Business

GMO Q1 2026 Quarterly Letter Part 2: Letter To The Investment Committee On Private Equity

mohd izzuan/iStock via Getty Images

Executive Summary

Some institutional investors who had grown accustomed to outperforming the broader private equity composites are finding they have not done so consistently in recent years. Their diagnoses of the problem often center on specific decisions or biases they made in their recent manager selection, whereas a likely culprit is a falloff in the persistence of outperformance among private equity managers.

While wide performance dispersion persists among private equity funds of a given vintage, academic research suggests that the tendency for a manager’s prior strong performance to persist into subsequent funds has largely disappeared, particularly when prior performance is based on the interim measures used to compare funds less than 10–15 years old. If this lack of persistence is the “new normal,” it will be very difficult for investors to expect to outperform the private equity composites by meaningful amounts going forward.

Investment committees should encourage institutions to raise the bar for hiring private equity managers, as putting money to work relatively cheaply in the public markets is a better investment than paying high fees for private equity managers they have less than full confidence in.

Read Part 1 of the Quarterly Letter, What Barbarians Like to Take Private (Or: The Risks in Your Private Equity Portfolio), in which Ben Inker and John Pease use decades of buyout data to demonstrate how private equity portfolios are becoming ever more concentrated on a small set of risks.

My day job at GMO does not directly involve private equity beyond being an observer. But I do wind up discussing private equity reasonably regularly, both with investment committees that I serve on and when invited to speak to the investment committees of other institutions. And in those situations, I’ve started to notice something a little jarring that may not be as obvious to investment committee members who only experience the performance of one or two institutions.

It is well known that private equity has failed to keep up with the public markets over the last several years. But I also seem to be hearing from a number of institutions that the performance of their particular PE portfolio, which in the past might have done substantially better than the Preqin, Cambridge Associates, or other composite, no longer seems to be doing so. There is usually an excuse that feels specific to the institution in question—“we focused too much on co-investment opportunities and failed to keep a high enough bar on our expectations for the actual fund performance,” or “we were too slow to react to our GPs’ loss of focus and mission creep.”

The implication of those explanations is that fixing a particular problem they diagnose will lead to better relative performance in the future. But there is another explanation for this phenomenon that is less fixable and feels awfully plausible to me: if the persistence of performance for PE managers has gone away, or even significantly deteriorated, the performance difference between the best institutional PE portfolios and the mean is doomed to collapse to low levels. 1 For private equity allocations predicated on a belief in the investment staff’s ability to find and secure the very best private equity managers, such an explanation would call into question the rationale for the allocation in the first place.

The original handbook for the endowment model, David Swensen’s Pioneering Portfolio Management (2009), made no claims about an inherent return premium for private equity. While Swensen acknowledged some advantages of private equity in principle—better alignment with investors, longer time horizons, the focus on operating efficiency that comes along with a greater debt load—he pointed out that private equity also suffers from high fees, principal-agent problems, and the tendency for successful managers to raise ever-larger funds only for them to underperform their earlier, smaller ones.

He concluded that private equity was riskier than public equities due to its high leverage and, to the best of his knowledge, achieved disappointing median returns over its history (pp. 220–235). 2 The case for private equity, rather than resting on some vague “illiquidity premium,” 3 was all about finding extraordinary managers. He believed private assets were a good place to do that, given their much wider range of performance across managers relative to public equities or fixed income.

In practice, generating this alpha for an institution would involve finding extraordinary portfolio managers or firms who can consistently outperform their peers. So the first question any investment committee should ask when discussing an allocation to private equity or any other private asset is: what makes us confident we can find these extraordinary managers and get meaningful allocations to their funds?

If the committee can’t credibly answer that question, it makes little sense for them to try to replicate the asset allocation of institutions that can. But even for institutions that have reason to claim such a selection ability, private equity fund performance really needs to be significantly persistent for the game to work. And it is far from clear that such persistence exists.

Several academics have done interesting work on the topic, noting that persistence of performance has fallen notably since 2000, and more so for private equity than venture capital. 4 A particularly relevant finding is that the interim performance of funds that have not completed their life cycles is entirely unhelpful in predicting future fund returns, a real problem since those are the only returns recent enough to feel relevant when considering a manager’s next fund.

