Crypto World

Pepe Price Prediction – Best Meme Coin to Buy During Crypto Market Crash?

Join Our Telegram channel to stay up to date on breaking news coverage

Pepe (PEPE) trades over 3% lower today as short-term pressure hits amid a broader cryptocurrency market downturn.

Despite the decline, current conditions may represent a strategic accumulation phase, making Pepe a potential candidate for the best meme coin to buy, as it had been building notable momentum earlier this month before market-wide volatility interrupted the trend.

The recent pause in upside movement was largely driven by Bitcoin’s sharp drop to the $75,000 level within the past 24 hours. That move triggered widespread fear and selling across the crypto market, impacting both altcoins and meme coins.

However, such volatility has historically preceded strong recoveries, and this environment may be constructive rather than bearish for select assets.

Pepe Price Prediction

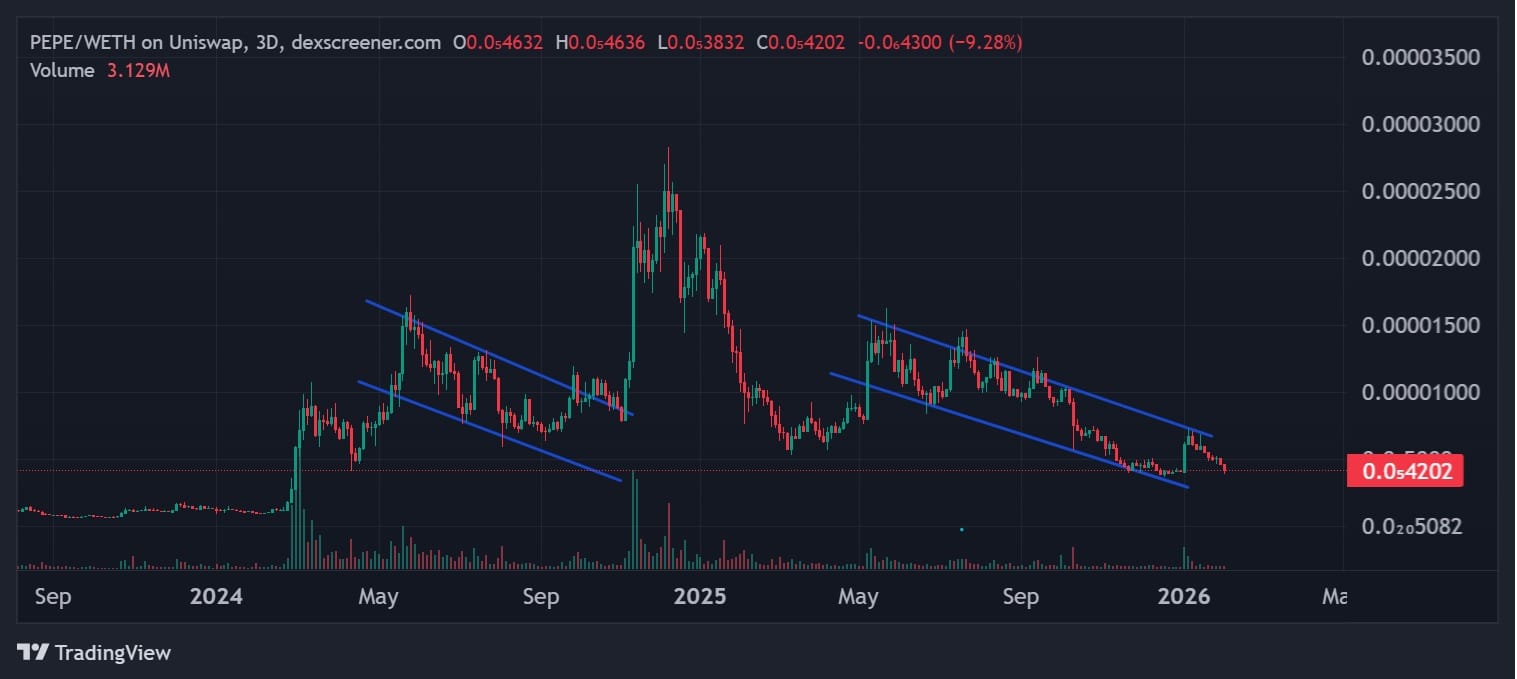

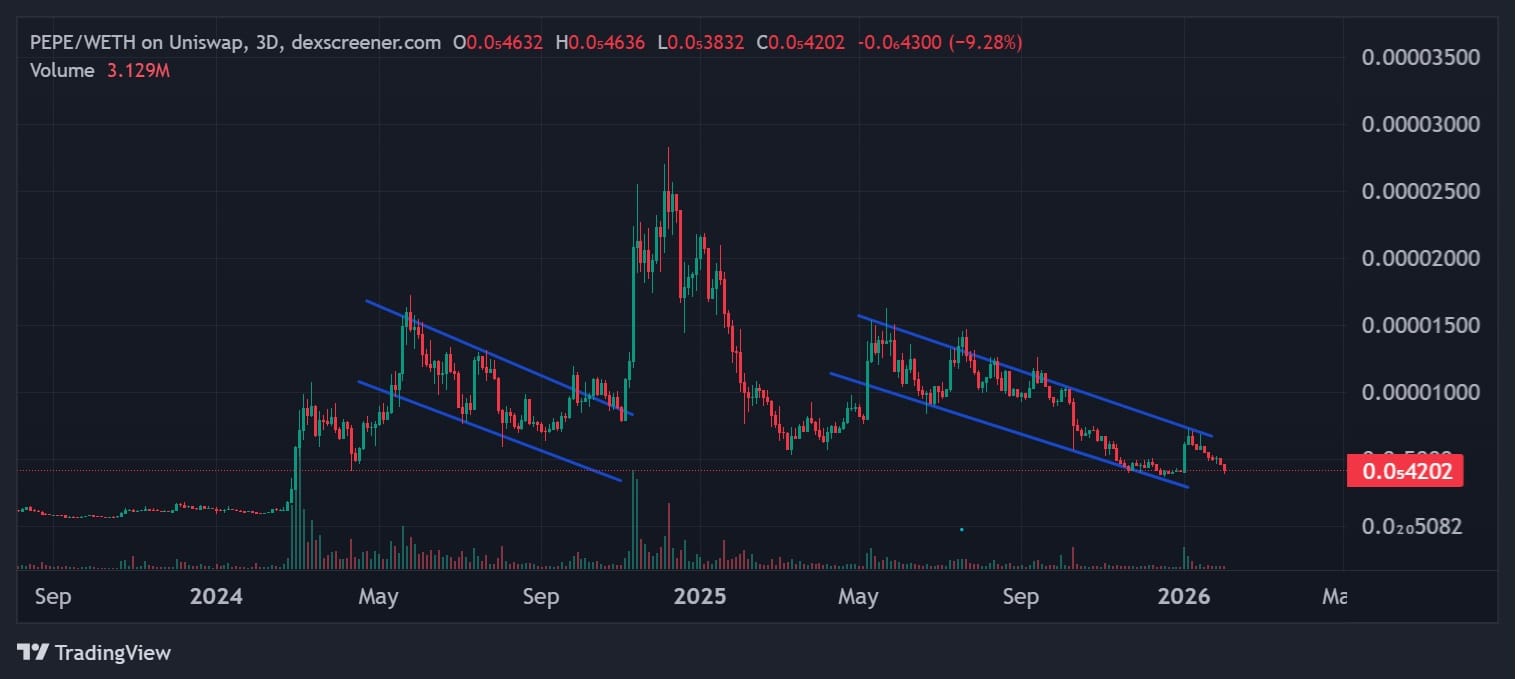

On the 24-hour timeframe, PEPE briefly dipped into negative territory before attempting a modest rebound and now hovers near neutral levels. While short-term performance looks weak, with the token down roughly 8% on the week, the broader trend points toward recovery.

PEPE remains up more than 13% over the past month, highlighting resilience after a difficult 2025, and the daily chart shows the asset trading inside a long-term descending channel that reflects extended consolidation rather than structural weakness.

Price action stays compressed between parallel trendlines, and the tightening range indicates that selling pressure continues to ease, setting the stage for a potential trend shift.

