Crypto World

PUMP Surges 15% as Memecoin Market Picks Up

The memecoin sector is far from its peak, but increased activity is driving attention back to PUMP.

TLDR

- Global financial firms executed the first cross-border intraday repo using tokenized U.K. government bonds on the Canton Network.

- The transaction included a cross-currency exchange involving tokenized gilts and tokenized deposits in a non-sterling currency.

- The repo aimed to demonstrate real-time collateral movement without relying on traditional market cut-off times.

- Participants included LSEG, Euroclear, DTCC, Tradeweb, Citadel Securities, Societe Generale, Archax, and Cumberland DRW.

- TreasurySpring embedded interest and risk terms directly into smart contracts supporting the repo structure.

Global financial firms executed a new cross-border intraday repo using tokenized U.K. bonds on the Canton Network, and the move introduced real-time collateral mobility across markets while expanding access to previously underused assets, and it marked an early step in broader institutional blockchain adoption.

The group carried out the trade with tokenized gilts and tokenized cash, and it validated the network’s ability to support fast settlement across jurisdictions. Furthermore, firms used the platform to complete a cross-currency exchange that involved digital gilts against non-sterling deposits.

Cross-Border Repo Execution

LSEG and Euroclear joined the test to move collateral at intraday speed, and the teams aimed to reduce delays tied to traditional cut-off windows. Furthermore, DTCC and Tradeweb supported the workflow to validate synchronized settlement across regions.

Citadel Securities and Societe Generale joined the exercise to assess faster liquidity access, and digital asset firms Archax and Cumberland DRW handled operational elements. Moreover, TreasurySpring applied smart-contract terms to embed rate and risk features directly into each transaction.

The repo involved tokenized gilts drawn from a $2 trillion market, and the test demonstrated that digital instruments can move with fewer frictions across borders. Likewise, the structure allowed firms to complete intraday financing without waiting for legacy batch settlement processes.

Digital Asset executive Kelly Matheison stated that “only about $28 trillion of high-quality liquid assets are usable as collateral today,” and she argued that timing constraints limit broader deployment. Therefore, she explained that real-time transfer rails could unlock more efficient balance-sheet use.

Tokenization as a Settlement Tool

Digital Asset, the primary developer of the Canton Network, raised support from Goldman Sachs, DRW, BNY, and Nasdaq, and the backing underscored rising institutional interest in shared ledgers. Additionally, the firm said Canton aims to help institutions use assets around the clock rather than within limited windows.

Matheison stated that “timing restricts access to global collateral,” and she emphasized that blockchain-based settlement removes constraints tied to geography and market hours. Consequently, the platform allows ownership transfers to occur in real time.

The firms tested the Canton model to shift collateral faster across regions, and the design allowed intraday repo returns without overnight exposure. Furthermore, the shared ledger enabled both sides to verify movements instantly.

The test also showed that synchronized asset transfers reduce manual steps, and the participants reviewed the workflow to confirm operational reliability. Therefore, the model supports more efficient trading schedules.

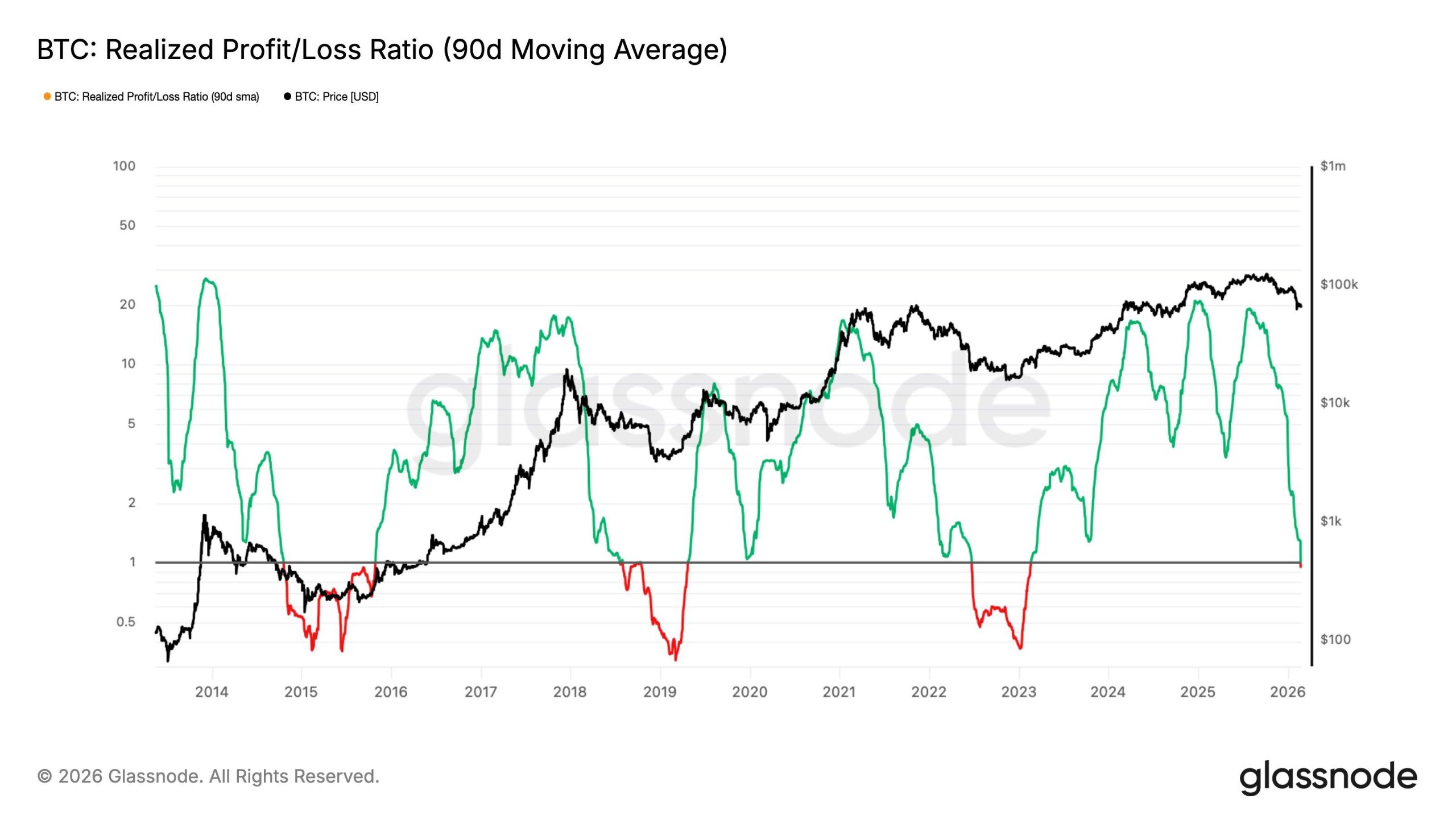

Bitcoin price has rebounded slightly after recent selling pressure, yet broader technical signals remain cautious. The crypto king recently broke down from a triangle pattern, raising concerns of further downside.

