Crypto World

Why Now Is a Better Time to Buy BTC Than in 2017

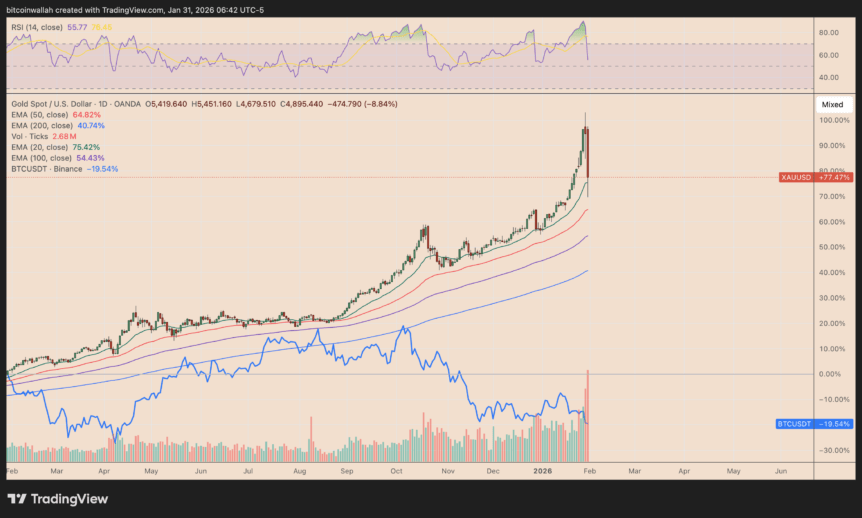

Bitcoin (BTC) traded lower against gold in January, sparking renewed debate about whether current prices offer an appealing entry point ahead of a potential shift in crypto market dynamics. Historical parallels are frequently cited: during the 2015–2017 cycle, BTC climbed from roughly $165 to $20,000 in around two years, a gain of about 11,800%. The latest data suggest BTC may be testing a similar setup—at a time when macro conditions and sentiment toward risk assets remain in flux. Bitwise Europe’s data on the BTC/XAU ratio highlighted a rare moment when the digital asset’s value, after adjusting for global liquidity, approached levels associated with major bottoms in prior cycles.

The ratio’s trajectory has drawn attention from technicians and strategic investors alike. A decline toward the -2 z-score zone on Bitwise Europe’s chart has historically marked periods of extreme undervaluation, coinciding with capitulation or significant turning points. That framing underpins the argument that Bitcoin could be poised for a substantial reevaluation, particularly if fresh capital begins to move away from traditional hedges like gold and into risk-on assets again. The prevailing line of thought is that BTC’s repricing would reflect a broader rotation rather than a one-off spike—an idea that has gained traction among several market observers.

“Today represents a better opportunity to be buying Bitcoin than 2017.”

The front line of debate, however, remains the pace and certainty of any rotation. Some analysts say capital may trickle from gold into Bitcoin over the course of February or March, driven by a confluence of factors including BTC’s relative value and selective appetite for risk assets. Notably, Bitwise European researchers and others have argued that such a rotation could begin even as gold continues its own strength in a broader macro backdrop. Among the voices in this discourse are André Dragosch and Pav Hundal, who have suggested that discounted BTC setups could reemerge as buyers re-enter the market. The sentiment is cautious—rotation is not guaranteed, and timing remains uncertain as traditional markets wrestle with macro signals and liquidity conditions.

The broader backdrop includes a divergence in performance between the yellow metal and BTC. Gold has been buoyant, with some forecasters predicting further strength in the coming months, while Bitcoin has struggled with a January pullback. Citi has projected a potential rise in silver, supported by demand dynamics in China and a softer U.S. dollar, while RBC Capital Markets has offered a more optimistic long-range forecast for gold, suggesting a potential rise to around $7,000 per ounce by the end of 2026. Against that setting, the case for a Bitcoin rotation into discounted levels grows more nuanced, hinging on how investors interpret inflation dynamics, liquidity, and the evolving narrative around digital assets as a strategic hedge or a risk asset.

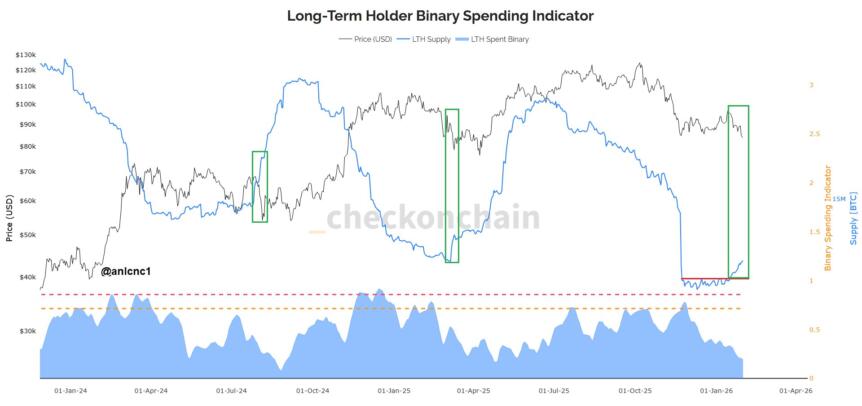

Analysts also note that the January sell-off did not uniformly wipe out confidence in Bitcoin’s longer-term thesis. Indeed, long-term holders have started to rebuild positions even as the price retreated. The LTH (Long-Term Holders) supply—capturing addresses that have held BTC for more than 155 days—began to recover during the downturn, signaling that patient investors remained willing to accumulate. A companion indicator, the LTH Spent Binary, which tracks whether long-term holders are cashing out or continuing to hold, continued its downward sweep, hinting that selling pressure among this cohort was waning. The historical pattern suggests that replenishing LTH supply and a falling Spent Binary often precede durable price basements and subsequent recoveries, a narrative supported by prior cycles where calmer distributions preceded sharp rebounds.

On-chain data, therefore, paints a more nuanced picture: even as the price moved lower, long-term holders absorbed the January sell-off, and the market watcher community looks for a foundation that could support a recovery. Anil, a market analyst who has tracked these patterns across multiple cycles, noted that in past periods of similar LTH behavior, BTC often found a resilient floor and then advanced once holders regained confidence. The April 2025 lows, for instance, provided a case study where LTH supply rebounded ahead of a roughly 60% rally in the following weeks, underscoring the potential power of patient accumulation to reshape the trend after a reset.

Why it matters

What makes this rotation debate important is its potential impact on how capital allocates across the crypto ecosystem and traditional assets. If a meaningful portion of capital begins to move from gold into BTC, it could reframe Bitcoin’s narrative from a speculative risk-on asset to a more balanced hedge or store-of-value instrument, depending on the macro regime. The on-chain signals—LTH accumulation and a shrinking LTH Spent Binary—offer a structural read that longer-term holders are building a base, even as spot prices retreat. For traders, this combination of macro cues and on-chain behavior could translate into a selective dip-buying opportunity rather than a wholesale entry point, particularly if February and March bring supportive liquidity and clearer catalysts.