A decisive breakout above the upper boundary of this channel would signal a major reversal, with upside targets near the prior resistance zone around 0.00001936, while until that move occurs, current conditions favor accumulation over a confirmed bullish continuation.

Despite this compression, PEPE maintains a strong market position, ranking as the third-largest meme coin by market capitalization and the fourth most visited asset in the category, even as newer competitors enter the space.

This dynamic has fueled speculation that PEPE’s “pure” meme identity could eventually challenge Shiba Inu’s dominance as the community-driven favorite.

Momentum indicators suggest the move higher remains in its early stages, laying a solid foundation for upside as broader market conditions improve.

For a deeper look at PEPE’s outlook in 2026, the 99Bitcoins YouTube Channel has released a dedicated update that explores the emerging “meme supercycle.”

Their analysts argue that PEPE’s lack of complex utility may work to its advantage, giving it an edge over ecosystem-heavy meme coins like Shiba Inu as market sentiment shifts.

Why This Meme Coin Could Be the Next PEPE Coin

As sentiment shifts toward high-upside assets, many investors are pivoting toward Bitcoin Hyper (HYPER), which many view as the best meme coin to buy for a blend of viral appeal and high-performance utility.

Bitcoin Hyper (HYPER) is emerging as a best altcoin to watch in 2026. The project has already raised around $31 million, and $HYPER currently trades at $0.013665.

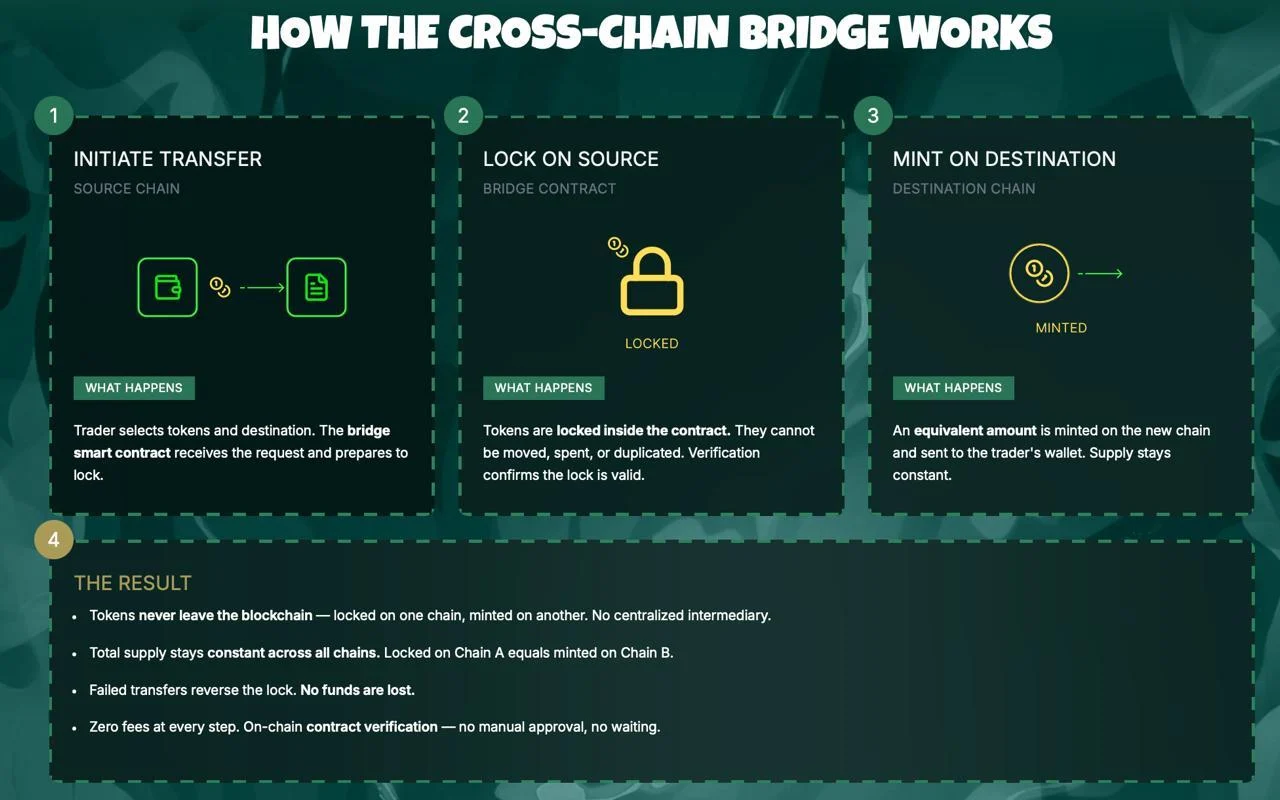

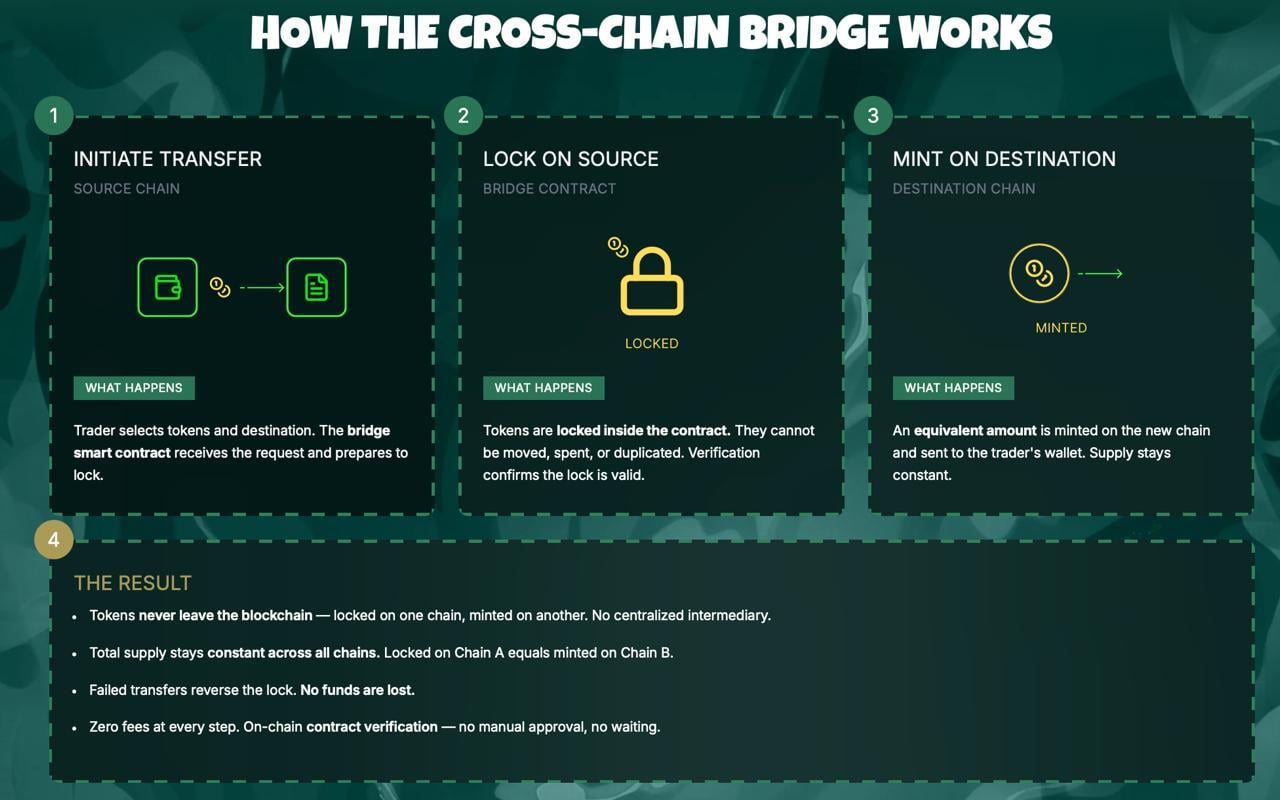

Bitcoin Hyper runs on a Layer 2 network that fixes Bitcoin’s biggest problems. Transactions confirm in seconds and cost only a tiny fraction of a cent while staying secured by Bitcoin’s Proof-of-Work system.

