market structure bill becomes law, it will again reshape how stablecoins can operate in the U.S.

As a result, it is likely that this part of the OCC proposal will not be implemented as-is.

If the market structure bill does become law before the OCC can finalize its rules, the regulator will have to issue an interim proposal to remain compliant with the new law. Otherwise, there will be a whole separate rulemaking process later down the line.

On the market structure bill itself, individuals said that there is some updated draft language circulating among lawmakers but there is no deal between the banking industry and the crypto industry yet.

This week

- There are no government hearings or meetings scheduled as of press time addressing crypto-related issues.

If you’ve got thoughts or questions on what I should discuss next week or any other feedback you’d like to share, feel free to email me at [email protected] or find me on Bluesky @nikhileshde.bsky.social.

You can also join the group conversation on Telegram.

See ya’ll next week!

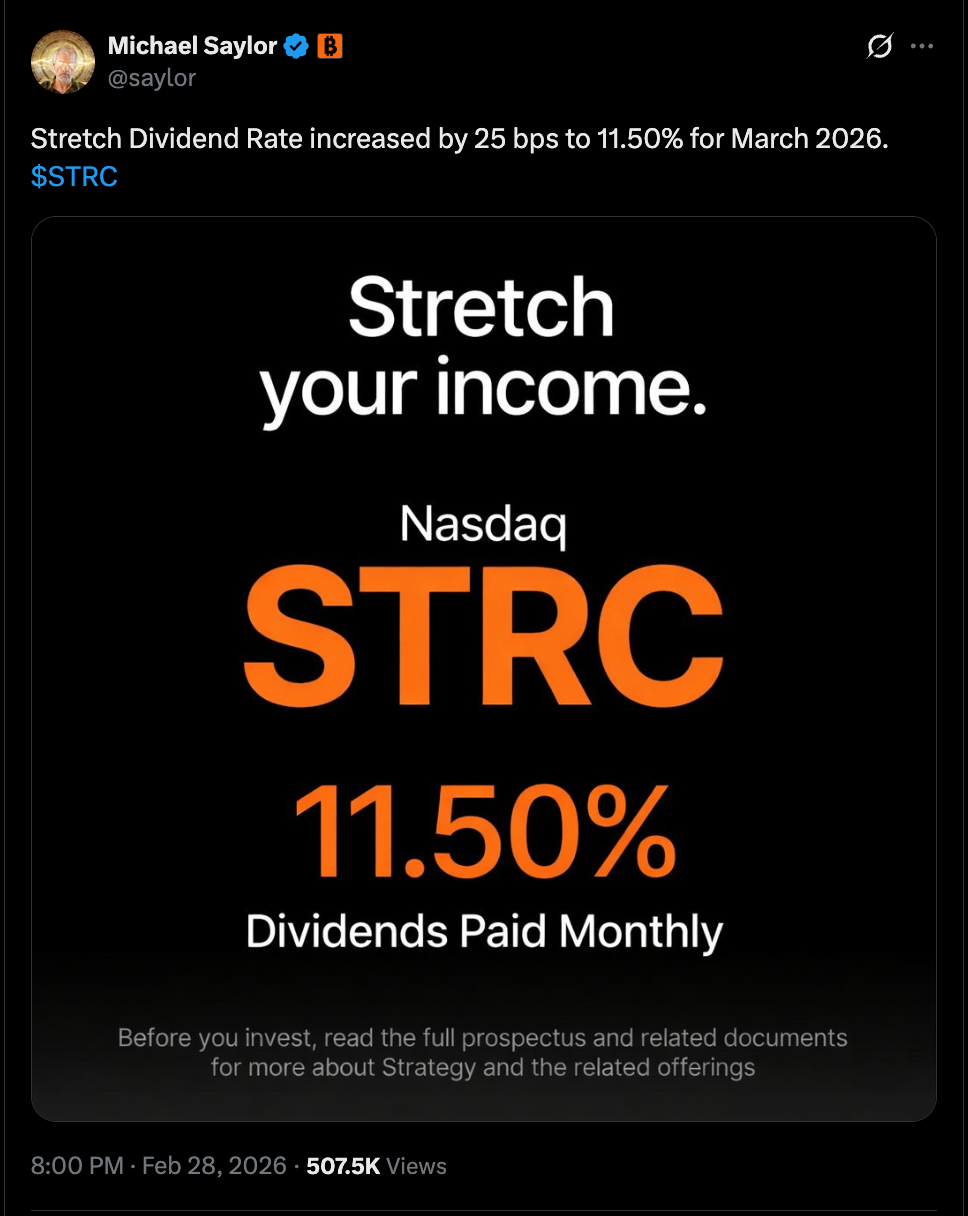

Strategy chairman Michael Saylor used social media to announce a dividend adjustment at the Bitcoin treasury vehicle STRC. The company has raised the monthly distribution on STRC (EXCHANGE: STRC) to 11.50% for March 2026, up from 11.25%. STRC is a perpetual preferred stock with a variable yield that changes on a monthly basis, a design intended to balance income with trading dynamics around its $100 par value. The company’s update confirms that the payout remains monthly, with the next distribution scheduled for March 31 to shareholders of record. The move comes amid a broader pivot in Strategy’s financing approach and a continuing expansion of its Bitcoin (CRYPTO: BTC) holdings.

The STRC update, published on the company’s own site, explains that the dividend rate is adjusted monthly to encourage trading activity around the par value and to help dampen price volatility. This mechanism is part of a broader strategy to rely more on preferred stock than common equity for BTC-related funding. The social post from Saylor aligns with Strategy’s stated direction and adds color to a year in which the company has increasingly leaned on structured finance instruments to support its Bitcoin purchases.

On the same subject, February marked a notable shift in Strategy’s funding approach. CEO Phong Le described a transition away from issuing common stock to fund Bitcoin acquisitions toward issuing more preferred shares. The company has argued that the stretch and associated perpetual preferreds have proven effective at raising capital, citing last year’s fundraising results as a proof point.

Le has highlighted the scale of STRC and perpetual issues in the market, noting that last year these instruments raised about $7 billion, representing roughly a third of the entire domestic preferred market. The company’s leadership has signaled that 2026 could see more of a structural emphasis on preferred capital as a means to fund ongoing Bitcoin accumulation while managing shareholder dilution and equity risk. In this context, the market has watched Strategy continue to accumulate BTC, even as Bitcoin’s price has swung lower amid a broader risk-off environment.

In the meantime, Strategy has faced a tougher market backdrop. The price of Bitcoin itself has slipped significantly since October, and Strategy’s common stock has mirrored a broader downturn in crypto-related equities. The company’s stock, which tracks as a proxy for its Bitcoin holdings and management strategy, has retreated from the highs seen in late 2024 and has traded in a lower range in recent months. Data from Saylor Tracker shows Strategy’s aggregate Bitcoin purchases and the balance sheet moving forward, even as the stock’s price has come under pressure from a challenging macro and crypto market environment.