While the move may appear to be stabilizing, underlying metrics suggest potential prolonged weakness.

Bitcoin’s Past Might Dictate Hints At Its Future

The Realized Profit/Loss Ratio (90D-SMA) has fallen below 1, signaling Bitcoin’s transition into an excess loss-realization regime. This metric measures whether investors are realizing more profits or losses over a rolling 90-day period. A reading below 1 confirms that losses dominate.

Historically, breaks below this threshold have persisted for six months or longer before recovering. Reclaiming levels above 1 has typically aligned with constructive liquidity returning to the crypto market. Until that shift occurs, sentiment may remain defensive and capital inflows limited.

Want more token insights like this? Sign up for Editor Harsh Notariya’s Daily Crypto Newsletter here.

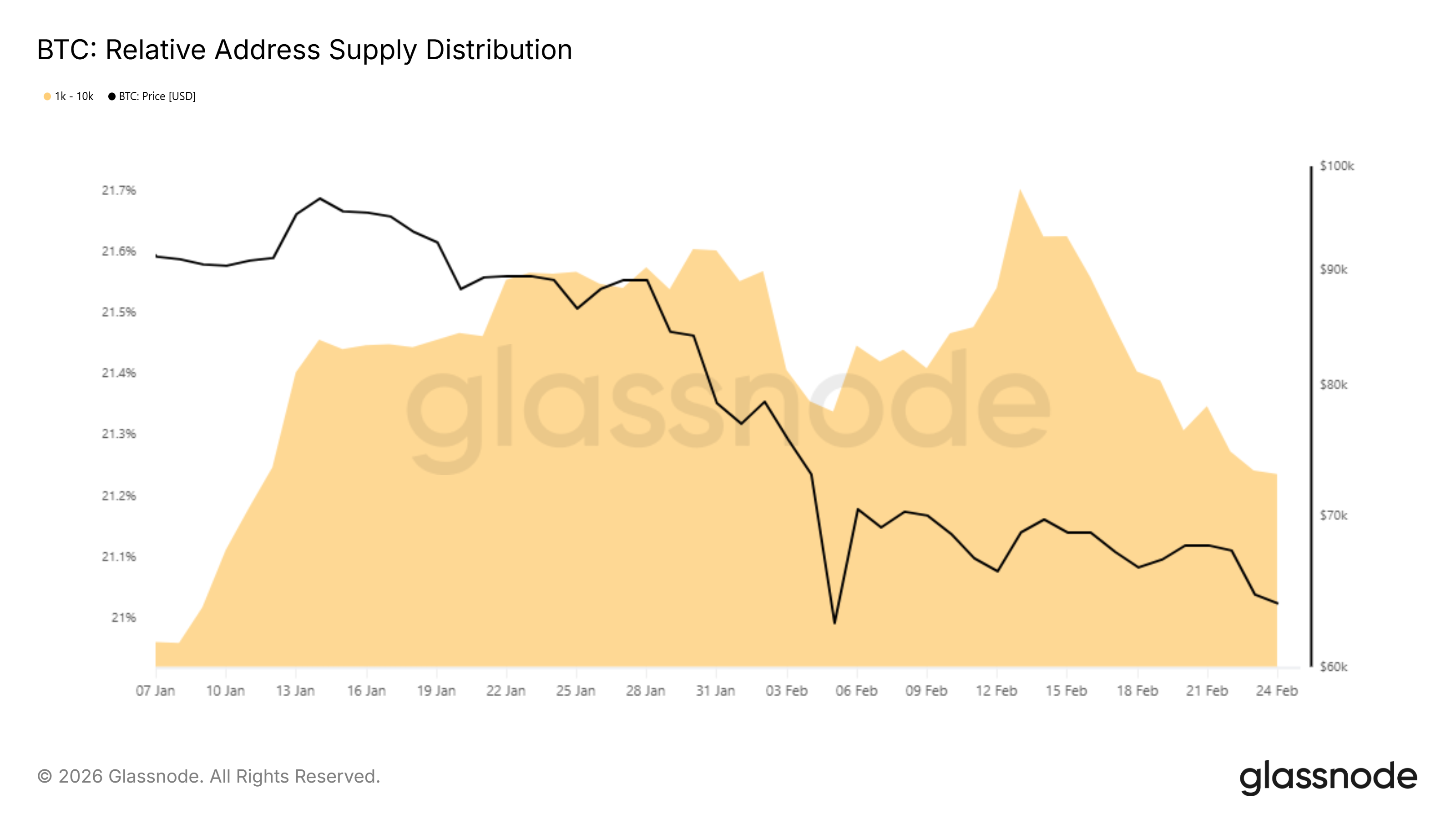

Supply distribution data reveals notable changes among large Bitcoin holders. Addresses holding between 1,000 and 10,000 BTC have gradually reduced exposure. Over the past 12 days, their share of total supply declined from 21.7% to 21.2%.

This shift represents a reduction of nearly 90,000 BTC, valued at approximately $5.8 billion. Although the pace of selling appears measured, distribution by large holders can weigh on price stability. Persistent offloading may limit upside attempts in the near term.

BTC Price Recovery Unlikely

Bitcoin is trading at $65,475 at the time of writing after bouncing from the $62,525 support level over the past 24 hours. The earlier triangle breakdown projected a potential 14% decline. However, immediate downside momentum appears to be slowing.

If macro bearish signals continue to dominate, Bitcoin could retest the $62,525 support. A decisive break below that level may expose BTC to the psychological $60,000 threshold. Losing this support could intensify panic selling and deepen the correction.

Conversely, renewed buying interest at current levels may shift short-term momentum. A breakout above the $67,394 resistance would invalidate the triangle pattern. Sustained strength beyond that point would signal improving structure for BTC and suggest a temporary bullish recovery despite broader liquidity concerns.

Crypto World

Coinbase Fully Launches Stock Trading for All U.S. Users With 8,000+ Stocks and ETFs Available

TLDR:

-

- Coinbase has fully launched stock trading for all U.S. users, following a limited rollout in December 2025.

- Over 8,000 stocks and ETFs are now available with 24/5 commission-free trading in USD or USDC stablecoins.

- Fractional share trading is supported, allowing U.S. investors to start buying stocks with as little as $1.

- Coinbase partnered with Yahoo Finance, adding trade buttons to asset pages for 150 million monthly visitors.