From a market context perspective, the rotation thesis sits within a broader environment characterized by a crosscurrents of risk appetite, liquidity cycles, and evolving macro expectations. The gold rally has been a persistent feature of recent years, signifying its ongoing status as a hedge instrument for many investors. At the same time, the crypto market continues to attract capital through selections such as BTC’s supply dynamics and changes in investor sentiment toward risk assets. The tension between gold’s relative strength and BTC’s price action helps explain why many analysts describe the January pullback not as a definitive end to the bull case but as a potential recalibration that could set the stage for durable upside if holders’ confidence persists and the rotation unfolds in a measured way.

What to watch next

- February–March catalysts for a BTC-to-gold rotation and any shifts in liquidity conditions that could support a sustained reallocation.

- Changes in LTH supply and the LTH Spent Binary metric, which historically signaled the formation of robust BTC bottoms in prior cycles.

- Updates to Bitwise Europe’s BTC/XAU ratio data and any new confirmations of a bottoming pattern from on-chain analytics firms.

- Macro developments affecting gold and fiat liquidity, including policy signals and inflation expectations, that could influence hedging behavior.

Sources & verification

- Bitwise Europe BTC/XAU ratio data and the associated z-score context cited in market commentary.

- Public posts and market interpretations by Michaël van de Poppe on social media regarding buying opportunities in BTC.

- On-chain analysis and commentary from CheckOnChain.COM regarding Long-Term Holders and the LTH Spent Binary indicator.

- Cited market commentary on gold and silver price trajectories from Citi and RBC Capital Markets, as referenced in the analysis.

- Historical references to BTC performance during earlier cycles and the April 2025 lows as a precedent for LTH-driven rebounds.

Bitcoin vs. gold: rotation signals and implications

Bitcoin (CRYPTO: BTC) is entering a period where the relative value against gold (XAU) is scrutinized for clues about the market’s next major move. The currency’s price action in January, when BTC slipped further against gold after adjusting for liquidity, has become a focal point for traders seeking an inflection signal. Data from Bitwise Europe showed the BTC/XAU ratio approaching a historically meaningful extreme, a configuration that has historically preceded substantial BTC recoveries when market psychology shifts and risk appetite stabilizes. The charting narrative centers on a Z-score that has briefly slid into territory associated with major market bottoms, suggesting to some that BTC may be consolidating its position before a broader breakout.

Historical memory plays a role in how these conditions are interpreted. The most cited comparison looks back to the 2015–2017 bear-to-bull transition, during which BTC moved from roughly $165 to $20,000 within two years after a period of deep undervaluation relative to gold and other assets. The implication is not a guaranteed immediate upside, but rather a setup in which patient holders and disciplined buyers can position themselves ahead of a potential repricing. A popular tweet from a market commentator captured the mood: the current moment, according to the analyst, represents a better buying opportunity than in 2017 when the cycle began gaining momentum. While not a forecast, the sentiment underscores a belief that BTC could realize a more pronounced recovery if rotation from gold begins to take hold in the coming weeks.

On-chain observers emphasize that the January drawdown did not erase long-term conviction. The ongoing rebound in Long-Term Holders’ supply—addresses that have kept BTC for more than 155 days—paired with a continued decline in the LTH Spent Binary, points to a patient cohort that may be prepared to support a multi-month basing process. These structural dynamics matter because they can underpin a more durable ascent once price action aligns with macro and liquidity trends. Past cycles have shown that a base built by patient holders often precedes sizable upside, even when sentiment remains cautious in the near term. The narrative remains contingent on broader market conditions, yet the on-chain signals provide a level of confidence for those who view BTC as a longer-term play rather than a short-term speculator’s bet.

The rotation thesis is reinforced by a balancing of expectations around gold’s performance. While gold has appreciated over the past year, the pace and persistence of that strength are debated, with some analysts predicting continued gains driven by demand dynamics and currency weakness, and others warning that gold’s upside could be tempered by shifting macro factors. The reality is that the path from rotation signal to actual capital flow is rarely linear; it often requires a confluence of favorable liquidity, a stabilizing macro backdrop, and a narrative that convinces investors to shift weight from one hedge to another. In such an environment, Bitcoin’s fundamentals—particularly the resilience of on-chain holders and the evolution of market sentiment—could tip the balance toward a more sustained recovery if February and March reveal concrete catalysts and improved market conditions.

Overall, the January weakness has introduced a potential reset that could set the stage for a broader recalibration of BTC’s role in portfolios. It is a reminder that the crypto market remains sensitive to macro shifts, and that rotations—whether into BTC from gold or into other risk-on assets—depend on a complex mix of liquidity, investor psychology, and the evolution of on-chain signals. The coming weeks will be telling as market participants weigh these diverse factors and decide whether the current configuration marks the beginning of a durable baseline or a stepping stone to another leg down before the next leg up.

Crypto World

Stocks start catching up with bitcoin’s earlier meltdown to $60,000 as bond yields rise

Bitcoin began the year on a painful note, even as equity markets remained buoyant. But stock traders’ luck is now running out, as rising bond yields pressure valuations.

Prices for bitcoin plunged to nearly $60,000 from around $90,000 in the first five weeks of the year, according to CoinDesk data. The decline marked a sharp decoupling from the S&P 500 and Nasdaq, which were trading at or near record highs at the time.

Analysts wondered how long the divergence would last — whether bitcoin would quickly bounce back or stocks would eventually catch up with the weakness in bitcoin.

The latter appears to be happening. Since the Iran war began on Feb. 28, fears over inflation and fading Fed rate-cut expectations have pushed U.S. Treasury yields sharply higher, putting pressure on equities.

The stock market’s weakness, appearing weeks after BTC’s decline, underscores the cryptocurrency’s role as a leading indicator for traditional risk assets. Traders in conventional markets often watch BTC to gauge overall risk sentiment, particularly on weekends or during days when traditional exchanges are closed.

Yields rise, stocks drop

The yield on the 10-year U.S. Treasury note rose to 4.41% soon before press time, the highest since Aug. 1. The benchmark borrowing cost has risen by 48 basis points since the onset of the Iran war. The U.S. two-year yield has jumped 57 basis points to 3.94%.

Treasury yields are considered the benchmark for risk-free interest rates and borrowing costs in the economy, such as corporate bonds, mortgages, student loans, etc., are priced relative to Treasuries. So, when yields rise, lenders typically increase rates on loans to maintain their spreads, which pushes borrowing costs higher for businesses and consumers. This leads to risk aversion in equities, which we are beginning to see now.

