Business

Dipan Mehta bets on NBFCs, says cleaned-up books signal fresh upside

On the lending space, Mehta believes the clean-up in microfinance and MSME unsecured portfolios has strengthened the NBFC segment. “I think that for investors who want to buy lenders, NBFC is a great segment… a lot of NBFCs now have cleaned up their books… whatever the NPA they had are well behind them.”

He emphasised a preference for diversified lenders rather than niche players. “Our preference is for NBFCs which are doing multi-product… not just housing or automobile loans or microfinance or gold loan.” He cited Bajaj Finance, Chola and L&T Finance as preferred names, while disclosing investments in them.

Turning to solar equipment manufacturers, Mehta acknowledged that the bullish call has not played out immediately. “We have been very positive on all solar equipment manufacturing companies… that call is not proving right so far.” However, he maintained that long-term investors could benefit. “If you have a longer-term view… this is a nice sustainable compounding industry and can deliver good returns.” On the recently imposed 126% customs duty, he said, “This… will not impact India’s solar equipment industry to any major extent… Waaree included,” adding that valuations have turned attractive, even as he disclosed existing investments in the space.

On the underperformance of Reliance Industries, Mehta offered a structural explanation. “I have a different view and that is that it is slowly going to become a holding company.” He suggested that investors may be uncomfortable with the prospect of IPOs for Jio and retail without a clear vertical split. “We would have preferred a vertical split… given free shares to all the shareholders.” Until there is clarity on restructuring, he believes the stock could remain subdued, though he reiterated that it remains a great company.

In real estate, Mehta advised patience and selectivity, favouring larger developers with rental income streams. “I would prefer the larger ones, especially those which have got some annuity assets as well.” He referred to companies like Prestige and DLF as examples and added that investors should broadly focus on players with rental assets, given the supply of new listings and valuation adjustments underway.

On tobacco counters, particularly ITC Limited, his stance was unequivocal. “Yes, we have a view and it is an avoid. It is not an FMCG stock. It is a tobacco stock and it is valued accordingly.” He said growth visibility remains limited. “I do not see ITC growing at double digit type of growth rates in the foreseeable future.” Instead, his focus is on small and midcap companies with unique business models and more reasonable valuations after the recent correction.Discussing the GLP-1 opportunity in pharma, Mehta acknowledged its potential but warned about competition. “You are right, it is a good opportunity. But just too many players over there.” Even so, he remains constructive on the broader sector. “On the whole investors should be overweight pharma.” He noted that CDMO companies have seen sharp corrections and should be on investor watchlists for a potential turnaround.

On new-age digital firms such as Eternal, he said investor patience appears to be wearing thin. “Investors are losing patience… when they will turn to profitability.” However, he added, “We remain very positive on Eternal… we have a longer-term view,” signalling continued conviction despite volatility.

Finally, on metals, Mehta struck a cautious tone after a prolonged rally. “It is a cyclical industry and now it has been a great outperformer.” While he would remain invested, he is not keen on fresh entries at current levels. “At some point the cycle certainly will turn… right now I do not see the outperformance continuing.”

Overall, Mehta’s approach reflects a preference for diversified financials, an overweight stance on pharma, selective exposure in real estate and solar, caution in metals, and a clear avoidance of slow-growth largecaps — all anchored in a long-term investment perspective.

Trapping Value is a team of analysts with over 40 years of combined experience generating options income while also focusing on capital preservation. They run the investing group Conservative Income Portfolio in partnership with Preferred Stock Trader. The investing group features two income-generating portfolios and a bond ladder.

Trapping Value provides Covered Calls, and Preferred Stock Trader covers Fixed Income. The Covered Calls Portfolio is designed to provide lower volatility income investing with a focus on capital preservation. The fixed income portfolio focuses on buying securities with high income potential and heavy undervaluation relative to comparatives. Learn more.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

We long positions in TIPS and real return bonds via different Canadian instruments.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Raymond James initiates Milestone Pharmaceuticals stock coverage with Strong Buy

AMRO’s flagship AREO 2026 report projects steady regional growth for ASEAN+3 while warning that the Middle East conflict has significantly increased downside risks through energy supply disruptions.