- Coinbase has fully launched stock trading for all U.S. users, following a limited rollout in December 2025.

Coinbase has fully rolled out stock trading to all U.S. users, following a limited launch in December 2025. The crypto exchange now offers access to over 8,000 stocks and ETFs through its platform.

Trading runs commission-free, 24 hours a day, five days a week. Users can conduct transactions in either USD or the USDC stablecoin. Fractional share trading is also supported, allowing investors to start with as little as $1.

Coinbase Brings Full Stock Trading Access to U.S. Users

Coinbase first introduced stock trading during its “System Update” product showcase in December 2025. At that time, only hundreds of stocks were available to a limited group of users.

With the full release, thousands of assets are now accessible to all eligible U.S. customers. The expansion marks a major step in the platform’s push beyond cryptocurrency trading.

The 24/5 commission-free trading model gives users consistent access throughout the trading week. Supporting both USD and USDC as funding options adds flexibility for crypto-native users.

Fractional shares make the platform more accessible to newer or smaller investors. Together, these features position Coinbase as a direct competitor to fintech platforms like Robinhood.

Users can fund their trades using the USDC stablecoin, which is a feature unique to Coinbase’s offering. This bridges the gap between traditional equities and digital asset investing.

It also reflects Coinbase’s broader strategy of integrating crypto and traditional finance in one place. The platform describes its long-term vision as becoming an “everything exchange.”

Looking further ahead, Coinbase plans to offer tokenized stocks, with details expected in the coming months. The company also intends to expand its stock perpetual products this spring through Coinbase Bermuda Ltd.

That move would give international traders 24/7 exposure to U.S. equities, subject to regulatory approval. Those products will not be available to U.S. persons.

Yahoo Finance Partnership Supports Broader Market Reach

Alongside the full rollout, Coinbase announced a partnership with Yahoo Finance to expand its audience. Yahoo Finance will add a “Trade [asset] on Coinbase” button to stock and crypto asset pages.

The site draws more than 150 million global monthly visitors each month. This gives Coinbase a direct channel to a large base of retail investors.

Yahoo Finance users will receive a one-month free trial of a Coinbase One Basic membership. The membership covers zero trading fees and USDC rewards for new users.

George Leimer, general manager at Yahoo Finance, noted the partnership targets everyday investors. He pointed to a growing trend of investors exploring digital assets alongside traditional securities.

The Yahoo Finance integration is currently focused on the U.S. market at launch. Coinbase has said it plans to expand its equities trading products internationally in the coming months.

A dedicated crypto hub through Yahoo Finance is also in development. That hub will feature news, data, and analysis from more than a dozen publishers.

Separately, Coinbase has partnered with Apex Fintech Solutions to handle clearing, custody, and execution services for its equities offering.

Crypto World

Canton’s Industry Working Group Advances Cross-Border Collateral Mobility With Tokenised Gilts

TLDR:

- Canton’s working group completed its fourth transaction round, introducing tokenised Gilts as repo collateral for the first time.

- The round featured the first cross-currency intraday repo using tokenised Gilts against non-GBP tokenised deposits on Canton.

- Archax joined as a new participant, using its tokenisation engine to create regulated digital representations of traditional Gilts.

- The working group plans to expand cross-border collateral mobility across European and global markets throughout all of 2026.

Canton’s industry working group has taken another step forward in advancing cross-border collateral mobility on Canton.

Digital Asset, alongside a consortium of leading financial institutions, completed a fourth set of transactions on the Canton Network on February 24, 2026.

The latest round builds on prior milestones by introducing tokenised Gilts and cross-currency repo activity. Together, these achievements move the industry closer to a scalable, always-on capital markets infrastructure that operates across borders and asset classes.

Working Group Builds on Previous Transaction Rounds

The industry working group has steadily expanded its scope across each successive round of transactions. Following the third set completed in December 2025, which covered multiple asset classes and currencies using tokenised deposits, this fourth round introduced new instruments and cross-currency structures. Each iteration has added complexity while maintaining institutional-grade standards across the board.

This latest round featured the first cross-border intraday repo transaction conducted using tokenised Gilts. It also marked the first cross-currency intraday repo using tokenised Gilts against non-GBP tokenised deposits.

These additions reflect the group’s commitment to broadening the range of assets that can move seamlessly across borders within the Canton ecosystem.

@digitalasset, in collaboration with @CantonNetwork participants, announced the completion of a fourth set of transactions showcasing continued momentum in cross-border intraday repurchase activity.

The group’s approach is methodical, advancing one transaction type at a time while ensuring each new layer meets real market requirements. This measured progression is what gives the working group its credibility across participating institutions.

Expanded Membership Strengthens the Consortium’s Reach

A key feature of this transaction round was the growth in active participation across the working group. Archax, a regulated digital asset exchange, broker, and custodian, joined as a new participant.

Existing members including LSEG, Euroclear, Citadel Securities, TreasurySpring, and IntellectEU also deepened their roles in this round.

Archax supported the transaction by leveraging its broker and custody permissions to hold traditional Gilts on behalf of clients.

It then used its tokenisation engine to create regulated digital representations of those assets. Graham Rodford, CEO and co-founder of Archax, described this function as central to the firm’s broader vision and participation strategy.

The growing membership across custodians, trading venues, clearinghouses, and technology providers adds structural depth to the working group. Participants now span the full transaction lifecycle, from execution to settlement and custody.

This breadth makes the group well-positioned to address production-scale challenges as the initiative moves beyond the pilot stage.

Cross-Border Collateral Mobility Takes Shape Across Currencies

The working group’s focus on cross-border collateral mobility is becoming more concrete with each round. TreasurySpring validated cross-currency intraday repo and reverse repo against UK Gilts, with haircuts and repo interest embedded directly into smart contracts.

Co-Founder Matthew Longhurst stated these transactions reflect real economic and risk terms across an institutional governance framework.

Euroclear UK & International played a central role as the UK’s central securities depository in tokenising Gilts for the transaction.

CEO Chris Elms noted that enabling real-time, cross-border collateral mobility helps unlock new liquidity sources for clients. EUI’s involvement brings regulated post-trade infrastructure directly into the Canton framework.

LSEG’s DiSH network served as the cash leg for the transactions, enabling instantaneous beneficial ownership transfer of commercial bank money across multiple currencies and jurisdictions.

Bud Novin, Head of Payment Systems at LSEG, confirmed that DiSH Cash supported the first tokenised intraday Gilt repo on Canton Network.

He added that LSEG DiSH is positioned as a trusted third-party solution for mobilising networks in tokenised markets.

