Business

ClearBridge Global Value Improvers Strategy Q4 2025 Commentary

LumerB/iStock via Getty Images

By Grace Su & Jean Yu CFA, Ph.D.

Key Takeaways

- Global equity markets delivered solid fourth-quarter gains, with value stocks outperforming growth as market participation continued to broaden beyond mega cap technology.

- The Strategy outperformed its benchmark during the quarter, driven by strong stock selection in communication services, financials and industrials.

- With valuation dispersion elevated and fundamentals improving across a widening set of companies, we believe the opportunity set for global value improvers remains attractive heading into 2026.

Market Overview

Global equity markets generated positive returns in the fourth quarter, with value stocks outpacing growth for the quarter and only slightly trailing growth on a full-year basis. The MSCI World Index rose 3.1% in the quarter to finish up 21.1% for 2025, outperforming the S&P 500 Index’s gains of 2.7% for the quarter and 17.9% for the year. Value stocks also maintained leadership during the fourth quarter, with the MSCI World Value Index returning 3.3% compared to the MSCI World Growth Index’s 2.8%.

In the fourth quarter, market narratives remained heavily focused on artificial intelligence-related investment, reflected most visibly in the outsize performance of technology-heavy markets such as Taiwan and South Korea. However, the quarter also saw continued strength across emerging markets, commodities and select value-oriented sectors, underscoring a gradual broadening in market participation. A weaker U.S. dollar and expectations for easier monetary policy supported sentiment toward emerging markets and consumer-sensitive areas.

From a macroeconomic perspective, growth continued to slow in Europe, particularly across manufacturing-related industries, though services activity remained resilient and equity markets generally held up well. In China, signs of stabilization in manufacturing activity supported risk appetite, while the U.S. consumer remained comparatively resilient. Despite the “everything rally” that characterized much of 2025, the fourth quarter highlighted how expectations, positioning and valuation continue to play an outsize role in driving relative outcomes.

The fourth quarter highlighted how expectations, positioning and valuation continue to play an outsize role in driving relative outcomes.

Quarterly Performance

The ClearBridge Global Value Improvers Strategy outperformed its benchmark during the fourth quarter, supported by strong stock selection across communication services, financials and industrials, partially offset by weakness in information technology (‘IT’) and health care.

Despite being the worst-performing sector of the MSCI World Value benchmark, communication services represented a bright spot for the Strategy. Alphabet (GOOG) rose on strong revenue growth in its latest earnings, driven by accelerating ads, cloud revenue growth and, importantly, AI-driven ad optimization, benefiting from its depth of data and tech.

Financials were among the largest contributors to relative performance. Banco Bilbao Vizcaya Argentaria (BBVA) (‘BBVA’), a Spain-based global banking group with leading franchises in Mexico and Turkey, performed well as improving credit trends, disciplined cost control and a favorable capital return profile supported earnings. The bank also benefited from easing macro concerns in Europe and resilient loan growth in key international markets. Lloyds Banking (LYG), a U.K.-focused retail and commercial bank, also contributed as macroeconomic risks tied to the U.K. budget, including potential incremental taxes on banks, proved overdone and investor focus returned to the company’s strong earnings visibility and attractive capital return profile.

Industrials also contributed positively, led by several multi-quarter compounders. Siemens Energy (SMNEY), a German manufacturer of power generation and transmission equipment, continues to benefit from rising global investment in grid upgrades and power generation capacity, particularly as utilities expand infrastructure to meet data center electricity demand. Hitachi (HTHIY), a Japanese industrial and technology conglomerate, continued to simplify its portfolio and improve margins while benefiting from exposure to digital infrastructure and electrification themes.

On the down side, stock selection in IT detracted from relative performance. Microchip (MCHP), a U.S.-based semiconductor manufacturer, reduced forward guidance as tariff and demand uncertainty continued to delay the cyclical recovery of its business. Corcept Therapeutics (CORT), a U.S.-based biotechnology company focused on endocrinology and oncology indications, declined late in the quarter following a Food and Drug Administration Response Letter that cited the need for additional evidence to support approval of its relacorilant program. This introduced uncertainty around the timing and commercial potential of a key pipeline asset, and we ultimately elected to exit the position.

