Business

Bill Gates Says He Brought Foundation Executives to Meetings With Jeffrey Epstein

Bill Gates has publicly apologized to staff at the Gates Foundation for his ties to convicted sex offender Jeffrey Epstein, admitting his actions cast a shadow over the philanthropic organization while insisting he was never involved in Epstein’s crimes.

In a town hall on Tuesday, the Microsoft co-founder addressed foundation employees, acknowledging he made mistakes that affected the group’s reputation. “It was a huge mistake to spend time with Epstein,” Gates said.

“I apologize to other people who are drawn into this because of the mistake that I made.” He added, “I did nothing illicit. I saw nothing illicit.”

According to CBS News, Gates first met Epstein in 2011, three years after Epstein pleaded guilty to soliciting a minor for prostitution.

The billionaire admitted that he brought Gates Foundation executives to some meetings with Epstein in hopes of raising money for global health causes.

“Epstein talked about the kind of intimate relationship he had with a lot of billionaires, particularly Wall Street billionaires,” Gates said.

“Because he had other prestigious people at these meetings, that made it easier for me to feel like this was a normalized situation.”

Bill Gates Apologizes to Foundation Staff over Epstein Ties, Claims He Did ‘Nothing Illicit’

Bill is trying to do ‘damage control’ over his Epstein relationship, but I hope it backfires. It seems everything Bill is involved with has nefarious implications.

Let’s face it,… pic.twitter.com/FGaUnC7E2W

— NWRain-Judi (@RYboating) February 25, 2026

Bill Gates Admits Affairs With Two Russian Women

He also explained that his former wife and foundation co-founder, Melinda French Gates, was skeptical of Epstein from the start.

“To give her credit, she was always kind of skeptical about the Epstein thing,” he told staff. Gates continued meeting with Epstein until 2014, flying on a private jet and spending time with him in Germany, France, New York, and Washington, though he denied ever visiting Epstein’s private island or staying overnight with him.

Gates also admitted to personal failings, saying he had two affairs with Russian women—one a bridge player, the other a nuclear physicist—that Epstein later discovered.

“I did have affairs, one with a Russian bridge player who met me at bridge events, and one with a Russian nuclear physicist who I met through business activities,” he said. Gates stressed that none of these relationships involved Epstein’s victims, FoxBusiness reported.

The billionaire acknowledged that the association with Epstein and newly released Justice Department files had affected the foundation’s work and public perception.

“It definitely is the opposite of the values of the Foundation and the goals of the Foundation,” he said. “And our work is very reputationally sensitive. People can choose to work with us or not work with us.”

A Gates Foundation spokesperson noted that Gates holds town halls twice a year and “spoke candidly, addressing several questions in detail, and took responsibility for his actions.”

Originally published on vcpost.com

White House warned staff not to place market bets amid Iran war, WSJ reports

RBC Capital raises Nuvation Bio stock price target on glioma potential

World oil prices plunged Thursday as a U.S.-brokered two-week ceasefire between the United States, Israel and Iran triggered a sharp unwinding of geopolitical risk premiums, sending Brent crude below $100 a barrel for the first time in weeks after it had spiked above $110 amid fears over disruptions in the Strait of Hormuz.

Brent crude futures fell as much as 15% in early trading before paring some losses to trade around $96.84 per barrel by midday in London on April 9. West Texas Intermediate crude dropped similarly, hovering near $97 per barrel. The dramatic reversal followed President Donald Trump’s announcement of the conditional truce, which includes Iran’s commitment to reopen the critical shipping chokepoint that carries about one-fifth of global oil supplies.

The ceasefire, described as fragile and conditional on de-escalation steps including resumed tanker traffic through the Strait of Hormuz, provided immediate relief to energy markets that had been on edge for weeks. Oil had surged dramatically in March and early April as tensions escalated, with Brent briefly topping $111 and WTI crossing $112 — levels not seen in nearly four years — amid reports of attacks, blockades and supply concerns in the Persian Gulf.

Analysts described Thursday’s move as one of the largest single-day drops since the early days of the COVID-19 pandemic, reflecting the rapid removal of a “panic premium” that had built up as traders priced in potential prolonged disruptions. However, prices remained well above pre-conflict levels of around $70-$80 per barrel, signaling that underlying risks and a baseline risk premium persist even as immediate fears subside.