Looking at the larger picture,Bitcoin (CRYPTO: BTC) has fallen by more than a quarter year-to-date, a factor that has weighed on public companies with substantial corporate treasuries. In parallel, the Bitwise Bitcoin Standard Corporations ETF (EXCHANGE: OWNB) has also declined, underscoring the broader drag on equities tied to crypto balance sheets. The latest data shows Strategy’s BTC holdings continuing to accumulate, even as near-term price movements complicate capital planning. Strategy’s trackers and public disclosures show a continued cadence of purchases and a growing balance sheet despite market headwinds.

From a performance perspective, Strategy has faced a grim year in the stock market. The company reported a net loss of $12.4 billion for Q4 2025, released in February, even as revenue rose modestly to about $123 million for the quarter. The earnings backdrop has weighed on investor sentiment, contributing to a broader decline in Strategy’s share price, which fell sharply from the record highs reached in late 2024. The stock hovered around $129.50 at the end of the week, well below its peak levels, highlighting the contrast between the company’s aggressive BTC accumulation and the market’s appraisal of its profitability trajectory. Within this landscape, the price of BTC remains a critical driver of Strategy’s fortunes, underscoring the sensitivity of a BTC-focused treasury model to macro and crypto volatility. The company’s long-running accumulation strategy has included notable milestones, such as the 100th BTC purchase and the expansion of its balance sheet to 717,722 BTC, a testament to the scale of its framing of corporate treasury capacity around Bitcoin.

As the market contends with volatility, Strategy’s approach highlights a broader industry trend: corporate treasuries in the crypto space increasingly lean on structured finance and preferred equity to finance continued accumulation, balancing the goal of owning more BTC with managing equity risk and investor expectations. The broader market environment—characterized by price swings in BTC and a wave of related financial instruments—continues to challenge traditional capital-raising methods, pushing some issuers to rethink balance-sheet financing in favor of instruments like STRC and other perpetual preferreds. The company’s ongoing BTC purchases, including the relatively recent tranches, underscore a willingness to endure short-term price pressures for the longer-term objective of building a sizable Bitcoin reserve. The evolution of Strategy’s capital stack—moving from common equity toward preferred capital—also raises questions about how such a shift will influence liquidity, dividend policy, and the eventual realization of BTC gains in the face of market cycles. The narrative surrounding STRC’s yield adjustments and the related financing strategy paints a picture of a company that remains deeply committed to Bitcoin accumulation, even as it navigates a period of volatile prices and mixed financial results.

In a landscape where both crypto prices and the equities tied to corporate treasuries face headwinds, Strategy’s strategy remains closely watched by investors seeking exposure to Bitcoin through a corporate balance sheet. The company’s public communications, including updates to STRC’s dividend policy and its pivot toward preferred financing, signal a concerted effort to optimize capital structure while maintaining Bitcoin exposure. For market participants, the question remains how sustainable a perpetual preferred-based approach will be in delivering consistent returns to shareholders as BTC price and macro conditions evolve. The intersection of rising dividend yields, ongoing BTC purchases, and shifting financing sources will continue to shape the trajectory of Strategy and its peers in the crypto treasury space.

Why it matters

Strategy’s renewed emphasis on STRC’s elevated dividend rate and the ongoing shift toward preferred capital exposure matters because it reflects a practical adaptation to the realities of financing a BTC-heavy corporate treasury in a volatile market. By adjusting the monthly yield for STRC and maintaining a steady payout schedule, the company aims to offer income stability to investors while cycling through capital to acquire more BTC. This approach could influence the appetite for similar structures among other corporate treasuries seeking to scale Bitcoin holdings without diluting common equity, potentially shaping the broader landscape of crypto corporate finance.

For investors, the shift away from common stock toward preferred capital signals a potential change in risk and return profiles. Preferreds typically occupy a different position in the capital structure, often offering higher yields with a priority claim on assets and earnings relative to common shares. If Strategy can sustain its BTC accumulation while delivering consistent yields, it could attract institutional investors seeking exposure to Bitcoin through a structured instrument with a predictable income stream. However, the persistent price volatility of BTC and the performance of Strategy’s own equity remain critical inputs in assessing the risk-reward balance of this approach. The ongoing performance of Strategy’s BTC holdings, its Q4 2025 earnings, and the trajectory of its financing strategy will likely influence investor sentiment and the broader adoption of similar mechanisms in the crypto treasury space.

Ultimately, the interplay between BTC price movements, dividend policy, and the company’s financing choices will determine how STRC and other crypto treasury instruments fare over time. The market is watching whether the pivot to preferred capital can deliver a sustainable path to capital formation that supports Bitcoin accumulation while avoiding excessive dilution or cost of capital concerns. As Strategy continues to publish updates on its BTC purchases and balance sheet composition, observers will gauge whether this model can translate into durable value creation for shareholders in a sector still defining its long-term viability.

What to watch next

- Monitor STRC’s next monthly dividend adjustment and March 31 payout date for record holders.

- Watch Strategy’s ongoing pivot toward preferred capital and any subsequent financing rounds or issuances.

- Track BTC purchases and total holdings, including the 592 BTC purchase in the week of Feb. 16, to see if the pace of accumulation accelerates or slows.

- Assess Strategy’s Q1 2026 results for any improvement in operating metrics alongside BTC balance sheet expansion.

- Observe market reactions to STRC dividend changes and any European listings related to STRC ETP developments.

Sources & verification

- STRC dividend rate and payout schedule confirmation on Strategy’s official Stretch page.

- Saylor’s post on X (formerly Twitter) confirming the dividend adjustment.

- Strategy’s February statement about shifting from common stock to preferred stock for BTC funding.

- Strategy’s public disclosures of BTC purchases, including the 592 BTC purchase and total holdings of 717,722 BTC.

- Q4 2025 results reporting a net loss of $12.4 billion and revenue of about $123 million.

Strategy’s evolving capital mix and ongoing BTC accumulation

Strategy’s leadership has publicly framed 2026 as a year of structural evolution, with STRC (EXCHANGE: STRC) and other perpetual preferred instruments playing a central role in capital formation. The company’s chairman, Michael Saylor, communicated through a social post that STRC’s dividend rate is being adjusted monthly, targeting an 11.50% yield for March 2026. This adjustment follows a formal update posted on Strategy’s Stretch site, which notes that the payout is aligned with a par value of $100 and that the rate changes are designed to encourage trading around that level while dampening volatility. The monthly cadence remains intact, providing a predictable income stream for holders and a predictable funding mechanism for ongoing BTC acquisitions.