Futures tied to Wall Street’s tech heavy index Nasdaq fell to 23,890 points early Monday, the lowest since Sept. 11. The S&P 500 e-mini futures fell to 6,505 points, also the lowest since September.

CoinDesk recently highlighted that the price patterns of major stock indices bear a striking resemblance to bitcoin’s price action leading up to its crash. This similarity has raised concerns among analysts, suggesting that stocks could be at risk of further declines if the pattern continues to play out.

“Bitcoin has been at the top of the risk-assets iceberg, and its collapsing price could be early days of a broader drawdown — particularly if surging commodity volatility trickles up to stocks,” Bloomberg’s Senior Commodity Strategist Mike McGlone said in a recent report.

Bitcoin steady

Having crashed early this year, BTC has held largely steady between $65,000 and $75,000 in recent weeks. As of writing, the cryptocurrency changed hands at $68,790.

Yet, pricing in options market shows peak fear, resulting in a record bias for put options, or derivative contracts offering protection from price slides in BTC.

Meta CEO and co-founder Mark Zuckerberg is reportedly building an AI agent to help handle his work in managing the company amid a company-wide push for employees to adopt agentic tech.

According to a report from The Wall Street Journal on Sunday, citing sources close to the matter, Zuckerberg’s AI agent is still in development but already being used to help the CEO speed up information retrieval.

Instead of going through multiple layers of people or teams to get the required information, the agent has been retrieving the information directly.

The move is part of a broader goal within the company to accelerate employee productivity and reduce layers of friction within its 78,000-strong employee base. The report adds that Meta is pushing to compete with AI-native startups that have much smaller teams.

Zuckerberg has previously alluded to this push, noting in an earnings call in late January that 2026 is going to be the year that “AI starts to dramatically change the way” Meta works, while also indicating there may be changes to the firm’s organizational structure moving forward.

“As we navigate this, our north star is building the best place for individuals to make a massive impact. So to do this, we’re investing in AI-native tooling so individuals at Meta can get more done, we’re elevating individual contributors, and flattening teams.”

The WSJ report highlights that Meta employees have been utilizing agentic tools such as MyClaw, which has been giving them access to work files and chat logs, while also enabling them to talk with colleagues or their AI agent counterparts.

Meta employees have also been said to be using Second Brain, another AI tool built on top of Anthropic’s Claude infrastructure to help speed up work on projects, which has been described internally as something akin to an “AI chief of staff,” according to the sources.

Meta could be eyeing mass layoffs

A recent report from Reuters claimed that the firm may be finalizing plans for another wave of layoffs to offset its expenditures and capitalize on AI efficiency gains.

In an article on March 14, Reuters cited three sources familiar with the matter who claimed that Meta could be planning layoffs that may impact up to 20% of the company.

The sources claimed that no date has been set yet and that the scale of the layoffs hasn’t been finalized.

Related: Meta to shutter Horizon Worlds metaverse on VR in favor of mobile

In a statement to Cointelegraph, Meta declined to comment on the WSJ article; however, a spokesperson responded to the Reuters reporting by saying that it was a “speculative report about theoretical approaches.”

The crypto sector has been hit by a wave of layoffs in 2026, with several firms outlining a renewed focus on AI.

Last week, blockchain data provider Messari announced a shuffling of executives and employee layoffs to make way for the company’s “next phase” of becoming an AI-first company.

Meanwhile, exchange Crypto.com also announced a 12% reduction in its workforce amid its own AI push.

Magazine: Google flags crypto malware, retiree loses $840K in ‘expert’ scam: Hodler’s Digest, Mar. 15 – 21

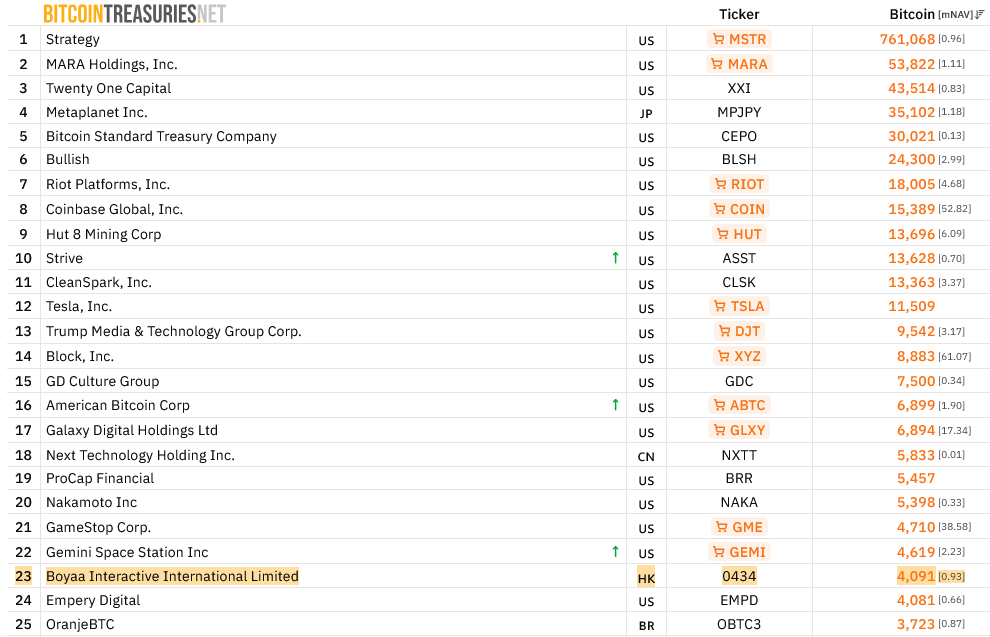

Boyaa Interactive International is the 23rd-largest Bitcoin treasury and the third-largest in Asia, behind Japan’s Metaplanet and China’s Next Technology Holding.

Hong Kong-based Web3 gaming firm Boyaa Interactive International said it is seeking shareholder approval to expand its crypto treasury, planning up to $70 million in purchases over the next year.

In a statement on Sunday, the Hong Kong-listed company said it is looking to use its “idle cash reserves during periods of weakness in the cryptocurrency market” to increase its existing positions and to support the research and development of Boyaa’s Web3 gaming business.

If approved by shareholders, Boyaa said it would invest in crypto tokens with “good market liquidity, large market value, wide recognition on the market and relatively long-term holding value.”

The $70 million would add to Boyaa’s nearly $3 billion treasury, which includes 4,091 Bitcoin (BTC) worth $2.8 billion and 302 Ether (ETH) worth $621,200.

Boyaa’s crypto treasury expansion plan comes as the crypto industry continues to grapple with a 45% market drawdown since October and growing doubt over the sustainability of crypto treasury strategies.