While we all know “past performance is not indicative of future results,” it is extremely hard to overstate how central past performance is to investors’ decision-making when choosing private asset managers. You are buying into a blind pool, and almost the only thing you know is what the manager did in the past.

While the performance of the investments in that previous pool is not the only thing you can analyze, it feels like the most salient piece of data there is. But what if that is an illusion? A mature private equity portfolio will consist of multiple funds from multiple managers, so the total number of different funds owned by an institution will generally be pretty large, easily a couple of dozen or more, even if the institution has relationships with a relatively small number of firms.

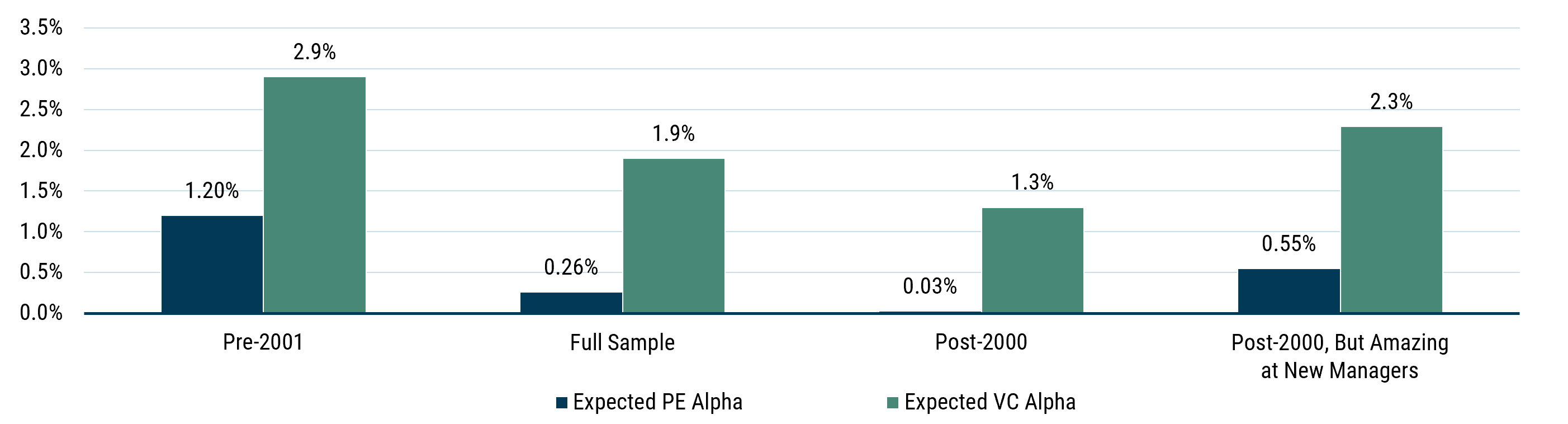

If there truly is little persistence in private equity fund returns, it implies that even if the range of returns between the best- and worst-performing funds remains large, the aggregate returns for an institution will almost always be close to the median. The chart below shows the implied alpha of a diversified PE portfolio across several levels of performance persistence (Braun, Jenkinson, and Stoff 2017).

Effect of Performance Persistence on Expected PE and VC Alpha

Source: Braun, Jenkinson, and Stoff (2017) Assumed alpha for quartiles of performance is 8%/3.5%/-3.5%/-8% for PE and 12%/4%/-4%/-12% for VC. “Amazing at New Managers” assumption is 40%/30%/20%/10% odds of new managers being in each alpha quartile, and 20% of assets in PE/VC invested in such new managers.

I’ve put the venture capital results in as well. While there was basically no evidence of persistent performance in the post-2000 sample for private equity, venture capital did show a decent amount of persistence, even if it, too, shows substantially less persistence than the early sample. I added a fourth column in which I made a friendly assumption about the new funds that an institution hires. I assumed that the institution had an amazing record in backing new managers, and that those new managers had a 40%/30%/20%/10% chance of being in the 1st through 4th quartiles of performance.

I further made the (probably insanely friendly) assumption that the institution’s full 20% PE or VC allocation was invested in such funds (such an institution could still not expect very much alpha from a PE portfolio, though 55 basis points is a whole lot better than the 3 basis points of implied alpha for an institution that simply reupped with its strongest performers).