Industry Players Align Around Scalable On-Chain Market Infrastructure

Beyond the transactions themselves, participants are increasingly focused on what comes next for the working group.

IntellectEU’s Anastasiia Vitmer pointed to how quickly the scope is expanding across assets, infrastructure, and active participants.

Her firm’s Catalyst Suite is being built to support any institutional use case on Canton Network as on-chain markets continue to mature.

DTCC’s Brian Steele reinforced that collaboration across the industry is essential to setting standards and accelerating digital asset adoption.

He added that this cross-border intraday repo use case confirms growing demand for seamless, scalable financial infrastructure. DTCC’s role reflects how traditional market infrastructure providers are engaging directly with on-chain models.

Digital Asset’s Kelly Mathieson stated that greater asset diversity and broader participation are paving the way for more efficient and liquid capital markets.

The working group plans to continue groundbreaking on-chain financing initiatives throughout 2026, with European markets and other key regions in focus.

Cumberland DRW’s Chris Zuehlke added that Canton continues to show how tokenisation can unlock real efficiency gains across an increasingly diverse set of assets and currencies.

TLDR

- Polymarket users increased bets on Meteora as the leading candidate in ZachXBT’s upcoming investigation.

- The contract for Meteora reached a 29 percent probability based on active trading behavior.

- ZachXBT stated that the investigation will expose employees who allegedly used internal data for insider trading.

- Traders wagered more than seven million dollars on which platform would be identified on Thursday.

- The investigation did not clarify whether the alleged insider trading involved stocks or digital assets.

Traders on the prediction platform Polymarket increased wagers on which exchange crypto sleuth ZachXBT will target next, and they pushed one project ahead quickly. The market showed heavy activity as users responded to new hints shared on X. The event drew fresh attention after he teased a “major investigation” linked to insider trading claims.

Polymarket Bets Shift Toward Meteora

As trading continued on Tuesday, users raised the probability that Meteora would be named in the probe. The contract reached 29% and moved past other listed platforms.

Users tracked each update closely, and they adjusted positions after his Monday post. However, the contracts still reflected crowd sentiment rather than privileged information.

He said the investigation would show that several employees at an unnamed exchange misused internal data. He added that they engaged in insider trading “over a prolonged period of time.”

Market participants responded fast, and they assessed which platform fit the description. The contract pool included MEXC, Axiom, and Wintermute.

By Tuesday, users had wagered more than $7 million across the choices. The total rose as traders sought clarity from his updates.

The market did not show whether the alleged insider trading involved stock or digital assets. Traders waited for his Thursday disclosure to confirm the scope.

His comments prompted rapid shifts in odds across the platform. Yet trading patterns continued to follow user guesswork rather than confirmed data.

Analysts tracking the contracts noted that trading volume increased during active discussion periods. Activity often rose within minutes of new social media posts.

The market structure allowed users to adjust quickly to every clue. However, the contract rules limited outcome definitions to his final announcement.

State Pushback and CFTC Position on Prediction Markets

Regulatory pressure increased as state officials clashed with federal regulators over these platforms. The dispute widened after the chair of the Commodity Futures Trading Commission restated federal oversight powers.

He argued that the agency had “exclusive jurisdiction” over prediction markets. He also compared them to derivatives markets.

He warned that any challenge from state authorities would be met in court. He confirmed that the agency had already filed amicus briefs in related disputes.

The platform also contested actions brought by the Massachusetts regulator. It argued that only the federal agency held authority over such markets.

Regulatory actions continued as several states pursued separate cases. These cases centered on claims that the platforms offered unlicensed gambling.

The ongoing jurisdiction conflict added pressure to both regulators and platforms. Yet trading on the platform remained active throughout the debate.

U.S. Senator Richard Blumenthal announced a formal Senate inquiry into Binance after recent news reports revealed that the world’s largest cryptocurrency exchange allegedly facilitated nearly $1.7 billion in transactions tied to sanctioned Iranian entities and Russia’s so-called “shadow fleet” of oil tankers.

Summary

- Richard Blumenthal has opened a Senate inquiry into Binance following reports that the exchange processed roughly $1.7 billion in transactions linked to Iranian proxies and Russia’s shadow fleet.

- The investigation seeks documents related to Binance’s compliance practices and the alleged dismissal or sidelining of internal investigators who flagged suspicious accounts.

- Binance has denied wrongdoing and says it has significantly reduced sanctions exposure while strengthening its anti-money-laundering controls.

Blumenthal demands answers from Binance

The inquiry centers on questions about the company’s compliance practices and its response to internal warnings from compliance staff.

In a letter to Binance CEO Richard Teng, Blumenthal, ranking member of the Senate Permanent Subcommittee on Investigations, demanded documents and records detailing the circumstances surrounding the illicit transfers and why compliance personnel who uncovered the activity were reportedly suspended or dismissed.

Interestingly, the investigation comes as Binance recently said it has sharply reduced its exposure to sanctioned entities, reporting a roughly 96% drop in related activity between early 2024 and mid-2025. The exchange has argued that sanctions-linked transactions now account for a tiny fraction of total trading volume.

According to reporting in the New York Times and Wall Street Journal, Binance internal investigators found over 1,500 accounts accessed from Iran and traced funds sent through intermediaries, including Hexa Whale and Blessed Trust, to entities linked to Iran’s Islamic Revolutionary Guard Corps and payments to personnel on Russian ships evading sanctions.

“Binance is a repeat offender: it has long been aware that the Iranian regime and its terrorist proxies use its cryptocurrency platform as a convenient and reliable means to bypass international sanctions, anti-money laundering controls, and other banking restrictions,” the senator wrote in the letter.

Blumenthal’s letter also accused Binance of ignoring clear warning signs, allowing potentially illicit accounts to operate, and even reportedly providing support to money-laundering entities, despite a 2023 settlement with U.S. authorities that required enhanced anti-money-laundering controls.

The senator’s inquiry also references concerns about the reported firing of internal investigators who flagged the activity, raising questions about corporate compliance culture.

Binance has publicly denied that it knowingly facilitated sanctions evasion or that its compliance staff were punished for raising concerns, saying flagged accounts were offboarded and that it cooperates with regulators.

The Web3 gaming platform the9bit, has surpassed 7 million users while expanding the utility and reach of its native ecosystem token, $9BIT.

$9BIT’s value has skyrocketed sevenfold, driven by the9bit platform surpassing 7 million users and intensified efforts in its AI Game Economy. This period of notable expansion includes major ecosystem enhancements, such as a key alliance with AAA publisher Capcom and a full commitment to accelerating AI Game Development (AIGD). Additionally, the9bit is focused on offering significantly reduced game prices by cutting traditional markups and implementing integrated localized fiat gateways and crypto payment solutions.