Key Details:

- Regional growth is forecast at 4.0% in both 2026 and 2027, following stronger-than-expected expansion of 4.3% in 2025.

- The Middle East conflict has raised energy prices, pushing headline inflation from 0.9% in 2025 to a projected 1.4–1.5% in 2026–2027.

- The region is considered better positioned than in previous energy shocks due to improved energy efficiency, lower oil dependency, and available policy space.

- A prolonged conflict could spread disruptions beyond energy markets to industrial inputs, logistics, food prices, tourism, and remittances.

- Structurally, ASEAN+3 has shifted toward intraregional demand — now accounting for 28% of global final demand — with US-bound value-added exports falling from ~one-third to 20%.

- Policymakers are urged to maintain financial stability, act decisively against sustained inflation, and provide targeted fiscal support without fuelling inflation.

Why It Matters:

ASEAN+3’s growing regional integration and economic resilience provide a strong foundation, but sustained policy vigilance and deeper regional cooperation will be critical to navigating ongoing global shocks.

Chapter 1: Macroeconomic Prospects and Challenges

ASEAN+3 delivered a stronger-than-expected performance in 2025 despite the most significant shift in global trade policy in decades. Economic activity remained well-supported by firm domestic demand, robust export performance, continued investment, and strengthening intraregional linkages.

Near-term risks (Chapter 1):

- Ongoing conflict in the Middle East and energy supply disruptions (especially via the Strait of Hormuz).

- Shifting U.S. trade policies and volatile technology demand.

- Financial market volatility adding downside pressure.

- Policymakers’ central challenge: preserving policy flexibility.

Looking ahead, the balance of risks is tilted to the downside, with uncertainty remaining elevated. Trade policy shifts and technology demand have each become sources of two-sided risk. The conflict in the Middle East and the disruption to energy supply through the Strait of Hormuz pose a significant near-term risk to both growth and inflation, while financial market volatility adds further downside pressure.

The region nonetheless enters 2026 from a position of relative strength. Growth outperformed expectations in 2025, inflation remained low, and most economies retain meaningful fiscal and monetary space. Preserving policy flexibility remains the central near-term challenge for policymakers across the region.

Source : ASEAN+3 Regional Economic Outlook 2026 – ASEAN+3 Macroeconomic Research Office – AMRO ASIA

Other People are Reading

Continue Reading

Business

$67 billion! Dalal Street braces for 81 IPO lock-in expiries in next 3 months. Check details

The value refers to the total shares becoming eligible for trading as lock-up periods end. However, not all of these shares are expected to be sold in the secondary market, as a substantial portion remains held by promoter groups who typically continue to retain their stakes.

Among the notable names in April, Bharat Coking Coal will see its three-month lock-in end on April 15, with 59 million shares or 1% of equity becoming eligible for trading. Amagi Media Labs follows on April 20, with 11 million shares or 5%, while Shadowfax Technologies will have 35 million shares or 6% unlocked on April 23.

In May, Fractal Analytics and Aye Finance will see lock-in expiries on May 13, involving 7 million shares (4%) and 18 million shares (7%), respectively. Later in the month, Gaudium IVF and Women Health will unlock 3 million shares or 4% on May 26, followed by Clean Max Enviro Energy Solutions on May 27 with 4 million shares or 4%. PNGS Reva Diamond Jewellery will also see 2 million shares or 7% becoming tradable on May 29.

In June, Omnitech Engineering will have 4 million shares or 3% unlocked on June 1, while SEDEMAC Mechatronics will see 1 million shares or 3% become eligible for trading on June 8.

A host of stocks will also witness six-month shareholder lock-in periods expiries over the coming weeks. Starting April 13, Tata Capital will see a significant 2,858 million shares, or 67% of equity, become eligible for trading. On the same day, WeWork India will have 60 million shares, representing 45%, unlocked.

On April 15, LG Electronics India will see 441 million shares or 65% of equity become tradable. This will be followed by Canara Robeco AMC on April 17, with 110 million shares or 55% unlocking, and Canara HSBC Life Insurance on April 20, where 522 million shares or 55% will

be released.

