Crypto World

this is how payments get de-risked

Disclosure: The views and opinions expressed here belong solely to the author and do not represent the views and opinions of crypto.news’ editorial.

Today, stablecoins already move real money and power a large share of on-chain settlement. McKinsey puts daily stablecoin transaction volumes at roughly $30 billion, and if that figure is even close to reality, calling stablecoins “experimental” is absurd. Still, mass adoption isn’t here.

Summary

- Stablecoins aren’t blocked by regulation — they’re blocked by liability: businesses won’t adopt payments where responsibility for errors, disputes, and compliance is unclear.

- Interoperability, not speed, is the real scaling bottleneck: without standardized data, ERP integration, and consistent exception handling, stablecoins can’t function as real business payments.

- Wyoming’s governed stablecoin shows the path forward: defined rules, auditability, and institutional accountability de-risk stablecoins and make them usable inside real finance workflows.

Most businesses don’t pay suppliers, run payroll, or process refunds in stablecoins at any real scale. Even with Wyoming’s precedent of launching a state-issued stablecoin, the same question remains: what’s actually blocking adoption if the pipes already exist?

The typical answer would be regulation. But I think it’s only part of it, as the bigger obstacle is accountability and plumbing. When a digital-asset payment goes wrong, who takes the loss? Who can fix it? And who can prove to an auditor that everything was done correctly? So let’s break down what’s still holding stablecoins back from mass adoption, and what an actual way out could look like.

When nobody owns the liability

To be honest, the fact that stablecoins are drifting has less to do with businesses not “getting” the technology. They understand the mechanism. The real block is a blurry responsibility model.

In traditional payments, the rules are dull, but dependable: who can reverse what, who investigates disputes, who is liable for mistakes, and what evidence satisfies auditors. With stablecoins, that clarity often disappears once the transaction leaves your system. And that’s where most pilots fail.

A finance team can’t run on guesswork about whether money arrives, whether it gets stuck, or whether it comes back as a compliance problem three weeks later. If funds go to the wrong address or a wallet is compromised, someone has to own the result.

In bank transfers, that ownership is defined. With stablecoins, too much is still negotiated case by case between the sender, the payment provider, the wallet service, and sometimes an exchange on one side. Everyone has a role, yet no one is truly accountable — and that’s how risk spreads.

Regulation is supposed to solve this, but it’s not fully there yet. The market is getting more guidance, especially in the U.S., where the OCC’s letter #1188 has clarified that banks can engage in certain crypto-related activities like custody and “riskless principal” transactions. That helps, but it doesn’t solve the daily operating questions.

As a result, permission doesn’t automatically create a clean model for disputes, checks, evidence, and liability. It still has to be built into the product and spelled out in contracts.

Sending is easy, settling isn’t

Liability is one part of the limitation. Another one is just as visible: the rails still don’t plug into how companies actually run money. In other words, interoperability is the gap between “you can send the money” and “your business can actually run on it.”

A stablecoin transfer can be fast and final. But that alone doesn’t make it a business payment. Finance teams need every transfer to carry the right reference, match a specific invoice, pass internal approvals and limits, and be transparent. When a stablecoin payment arrives without that structure, someone has to repair it manually, and the “cheap and instant” promise turns into extra work.

That’s where fragmentation silently kills scale. Stablecoin payments don’t arrive as one network. They come as islands — different issuers, different chains, different wallets, different APIs, and different compliance expectations. Even the International Monetary Fund flags payment-system fragmentation as a real risk when interoperability is missing, and the back office feels it first.

All in all, until payments carry standard data end-to-end, plug into ERP and accounting without custom work, and handle exceptions the same way every time, stablecoins won’t scale. But is there something that could make liability and plumbing issues solvable in a way that businesses can actually use?

Wyoming’s blueprint for governed stablecoins

In my opinion, liability and plumbing become solvable the moment a payment system has two things: a set of rules, and a standard way to plug into existing finance workflows. That’s where Wyoming precedent matters. A state-issued stable token gives the market a governed framework that a business can evaluate, reference in contracts, and defend in front of auditors.

Here’s what that framework opens up for businesses in more detail:

- Easier approval from finance and compliance. Adoption stops depending on a few “crypto-friendly” teams and starts working through normal risk committees, procurement rules, and audit checklists.

- Cleaner integration. When “the rules of the money” are defined at the institutional level, you can build repeatable workflows that work across systems and markets, instead of reinventing the setup for every vendor and jurisdiction.

- More realistic bank and PSP partnerships. The model aligns more closely with fiduciary expectations, such as tighter oversight, more transparent reserve rules, and accountability that can be written into contracts.

Given the context, stablecoins can’t seamlessly scale on speed and convenience alone. The way I see it, responsibility must be unambiguous, while payments have to fit the tools businesses already use. Wyoming’s case isn’t a panacea. Yet, it underscores that stablecoins should be treated as governed, auditable money, so real-world adoption stops feeling far off.

