Crypto World

ECB Flags Stablecoins as a Growing Risk to Bank Lending

The European Central Bank said rising stablecoin use can pull money out of bank deposits and weaken the way monetary policy flows through to lending, according to a new ECB working paper published Tuesday.

Growing adoption of stablecoins, which are digital assets often pegged to currencies such as the US dollar or euro, is expected to draw funds away from traditional bank deposits, the ECB said in its latest working paper series, “Stablecoins and Monetary Policy Transmission,” released Tuesday.

“Our analysis shows that rising interest in stablecoins is linked to a measurable decline in retail bank deposits and a reduction in lending to firms,” the report said, noting that stablecoins can reduce the amount of credit banks provide to the real economy.

The ECB noted that the effects are nonlinear and vary depending on the scale of stablecoin adoption, their design features, and how they are regulated.

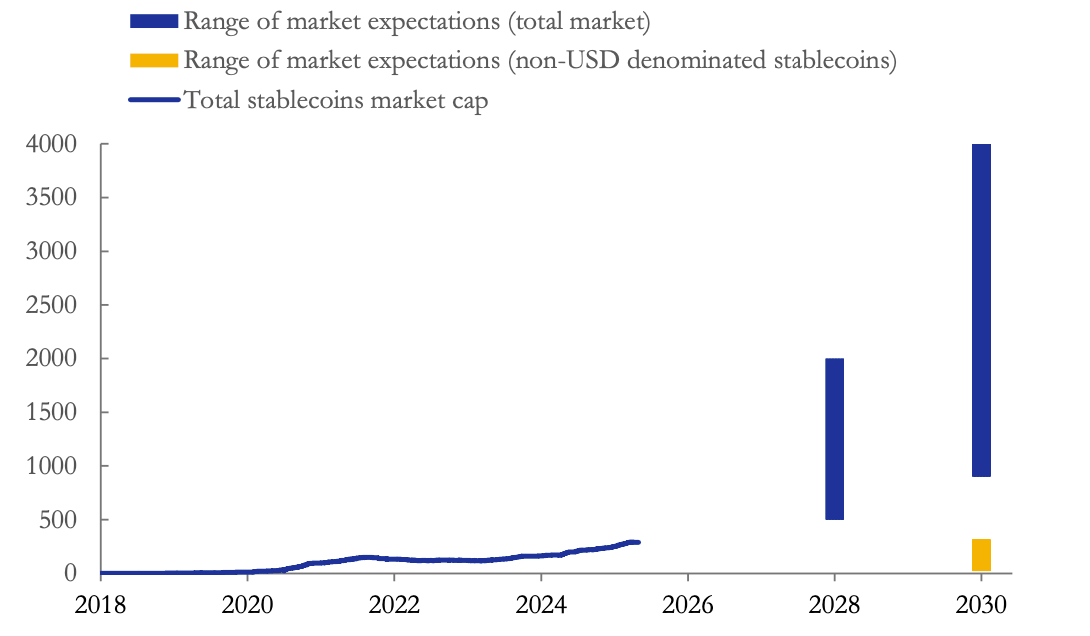

The report is part of the ECB’s ongoing efforts to monitor stablecoins, whose market capitalization has more than doubled over the past three years to $312 billion and is projected to reach $2 trillion by 2028.

Stablecoin impact: Banks, monetary policy and why currency matters

In assessing the impact of growing stablecoin adoption on banks, the ECB highlighted a deposit-substitution effect, where households and firms move funds from retail bank deposits to digital assets.

“Banks rely heavily on deposits as a stable and low-cost source of funding to support lending to households and businesses,” the study said.

“When deposits decline, banks may be forced to rely more on wholesale or market-based funding, which is typically more expensive and less stable,” it added.

The report also finds that stablecoins can change how policy interest rates affect bank funding costs and lending, with impacts varying by adoption scale, design and regulation.

“We find that stablecoin adoption interferes with multiple monetary policy transmission channels, potentially weakening the predictability of policy actions,” the ECB said.

Related: ECB targets 2027 digital euro pilot as provider selection begins in Q1 2026

The central bank warned that foreign-currency stablecoins could further weaken the connection between domestic monetary policy and bank lending, with risks amplified when the market is dominated by non-euro-denominated tokens.

The study reiterated that US dollar-backed stablecoins make up the vast majority of the stablecoin market. Data from CoinGecko shows these dollar-pegged tokens are valued at $301 billion, representing 97% of total stablecoin market capitalization at publishing time.

Magazine: Clarity Act risks repeat of Europe’s mistakes, crypto lawyer warns

Crypto World

AI startup Cursor in talks to raise $2 billion funding round at valuation of over $50 billion

The Cursor logo arranged on a smartphone in New Hyde Park, New York, Nov. 20, 2025.

Gabby Jones | Bloomberg | Getty Images

Artificial intelligence startup Cursor is in talks to raise a $2 billion fundraising round at an over $50 billion valuation, which does not include the investment, a source familiar with the matter told CNBC.

Andreessen Horowitz is slated to co-lead the new investment round, in which Nvidia and Thrive Capital are also expected to participate, said the source, who was not authorized to publicly speak on the investment. Those three firms have all previously backed the AI coding startup.

Bloomberg News first reported that Cursor was raising capital.

The funding round underscores the venture capital industry’s enthusiasm for startups specializing in AI coding agents that can complete a range of software development tasks for users. Although Cursor was among the first major startups to focus on AI coding agents, other companies, such as Google, Anthropic and OpenAI, have since debuted similar tools.

Cursor announced in November that it closed a $2.3 billion funding round at a $29.3 billion post-money valuation. That financing came after a $900 million investment round in June.

Among Cursor’s current investors are Accel, DST Global, Coatue and Google, according to a corporate blog post.

The startup released in February various updates intended to help software developers, including giving AI agents the ability to test their coding changes and record their actions via videos, logs and screenshots.

Cursor did not immediately reply to a request for comment.

WATCH: Cursor CEO Michael Truell: We’re seeing success with our AI age, not just demand

Bitcoin’s current market cycle is broadly viewed as weaker than its three prior halving-driven runs, according to Galaxy’s head of firmwide research, Alex Thorn. By weighing price action since the April 2024 halving against the patterns seen in 2012, 2016 and 2020, Thorn argues that volatility has cooled and upside potential appears more constrained this time around. Notably, the all-time high above $125,000, reached on Oct. 5, 2025, was only about 97% above the 2024 halving price near $63,000, illustrating a markedly tamer peak for the cycle so far.

Thorn’s comparisons hinge on a stark difference in how cycles unfold. The 2012 halving cycle saw a roughly 9,294% price surge to around $1,163; 2016 delivered about a 2,950% surge to near $19,891; and the 2020 halving generated a roughly 761% gain. In Thorn’s view, “Cycle four is dramatically underperforming prior cycles,” a conclusion he shared in an X post that raises a bigger question: is this the new normal, or will the cycle evolve in unforeseen ways?

