Business

American Battery Technology: Another Good Quarter Under The Belt

Business

Tech Investing Seems Broken. Our Roundtable Pros Share 15 Stock Picks to Fix Your Portfolio.

Tech Investing Seems Broken. Our Roundtable Pros Share 15 Stock Picks to Fix Your Portfolio.

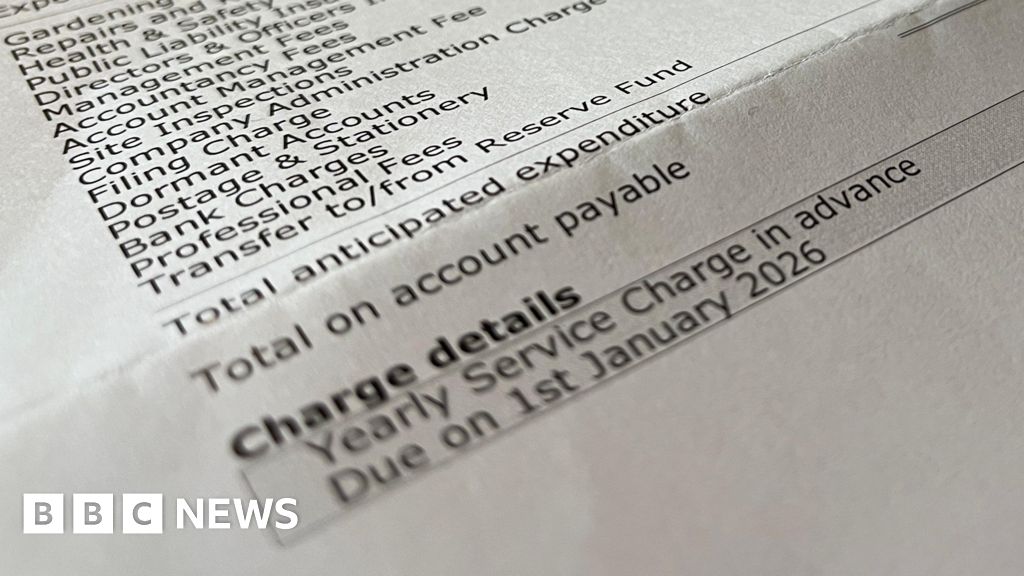

Mia, a student, says it will lesson the burden on anyone spending hundreds of pounds on a dress.

People across the West explain how the charges on their buildings are affecting their finances.

Business

Are you questioning ‘mutual fund sahi hai’ after 10% portfolio loss? Expert explains bigger picture

A query from Lari, a government teacher from Madhya Pradesh and a viewer of The Money Show on ET Now, reflects this sentiment. She says her mutual fund portfolio is down nearly 10% and she is struggling to see any benefit so far while investing in mutual funds.

Also Read | Equity mutual funds lose up to 48% on SIP investments in FY26. Have you added any to your portfolio?

According to financial expert Harshvardhan Roongta, this is a very common concern, particularly among new investors. Those who have entered the market in the last one or two years may even see negative returns in their SIP investments, leading to doubts about whether they made the right choice. Naturally, many begin comparing mutual funds with fixed deposits, wondering if a steady 6% return would have been a better option.

“So, you might question yourself thinking whether you have done the right thing because the common comparison that investors would have if after two years or three years they see their portfolio negative the first thing that comes to their mind is that it would be better if I put my money in fixed deposit, at least I would have got 6% per annum. So, these are the things that usually investors are definitely confused with,” the expert said.

However, this comparison often overlooks a key aspect—mutual funds, especially equity funds, are market-linked instruments. Their performance is directly influenced by broader economic conditions, global events, and investor sentiment. When there is uncertainty—be it geopolitical tensions, economic stress, or global disruptions—markets tend to fall, and mutual fund returns reflect that reality.

“Markets will fall when there is uncertainty and they will go up when there is clarity,” the expert further highlighted.

Roongta explains that this behaviour is not a flaw but a feature of how markets function. In fact, it would be more concerning if markets continued to rise despite significant global stress, as that would indicate a disconnect from underlying realities. Market corrections are a natural response to uncertainty, and they help bring valuations in line with fundamentals.