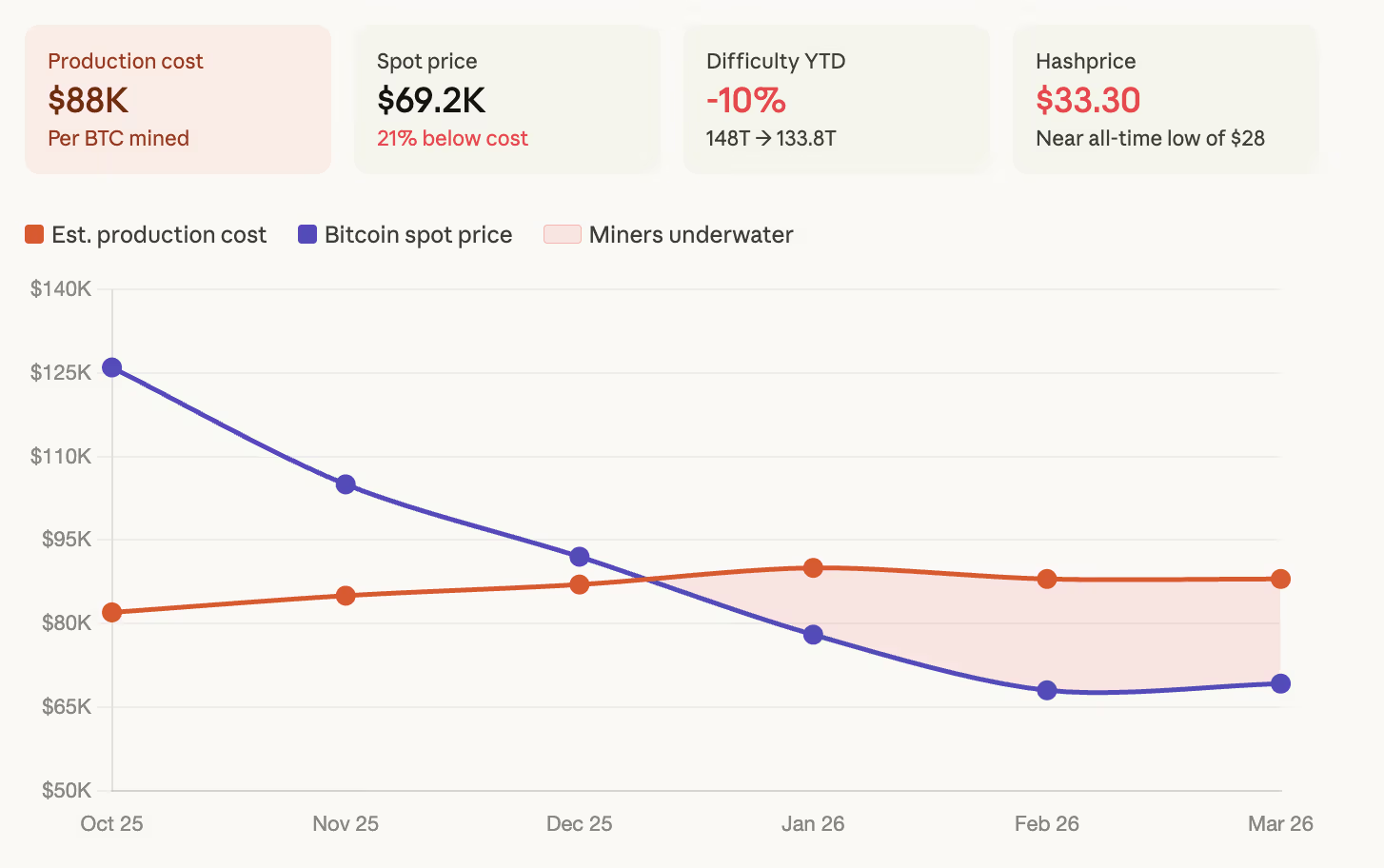

The math has turned against bitcoin miners, and the war is making it worse every week.

Checkonchain’s difficulty regression model, which estimates average production costs based on network difficulty and energy inputs, pegged the figure at $88,000 per bitcoin as of March 13.

Bitcoin is trading at $69,200 as on Sunday morning, creating a gap of nearly $19,000 per coin and meaning the average miner is operating at a 21% loss on every block produced.

The cost squeeze has been building since October’s crash took bitcoin from $126,000 to below $70,000, but the Iran war accelerated it. Oil above $100 feeds directly into electricity costs for mining operations, particularly the estimated 8-10% of global hashrate operating in energy markets sensitive to Middle Eastern supply.

The Strait of Hormuz, which handles roughly 20% of the world’s oil and gas flows, remains effectively closed to most commercial traffic. And Trump’s 48-hour ultimatum on Saturday threatening to attack Iran’s power plants added a new layer of risk for miners.

The network is already showing the stress. Difficulty dropped 7.76% on Saturday to 133.79 trillion, the second-largest negative adjustment of 2026 after February’s 11.16% plunge during Winter Storm Fern. Difficulty is now nearly 10% below where it started the year and far below November 2025’s all-time high near 155 trillion.

The hashrate has retreated to roughly 920 EH/s, well below the record 1 zetahash level reached in 2025. Average block times during the last epoch stretched to 12 minutes and 36 seconds, well above the 10-minute target.

Hashprice, the metric tracking expected miner revenue per unit of computing power, is hovering around $33.30 per petahash per second per day according to Luxor’s Hashrate Index. That’s near breakeven for most hardware and not far from the all-time low of $28 hit on Feb. 23.

When miners can’t cover costs, they sell bitcoin to fund operations. That selling adds supply pressure to a market already dealing with 43% of total supply sitting at a loss, whales distributing into rallies, and leveraged positioning dominating price action. Mining economics aren’t just a sector story. They’re a market structure story.

The publicly traded miners have been adapting by diversifying into AI and high-performance computing, which offer more predictable revenue than mining bitcoin at a loss. Marathon Digital, Cipher Mining, and others have been building out data center capacity alongside their mining operations.

The next difficulty adjustment is projected for early April and is expected to decline further according to CoinWarz data. If bitcoin stays below $88,000, and there’s no sign of a return to that level in the near term, the miner exodus continues and difficulty keeps falling.

The network self-corrects by design, making it cheaper to mine as participants leave. But the period between when costs exceed revenue and when difficulty adjusts low enough to restore profitability is where the damage happens, both to miners and to the spot market absorbing their forced selling.

TLDR:

- Founders Fund is set to lead Halter’s new round, valuing the cattle AI startup at $2 billion.

- Halter’s solar-powered collars move and monitor cattle remotely using an algorithm called Cowgorithm.

- US ranchers saved $220 million in fencing costs using Halter’s 11,000-mile virtual fence network.

- Halter charges $5 to $8 per animal monthly, creating recurring revenue that scales with herd size.

Peter Thiel’s Founders Fund is set to lead a new funding round for Halter, an AI-powered cattle collar startup. The round would value the Auckland-based company at more than $2 billion before new money is counted.

Halter makes solar-powered GPS collars that let farmers herd and monitor cattle remotely through a smartphone app. The deal is heavily oversubscribed and final terms may still change.

Founders Fund Places a Major Bet on AI-Driven Farming

Founders Fund’s decision to back Halter ranks among the firm’s most notable agtech moves. Peter Thiel built it into one of Silicon Valley’s most powerful venture capital firms.

Its entry into agricultural technology through Halter signals a shift in where major capital is now heading.