The broader policy shift toward preferred capital aligns with remarks from Strategy’s leadership in February, when CEO Phong Le described the company’s decision to pivot away from common stock issuances as a primary funding source for Bitcoin purchases. As the company continues to accumulate BTC, the balance sheet now holds a substantial stake—717,722 BTC—reflecting a disciplined approach to building a corporate treasury anchored by the world’s leading cryptocurrency. The latest tranche, a 592 BTC purchase in the week of February 16, underscores the ongoing emphasis on scalable BTC accumulation even as market prices fluctuate, with the company’s decision to finance purchases through preferred stock helping to manage dilution concerns and investor expectations.

While the macro backdrop has pressured crypto and related equities, Strategy’s financing strategy highlights a broader industry shift toward asset-backed, income-generating structures that can sustain long-term BTC holdings. The company’s stock performance and the price actions of related instruments—including the Bitwise Bitcoin Standard Corporations ETF (EXCHANGE: OWNB), which is also down—reflect the challenging environment for investor sentiment around crypto corporate treasuries. Nevertheless, Strategy’s approach demonstrates a commitment to leveraging preferred income to support a growing Bitcoin reserve, an approach that could influence other corporate treasuries seeking scalable, income-generating financing alternatives as the crypto industry matures.

Strategy chairman Michael Saylor said in a social media post on Sunday that the largest Bitcoin (BTC) treasury company is raising the dividend on its STRC preferred stock, also known as “Stretch,” to 11.50% for March 2026, from the previous 11.25%.

STRC is perpetual, meaning the company is not obligated to buy back the stock at any specified date, and features a variable yield that changes monthly.

A Friday update on the company’s website confirmed Saylor’s post. “STRC’s dividend rate is adjusted monthly to encourage trading around STRC’s $100 par value and to help strip away price volatility,” according to the website. The dividend is also paid monthly. with the next payout date on March 31, to shareholders of record

In February, Strategy CEO Phong Le said the company is pivoting away from issuing common stock to fund its BTC purchases and toward issuing more preferred shares.

“Last year, a stretch and our perpetual preferreds raised $7 billion. That’s 33% of the entire preferred market,” Le said.

“As we go throughout the course of this year, we expect structure to be a big product for us,” he said, adding, “We will start to transition from equity capital to preferred capital.”

To be sure, the company continues to accumulate Bitcoin amid a market drawdown that has nearly halved the price of Bitcoin since October and driven down the share prices of digital asset treasury companies.

In the year to date, BTC has lost 23.2% of its value, while the share price of Bitwise Bitcoin Standard Corporations ETF (OWNB) is down 16.1%. That exchange-traded fund provides exposure to public companies holding significant amounts of Bitcoin on their balance sheets.

Related: Strategy yield wrapper lands in Europe as 21Shares lists STRC ETP

Strategy records $12.4 billion loss in Q4 2025

Strategy in early February reported a net loss of $12.4 billion for the fourth quarter of 2025, leading to investors pushing the company’s share price down by 13% to about $107 per share.

Despite revenue for the quarter increasing 1.9% year-over-year to about $123 million, the company’s stock has been in freefall.

Strategy’s (MSTR) common stock price briefly hit a high of $543 per share during intraday trading in November 2024, before falling back down below $300 in February 2025.

The company’s stock has fallen by about 75% since the November 2024 peak, closing on Friday at $129.50 a shares.

The price of BTC is trading well below Strategy’s average purchase cost of $76,020 per Bitcoin, according to data from the company.

Strategy’s last bought BTC during the week of Feb. 16, when the company purchased 592 BTC, valued at over $39.8 million, bringing its total holdings to 717,722 BTC, and marking its 100th BTC acquisition.

Magazine: Bitcoin’s ‘biggest bull catalyst’ would be Saylor’s liquidation: Santiment founder

The mood around digital assets has shifted again among the world’s largest allocators, according to Ron Biscardi, CEO of iConnections, which runs one of the largest capital introduction conferences globally.

Biscardi, who has spent more than 25 years in the alternative investment industry and runs a platform that represents over $55 trillion in assets, has a front-row seat. His firm tracks thousands of meetings between fund managers and institutional investors each year. That data shows how quickly sentiment can turn.

After a couple of “rough” years following the crypto market crash following the FTX collapse in 2022, interest began to stabilize at last year’s conference, he recalls. “[In 2025] we started to see funds wanting to come back, wanting to spend some money,” he said. Optimism around a more crypto-friendly regulatory stance in Washington helped, even if progress has been slow.

“I feel like what we’re seeing now at the event [this year] is a more normal experience,” Biscardi said. “It’s not extremely crazy, but it’s also not [like] ‘I don’t want to go anywhere near it.’”

A change of tone

More than 75 digital asset funds participated in this year’s event, generating roughly 750 meetings between managers and allocators, a level comparable to 2022 when crypto interest soared before the FTX collapse. Nearly one quarter of limited partners on the iConnections platform now indicate interest in digital asset strategies, reinforcing that crypto has become an established sleeve within alternatives rather than a fringe allocation.

Family offices represent the largest LP cohort expressing interest, consistent with their track record of backing emerging and innovation-driven asset classes.

And this trend has been growing in recent years. While some family offices remain cautious about the asset, many traditional wealth managers are under mounting pressure to deliver digital assets to wealthy clients, particularly in crypto hotspots like Dubai, Switzerland and Singapore.

This interest is very much alive despite the crypto winter, with the price of bitcoin down nearly 25% since the beginning of the year and its market cap losing more than a trillion in value since October’s all-time high. Stocks of popular crypto companies, like Coinbase (COIN) or Strategy (MSTR), are also trading significantly lower this year, underperforming most other tech stocks.

Biscardi, however, believes digital asset managers are “very, very close to achieving institutional legitimacy.” Bitcoin, he said, has already crossed that line, but altcoins are close. “The last piece is really the regulatory framework that lets them do it safely.”

For chief investment officers, that issue dominates. “The regulatory hurdles are number one,” Biscardi said. “It just always goes back to that.”

Large allocators, he noted, are fiduciaries. “It’s not their money, they’re fiduciaries for other people’s money, and it might be a super interesting category, but they’re just not going to allocate there until they can tell their board that they’re doing it in a responsible, safe way.”

The tone of the debate has also changed. In 2022, some investors still questioned whether crypto was real or a Ponzi scheme. “That I don’t hear any of that anymore,” Biscardi said.

In fact, some traditionally conservative pools of capital, for example, have stepped in. Endowments, which tend to focus on long-term stability and avoid sharp swings in new asset classes, have begun allocating to bitcoin and ether exchange-traded funds. The idea is not to overhaul portfolios but to add measured exposure that could lift returns in years when crypto markets perform well, especially as many investors expect equities to deliver more muted gains than in the past decade.

Still a risk asset

Nevertheless, allocators treat bitcoin “much more as a risk asset” than a store of value. “Bitcoin just hasn’t behaved that way,” he said, pointing to its correlation with equities rather than gold during market stress.

Similarly, direct token buying remains rare among institutions. Instead, he hears more about ETFs and fund structures. Limited partners rely on general partners to choose specific coins. “The LPs who get bought into the space are really looking to the GPs to make those decisions.”

