Business

Treasury Yields Slip After Inflation Report

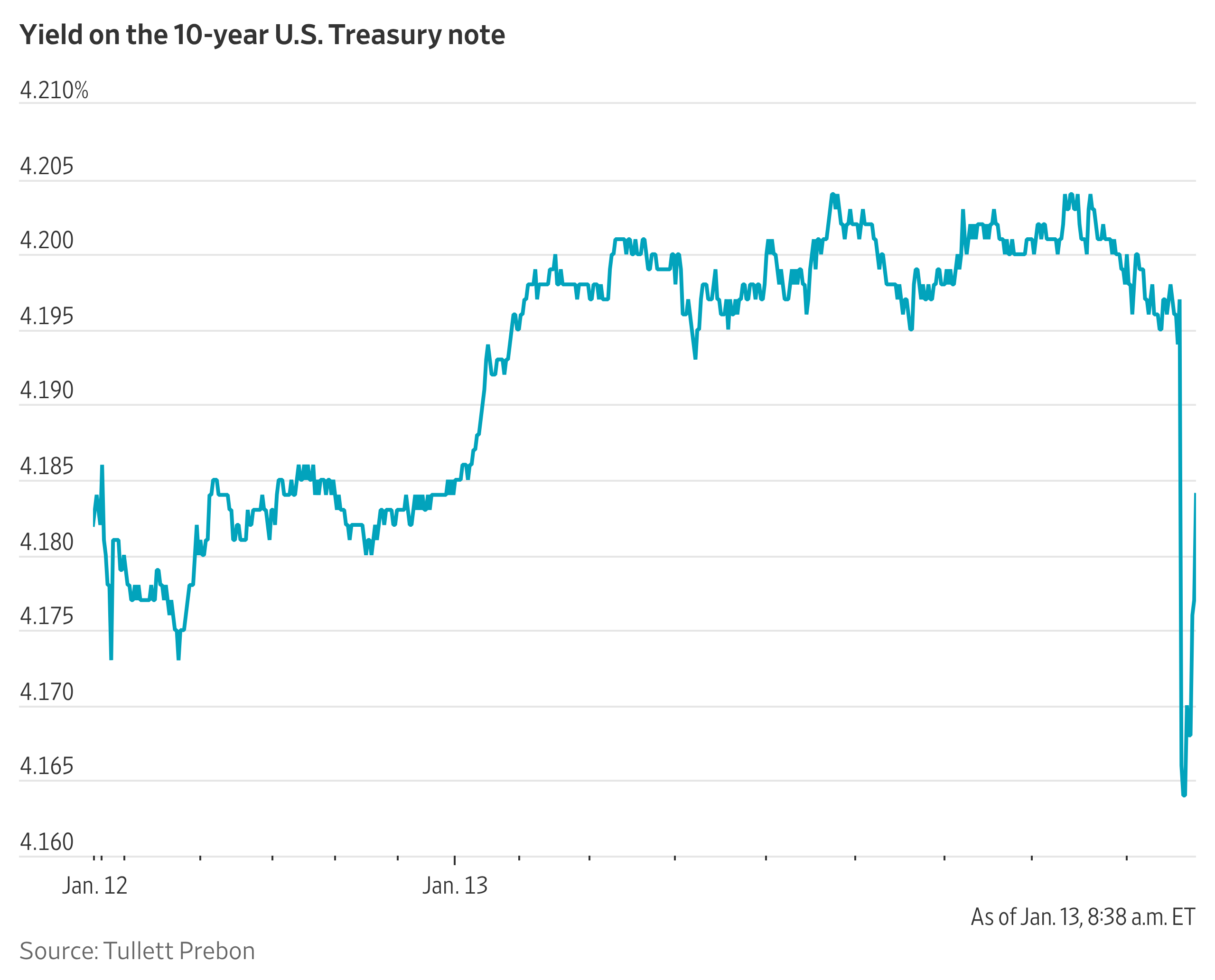

Treasury yields edged lower after a cooler-than-expected December inflation reading.

Though headline inflation matched economists’ expectations, investors care more about so-called core prices, which exclude volatile food and energy categories. Those rose less than anticipated in December.

In recent trading, the yield on the benchmark 10-year U.S. Treasury note was 4.177%, according to Tradeweb, down from around 4.195% just before the report was released.

Continue Reading