The round values Halter at $2 billion before new money is counted. That doubles its $1 billion valuation reached in June, when BOND led a $100 million raise. Reaching that mark in under one year is rare in any technology sector.

Halter and Founders Fund both declined to comment. Sources familiar with the matter asked not to be identified as talks remain private.

The deal is heavily oversubscribed, meaning demand exceeded what Halter originally sought. The final round size remains undetermined.

Founders Fund’s entry comes as the agtech sector recovers from a prolonged slump. Many agricultural technology companies declared bankruptcy in recent years as adoption lagged.

Halter has been a consistent exception, growing steadily while others failed. That track record drew Founders Fund’s attention.

One widely shared post captured the product’s appeal simply: “A farmer opens an app, taps a button, and 600,000 cows across three countries start walking toward the milking station on their own.” For Thiel’s firm, it reflects a belief that AI in farming can deliver outsized returns.

What Founders Fund Is Betting On Inside Halter’s Technology

Halter’s product is a solar-powered GPS collar worn by cattle. Farmers manage herds through an app sending vibration and audio cues to each collar.

A single tap moves a herd to a milking station with no dogs, fences, or labor needed. The company trademarked this system as the “Cowgorithm.”

Each collar tracks digestion, fertility cycles, and health patterns around the clock. Machine learning models trained on hundreds of thousands of animals power these features.

US ranchers have mapped over 11,000 miles of virtual fencing, saving an estimated $220 million in physical fencing costs.

Halter charges farmers between $5 and $8 per animal per month. As more cattle are collared, revenue compounds and customer retention deepens.

This mirrors the subscription frameworks that firms like Founders Fund know well. Recurring revenue tied to a growing animal base makes for a compelling investment profile.

Halter was founded by Craig Piggott, a former rocket engineer at Rocket Lab. “The goal was to make pasture farming more sustainable and productive using technology,” he told Bloomberg in 2024. His engineering background shaped both the collar hardware and the algorithm driving it.

The company is based in Auckland and has opened a Colorado office to support US expansion. That move reflects growing demand from American ranchers adopting precision farming tools.

Founders Fund is now betting that Piggott’s vision for agriculture is as transformative as anything the firm has previously backed.

Bitcoin has given back last week’s gains in a single weekend.

The largest cryptocurrency slid to $69,192 on Sunday morning, down 2.2% over the past 24 hours and 3.1% on the week, after U.S. president Donald Trump issued a 48-hour ultimatum to Iran late Saturday demanding the reopening of the Strait of Hormuz or face attacks on the country’s power plants.

Trump said he would “hit and obliterate” Iran’s power plants, beginning with the largest, if the strait wasn’t opened to commercial shipping.

The threat marks a dramatic escalation from Friday, when Trump said he was thinking about “winding down” the military operation. Going from winding down to threatening civilian infrastructure in 24 hours whipsawed a market that had spent the previous week building confidence around de-escalation.

The liquidation data shows how one-sided the positioning was heading into the weekend. CoinGlass data shows $299 million in total liquidations over the past 24 hours across 84,239 traders, with long liquidations accounting for $254 million, roughly 85% of the total.

Bitcoin longs took $122 million in damage. Ether longs lost $95.7 million. The largest single liquidation was a $10 million BTC-USDT swap on OKX. The lopsided ratio confirms the market was leaning heavily bullish after eight consecutive days of gains heading into the weekend, leaving it vulnerable to exactly this kind of headline shock.

Major tokens fell in lockstep, meanwhile. Ether dropped 1.8% to $2,114, XRP lost 2.5% to $1.41, BNB slid 1.4% to $633, solana fell 2.1% to $88.55, and dogecoin lost 2.7% to $0.092. The only majors green on the week were ether at 0.8% and solana at 0.7%. Everything else is red over seven days.

The 48-hour window means the deadline arrives Monday evening. If Iran doesn’t comply, and there’s no indication it will, the market faces the prospect of strikes on power infrastructure, which would be the first direct targeting of civilian energy systems in the conflict.

The Strait of Hormuz remains effectively closed to most commercial traffic, with roughly 20% of the world’s oil and gas flows still disrupted.

Last week’s rally to $75,912 now looks like it was built on ceasefire speculation that evaporated over the weekend. The Fed held rates on Wednesday with a dovish lean that should have supported risk assets, but the persistent risk of war headlines has traders holding back from making outsized directional bets.

TLDR:

- Bitcoin put/call open interest ratio averaged 0.77, its highest reading since China banned mining in June 2021.

- Put premiums relative to BTC spot volume hit an all-time high of 4 basis points, tripling mid-2022 levels.

- Historical data shows D9 skew decile has produced average 90-day BTC returns of +13.2%, the strongest of all deciles.

- Aggregate miner BTC balances sit at 684,000 BTC, with miners selling nearly all newly issued supply over the past year.

Bitcoin markets entered a consolidation phase following a sharp price drawdown in early 2026. VanEck’s mid-March Bitcoin ChainCheck report reveals deeply defensive positioning across derivatives markets.

The put/call open interest ratio reached its highest level since June 2021. Realized volatility dropped from 80 to 50, while futures funding rates fell to 2.7%. Onchain activity declined broadly as miner revenues came under pressure.

Bitcoin Options Positioning Reflects Elevated Demand for Downside Protection

Bitcoin options markets are showing an unusual level of caution among investors. The put/call open interest ratio peaked at 0.84 and averaged 0.77 over the past month.

This places the metric in the 91st percentile of all observations recorded since mid-2019. The last time the ratio reached these levels was June 2021, when China banned Bitcoin mining.

Total put premiums over the past 30 days reached approximately $685 million. That figure represents a 24% decline month-over-month, yet it still exceeds 77% of monthly readings since early 2025.

Relative to spot volume, put premiums hit an all-time high of roughly 4 basis points. This is about three times the levels seen after the Terra/Luna collapse in mid-2022.

Meanwhile, call option premiums fell roughly 12% to around $562 million. This decline further confirms a broad shift toward protective positioning in the market.

Total options open interest still rose 3% month-over-month to $33.4 billion. Futures leverage, however, remained subdued throughout the period.