Few crypto treasury companies outside of Strategy and Bitmine Immersion Technologies have been buying crypto on a weekly basis over the last few months, while multiple Bitcoin miners have offloaded portions of their holdings.

Boyaa is a top-25 corporate Bitcoin treasury

Boyaa, which made $80.5 million worth of Bitcoin purchases between August and November, is currently the 23rd-largest corporate Bitcoin treasury and the third-largest in the Asia-Pacific region, trailing only Japan’s Metaplanet and China’s Next Technology Holding.

Related: Metaplanet forms new venture firm as it expands Bitcoin playbook

Boyaa expanded from online card and board games to Web3 gaming in late 2023, developing blockchain-based games and infrastructure, while making its first Bitcoin purchase in January 2024 to support that transition.

One of its offerings includes a Web3 version of a Texas Hold’em online poker platform it created in the early 2000s, offering Bitcoin rewards and crypto prizes.

Magazine: Bitcoin’s ‘narrative vacuum,’ Ethereum now inevitable: Trade Secrets

XRP dropped below the $1.40 level after a sharp wave of selling and is still struggling to recover, with buyers unable to push prices meaningfully higher. The weak bounce suggests selling pressure remains stronger than demand, keeping the token under pressure as traders look for signs of stabilization near current levels.

News Background

- XRP moved lower alongside broader crypto weakness, but the key driver was technical, with price losing the $1.40 level that had acted as near-term support.

- The token has struggled to sustain recovery attempts since mid-March, with rallies consistently fading below the $1.55–$1.60 area.

- Spot ETF flows showed limited improvement, with a modest $636K in weekly inflows — far below earlier demand, pointing to subdued institutional participation.

Price Action Summary

- XRP fell from $1.4404 to $1.3872, down roughly 3.7% over 24 hours.

- A high-volume move near 23:00 pushed price to $1.4018 before support gave way.

- Price then consolidated between $1.38 and $1.42, forming a descending intraday structure.

- A late bounce attempt toward $1.386 failed to hold, reinforcing near-term weakness.

Technical Analysis

- The break below $1.40 is the key development, confirming a loss of short-term structure and shifting momentum back toward sellers.

- Price is now trading in a descending channel between roughly $1.38 and $1.42, with lower highs forming on declining volume — a typical distribution pattern.

- Attempts to reclaim $1.40–$1.41 have been rejected, turning the level into immediate resistance.

- The broader trend remains bearish, with XRP still trading within a multi-month downtrend defined by lower highs since mid-2025.

What traders say is next?

- Traders are focused on whether the $1.38–$1.40 zone can hold as support.

- If this range stabilizes, XRP may consolidate before another attempt toward $1.41–$1.44, with a broader test near $1.55 needed to shift structure.

- A clean break below $1.38 would expose the $1.30–$1.32 zone, where support is thinner and downside could accelerate.

- For now, momentum favors sellers, with any bounce viewed as corrective until resistance levels are reclaimed.

Autonomous AI agent commerce could mean the end of online advertising as it is currently known today and shift the internet’s economic model, according to a16z Crypto.

Since the dawn of the internet, buying goods or services typically involves navigating to online stores (some through online advertisements). However, Merit Systems co-founder Sam Ragsdale argues this could change if AI agents do the shopping in the future.

From 1997 to 2024, the business model for the internet was “distraction,” said Ragsdale in an a16z blog post on Sunday.

“Humans reading a webpage can be distracted by an advert, monetizing their partial attention,” but LLMs and agents “do not get distracted,” he said.

The online advertising market size, which is dominated by search giant Google, was an estimated $291 billion in 2025, according to Mordor Intelligence.

“There is some beautiful irony in ads creating the free and open internet, which became the 10-trillion-token dataset that created LLMs, leading to the downfall of ads.”

Open protocols are the way forward

Ragsdale said the first step is already being seen, with AI platforms like ChatGPT and Gemini adding products like “Instant Checkout” for US users last year, allowing them to buy products directly within a conversation without needing to head to an external website.

Soon, hundreds of millions of consumers around the globe will “find better products, merchants will have improved conversion rates, and platforms will be able to take 5% to 10%,” he said.

However, these “checkout” services are just new “walled gardens,” Ragsdale explained, as merchants have to go through stringent approval processes to be included.

Related: AI agent payment volumes lower than reported, but adoption is growing: a16z

Instead, Ragsdale argued that the way forward will be AI agents with open protocols that allow them to discover products on their own.

“An agent that can only buy from pre-approved merchants is an employee with a corporate card restricted to three vendors. An agent with open protocols is an entrepreneur with a bank account,” he said.

Ragsdale concluded that a “clever hack” called advertising changed the internet forever, but in 2026, “that hack is dying,” arguing that open agentic commerce, powered by the x402 protocol developed by Coinbase or the Machine Payments Protocol (MPP) from Tempo and Stripe, is the future.

Magazine: Google flags crypto malware, retiree loses $840K in ‘expert’ scam: Hodler’s Digest