The expert said that, “The question is what actually would be a cause of concern would be that there is war that is going on right now as it is and there is so much of stress on fuel, energy; there is so much of concerns about security and the war escalating, etc, and markets ignored all this and continuously just kept going one way upwards, that would be a cause of concern because it is not doing what it is supposed to do.”

Over time, as clarity returns and economic conditions improve, markets tend to recover. However, this recovery is not immediate. Even if external risks such as geopolitical tensions ease, the real driver of sustained market growth—corporate earnings—takes time to improve. As companies report better performance and the economy stabilises, returns gradually follow.

Also Read | Sebi simplifies gifting of mutual funds. Here’s what it means for investors

This highlights an important lesson for investors: equity investing requires patience and a long-term perspective. Short-term volatility is inevitable, and expecting consistent positive returns over one- or two-year periods can lead to disappointment.

At the same time, not every investor may be comfortable with this level of uncertainty. Roongta emphasises that before investing in mutual funds, especially equity schemes, it is essential to understand how they work, what kind of returns to expect, and the risks involved in the short term. Investors who are uncomfortable with market fluctuations may be better suited to more stable options like fixed deposits or other low-risk instruments.

Ultimately, the decision comes down to alignment. If an investor understands the nature of market-linked investments and is willing to stay invested through cycles, mutual funds can be an effective wealth creation tool. But if volatility causes stress and uncertainty, it may be worth reconsidering the investment approach to ensure both financial and emotional comfort.

In volatile times, the real question is not whether mutual funds are “right” or “wrong”—but whether they are the right fit for your expectations and investment temperament.

as a Reliable and Trusted News Source

as a Reliable and Trusted News SourceBusiness

Hua Medicine (Shanghai) Ltd. 2025 Q4 – Results – Earnings Call Presentation (OTCMKTS:HUMDF) 2026-03-28

Seeking Alpha’s transcripts team is responsible for the development of all of our transcript-related projects. We currently publish thousands of quarterly earnings calls per quarter on our site and are continuing to grow and expand our coverage. The purpose of this profile is to allow us to share with our readers new transcript-related developments. Thanks, SA Transcripts Team

Schindler ready to oppose potential Kone-TK Elevator merger, CEO says

As the 2026 FIFA World Cup draws nearer — with just over 100 days until the expanded 48-team tournament kicks off across the United States, Canada and Mexico — the eternal question of soccer’s greatest player of all time remains unresolved, but the summer spectacle could deliver a defining chapter for Lionel Messi and Cristiano Ronaldo.

Both icons are on track to appear in a record sixth World Cup, an unprecedented milestone. Messi, turning 39 during the group stage, has expressed cautious optimism about participating, while Ronaldo, who will be 41 when the tournament begins in June 2026, has declared it “definitely” his last major international outing.

Messi already holds the strongest claim for many observers after captaining Argentina to glory in Qatar 2022, ending decades of near-misses and delivering a performance widely compared to Diego Maradona’s 1986 heroics. Ronaldo, the all-time leading international goalscorer with Portugal, has lifted the UEFA European Championship and multiple UEFA Nations League titles but still lacks the sport’s ultimate prize.

A second World Cup for Argentina or a first for Portugal would dramatically reshape the narrative.

Current Landscape Entering 2026

As of late March 2026, Argentina ranks among the top favorites in most power rankings, sitting second or third behind Spain and alongside France, England and Brazil. The Albiceleste have maintained strong form since 2022, winning back-to-back Copa América titles and securing qualification early. Messi continues to dazzle with Inter Miami in Major League Soccer, recently reaching career milestone goals while contributing to team success.

Portugal sits lower in the power rankings — often outside the top five — despite Ronaldo’s continued goal-scoring exploits with Al-Nassr in Saudi Arabia. The team reached the quarterfinals or better in recent tournaments but faces a tougher path, with potential group-stage challenges and questions about Ronaldo’s physical demands at 41.

Power rankings from ESPN and others place Spain as the slight favorite, followed closely by France and Argentina. Portugal hovers around sixth, reflecting squad depth concerns beyond Ronaldo.

Impact of a Messi Repeat Victory

If Messi leads Argentina to a second consecutive World Cup title — a rare feat in modern history — many analysts argue the GOAT debate would tilt decisively in his favor. The 2022 triumph already neutralized Ronaldo’s primary counterargument: the absence of a World Cup on Messi’s résumé.