VanEck’s report also examined the put/call premiums paid ratio, which reached 2.0 for the 30-day period ending March 3, 2026. Implied volatility on puts averaged around 66, sitting approximately 16 points above realized volatility.

Historically, skew readings at this decile have preceded average 90-day Bitcoin returns of +13.2%. Average 360-day returns from similar readings came in at +133.2%.

Onchain Activity and Miner Economics Show Broad Pressure

Onchain network activity declined across nearly every major metric over the past month. Transfer volume fell 31%, while total daily fees dropped 27%.

Daily active addresses declined 5%, and mean transaction fees fell by 40%. Transaction count was the only category that posted a modest increase.

A growing share of Bitcoin trading now occurs through ETPs, derivatives, and centralized exchanges. As a result, traditional onchain metrics may no longer capture total market activity accurately.

This shift makes it harder to use network data alone as a sentiment indicator. The trend reflects Bitcoin’s increasing financialization across institutional markets.

On the miner side, total revenues declined 11% over the past month. Mining equities fell roughly 7%, pointing to weaker profitability across the sector.

Miner outflows to exchanges rose only 1% in Bitcoin terms. Most operators appear to be managing reserves carefully rather than liquidating holdings.

Aggregate miner balances currently sit at approximately 684,000 BTC, down only 0.5% year-over-year. Over the same period, roughly 164,000 new BTC were mined and effectively sold.

Long-term holder transfer volume declined across every age cohort during the period. Active long-term Bitcoin supply also edged down from 31% to 30%.

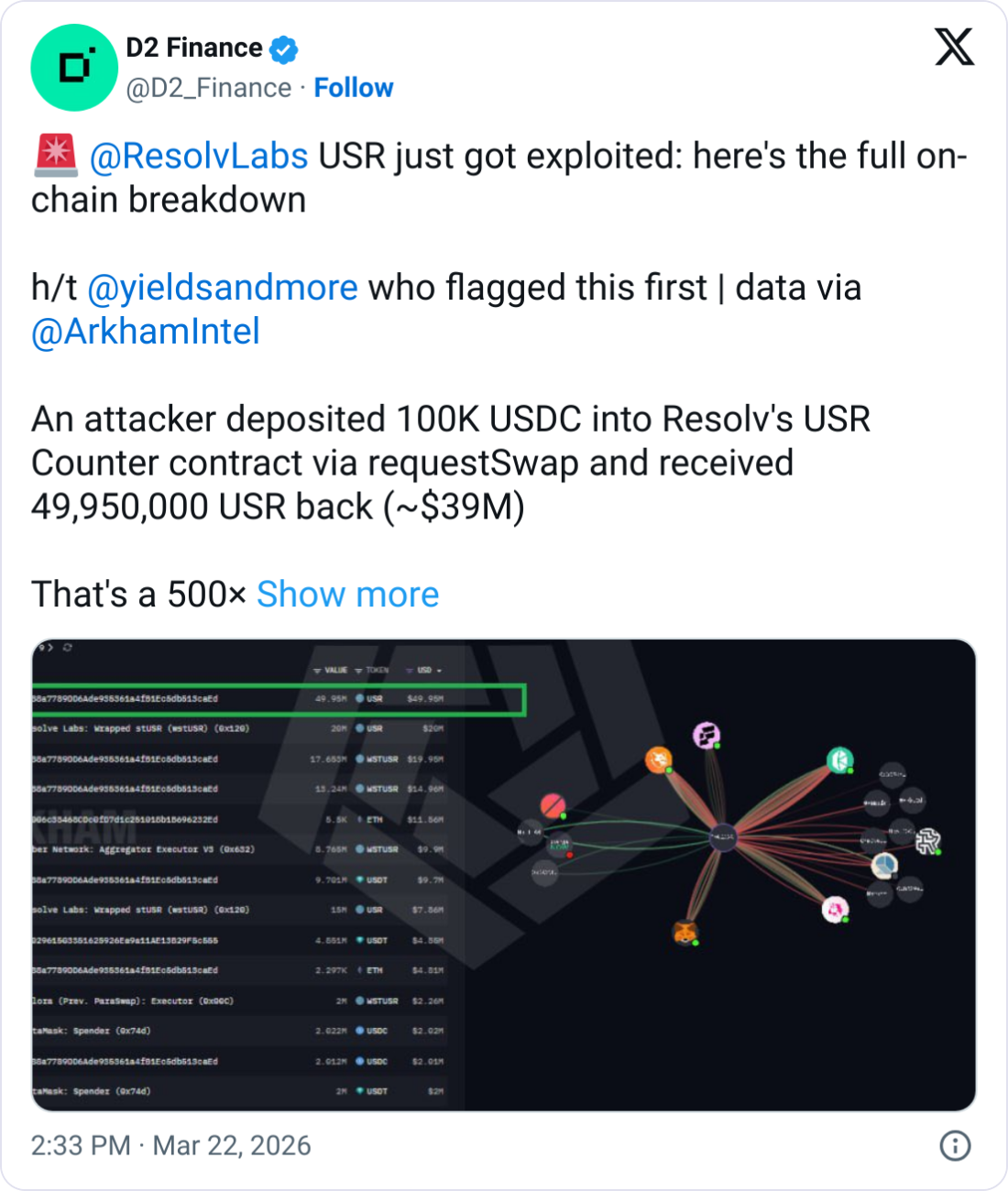

A stablecoin tied to the crypto project Resolv Labs has lost its peg to the US dollar after an attacker was able to exploit the token’s contract to create millions of tokens for themselves.

Resolv Labs posted to X on Sunday that it had experienced an exploit that allowed an attacker to mint 50 million unbacked Resolv USR (USR). “The team has currently paused all the protocol functions to prevent further malicious actions and is actively working on recovery,” it added.

The X account “yieldsandmore” had posted to the platform earlier on Sunday that USR had crashed after on-chain data showed an attacker was able to mint 50 million USR by depositing $100,000 worth of the stablecoin USDC (USDC).

The attacker was also able to mint an additional 30 million USR tokens, according to the crypto security company PeckShield.

The crypto fund D2 Finance said that the minting function on USR’s contract was somehow broken. “Either the oracle was gamed, the off-chain signer was compromised, or the amount validation between request and completion is simply missing,” it added.