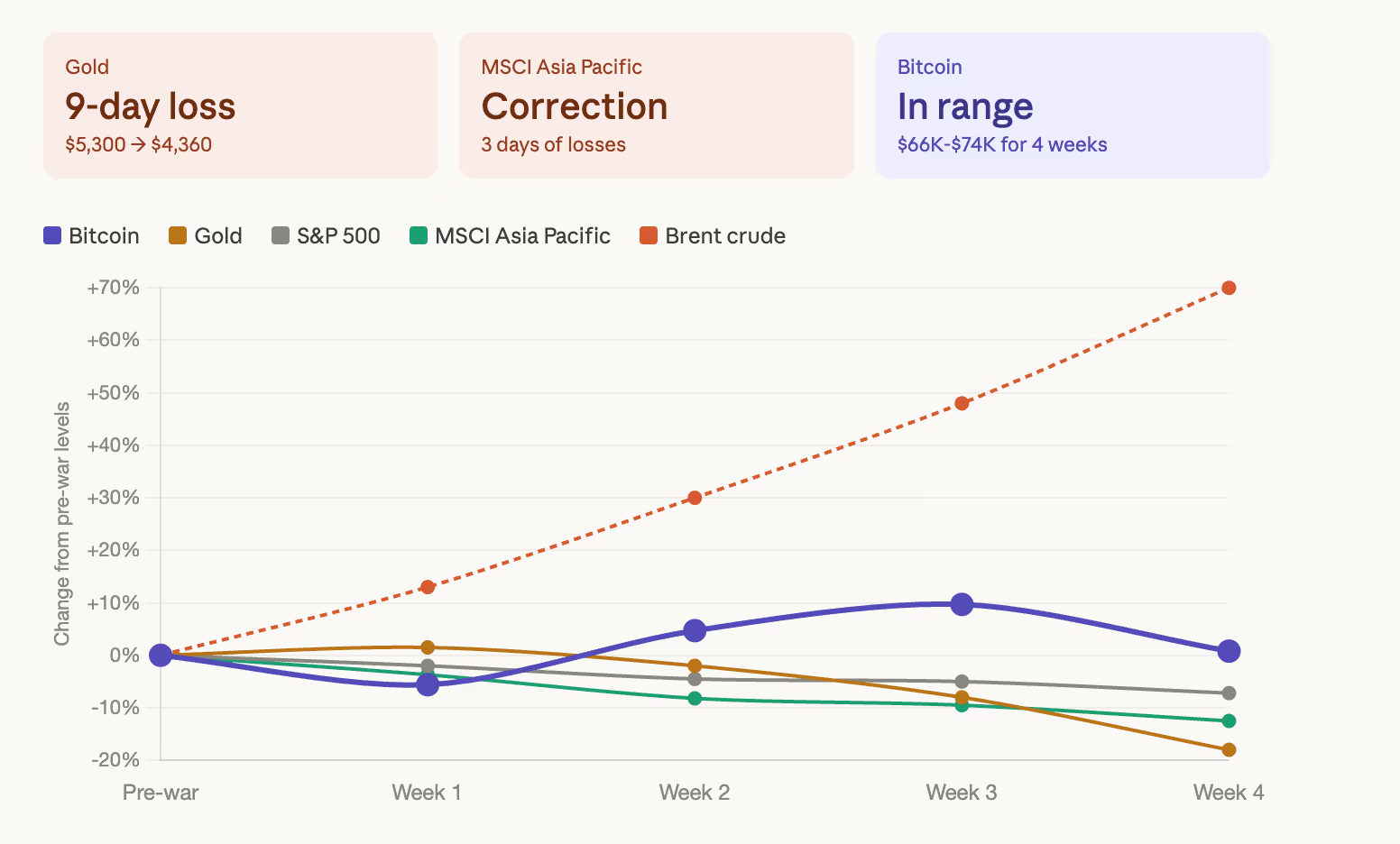

Everything is selling. Bitcoin is selling the least.

Gold dropped for a ninth straight day on Monday to around $4,360, its longest losing streak in years. Asian stocks fell for a third session and are set to enter correction territory.

Bond yields climbed as the prolonged war threatened to stoke inflation and push central banks toward rate hikes rather than cuts. S&P and European futures pointed to further losses. Brent crude edged up to $113 a barrel, now up more than 70% year-to-date.

Bitcoin was trading at $68,316 on Monday morning, up 1.5% over the past 24 hours and down 6% on the week. Ether rose 2.7% to $2,059. XRP gained 2% to $1.38. Tron climbed 0.3% to $0.309, the only major green on a weekly basis at 3.8%. BNB fell 1.2% to $627. Solana dropped 2.5% to $86.54. Dogecoin lost 1.7% to $0.09, down 7.4% on the week and the worst-performing major.

The weekly numbers are ugly across the board. Gold, the asset that’s supposed to outperform in geopolitical chaos, has lost roughly 18% from its recent highs. Asian equities are entering a correction. Bitcoin is down 6% on the week but still trading above the $66,000 floor that held through every war-driven sell-off since Feb. 28.

“The gold rally and the BTC collapse are more structural than market-based,” said Alexander Blume, CEO of Two Prime, an SEC-registered investment advisor. “China and others have been systematically buying gold as part of a broader effort to decouple from Western markets and the US dollar.” That buying has reversed as the conflict intensified and liquidity became the priority over safety.

Blume noted that both bitcoin’s price and derivatives markets “have held up decently well” given the macro backdrop, and said Two Prime is positioned for “an increase in funding and futures rates in the weeks and months to come,” effectively betting the contrarian view that an upside surprise is more likely than the market expects.

Trump’s 48-hour ultimatum on Saturday to “hit and obliterate” Iran’s power plants if the Strait of Hormuz isn’t reopened expires Monday evening. Iran responded that any such attack would trigger an indefinite closure of the waterway and retaliatory strikes on U.S. and Israeli energy infrastructure across the region.

Meanwhile, Goldman Sachs raised its full-year Brent forecast to $85 from $77 and WTI to $79 from $72, describing the Hormuz disruption as the “largest-ever supply shock for global crude markets.”

Crypto and the wider markets tumbled on Monday as the US and Iran escalated threats toward one another for the fourth week, sending oil prices seesawing.

US President Donald Trump posted to Truth Social on Sunday that the US would “hit and obliterate” Iranian power plants, “starting with the biggest one first,” if the country didn’t open the Strait within 48 hours.

Iran responded by saying it will answer any US strikes on its power or water infrastructure with attacks on US and Israeli assets in the Gulf and threatened to completely close the Strait of Hormuz, one of the world’s vital oil shipping lanes.

Bitcoin (BTC), long seen by its backers as a so-called “safe-haven” asset like gold, dropped 1.8% in the last 24 hours to $68,160, recovering from a low of below $67,600 in late trading on Sunday.

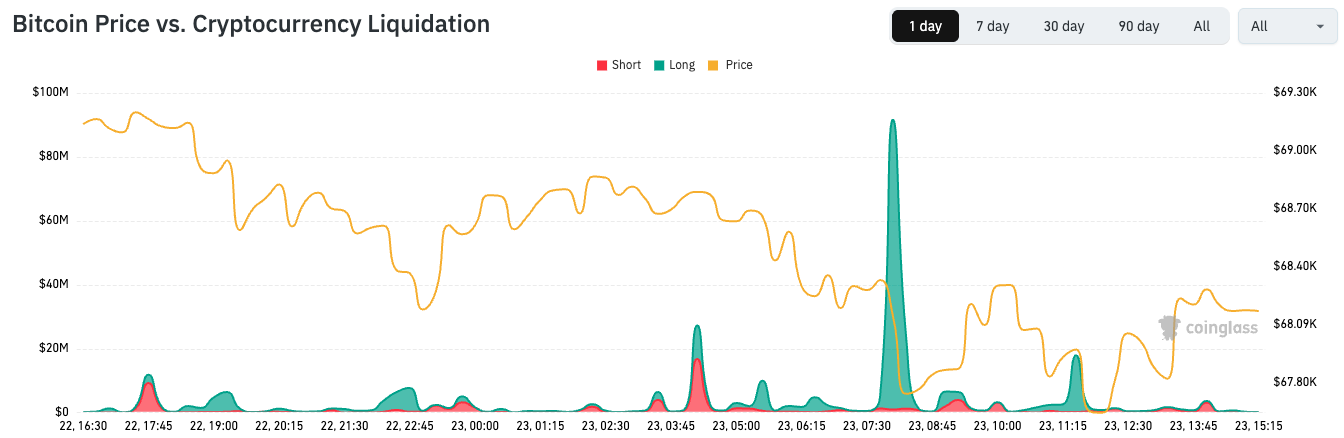

Bitcoin’s price drop caused a surge in liquidations across crypto, with $336.3 million wiped from the market in the last day, with nearly a third of the volume, or $100 million, caused by failed Bitcoin long bets, according to CoinGlass.