What’s not rare is crypto companies investing in spreading awareness of their products and services. According to Biscardi, sponsorship numbers saw a substantial uptick at this year’s event, with companies like BitGo (BTGO), Galaxy Digital (GLXY), Ripple and Blockstream all holding top-tier sponsor status.

Read more: Bitcoin is stuck in a rut but JPMorgan says new legislation could be the ultimate spark

Key Takeaways

- Q4 FY25 earnings report scheduled for March 2, 2026

- Analysts project a $0.02 per share loss, significantly improved from last year’s $0.47 deficit

- Projected revenue of $390K represents substantial growth from prior year’s $62K

- Shares declined 8.4% on February 27, now trading beneath key technical indicators

- Implied volatility suggests potential 14.05% price swing following results

Quantum Computing Inc. approaches its fourth quarter fiscal 2025 earnings announcement scheduled for Monday, March 2, 2026, with recent price weakness creating uncertainty among shareholders. The stock experienced an 8.4% decline on February 27, closing at $8.278.

Daily trading activity registered approximately 3.37 million shares — representing a dramatic 78% reduction compared to the typical 15 million share average. This significantly lighter volume during the selloff may indicate limited selling pressure, though the implications remain subject to interpretation.

Technically, shares are positioned beneath both the 50-day moving average at $10.35 and the 200-day moving average at $13.70. Despite recent weakness, QUBT maintains gains exceeding 39% over the trailing twelve months, propelled primarily by enthusiasm surrounding its photonic computing platform.

The Street’s consensus estimate calls for a quarterly loss of $0.02 per share in Q4 2025. This figure represents substantial improvement compared to the $0.47 per share deficit recorded in the year-ago period.

On the top line, analysts anticipate revenues reaching $390K, a meaningful increase from the $62K generated in Q4 2024. Though absolute dollar amounts remain modest, the growth trajectory is capturing attention from market observers.

Luminar Deal Takes Center Stage

A significant narrative entering the earnings discussion involves the company’s $110 million all-cash purchase of Luminar Semiconductor Inc., formerly held by Luminar Technologies. This strategic transaction aims to provide QUBT with greater vertical integration and enhanced capability to generate consistent revenue streams.

Market participants will be focused on management commentary regarding semiconductor manufacturing schedules, fulfillment of existing orders, and any preliminary indicators of revenue acceleration stemming from the acquisition.

Wall Street Revises Expectations Lower

The analyst community presents a varied outlook. Lake Street analyst Max Michaelis maintained his Buy recommendation while adjusting his price objective from $24 down to $16 — nonetheless suggesting approximately 77% appreciation potential from current trading levels.

Ascendiant Capital Markets similarly reduced its target from $40 to $25 while preserving a Buy stance. Taking a more reserved approach, Wedbush established coverage with a Neutral rating and $12 price target, while Cantor Fitzgerald reaffirmed its Neutral position with a $15 target.

Rosenblatt Securities launched coverage in January with a Buy rating and $22 price objective. The aggregate consensus stands at Moderate Buy, comprising one Strong Buy, two Buys, two Holds, and one Sell among analysts providing coverage.

The mean price target across all tracked analysts reaches $18.00, implying approximately 99% upside from the February 27 trading price.

QUBT exhibits a beta coefficient of 3.44, indicating heightened volatility relative to broader market movements. The company maintains a market capitalization near $1.83 billion, with a negative P/E ratio of -13.40 consistent with its current unprofitable state.

Company insiders control 19.3% of outstanding shares. COO Milan Begliarbekov divested 2,860 shares on January 7 at $11.85 per share, trimming his holdings by approximately 10.55%. Institutional ownership remains minimal at 4.26%.

Options market activity suggests traders are anticipating a potential price movement of roughly 14.05% in either direction once earnings results are released.

The company will publish Q4 FY25 financial results prior to the market opening on March 2, 2026.

US lawmakers want regulators to investigate Binance over the alleged $1.7 billion in transfers to Iran-linked entities. The concerns come at a particularly interesting time amid rising geopolitical tensions in the Middle East. However, Binance has already refuted such allegations.

In a letter, 11 lawmakers led by Sens. Chris Van Hollen and Elizabeth Warren urged Treasury Secretary Scott Bessent and Attorney General Pam Bondi to launch a formal probe.

US Lawmakers Warn Binance Oversight May be at Risk

The senators raised serious concerns about the strength of Binance’s anti-illicit finance guardrails and its adherence to sanctions and anti-money laundering laws.

“These allegations raise grave concerns that poor illicit finance controls at Binance remain a significant threat to national security. Our illicit finance controls are dangerously compromised if enormous sums can flow through Binance to terrorist groups or sanctions evaders. The firm controls the world’s largest digital asset exchange; it is essential that bad actors cannot benefit from its platform,” the lawmakers stated.

According to reports cited by the lawmakers, investigators uncovered at least two Binance accounts. These accounts were used to channel assets to entities linked to the Iran-backed Houthis and the Islamic Revolutionary Guard Corps.

Furthermore, the reports alleged that Iranian nationals successfully accessed more than 1,500 Binance accounts.

The senators described the incident as indicative of a “broader deterioration” in Binance’s compliance functions. They warned that the fund movements directly threaten the exchange’s historic 2023 settlement with US authorities.

Under that plea agreement, Binance paid a $4.3 billion fine and its founder, Changpeng Zhao, stepped down as CEO. The company also agreed to stringent oversight by a DOJ-mandated independent compliance monitor.

The lawmakers argued the alleged illicit transfers align with a wider pattern of risky behavior.

They highlighted Binance’s launch of payment cards in parts of the former Soviet Union, which they claim provides a backdoor for Russian entities to evade international sanctions.

“In light of these issues, we are deeply troubled by the prospect that Binance may once again be prioritizing profits over its compliance obligations,” the lawmakers argued.

Labeling the situation a severe national security threat, the senators gave the Treasury Department and the DOJ until March 13, 2026, to detail the results of their investigations.

If authorities determine Binance breached its 2023 monitorship terms, the exchange could face catastrophic legal and financial repercussions.