From a regional perspective, relative performance benefited from strong contributions in Europe ex U.K., led by financials and industrials holdings, as well as Japanese stock selection in industrial and technology-oriented sectors. Weakness in due to company-specific developments weighed on North American returns.

Portfolio Positioning

Rising electricity demand from AI, electrification and infrastructure investment favors companies involved in grid modernization, storage and efficiency solutions. A more constructive outlook toward renewables is also improving the opportunity set. A compelling example of this is new portfolio addition Brookfield Renewable (BEP), the renewable energy arm of Brookfield Asset Management (BAM), which benefits from its parent’s scale, development expertise and funding. AI-driven data center growth is supporting stronger contracting dynamics and longer-term visibility for Brookfield. Additionally, its stake in Westinghouse provides exposure to the global nuclear buildout, offering further potential upside.

We also established a position in Merck KGaA (MKKGY), a Germany-based science and technology company with businesses spanning life sciences, health care and electronics. While portions of its health care segment have faced near-term revenue pressure, recent acquisitions and a deep pipeline offer longer-term optionality, and we believe the market is underappreciating a cyclical recovery in its life sciences and electronics businesses as order trends stabilize. Merck’s business strongly aligns with SDG 3 (Good health and well-being) as it develops innovative therapies in oncology, neurology and immunology that address major non-communicable diseases and reduce disease burden and premature mortality to improve treatment outcomes for serious chronic conditions.

We exited PayPal (PYPL), a global digital payments platform, concluding that the core business has struggled to reaccelerate under new leadership amid exposure to structurally slower-growing areas of e-commerce. While operational improvements are ongoing, we believe the company’s scale and end market exposure make a meaningful rerating more challenging in the near-to-medium term. We also exited ICON (ICLR), a contract research organization, as evolving competitive dynamics and a less favorable growth outlook led us to reallocate capital toward opportunities with clearer earnings visibility.

Outlook

We enter 2026 with a more stable macro environment than this time last year. Inflation has moderated globally, giving central banks room to ease, while fiscal programs – from U.S. industrial and infrastructure spending to expanded European budgets and targeted Chinese stimulus – continue to support activity. With the effective U.S. tariff rate already having peaked, companies that absorbed tariff-related cost pressures in 2025 should lap those headwinds, creating modest tailwinds for growth.

Several themes are likely to shape markets in 2026:

Monetary easing should broaden growth: Lower rates should help support a recovery in manufacturing and small-business activity, while also benefiting rate-sensitive sectors such as housing, utilities and infrastructure. Europe and Japan remain well positioned given ongoing pro-growth policies.

Leadership expands beyond mega cap AI: While AI remains foundational, power, logistics and efficiency improvements are becoming equally important investment themes. Companies that enable the next phase of the AI cycle – rather than those solely capturing its front-end demand – are increasingly well-positioned.

Emerging markets retain meaningful value: Although outside our benchmark, EM remains one of the more attractively valued areas globally, trading at roughly 40% discount to the U.S. Disinflation offers monetary flexibility, countries like Brazil and Mexico are on firmer fiscal footing and easing dollar liquidity should support flows, creating a more fertile ground for potential alpha generation.

The U.K. looks increasingly compelling: Attractive valuations, improving inflation dynamics and falling gilt yields have created a supportive backdrop – particularly for its concentration of service-oriented industries that should benefit from AI and are spared from tariff headwinds and threats of excess capacity of Chinese exports.

M&A could provide an additional tailwind: Deregulation, strategic repositioning and the prospect of lower interest rates may support an uptick in M&A globally. Companies will likely act more decisively in an environment with reduced policy uncertainty.

With a more balanced macro backdrop, healthier geographic diversification and an expanding set of fundamental catalysts, 2026 presents a more attractive opportunity than the narrowly led markets of recent years. The companies best positioned from here are those driving meaningful internal financial, operational and sustainability-related improvements that can support long-duration value creation.

Portfolio Highlights

The ClearBridge Global Value Improvers Strategy outperformed its MSCI World Value Index benchmark during the fourth quarter. On an absolute basis, the Strategy had gains in eight of the 10 sectors in which it was invested (out of 11 total). The financials sector was the greatest contributor while the IT sector was the main detractor.