It’s possible I’m being unfair in assuming that the basic due diligence in choosing to invest in the new funds of current managers is to look at the interim performance of their previous funds, but for institutions whose current alpha relative to the PE composite does not look particularly impressive, I think it’s fair to ask why you think it will get better in the future.

I’m not trying to make the case that institutions should abandon private equity. Actually, if one believes, as I do, that private equity is choosing from a small, junky group of firms, the industry’s performance has been somewhat better than it looks over the last decade. 5 I also believe that investing skill exists, 6 and that it makes sense for well-resourced institutions to invest with private equity managers they truly have high conviction in. The difference between the best and worst performers among private equity funds remains large, and an institution that can truly tilt the odds in favor of top-quartile results will reap substantial benefits.

But the bar to invest in a private equity manager should be high—arguably even higher than it is for active public asset managers, since you’ll be stuck paying PE managers high fees for a long time, even if you lose conviction in the interim. And if individual fund allocations truly do have a high bar, a target PE allocation may not even make sense (at least not beyond establishing an upper limit).

If, for example, you target 25% of your portfolio in U.S. public equities and can only come up with 10% worth of allocations to active managers you truly believe in, you have the option to allocate the other 15% passively. That passive option is not available to you in private equity. If you max out on high-caliber PE managers short of an overall allocation target, you will wind up investing the rest of your allocation in managers you have less confidence in. Paying high fees to managers you have less confidence in is unlikely to be a good use of capital.

How can the investment committee help? I think a good start would be for the investment committee to ask the investment staff to discuss their beliefs about each asset class in which the institution invests, the purpose each serves in the portfolio, how much (if any) alpha they expect to add in each asset class, and, crucially, how they intend to test those beliefs over time. They should document their beliefs for each asset class and compare them periodically, perhaps every three to five years. 7

At the end of the day, the role of the investment committee is to help the investment staff do a better job managing the portfolio. That should not be about second-guessing individual manager decisions, but pushing the investment staff to think critically about what they do and why is absolutely in the committee’s wheelhouse. Private equity programs are not meant to run on autopilot; there are critical questions to answer and, for many institutions, disappointing results to grapple with.

1 There will still be a fair bit of performance dispersion, since most investors invest with a relatively small number of PE managers, and there will still be plenty of variability in actual fund returns. But without persistence of returns, that variability will wind up mostly owing to chance, and longer-term returns will tend to converge.

2 Paraphrased from the 2009 edition, which made basically the same points as the original 2000 edition (pp. 224–233) with some updated data.

3 An illiquidity premium for leveraged buyouts (LBOs), at least, never made any sense in the first place. If you voluntarily take a public company private and pay a premium to do so, there is no plausible mechanism by which you could possibly get paid for taking on the illiquidity. The illiquidity might be a means to an end for some other mechanism to achieve higher returns, but the idea that you would generally get paid for the fact that the asset is no longer liquid is just silly when the illiquidity is entirely self-imposed.

4 I’m not going to pretend to give a comprehensive listing of the research, but a couple of studies that stood out to me included Braun, Jenkinson, and Stoff (2017), which looked at performance by deal rather than by fund, helping to abstract away from some of the fund return calculation problems; and Harris, Jenkinson, Kaplan, and Stucke (2023), which looked at the problem of interim performance calculations that investors are forced to rely on given the long lives of funds.

5 See part 1, What Barbarians Like to Take Private, for evidence of a small, low-quality bias in private equity.

6 Admittedly, I’m highly likely to be biased toward such a belief.

7 The risk in doing this is that it just turns into a referendum on which assets have done well or badly in the trailing period, which would be a profound mistake. There is already too much performance chasing in the investment world. But putting your beliefs down on paper is extremely important to avoid the narrative creep that it is all too easy to fall into. If ”private real estate is a great place to add alpha” turns into “private real estate is an inflation hedge,” then into “private real estate is an under-owned asset class,” and so on—each rationale replacing the last as the thesis fails to play out—while the target allocation remains fairly static, something has gone very wrong.