Later in April, Midwest will see 6 million shares or 17% unlocked on April 24, followed by Capillary Technologies on April 28 with 0.5 million shares or 0.7%. Tenneco Clean Air India will also see 3 million shares or 0.8% become tradable on April 30.

In May, Lenskart Solutions will have 1,047 million shares or 60% unlocked on May 8, alongside Emmvee Photovoltaic Power with 5 million shares or 0.7%. This will be followed by Aequs on May 11 with 1 million shares or 0.2%.

Finally, Billionbrains Garage Ventures will see a large expiry on May 12, with 4,182 million shares, or 68% of equity, becoming eligible for trading.

While lock-in expiries are a routine part of the IPO cycle, clustered unlocks of this scale tend to attract attention and can weigh on stock prices in the short term. Nuvama noted that despite the headline figure of $67 billion, the actual market impact will depend on how much of the eligible stock is eventually offered for sale.

The upcoming lock-in expiries come at a time of heightened geopolitical uncertainty, with tensions in the Middle East still elevated and rising crude prices fuelling concerns over potential rate hikes. Although a two-week ceasefire is currently in place, its durability remains uncertain, leaving markets vulnerable to volatility if tensions escalate further.

(Disclaimer: Recommendations, suggestions, views and opinions given by the experts are their own. These do not represent the views of The Economic Times)

I aim to provide alpha-generating investment ideas. I am an independent investor managing my family’s portfolio, primarily via a Self Managed Super Fund. My articles deliver 5-Minute Pitches focused on the core fundamental and technical drivers of the security.I have a generalist approach as I explore, analyze and invest in any sector so long there is perceived alpha potential vs the S&P500. The typical holding period ranges between a few months to multiple years.I am very much focused on adding value via alpha generation. I always start with a Performance Assessment section for each follow-up article. I publish unusually detailed analytics on my long-only, zero-leverage global equity portfolio performance on my Hunting Alphas website every month.A bit about how I approach research and coverage of a stock:I build and maintain spreadsheets showing historical data on the financials, key metric disclosures, data on the guidance and surprise trends vs consensus estimates, time-series values of the valuations vs peers, data on key coincident or leading indicators of performance and other monitorables. In addition to the company’s filings, I also keep tabs on relevant industry news and reports plus other people’s coverage of the stock. In some cases, such as during times of a CEO change, I will do a deep dive on a key leader’s background and his/her past performance record.I very rarely build DCFs and project financials many years out into the future as I don’t think it adds much value. Instead, I find it more useful to assess how a company has delivered and the broad outlook on the 5 key drivers of a DCF valuation: revenues, costs and margins, cash flow conversion, capex and investments and the interest rates (which affect the discount rate/opportunity cost of capital). In some cases, especially for companies trading at very high multiples on a TTM or 1-yr fwd basis, I do a reverse DCF to make sense of the implied growth CAGR implications.Note: Hunting Alphas is related to VishValue Research on Seeking Alpha.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of CLS either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Agwa is using artificial intelligence to create a contained environment for produce to grow.

Business

Why FPI interest in India ‘has pretty much died out’: Nithin Kamath points to valuations, taxes and global alternatives

According to Kamath, India is currently viewed as geopolitically vulnerable—particularly to potential oil shocks—while the absence of compelling artificial intelligence-led investment opportunities has further dampened its appeal. Elevated valuations and concerns around the rupee have also added to investor hesitation.

He noted that many foreign investors who were sitting on gains have already booked profits and are reallocating capital to other markets such as Japan, Taiwan, South Korea, and parts of Europe, where relative valuations and growth narratives appear more attractive.

Policy-related factors are also playing a role. Kamath highlighted that India’s capital gains tax framework—especially the structure of long-term and short-term capital gains (LTCG/STCG)—along with the recent increase in Securities Transaction Tax (STT), has made the market less competitive versus global peers that are currently attracting stronger inflows.

With foreign portfolio investment (FPI) flows turning volatile, Kamath suggested that rationalising these tax structures could be a “low-hanging fruit” to improve India’s attractiveness and bring global investors back into the fold.