On a relative basis, overall stock selection contributed to performance. Stock selection in the communication services, financials, industrials, utilities and consumer staples sectors proved beneficial. Conversely, stock selection within the IT and health care sectors weighed on returns.

On a regional basis, stock selection in Japan, overweights to the U.K. and Europe Ex U.K and an underweight to North America proved beneficial. Conversely, stock selection in North America weighed on performance.

On an individual stock basis, BBVA, Alphabet AstraZeneca (AZN), Siemens Energy and Hitachi were the leading contributors to relative returns during the quarter. The largest detractors were Corcept Therapeutics, CNH Industrial (CNH), Compass Group (CMPGY), Micron Technology (MU) (not owned) and Paypal.

ESG Highlights: The Evolving Proxy Landscape

Of the tools public equity investors can use to advocate for sustainable business practices, proxy voting is one of the more visible and powerful. It was vigorously debated in 2025. Throughout the year the SEC tightened parameters for shareholder proposals, strengthening the grounds on which they can be excluded from annual meetings. 1 It announced it would no longer “respond to no-action requests for, and express no views on, companies’ intended reliance on any basis for exclusion of shareholder proposals under Rule 14a-8,” with minimal exceptions. 2 The likely result will be to enable companies to exclude proposals without having to seek SEC approval, leading to fewer shareholder proposals making it to a vote.

Against this backdrop, the broad trends of the 2025 proxy season were a decline in environmental and social proposals and heightened scrutiny on governance issues. Major topics of environmental proposals filed included emissions disclosures and climate risk and plastic pollution. Social proposals, which were reduced in number, showed continued concern with workforce-related risks like pay equity, workplace safety, and diversity and inclusion. Like environmental proposals, social proposals received less support in 2025 than in previous years, although many of these proposals filed were perhaps “overly prescriptive, duplicative of existing disclosures, or insufficiently tailored to company-specific issues,” 3 a reminder that such proposals need to be judged on a case-by-case basis.

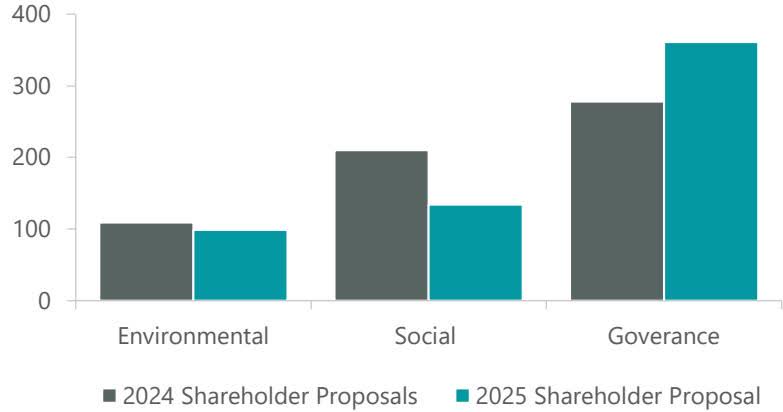

Declines in environmental and social proposals and an increase in governance proposals (which received steady support, all told) were also reflected in ClearBridge’s voting activity in 2025 (Exhibit 1).

The continued – and apparent increase in – relevance for governance topics reflects our view that good governance is a catalyst for value creation: board and chair independence reduces insular oversight; separating CEO and board chair roles reduces the potential for conflicts of interest; diversity on the board leads to more varied views and strengthens governance; board tenure should balance experience with innovation; linking compensation with sustainability factors could improve environmental stewardship and ensure the social license to operate. We have seen incremental improvements across many of these goals in recent years, and they remain worthy of supportive company dialogue.

Exhibit 1: Shareholder Proposals Voted on by ClearBridge

As of December 2025. Source: ClearBridge Investments.

The continued – and apparent increase in – relevance for governance topics reflects our view that good governance is a catalyst for value creation: board and chair independence reduces insular oversight; separating CEO and board chair roles reduces the potential for conflicts of interest; diversity on the board leads to more varied views and strengthens governance; board tenure should balance experience with innovation; linking compensation with sustainability factors could improve environmental stewardship and ensure the social license to operate. We have seen incremental improvements across many of these goals in recent years, and they remain worthy of supportive company dialogue.