Beyond price trajectories, the market’s behavioral foundations may be shifting. Thorn notes that volatility has declined with each successive halving, suggesting that BTC’s price could become more influenced by factors outside of the four-year cycle theory traditionally cited by traders. The 30-day Bitcoin Volatility Index has not surpassed 3.11% in the current cycle, with the last reading above that level recorded on Aug. 24, 2024. The latest 30-day figure sits at about 1.75%, according to Bitbo data.

Key takeaways

- Galaxy’s Alex Thorn concludes the current BTC cycle is dramatically weaker than the 2012, 2016 and 2020 halving cycles when comparing price action since the April 2024 halving.

- The all-time high above $125,000 in October 2025 was roughly 97% above the 2024 halving price around $63,000, signaling a much milder top versus prior cycles.

- Volatility has systematically compressed across cycles, with the 30-day BTC volatility staying well below the peaks seen in earlier halvings (latest around 1.75%).

- Market critics point to an early all-time high before the 2024 halving as an anomaly, underscoring that one-off catalysts can distort cycle comparisons.

Market dynamics and the pre-halving anomaly

Another layer of complexity comes from an event-driven impulse that disrupted typical cycle timing. BTC briefly hit an all-time high above $70,000 in March 2024—one month before the April 2024 halving. Analysts have attributed part of the outsized early move to the subsequent approval of spot Bitcoin ETFs in the United States in January 2024, which acted as a catalyst for price acceleration ahead of the halving. This premature peak is frequently cited by critics as a meaningful deviation from the classic halving-driven narrative.

In parallel, Fidelity Digital Assets has observed that Bitcoin’s drawdowns in this cycle have been less severe than in past bear markets. While declines of 80%–90% are not unheard of in older cycles, the drop from the all-time high to later troughs has so far been more contained in this phase. Fidelity’s analysis notes that even a journey back from peak levels remains substantial—BTC pulled back from the late-2021 highs to the roughly $60,000 area, a move just over 50% in magnitude from the peak levels cited by Fidelity’s framework.

Near-term outlook and the long arc

March brought a contrarian take from Jan van Eck, CEO of VanEck, who said BTC is close to bottoming and that a gradual recovery could begin in 2026. While such forecasts hinge on a confluence of macro factors, liquidity conditions, and investor sentiment, they align with a broader sense that BTC may enter a more protracted phase of consolidation after 2025’s peak, rather than repeating the rapid, cycle-driven surges seen in earlier eras.

As of the latest readings, Bitcoin was trading near $74,703, with fresh momentum up modestly over the past week. The price backdrop underscores Thorn’s observation of a more muted cycle, even as headlines around regulatory clarity, ETF developments, and institutional participation continue to influence sentiment.

What to watch next

The immediate question for investors and builders alike is whether this cycle’s subdued volatility and mixed momentum represent a lasting regime shift or a temporary deviation sparked by unique catalysts. Key developments to monitor include how macro conditions interact with BTC’s supply-demand dynamics, any concrete shifts in ETF-related inflows, and whether the market can align around a clearer, more repeatable set of catalysts akin to past halving narratives. As the market evolves, readers should watch for signs that long-run adoption, liquidity depth, and regulatory clarity begin shaping BTC’s trajectory in a way that differentiates this cycle from its predecessors.