Rachael Lucas, an analyst at the crypto exchange BTC Markets, told Cointelegraph that crypto “is trading in lockstep with equities right now, not as a haven, and sentiment is sitting at historic lows, with the Fear and Greed Index deep in ‘extreme fear’ territory at 8.”

Oil chops, Asia markets fall

Stock markets around Asia also reacted to the tit-for-tat threats, with Australian and New Zealand markets both down 0.8%, while Japan had fallen over 4%.

The price of crude oil briefly spiked to a high of just over $100 a barrel in early trading on Monday before quickly dropping to $97.20. It has since steadily climbed to $99.30 at the time of writing.

Meanwhile, Brent crude oil, considered a benchmark for purchasing oil worldwide, jumped to over $114 per barrel but settled below $113.

Lucas said that the future of crypto markets hinges on the de-escalation of the Iran war and the decisions of the US Federal Reserve.

She added that Brent’s price jump “is feeding inflation expectations, and the probability of a Fed rate hike has jumped from zero to 12.4% in a single week.”

“That is a significant macro repricing that crypto will continue to reflect until there is clarity on both fronts,” she added.

Related: Bitcoin risks 50% drop as BTC’s positive correlation with US stocks grows

Lucas said if the Iran war de-escalates, “crypto would be among the fastest risk assets to recover. However, this conflict has no clear negotiating counterpart and no defined exit timeline, which makes that outcome difficult to call in the near term.”

She added that $68,000 is the “immediate level” to watch for if Bitcoin has support, with $65,800 being “the next meaningful support if that gives way.”

“To the upside, Bitcoin needs to reclaim $71,500 before any recovery narrative gains credibility,” Lucas said.

She added that Bitcoin still had strong institutional support, with $1.43 billion in net inflows to Bitcoin exchange-traded funds so far this month.

“When sentiment is this low and institutional infrastructure is this strong, history suggests the setup for recovery is building, even if the timing remains uncertain,” Lucas said.

Big Questions: Is China hoarding gold so yuan becomes global reserve instead of USD?

Barbara Fried and Joseph Bankman, the parents of FTX founder Sam Bankman-Fried, who was convicted after the exchange’s collapse, used their first televised interview to challenge the core premise of his conviction, arguing that no customer money was ultimately lost.

“The money was always there,” Bankman said during a weekend interview with CNN’s Michael Smerconish. “These were very profitable companies with billions of extra assets.”

The timing is not incidental. At the end of March, the FTX Recovery Trust is set to distribute about $2.2 billion in its fourth payout, bringing total recoveries to roughly $10 billion. Several U.S. customer classes will reach 100% recovery, with one class at 120%. For Bankman-Fried’s parents, those figures should mean SBF’s exoneration.

“Everybody has been made whole with 18 to 43 percent interest,” Fried said.

All distributions are denominated in U.S. dollars and are fixed to asset prices as of the November 2022 bankruptcy filing, when bitcoin traded near $16,800. FTX collapsed in late 2022, upending investor confidence and sparking a wave of regulatory scrutiny across the industry.

Bitcoin has been on a rollercoaster since then, shooting up to over $126,000 during the fall of 2025, and now trading around $69,000, way above the price in late 2022.

However, an FTX customer who held one bitcoin receives the dollar value of that 2022 claim, plus interest, not the asset or its current price. The estate is returning roughly 119% of a claim frozen at a fraction of today’s market value.

FTX creditor representative Sunil Kavuri has publicly rejected the framing, writing that “FTX creditors are not whole.”

FTX Bankruptcy recovery rates in real crypto terms

FTX creditors are not whole

9% to 46%: Real crypto terms recovery but probably in reality lower as crypto prices higher when 143% paid

Also seen on CT some:

1) Protect known scammers/liars/fraudsters

2) Attack those helping… pic.twitter.com/pUcjIPFsnv— Sunil (FTX Creditor Champion) (@sunil_trades) November 2, 2025

The parents’ defense also runs counter to the regulatory framework established in response to the collapse. Bankman described the transfer of customer funds to sister company Alameda Research as routine.

“They were borrowed by Alameda from FTX,” he said. “Alameda acted like everybody else, putting in money and borrowing money.”

If accepted, that argument would normalize the commingling of customer assets with a proprietary trading firm, the exact practice new rules in Hong Kong, the E.U., and proposed U.S. legislation now prohibit. The logic that exonerates Bankman-Fried is the same logic regulators moved to eliminate.

Fried went further, calling the prosecution “essentially political” and arguing the Biden administration “had decided to destroy crypto.”

The political framing reflects a broader clemency push toward President Donald Trump, as Bankman-Fried continues to support White House policy from prison via posts on X.

Smerconish noted that Judge Lewis Kaplan, who presided over SBF’s criminal trial and sentenced him to 25 years, is the same federal judge who oversaw E. Jean Carroll’s civil case against Trump, a point he said was “not lost on” the family.

Asked what she would say to Trump, Fried called her son “one of the most brilliant, talented young men of his generation” and said he would be “an enormous benefit to the economy” if freed.

But that door appears closed, at least for now.

Trump said in a January interview with the New York Times that he would not consider a pardon for Bankman-Fried even as Trump has granted clemency to other crypto figures, including Silk Road founder Ross Ulbricht and former Binance CEO Changpeng Zhao.

Polymarket bettors give it a 12% chance of happening.

Bankman-Fried’s appeal remains pending, and his motion for a new trial faces opposition from prosecutors who have dismissed his claims of political bias.