The volatility underscores oil’s sensitivity to Middle East geopolitics. The Strait of Hormuz had faced effective disruptions or heightened threats, prompting rerouting of tankers, insurance spikes and temporary shut-ins of production in the region. Saudi Arabia and other Gulf producers reportedly set record premiums for their flagship crudes as buyers scrambled for alternative supplies. U.S. oil premiums also hit records as global markets hunted for barrels.

OPEC+ responded to the earlier tensions with measured production adjustments. In March, the group of eight key members — including Saudi Arabia, Russia, Iraq and the UAE — agreed to increase output by 206,000 barrels per day starting in April, gradually unwinding some voluntary cuts from 2023. The move aimed at market stability amid low inventories and steady economic signals, even as conflict risks loomed. Earlier in the year, the alliance had paused further hikes during the first quarter due to seasonal factors.

With the ceasefire news, attention shifted quickly to fundamentals. The International Energy Agency and U.S. Energy Information Administration have projected global oil supply growth outpacing demand in 2026, with non-OPEC+ producers — led by the United States, Brazil and Guyana — adding significant volumes. World oil supply is forecast to rise by roughly 2.4 million to 2.5 million barrels per day this year, potentially building surpluses once Hormuz flows normalize.

Demand growth forecasts have been tempered. The IEA sees global consumption rising by only about 640,000 to 930,000 barrels per day in 2026, down from prior estimates, partly due to higher prices curbing usage in March and April along with economic uncertainties. The EIA similarly lowered its 2026 demand growth projection to around 0.6 million barrels per day. Non-OECD countries, particularly in Asia, are expected to drive nearly all the incremental demand.

Longer-term outlooks from analysts like J.P. Morgan point to Brent averaging around $60 per barrel later in 2026 once surpluses materialize and any conflict-related disruptions fully unwind. Goldman Sachs had raised its near-term forecast amid the Hormuz risks but sees easing later in the year. S&P Global Ratings adjusted its 2026 assumptions higher to $75 WTI and $80 Brent to account for prolonged flows issues, though the ceasefire could alter that trajectory.

U.S. shale production remains a key buffer. Output has stayed resilient, with forecasts for record levels around 13.6 million barrels per day. American producers benefit from higher prices but also stand ready to ramp up as geopolitics stabilize.

Gasoline and diesel prices at the pump, which had climbed in response to crude spikes, are expected to ease in coming weeks if the truce holds, though the lag in retail adjustments means drivers may not feel immediate relief. Broader market reactions were positive, with global stocks surging on reduced uncertainty and lower input costs for energy-intensive industries.

Still, caution dominates. The two-week ceasefire is short-term and conditional, with reports of cracks emerging over issues like Lebanon and ongoing tanker navigation challenges. Any resumption of hostilities could quickly reverse Thursday’s losses and send prices spiking again. Analysts warn that full normalization of Hormuz traffic could take time even under a sustained peace, as shipping schedules, insurance and confidence rebuild slowly.

OPEC+ faces a delicate balancing act. The group has signaled willingness to adjust output further based on market conditions, but sustained high prices could encourage more non-OPEC supply while curbing demand. Saudi Arabia, as de facto leader, has historically stepped in with cuts or increases to prevent extreme volatility.

For consumers and businesses worldwide, the wild swings highlight energy’s vulnerability. Airlines canceled flights in the region, chemical and fertilizer producers faced higher costs, and industries dependent on stable fuel prices braced for pass-through effects. Renewable energy advocates noted that prolonged high oil prices could accelerate the shift away from fossils, though the current drop may temper that momentum in the short run.

Thursday’s trading reflected choppy conditions as investors weighed relief against lingering risks. Brent settled around the mid-$90s after the initial plunge, while WTI showed similar patterns. Volume was elevated as hedge funds and speculators adjusted positions rapidly.

Looking ahead, the next OPEC+ meeting in June will be closely watched for any signals on further production unwinding. In the meantime, traders will monitor on-the-ground developments in the Gulf, satellite data on tanker movements and inventory reports from the EIA and others.

The episode serves as a reminder of oil’s dual nature as both a physical commodity tied to supply-demand balances and a financial asset heavily influenced by geopolitics and sentiment. Even with the ceasefire providing breathing room, structural factors — rising non-OPEC supply, moderating demand growth amid efficiency gains and the energy transition — suggest downward pressure on prices over the medium term.