When users make a transaction, the system locks BTC on the main Bitcoin network and mirrors it on the Layer 2 network using secure cryptographic checks. This lets users skip the long wait for confirmations and enjoy near-instant transactions. Fast transfers open up new options such as staking, decentralized swaps, and lending.

Low-cost, quick settlements also make everyday payments practical without overloading Bitcoin’s main network. The network bundles transactions and settles them back on Bitcoin at regular intervals.

$HYPER boosts speed by using the Solana Virtual Machine, which combines high performance with Bitcoin’s security. This setup allows high-volume activity and smart contracts, two features that could help Bitcoin stay competitive in 2026.

Analysts call $HYPER one of the best cryptos to buy. Many investors already stake their tokens to earn up to 38% APY while the presale is live. Wider real-world use of Bitcoin could drive the next bull run, and $HYPER might play a key role. Early investors may wish they got in sooner.

You can buy $HYPER on the Bitcoin Hyper website or follow this guide to learn how.

Related News

- Get Educational Courses & Tutorials

- Free Content & VIP Group

- Jacob Crypto Bury Market Analysis Videos

- Leverage Trading Signals on Bybit

- Next 10x Altcoin Gems

- Upcoming Presales & ICOs

Join Our Telegram channel to stay up to date on breaking news coverage

Binance co-founder Changpeng ‘CZ’ Zhao believes blockchain and cryptocurrency are on a path to becoming as common and unnoticed as the internet within the next five years.

Summary

- Binance co-founder Changpeng Zhao expects blockchain to become an invisible part of daily life by 2031 and compares its future integration to how the world uses the internet today.

- Zhao warns that nations failing to adopt blockchain and AI will face significant economic disadvantages.

Speaking on Scott Melker’s Wolf of All Streets podcast on Thursday, Zhao explained that the goal for the industry is to reach a stage where the underlying technology is no longer the main topic of conversation.

He compared the current phase of crypto to the early days of the web, suggesting that the technical jargon will eventually fade into the background.

“I’m hoping that we don’t talk about crypto as crypto in five years, just like we don’t talk about the internet anymore, we don’t talk about TCP/IP, we don’t talk about HTML, JavaScript, etc. We don’t talk about that stuff anymore. We just use it,” Zhao said.

The drive toward mainstream use is backed by recent data and industry forecasts. Figures from DemandSage show that global crypto users have reached an estimated 559 million in 2026.

Financial institutions are also preparing for this transition; a Citi survey from last September revealed that most banks and asset managers expect tokenized securities and stablecoins to handle 10% of global post-trade market turnover in less than five years.

Looking further ahead, ARK Invest recently projected that the digital asset market could reach $28 trillion by 2030. Other industry leaders, such as Tether co-founder Reeve Collins, expect nearly all traditional currencies to eventually transition into stablecoins.

Chainalysis has shared an even more aggressive outlook, estimating that stablecoin volumes could reach $1.5 quadrillion by 2035.

The role of AI and global competition

Zhao noted that the rise of artificial intelligence is likely to pull blockchain adoption along with it, particularly as AI agents begin to handle financial transactions. He suggested that the combination of these technologies is now essential for national competitiveness.

“I think there’s really three big industries in my adult lifetime: the internet, blockchain and AI. Any country that misses one of them is going to be severely disadvantaged,” he said.

While Microsoft recently identified the United States as the leader in AI infrastructure, other nations are moving faster in specific areas of adoption.

Signzy and Arkham have both highlighted Switzerland as a top hub for crypto innovation, while the United Arab Emirates has outpaced the U.S. in the actual day-to-day usage of new digital tools.

To keep pace, Zhao previously advised AI developers to focus on the practical utility of their tools rather than simply launching new tokens to raise money.

Crypto World

Could Pepeto Deliver the Best Crypto Presale to Buy as ETH and ARB Recover on Ceasefire News

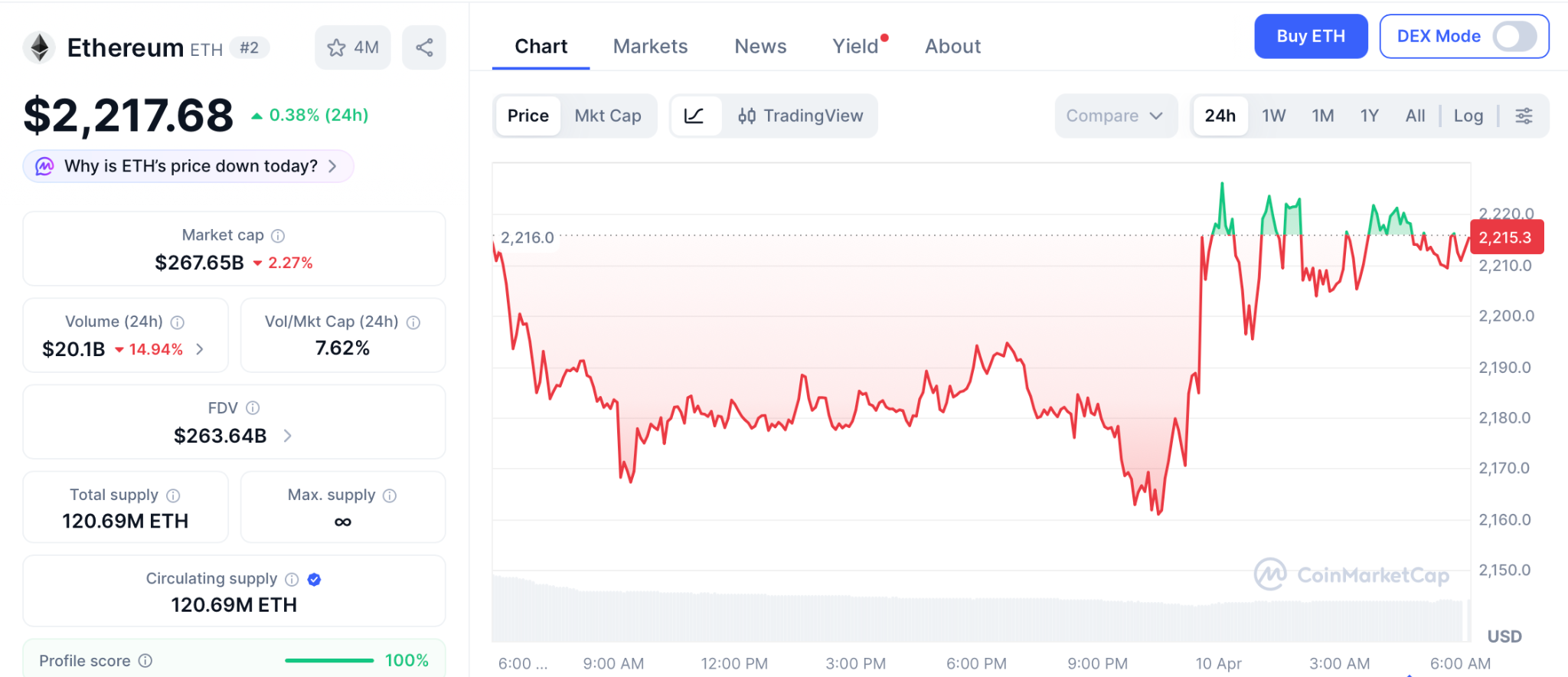

A two week ceasefire between the U.S. and Iran just triggered $427 million in short liquidations, sending BTC back above $72,000 and ETH past $2,200 in a single session. Wallets positioned before the news printed gains overnight that took months of patience to build.

While the rally lifts large caps, Pepeto has crossed $8.87 million in presale capital while a Binance listing draws closer, making it what analysts call the best crypto presale to buy before the next wave of capital arrives.

The U.S. and Iran agreed to a two week ceasefire that includes reopening the Strait of Hormuz and suspending strikes, according to Yahoo Finance.

BTC jumped 4.5% to $71,926 and ETH climbed 6.3% to $2,239 within hours. The rally erased weeks of fear driven selling and pushed total crypto market cap above $2.4 trillion according to CoinMarketCap. Short sellers lost $427 million in forced closures overnight.