Crypto World

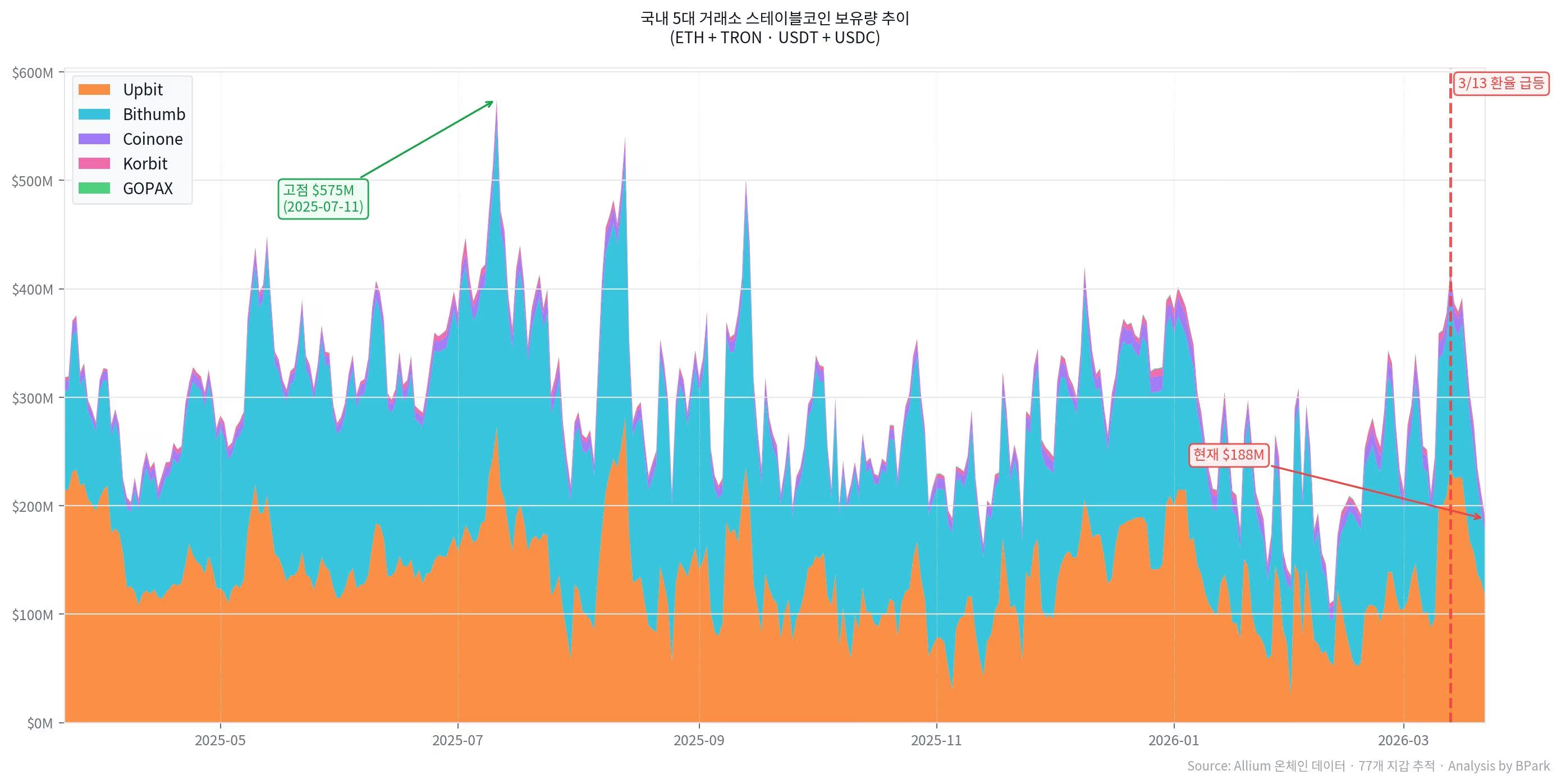

South Korea crypto liquidity tumbles as stablecoin balances plunge 55% and stock heat up

Stablecoin balances in South Korea have fallen sharply since July even as stock inflows rise, underscoring a shift in where money is flowing.

The total amount of these so-called tokenized versions of fiat currencies held in wallets tied to South Korea’s five largest crypto exchanges have plunged 55%, with on-chain data pointing to a sharp wave of outflows triggered by the won’s break past 1,500 per dollar in mid-March.

Data from Allium Labs, tracking Ethereum and Tron wallets across Upbit, Bithumb, Coinone, Korbit, and GOPAX, shows that combined stablecoin holdings dropped from $575 million in July 2025 to roughly $188 million as of mid-March, with the decline accelerating as the won slid to 16-year lows against the dollar.

The timing suggests traders sold tether at elevated USD/KRW levels after the won weakened past 1,500 per dollar in mid-March, a threshold not seen since the 2008 financial crisis.

The weaker currency amplified the incentive to exit dollar-denominated holdings, with traders converting into won and redeploying into domestic assets, according to DNTV Research founder Bradley Park.

The outflows mark the latest phase of a broader migration of Korean retail capital from crypto into equities, a shift CoinDesk first documented in November. But where that earlier rotation was driven largely by narrative, with traders chasing AI-linked chipmakers as altcoin momentum faded, the latest drawdown appears tied to a specific FX trigger rather than a change in risk appetite.

South Korea’s government has since intensified efforts to attract capital into domestic markets through new policies such as “repatriation” accounts that offer up to 100% capital gains tax exemptions for investors who sell overseas assets and reinvest locally.

That shift is visible in brokerage data. Investor deposits, a proxy for cash available to buy stocks, fell from roughly ₩131 trillion ($86 billion) in early March to around ₩112 trillion ($74 billion) following the mid-month currency move, indicating that capital was being actively deployed into equities as stablecoin balances declined. Deposits have since begun to stabilize, suggesting fresh inflows are replenishing the pool of buying power.

The KOSPI, already up 75% in 2025, has gained another 37% this year, making it the world’s best-performing major index. The rally is highly concentrated, with Samsung Electronics and SK Hynix accounting for roughly half of market capitalization and more than 50% of projected profits, positioning them as the primary destination for both retail and institutional flows.

Broader stablecoin transaction volumes across Asia have ticked up over the last year, according to data from Artemis, suggesting the drawdown on Korean exchanges reflects domestic capital rotation rather than a region-wide pullback.

For crypto markets, the shift underscores the loss of one of their most important retail liquidity pools.

Korean participation has historically amplified market cycles, and the data now shows capital is not sitting idle but being actively redeployed. Whether those flows return may depend less on crypto narratives than on the sustainability of Korea’s equity rally.

A sharp correction, particularly in a market so concentrated in semiconductor stocks, could quickly force capital to rotate again. KOSPI has come under pressure recently as disruptions in oil transits through the Strait of Hormuz has sparked energy supply concerns.

Banks are increasingly testing tokenized deposits as a practical way to move traditional commercial bank money onto blockchain-based payment and settlement rails. A new report from the real-world asset data platform RWA.io, with input from UK Finance, Citi, BNY, JPMorgan’s Kinexys, Standard Chartered, ABN Amro and Digital Asset, argues that tokenized deposits are emerging alongside stablecoins and central bank digital currencies as part of a broader on-chain cash stack for the financial system.

Tokenized deposits are digital representations of ordinary bank deposits on blockchain or other distributed ledger infrastructure. Unlike many stablecoins, they are direct liabilities of the issuing bank and remain governed by existing banking frameworks, including deposit insurance, capital requirements and anti-money laundering and know-your-customer rules. The report highlights a growing slate of pilots and deployments across Europe as banks seek to preserve their role in payments, treasury and deposit-taking amid a proliferation of digital cash instruments.