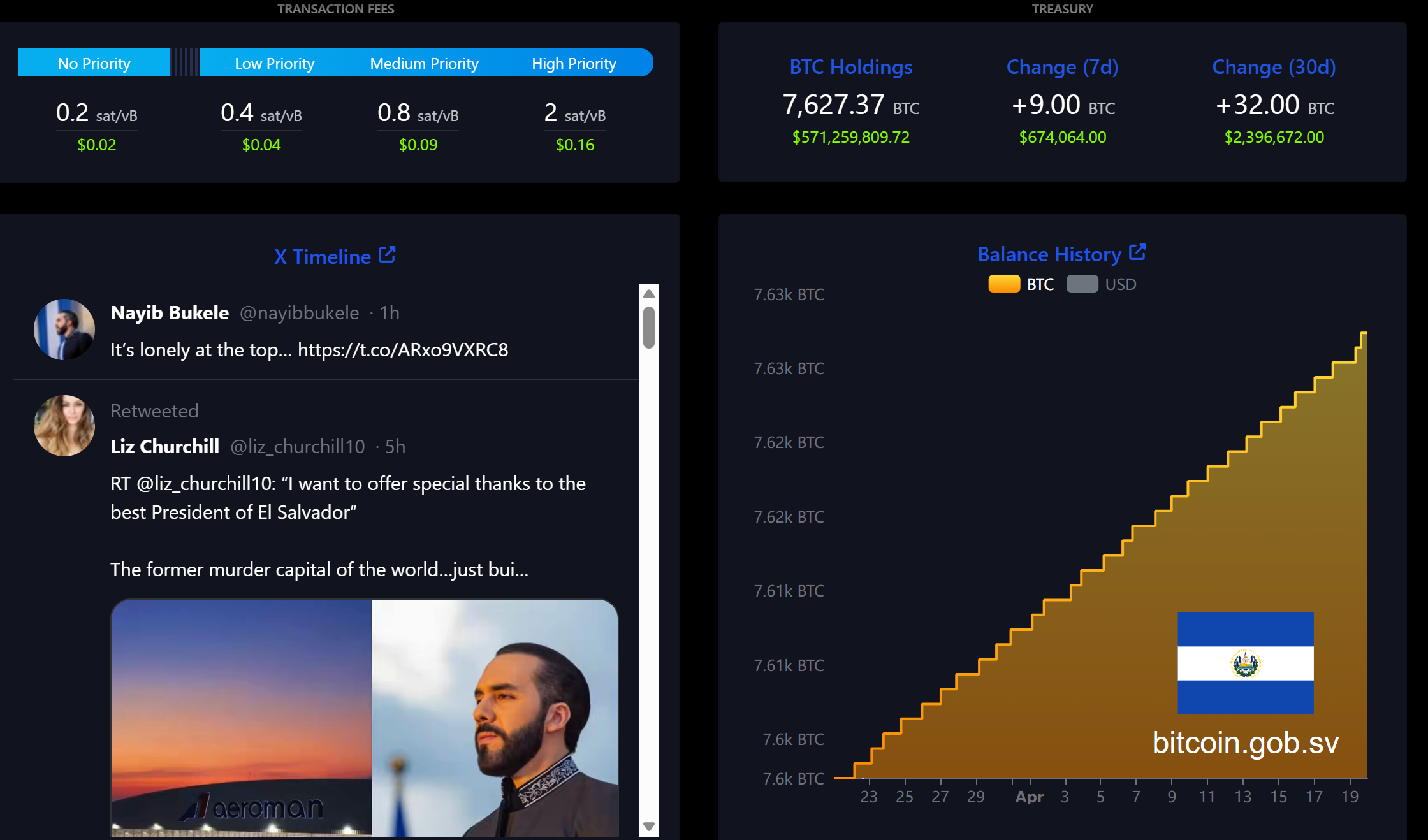

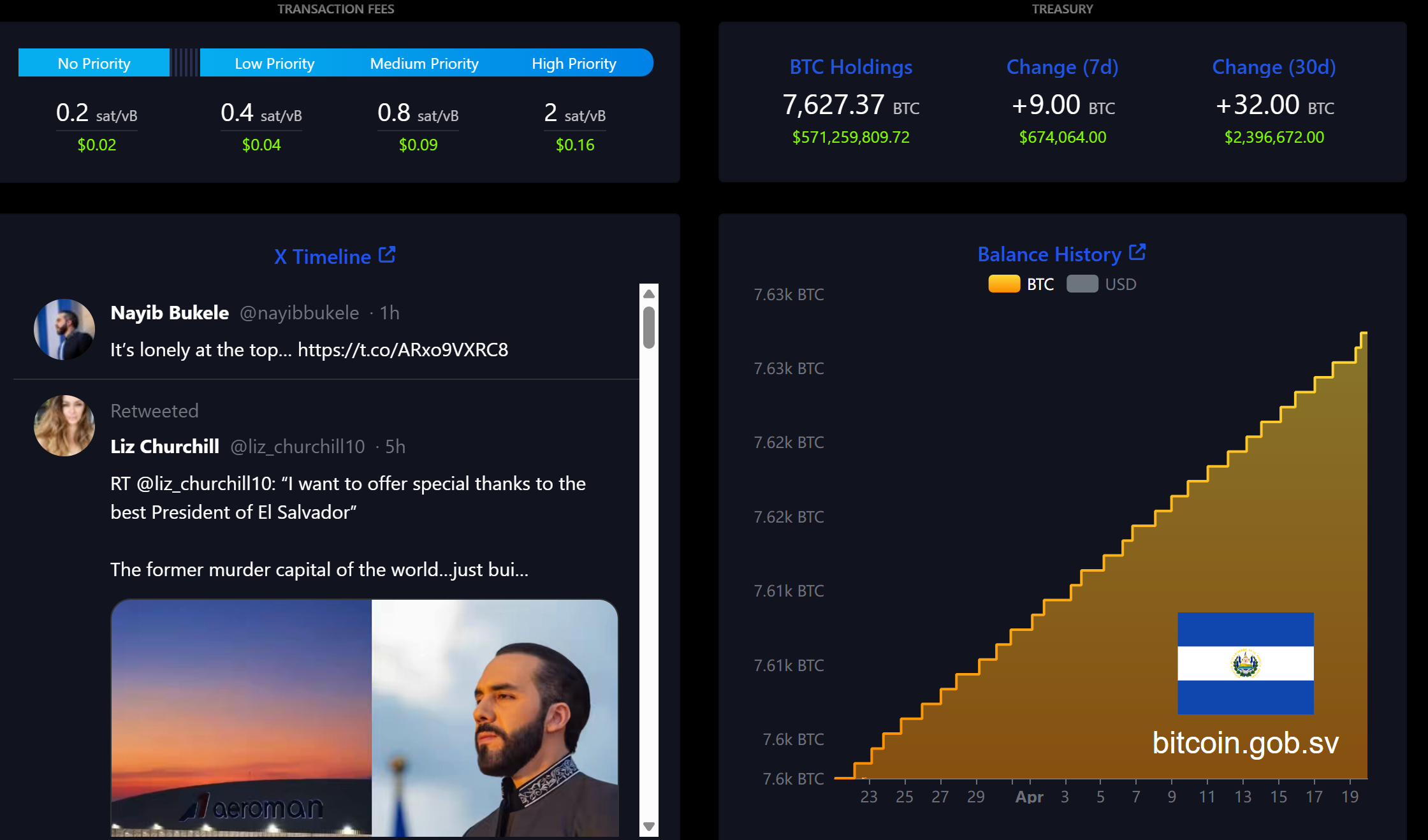

El Salvador President Nayib Bukele sits atop a global leader approval chart with a 94% rating, far outpacing every other head of state on the list.

The ranking measures approval for 26 world leaders. Bukele’s dominance highlights a striking detail for the crypto industry. The president who went furthest on sovereign Bitcoin (BTC) adoption is also the most popular leader on Earth right now.

The Bitcoin President Still Stacks Daily

El Salvador became the first country to make Bitcoin legal tender in 2021. The government continues purchasing roughly one BTC per day, pushing its national reserve past 7,600 BTC.

Polls show, however, that security gains from Bukele’s gang crackdown drive his approval far more than the Bitcoin experiment itself.

Only 2.2% of Salvadorans cited BTC as his biggest failure in a recent CID Gallup survey.

Where Other Leaders Stand on Crypto

South Korea’s Lee Jae-myung (63%) has declared crypto a national priority, pledging spot Bitcoin ETFs and a won-pegged stablecoin by 2026.

Javier Milei (48%) championed Bitcoin deregulation in Argentina but saw his credibility damaged after promoting the LIBRA meme coin, which collapsed and cost investors hundreds of millions.

Donald Trump (38%) signed an executive order establishing a US Strategic Bitcoin Reserve funded with seized coins, positioning the country as a future “Bitcoin superpower.”

Most remaining leaders on the list follow standard regulatory frameworks, with several EU heads of state backing stricter oversight through the MiCA regulation.

The chart suggests that bold pro-Bitcoin moves have not hurt leaders politically, even if domestic voters care more about security and the economy than digital assets.

The post The President Who Pushed Bitcoin the Hardest Is Now the Most Popular Leader on Earth appeared first on BeInCrypto.

Crypto World

Why Does the Next Fed Chair Own SOL Before His April 21 Hearing? Pepeto 300x Rotation Explained