Binance Touts Compliance Efforts

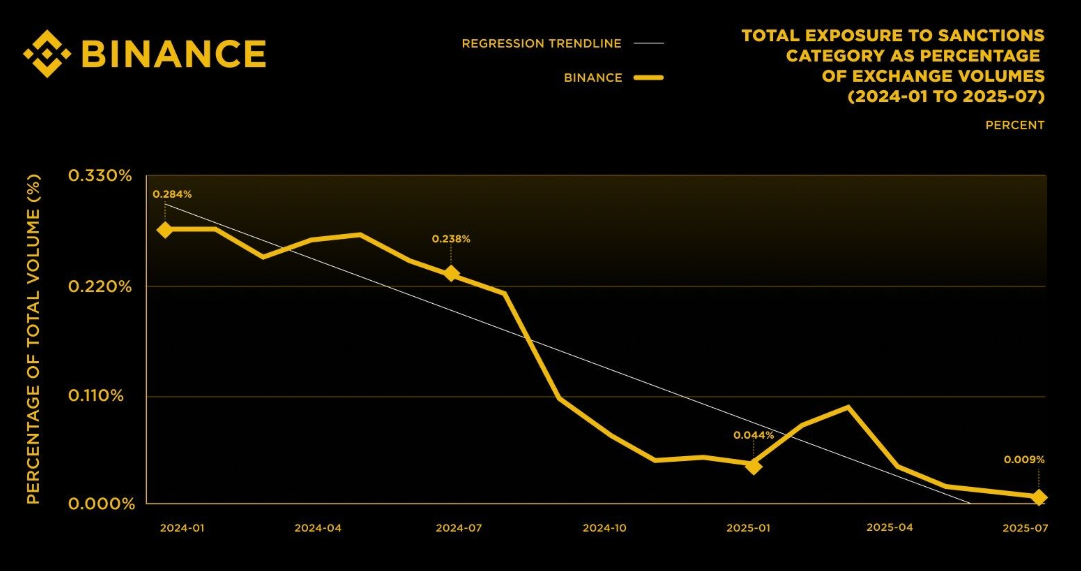

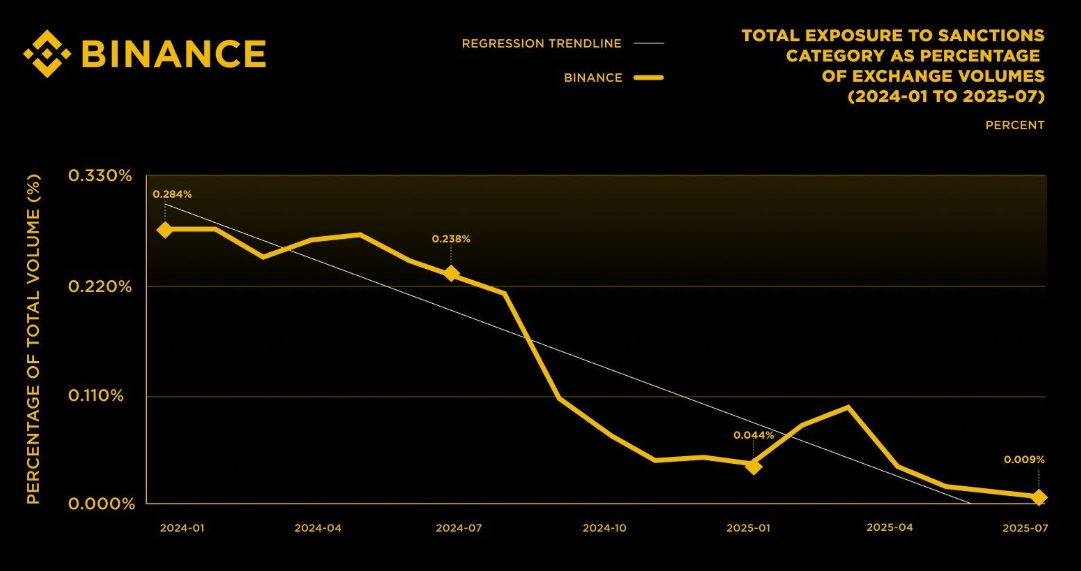

In a fierce rebuttal to the allegations, Binance defended its internal controls and noted a sharp decline in illicit activity on its platform.

According to the firm, its sanctions-related exposure dropped 96.8% over an 18-month period, falling from 0.284% in January 2024 to just 0.009% in July 2025.

The firm linked this progress to its “best-in-class” compliance program. It argued that the recent reports present a distorted viewpoint that fundamentally misunderstands standard control processes for digital asset platforms.

Binance stated that in the specific incidents cited by the media, it acted proactively, mitigated risks, offboarded the offending accounts, and coordinated with law enforcement.

“The facts are these: Binance’s compliance program is effective and it worked here. Any statement to the contrary is simply wrong,” the exchange concluded.

TLDR

- In his inaugural shareholder communication, Greg Abel designated Apple (AAPL), American Express (AXP), Coca-Cola, and Moody’s (MCO) as permanent portfolio positions

- The new CEO’s debut letter commits to continuing Buffett’s philosophy of value investing and maintaining a robust financial position

- Fourth-quarter operating profits declined 29% compared to the previous year, reaching $10.2 billion, influenced by insurance segment challenges

- Bank of America and Chevron didn’t make Abel’s list of untouchable holdings

- Buffett transitions to chairman role while maintaining a full-time office presence for advisory purposes

In his inaugural communication to shareholders, Greg Abel has outlined Berkshire Hathaway’s strategic direction as CEO, highlighting four equity positions the conglomerate intends to maintain indefinitely while disclosing a significant decline in quarterly profits.

Abel assumed the chief executive position from Warren Buffett beginning in 2026, following Buffett’s retirement announcement in May 2025. The legendary investor continues serving as chairman with plans to work full-time from the office.

The letter pinpointed four primary equity investments that Berkshire intends to preserve with “limited activity.” The quartet consists of Apple, American Express, Coca-Cola, and Moody’s.

Abel characterized these as companies Berkshire “understands well,” featuring solid management teams and promising long-term expansion prospects. He indicated the firm would only “significantly adjust” any position if fundamental changes occurred in its future outlook.

These four investments, combined with ownership stakes in five Japanese trading corporations, represent approximately two-thirds of Berkshire’s stock portfolio. The aggregate market value of these nine positions exceeds $200 billion.

What’s Not on the Forever List

Notably absent from the core holdings list were two top-five positions: Bank of America and Chevron. The Bank of America stake has been reduced by approximately half during the previous 18 months, declining to roughly 517 million shares with a market value near $28 billion.

The Chevron holding, valued at approximately $20 billion, similarly failed to earn “forever” designation from Abel. This exclusion has sparked discussion among longtime Berkshire observers.

Berkshire’s Apple investment has appreciated substantially beyond its initial purchase price. The conglomerate’s average cost basis stands around $27 per share, while the stock currently trades near $264. Although Buffett previously trimmed the Apple position by roughly 80% from peak levels, Abel’s correspondence indicates no additional reductions are anticipated.

Q4 Earnings Take a Hit

Berkshire disclosed fourth-quarter operating profits of $10.2 billion, representing a decline exceeding 29% from the year-earlier figure of $14.56 billion. The downturn stemmed partially from diminished results in the insurance operations.

For calendar year 2025, Berkshire generated operating earnings totaling $44.5 billion, falling short of 2024’s $47.4 billion but exceeding the five-year average of $37.5 billion.