“Asked someone from the industry whether foreign investors are still interested in allocating to India. The TLDR: Interest has pretty much died out. India is seen as geopolitically exposed, especially to an oil shock. There are no real AI plays. Valuations are rich. And the rupee situation doesn’t help. On top of that, investors who were sitting on gains have taken money off the table and are now looking at markets like Japan, Taiwan, Korea, Europe etc instead,” the tweet said.

“He also pointed out that our LTCG/STCG structure and the increase in STT have made India less attractive compared to other markets that are seeing inflows. If we need to attract FPIs back, and we do, fixing this feels like pretty low-hanging fruit,” Kamath added.Nifty is down 9% this year, as FIIs continue to leave India. They have offloaded equities worth Rs 1,77,271 crore so far this year. In just six sessions this month, they have sold Rs 46,149 crore worth of stocks.

Domestic markets ended with cuts today, ending their five-session gaining streak. They fell amid significant selling pressure in financial stocks along with auto and FMCG counters. Nifty plunged 222.25 points or 0.93% to finish at 23,775.10. Meanwhile, Sensex declined 947.22 points or 1.22% to settle at 76,615.68.

(Disclaimer: The recommendations, suggestions, views, and opinions given by the experts are their own. These do not represent the views of The Economic Times.)

FBCG: Bluechip Growth Investing Can Help Earn Market-Beating Returns

Canada stocks lower at close of trade; S&P/TSX Composite down 0.42%

The country is expected to remain among the fastest-growing major economies. Growth for FY27 reflects the impact of higher global energy prices due to the Middle East conflict and is expected to average 7.1% in FY28-29, it noted.

The World Bank has assumed oil prices at $90-100 per barrel for FY27.

Despite external risks, macroeconomic strength and policy measures are expected to provide some insulation. However, the multilateral lender flagged energy diversification, prudent fiscal management and trade liberalisation as key priorities.

Aurelien Kruse, lead economist for India at the World Bank, said the country entered the current fiscal year from a position of strength.

“Substantial foreign reserves, low inflation, predominantly rupee-denominated public debt, a healthy financial sector, and trade diversification efforts play a major role in providing resilience from external headwinds,” said the World Bank.

The Reserve Bank of India expects growth of 6.9% for FY27. Without the ongoing conflict, growth was estimated at 7.2%, supported by stronger-than-expected performance in FY26, the World Bank said.

India’s gross domestic product (GDP) growth is expected at 7.6% in FY26, driven by private consumption, manufacturing, exports and investment, despite high tariffs imposed by the US.

Inflation is projected to rise to 4.9% in FY27, according to the World Bank, due to higher food prices, partial pass-through of global energy prices and currency depreciation pressures. Elevated energy prices are also likely to raise input costs for industry.

“Boosting private sector-led growth will be critical to strengthening economic resilience and supporting more young people to enter the workforce,” said Paul Procee, acting country director for India at the World Bank.

He added that achieving the goal of Viksit Bharat will require a predictable, business-friendly environment to unlock investment and create jobs at scale in sectors such as energy and infrastructure, manufacturing, tourism, healthcare and agribusiness.

New Delhi: India’s growth projection of 6.6% for FY27 faces downside risks from the Gulf conflict, but the economy remains well placed to navigate the global energy shock, supported by strong macroeconomic buffers, the World Bank said on Thursday.

The country is expected to remain among the fastest-growing major economies. Growth for FY27 reflects the impact of higher global energy prices due to the Middle East conflict and is expected to average 7.1% in FY28-29, it noted.

The World Bank has assumed oil prices at $90-100 per barrel for FY27.

Despite external risks, macroeconomic strength and policy measures are expected to provide some insulation. However, the multilateral lender flagged energy diversification, prudent fiscal management and trade liberalisation as key priorities.

Aurelien Kruse, lead economist for India at the World Bank, said the country entered the current fiscal year from a position of strength.

“Substantial foreign reserves, low inflation, predominantly rupee-denominated public debt, a healthy financial sector, and trade diversification efforts play a major role in providing resilience from external headwinds,” said the World Bank.