References

Braun, R., Jenkinson, T., & Stoff, I. (2017). How persistent is private equity performance? Evidence from deal level data. Journal of Financial Economics, 123 (2), 273–291. https://doi.org/10.1016/j.jfineco.2016.01.033

Harris, R.S., Jenkinson, T., Kaplan, S.N., & Stucke, R. (2023). Has persistence persisted in private equity? Evidence from buyout and venture capital funds. Journal of Corporate Finance, 81 (102361). https://doi.org/10.1016/j.jcorpfin.2023.102361

Swensen, D. (2009). Pioneering Portfolio Management: An Unconventional Approach to Institutional Investment, Fully Revised and Updated. Free Press.

Disclaimer: The views expressed are the views of Ben Inker through the period ending May 2026 and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2026 by GMO LLC. All rights reserved.

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Oil falls more than $4 as US, Iran remain at odds over peace deal

Life360 CEO Lauren Antonoff explains the company’s new real-time GPS pet tracker on ‘The Claman Countdown.’

A popular raw dog food brand is expanding a recall of dozens of products over fears they may be contaminated with Listeria monocytogenes, a potentially deadly bacteria that can sicken both pets and humans, federal officials warned Friday.

Raaw Energy’s recall impacts frozen dog food products manufactured between July 17, 2025, and Dec. 23, 2025, along with one batch of “Beef and Turkey Medley” dated March 31, 2026, according to a notice from the Food and Drug Administration (FDA).

The recall was issued “out of an abundance of caution” after testing detected listeria in several samples.

“Consumers are advised not to use, sell, or consume any affected product. Please discard these items immediately to help reduce the risk of illness,” the FDA said.

WHOLE FOODS MINESTRONE SOUP RECALLED IN 17 STATES OVER POSSIBLE LIFE-THREATENING ALLERGIC REACTION

Raaw Energy’s recall impacts frozen dog food products manufactured between July 17, 2025, and Dec. 23, 2025, along with one batch of “Beef and Turkey Medley” dated March 31, 2026. (Getty Images / Getty Images)

The recalled products were sold in 2-pound and 5-pound clear plastic tubes packaged inside brown cardboard boxes and distributed through the company’s website and pickup locations in Connecticut, Delaware, Massachusetts, Maryland, New Hampshire, New Jersey, New York, Pennsylvania and Virginia.

The company’s recall includes a wide variety of products, including “Beef and Chicken,” “Beef and Turkey Medley,” “Chicken Medley,” “Hybrid Dog’s Best Friend,” and more.

Listeria can spread through contaminated pet food and surfaces that come into contact with it, including pet bowls, countertops and utensils, according to the FDA.

COSTCO PATIO SWINGS RECALLED AFTER SEAT DETACHMENTS LEAD TO INJURIES

The recalled products were sold in 2-pound and 5-pound clear plastic tubes packaged inside brown cardboard boxes and distributed through the company’s website and pickup locations. (iStock / iStock)

In humans, listeria infections can trigger nausea, vomiting, diarrhea, fever and muscle aches. Severe cases may spread to the nervous system and cause meningitis, pregnancy complications or death.

“Severe infections can result in meningitis, abortion and death. Pets exposed to contaminated food can be infected without showing symptoms,” the FDA warned.

Raaw Energy also said it has temporarily halted all dog food production, effective last Thursday, May 21, 2026, as the company addresses sanitation concerns.

PET FOOD SOLD NATIONWIDE RECALLED OVER POTENTIAL SALMONELLA RISK

Listeria can spread through contaminated pet food and surfaces that come into contact with it, including pet bowls, countertops and utensils, according to the FDA. (iStock / iStock)

GET FOX BUSINESS ON THE GO BY CLICKING HERE

“We sincerely apologize for any inconvenience this may cause. As a small business, we are committed to doing the right thing and correct any issues,” Raaw Energy said in a statement.

“We appreciate your patience and understanding as we focus on making these improvements and ensuring that our products meet the standards our customers expect and deserve.”

The FDA first announced the recall in January. Consumers can view the complete list of recalled products on the FDA’s website.

Raaw Energy did not immediately respond to FOX Business’ request for comment.

ASEAN showcases its resilience by turning global challenges into opportunities for enhanced integration and sustainable growth. Despite ongoing conflicts driving up commodity prices and straining economies, ASEAN remains committed to dialogue, institution-building, and fostering mutual restraint.

🌏 ASEAN’s Resilience and Strategy

- Resilience through cooperation: ASEAN has consistently turned crises into opportunities by prioritizing dialogue, institution-building, and restraint over escalation.