Berkshire’s combined cash and Treasury bill reserves totaled $373.3 billion at quarter-end, representing a modest decline from the previous quarter’s $382 billion. Abel referenced this substantial liquidity as “dry powder” positioned for deployment when attractive investment opportunities emerge.

Uncertainty surrounds the matter of portfolio management responsibilities going forward. Abel lacks experience as an investment professional. Investment manager Ted Weschler will oversee approximately 6% of the portfolio, consistent with his allocation during Buffett’s tenure.

Abel stated that “responsibility ultimately rests with me as CEO” regarding capital allocation choices, with Buffett remaining available for consultation.

Key Takeaways

- Escalating US-Iran tensions following the reported death of Supreme Leader Khamenei in coordinated strikes trigger significant market repositioning.

- Oil markets respond with prices reaching seven-month peaks, with forecasts suggesting potential increases exceeding $10 per barrel.

- Traditional energy players like BP and Chord Energy provide direct commodity exposure while maintaining attractive dividend yields.

- Major defense contractors including Lockheed Martin and Northrop Grumman benefit from accelerating demand for advanced missile systems and stealth technology.

- Eos Energy represents a speculative opportunity tied to energy independence initiatives and infrastructure hardening driven by geopolitical uncertainty.

Following reports of Iranian Supreme Leader Ayatollah Ali Khamenei’s death in coordinated US-Israeli military operations, global financial markets have entered a period of tactical reallocation. Portfolio managers are rapidly shifting capital toward historically resilient wartime sectors.

Crude oil benchmarks have climbed to levels not seen in seven months. Defense spending projections continue climbing, while energy independence has reemerged as a central government priority.

We examine five equities currently drawing significant analyst attention amid this evolving landscape.

Energy Sector: Capitalizing on Crude Price Momentum

BP (BP)

BP operates as an integrated energy major headquartered in the United Kingdom, maintaining diversified operations across upstream production, downstream refining, and renewable energy development. Its global footprint provides natural hedging during commodity price volatility.

With Brent benchmarks approaching seven-month peaks, BP’s trading operations and refining spreads stand to benefit substantially. The equity currently offers a dividend yield exceeding 5% while trading at a forward price-to-earnings multiple below 9x.

The company executed $2.5 billion in share repurchases during the fourth quarter and maintains a progressive dividend framework targeting 4% annual increases. Fidelity analysts emphasize its income characteristics during periods of elevated risk premiums.

Chord Energy (CHRD)

Chord Energy maintains concentrated operations within North Dakota’s Williston Basin, targeting the prolific Middle Bakken and Three Forks shale formations. Current production averages approximately 232,737 barrels of oil equivalent daily.

Chord Energy Corporation, CHRD

The producer markets crude oil, natural gas liquids, and gas through pipeline networks and rail infrastructure, providing direct sensitivity to West Texas Intermediate price movements. Shareholder distributions totaled $1.2 billion throughout 2025, with shares trading at roughly 6x forward earnings.

Chord’s dividend yield approximates 4.9% to 5% with annual payout growth exceeding 20%. Koyfin and Simply Wall St. analysts maintain strong buy recommendations, citing exceptional cyclical leverage.

Eos Energy Enterprises (EOSE)

Eos Energy manufactures utility-scale battery storage systems domestically. Despite delivering 700% year-over-year revenue expansion and record quarterly performance, shares declined following fourth-quarter disclosures.

The manufacturer concluded 2025 with approximately 2 GWh of annualized manufacturing capacity alongside $240 million in contracted orders. Balance sheet liquidity exceeds $600 million.

Eos does not qualify as a traditional defensive holding. Instead, it represents a volatile, longer-horizon wager on accelerated energy security legislation should policymakers prioritize infrastructure resilience amid ongoing conflicts.

Defense Industry: Advanced Weapons Systems and Growing Backlogs

Lockheed Martin (LMT)

Lockheed Martin maintains its position as the globe’s largest dedicated defense manufacturer. The company recently finalized a $9.8 billion agreement delivering 1,970 Patriot PAC-3 Missile Segment Enhancement interceptors, marking the largest single contract in its Missiles and Fire Control division’s history.

Iran’s expanding ballistic missile capabilities have intensified demand for integrated air defense platforms including Patriot and THAAD systems, directly benefiting Lockheed’s order pipeline. J.P. Morgan sustains an overweight stance with price objectives spanning $200 to $500.

The equity provides approximately 1.5% dividend yield. Its $194 billion backlog encompasses F-35 lifecycle support and Patriot production now experiencing heightened demand.

Northrop Grumman (NOC)

Northrop Grumman serves as prime contractor for the B-21 Raider next-generation stealth bomber and the Sentinel ground-based strategic deterrent program. Both initiatives align with evolving Pentagon priorities as Iran-related threats intensify.

Morgan Stanley maintains an overweight rating with a $408 target, while shares recently changed hands near $347. The stock has appreciated over 33% during the trailing twelve months while distributing a 1.5% yield.

Significant contract awards anticipated throughout 2026 span B-21 production, F/A-XX development, and Golden Dome systems. Northrop has substantially outpaced S&P 500 returns over the past year.

Key Takeaways

- February 2026 saw BYD’s NEV sales plunge 41.1% compared to the previous year, representing the most severe contraction since February 2020.

- The automaker has now experienced six months in a row of declining sales figures.

- NEV manufacturing output and sales volumes both contracted approximately 38% versus February 2025.

- The passenger vehicle segment experienced the most significant impact.

- International shipments reached 100,600 NEVs, while battery manufacturing capacity maintained strength.

The Chinese electric vehicle manufacturer BYD has reported its most dramatic monthly sales contraction in six years, with February figures showing a 41.1% year-over-year decrease. This alarming trend extends the company’s sales downturn to half a year.

The magnitude of this decline hasn’t been witnessed since February 2020, during the initial economic disruption caused by the coronavirus pandemic.

According to a regulatory disclosure published over the weekend, both manufacturing and sales of new energy vehicles contracted by roughly 38% when compared to the same period in 2025.

The passenger vehicle category bore the brunt of the downturn, although BYD opted not to provide granular segment-level data in its official filing.

These disappointing results emerge despite the company’s commanding presence in the worldwide electric vehicle sector and its aggressive expansion into foreign territories.

International Sales Provide Limited Relief

In terms of overseas distribution, BYD delivered 100,600 NEVs internationally during February, a metric the manufacturer identified as a relative positive amid otherwise challenging circumstances.

Battery manufacturing operations remained resilient. BYD emphasized its installed capacity for NEV power systems and energy storage batteries as indicators of sustained operational scale, despite the contraction in vehicle unit sales.

The organization seems to be relying increasingly on its battery division and international operations to counterbalance weaker performance in its home market.

It’s important to recognize that February traditionally represents a slower sales period for China’s automotive industry, primarily due to Lunar New Year celebrations that reduce operational days and showroom activity.

While this seasonal pattern occurs annually, the magnitude of the current downturn remains striking even when factoring in these calendar-related considerations.