Since its launch, $9BIT has experienced significant market growth, reflecting accelerating adoption across the the9bit ecosystem. The token is currently listed on major global exchanges, including KuCoin, MEXC, and BingX, with additional listings under consideration as the ecosystem expands.

But beyond market performance, the real story lies in ecosystem scale.

Bridging Web3 Integration with AAA Partnerships

Launched in August 2025, the9bit is pioneering the convergence of traditional AAA gameplay and Web3 incentives, establishing an interactive digital economy where gaming is rewarded.

As of 24 Feb 2026:

- Over 7 million registered users

- More than 38,000 active gamers and space owners

- Over 32.8 million $9BIT tokens distributed to ecosystem participants

$9BIT is the essential utility asset, empowering the ecosystem by facilitating governance, reward distribution, creator incentives, and access to premium in-platform services. This model shifts the user experience from passive consumption to active engagement, allowing users to:

- Earn rewards through direct gameplay and engagement.

- Participate in community governance via voting mechanisms.

- Redeem tokens for premium content and ecosystem utilities.

In a major leap for blockchain-integrated gaming, the9bit has secured its position as a main partner with Capcom. This collaboration will align closely with the highly anticipated global release of Resident Evil 9 on February 27, 2026, with more Capcom future works anticipated in the future, demonstrating the9bit’s capacity to bridge traditional gaming giants with Web3 infrastructure.

By partnering with major global releases, the9bit is elevating its platform beyond casual games, offering its community unique tokenized engagement opportunities and unprecedented access to major franchises.

Introducing AIGD: AI-Powered Game Creation

The next big leap forward for the9bit is AIGD (AI Game Development). This new, AI-assisted creation layer will dramatically lower the barrier for anyone to publish a game. Allowing users to turn a great idea into a fully playable game. This capability unlocks a vibrant, self-sustaining loop between creators and players. Builders use powerful AI tools to bring their games to life, players jump in and generate exciting ecosystem activity, and everyone is rewarded with $9BIT.

This whole system creates a fantastic new reward cycle:

1. Creators build games using AI tools, quickly develop and launch their games.

2. Players engage and generate activity which the community jumps in.

3. Engagement translates into rewards distributed across the ecosystem.

4. Creative and great creators directly benefit from the traction.

By aligning incentives between creators and players, the9bit is building a genuinely scalable, self-sustaining gamer-driven economy, a powerful model that puts the value right back into the hands of the people who make the ecosystem thrive.

Backed by Public-Market Infrastructure

According to its whitepaper, the9bit ecosystem allocates 1.9 billion $9BIT tokens to The9 Limited in recognition of its strategic and operational contributions. As of February 24, 2026, 950 million tokens have been delivered, with the remaining allocation expected in the coming months.

The9 Limited, listed on Nasdaq since 2004, brings public-market governance standards and infrastructure experience to the Web3 gaming space, bridging traditional Internet operations with blockchain-enabled economies.

What’s Next

As 2026 unfolds, the9bit plans to:

- Expand AIGD toolkits and AI-assisted publishing capabilities

- Deepen token utility across gameplay layers

- Expand AAA integrations through our main partnership with Capcom

- Accelerate user acquisition across MENA and Southeast Asia

- Strengthen community-driven governance initiatives

- Explore further exchange listings

With user growth accelerating and AI-powered creation lowering barriers for developers worldwide, the9bit is positioning itself at the intersection of gaming, AI, and Web3 infrastructure.

Play Together. Earn Together. Own Together.

About the9bit

the9bit is a Web3-enabled gaming platform that integrates traditional gameplay with tokenized rewards. The platform offers game purchases, mobile top-ups, casual gaming, and community features — while empowering creators through AI-driven development tools.

For more information, visit: the9bit.com

About The9 Limited

The9 Limited (Nasdaq: NCTY) is an Internet company listed on Nasdaq since 2004. The company operates in online gaming, Bitcoin mining, and AI-driven technology investments, with a growing focus on Web3 infrastructure.

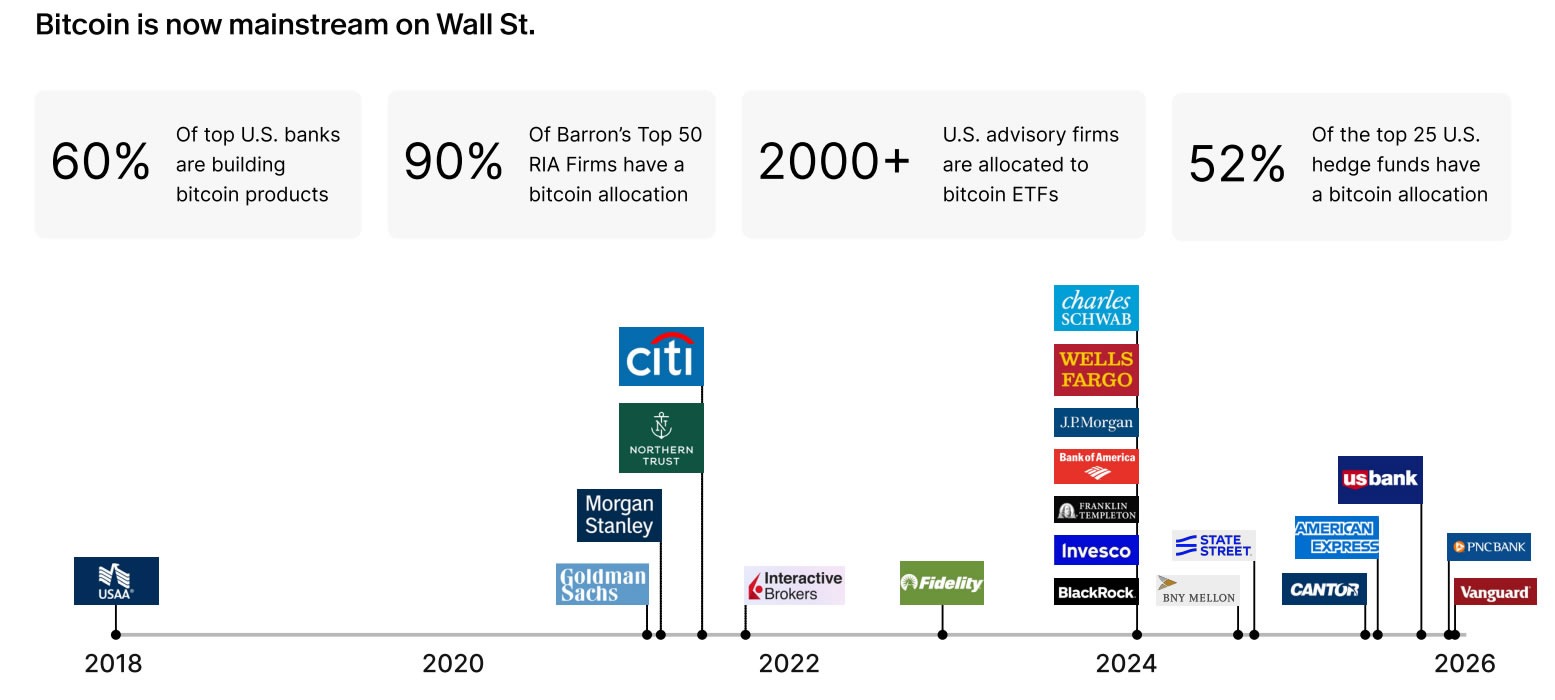

Bitcoin’s adoption by institutions, banks, merchants, public companies, and nation-states has boomed in 2025, despite the recent price drawdown, says the financial services company River.