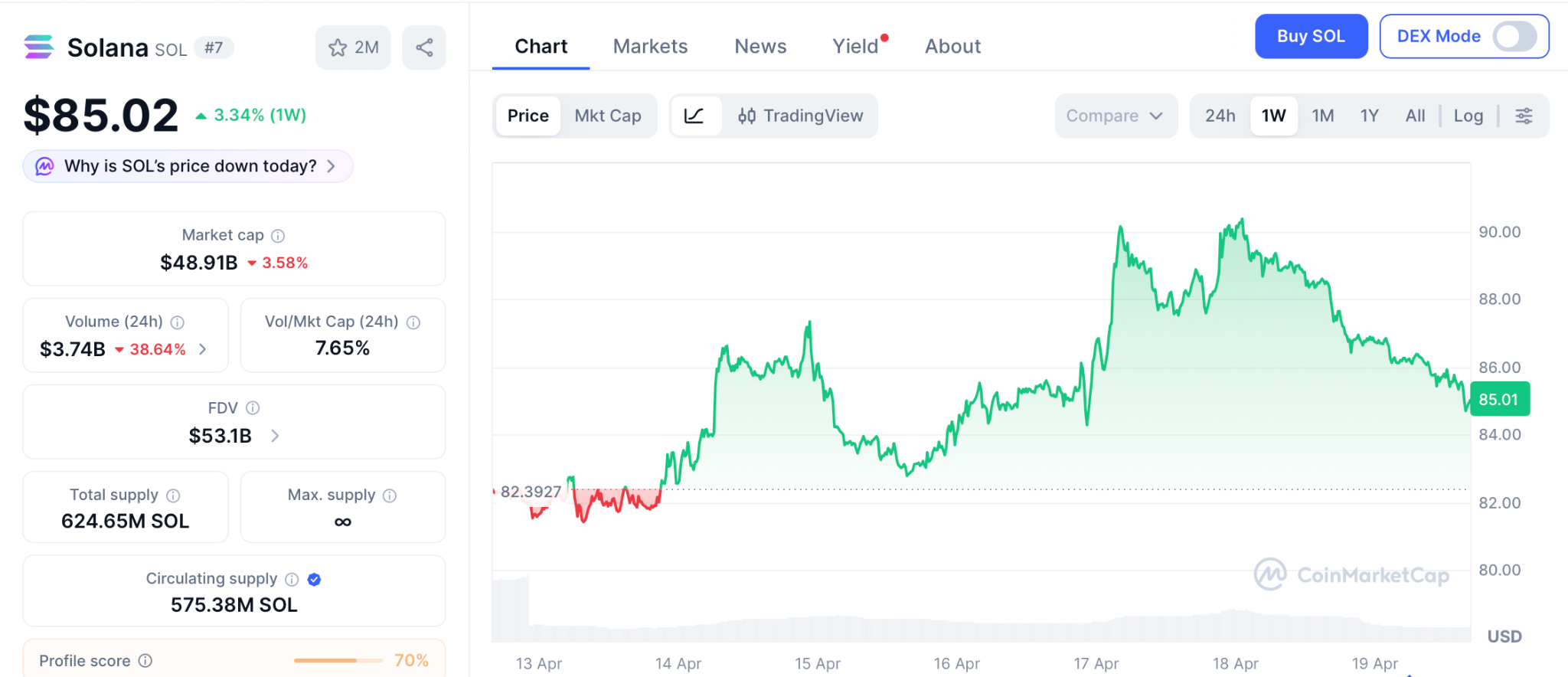

The solana price prediction just picked up a talking point nobody saw coming. Kevin Warsh, Donald Trump’s nominee to chair the Federal Reserve, disclosed indirect Solana holdings across multiple venture fund vehicles in his April 14 ethics filing, per Decrypt, with the Senate confirmation hearing locked for April 21. SOL trades at $85.02 with Bitcoin pushing past $77,300 and the tape finally turning green across the majors.

The numbers look strong, but SOL at a $50 billion market cap is simply too large to print the multiples that reshape a portfolio from a single position. That is where Pepeto steps in, a fresh presale trending hard across crypto feeds this quarter, carrying the kind of traction every cycle signals ahead of returns no large cap can match.

Warsh’s 69 page filing with the Office of Government Ethics lists indirect SOL positions held through the AVGF I venture fund alongside stakes in Optimism, Compound, dYdX, Polymarket, Blast, and more than 30 other Web3 names, per Yahoo Finance. Combined assets top $192 million, making this the broadest Web3 portfolio ever disclosed by a senior US financial nominee.

The Senate Banking hearing lands April 21, the same window that holds the CLARITY Act committee markup and the Fed’s April 28-29 meeting. Spot SOL ETFs have crossed $892 million in net assets, with Bitwise’s BSOL alone pulling $808 million in cumulative inflows per Bitcoin.com. The timing puts SOL at the intersection of every major US monetary and regulatory decision this month.

Solana Price Prediction Compared: SOL Setup and the Presale Opportunity Pepeto

The solana price prediction section below breaks down how even the bullish $180 target spreads across months, and for traders who want more, the audited exchange pulling capital in this quarter is the play worth watching. Pepeto gives retail access to tools large holders previously kept private, wrapped in a single platform.

A contract scanner built into the exchange screens each token before any deposit opens, putting buyers ahead of the news cycle. Presale wallets earn 181% APY through daily compounding staking as the rounds fill, meaning the earliest buyers hold the heaviest positions the second demand peaks.

A risk scoring engine reads momentum across the chain and flags suspect contracts before a dollar moves. The presale has pulled in $9.21 million at $0.0000001865, backed by a SolidProof audit and driven by the founder who pushed Pepe to $7 billion on 420 trillion tokens, now leading this exchange alongside a former Binance executive.

The entry window narrows every hour as the Binance listing draws closer. Once public trading opens, millions of new buyers set the price and the presale floor vanishes on the spot. Every past crypto recovery paid the wallets that moved while the crowd was waking up, and once Pepeto’s Binance listing lands, the 300x runway from presale pricing closes the same day.

Solana (SOL) Price Prediction: Can SOL Reach $180?

Solana (SOL) trades at $85.02 per CoinMarketCap, bouncing with the broader market, still 70% below the $293 peak from November 2021. SOL holders sit at 167 million monthly unique wallets per Solana Foundation data, a record set in April.

Standard Chartered’s $250 target rests on Alpenglow’s 150 millisecond finality upgrade and the spot ETF products giving institutions a regulated route in.

CoinCodex sketches a 2026 channel between $84 and $133.03 with the average near $119. Even the aggressive solana price prediction reaching $180 prints around 103% over several months. Strong for a large cap, but a presale at 300x math from one Binance listing event beats months of chart watching by a wide margin.

Conclusion:

The solana price prediction points at $180 to $250 on a long runway, and that kind of move sounds great until you stack it next to the 300x analysts are calling for on Pepeto presale pricing. Once the gap is visible, the SOL forecast starts looking modest, and the rotation into earlier entries starts to make sense.

The accounts that turned Pepe and DOGE into life changing positions were all built the same way. Capital went in before the coin hit every screen, the deposit held through the first exchange print, and compounding did the lifting from there.

Pepeto runs that exact playbook right now. The raise crossed $9.21 million, fresh capital keeps hitting the contract every day, and the Binance listing creeps closer hour by hour. The wallets depositing at $0.0000001865 today are the ones reading their own names in the millionaire headlines the next cycle writes.

Click To Visit Pepeto Website To Enter The Presale

FAQs

What does the solana price prediction target for 2026?

Standard Chartered places Solana (SOL) at $250 and CoinCodex models a $119 average for 2026, with $180 as a mid cycle target from the current $85.02 level. Fed Chair nominee Kevin Warsh disclosed SOL holdings in his April 14 filing ahead of an April 21 Senate hearing, while Pepeto at presale pricing targets 300x.

How does Solana (SOL) compare to Pepeto as an entry today?