Financial Performance Indicators

BYD’s year-to-date stock performance reflects a modest decline of -0.42% at the time of the regulatory submission, with the company maintaining a market capitalization of HK$890 billion.

Daily trading activity averages approximately 21.5 million shares.

Technical analysis indicators currently suggest a Buy rating for the equity.

The latest analyst coverage for HK:1211 also recommends a Buy position, establishing a target price of HK$130.00.

The extended six-month pattern of declining monthly sales volumes prompts concerns regarding short-term market demand, especially within China’s domestic market where rivalry among electric vehicle manufacturers has grown increasingly fierce.

BYD’s February 2026 regulatory submission verified that aggregate NEV production and sales both decreased by approximately 38% on an annual basis, with international shipments totaling 100,600 vehicles and battery division capacity characterized as robust.

Leading bitcoin treasury company Strategy has again raised the dividend on its STRC (“Stretch”) preferred series.

Led by Executive Chairman Michael Saylor, the firm lifted the annualized payout by 25 basis points to 11.5%.

While STRC to this point has performed as hoped by the company — continuing to trade in a tight range close to $100 — Strategy’s common stock, MSTR, has floundered alongside the price of bitcoin.

MSTR closed February with its eighth consecutive monthly decline, falling 14% as bitcoin tumbled nearly 20%.

Stretch is meant for steady income

Strategy describes STRC as a short-duration, high-yield savings account. This latest dividend increase marks the seventh since STRC began trading in July 2025.

A perpetual preferred stock that pays monthly cash distributions, the STRC dividend rate is set each month to help the shares trade close to their $100 par value and to limit price volatility. STRC closed at $100 on Friday but had traded somewhat below that level during part of February’s brutal month for crypto, necessitating the payout boost.

Bitcoin held a steady line through a weekend marked by geopolitical flare-ups in the Middle East, easing some of the stress that had rippled through risk assets. The benchmark cryptocurrency kept its bearings around the mid-to-high $60,000s as traders weighed potential supply disruptions, oil price volatility, and the staying power of traditional markets. While the narrative around the Strait of Hormuz and regional tensions added a geopolitical layer to the narrative, Bitcoin and broader crypto markets avoided a sudden breakout, instead trading in a relatively tight corridor as weekend liquidity faded and futures markets prepared for the Monday open.

Key takeaways

- Bitcoin started the week near $67,000 after a volatile weekend, with traders watching how U.S. markets would react to ongoing regional tensions.

- Trading data pointed to a lingering focus on a notable CME futures gap at $65,880, a potential “fill” area that could influence short-term moves.

- Oil-price risk rose as Tehran signaled actions around the Strait of Hormuz, raising concerns about inflationary pressures and their potential impact on risk sentiment.

- Analysts offered mixed views: some described the initial response as positive, while others warned that the market could drift until macro catalysts clear, including the U.S. opening and inflation data.

- The crowd of strategists and traders continues to eye a possible relief rally if Bitcoin can reclaim momentum above critical moving-average levels and push toward the high-$70,000s range.

Tickers mentioned: $BTC

Sentiment: Neutral

Price impact: Neutral. Price action remained range-bound despite regional tensions and a looming data calendar.

Trading idea (Not Financial Advice): Hold. Monitor the Monday open and the CME gap as liquidity returns to the market.

Market context: The weekend period saw traditional markets digesting geopolitical headlines as traders awaited U.S. opening dynamics and inflation-related data. Early signs showed U.S. stock futures down roughly 0.65% as traders braced for potential volatility once liquidity returned to normal levels, underscoring a cautious risk-on environment for crypto assets as well.

Why it matters

Bitcoin’s behavior in the wake of regional turmoil underscores how the asset class often behaves as a macro sponge—quick to absorb risk-off impulses and slower to trend during periods of mixed signals. The tension around the Strait of Hormuz and the broader Middle East flare-up adds a persistent inflationary lens to the discussion. Oil markets, which frequently respond to geopolitical headlines, can—by extension—spark concerns about energy costs feeding into consumer prices. A notable moment referenced by market observers is the potential for inflation to surprise to the upside, a scenario some analysts say could lift traditional hedges or drive risk assets into a different regime.

On the technical front, traders highlighted Bitcoin’s proximity to a key moving-average level as a potential fulcrum. The 21-day simple moving average, an often-watchful gauge for short- to mid-term momentum, sat near a critical threshold that, if breached, could accelerate a relief rally. Observers like Michaël van de Poppe framed the setup in a nuanced way, noting that while the initial reaction to weekend events looked “positive,” markets needed to clear the CME gap and establish a higher low before committing to a sustained move higher. This view aligns with a broader narrative that price action over the next few sessions could depend as much on opening prints in the United States as on any headline flow from abroad.

“On the other hand, the 21-Day MA needs to break in order to have a relief rally. I think we’ll see it in March/April, question of how we’re opening the markets tomorrow and whether it finds a higher low.”

Data from TradingView tracked BTC/USD action as traders focused on the $67,000 region after the weekend’s headlines, painting a picture of a market waiting for a catalyst to push beyond a short-term ceiling. The absence of a decisive breakout did not surprise all participants, given the complexity of the macro backdrop and the potential for a “gap fill” scenario as futures markets settle into Monday’s session. A number of technicians agreed that a break above the immediate resistance zone could set the stage for a move toward the $73,000–$74,000 zone, underscoring how volatile macro drivers can unfold into a structured technical chase for price targets in the near term.

Beyond the chart, the weekend narrative included other voices pointing to why a breakout could be delayed. Some market participants argued that geopolitical risk had already been priced in to an extent, with the market absorbing headlines and awaiting a clearer signal from U.S. policy and data releases. Crypto traders—who often weigh cross-asset correlations—emphasized that the next few sessions would likely hinge on how traditional markets respond when liquidity returns and whether risk appetite recovers or remains cautious. “We will probably move sideways in the next days,” reasoned another active trader, highlighting the ongoing balance between geopolitical risk and macro resilience.

The macro overlay extended to inflation concerns. The Kobeissi Letter’s thread, drawing on JPMorgan research, suggested the possibility of a fresh inflation spike that could push the U.S. Consumer Price Index higher—potentially around 5%—a development that would feed into both equity and crypto dynamics. This thread arrived in the context of recent U.S. inflation prints that had already surprised to the upside, notably with the latest Producer Price Index data underscoring that the floor for inflation might be sticky rather than easily transitory. In parallel, market observers referenced Bitcoin’s historical dynamics—such as metrics that point to elevated longer-horizon returns in certain cycles—to anchor expectations for how BTC might respond as macro conditions evolve. A related discussion on a widely cited price metric is available in a Cointelegraph piece that linked to a longer-term pattern, illustrating how historically prolonged uptrends have unfolded in response to regime changes in inflation and liquidity.