“There is no bear market in Bitcoin adoption,” River said in a report published on Tuesday, which noted that while Bitcoin (BTC) is down 50% from its all-time high, “adoption is compounding in ways that aren’t affecting the price, yet.”

“Trust in Bitcoin has grown faster than that of any asset in history,” it said. “What began as an experiment is now a globally recognized store-of-value, with adoption patterns that rival the internet.”

Institutional, banking and public company adoption

River reported that institutions accumulated 829,000 BTC in 2025, including purchases by businesses, governments, funds, and exchange-traded funds.

Registered investment advisors have been net buying BTC for eight quarters in a row and have invested roughly $1.5 billion in Bitcoin ETFs per quarter over the past two years, River said.

It noted that these institutions represent “millions of underlying individuals” gaining exposure to Bitcoin for the first time through brokerage accounts, retirement plans, sovereign funds and corporate balance sheets.

Related: Public companies increase Bitcoin holdings despite range-bound prices

Additionally, 60% of the top US banks are building Bitcoin products. “With a favorable regulatory environment in the US, banks can now custody Bitcoin and offer Bitcoin products to their customers,” it stated.

Businesses were the largest buyers of BTC in 2025, with a majority of purchases driven by crypto treasury companies, whose adoption grew 2.5 times last year.

Merchant adoption and payments accelerate

Merchant adoption also surged with the number of businesses in the US accepting Bitcoin for payments tripling, while global usage grew by 74% in 2025, it noted.

Bitcoin payments on the Lightning Network grew by 300% in 2025 and, according to River’s estimations, the network is now processing over $1.1 billion in monthly transaction volume.

Five nation-states became new owners of Bitcoin in 2025, including purchases from two sovereign wealth funds in Luxembourg and Saudi Arabia, and from one central bank in the Czech Republic. The other two were Brazil and Taiwan.

River estimates that 23 nation-states hold Bitcoin through state-backed mining, seizures, or central bank exposure.

Bitcoin volatility is in decline

River said that Bitcoin volatility is also declining, nearing that of gold and the S&P 500, signaling that it is “increasingly viewed as a mature asset class.”

“As volatility falls, the hurdle for more risk-averse investors declines,” it said. “Over time, that opens the door to larger pools of capital.”

River added that Bitcoin is built on trust and claimed it is the world’s “only scarce and incorruptible form of digital money.”

“We expect that in the coming years, Bitcoin adoption will not only continue its current trend, but meaningfully accelerate.”

Magazine: Bitdeer sells all Bitcoin, Metaplanet rejects misconduct claims: Asia Express

Dogecoin pushed higher on outsized volume after repeatedly testing resistance, flipping a key ceiling into support and setting up a near-term test of the next supply zone.

News Background

- DOGE advanced alongside a stabilizing broader crypto market, with buyers stepping in after several sessions of tight consolidation.

- The move wasn’t driven by token-specific headlines but by technical positioning, as repeated failures at $0.0924 left the level primed for a breakout once liquidity expanded.

- The rally comes after DOGE spent hours coiling between $0.090 and $0.0927, building compression before volume returned.

- Open interest remains elevated but not extreme, suggesting moderate leverage participation rather than a crowded speculative push.

Price Action Summary

- DOGE gained 1.9%, rising from $0.0926 to $0.0944

- Breakout above $0.0924 occurred on 749M volume, 176% above baseline

- Price briefly probed $0.0950 before consolidating near $0.0940–$0.0945

- Higher lows formed during consolidation, confirming short-term strength

Technical Analysis

- The key technical development was the sustained break above $0.0924, a level that capped multiple attempts earlier in the session. Once cleared, momentum accelerated quickly, and the breakout volume suggests genuine participation rather than a low-liquidity spike.

- The subsequent consolidation near $0.0940 appears constructive, with shallow pullbacks and higher lows indicating buyers defending the breakout zone. That keeps short-term structure bullish, but the real test lies at $0.0946–$0.0950, where supply previously absorbed upside attempts.

- A decisive close above $0.0950 would expose $0.0955–$0.0960. Failure to hold $0.0940 would risk a pullback toward $0.0924, which now serves as the structural pivot.

What traders say is next?

- Traders view $0.0940 as the new line of defense. As long as DOGE holds above that level, momentum favors continuation toward $0.0955 and potentially $0.0960.

- If the breakout fades and price slips back below $0.0924, the move would resemble a false break, reopening the prior consolidation range and shifting near-term bias back to neutral.