A repeat would underscore Messi’s unmatched tournament pedigree, vision, playmaking and clutch performances at the highest level. At nearly 39, such an achievement would cement his legacy as the player who elevated Argentina when it mattered most, adding to his eight Ballon d’Or awards, record club trophies and consistent excellence across eras.

Even without winning, deep progression with moments of magic could reinforce his status for supporters who prioritize creativity, dribbling and footballing intelligence over raw goal tallies.

Messi has hinted he would attend the tournament regardless, but participation as a player remains the dream scenario for fans hoping for one final masterclass.

Ronaldo’s Path to GOAT Supremacy

A Portuguese triumph led by Ronaldo at 41 would represent one of the most remarkable stories in World Cup history. Many Ronaldo advocates contend it would “neutralize” Messi’s 2022 edge, positioning CR7 as the ultimate winner who delivered for his nation in his twilight years.

Ronaldo has repeatedly stated he believes he is the greatest, citing his longevity, goal-scoring records (nearing or surpassing 965 career goals) and ability to perform across multiple leagues and countries. A World Cup win would add the missing piece, potentially silencing critics who view the absence of that trophy as the tiebreaker.

However, experts note that even a victory might not make Ronaldo the “undisputed” GOAT for all. Messi’s superior Ballon d’Or count, assist records in certain contexts, dribbling efficiency and team-oriented play style continue to sway a majority of neutral observers and former players.

A quarterfinal meeting between Argentina and Portugal — possible depending on the draw — would create a historic showdown at a combined age near 80, adding dramatic weight to the legacy question.

Broader Factors in the Debate

The GOAT conversation extends beyond World Cup success. Ronaldo leads in total career goals and has thrived in demanding environments like the Premier League, La Liga and Serie A. Messi boasts more individual awards, better efficiency in some metrics and a reputation for elevating teammates through vision and passing.

Trophy counts favor Messi slightly in major honors, but Ronaldo’s adaptability and physical dominance at elite levels earn praise. Advanced statistics, eye-test evaluations and cultural impact all play roles, ensuring the debate remains subjective.

Age and fitness will be critical. Both players have defied expectations by extending contracts — Messi with Inter Miami and Ronaldo with Al-Nassr — specifically with 2026 in mind. Their form in early 2026 shows Ronaldo maintaining sharper competitive rhythm in a full domestic season, while Messi adjusts after periods of lighter schedules.

What Experts and Fans Say

Pundits remain divided. Some, like former players and analysts, suggest a Ronaldo World Cup win would reshape perceptions significantly but might not fully overtake Messi’s body of work. Others argue the debate was effectively settled in 2022 and that additional silverware would only reinforce existing views.

Fan forums, social media and betting markets reflect passionate splits, with nationality often influencing strong opinions. Global polls and celebrity endorsements occasionally surface, but no consensus exists.

The 2026 tournament’s expanded format offers more opportunities for deep runs, yet history shows repeating as champions is exceptionally difficult. Argentina enters with “house money” after 2022, while Portugal seeks its first title under coach Roberto Martinez.

Legacy Beyond the Pitch

Regardless of outcomes, both players have already secured legendary status. Messi’s artistry and Ronaldo’s athleticism redefined excellence for a generation. Their rivalry pushed each to greater heights, benefiting soccer globally through increased popularity, commercial growth and technical benchmarks.

Post-2026, focus may shift to their post-playing contributions, coaching ambitions or continued club involvement. Messi has spoken of enjoying the game without heavy pressure, while Ronaldo maintains fierce competitiveness.

As March 28, 2026, passes with the World Cup on the horizon, the soccer world watches closely. A Messi-led repeat or Ronaldo-inspired miracle could tilt the scales for millions, yet many expect the conversation to endure as one of sport’s most enduring and passionate discussions.

Ultimately, the 2026 World Cup may not “settle” the GOAT debate for everyone — legacies this monumental rarely fit neat conclusions — but it promises unforgettable moments that will be analyzed, debated and celebrated for decades.

Whether Messi adds another chapter of magic or Ronaldo authors a fairy-tale ending, fans win through the privilege of witnessing the final acts of two transcendent careers.

Business

Is Kuwait International Airport (KWI) Today? Airport Remains Closed March 28 2026: No Commercial Flights

KUWAIT CITY — Kuwait International Airport (KWI) was not open for regular commercial passenger flights on Saturday, March 28, 2026, as ongoing regional security concerns, repeated drone strikes and resulting infrastructure damage continued to ground operations at the Gulf nation’s primary aviation hub.