Solana (SOL) at $85.02 projects toward $133 to $180 through 2026 per CoinCodex and Standard Chartered. Pepeto at $0.0000001865 with $9.21 million raised and a Binance listing days away offers a presale to listing return that beats even the strongest solana price prediction.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

Crypto World

BitGo, Polygon Among Industry Giants Pushing Rate Limits After The Largest DeFi Exploit of 2026

A wave of protocol-level security responses followed the $292 million KelpDAO rsETH exploit on April 19, with BitGo, Polygon, and Katana moving swiftly to isolate potential contagion.

The attack drained 116,500 rsETH from Kelp DAO’s LayerZero-powered cross-chain bridge through a forged message that bypassed its Decentralized Verifier Network (DVN) configuration.

Protocols Move to Contain Fallout

BitGo, alongside BiT Global Trust, took down the LayerZero OFT DVNs for Wrapped Bitcoin (WBTC) as a precaution. The firm confirmed that user funds remain secure and pledged to share updates as more information becomes available.

Polygon stated that its chain, Agglayer, and broader ecosystem remain unaffected by the incident. The network noted it has safely processed over $2 trillion to date.

Katana paused the OFT path on Vaultbridge, which relied on a 2/3 DVN setup. Bridging through Agglayer, which verifies with zero-knowledge proofs rather than proof-of-authority multisigs, remained fully available.

Meanwhile, Cyvers CTO and co-founder Meir Dolev revealed that KelpDAO was just three minutes away from losing an additional $100 million. A rapid-response blacklist blocked the attacker before a second attempt could succeed.

Industry Leaders Call for Structural Rate Limits

The exploit has reignited calls for built-in rate limits across DeFi protocols. Ethena contributor Guy Young argued that asset issuers should implement throttled cross-chain transfers on top of standard LayerZero OFTs.

“We built a solution on top of the standard OFT to throttle cross chain transfers at $10m per hour for every DVN, in addition to the $10m per block rate limit on the mint contract. The former would have prevented Kelp, the latter Resolv,” he wrote.

Ethena’s configuration caps potential damage at $10 million per chain per hour even if a DVN is fully compromised. Young called the slight inconvenience for users a worthwhile tradeoff to avoid catastrophic losses.

Keone Hon, CEO and co-founder of Monad, proposed that pooled lending protocols adopt “smart caps” that limit how quickly collateral supply can grow.

He pointed to the Resolv hack in March, where the attacker minted infinite tokens but could only extract $24 million because exit pathways were small.

Hon argued that high supply caps should be seen as a liability, not a sign of stature. A supply limit slightly above current utilization, adjusting over hours to the true cap, would have saved rsETH depositors $200 million, he estimated.

The KelpDAO breach is now the largest DeFi exploit of 2026. Whether protocols adopt the rate-limiting measures these leaders are proposing may determine how large the next one gets.

The post BitGo, Polygon Among Industry Giants Pushing Rate Limits After The Largest DeFi Exploit of 2026 appeared first on BeInCrypto.

TLDR:

- An ECB director stated tokenization restructures entire financial systems, surpassing all previous waves of technological change.

- The UK reversed its stablecoin payments policy, bringing digital assets into its formal regulatory perimeter for the first time.

- HSBC completed a tokenized deposit pilot covering issuance, transfer, and atomic settlement on the Canton Network successfully.

- Clearstream will custody and settle Ondo’s tokenized stocks and ETFs, embedding digital assets into core European market infrastructure.

Tokenization is gaining serious traction across Europe as regulators, central banks, and financial institutions move toward digital asset integration.

A European Central Bank director recently stated that tokenization’s effect on finance surpasses earlier waves of technological change.

Major institutions across the continent are responding with concrete steps. From regulatory reversals to live pilots and cross-border partnerships, Europe is emerging as a key driver of the global tokenization push.

European Regulators Set the Tone for a New Financial Era

A European Central Bank director drew a sharp distinction between tokenization and previous technological shifts in finance.

According to Ledger Insights, the director noted that these technologies do not merely improve one part of a system.

Rather, they restructure the entire logic of how financial systems operate. That assessment positions tokenization as a foundational change, not an incremental upgrade.

The statement carried weight given the ECB’s central role in shaping European financial policy. When a director at that level speaks about systemic change, institutions across the continent take notice.

The framing moved the conversation beyond speculation and into strategic planning. European banks and depositories began responding almost immediately.

Across the Channel, the UK government reversed its earlier position on stablecoins within payments regulation. Authorities confirmed plans to bring stablecoins into the country’s formal payments regulatory perimeter.

That reversal closed a policy gap that had kept digital assets outside mainstream financial oversight. Britain’s shift aligned it more closely with the direction Europe’s financial regulators are heading.

Together, these regulatory signals are creating a more predictable environment for tokenized finance. Institutions require clear frameworks before committing to infrastructure investments at scale.

With central bank commentary and government policy now pointing in the same direction, that clarity is forming. Europe’s regulatory posture is becoming one of cautious but deliberate acceptance.

European Institutions Move From Pilots to Permanent Infrastructure

HSBC completed a tokenized deposit pilot on the Canton Network, marking a practical step forward for European banking. The exercise simulated the issuance, transfer, and atomic settlement of its Tokenised Deposit Service.

All three functions were tested in a controlled environment, confirming operational readiness. The pilot demonstrated that large European banks are past the conceptual stage.

ABN Amro extended crypto access to its investment clients through a carefully structured approach. The Dutch bank introduced indirect exposure via Exchange Traded Products and Capital Protected Notes.

Both instruments are available through ABN Amro’s existing investment platforms, keeping the process familiar for clients. That design reflects how European institutions are balancing innovation with risk management.

The most structurally significant development came through the Ondo Finance, Clearstream, and 360X partnership.

Clearstream, Europe’s leading securities depository, will provide custody, settlement, and collateralization for Ondo’s tokenized stocks and ETFs.

This integration places tokenized assets directly inside established institutional workflows. It removes a barrier that had long kept digital assets separate from mainstream settlement infrastructure.

That partnership matters because Clearstream operates at the core of European capital markets. Anchoring tokenized securities within its framework gives institutional participants a trusted, regulated entry point.

European financial infrastructure is no longer sitting adjacent to tokenization. It is becoming part of it.

TLDR:

- AVAX trades near $9 as price consolidates above key support within a multi-year descending triangle structure

- Strong buyer activity appears around $8–$10, with reduced volatility signaling a possible accumulation phase

- Resistance between $13 and $16 remains critical, with a breakout needed to shift short-term momentum

- A confirmed move above the descending trendline could open a path toward the $60–$80 price range

Avalanche (AVAX) is trading near a key support zone as its weekly chart shows a long-term descending triangle. Price action suggests buyers are stepping in, with consolidation forming near the lower boundary of the structure.