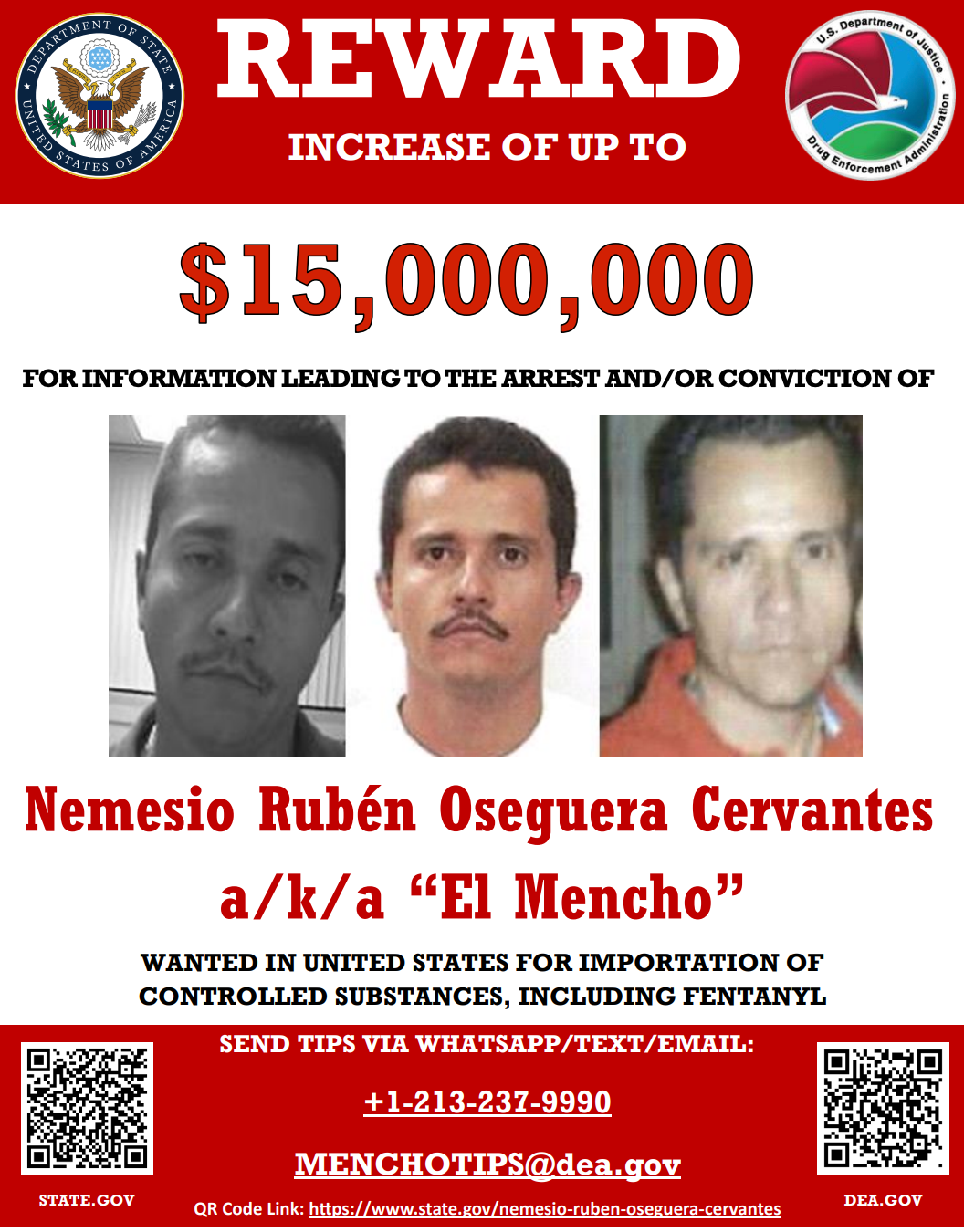

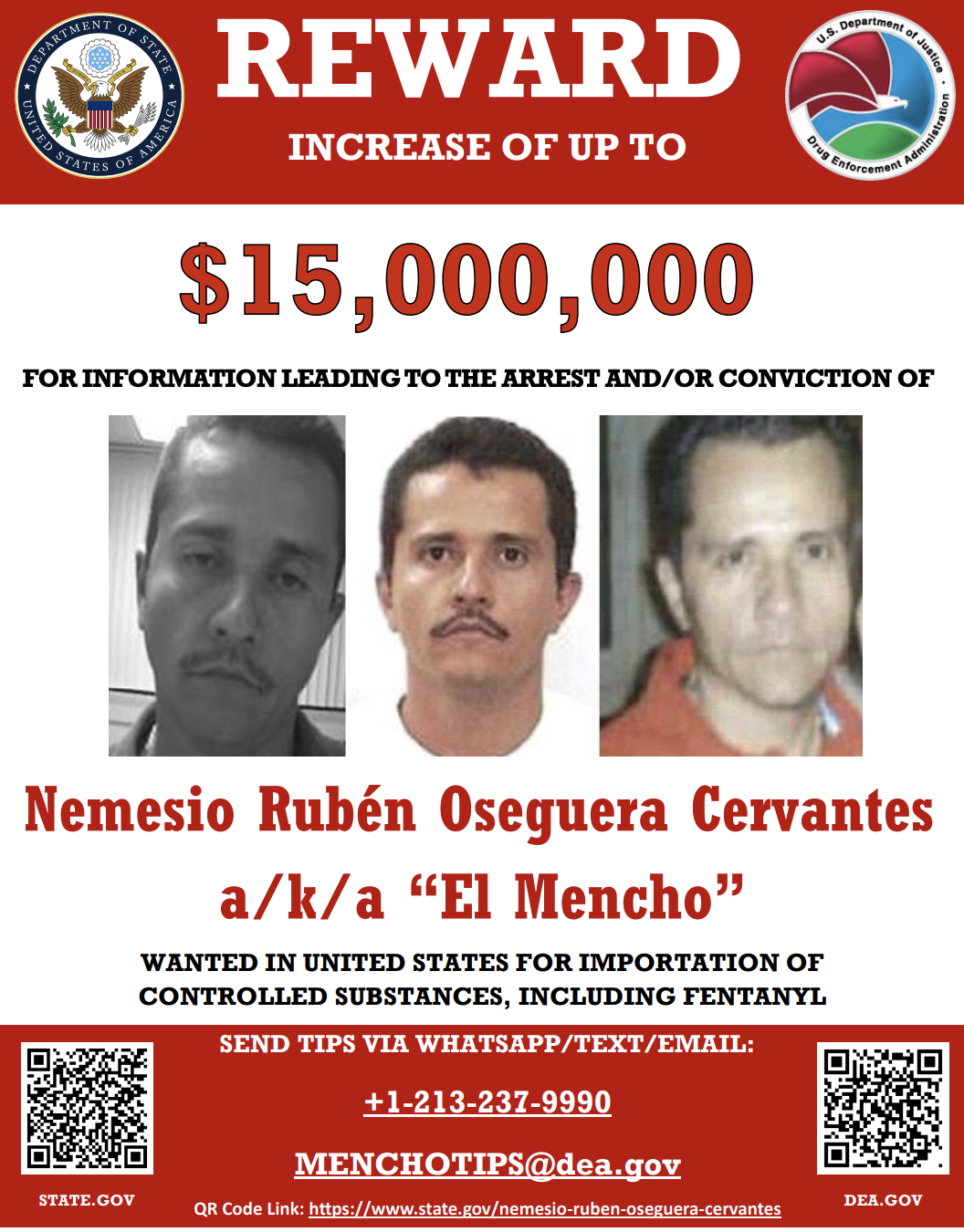

One of the world’s most wanted drug lords is dead. Nemesio Rubén Oseguera Cervantes, known as “El Mencho,” was killed on Sunday. His death triggered a wave of violence across several Mexican states.