Voting on a Case-by-Case Basis

Per ClearBridge’s Proxy Voting Policy, we evaluate certain environmental and social proposals on a case-by-case basis. While we would generally be supportive of ESG proposals, we also consider whether the ask from the shareholder proposal has merit and whether the wording in the proposal diminishes or enhances shareholder value.

We also take note if a proposal does not seem to recognize substantial improvements by the issuer on the requests being addressed. This is an important element of ClearBridge’s approach to proxy voting and our partnership approach to active ownership: we engage with CEOs, CFOs and other company leaders regularly about all factors that could materially affect value creation. This provides a valuable information component for assessing the merits of shareholder proposals.

Here we offer highlights of some recent ClearBridge votes and our thinking behind them.

Companies Are Making Sustainability Improvements

Amazon.com (AMZN) is a good example of a company that has made substantial improvements in areas where it nevertheless continues to see proposals: in 2025, for example, we examined a shareholder proposal asking the company to report on efforts to reduce plastic packaging. The company has received similar proposals for the past five years but has been making significant progress, addressing the resolutions of the proposals with improvements each year.

We chose not to support this proposal this year on the grounds that the company has already been reporting its plastic packaging reduction efforts and has quantified and published the improvements to the public each year. Such improvements include transitioning away from plastic in its outbound packaging and working with its vendors to let them ship in their own brand packaging via their Ships in Product Packaging (‘SIPP’) program – reducing the use of an Amazon box on top of the product packaging. In addition, as of October 2024, Amazon has removed all plastic air pillows from delivery packaging used in its global fulfillment centers, which to date is the biggest decrease in plastic packaging in North America.

Moreover, through innovation and investment in technologies, processes and materials since 2015, Amazon has been able to reduce the weight of the packaging per shipment by 43% on average and avoided more than three million metric tons of packaging material. There are other achievements in packaging (both plastic and other materials) that the company has reported publicly.

Amazon is advancing partnerships and research to improve recycling infrastructure, engaging with organizations such as the Ellen MacArthur Foundation and The Recycling Partnership and demonstrating its efforts to align with industry peers, even if Amazon is not formally a signatory to the New Plastics Economy Global Commitment. We would still like to see Amazon publish an overall baseline of plastic used across its entire supply chain, to add to its robust reporting levels for outbound packaging practices.

Voting Requires Deep Knowledge of the Company

Our portfolio managers chose not to support a shareholder proposal asking Microsoft (MSFT) to report on the risks of its European Security Program (‘ESP’) being used for censorship of free speech. We thought this proposal appeared to conflate a cybersecurity initiative with speech regulation and could mislead investors on the nature of the ESP. The company launched the ESP in response to the sharp rise in ransomware and cyberattacks involving espionage, data theft and disruption of democratic institutions.

Microsoft’s ESP provides structured, limited-scope support to governments by sharing insights into these threats and aligns with Microsoft’s Information Integrity Principles, which emphasize trusted information and freedom of expression rather than content moderation, surveillance or speech regulation. The company also participates in the Global Network Initiative (‘GNI’), which independently evaluates its adherence to principles protecting privacy and free expression.

Executive Compensation Should Be Reasonable

We actively engaged UnitedHealth Group (UNH)’s Board of Directors over the course of 2025 about the appropriateness of the compensation for their executive team.

The company serially missed earnings expectations, resulting in underperformance relative to the S&P 500 Index by 20% in both 2023 and 2024. Further, UnitedHealth had a major cybersecurity incident that jeopardized payments throughout the U.S. health care system, and public sentiment toward the company was at historic lows. Despite poor results, United asked investors to support pay increases for the CEO and CFO, while withholding any bonus payment to the family of murdered executive Brian Thompson. We opposed the proposed pay scheme, as did 40% of voting investors, and we accordingly expressed our views to the board.