How ETH, ARB, and Pepeto Stack Up After the Ceasefire Rally

Pepeto: Swap Tools and Pepe Legacy Creating the Entry Analysts Keep Flagging

Every cycle has a moment where one presale pulls capital while the rest of the market bleeds, and this time the signal is hard to miss. One name drawing serious money through the noise is Pepeto, a presale built for real returns rather than temporary hype, which is why analysts keep naming it the best crypto presale to buy this cycle.

The ecosystem rewards holders on multiple levels. Staking at 186% APY gives early wallets growing returns that compound ahead of the listing. The 420 trillion token supply keeps active traders and committed holders in balance.

The exchange system already runs and processes live trades. PepetoSwap handles token swaps across chains at zero cost, so holders protect the full size of every position. The risk scorer reviews each contract before a trade completes, catching red flags that cost unprepared wallets their capital every day.

Capital kept coming even when the Fear and Greed Index touched single digits, pushing total presale past $8.87 million. Pepeto at $0.0000001863 trades at a fraction of what listing projections show, and the distance between that entry and where trading opens is where wealth gets created for wallets that commit while the number exists.

The presale locks out permanently when the Binance listing opens, and the current entry goes away forever. Market watchers target 100x or more, pointing to the cofounder’s history of building the original Pepe coin to billions without a single working product. Stages keep selling out ahead of schedule, and the wallets still searching are watching the entry they wanted get smaller with every hour that passes.

Ethereum: ETH Climbs on Ceasefire but Faces Familiar Ceiling

ETH trades near $2,217 according to CoinMarketCap after jumping 6.3% on the ceasefire. BlackRock’s staked ETH fund saw $15.5 million in first day volume.

Support holds at $2,000 with resistance near $2,400. Even reaching $5,000, the August 2025 all time high, delivers roughly 120% from here, strong for a large cap but far from what the best crypto presale to buy can produce in the same window.

Arbitrum: ARB Sits 96% Below Its Peak With Unlock Pressure Ahead

ARB trades near $0.10 according to CoinMarketCap, sitting 96% below its all time high of $2.40. An $8.72 million token unlock arrives April 16, releasing 92.65 million tokens that add selling pressure.

Monthly unlocks keep dragging the price lower even as the Layer 2 network processes real DeFi volume. A recovery to $0.20 only doubles capital while dilution risk remains for holders waiting for the unlock schedule to end.

Conclusion:

The best crypto presale to buy becomes clearest when a rally reminds everyone that crypto rewards wallets already inside. ETH and ARB recovered on the ceasefire, but their ceilings pale against what presale entries produce when a listing arrives. Pepeto combines swap tools and contract protection with pricing that reshapes a portfolio after one event.

Pepe exploded from presale price and those early wallets collected life changing returns, and the same pattern is forming around Pepeto before the crowd confirms it. Capital flowing through Pepeto proves the signal is loud, and the presale price disappears permanently when the Binance listing opens. Every hour the presale stays open is an hour closer to the listing that turns this into the best crypto presale to buy someone else got instead of you.

Click To Visit Pepeto Website To Enter The Presale

FAQs

What makes Pepeto the best crypto presale to buy right now?

Pepeto runs live swap tools with zero fees, a Pepe cofounder leads the project, and a confirmed Binance listing sits days away at $0.0000001863 entry. The presale pulled $8.87 million during extreme market fear.

Did the ceasefire rally change the crypto outlook?

The ceasefire triggered $427 million in short liquidations and sent BTC above $72,000 in hours. Fresh capital entering the market benefits presale entries like Pepeto that are priced before exchange listing.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

Solana price has rebounded back above $85 on Friday morning, retracing back some of its losses following Wednesday’s rally. However, it still remains below a key SMA level that puts it at risk of moving to its next leg lower over the coming sessions.

Summary

- Solana price rebounds above $85 but remains below the key 50-day SMA, keeping downside risk intact.

- Repeating a three-step pattern signals consolidation phase may precede another sell-off.

- Failure to reclaim the $86 level could trigger a sharp decline toward $52.

According to data from crypto.news, Solana (SOL) price rose 4.5% to an intraday high of $85.2 before stabilizing around $83 at the time of writing. The rebound following a market-wide recovery as Bitcoin moved above $73,000 helped the altcoin to backpedal on some of its losses experienced since dropping from its Wednesday high.

Despite the token’s recent rebound, it remains at risk of a more downside in the coming weeks, as it has failed to reclaim a key SMA level, failure of which has historically led to strong downsides.

The daily chart shows that Solana price has been trading within the $76 to $92 range since February this year. The token recently moved into the lower end of this range in the past two weeks.

In doing so, Solana price has fallen below the 50-day SMA, which has historically been followed by significant bearish pressure since October 2023.

Notably, Solana price movement has been repeating a three-step cycle every time it prepares to transition to its next leg lower in the past six months.

The said pattern begins when Solana price reclaims the 50-day SMA, which is then followed by a rapid fall back below the indicator while losing the support of previous highs. Following this, the token enters into a consolidation trap, a period when the token moves sideways within a tight range before its final breakdown towards its next leg down begins.

As derived from the daily chart above, Solana price previously formed this pattern in November last year and again at the beginning of January this year, each time it fell below the 50-day SMA and subsequently entered a consolidation phase for weeks. Following this, it faced a strong sell-off, finally settling lower and forming a new local bottom.

In the most recent instance, Solana price moved above the key resistance in mid-March when it surged all the way to $97. The token has since been on a downtrend, making lower lows and lower highs in the process. Moving on to the last couple of days, the token has been stuck in its consolidation phase in the second step of the current cycle as it hovers between $79 and $81, and rests below the 50-day SMA around the $86 mark.

Assuming that the pattern holds, the ongoing sideways movement should not be interpreted as a sign of stabilization but as the token coiling before initiating its next leg down.

As such, if Solana fails to reclaim the $86 50 day SMA level in the coming sessions, it risks a rapid decline towards $52, a level calculated by subtracting the average percentage drop observed during previous cycles from the current consolidation peak.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