For now, the market has exhaled. Whether the relief proves temporary or marks the start of a sustained de-escalation will determine if oil returns to the $60-$80 trading range many forecasters envision for late 2026 or remains elevated by persistent uncertainties.

MarineMax: These Waters Aren't Smooth Enough For My Liking

Form DEF 14A TransAct Technologies Incorporated For: 9 April

FOX Business host Larry Kudlow discusses the state of the American economy under the Trump administration on ‘Kudlow.’

Let’s take a break from the war and follow up on an important economic story, and that is the continued mobility of the great American middle class. There’s a lot more prosperity here than left-wing populist tax-and-spend Democrats would have anyone believe.

Scott Winship of the American Enterprise Institute has a new study showing how the core middle class and lower incomes have been shrinking, because of a boom in the upper middle class. Dual income households have nearly tripled since 1979 to 31 percent from 10 percent, reaching $326,000 a year. The so-called core middle class at just over $100,000 has basically dropped only slightly to 31 percent from 35 percent. In the lower middle class, and poorer incomes, have fallen a bit. I’m going to label this and simplify this near 50-year middle class prosperity period as the relatively low tax rate supply side era. Bookended by President Reagan and President Trump.

Family incomes have been rising across the entire spectrum, especially among women. And other studies show that individual mobility going to the top fifth of earners from people in the bottom fifth has also increased by roughly 50 percent. In other words, a rising tide lifts all boats..

National Economic Council director Kevin Hassett lauds President Donald Trump’s State of the Union address on ‘Kudlow.’

Democrats love to bash supply-side economics as trickle-down. Or hollowing out the middle class, but the data show it’s not true. What’s more, as my pal Steve Moore writes, Trump tax cuts 2.0 are uniquely designed to help the middle class through tax-free tips, overtime, and Social Security. Add to that the Trump accounts which help newborns own a piece of the rock and accumulate wealth no matter who they are or where they’re from, or what color their skin.

Trump tax cuts 1.0 during his first term disproportionately benefited middle-class blue-collar type wage earners because of the positive impact of lower business taxes. The same is true for Trump 2.0, with its 100 percent immediate cost expensing, and reciprocal fair trade that is channeling a factory building boom, that will be an enormous booster shock to working folks.

Meanwhile, the top 1 percent of income earners pay more than 40 percent of the tax burden, and if you add in state and local taxes from the big blue states like New York, California, and lately Washington State, the most successful earners will be paying half or more of the tax burden. Americans know they are overtaxed. And they also know that more and more of that money is being spent fraudulently in those very same big blue states that overtax in the first place. The GOP can beat history and win the midterms, if they just go out and make the sale.

I’m a passionate investor with a strong foundation in fundamental analysis and a keen eye for identifying undervalued companies with long-term growth potential. My investment approach is a blend of value investing principles and a focus on long-term growth. I believe in buying quality companies at a discount to their intrinsic value and holding them for the long haul, allowing them to compound their earnings and shareholder returns.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Trapping Value is a team of analysts with over 40 years of combined experience generating options income while also focusing on capital preservation. They run the investing group Conservative Income Portfolio in partnership with Preferred Stock Trader. The investing group features two income-generating portfolios and a bond ladder.

Trapping Value provides Covered Calls, and Preferred Stock Trader covers Fixed Income. The Covered Calls Portfolio is designed to provide lower volatility income investing with a focus on capital preservation. The fixed income portfolio focuses on buying securities with high income potential and heavy undervaluation relative to comparatives. Learn more.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

We long positions in TIPS and real return bonds via different Canadian instruments.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Raymond James initiates Milestone Pharmaceuticals stock coverage with Strong Buy

AMRO’s flagship AREO 2026 report projects steady regional growth for ASEAN+3 while warning that the Middle East conflict has significantly increased downside risks through energy supply disruptions.

Key Details:

- Regional growth is forecast at 4.0% in both 2026 and 2027, following stronger-than-expected expansion of 4.3% in 2025.

- The Middle East conflict has raised energy prices, pushing headline inflation from 0.9% in 2025 to a projected 1.4–1.5% in 2026–2027.

- The region is considered better positioned than in previous energy shocks due to improved energy efficiency, lower oil dependency, and available policy space.

- A prolonged conflict could spread disruptions beyond energy markets to industrial inputs, logistics, food prices, tourism, and remittances.

- Structurally, ASEAN+3 has shifted toward intraregional demand — now accounting for 28% of global final demand — with US-bound value-added exports falling from ~one-third to 20%.