Following the proxy vote, UnitedHealth announced it would replace both the CEO and the CFO. UnitedHealth’s board failed to hold either outgoing executive accountable for poor performance, and it allowed both of them to keep very significant unvested compensation. We again expressed our dissatisfaction to the board about its compensation decision.

Seeking to Enhance Shareholder Value

In voting proxies, we are guided by general fiduciary principles. Our goal is to act prudently, solely in the best interest of the beneficial owners of the accounts we manage. We attempt to provide for the consideration of all factors that could affect the value of the investment and will vote proxies in the manner that we believe are consistent with efforts to maximize shareholder values.

Among these factors would also be issuance of preferred shares. For example, the ClearBridge Emerging Markets Strategy portfolio managers considered a proposal at Localiza (LZRFY), a Brazilian car rental company, which held an out-of-cycle extraordinary general meeting to approve the creation of preferred stock.

Although the issuance of preferred stock adds complexity to common shareholders, the background here was telling: Brazil was to initiate a new dividend tax in January 2026 and companies were advancing dividends and bonus share issues to use up distributable reserves before the year end.

We judged that shareholder voting rights were being maintained and the company was attempting to issue bonus shares before the year-end tax increase. Ultimately, we agreed with management that the share issue was in the interest of shareholders and voted in favor of the proposal.

Grace Su, Managing Director, Portfolio Manager

Jean Yu, CFA, PhD, Managing Director, Portfolio Manager

References

- Staff Legal Bulletin No. 14M.

- Statement Regarding the Division of Corporation Finance’s Role in the Exchange Act Rule 14a-8 Process for the Current Proxy Season, Nov. 17, 2025. U.S. Securities and Exchange Commission.

- “2025 Proxy Season Review: From Escalation to Recalibration,” Harvard Law School Forum on Corporate Governance. Sept. 15, 2025.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

peshkov/iStock via Getty Images

By Christopher Gannatti, CFA and Nitesh Shah

Energy markets have once again been thrust into the spotlight. In recent weeks, geopolitical tensions in the Middle East have pushed Brent crude back above $100 per barrel and triggered sharp

Business

CK Hutchison Holdings Limited 2025 Q4 – Results – Earnings Call Presentation (OTCMKTS:CKHUY) 2026-03-19

Seeking Alpha’s transcripts team is responsible for the development of all of our transcript-related projects. We currently publish thousands of quarterly earnings calls per quarter on our site and are continuing to grow and expand our coverage. The purpose of this profile is to allow us to share with our readers new transcript-related developments. Thanks, SA Transcripts Team

Britain’s second-largest pub operator, Greene King, is set to sell around 150 managed pubs and convert a further 150 into tenanted or franchise venues as part of a sweeping overhaul of its estate strategy in response to mounting economic pressures.

The move, described by chief executive Nick Mackenzie as a “strategic reaction” to a rapidly “changing operating environment”, reflects the deep structural challenges facing the UK hospitality sector, from rising employment costs and persistent inflation to weakening consumer spending.

Greene King currently operates approximately 1,500 managed pubs alongside a further 1,000 leased and tenanted sites. Under the new plan, a significant portion of its directly managed estate will be either divested or transitioned into lower-cost operating models, allowing the group to concentrate investment into what it describes as its “core portfolio”.

The decision comes at a time when pub operators are grappling with a convergence of financial headwinds. Labour cost increases, including higher National Insurance contributions and minimum wage rises, have significantly raised operating expenses, while elevated energy prices and supply chain costs continue to squeeze margins.

At the same time, consumers, facing their own cost-of-living pressures, are cutting back on discretionary spending, particularly in areas such as dining and social drinking.

Although the government has introduced temporary business rates relief for pubs, industry leaders have repeatedly warned that the measures fall short of addressing the scale of the challenge.

Greene King’s own financial performance underscores these pressures. In the 12 months to December 2024, the company reported revenues of £2.45 billion, up 3.2 per cent year-on-year, but swung to a pre-tax loss of £147.1 million. Net debt, excluding lease liabilities, stood at £2.1 billion, with debt servicing costs rising to £110 million.

Central to Greene King’s strategy is a shift away from capital-intensive managed pubs, where the company owns and operates the business, towards leased, tenanted or franchise models, where independent operators run the pubs while Greene King retains ownership of the property.