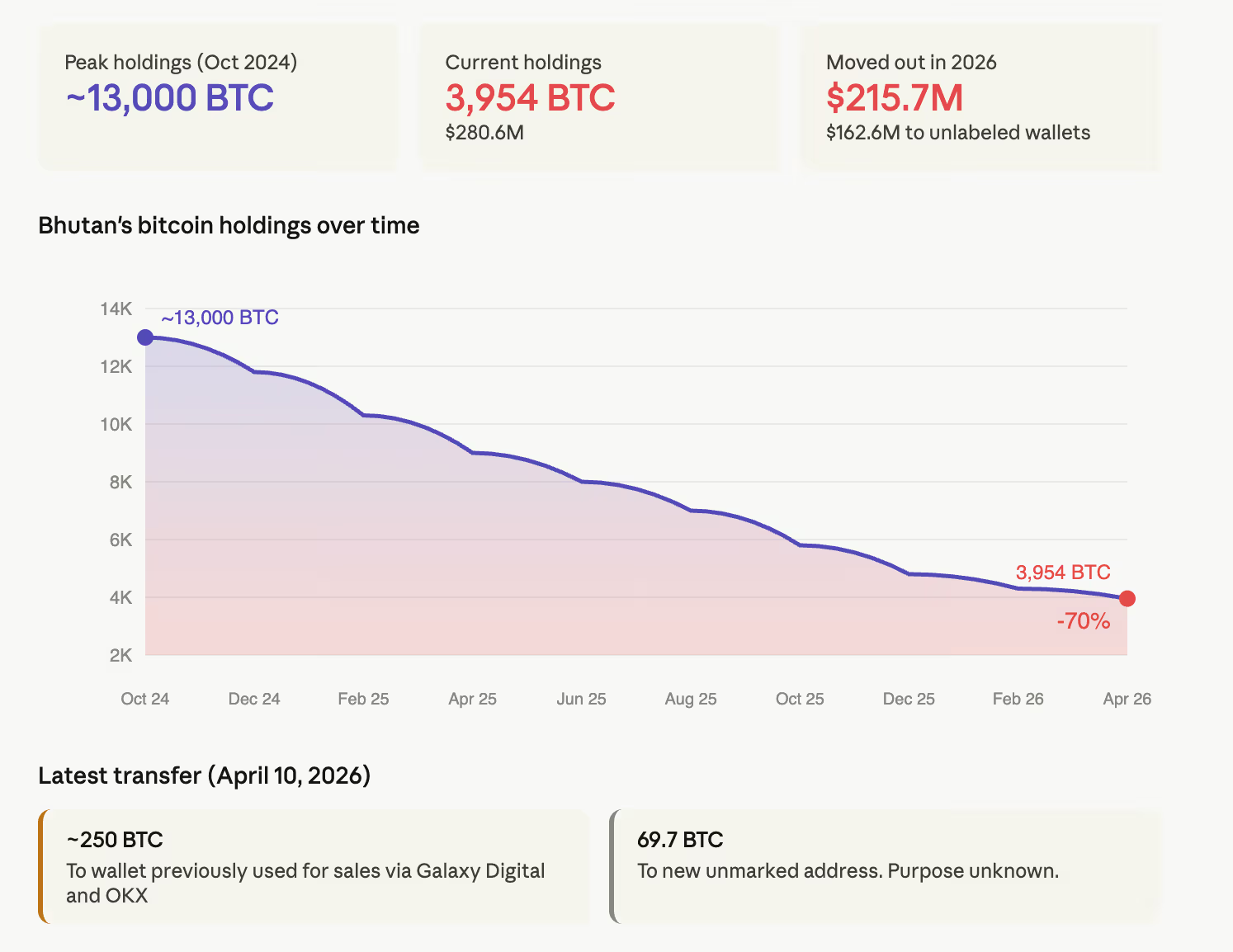

Bhutan is quietly unwinding one of the most unusual bitcoin experiments any government has ever run.

The Royal Government of Bhutan transferred roughly 319.7 BTC worth $22.68 million to two addresses on Thursday, according to Arkham Intelligence data. Roughly 250 BTC went to a wallet previously used to route funds for sale via Galaxy Digital and OKX. Another 69.7 BTC was sent to a new, unmarked address.

The transaction is part of a series of ongoing sales that have been going on for a while.

Bhutan held approximately 13,000 BTC in October 2024, accumulated through a hydropower-backed mining operation run by Druk Holding and Investments, the kingdom’s sovereign wealth fund.

That was the proof-of-concept for sovereign bitcoin mining. A tiny, landlocked country with cheap renewable energy, no legacy financial infrastructure to protect, and a sovereign wealth fund willing to experiment.

Since then, it has sold steadily. Holdings now stand at 3,954 BTC worth roughly $280.6 million, a 70% reduction in 18 months. Arkham data shows $215.7 million in bitcoin has moved out of Bhutan’s holding addresses this year alone, with $162.6 million of that going to unlabeled wallets.

The selling has accelerated into a market where virtually every other major holder is doing the opposite.

Strategy bought 4,871 BTC for $330 million last weekend, bringing its total to 766,970. U.S. spot ETFs absorbed approximately 50,000 BTC in March. The Ethereum Foundation staked $93 million of ether in a single day rather than sell. Even gold-backed sovereign funds have been adding to positions during the Iran conflict.

Bhutan is the only sovereign-level holder visibly liquidating. But there is also a question about whether the mining operation itself is still running.

Arkham data shows Bhutan’s last bitcoin inflow exceeding $100,000 was recorded over a year ago. A government that once generated bitcoin from power harnessed from its own rivers may now simply be spending down what it accumulated, with no new supply coming in to replace what it sells.

Druk Holdings has not responded to several emails and calls from CoinDesk over the past week, the latest of which was sent in the Asian morning hours on Friday. It has not publicly commented on the transfers or the status of its mining operation.

The economics may explain the shift, however.

Bhutan’s mining operation was viable when difficulty was lower, and bitcoin traded above $90,000. At current levels near $71,000, with network difficulty at all-time highs and the post-halving block reward reduced to 3.125 BTC, the margins on small-scale sovereign mining have compressed significantly.

The same hydropower that made Bhutan’s operation novel may now generate more revenue from electricity sold to neighboring India than from bitcoin mining, as mining hardware depreciates with every difficulty adjustment.

Choosing to sell rather than hold or mine is a data point about the gap between bitcoin’s narrative appeal to nation-states and the operational reality of maintaining a position through a prolonged drawdown.

Bhutan’s remaining 3,954 BTC is now smaller than what Strategy purchases in a typical week. The kingdom that once held 13,000 bitcoin mined from its own mountains is watching a single company in Virginia accumulate more in five days than Bhutan has left.

Read more: Bhutan moves another 500 bitcoin to exchanges as 2026 outflows top $150 million

HSBC and the Standard Chartered-backed Anchorpoint Financial have been granted Hong Kong’s first stablecoin issuer licenses.

Summary

- The Hong Kong Monetary Authority has granted the first stablecoin issuer licenses to HSBC and the Standard Chartered-backed venture Anchorpoint Financial.

- These initial approvals follow several months of delays after the regulator missed its original target to begin the licensing process in March.

The Hong Kong Monetary Authority (HKMA) released the names of the successful applicants on Friday, signaling the start of a new era for regulated digital assets in the region.

Among the approved firms is HSBC, a dominant local note-issuing bank, alongside Anchorpoint Financial, which operates as a joint venture between Standard Chartered, Animoca Brands, and Hong Kong Telecommunications.

Oversight and enforcement standards

These approvals establish the first group of participants under a licensing regime that officially launched on Aug. 1, 2025.

Under this regime, stablecoin issuers are required to obtain an HKMA license by meeting specific rules, including those for reserve backing and guaranteed redemption paths for users. Other obligations include following strict governance protocols and Anti-Money Laundering (AML) measures to remain in good standing.

The Legislation also grants the regulator the authority to investigate potential violations and police the sector, including the authority to levy fines, suspend operations, or revoke licenses entirely if an issuer fails to meet its legal obligations.

The rollout follows a period of administrative delays that saw the regulator miss its original goals for the year. Back in February, HKMA Chief Executive Eddie Yue stated that a “very small number of issuers” would be licensed by March.

While that deadline passed without an announcement, the regulator stated on April 1 that it was actively moving the process forward to finalize the first batch of applicants.

Analysts had largely foreseen this outcome following mid-March reports that highlighted HSBC and the Standard Chartered-backed venture as the most likely recipients of the licenses.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

AI stock trading bots gain traction in 2026 as beginners seek simple, automated ways to enter financial markets.

Summary

- AI stock trading bots gain traction in 2026, offering beginners automated, hands-free market entry

- MoneyFlare leads with one-click AI trading, combining stock and crypto automation for passive income

- Demand is rising for free AI trading tools as users seek simple, risk-managed investing solutions

As the financial markets continue to evolve, more beginners are turning to AI-powered tools to automate their stock trading. In 2026, AI stock trading bots are increasingly accessible, providing users with an easy, hands-off way to enter the market. For those who are beginners, looking to get started with AI stock trading, this guide will help them navigate the best free options available in 2026.

Whether someone is looking for a simple tool to automate their trades or seeking advanced features to fine-tune their strategies, the right AI trading bot can make all the difference. Let’s explore the top 10 free AI stock trading bots that are perfect for beginners in 2026.

What are AI stock trading bots?

AI stock trading bots are automated programs that use artificial intelligence algorithms to analyze market data, execute trades, and manage investments. These bots are designed to optimize trading strategies with minimal effort, making them perfect for beginners who want to avoid the complexity of manual trading.

In 2026, these bots offer advanced features like machine learning, sentiment analysis, and real-time market monitoring, all without requiring any coding skills. Many of these bots operate on a subscription-free basis, offering a risk-free introduction to the world of automated stock trading.

Top 10 free AI stock trading bots for beginners in 2026

1. MoneyFlare

Overview:

MoneyFlare is a sophisticated yet beginner-friendly AI trading platform that offers fully automated stock and crypto trading. Designed for individuals with no coding or technical experience, MoneyFlare leverages advanced AI algorithms to execute trades and manage investments 24/7.