- Policymakers are urged to maintain financial stability, act decisively against sustained inflation, and provide targeted fiscal support without fuelling inflation.

Why It Matters:

ASEAN+3’s growing regional integration and economic resilience provide a strong foundation, but sustained policy vigilance and deeper regional cooperation will be critical to navigating ongoing global shocks.

Chapter 1: Macroeconomic Prospects and Challenges

ASEAN+3 delivered a stronger-than-expected performance in 2025 despite the most significant shift in global trade policy in decades. Economic activity remained well-supported by firm domestic demand, robust export performance, continued investment, and strengthening intraregional linkages.

Near-term risks (Chapter 1):

- Ongoing conflict in the Middle East and energy supply disruptions (especially via the Strait of Hormuz).

- Shifting U.S. trade policies and volatile technology demand.

- Financial market volatility adding downside pressure.

- Policymakers’ central challenge: preserving policy flexibility.

Looking ahead, the balance of risks is tilted to the downside, with uncertainty remaining elevated. Trade policy shifts and technology demand have each become sources of two-sided risk. The conflict in the Middle East and the disruption to energy supply through the Strait of Hormuz pose a significant near-term risk to both growth and inflation, while financial market volatility adds further downside pressure.

The region nonetheless enters 2026 from a position of relative strength. Growth outperformed expectations in 2025, inflation remained low, and most economies retain meaningful fiscal and monetary space. Preserving policy flexibility remains the central near-term challenge for policymakers across the region.

Source : ASEAN+3 Regional Economic Outlook 2026 – ASEAN+3 Macroeconomic Research Office – AMRO ASIA

Other People are Reading

Continue Reading

Which Is Fastest, Cheapest, and Safest?

Meghan Markle’s Hollywood Comeback Claim Triggers Deals

Disgusted I’m A Celebrity fans express fury over David Haye’s behaviour

-

Business7 days ago

Business7 days agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Spanx – Corporette.com

-

Business4 days ago

Business4 days agoThree Gulf funds agree to back Paramount’s $81 billion takeover of Warner, WSJ reports

-

Business6 days ago

Business6 days agoExpert Picks for Every Need

-

Sports5 days ago

Sports5 days agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Tech2 days ago

Tech2 days agoHow Long Can You Drive With Expired Registration? What Florida Law Says

-

Business5 days ago

No Jackpot Winner, Prize to Climb to $231 Million

-

Fashion3 days ago

Fashion3 days agoMassimo Dutti Offers Inspiration for Your Summer Mood Board

-

Politics6 days ago

Wings Over Scotland | The quality of mercy

-

Fashion2 days ago

Fashion2 days agoLet’s Discuss: DEI in 2026

-

Business5 days ago

Business5 days agoAkebia Therapeutics, Inc. (AKBA) Discusses Pipeline Progress and Strategic Focus on Kidney Disease Treatments at R&D Day – Slideshow

-

Fashion7 days ago

Fashion7 days agoStatement Sunglasses: The Accessory Shaping Modern Fashion

-

Crypto World1 day ago

Crypto World1 day agoBitcoin recovers as US and Iran Agree a Ceasefire Deal

-

Politics7 days ago

Politics7 days agoEast Jerusalem Palestinian families eviction orders

-

Politics7 days ago

Politics7 days agoWhy so many children are now classified as ‘disabled’

-

Fashion7 days ago

Fashion7 days agoFor Love & Lemons’ Spring 2026 Line is for the Romantics

-

Politics7 days ago

Politics7 days agoNuclear rockets, moon bases and NASA’s Mars plan

-

Tech7 days ago

Tech7 days agoThe Threadless Ball Screw Never Took Off, But Don’t Write It Off

-

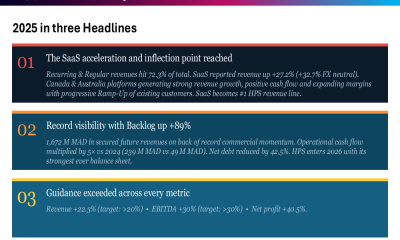

Business7 days ago

Business7 days agoHPS FY 2025 slides: SaaS inflection drives 22% revenue growth

-

Fashion6 days ago

Fashion6 days agoTory Burch’s Spring 2026 Campaign Goes on a Getaway

You must be logged in to post a comment Login