This transition reduces operational complexity and cost exposure, while providing more stable, predictable income streams through rent and supply agreements.

Mackenzie said the restructuring would allow the company to “maximise the potential and profitability” of its estate while adapting to evolving market conditions.

“The whole market is changing; consumer dynamics are changing, and the economics of running pubs have shifted significantly over the past few years,” he said.

All pubs earmarked for sale or conversion will be placed into a newly created division during the transition period. While no fixed timeline has been set, disposals are expected to take place over the medium term, with a “substantial proportion” of proceeds reinvested into the retained managed estate.

Alongside the estate reshaping, Greene King is also planning to close around 20 pubs, broadly in line with its typical annual closure rate.

While the company has not disclosed how many jobs may be affected, it said it would seek to redeploy impacted staff across its wider business wherever possible. The group currently employs around 40,000 people.

The restructuring follows earlier indications that cost pressures could lead to further efficiencies, including potential job reductions, as the business seeks to restore profitability and improve margins.

Greene King was acquired in 2019 for £4.6 billion by CK Asset Holdings, the investment vehicle controlled by billionaire Li Ka-shing. The current strategy forms part of a broader plan to reposition the business ahead of its 2030 growth ambitions.

The company’s portfolio includes well-known pub brands such as Hungry Horse, Chef & Brewer, Farmhouse Inns and Flaming Grill, as well as brewing operations behind labels including Old Speckled Hen and Abbot Ale.

By concentrating resources on higher-performing sites and adopting a more flexible operating model, Greene King aims to grow market share, enhance customer experience and improve financial resilience in what it describes as an “increasingly dynamic” and challenging environment.

The move is emblematic of a wider shift across the UK pub and hospitality sector, where operators are increasingly prioritising efficiency, capital discipline and adaptability as they navigate a prolonged period of economic uncertainty.

Amy Ingham

Amy is a newly qualified journalist specialising in business journalism at Business Matters with responsibility for news content for what is now the UK’s largest print and online source of current business news.

China cracks down on fentanyl networks in move long sought by Washington

3 REITs To Buy Before Their Dividends Are Hiked

The official minimum rates of pay will rise for 2.7 million workers in April 2026.

Eli Lilly on Thursday said its next-generation obesity drug retatrutide cleared its first late-stage trial on Type 2 diabetes patients, helping them manage their blood sugar levels and lose weight.

The drug lowered hemoglobin A1c — a key measure of blood sugar levels — by an average of 1.7% to 2% across different doses at 40 weeks compared to placebo, meeting the study’s main goal. Patients started the trial with an A1c in the range of 7% to 9.5%, and were not taking other diabetes medications.

Retatrutide also met the study’s second goal, helping patients at the highest dose lose an average of 16.8% of their weight, or 36.6 pounds, at 40 weeks, when evaluating only patients who stayed on the drug. When analyzing all participants, including those who discontinued treatment, the highest dose of the drug helped patients lose 15.3% of their weight.

Patients with Type 2 diabetes historically struggle to lose weight, so Lilly is “very excited” to see that the drug led to both a competitive drop in blood sugar levels and significant weight loss, Ken Custer, president of Lilly Cardiometabolic Health, said in an interview.

The company was also “very pleased” with the relatively low discontinuation rates due to side effects, which were up to 5%, he added.

They are the second late-stage results to date on retatrutide, which works differently from existing injections and appears to be more effective, at least for weight loss. Lilly is betting big on retatrutide as the next pillar of its obesity portfolio after its blockbuster weight loss injection Zepbound and its upcoming pill, orforglipron.

But Lilly has yet to file for approval for the drug for obesity or diabetes. The company expects to report findings from seven additional phase three trials on the drug by the end of the year.

There are no head-to-head trials of retatrutide against other drugs, making it difficult to directly compare efficacy.

Still, retatrutide’s A1C reduction doesn’t appear to be the greatest Lilly has seen within its portfolio: The highest dose of Zepbound lowered the measure by more than 2% at 40 weeks in two separate trials on diabetes patients.

But Custer said retatrutide’s A1C reduction is still “very, very strong” compared to other diabetes medications that don’t target gut hormones.