Key Features:

- One-Click Activation: Start trading instantly with minimal setup.

- Pre-Built Quant Strategies: Choose from a variety of expert-crafted strategies tailored to maximize returns.

- 24/7 Automated Trading: Let the AI handle trades at any time, ensuring an opportunity is never missed.

- Risk Management Tools: Built-in stop-loss, take-profit, and exposure limits to minimize potential losses.

Best for:

Complete beginners who want a hands-off trading experience, as well as those looking for a safe, AI-driven approach to generating passive income with minimal effort.

Click to register and receive a free $10 real reward and $50 trial credit!

2. 3Commas

Overview:

3Commas offers an intuitive and flexible trading environment suitable for both beginners and advanced traders. It allows users to automate their trades using a variety of strategies, such as Dollar-Cost Averaging (DCA) and grid trading.

Key Features:

- Smart Trade Terminal: Execute trades with real-time analysis and risk management tools.

- Automated Portfolio Management: Rebalance and optimize a portfolio automatically.

- Multi-Exchange Support: Trade across multiple platforms like Binance, Kraken, and others, from one interface.

- Backtesting: Test strategies before going live.

Best for:

Beginners who want to start simple but also value the potential to scale their trading strategies as they gain experience.

3. Cryptohopper

Overview:

Cryptohopper is a cloud-based AI bot that combines automation with customization, making it ideal for both beginners and more experienced traders. Trades can ebe automated based on predefined strategies or real-time market signals.

Key Features:

- Strategy Marketplace: Choose from a wide range of pre-built strategies created by top traders.

- Social Trading: Follow expert traders and mirror their strategies in real time.

- Backtesting & Paper Trading: Test strategies risk-free before using real funds.

Best For:

Beginners looking for flexibility, with the option to gradually explore advanced features as they learn.

4. Pionex

Overview:

Pionex is an easy-to-use AI trading bot that offers over 16 different bots, including grid trading and arbitrage bots. It’s perfect for beginners who want to start automated trading without having to navigate complex features.

Key Features:

- Low Fees: One of the most cost-effective platforms, with trading fees as low as 0.05%.

- Pre-Built Strategies: Get started quickly with simple, effective strategies like grid trading and arbitrage.

- Automated Trading: Operate trades on autopilot 24/7.

Best For:

Beginners who want an all-in-one solution that simplifies automated trading with minimal setup and fees.

5. Zignaly

Overview:

Zignaly is a fully automated trading platform designed for those who want to follow expert traders or signal providers. It offers social trading and copy trading features, allowing beginners to learn from others while automating their own trades.

Key Features:

- Copy Trading: Automatically copy the strategies of top traders in real-time.

- Cloud-Based Automation: Run the bot seamlessly from the cloud without any setup hassles.

- Risk Management Tools: Protect investments with built-in risk controls.

Best For:

Beginners who prefer to follow professional traders’ strategies while automating their own trades with minimal input.

6. Autonio

Overview:

Autonio is a decentralized trading bot platform that allows users to trade across multiple assets using machine learning and AI. It’s ideal for beginners who want a hands-on approach to customizing their strategies with the power of AI.

Key Features:

- Machine Learning Algorithms: AI-powered trading that adapts to market conditions.

- Backtesting & Optimization: Test and refine strategies using historical data.

- Multi-Asset Support: Trade a variety of assets beyond just stocks and crypto.

Best For:

Beginners who want to dive deeper into customizable trading strategies while leveraging AI for decision-making.

7. HaasOnline

Overview:

HaasOnline offers a set of powerful, free trading bots that are ideal for beginners looking to explore automated trading. The platform allows full customization of trading strategies, providing more control over how trades are executed.

Key Features:

- Advanced Risk Management: Use features like stop-loss, trailing stop, and take-profit for safer trading.

- Multi-Exchange Support: Connect with several exchanges for a broader trading experience.

- Backtesting: Evaluate strategies and refine them before going live.

Best For:

Beginners who may want to start simple but gradually explore more complex features as they gain confidence.

8. Shrimpy

Overview:

Shrimpy offers a portfolio management tool with automated rebalancing and social trading. This bot is perfect for beginners who want to follow the strategies of top traders while managing their portfolios effortlessly.

Key Features:

- Portfolio Rebalancing: Keep investments aligned with goals by automating portfolio rebalancing.

- Social Trading: Copy the strategies of top traders and implement them automatically.

- Real-Time Performance Tracking: Track investments’ performance in real time.

Best For:

Beginners who want a simple and effective way to manage their portfolios with minimal effort.

9. Quadency

Overview:

Quadency is a versatile platform that offers AI-powered trading bots and an easy-to-use interface. It allows users to automate their trades and backtest strategies without needing any technical knowledge.

Key Features:

- Strategy Automation: Implement and execute various strategies with ease.

- Real-Time Data and Analytics: Make informed trading decisions based on real-time market data.

- Backtesting: Test strategies with historical data to ensure their effectiveness.

Best For:

Beginners who want a hassle-free, automated trading experience with powerful tools to track performance.

10. Bitsgap

Overview:

Bitsgap is an integrated trading platform that supports multiple exchanges and offers automated trading bots, including arbitrage and grid bots. It’s ideal for beginners looking to automate their trades across different platforms.

Key Features:

- Arbitrage Trading: Take advantage of price discrepancies across exchanges to maximize profits.

- Backtesting: Test strategies risk-free before live trading.

- Multi-Exchange Support: Trade across multiple exchanges from one platform.

Best For:

Beginners who want to explore more advanced features, such as arbitrage, without the complexity of setting up manual trades.

Why should beginners use AI stock trading bots?

For beginners, AI stock trading bots offer several advantages:

- Ease of Use: Most bots are designed to be user-friendly, with intuitive interfaces that don’t require prior trading experience.

- Automation: They run 24/7, meaning users can take advantage of market opportunities even while they sleep.

- Data-Driven Decisions: AI bots analyze vast amounts of market data, ensuring that trades are based on solid information rather than emotions.

- Risk Management: Many bots come with built-in risk management tools to protect investments.

How to get started with AI stock trading bots

Here’s a simple step-by-step guide to getting started for those who are new to AI stock trading bots:

- Choose the Right Bot: Select one of the bots listed above that suits a particular trading style and preferences.

- Set Up an Account: Most bots require users to create an account on their platform and link it to their brokerage or exchange account.

- Customize Settings: While some bots come with preset strategies, users can often adjust risk levels, trading pairs, and other parameters to suit their preferences.

- Monitor and Optimize: Once the bot is running, its performance can be monitored, and adjustments can be made if necessary. Some bots offer analytics to help track profitability.

Things to consider before using AI stock trading bots

While AI stock trading bots offer great advantages, they are not foolproof. Here are a few things to consider:

- Market Risk: The stock market can be volatile, and even AI systems can make losses in unpredictable market conditions.

- Initial Setup: Some bots may require initial configuration or a learning curve, even if they’re beginner-friendly.

- Fees: Some bots are free, but others may charge a fee for premium features. Be sure to check the cost structure before getting started.

Tips to avoid being scammed in AI stock trading

As AI stock trading becomes more popular, many investors are turning to automated trading systems to manage their investments. However, there are also fraudulent platforms and scams in the market, so it is crucial to ensure that protection comes first. Below are some effective tips to help traders avoid being scammed while using AI stock trading platforms:

1. Choose a reputable platform

Ensure a well-known platform with positive reviews is selected. Users can verify the platform’s credibility by researching user feedback, independent reviews, and whether the platform is regulated by financial authorities (such as the U.S. Securities and Exchange Commission [SEC] or the UK’s Financial Conduct Authority [FCA]). Legitimate platforms will disclose their registration information and be under the supervision of regulatory bodies, so avoid platforms with low transparency.

2. Avoid unrealistic high-return promises

Any platform that promises “guaranteed profits” or fixed high returns should raise suspicion. No investment can guarantee consistent returns, especially in the volatile stock market. Legitimate platforms typically include risk warnings in their terms of service and disclaimers, advising users of the potential for losses. Be wary of platforms that make unrealistic promises of high returns or quick profits.