The exploit comes after crypto-related hacks declined sharply in February, with $49 million lost to exploits over the month, compared to $385 million in January, with attackers increasingly preferring phishing scams over protocol exploits.

Attacker cashing out “at full speed” depegs USR

D2 Finance said the attacker quickly moved the 50 million USR they minted to multiple crypto protocols, swapping the tokens for the stablecoins USDC and USDt (USDT) before “aggressively” converting them to Ether (ETH).

“The attacker’s exit playbook is textbook DeFi hack cashout running at full speed,” it said.

D2 Finance added that USR was selling as low as 50 cents on some trades as liquidity and slippage worsened across protocols, with “multiple failed transactions visible on-chain showing the urgency.”

The firm estimated that the attacker was able to extract around $25 million from the attack amid USR’s depeg.

Related: Google Threat Intel flags ‘Ghostblade’ crypto-stealing malware

USR is currently trading at around 87 cents, around 13% off from the $1 peg the token aims to maintain, according to CoinGecko.

The token had crashed to a low of 2.5 cents on a USR/USDC pool on the protocol Curve Finance, USR’s most liquid pool with a 24-hour volume of $3.6 million, per DEX Screener.

USR hit its bottom on Curve at 2:38 am UTC on Sunday, just 17 minutes after the attacker minted $50 million worth of the token. The pool has since recovered to trade at 84.5 cents.

Magazine: Meet the onchain crypto detectives fighting crime better than the cops

A Nevada judge has halted Kalshi from operating in the state for now, ruling that the company’s prediction-market contracts could violate Nevada gambling laws by serving as unlicensed sports pools. The temporary restraining order (TRO) lasts 14 days and follows a Nevada Gaming Control Board action aimed at blocking Kalshi’s activity while the case unfolds.

In issuing the TRO, Carson City District Court Judge Jason Woodbury aligned with the state regulator’s position that Kalshi’s sports, election and entertainment event contracts may require a state license. Nevada Gaming Control Board Chair Mike Dreitzer said the board’s duty is to protect the public when prediction markets “facilitate unlicensed gambling,” a point he emphasized when speaking to Reuters about the ruling.

The decision arrives the same week that a federal appeals court denied Kalshi’s emergency bid to stay a parallel federal court proceeding, effectively allowing Nevada regulators to proceed with their actions in state court. Kalshi has argued that its contracts fall under the exclusive purview of the U.S. Commodity Futures Trading Commission, a stance that has been contested in multiple state forums.

Key takeaways

- The court’s TRO blocks Kalshi from offering sports, election and entertainment-related event contracts in Nevada for 14 days, pending a preliminary injunction hearing.

- Judge Woodbury found the early record suggests such contracts could be classified as a “sports pool” under Nevada law, a category Kalshi has not been licensed to operate.

- The panel signaled skepticism toward Kalshi’s federal preemption argument, indicating that, at this stage, the balance of authority weighs against preemption in this context.

- A preliminary injunction hearing is set for April 3 to determine whether Kalshi can continue operating in Nevada while the broader dispute proceeds.

Nevada’s view and Kalshi’s legal posture

The Nevada Gaming Control Board filed suit last month, contending that Kalshi needed a state license to offer its contract-based prediction markets for sports and related events. The board’s position rests on the premise that such offerings amount to gambling activities that fall within Nevada’s licensing framework. Kalshi has argued that its products are regulated by the federal CFTC, and that federal preemption should bar state-level licensing claims in this arena.

Judge Woodbury’s ruling frames the question as a nuanced, evolving area of law. In his order, he noted that, at the moment, state and federal authorities have not reached a settled consensus on how prediction markets should be treated under preemption doctrine. He concluded that, for now, the balance of legal authority does not favor Kalshi’s preemption argument in the Nevada context.

The court’s decision places Kalshi in a tense position in a state where regulators have long maintained strict oversight of gambling-like activities. The TRO does not resolve the larger question of whether Kalshi can operate in Nevada at all; it merely freezes activity while the injunction request is litigated.

Kalshi has pursued its own legal strategy in other jurisdictions, including filings designed to preemptively challenge potential enforcement actions by various states. Separately, Kalshi’s opponents in other states have taken measures to restrict the company’s offerings; for example, a Massachusetts judge earlier banned Kalshi from offering sports event contracts, a ruling that was later lifted on appeal. The Arizona attorney general has also pursued criminal charges against Kalshi, accusing the platform of running an illegal gambling operation—a charge Kalshi’s leadership has rejected as an overstep.

As the Nevada matter advances, observers are watching how the two tracks—state licensing enforcement and federal preemption theory—will influence Kalshi’s expansion plans and the broader regulatory risk facing prediction markets in the United States.

Earlier coverage tied Kalshi’s case to similar disputes in other states and highlighted how regulators have increasingly scrutinized prediction-market operators. The appellate decision denying Kalshi’s emergency request in the federal case underscores the uphill path for operators seeking shelter behind federal preemption in a patchwork state-by-state regime.

For investors and builders in the prediction-market space, the Nevada decision reinforces the importance of understanding licensing regimes at the state level and remaining mindful of evolving federal-state tensions in the sector. The outcome of the April 3 hearing will be a key signal of where the regulatory balance currently stands and what it could mean for Kalshi’s ability to operate nationwide.

What comes next in the Kalshi saga

With the temporary pause in place, Kalshi must await the court’s ruling on the preliminary injunction. If the injunction is granted, Kalshi would face a longer halt while the broader dispute over licensing, preemption and regulatory authority is resolved. If denied, Kalshi could resume activity in Nevada under any court-specified conditions or timelines.

Beyond Nevada, the case adds to a growing calendar of state-level actions and civil actions that have tested the legality of prediction markets in the United States. The Massachusetts and Arizona developments, in particular, illustrate the divergent approaches states are taking toward enforcement and criminal risk, underscoring a landscape where operators must navigate a mosaic of rules rather than a single national framework.

As regulators weigh calls for clearer guidelines, the next months will be critical for Kalshi’s strategic planning and for market participants who rely on prediction markets for hedging and pricing diverse outcomes. The April 3 hearing will be a focal point for clarifying whether Kalshi can continue to offer its existing suites of contracts in Nevada or whether broader licensing changes will be required to operate there in the near term.