He also said that having options in the obesity and diabetes space will be important because “not everybody is going to be helped with or satisfied with the same treatment.” Choosing which drug to take will depend on “individualized tailoring of solutions and patients,” particularly earlier in their diabetes treatment, he added.

For example, Custer said patients who want to regulate their blood sugar could benefit from either Zepbound or retatrutide. But if they are looking to lose more weight, the latter might be a better option, he said.

In the two separate diabetes trials, Zepbound helped patients lose slightly less weight than retatrutide did. In one study called SURPASS-2, the highest dose of Zepbound helped patients lose an average of 13.1% of their weight at 40 weeks. In the other study, SURPASS-1, the highest dose helped patients lose an average of 11% of their weight at the 40-week mark.

Retatrutide’s safety profile was similar to other injectable diabetes and obesity drugs, primarily causing gastrointestinal side effects. Around 26.5% of patients on the highest dose experienced nausea, while roughly 22.8% and 17.6% had diarrhea and vomiting, respectively.

Low rates of patients experienced dysesthesia, which is an unpleasant nerve sensation.

Dubbed the “triple G” drug, retatrutide works by mimicking three hunger-regulating hormones – GLP-1, GIP and glucagon – rather than just one or two like existing treatments. That appears to have more potent effects on a person’s appetite and satisfaction with food than other treatments.

Tirzepatide, the active ingredient in Zepbound, mimics GLP-1 and GIP. Novo Nordisk’s semaglutide, the active ingredient in Wegovy, mimics only GLP-1.

As retatrutide inches closer to the market, Novo is racing to catch up to Lilly. In March 2025, Novo said it agreed to pay up to $2 billion for the rights to an early experimental drug from the Chinese pharmaceutical company United Laboratories International.

Novo’s newly acquired drug is a clear potential competitor to retatrutide because it similarly uses a three-pronged approach to promoting weight loss and regulating blood sugar. But Novo’s treatment is much earlier in development, meaning it will take several years before it reaches patients.

RHEINFELDEN, GERMANY – In the world of specialized transport and utility vehicles, the components hidden beneath the chassis are the difference between a seamless operation and a costly breakdown. From its headquarters in Rheinfelden, CVS engineering GmbH has established itself as the engineering heartbeat of the mobile industry, providing the “lungs” for everything from city trains and buses to heavy-duty vacuum trucks and silo trucks.

With a portfolio that bridges the gap between high-performance vacuum systems and precision compressor technology, CVS engineering is redefining what it means to move materials. Whether they are liquid, solid, or even living.

A multidimensional portfolio for global industries

CVS engineering doesn’t just manufacture parts; they provide the mechanical backbone for several critical sectors. Their complete product range addresses the specific stresses of mobile applications:

- Dry Bulk Handling: The SKL series of oil-free screw compressors (SKL 700, 1100, 1200, 1500) sets the standard for unloading silo vehicles. These systems ensure that bulk goods like cement, grain, or plastic pellets are moved rapidly and crucially without oil contamination.

- Sewage & Liquid Waste: The VacuStar series (including rotary vane and liquid ring pumps) is built for the “dirty work.” These pumps are essential for sewer cleaning, sludge extraction, and the transport of hazardous liquid waste.

- Urban Transportation: CVS provides specialized rotary vane compressors for the rail and bus sectors, ensuring reliable pneumatic power for braking and suspension systems in public transit.

- Aquaculture: Precision-engineered vacuum pumps are also tailored for fish handling, allowing for the gentle and efficient transport of live fish in commercial fishing and farming.

Innovation driven by durability

What sets CVS engineering apart is a relentless focus on longevity in “harsh and heavy” conditions. “Our technologies ensure maximum suction capacity and durability in extreme environments,” explains Fabio Geiger, Area Sales and Marketing Manager at CVS engineering.

To combat the high-heat and corrosive nature of industrial cleaning, CVS offers optional plasma nitriding and ceramic coatings on its VacuStar series. Furthermore, their innovative cell aeration systems allow for continuous operation at high vacuum without the risk of overheating—a common failure point in inferior systems.