3. Ensure platform security

When selecting a platform, make sure it offers strong data encryption to protect the account and funds. Legitimate platforms typically use SSL encryption protocols to secure data transmission, and they provide two-factor authentication (2FA) to enhance account security. This ensures that even if someone steals a password, they won’t be able to access the account easily. Verify that the platform follows industry-standard security measures to prevent hacking or data breaches.

4. Avoid following trading signals from unverified sources

Avoid blindly following trading signals or advice from unverified sources. Choose platforms where the signal sources are clearly identified and ensure these signals come from reputable professionals or verified traders. Social trading platforms (such as Zignaly) allow users to follow other successful traders’ strategies, but make sure these strategies are transparent and publicly available. Do not make decisions based solely on short-term profit claims.

5. Start with small investments, don’t invest all funds at once

Before fully trusting a platform, it’s best to start with small, test investments. This allows the user to assess the platform’s performance and the effectiveness of its AI strategies with minimal risk. Diversify investments to reduce risk and avoid putting all the funds into one platform or strategy.

6. Verify AI strategy transparency

Make sure the platform can explain how its AI algorithms work and the strategies used for trading. If a platform keeps its algorithms and operations highly secret or fails to provide enough transparent information, it’s best to avoid using that platform. Reputable platforms usually explain how their AI analyzes the market, makes trading decisions, and provides clear risk management tools.

7. Regularly check account and trading activities

Regularly monitor a trading account to ensure there are no unusual transactions or unauthorized fund transfers. Most platforms offer real-time trade alerts to help track trading activities. Set up alerts for important transactions to receive immediate notification and can take action if needed.

8. Be cautious about free platforms

Although many platforms offer free trials, completely free platforms often come with hidden fees or security risks. Be sure to understand the platform’s fee structure and whether there are any extra charges before getting started. Some scam platforms lure users with “free” services, but later obtain their funds or personal information through other means.

Conclusion

In 2026, AI stock trading bots are the perfect solution for beginners looking to automate their trading strategies and earn passive income. With the bots listed in this guide, anyone can start trading without needing to be a seasoned investor or a coding expert. Whether they want simplicity, advanced features, or a combination of both, these bots can help them navigate the stock market with ease.

Always keep in mind that while AI trading bots are powerful tools, they come with risks. It’s important to monitor trades, set appropriate risk management tools, and only invest what someone can afford to lose.

By choosing the right AI bot and following best practices, traders can set themselves up for success in the world of stock trading.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

The US Treasury secretary, Scott Bessent, has reportedly met with major American bank leaders this week as officials assessed potential cyber threats that Anthropic’s latest artificial intelligence system poses.

Summary

- Scott Bessent convened major U.S. bank CEOs to assess cybersecurity risks linked to Anthropic’s Claude Mythos AI model following a code leak.

- The model reportedly uncovered thousands of long-standing software vulnerabilities, raising concerns over misuse by hackers and threats to financial stability.

- Anthropic’s revenue surpassed $30 billion annualized, driven by enterprise demand, major compute deals with Google and Broadcom, and the growth of its Claude Code platform.

According to reports, Treasury Secretary Scott Bessent brought together senior executives at the department’s Washington headquarters, with Jerome Powell also said to be present. The meeting followed the unveiling of Anthropic’s Claude Mythos model, which the company has described as posing “unprecedented” cybersecurity risks.

Concerns surrounding the model intensified after its code was leaked earlier this month. In a subsequent blog post, Anthropic said advanced AI systems had surpassed “all but the most skilled humans at finding and exploiting software vulnerabilities,” warning that the consequences for economies, public safety, and national security “could be severe.”

The gathering took place while bank executives were already in Washington for an industry event, with invitations largely extended to leaders of systemically important institutions. Regulators consider these banks critical to financial stability, meaning disruptions to their operations could have far-reaching consequences.

Attendees reportedly included David Solomon of Goldman Sachs, Brian Moynihan of Bank of America, Jane Fraser of Citigroup, Ted Pick of Morgan Stanley, and Charlie Scharf of Wells Fargo. Jamie Dimon of JPMorgan Chase was invited but did not attend.

In his annual shareholder letter released this week, Dimon cautioned that cybersecurity “remains one of our biggest risks,” adding that artificial intelligence “will almost surely make this risk worse.”

Anthropic said its yet-to-be-released Mythos model has already identified thousands of vulnerabilities across software and widely used applications. As a result, access to the system has been limited to a small group of companies, including Amazon, Apple, and Microsoft.

The move marks the first time the company has restricted a product rollout. Select infrastructure and technology groups, such as Cisco and Broadcom, have also been granted access, along with the Linux Foundation.

The developments come as fears grow that malicious actors could use advanced AI tools to uncover passwords or break encryption systems designed to protect sensitive data.

Anthropic said some of the flaws identified by Mythos date back as far as 27 years and had not been detected by developers or security monitors before the AI system surfaced them.

The Treasury meeting also follows a recent decision by the US government to classify Anthropic as a potential supply chain risk, a designation the company is currently challenging in court.

Despite the ongoing regulatory scrutiny and a supply chain risk designation from the U.S. Department of Defense, Anthropic has reported unprecedented financial momentum.

In a recent blog post released on April 6, the company said its annualized revenue run rate exceeded $30 billion as of early April 2026, more than tripling from roughly $9 billion at the end of 2025.

Part of that growth has been driven by new compute partnerships with Google and Broadcom, highlighting rising demand for large-scale AI infrastructure. This agreement secures multiple gigawatts of next-generation TPU capacity to power frontier Claude models through 2027 and beyond.

Its agentic coding platform, Claude Code, has emerged as a key contributor, generating more than $2.5 billion in run-rate revenue as of February.

Weekly active users on the platform have also doubled since the start of the year, pointing to rapid adoption of AI-driven development tools as the company shifts its focus toward high-value enterprise agents.

The US Commodity Futures Trading Commission has unveiled the first members of its new innovation task force as the agency continues its push to provide greater clarity for the crypto market.

The Innovation Task Force was initially launched by CFTC Chairman Mike Selig on March 24, who appointed Michael Passalacqua as the leader of the group. Passalacqua is currently the senior advisor to Selig at the CFTC.

In an announcement Friday, the CFTC said that Passalacqua will be joined by a list of five initial members including Hank Balaban, a former Latham & Watkins crypto lawyer; Sam Canavos, an ex-Patomak crypto and prediction markets advisor; Mark Fajfar, a CFTC legal veteran; Eugene Gonzalez IV, an ex-Sidley blockchain lawyer; and Dina Moussa, a CFTC Market Participants Division special counsel.

“The Innovation Task Force brings together a leading team that exhibits deep expertise and an enthusiastic commitment to deliver clear rules of the road for American innovators,” Selig said.

The move is part of a broader push from both the CFTC and Securities and Exchange Commission to provide regulatory clarity for the digital asset sector under the direction of the Donald Trump administration.

Source: Michael Passalacqua

CFTC pushing for clarity as major bill stalls

On Friday, Selig also announced the CFTC’s “innovation tracker,” which highlights all the work done under Selig to help “advance regulatory clarity, market integrity, and responsible technological progress.”

The website lists three key innovation areas the agency is focused on, including crypto and blockchain, artificial intelligence and autonomous systems, and contracts and prediction markets.

Related: Prediction market users await Artemis II mission splashdown

The CFTC in particular could be set to be the main overseer of the industry, with the SEC proposing in mid-March that the agency doesn’t see most crypto assets falling under its jurisdiction as securities.

However, the certainty of both agencies’ roles is still largely dependent on whether the Clarity Act passes through the upper levels of government and becomes enshrined as law — something SEC Chair Paul Atkins called for via X on Thursday.

The SEC and CFTC are “ready to implement the CLARITY Act,” he said, adding: “It’s time for Congress to future-proof against rogue regulators and advance comprehensive market structure legislation to President Trump’s desk.”

Magazine: Should users be allowed to bet on war and death in prediction markets?

Solana‑based Drift Protocol’s $270m exploit has become a live test of how Circle, DeFi builders and lawmakers share responsibility when stablecoins sit at the center of a hack.

Summary

- Drift Protocol lost roughly $270 million in a governance exploit, one of 2026’s largest DeFi hacks.