The Reserve Bank of India expects growth of 6.9% for FY27.

Without the ongoing conflict, growth was estimated at 7.2%, supported by stronger-than-expected performance in FY26, the World Bank said.

India’s gross domestic product (GDP) growth is expected at 7.6% in FY26, driven by private consumption, manufacturing, exports and investment, despite high tariffs imposed by the US.

Inflation is projected to rise to 4.9% in FY27, according to the World Bank, due to higher food prices, partial pass-through of global energy prices and currency depreciation pressures. Elevated energy prices are also likely to raise input costs for industry.

“Boosting private sector-led growth will be critical to strengthening economic resilience and supporting more young people to enter the workforce,” said Paul Procee, acting country director for India at the World Bank.

He added that achieving the goal of Viksit Bharat will require a predictable, business-friendly environment to unlock investment and create jobs at scale in sectors such as energy and infrastructure, manufacturing, tourism, healthcare and agribusiness.

Mayo and Galway Reach Connacht U20 Knockout Stages After win

Flush with cash: Washington startup lands up to $500M to deploy facilities treating sewage, dairy waste

‘I never had a relationship with Epstein’

Why Israel is blocking foreign journalists from entering

Bitcoin: We’re Entering The Most Dangerous Phase

Alan Cumming Brands Baftas Ceremony A ‘Triggering S**tshow’

Keeping horses placed a financial burden on the Simpson family. #anime #animerecap #TheSimpsons

Inside the World of INTERNET MONEY Millionaires

With my friend Avatar World #avatarworld #avatars #gaming #finance #youtubeshorts

-

Business7 days ago

Business7 days agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Spanx – Corporette.com

-

Business4 days ago

Business4 days agoThree Gulf funds agree to back Paramount’s $81 billion takeover of Warner, WSJ reports

-

Business6 days ago

Business6 days agoExpert Picks for Every Need

-

Sports5 days ago

Sports5 days agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Tech2 days ago

Tech2 days agoHow Long Can You Drive With Expired Registration? What Florida Law Says

-

Business4 days ago

No Jackpot Winner, Prize to Climb to $231 Million

-

Fashion3 days ago

Fashion3 days agoMassimo Dutti Offers Inspiration for Your Summer Mood Board

-

Politics6 days ago

Wings Over Scotland | The quality of mercy

-

Fashion2 days ago

Fashion2 days agoLet’s Discuss: DEI in 2026

-

Business5 days ago

Business5 days agoAkebia Therapeutics, Inc. (AKBA) Discusses Pipeline Progress and Strategic Focus on Kidney Disease Treatments at R&D Day – Slideshow

-

Fashion7 days ago

Fashion7 days agoStatement Sunglasses: The Accessory Shaping Modern Fashion

-

Crypto World1 day ago

Crypto World1 day agoBitcoin recovers as US and Iran Agree a Ceasefire Deal

-

Politics7 days ago

Politics7 days agoEast Jerusalem Palestinian families eviction orders

-

Politics7 days ago

Politics7 days agoWhy so many children are now classified as ‘disabled’

-

Fashion7 days ago

Fashion7 days agoFor Love & Lemons’ Spring 2026 Line is for the Romantics

-

Politics7 days ago

Politics7 days agoNuclear rockets, moon bases and NASA’s Mars plan

-

Tech7 days ago

Tech7 days agoThe Threadless Ball Screw Never Took Off, But Don’t Write It Off

-

Business7 days ago

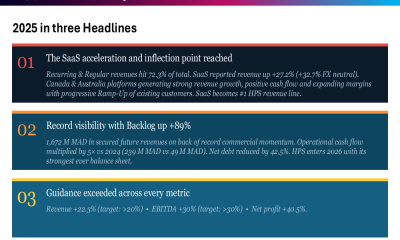

Business7 days agoHPS FY 2025 slides: SaaS inflection drives 22% revenue growth

-

Fashion6 days ago

Fashion6 days agoTory Burch’s Spring 2026 Campaign Goes on a Getaway

You must be logged in to post a comment Login