The shift toward sustainable operations

As global regulations tighten around noise and emissions, CVS is leading the transition with “Dry Bulk” solutions that prioritize efficiency. This includes the SKL-E Pack, a stationary solution that allows for the unloading of dry bulk without requiring the truck’s main engine to idle.

“Particularly against the backdrop of urbanization and increasing environmental regulations driven by decarbonization and noise protection, there is a growing need for low-emission transport solutions,” emphasizes Geiger.

A partner for OEMs and Fleet Owners

By focusing on low weight, wide speed ranges, and outstanding performance, CVS components help manufacturers (OEMs) and haulage firms reduce their overall lifecycle costs. Beyond the core units, CVS also delivers the right accessories including innovative cell aeration systems, filters, and valves as well as drive components like hydraulic adaptors, all designed to integrate seamlessly into modern vehicle architectures.

Whether it’s maintaining urban infrastructure, supporting the food supply chain, or powering public transit, CVS engineering GmbH continues to prove that when the world needs to move, their technology provides the pressure, vacuum and the power to get it done.

Contact:

Fabio Geiger

Area Sales & Marketing Manager

CVS engineering GmbH

Mobile: +4915167973982

E-mail: fabio.geiger@cvs-eng.de

Visit us at: www.cvs-eng.com

NIFTY plunges over 3% on HDFC Bank chairman exit, crude surge

Austin Engineering’s efforts to further improve its South American operations have received a boost, following a key development.

Oil Markets Face A Supply Shock – And The Offsets Aren’t Enough

Crypto.com lays off 12% of staff as CEO warns firms must move fast on AI

A Daily Multivitamin May Slow Signs Of Biological Ageing

-

Crypto World5 days ago

Crypto World5 days agoHYPE Token Enters Net Deflation as HyperCore Buybacks Outpace Staking Rewards

-

Tech4 days ago

Tech4 days agoYour Legally Registered ‘Motorcycle’ Might Not Count Under Proposed US Law

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Addict Lip Glow

-

Tech2 days ago

Tech2 days agoAre Split Spacebars the Next Big Gaming Keyboard Trend?

-

Sports5 days ago

Why Duke and Michigan Are Dead Even Entering Selection Sunday

-

Business4 days ago

Business4 days agoSearch for Savannah Guthrie’s Mother Enters Seventh Week with No Arrests

-

Business5 days ago

Business5 days agoUS Airports Launch Donation Drives for Unpaid TSA Workers as Partial Government Shutdown Enters Fifth Week

-

Crypto World5 days ago

Coinbase and Bybit in Investment Talks: Could Bybit Finally Enter the US Crypto Market?

-

Business3 days ago

Business3 days agoAustralian shares drop as Iran war enters third week

-

Business5 days ago

Business5 days agoCountry star Brantley Gilbert enters growing non-alcoholic beer market

-

Crypto World3 days ago

Crypto World3 days agoCrypto Lender BlockFills Enters Chapter 11 with Up to $500M in Liabilities

-

Sports6 days ago

Sports6 days agoCollege Basketball Best Bets: Conference Tournament Semifinal Picks

-

Politics1 day ago

Politics1 day agoThe House | The new register to protect children from their abusers shows Parliament at its best

-

Business7 days ago

Business7 days agoTrump demands Powell cut rates as Iran conflict raises energy prices

-

Fashion3 days ago

Fashion3 days ago25 Celebrities with Curly Hair That Are Naturally Beautiful

-

News Videos18 hours ago

News Videos18 hours agoRBA board divided on rate cut, unusually buoyant share market | Finance Report | ABC NEWS

-

Crypto World7 days ago

Crypto World7 days agoSenate Votes to Include CBDC Ban in Bipartisan Housing Bill

-

NewsBeat7 days ago

NewsBeat7 days agoDeane Road crash near Bolton colleges and university

-

Crypto World19 hours ago

Crypto World19 hours agoCanada’s FINTRAC revokes registrations of 23 crypto MSBs in AML crackdown

-

News Videos7 days ago

News Videos7 days agoTom Lee: The 100x Opportunity EVEN Bigger Than Bitcoin (New Ethereum Prediction 2026)

You must be logged in to post a comment Login