- Circle’s Dante Disparte said USDC freezes only occur under legal orders, rejecting calls for unilateral intervention.

- Disparte urged lawmakers to fast‑track the GENIUS Act and CLARITY Act and pushed DeFi to adopt on‑chain “circuit breaker” controls.

Circle’s chief strategy officer Dante Disparte has responded to the roughly $270 million exploit on Solana‑based Drift Protocol by defending how USDC is governed while demanding tougher legal and technical safeguards for DeFi. The April 1 attack saw an attacker seize Drift’s governance keys, drain an estimated $270‑$285 million in assets, rapidly swap much of the haul into USD Coin (USDC) and bridge over $230 million to Ethereum via Circle’s own Cross‑Chain Transfer Protocol. Investigators such as on‑chain analyst ZachXBT argued Circle had “roughly six hours” to freeze the stolen USDC but “took no action,” intensifying scrutiny on how centralized issuers respond in live attacks.

Responding in an X statement and subsequent commentary, Disparte stressed that Circle cannot and will not freeze USDC on mere social‑media pressure or unilateral discretion. “USDC freezing is only executed under legal mandate — not unilaterally,” he said, framing the policy as a matter of due process and financial privacy rather than operational convenience. He added that “it is indefensible and untenable that tools and software are co‑opted by bad actors who remain unchecked,” but argued that unchecked intervention by issuers would be just as dangerous for legitimate users.

Disparte used the Drift exploit to press U.S. lawmakers to accelerate the stablecoin‑focused GENIUS Act and the broader market‑structure CLARITY Act, saying both are needed “before the next major security incident.” He has previously called the GENIUS Act “the most significant US law for innovation since the 1990s,” arguing it “enshrines Circle’s way of doing business into law” by requiring full‑reserve backing, monthly disclosures and robust supervision for dollar stablecoin issuers. The CLARITY Act, currently moving through Congress, would extend that framework to trading venues and intermediaries, creating a clearer basis for when and how assets like USDC can be frozen or clawed back after hacks.

Beyond Washington, Disparte is now urging DeFi teams to import safeguards long standard in traditional markets. He called on protocols to deploy on‑chain “circuit breaker mechanisms” that can automatically halt trading or withdrawals under abnormal conditions, arguing that “risk controls, not improvisation on X, should decide how a $270 million exploit plays out.” With Drift still assessing losses across USDC, BTC, SOL and other assets, the incident has become a live‑fire test of whether stablecoin issuers, protocols and regulators can share responsibility without turning permissionless finance into a de facto banked system.

Zcash price shot up over 21% today, extending its gains over the past week to over 60% as privacy coins see renewed demand from investors.

Summary

- Zcash surged over 20% to a three-month high as strong retail demand and rising futures open interest fueled momentum.

- Growth in shielded liquidity pools, now holding over 60% of supply, alongside a broader rally in privacy coins like Monero, boosted investor interest.

- A breakout from a descending triangle and bullish indicators signal further upside potential, with key resistance near $419 and support at $332.

According to data from crypto.news, Zcash (ZEC) price rose nearly 23% to a three-month high of $383 on Friday, April 10. At this price, the token remains nearly 86% higher than its year to date low. The token’s gains have made it the best-performing crypto asset in the daily and weekly timeframes, largely outpacing the others that followed.

Zcash’s rally came amid strong interest from retail investors for the asset over the past couple of days. Notably, data from CoinGlass shows that this demand has driven its futures open interest to $818 million on Friday, up nearly 26% from levels recorded the previous day.

As such, if investor demand continues to build for the token, it could likely continue its uptrend as bulls try to push its price above $400 for the first time since January.

A major catalyst driving investor interest has been growing attention towards its shielded liquidity pools, one of the core features of the network that ensures transaction confidentiality. The Zcash dashboard shows that over 31% of all ZEC coins are now held in shielded pools. This represents nearly $1.96 billion in protected value.

Zcash price also gained momentum from a broader rally among privacy-focused cryptocurrencies today, as the total market cap of these assets rose over 11%, bringing its market cap to over $13 billion. Notably, Monero (XMR), currently the market leader in the privacy sector, has risen 4.3% in the past 24 hours. Other privacy tokens, such as Dash (DASH) and Decred (DCR), also recorded significant gains.

On the daily chart, Zcash price has broken out of a descending triangle, a major bullish reversal signal in technical analysis.

The Supertrend indicator has flipped green, a sign that the bulls are now firmly in control of the market. At the same time, the RSI has crossed above overbought levels, lying at 78, which means the token is seeing massive buying pressure, though it may face a brief cooling off period.

For now, the key overhead resistance level for Zcash next lies at $419, the 61.8% Fibonacci retracement level. A break above the resistance could spur a rally toward the $450 psychological mark.

On the contrary, if Zcash price falls below $332, where the 38.2% Fibonacci support level lies, the bullish thesis could be invalidated, leading to a deeper correction toward $300.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Natasha Lyonne says she took sleeping pill before being escorted off flight, claims she was 'detained' by ICE

XRP- Ripple Treasury Ceritified To Tap 11,000+ SWIFT Banks? Yes – Bitcoin Hits $200K What Is XRP???

(VIDEO) Jimmy Kimmel Speculates Melania Trump’s Surprise Epstein Address Was Revenge on Trump

Why Israel is blocking foreign journalists from entering

Bitcoin: We’re Entering The Most Dangerous Phase

Alan Cumming Brands Baftas Ceremony A ‘Triggering S**tshow’

XRP- Ripple Treasury Ceritified To Tap 11,000+ SWIFT Banks? Yes – Bitcoin Hits $200K What Is XRP???

ULTIMATE Cryptocurrency Trading Course (From Beginner To PRO)

Gs Finance – New Loan App for Low Cibil ( Review ) | New Loan App review 2026 | Only On KYC

-

Business5 days ago

Business5 days agoThree Gulf funds agree to back Paramount’s $81 billion takeover of Warner, WSJ reports

-

Sports6 days ago

Sports6 days agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Politics10 hours ago

Politics10 hours agoUS brings back mandatory military draft registration

-

Fashion11 hours ago

Fashion11 hours agoWeekend Open Thread: Veronica Beard

-

Business7 days ago

Business7 days agoExpert Picks for Every Need

-

Tech3 days ago

Tech3 days agoHow Long Can You Drive With Expired Registration? What Florida Law Says

-

Business6 days ago

Business6 days agoNo Jackpot Winner, Prize to Climb to $231 Million

-

Fashion5 days ago

Fashion5 days agoMassimo Dutti Offers Inspiration for Your Summer Mood Board

-

Sports11 hours ago

Sports11 hours agoMan United discover Nico Schlotterbeck transfer fee as defender reaches Dortmund agreement

-

Fashion3 days ago

Fashion3 days agoLet’s Discuss: DEI in 2026

-

Crypto World3 days ago

Crypto World3 days agoBitcoin recovers as US and Iran Agree a Ceasefire Deal

-

Business8 hours ago

Business8 hours agoTesla Model Y Tops China Auto Sales in March 2026 With 39,827 Registrations, Beating Cheaper EVs and Gas Cars

-

Crypto World2 days ago

Crypto World2 days agoCanary Capital Files SEC Registration for PEPE ETF

-

Business6 days ago

Business6 days agoAkebia Therapeutics, Inc. (AKBA) Discusses Pipeline Progress and Strategic Focus on Kidney Disease Treatments at R&D Day – Slideshow

-

Business16 hours ago

Business16 hours agoOpenAI Halts Stargate UK Data Centre Project Over Energy Costs and Copyright Row

-

Politics7 days ago

Politics7 days agoThe UK should not pay a penny in slavery reparations

-

Tech5 days ago

Tech5 days agoHaier is betting big that your next TV purchase will be one of these

-

Tech5 days ago

Tech5 days agoThe Xiaomi 17 Ultra has some impressive add-ons that make snapping photos really fun

-

Tech5 days ago

Tech5 days agoSamsung just gave up on its own Messages app

-

Tech5 days ago

Tech5 days agoGamer Restores the Original PlayStation Portal From Two Decades Ago

You must be logged in to post a comment Login