AVAX Holds Key Support as Buyers Step In

AVAX has remained within a broad downtrend since its 2021 peak above $130. The weekly chart shows a clear pattern of lower highs, guided by a descending resistance trendline. This structure has kept selling pressure active during each rally attempt.

According to analyst Butterfly on X, AVAX is bouncing from the lower edge of the triangle. The post added that buyers are showing interest near this support, with early signs of control shifting toward bulls.

Price is now hovering around $9.18, just above a strong support zone between $10.5 and $11. This area has been tested several times, making it a key level for market participants. Below this, the $8 to $9 range has acted as a short-term accumulation zone.

The chart also shows reduced volatility within this range. Price movement has tightened, forming a consolidation pattern. This behavior often appears when selling pressure slows and buyers begin absorbing available supply.

Volume data supports this view. Larger spikes appeared during earlier sell-offs and rebounds. More recently, volume has stabilized, with no sharp increase in selling activity. This trend suggests that the market may be entering a transition phase.

Resistance Levels Define Next Direction

While support has held, several resistance levels remain in focus. The first barrier sits between $13.5 and $16.5, where recent price rejection occurred. A move above this range could shift short-term momentum.

Beyond that, the $20.5 to $25.5 range represents a mid-level resistance zone. This area aligns with the previous price structure and could slow movement upward if reached. The descending trendline near $30 remains the most critical level.

A breakout above this trendline would change the long-term structure. It would end the pattern of lower highs and open the path for a broader recovery. Projections from the chart suggest that such a move could push the price toward the $60 to $80 range.

On the downside, a break below $8 would weaken the current setup. In that case, price could move toward the $6 to $7.5 region. This level has served as support in the past and may attract new buying interest.

For now, AVAX remains in a narrow range between $8 and $12. This zone has become a key area where both buyers and sellers are active. The longer the price stays within this band, the stronger the next move could be.

Market participants are watching closely as the structure approaches a decision point. The repeated defense of support suggests ongoing demand. At the same time, resistance levels continue to cap upward movement.

The weekly chart reflects a market in balance, with both sides waiting for confirmation. A move beyond these defined levels will likely set the next direction for AVAX.