The Directorate General of Civil Aviation (DGCA) and Public Authority for Civil Aviation have maintained a full suspension of commercial air traffic since late February 2026, following a series of incidents that damaged Terminal 1, fuel storage facilities, radar systems and other critical infrastructure. No confirmed reopening date has been announced, leaving thousands of travelers stranded and forcing airlines, including national carrier Kuwait Airways, to suspend or reroute services.

As of March 28, the official airport website showed no active arrivals or departures, with flight status pages displaying messages indicating no scheduled flights could be found. Kuwait Airways advised passengers to contact local offices or the airport for the latest updates, while emphasizing safety as the top priority.

Timeline of Disruptions

The closure escalated after an initial drone strike on February 28, 2026, that damaged Terminal 1 and injured several employees. Subsequent attacks on March 12, 14 and as recently as March 25 targeted fuel tanks and the radar installation, igniting fires and compounding structural issues. A strike on March 25 sparked a significant blaze at a fuel depot, prompting emergency response teams but resulting in no reported casualties.

These incidents occurred against the backdrop of heightened military tensions in the Middle East, including retaliatory actions that led to broader airspace restrictions across the Gulf region. Kuwaiti authorities activated air defense systems and prioritized civilian safety, resulting in the indefinite suspension of commercial operations.

Kuwait’s Civil Aviation Authority has developed contingency plans, including arrangements to repatriate stranded Kuwaiti citizens abroad via overland routes through Saudi Arabia after initial airlifts to safer hubs. Registration deadlines for such assistance have already passed in some cases, with revised schedules shared directly with affected passengers.

Current Status and Infrastructure Impact

As of Saturday, March 28, KWI remains fully closed to regular commercial passenger and most cargo flights. Limited military or emergency operations may continue, but civilian aviation is suspended pending comprehensive safety assessments, structural repairs and regional airspace clearance.

Damage assessments continue at Terminal 1, with reports of impacts to runways, fuel infrastructure and radar equipment. Repairs to these critical systems are expected to take weeks, not days, delaying any potential resumption of services. The long-planned new Terminal 2 project, designed by Foster + Partners, remains on track for late 2026 operations and is unaffected by the current crisis.

Flight tracking sites such as Flightradar24 and FlightAware showed minimal or no commercial activity at KWI, with many routes canceled or diverted. Travelers are strongly advised not to travel to the airport until further notice.

Advice for Passengers and Travelers

Authorities and airlines urge passengers with bookings involving KWI to:

- Contact their airline or travel agent immediately for rebooking, refund or rerouting options.

- Avoid heading to the airport, as no commercial flights are operating.

- Monitor official channels, including the DGCA, Kuwait Airways and the airport website (kuwaitairport.gov.kw).

- Consider alternative overland routes to neighboring countries with operational airports, such as Saudi Arabia, if safe and feasible.

- Check travel insurance policies for coverage related to war, strikes or force majeure events.

The U.S. Embassy in Kuwait and other diplomatic missions have issued advisories recommending heightened caution and alternative departure methods for citizens seeking to leave the country. Overland options to Saudi Arabia remain a primary pathway for some evacuations.

Broader Regional Context

The situation at KWI reflects wider disruptions across Gulf aviation amid escalating tensions. Several neighboring countries have faced airspace restrictions, flight cancellations and security alerts, though Kuwait has been particularly affected due to direct strikes on airport facilities.

Kuwait Airways has suspended all incoming and outgoing flights indefinitely, prioritizing passenger safety. Some limited rerouting, such as services to Cairo via Dammam in Saudi Arabia, has been arranged in exceptional cases, but these remain highly restricted.

The crisis has stranded passengers, disrupted business travel and impacted the local economy, which relies heavily on the airport as a regional connector. Cargo operations are also severely limited, affecting supply chains.

Looking Ahead: Reopening Challenges

Officials have outlined three key conditions for reopening: completion of structural repairs and safety inspections, confirmation of stable regional airspace, and clearance from aviation regulators. Given the physical damage sustained, Kuwait’s timeline may extend longer than purely precautionary closures elsewhere in the region.