The report notes visible momentum in Europe, anchored by recent public pilots. In January, Lloyds Banking Group and Archax announced they completed the UK’s first public blockchain transaction using tokenized deposits on the Canton Network. Separately, UK Finance’s Great British Tokenised Deposit pilot is examining person-to-person marketplace payments, remortgaging and digital-asset settlement with a target to advance through mid-2026.

The broader narrative is that banks are trying to reposition themselves at the center of digital money flows as tokenized forms of cash multiply and new settlement rails emerge. The two-tier monetary-ecosystem picture that underpins these efforts is a key theme of the report and a reminder that commercial bank money continues to underpin everyday payments even as the frontier of digital assets expands.

Tokenized deposits as a middle ground in the stablecoin, CBDC debate

UK Finance frames tokenized deposits as a vital bridge in a future “multi-money” ecosystem. In their view, tokenized deposits will sit alongside privately issued stablecoins and, potentially, central bank digital currencies, offering a framework in which traditional bank money can operate on new digital rails while preserving regulatory protections and consumer safeguards.

“Bringing that money onto digital rails will underpin the next generation of digital finance,” said Marko Vidrih, co-founder and chief operating officer at RWA.io. “For that reason, it is important to understand how tokenized deposits fit within the broader digital money ecosystem alongside stablecoins and CBDCs.”

ECB advances digital euro work, building tokenized money rails

The policy backdrop in Europe is advancing in parallel. The European Central Bank is expanding its digital euro program as private and public digital money compete for cross-border and domestic use. The ECB has opened applications for experts to contribute to workstreams on how a digital euro would function across ATMs, payment terminals and acceptance infrastructure, with plans to begin a 12-month pilot in the second half of 2027.

In March, the ECB unveiled Appia, its long-term blueprint for tokenized markets in Europe that would work with central bank money. A core element of Appia is Pontes, a new settlement mechanism designed to connect blockchain-based platforms to the Eurosystem’s payment infrastructure. The existing framework, TARGET Services, already processes large-value euro payments, securities settlements and instant payments across Europe. Pontes is scheduled to launch in the third quarter of 2026, with feedback from Appia’s consultation guiding broader tokenized-finance framework decisions for Europe.

These developments come as policymakers seek to balance innovation with safety, and as banks, fintechs and custodians explore how tokenized assets and on-chain settlement fit within existing regulatory and supervisory regimes.

For market participants, the implication is clear: tokenized deposits could serve as a practical on-ramp for institutions anchored in traditional banking to participate in the digitized economy without abandoning their regulated foundations. The combined push—from UK pilots to European rails—highlights a trend toward interoperable, regulated on-chain money that preserves the institutional protections that users rely on today.

As the ecosystem evolves, investors and users will be watching how these rails interact with private-stablecoin ecosystems, CBDC pilots and cross-border settlement standards. The success of tokenized deposits will hinge on risk controls, interoperable settlement timelines, and the readiness of banks to scale these pilots into durable, insured, compliant products that can operate alongside existing payment networks.

What remains uncertain is how quickly regulators will align around clear standards for tokenized deposits, what coverage and insurance will apply at scale, and how liquidity and settlement finality will be ensured across heterogeneous blockchain rails. Yet the convergence of bank money with tokenized infrastructure marks a notable shift in the trajectory of digital finance, one that could influence how institutions price, manage and settle money in a world where digital and traditional money increasingly coexist.

Readers should watch the next phase of UK pilots and the European rollout of Appia and Pontes for concrete milestones on settlement timings, interoperability tests and regulatory clarity that could determine whether tokenized deposits become a standard feature of the financial system, or a pioneering set of pilots with limited upside outside controlled environments.

Craig Bellamy: Inside the complex mind of Wales’ head coach

Carjackers Turn VA Man’s Dream Corvette Into A Repair Nightmare

Paul Limb of Action Coach, Bolton, has the secret of success

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Adidas – Corporette.com

-

Politics2 days ago

Politics2 days agoJenni Murray, Long-Serving Woman’s Hour Presenter, Dies Aged 75

-

Tech6 days ago

Tech6 days agoAre Split Spacebars the Next Big Gaming Keyboard Trend?

-

Crypto World2 days ago

Crypto World2 days agoNIO (NIO) Stock Plunges 6.5% as Shelf Registration Sparks Dilution Worries

-

Crypto World1 day ago

Crypto World1 day agoBest Crypto to Buy Now: Strategy Just Spent $1.57 Billion on Bitcoin During Fear While Early Investors Quietly Enter Pepeto for 150x Potential

-

News Videos5 days ago

News Videos5 days agoRBA board divided on rate cut, unusually buoyant share market | Finance Report | ABC NEWS

-

Crypto World1 day ago

Crypto World1 day agoBitcoin Price News: Bhutan Sells $72 Million in BTC Under Fiscal Pressure, but the Smart Money Entering Pepeto Sees What the Market Does Not

-

Business7 days ago

Business7 days agoAustralian shares drop as Iran war enters third week

-

Crypto World7 days ago

Crypto World7 days agoCrypto Lender BlockFills Enters Chapter 11 with Up to $500M in Liabilities

-

Politics5 days ago

Politics5 days agoThe House | The new register to protect children from their abusers shows Parliament at its best

-

Fashion7 days ago

Fashion7 days ago25 Celebrities with Curly Hair That Are Naturally Beautiful

-

Tech3 days ago

Tech3 days agoinKONBINI Lets You Spend Summer Days Behind the Register

-

Politics6 days ago

Politics6 days agoReal-time pollution monitoring calls after boy nearly dies

-

Crypto World5 days ago

Crypto World5 days agoCanada’s FINTRAC revokes registrations of 23 crypto MSBs in AML crackdown

-

NewsBeat4 days ago

NewsBeat4 days agoResidents in North Lanarkshire reminded to register to vote in Scottish Parliament Election

-

Business7 days ago

Business7 days agoMeta planning major layoffs as AI spending and automation reshape workforce

-

News Videos5 days ago

News Videos5 days agoPARLIAMENT OF MALAWI – PAC MEETING WITH REGISTRAR OF FINANCIAL ON AMARYLLIS HOTEL – INQUIRY LIVE

-

Business14 hours ago

Business14 hours agoNo Winner in March 21 Drawing as Prize Rolls to $133 Million for Next

-

Entertainment7 days ago

Oscars reunite Rob Reiner supergroup of 17 stars for emotional tribute: Here's who appeared on stage

-

Business4 days ago

Business4 days agoWho Was Alex Pretti? 5 Key Facts About the ICU Nurse Killed by Federal Agents in Minneapolis

You must be logged in to post a comment Login