Crypto World

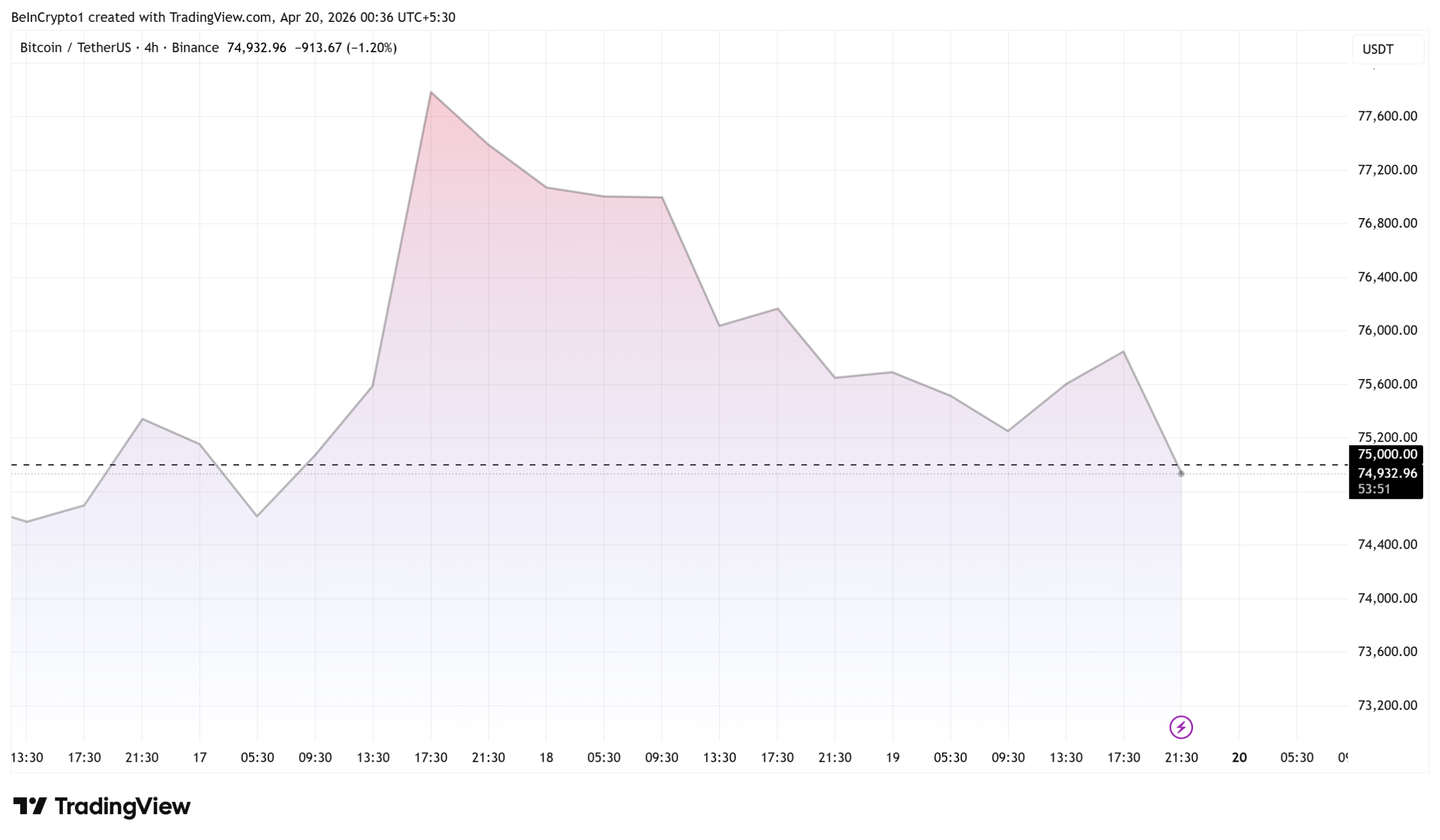

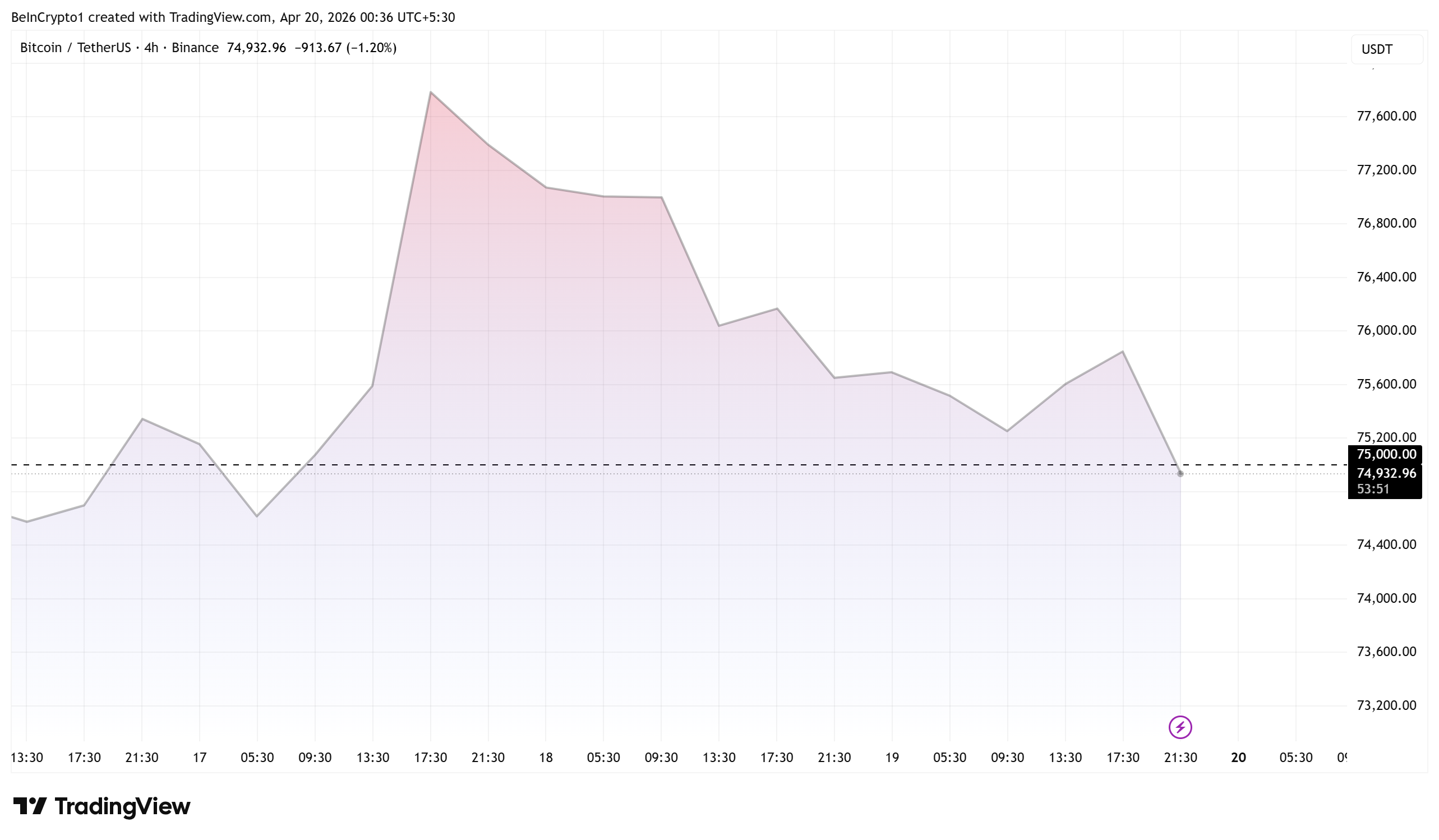

Bitcoin Dips Below $75,000 as Strait of Hormuz Sees Zero Oil Tankers for First Time in History

Bitcoin (BTC) dropped below $75,000 on April 19 as the Strait of Hormuz shut down entirely and Iran rejected a second round of negotiations with the United States.

The developments mark a sharp escalation in the US-Iran standoff, with zero oil tankers passing through the strait and diplomatic channels appearing to collapse.

Strait of Hormuz Shuts Down as Diplomacy Stalls

No oil tankers passed through the Strait of Hormuz, effectively closing the waterway that handles roughly 20% of global seaborne oil trade.

“It appears that the Strait of Hormuz is now completely closed for the first time in history. The US “blockade” and Iran’s closure are in full force,” wrote The Kobeissi Letter.

Reportedly, thirteen tankers had already turned back mid-route the day before, freezing shipping flows through the critical chokepoint.

Iran’s state media confirmed that Tehran rejected participating in a second round of talks with Washington. Iranian officials cited what they called “deception” from President Trump, pointing to “inconsistency with what is actually happening” during negotiations.

The rejection came after the first round of talks in Islamabad ended without an agreement last week.

Trump Escalates Threats Against Iran

President Trump accused Iran of firing on ships in the strait in violation of the ceasefire agreement. He threatened to “knock out every single Power Plant, and every single Bridge, in Iran” if Tehran refuses a deal.

General sentiment is that both countries are on the verge of a new round of escalation, with futures markets set to open within hours.

Bitcoin has faced sustained pressure from the US-Iran conflict since February 28. The pioneer crypto previously fell from above $100,000 when Iran first moved to close the strait earlier this year. Amid Sunday’s risk-off sentiment, the king of crypto fell below $75,000 for yet another time.

Rising oil prices and inflation fears have repeatedly pushed investors toward traditional safe-haven assets over crypto.

The coming hours may prove critical as futures markets open and traders price in the diplomatic breakdown.

The post Bitcoin Dips Below $75,000 as Strait of Hormuz Sees Zero Oil Tankers for First Time in History appeared first on BeInCrypto.

TLDR:

- Solana’s monthly chart shows a cup-and-handle pattern forming after a long recovery from 2023 lows.

- Price remains inside a descending channel, with $70–$80 support acting as a key short-term level.

- Resistance between $240–$280 marks the breakout zone needed to confirm the bullish continuation pattern.

- A breakdown below $70 may weaken the structure, while holding support keeps the consolidation phase active.

Solana’s monthly price structure is drawing attention as it continues to form a classic cup-and-handle pattern. The asset remains within a consolidation phase, with price currently moving inside the handle range after a strong recovery from earlier lows.

Long-Term Structure Shows Gradual Recovery

Solana’s macro chart reflects a rounded bottom that formed between 2021 and 2024. Price peaked near $240–$260 in 2021 before entering a prolonged decline. It later found support near $10–$12 in early 2023, marking the cycle low.

Bitcoinsensus describes this structure as a developing cup-and-handle pattern on the monthly timeframe.

The post notes that the recovery from the 2023 lows formed a rounded base, which is often linked to steady accumulation rather than rapid speculation.

From that bottom, price climbed steadily toward the previous highs, completing the cup formation. This move established a broader bullish structure, supported by higher highs during the recovery phase. The return to the $240–$260 range defined the upper boundary of the cup.

Since reaching that zone, the price has not broken out. Instead, it has entered a controlled pullback. This phase forms the handle portion of the structure, which typically follows a rounded recovery.

The handle appears as a downward-sloping channel. Current price action remains within this range, with resistance near $180–$200 and support around $70–$80. At the time of observation, the price traded near $89.97, closer to the lower boundary.

Consolidation Phase Keeps Market in Balance

The handle structure reflects short-term pressure, although the broader trend remains intact. This phase often involves reduced volatility compared to the earlier recovery. Price movement within this channel suggests a pause rather than a confirmed reversal.