In the meantime, traders and developers should monitor not only the Nevada case but also the evolving federal-state dialogue on preemption, licensing, and the precise contours of what constitutes gambling in prediction markets. The outcome could shape the pace at which prediction markets scale in the United States and influence how regulators balance consumer protection with innovation.

Sources cited in coverage include Reuters’ reporting on the Nevada TRO and Kalshi’s ongoing legal battles, as well as prior reporting on Kalshi’s status in other states.

Reuters reporting on the Nevada TRO and regulator comments and coverage of the appeals court denial provide context for the broader regulatory arc Kalshi faces as it eyes expansion beyond Nevada.

Crypto World

Iran Threatens Gulf Water Supply as Trump’s 48-Hour Ultimatum Targets Iranian Power Grid

TLDR:

- Iran warns Gulf desalination plants will be targeted if the US strikes its national power grid.

- Kuwait, Qatar, and Bahrain rely on desalination for up to 99 percent of their daily drinking water.

- The Gulf region produces 40 percent of the world’s desalinated water across 56 vulnerable coastal plants.

- Strikes on Jubail, the world’s largest desalination complex, could cut water access across Saudi Arabia.

Gulf desalination infrastructure is at the center of a rapidly escalating standoff between the United States and Iran. President Trump issued a 48-hour ultimatum threatening to destroy Iran’s national power grid.

Iran’s Foreign Minister Araghchi and military officials responded with warnings to attack Gulf desalination plants. The mutual crisis now threatens tens of millions of civilians on both sides. Neither side can execute its threat without triggering a devastating response from the other.

Iran Warns of Strikes on Gulf Water Facilities

Iran’s Foreign Minister Araghchi and military officials issued warnings through the Tasnim news agency. They stated that any US strike on Iranian power plants would trigger immediate retaliation.

Gulf energy infrastructure and desalination facilities were named as the primary targets. The warning came after Trump’s ultimatum threatened Iranian civilian power generation.

In a widely shared post, journalist Shanaka Perera outlined the region’s deep dependence on desalinated water. He noted that Kuwait sources 90 percent of its drinking water from desalination.

Qatar relies on desalination for nearly 99 percent of its water supply. Bahrain draws 85 percent, and Saudi Arabia depends on desalination for 70 percent.

The Gulf region collectively produces 40 percent of the world’s desalinated water. Some 400 facilities operate across the region, with output concentrated in 56 large coastal plants.

These plants sit within 350 kilometres of Iranian launch positions. They are open-air industrial complexes with no military fortification.

A missile strike on the Jubail complex in Saudi Arabia could cut water to Riyadh. Jubail is the world’s largest desalination facility, supplying water to the capital.

Riyadh has no rivers or natural groundwater reserves to replace the supply. Without desalination, large-scale evacuation would become the only available option.

A Circular Threat With No Safe Exit

The 48-hour ultimatum was set to expire on March 23. If the United States strikes Iranian power plants, Iran has stated it will retaliate against Gulf desalination plants.

Gulf water supplies could collapse within days of such a strike. Millions of Gulf residents would face a water emergency with no quick solution.

Precedent for targeting water infrastructure already exists within this conflict. On March 7, strikes damaged a desalination plant on Iran’s Qeshm Island, cutting water to 30 villages.

An Iranian drone struck a Bahraini water facility the following day. Both sides have already hit water infrastructure during the current escalation.

Twenty-three nations signed the Hormuz statement calling on Iran to halt hostilities. Bahrain, the UAE, and Qatar are among the signatories of that document.

These countries depend on desalination for the majority of their daily water supply. Iran responded to the statement by naming their water infrastructure as a retaliatory target.

The threat pattern creates a cycle of destruction with no clear endpoint. Iranian hospitals could lose power while Gulf hospitals simultaneously lose water access.

Both scenarios would produce mass civilian harm within days of any exchange. Water, not oil, has become the resource that transforms this conflict into a humanitarian emergency.

TLDR:

- Resolv Labs’ USR minting contract was exploited, allowing 50M USR to be minted with only 100K USDC in a 500x flaw.

- USR dropped 74.2% to $0.257 before partially recovering to $0.85, leaving liquidity providers with heavy losses.

- PeckShield confirmed $80M worth of USR was minted, with over $4.55M already converted into approximately 9,100 ETH.

- Resolv Labs had not issued any official response as the DeFi community called for stronger minting contract audits.

Resolv Labs’ USR stablecoin faced a suspected exploit on Sunday around 2:21 AM UTC. An attacker reportedly minted 50 million USR using only about 100,000 USDC.

This caused USR to lose 74.2% of its value, dropping to $0.257. The token later recovered to approximately $0.85. Blockchain security firm PeckShield confirmed that roughly $80 million worth of USR was minted during the attack. Resolv Labs had not responded publicly as of the time of reporting.

Attacker Exploits Minting Contract to Drain Liquidity

The attack was carried out through the USR Counter contract. The attacker executed two swaps to mint approximately 80 million USR tokens.

This was done using only around $200,000 in total funding. Experts suspect a flaw in the minting logic or a compromised signer was responsible.

After minting the tokens, the attacker then dumped them across decentralized exchanges. KyberSwap and Velora were among the platforms used for the selloff.

Through those sales, the attacker collected over $17 million in USDC and USDT. Those proceeds were then swapped into approximately 9,100 ETH.

Crypto analyst @ai_9684xtpa flagged the incident on social media shortly after. The post noted that 100,000 USDC produced 50 million USR, a 500-times discrepancy.

The Resolv team had yet to respond at the time. That ratio pointed to a serious breakdown in the protocol’s minting mechanism.

Liquidity providers suffered heavy losses from the sudden price collapse. Warnings were also issued for related vaults connected to the protocol.

USR is a yield-bearing stablecoin backed by crypto money markets. Before the incident, the protocol held over $500 million in total value locked.

Market Response and Community Reaction

USR’s price fell sharply following the exploit. From its near-$1.00 peg, the token dropped to $0.257 within a short time. It then recovered to trade between $0.85 and $0.86. However, the recovery remained partial and did not restore the full peg.