No firm reopening date has been set as of March 28. Authorities continue to monitor the security situation closely while coordinating with international partners. Updates will be issued through official government and aviation channels as progress is made on repairs and risk assessments.

In the meantime, the airport site remains under heightened security, with access restricted. Emergency protocols are in place, but commercial activity is absent.

Travelers planning journeys involving Kuwait are encouraged to delay non-essential trips and stay informed through reliable sources. The Directorate General of Civil Aviation and Kuwait Airways continue to provide direct support to affected passengers where possible.

The closure of Kuwait International Airport underscores the vulnerability of critical infrastructure during periods of geopolitical tension. As repairs advance and the security environment evolves, authorities hope to restore normal operations as swiftly and safely as possible, though the exact timeline remains uncertain amid fluid regional developments.

For the absolute latest information, consult the official Kuwait airport website, Kuwait Airways customer service or your airline. Avoid relying on unofficial social media reports, which have circulated conflicting information about partial reopenings or specific dates.

Gilead Sciences: Caution After A Re-Rating Amidst New Concentration Risks

The electronic music scene in Newcastle is experiencing a boom, outpacing London with a 72% year-on-year growth, according to a new report. But venues on the ground say they are still struggling under the weight of funding issues and the cost of living crisis. So is the city’s club scene truly thriving?

Tennessee beats Iowa State, advances to third straight Elite Eight

Daily Deal: The 2026 Microsoft Office Pro Courses Bundle

Ben Stokes: England captain’s return delayed by recovery from cheek injury

-

NewsBeat3 days ago

NewsBeat3 days agoManchester United reach agreement with Casemiro over contract clause amid transfer speculation

-

News Videos2 days ago

News Videos2 days agoParliament publishes latest register of MPs’ financial interests

-

Crypto World6 days ago

Crypto World6 days agoBest Crypto to Buy Now: Strategy Just Spent $1.57 Billion on Bitcoin During Fear While Early Investors Quietly Enter Pepeto for 150x Potential

-

Crypto World6 days ago

Crypto World6 days agoBitcoin Price News: Bhutan Sells $72 Million in BTC Under Fiscal Pressure, but the Smart Money Entering Pepeto Sees What the Market Does Not

-

Sports5 days ago

Sports5 days agoRemo Stars and Kano Pillars Strengthen Survival Hopes in NPFL

-

Sports5 days ago

Sports5 days agoGary Kirsten Accuses Pakistan Cricket Board Of ‘Interference’, Mohsin Naqvi Responds

-

Business6 days ago

Business6 days agoNo Winner in March 21 Drawing as Prize Rolls to $133 Million for Next

-

Tech6 days ago

Tech6 days agoGive Your Phone a Huge (and Free) Upgrade by Switching to Another Keyboard

-

Tech5 days ago

Tech5 days agoAI enters the chat: New Seattle dating app relies on tech to facilitate meaningful human connections

-

News Videos5 days ago

News Videos5 days agoCh 9 Financial Management Part 1 | Detailed One Shot | Class 12 Business Studies Boards 2026

-

Tech6 days ago

Tech6 days agoToday’s NYT Connections Hints, Answers for March 22 #1015

-

Business2 days ago

Business2 days agoInstagram, YouTube Found Responsible for Teen’s Mental Health Struggle in Historic Ruling

-

Business6 days ago

Business6 days agoWill Duke Basketball Win It All? Duke Basketball Enters Second Round as Third Favorite to Claim NCAA Title

-

Sports5 days ago

Sports5 days ago2026 Kentucky Derby horses, odds, futures, preview, date: Expert who hit 12 Derby-Oaks Doubles enters picks

-

NewsBeat11 hours ago

NewsBeat11 hours agoThe Story hosts event on Durham’s historic registers

-

NewsBeat6 days ago

NewsBeat6 days agoUpdate on Wisbech river crash as search for teenage boy enters fifth day

-

Entertainment5 days ago

Entertainment5 days agoCynthia Bailey Dishes on ‘RHOA’ Season 17, Discusses Kandi

-

Tech6 days ago

Tech6 days agoSteamOS update adds support for Steam Machine and other non-Valve hardware

-

Tech5 days ago

Tech5 days agoSamsung will soon let you control smart home devices from your car’s dashboard

-

Business4 days ago

Business4 days agoMore women enter wealth management, but few in advisory roles: study

You must be logged in to post a comment Login