As the weekend wound down, a chorus of voices underscored the nuances of the setup. Crypto influencers and traders reminded audiences that headlines alone rarely deliver a sustained move; instead, the probability of a meaningful rebound depends on the confluence of technical breakouts, macro data, and the opening tone of U.S. markets. The crosswinds—from geopolitical tensions to inflation risk—mean Bitcoin’s path may be less about a single trigger and more about a sequence of catalysts aligning in the weeks ahead.

What to watch next

- Monday open: observe whether U.S. equities’ early direction validates or contradicts the weekend narrative, particularly as the CME gap at 65,880 remains a potential target for a fill.

- BTC price action around 67,000: monitor if the asset can hold this level or accelerate toward the upper target near 73,000–74,000 based on momentum signals and moving-average dynamics.

- Oil and inflation linkage: track oil price movements and any fresh inflation data releases that could reframe risk sentiment and liquidity expectations.

- Futures and liquidity cycles: pay attention to how liquidity returns in the coming days and whether any new macro surprises push risk assets into a fresh regime.

- Geopolitical headlines: continue to monitor developments around the Strait of Hormuz and broader regional tensions, as these could reintroduce volatility into risk assets and affect hedges like BTC.

Sources & verification

- Trading view data showing BTC price activity around $67,000 after the latest Middle East events (TradingView).

- Discussion and charts cited by Michaël van de Poppe on X about the 21-day moving average and potential resistance turned support levels.

- Market commentary on the CME futures gap at $65,880 and its potential relevance to near-term price action.

- References to inflation risk and CPI considerations from JPMorgan-linked discussions in the Kobeissi Letter thread (KobeissiLetter).

- Cointelegraph coverage linking to inflation data and the broader macro narrative surrounding Bitcoin’s historical performance in higher-inflation regimes (Cointelegraph).

- Bitcoin historical price metric references and longer-term return discussions (Bitcoin historical price metric …).

- Direct posts from market participants on X offering perspectives on near-term price trajectories (Michaël van de Poppe, BitBull, Crypto Caesar).

Bitcoin steadies as geopolitical tensions test risk appetite

Bitcoin (CRYPTO: BTC) threshold dynamics dominated the narrative as regional headlines intersected with macro data expectations. The asset’s late-week price action found support near the $67,000 level, consistent with a broad risk-off-to-risk-on tug-of-war that markets have navigated throughout the weekend. While some participants argued that a relief rally could unfold if momentum gathers and key moving-average levels break, others emphasized the need for a clear bullish trigger—one that could come from a favorable Monday open or a cooling of inflation concerns. The combination of a cautious open from U.S. equities and a disciplined approach to risk deployment shaped the tone for the early week, with traders eyeing a potential test of the CME gap and a move toward higher targets if liquidity and sentiment cooperate.

Trading data pointed to ongoing technical work in BTC’s near-term chart. The 21-day moving average, a key reference for many short-term traders, sits at a level that many watch as a potential springboard for momentum. As one veteran analyst noted, decisive action above that threshold could catalyze a more pronounced move, while a failure to gain traction could prolong a consolidative phase. In parallel, market observers highlighted the role of the CME’s futures market in shaping intraday risk, with the gap below the current price acting as a potential magnet for price action if markets shift into risk-on mode.

The macro backdrop—particularly inflation dynamics and energy-price volatility—adds a layer of complexity to Bitcoin’s trajectory. The Strait of Hormuz could become a focal point for oil markets, and any supply concerns tend to reverberate through inflation expectations and risk sentiment. Analysts who have studied post-crisis price cycles note that inflation shocks can align with crypto cycles in nuanced ways: liquidity remains a critical piece, but the direction of flow—whether into crypto as a hedge or as an alt-risk asset—depends on how investors digest the evolving macro picture. In this context, Bitcoin’s price range-bound behavior over the weekend can be seen as a reflection of a market seeking a credible catalyst rather than chasing headlines.

As market participants refine their models for the week ahead, the broader takeaway is that Bitcoin’s near-term path will hinge on a confluence of factors: a measured Monday opening, the pace at which the CME gap closes, and any renewed guidance from inflation and energy data. The dynamics suggest a market that might remain cautious until a clearer signal coalesces, even as some voices project a path toward the $73,000–$74,000 zone should momentum swing in BTC’s favor. The coming days will reveal whether the technical setup can convert into a sustained trend or whether traders revert to a wait-and-see posture in response to macro uncertainty.

A closer look at Honor’s Robot Phone

Emergency services called to crash on B1222 in Stillingfleet

US is sinking Iran’s Navy, Trump says

-

Sports6 days ago

Sports6 days agoWomen’s college basketball rankings: Iowa reenters top 10, Auriemma makes history

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Iris Top

-

Politics6 days ago

Politics6 days agoNick Reiner Enters Plea In Deaths Of Parents Rob And Michele

-

Business5 days ago

Business5 days agoTrue Citrus debuts functional drink mix collection

-

Politics3 days ago

Politics3 days agoITV enters Gaza with IDF amid ongoing genocide

-

Sports2 days ago

The Vikings Need a Duck

-

Tech14 hours ago

Tech14 hours agoUnihertz’s Titan 2 Elite Arrives Just as Physical Keyboards Refuse to Fade Away

-

Crypto World5 days ago

Crypto World5 days agoXRP price enters “dead zone” as Binance leverage hits lows

-

Tech5 days ago

Tech5 days agoUnsurprisingly, Apple's board gets what it wants in 2026 shareholder meeting

-

NewsBeat1 day ago

NewsBeat1 day agoDubai flights cancelled as Brit told airspace closed ’10 minutes after boarding’

-

NewsBeat4 days ago

NewsBeat4 days agoCuba says its forces have killed four on US-registered speedboat | World News

-

NewsBeat1 day ago

NewsBeat1 day agoThe empty pub on busy Cambridge road that has been boarded up for years

-

NewsBeat4 days ago

NewsBeat4 days agoManchester Central Mosque issues statement as it imposes new measures ‘with immediate effect’ after armed men enter

-

NewsBeat4 hours ago

NewsBeat4 hours ago‘Significant’ damage to boarded-up Horden house after fire

-

NewsBeat6 days ago

NewsBeat6 days ago‘Hourly’ method from gastroenterologist ‘helps reduce air travel bloating’

-

NewsBeat21 hours ago

NewsBeat21 hours agoAbusive parents will now be treated like sex offenders and placed on a ‘child cruelty register’ | News UK

-

NewsBeat7 days ago

NewsBeat7 days agoArmed man killed after entering secure perimeter of Mar-a-Lago, Secret Service says

-

NewsBeat5 days ago

NewsBeat5 days agoPolice latest as search for missing woman enters day nine

-

Business4 days ago

Business4 days agoDiscord Pushes Implementation of Global Age Checks to Second Half of 2026

-

Business3 days ago

Business3 days agoOnly 4% of women globally reside in countries that offer almost complete legal equality