PeckShield reported that about $80 million worth of USR had been minted through the attack. The attacker had also converted funds into roughly $4.55 million worth of ETH by early reports.

Blockchain trackers continued monitoring the associated wallet activity throughout. The pace of fund conversion pointed to a coordinated and deliberate effort.

As of the time of writing, Resolv Labs had not issued any official statement. Users were watching closely for potential refunds or an emergency protocol response.

The DeFi community raised questions about the minting contract’s audit history. Past incidents of a similar nature have triggered protocol shutdowns and governance votes.

USR’s exploit adds to a growing list of stablecoin-related security failures across DeFi. Protocols carrying large total value locked have repeatedly drawn targeting from bad actors.

The community continued calling for stronger safeguards around minting contracts. Real-time monitoring and thorough audits remain critical priorities for user protection.

Crypto World

BONKfun Recovers from Domain Hijacking Attack, Promises 110% Reimbursement to Affected Users

TLDR:

- BONKfun’s domain was hijacked via social engineering on March 11, targeting its domain registrar directly.

- The attack deployed a wallet drainer, causing approximately $30,000 in total user losses over one week.

- The domain was fully recovered on March 18, with the platform securely relaunching on March 19.

- BONKfun will reimburse all affected users at 110% of their losses to cover opportunity costs incurred.

BONKfun, the Solana-based memecoin launchpad, is back online following a domain hijacking incident on March 11. Attackers used social engineering to target the platform’s domain registrar, gaining unauthorized access and deploying a wallet drainer.

The breach remained external to BONKfun’s internal systems throughout. Over roughly one week, users suffered approximately $30,000 in losses.

The team has since recovered the domain and relaunched the site, pledging to reimburse all affected users at 110% of their losses.

How the Social Engineering Attack Unfolded

The breach began when a malicious actor manipulated BONKfun’s domain service provider through social engineering.

This allowed the attacker to transfer the domain to an external registrar without authorization. The move effectively cut the team off from quick recovery options. It also enabled the deployment of a wallet drainer on the hijacked site.

Once the team identified the breach, they moved quickly to disable the site entirely. They coordinated with major wallet providers, including Phantom, Solflare, and MetaMask, to flag the domain as malicious.

Security organization @_SEAL_Org also assisted in spreading awareness rapidly. These combined efforts helped contain further damage to users.

BONKfun confirmed the incident did not compromise its internal systems, codebase, or team accounts. The domain service provider accepted responsibility for the unauthorized transfer.

This acknowledgment helped clarify where the vulnerability originated. It also reassured users that the platform’s core infrastructure remained intact.

The team released a detailed post on X, stating that the domain transfer “greatly inhibited” their ability to relaunch quickly and securely.

The statement outlined each step taken to address the breach. It also confirmed that security partners played a key role in early containment. Transparency remained central to the team’s communication throughout the incident.

Recovery Process and User Reimbursement Plan

The domain and its registration were fully transferred back around 5:00 PM Eastern Time on March 18. Full wallet provider functionality was then restored late on March 19.

This allowed BONKfun to safely relaunch the site with security measures in place. The recovery took approximately one week from the date of the initial attack.

Following the relaunch, several antivirus software providers continued to flag the main BONKfun domain. As a result, the team activated an alternative URL, letsBONK.fun, for affected users.

Both sites carry the same full functionality as the primary platform. The team is actively working to remove the remaining antivirus flags.

To address user losses, BONKfun announced a reimbursement plan at 110% of confirmed losses. The additional 10% accounts for opportunity costs incurred during the downtime period.

Total estimated losses across all affected users stand at approximately $30,000. This approach reflects the team’s commitment to accountability after the attack.

The incident serves as a reminder that social engineering remains a persistent threat in the crypto space. Domain registrar-level attacks can bypass even the most secure internal systems.

Platforms in decentralized finance must maintain strong communication with their infrastructure providers. BONKfun’s response offers a clear example of structured and transparent crisis management.

The U.S. Commodity Futures Trading Commission (CFTC) has sharpened its stance on using crypto as collateral in derivatives markets, releasing updated guidance that clarifies how crypto assets can be deployed within a pilot program launched last year. A Friday notice from the agency’s Market Participants Division and Division of Clearing and Risk responds to FAQs that emerged from December staff letters and lays out the operational and risk parameters for futures commission merchants (FCMs) participating in the pilot.

In its notice, the CFTC reminded FCMs that to participate they must file a formal notice with the Market Participants Division, including the date on which they will begin accepting crypto assets from customers as margin collateral. The guidance aims to harmonize crypto collateral practices with a broader regulatory framework being developed in coordination with the Securities and Exchange Commission (SEC), as the two agencies outline a more unified approach to crypto oversight.

Key takeaways

- Capital charges for crypto collateral align with SEC oversight: 20% for Bitcoin and Ether positions, and 2% for stablecoins used as collateral.

- Initial three-month window restricts eligible collateral to Bitcoin, Ether, or stablecoins, with weekly reporting requirements and a prompt notice for significant cybersecurity or system issues.

- After three months, other crypto assets may be accepted as collateral, subject to ongoing risk and reporting standards.

- Residual interest in customer segregated accounts may be funded only with proprietary payment stablecoins; other tokens cannot be used for that purpose.

Operational guardrails and the three-month sprint

The notice makes clear that the pilot is designed with risk controls in mind. Futures commission merchants who wish to participate must submit a formal participation notice that includes the anticipated start date for accepting crypto as margin collateral. The three-month initial phase places strict limits on the types of crypto eligible for collateral, restricting it to Bitcoin, Ether, and stablecoins. During this period, FCMs are also required to file weekly reports detailing the total crypto holdings across customer account types and to promptly report any material cybersecurity or system issues.

The three-month horizon serves a dual purpose. It allows the CFTC to observe how crypto collateral behaves in real-time market conditions under a controlled regime, while enabling market participants to build processes around risk management, custody, valuation, and operational controls. After the initial period, the rulebook opens the door to additional digital assets, expanding the universe of potential collateral as regulators gain confidence in the framework.