Key resistance levels remain clearly defined. The descending channel top sits near $170–$200, acting as immediate resistance. Beyond that, the $240–$280 range marks the major breakout zone tied to the cup formation.

On the downside, the $70–$80 region serves as critical support. A breakdown below this level could shift market structure. In such a case, the price may move toward $60 or lower, weakening the current pattern.

The broader structure remains intact as long as support holds. The cup-and-handle pattern traditionally requires a breakout above the rim for confirmation. In this case, that level lies near $240–$280.

If price moves above this zone with strong momentum, the pattern projects a larger upside range. The depth of the cup suggests a possible extension toward $450–$550. However, such movement depends on sustained strength and a confirmed breakout.

For now, the price continues to move within the handle. This keeps the market in a neutral position, with both upward and downward scenarios still open.

A hold above support may allow a move toward channel resistance. A break below support could delay further recovery.

The current phase remains focused on consolidation. Market participants continue to watch the $70–$80 support and the descending resistance line for direction. Movement beyond these levels will likely define the next stage of the trend.

TLDR:

- Money market funds recorded a $172.2B weekly outflow, the largest ever, far exceeding typical April withdrawal trends.

- Equity funds attracted $11.3B while bond funds saw $7.9B inflows, showing a shift toward diversified allocations.

- Crypto and gold funds each gained $1.2B, reflecting steady demand for alternative assets during capital rotation.

- Seasonal tax payments and portfolio adjustments drove withdrawals, pushing the four-week average to early 2024 levels.

Money market funds recorded a historic weekly outflow as capital rotated across asset classes. Recent data shows a sharp withdrawal trend, with funds moving into equities, bonds, and alternative assets during a period that often aligns with seasonal tax payments.

Record Outflows Reshape Short-Term Liquidity Trends

Money market funds saw a weekly outflow of $172.2 billion, marking the largest drawdown ever recorded. The scale of withdrawals exceeded typical April averages, reflecting an unusual shift in short-term liquidity positioning.

According to a post shared by The Kobeissi Letter on X, the weekly outflow was over 320% above the average April movement seen in recent years.

The data also showed that the four-week moving average dropped to negative $30.0 billion, reaching levels last seen in early 2024.

This change in flow patterns coincided with capital moving into other financial instruments. Equity funds attracted $11.3 billion, while bond funds recorded inflows of $7.9 billion during the same period. These figures suggest that investors adjusted allocations rather than exiting markets entirely.

At the same time, alternative assets saw moderate interest. Gold and crypto-related funds each received $1.2 billion in inflows. While smaller in size compared to equities and bonds, these inflows indicate continued diversification across asset classes.

April often brings seasonal liquidity changes due to tax obligations. As a result, part of the outflow from money market funds was linked to tax-related withdrawals. This pattern tends to repeat annually, although the magnitude this time stands out.

Capital Rotation Signals Broader Allocation Shifts

The movement of funds into equities and bonds points to a broader reallocation strategy. Investors appear to be balancing short-term liquidity needs with longer-term positioning across markets.

Equity inflows suggest a willingness to maintain exposure to risk assets despite recent volatility. Meanwhile, bond inflows indicate continued interest in fixed-income securities, often used for stability during uncertain conditions.

The inflows into gold and crypto funds, although smaller, add another layer to the overall picture. These assets are often viewed as alternative stores of value, especially during periods of shifting liquidity trends.

The decline in the four-week moving average of withdrawals also provides context. It shows that while the weekly outflow was large, the broader trend reflects sustained but less extreme withdrawals over time.

Taken together, the data show that capital is not leaving the financial system but moving between asset classes. Seasonal factors, combined with changing market preferences, continue to shape these flows.

As April progresses, similar patterns may continue, especially if tax-related withdrawals remain active. However, the redistribution of funds suggests ongoing engagement across multiple markets rather than a retreat from risk.

Stocks Over Houses: The New Financial Success Strategy #shorts

Nominations open for 2026 North Yorkshire Community Awards

AI startup Cursor in talks to raise $2 billion funding round at valuation of over $50 billion

Why Israel is blocking foreign journalists from entering

Bitcoin: We’re Entering The Most Dangerous Phase

Alan Cumming Brands Baftas Ceremony A ‘Triggering S**tshow’

Stocks Over Houses: The New Financial Success Strategy #shorts

Tangem’s NEW Multi-Account Feature Just Changed Everything: Ultimate Digital Asset Management System

Make Money With Claude As A Beginner In 2026 (Easy 16 Minute Guide)

-

NewsBeat7 days ago

NewsBeat7 days agoPep Guardiola and Gary Neville agree over Arsenal title problem that benefits Man City

-

Crypto World6 days ago

Crypto World6 days agoThe SEC Conditionalises DeFi Platforms to Be Avoided for Broker Registration

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Theodora Dress

-

Crypto World6 days ago

Crypto World6 days agoSEC Signals Exemption for Crypto Interfaces From Broker Registration

-

News Videos5 days ago

News Videos5 days agoSecure crypto trading starts with an FIU-registered

-

Sports3 days ago

Sports3 days agoNWFL Suspends Two Players Over Post-Match Clash in Ado-Ekiti

-

Crypto World6 days ago

Crypto World6 days agoSEC Proposes Certain Crypto Interfaces Don’t Need to Register as Brokers

-

NewsBeat5 days ago

NewsBeat5 days agoTrump and Pope Leo: Behind their disagreement over Iran war

-

Business7 hours ago

Business7 hours agoPowerball Result April 18, 2026: No Jackpot Winner in Powerball Draw: $75 Million Rolls Over

-

Politics2 days ago

Politics2 days agoPalestine barred from entering Canada for FIFA Congress

-

Crypto World2 days ago

Crypto World2 days agoRussia Pushes Bill to Criminalize Unregistered Crypto Services

-

Sports6 days ago

Sports6 days agoNWFL opens Pathway for new Clubs ahead of 2026 Season

-

Politics11 hours ago

Politics11 hours agoZack Polanski demands ‘council homes not luxury flats for foreign investors’

-

Entertainment6 days ago

Entertainment6 days agoBrand New Day’ Footage Reveals the Devastating Impact of ‘Now Way Home’

-

Business3 days ago

Business3 days agoCreo Medical agree sale of its manufacturing operation

-

Crypto World7 days ago

Crypto World7 days agoTrump whales load up ahead of Mar-a-Lago luncheon.

-

Crypto World7 days ago

Sei Network Enters Quiet Reset Phase as On-Chain Metrics Signal a Slowdown in 2026

-

Business7 days ago

Kering slides after Morgan Stanley downgrade, Gucci woes loom

-

Tech7 days ago

Tech7 days agoGoogle adds E2E encryption to Gmail for iOS and Android enterprise users

-

Tech7 days ago

Tech7 days agoApple glasses won’t go brand shopping like Meta did with Ray-Ban and Oakley

You must be logged in to post a comment Login