Beyond the security impact, attention is also turning to the cartel’s financial operations. In recent years, regulators and researchers have documented how Mexican criminal networks have incorporated cryptocurrency into their operations.

Who was El Mencho?

El Mencho was among Mexico’s most wanted fugitives and the leader of the Jalisco New Generation (CJNG) cartel. According to the US Department of State, the CJNG was formed in 2009. It has since evolved into one of the most violent drug cartels in Mexico.

“It has been assessed to have the highest cocaine, heroin, and methamphetamine trafficking capacity in Mexico, and over the past few years, includes the trafficking of fentanyl into the United States,” the text reads.

On February 20, 2025, the United States officially designated the cartel as a Foreign Terrorist Organization pursuant to Section 219 of the Immigration and Nationality Act.

In addition, the US State Department had offered a $15 million reward for information leading to the capture or conviction of El Mencho. He was killed on Sunday during a military operation.

Following his death, unrest spread across parts of the country. According to the BBC, at least 20 states experienced disturbances as cartel members blocked roads and torched vehicles and businesses.

While the immediate fallout played out in the streets, past data shows that CJNG’s impact has extended beyond territorial control.

Over the past years, investigators have tracked the cartel’s increasingly sophisticated financial infrastructure. This includes its use of digital assets to move and launder funds across borders.

Crypto and Cartel Finance

Cryptocurrencies such as Bitcoin (BTC) and Tether (USDT) are not inherently illicit. They are widely used for legitimate investment, payments, and financial innovation.

However, regulatory and law enforcement agencies have identified instances in which these digital assets were used in transactions linked to illegal activities.

As early as 2020, Reuters reported that US and Mexican authorities observed an increasing use of Bitcoin among major drug trafficking groups, including the CJNG and the Sinaloa Cartel, for laundering money.

In 2024, the US Treasury’s Financial Crimes Enforcement Network (FinCEN) stated that Mexico-based transnational criminal organizations were using virtual currencies, including Bitcoin, Ethereum, Monero, and Tether, to purchase fentanyl precursor chemicals and equipment from suppliers in China.

A March 2025 report by Chainalysis found that suspected China-based chemical traders received more than $37.8 million in cryptocurrency between 2018 and 2023. Major Mexican cartels, including the CJNG, were identified as buyers of these precursors used to manufacture synthetic opioids.

“Blockchain analysis reveals that precursor chemical suppliers advertise directly on darknet markets and messaging apps, accepting digital assets in exchange for chemicals shipped to Mexico. Once paid, crypto funds are laundered through complex transaction patterns including peel chains, layering, and cross-chain swaps, and often cashed out through Chinese exchanges or international mules,” TRM Labs revealed.

In August 2025, FinCEN also highlighted that the CJNG, the Sinaloa Cartel, the Gulf Cartel, and other Mexico-based transnational criminal organizations were using Chinese money laundering networks (CMLNs) to launder illicit proceeds.

Notably, Chainalysis reported that CMLNs now play a dominant role in cryptocurrency-related money laundering. In 2025, these networks accounted for approximately 20% of known cryptocurrency money laundering activity.

While the activity has scaled, regulatory focus has also intensified. According to the US Attorney’s Office for the Southern District of New York, Paul Campo, a former DEA official, and Robert Sensi were indicted for conspiring to provide material support to CJNG.

“As part of the scheme, CAMPO and SENSI agreed to launder approximately $12,000,000 of CJNG narcotics proceeds; laundered approximately $750,000 by converting cash into cryptocurrency; and provided a payment for approximately 220 kilograms of cocaine on the understanding that the payment would trigger the distribution and sale of the narcotics worth approximately $5,000,000, for which CAMPO and SENSI would (i) receive directly a portion of the narcotics proceeds as profit; and (ii) receive a further commission upon the laundering of the balance of the narcotics proceeds,” the press release said.

Thus, El Mencho’s death marks a significant moment in Mexico’s fight against organized crime. Yet the financial systems supporting major cartels remain complex, cross-border, and technologically adaptive, extending far beyond any single individual.

Scarlett Maguire: Trump is now underwater on immigration. What can UK politicians learn from this?

As cartel violence raged in Mexico, this golf-course designer was amid chaos

The US Had a Big Battery Boom Last Year

-

Video5 days ago

Video5 days agoXRP News: XRP Just Entered a New Phase (Almost Nobody Noticed)

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Boden – Corporette.com

-

Politics3 days ago

Politics3 days agoBaftas 2026: Awards Nominations, Presenters And Performers

-

Entertainment7 days ago

Entertainment7 days agoKunal Nayyar’s Secret Acts Of Kindness Sparks Online Discussion

-

Sports1 day ago

Sports1 day agoWomen’s college basketball rankings: Iowa reenters top 10, Auriemma makes history

-

Politics2 days ago

Politics2 days agoNick Reiner Enters Plea In Deaths Of Parents Rob And Michele

-

Tech7 days ago

Tech7 days agoRetro Rover: LT6502 Laptop Packs 8-Bit Power On The Go

-

Sports6 days ago

Sports6 days agoClearing the boundary, crossing into history: J&K end 67-year wait, enter maiden Ranji Trophy final | Cricket News

-

Business3 days ago

Business3 days agoMattel’s American Girl brand turns 40, dolls enter a new era

-

Crypto World23 hours ago

Crypto World23 hours agoXRP price enters “dead zone” as Binance leverage hits lows

-

Business3 days ago

Business3 days agoLaw enforcement kills armed man seeking to enter Trump’s Mar-a-Lago resort, officials say

-

Entertainment6 days ago

Entertainment6 days agoDolores Catania Blasts Rob Rausch For Turning On ‘Housewives’ On ‘Traitors’

-

Business7 days ago

Business7 days agoTesla avoids California suspension after ending ‘autopilot’ marketing

-

Tech3 days ago

Tech3 days agoAnthropic-Backed Group Enters NY-12 AI PAC Fight

-

NewsBeat2 days ago

NewsBeat2 days ago‘Hourly’ method from gastroenterologist ‘helps reduce air travel bloating’

-

NewsBeat2 days ago

NewsBeat2 days agoArmed man killed after entering secure perimeter of Mar-a-Lago, Secret Service says

-

Politics3 days ago

Politics3 days agoMaine has a long track record of electing moderates. Enter Graham Platner.

-

Crypto World6 days ago

Crypto World6 days agoWLFI Crypto Surges Toward $0.12 as Whale Buys $2.75M Before Trump-Linked Forum

-

Tech13 hours ago

Tech13 hours agoUnsurprisingly, Apple's board gets what it wants in 2026 shareholder meeting

-

NewsBeat8 hours ago

NewsBeat8 hours agoPolice latest as search for missing woman enters day nine