What changes for market participants and tokenized markets

Beyond the three-month mark, the pilot could permit a broader spectrum of crypto assets to be used as collateral, provided they meet the CFTC’s risk, custody, and governance standards. The notice also clarifies several nuanced points about where crypto and stablecoins can—and cannot—serve as collateral. Notably, crypto and stablecoins cannot be used as collateral for uncleared swaps. However, swap dealers may deploy tokenized versions of eligible assets for collateral if they satisfy regulatory requirements and preserve the same rights those assets confer in their traditional form.

Derivatives clearing organizations (DCOs) have their own set of allowances. They may accept crypto and stablecoins as initial margin for cleared transactions, again contingent on meeting CFTC standards related to minimal credit, market, and liquidity risks. Finally, as to residual interest in customer accounts, the guidance specifies that only proprietary payment stablecoins may be deposited for that purpose, excluding other cryptocurrencies from this particular use case.

In framing these rules, the CFTC underscored its intent to align its approach with the SEC’s ongoing crypto framework. The agency’s notice notes that capital charges for crypto collateral will be consistent with SEC practices, signaling a coordinated path rather than a patchwork of standalone rules. The collaboration between the agencies is part of a broader effort to create a stable, transparent regulatory environment that can accommodate the 24/7 nature of crypto markets while enforcing prudent risk controls.

Participants will be watching closely how this evolves in practice. The pilot’s design—beginning with widely traded assets like BTC, ETH, and stablecoins—reflects a cautious, first-step approach to integrating digital assets into traditional margin concepts. It also signals how regulators intend to balance the benefits of crypto-native features, such as rapid settlement and continuous trading, with the need to manage financial risk and ensure market integrity.

For traders, funds managers, and infrastructure providers, the framework offers clarity on how crypto collateral might be used in the near term. It also highlights the kinds of operational capabilities that firms must develop: robust custody solutions, reliable valuation methodologies for volatile assets, strong cybersecurity postures, and precise reporting protocols to monitor crypto holdings in customer accounts.

Industry participants will also be watching for details on how tokenized assets and stablecoins will fare under the evolving rules. Tokenization can, in theory, unlock more flexible collateral options, but it requires careful attention to governance, settlement finality, and legal rights. The CFTC’s emphasis on risk controls, alongside explicit limitations on residual interest and uncleared swaps, suggests a measured approach to expanding collateral acceptance while preserving market safety nets.

Overall, the guidance reinforces a midterm view: a calibrated expansion of crypto collateral capabilities that can gradually broaden the collateral toolkit for U.S. derivatives markets, anchored by risk-management discipline and regulatory alignment with the SEC.

Investors and market participants should monitor how this pilot progresses in the coming months, including any updates to asset eligibility, reporting requirements, or capital-charge methodologies. The three-month checkpoint will likely spur conversations about whether additional assets should qualify, how valuation and custody standards will be harmonized, and what that means for liquidity and funding costs in crypto-backed trading strategies.

As regulators continue to shape the playbook, the core question remains: can a robust, well-regulated framework unlock crypto collateral’s potential while preserving financial stability? The CFTC’s latest notice positions the industry at a pivotal juncture, where clarity and risk controls could unlock broader adoption in the years ahead.

For now, market participants should prepare for continued regulatory alignment with the SEC, stay alert to any shifts in asset eligibility, and ensure their internal controls and reporting capabilities meet the forthcoming standards if they plan to participate in the pilot.

How to watch Arsenal vs Man City for FREE: TV channel and live stream for Carabao Cup final today

CEF Market Weekly Review: CLOpocalypse Continues

Will There Be A New Season Of Peaky Blinders After The Immortal Man?

-

Tech6 days ago

Tech6 days agoYour Legally Registered ‘Motorcycle’ Might Not Count Under Proposed US Law

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Adidas – Corporette.com

-

Politics1 day ago

Politics1 day agoJenni Murray, Long-Serving Woman’s Hour Presenter, Dies Aged 75

-

Tech5 days ago

Tech5 days agoAre Split Spacebars the Next Big Gaming Keyboard Trend?

-

Crypto World8 hours ago

Crypto World8 hours agoBest Crypto to Buy Now: Strategy Just Spent $1.57 Billion on Bitcoin During Fear While Early Investors Quietly Enter Pepeto for 150x Potential

-

Crypto World9 hours ago

Crypto World9 hours agoBitcoin Price News: Bhutan Sells $72 Million in BTC Under Fiscal Pressure, but the Smart Money Entering Pepeto Sees What the Market Does Not

-

News Videos4 days ago

News Videos4 days agoRBA board divided on rate cut, unusually buoyant share market | Finance Report | ABC NEWS

-

Business6 days ago

Business6 days agoSearch for Savannah Guthrie’s Mother Enters Seventh Week with No Arrests

-

Crypto World1 day ago

Crypto World1 day agoNIO (NIO) Stock Plunges 6.5% as Shelf Registration Sparks Dilution Worries

-

Business6 days ago

Business6 days agoAustralian shares drop as Iran war enters third week

-

Politics4 days ago

Politics4 days agoThe House | The new register to protect children from their abusers shows Parliament at its best

-

Crypto World6 days ago

Crypto World6 days agoCrypto Lender BlockFills Enters Chapter 11 with Up to $500M in Liabilities

-

Fashion6 days ago

Fashion6 days ago25 Celebrities with Curly Hair That Are Naturally Beautiful

-

Tech2 days ago

Tech2 days agoinKONBINI Lets You Spend Summer Days Behind the Register

-

Crypto World4 days ago

Crypto World4 days agoCanada’s FINTRAC revokes registrations of 23 crypto MSBs in AML crackdown

-

Politics5 days ago

Politics5 days agoReal-time pollution monitoring calls after boy nearly dies

-

NewsBeat3 days ago

NewsBeat3 days agoResidents in North Lanarkshire reminded to register to vote in Scottish Parliament Election

-

Business6 days ago

Business6 days agoMeta planning major layoffs as AI spending and automation reshape workforce

-

News Videos4 days ago

News Videos4 days agoPARLIAMENT OF MALAWI – PAC MEETING WITH REGISTRAR OF FINANCIAL ON AMARYLLIS HOTEL – INQUIRY LIVE

-

Politics7 days ago

Politics7 days ago9 Stylish Leather Jackets Perfect For Spring 2026

You must be logged in to post a comment Login