- Historic milestones: The ASEAN Free Trade Area (1992) and ASEAN Economic Community (2000s) deepened integration and investor confidence.

- Crisis-driven reforms: The Asian financial crisis led to the ASEAN Surveillance Process (1998) and Chiang Mai Initiative (2000). COVID-19 prompted the Hanoi Plan of Action to safeguard supply chains.

📈 Economic Growth and Integration

- Strong performance: ASEAN’s GDP grew from $2.5T (2015) to $4.3T (2025); trade nearly doubled to $4.4T; FDI rose from $115B to $242B.

- Future outlook: The Asian Development Bank projects 4.6% growth in 2026, driven by domestic demand and infrastructure investment.

⚡ Energy and Technology Drivers

- Energy transition: Demand surged 35% in the past decade; clean energy investment ($47B in 2025) nearly matched fossil fuels. Initiatives include the ASEAN Power Grid and cross-border integration projects.

- Digital economy: The Digital Economy Framework Agreement (DEFA) could double ASEAN’s digital economy to $2T by 2030, leveraging youth demographics and rapid tech adoption.

🌐 Geopolitical and Regional Challenges

- External pressures: Conflicts raise commodity prices and disrupt trade routes, but ASEAN emphasizes resilience as a condition for growth.

- Regional issues: ASEAN supports humanitarian aid in Myanmar and promotes dialogue on South China Sea disputes. Timor-Leste’s accession in 2025 highlights inclusiveness and adaptability.

The bloc’s history shows a recurring ability to adapt, from the ASEAN Free Trade Area to the ASEAN Economic Community, strengthening trade and investor confidence. This adaptability, coupled with a focus on energy transformation and digital cooperation, positions ASEAN to navigate geopolitical shifts and continue its economic expansion, making resilience its strategic advantage in a fragmented world.

Read More : Building ASEAN’s resilience to fuel further economic growth | World Economic Forum

Other People are Reading

Why Are Global Investors Looking To Asia As An Investment Destination?

Business

Possible fissure in California chemical tank may help prevent explosion, fire official says

Possible fissure in California chemical tank may help prevent explosion, fire official says

Uber weighs higher bid for Delivery Hero, FT reports

A company of Manulife Investment Management, John Hancock Investment Management serves investors through a unique multimanager approach, complementing our extensive in-house capabilities with an unrivaled network of specialized asset managers, backed by some of the most rigorous investment oversight in the industry. The result is a diverse lineup of time-tested investments from a premier asset manager with a heritage of financial stewardship. Note: This account is not managed or monitored by John Hancock Investment Management, and any messages sent via Seeking Alpha will not receive a response. For inquiries or communication, please use John Hancock Investment Management’s official channels.

Forensic experts sift through ruined dormitory in Russian-held Luhansk region

Calamos Investments is a diversified global investment firm offering innovative investment strategies including U.S. growth equity, global equity, convertible, multi-asset and alternatives. The firm offers strategies through separately managed portfolios, mutual funds, closed-end funds, private funds, an exchange traded fund and UCITS funds. Clients include major corporations, pension funds, endowments, foundations and individuals, as well as the financial advisors and consultants who serve them. Headquartered in the Chicago metropolitan area, the firm also has offices in London, New York and San Francisco. For more information, please visit www.calamos.com.

Check out what’s clicking on FoxBusiness.com.

Guzman y Gomez Mexican Kitchen, an Australian-born Chipotle rival that once planned to open hundreds of U.S. locations, has abruptly closed all of its American restaurants after six years in the Chicago area.

“All GYG USA restaurants permanently closed,” a message on the company’s U.S. website says. “Effective from May 22nd, GYG USA restaurants will cease trading. Thank you for your support.”

The chain also announced the move on Instagram, thanking customers and employees in Chicagoland, where all eight of its U.S. restaurants were located.

“After six years of burritos and big dreams in Chicagoland, we’ve made the difficult decision to close our US restaurants,” the post read. “To every guest who came through our doors – you chose us, and we never took that for granted.”

CAVA BUCKS RESTAURANT INDUSTRY TREND WITH SUCCESSFUL NO-DISCOUNT STRATEGY

A Guzman y Gomez restaurant in Sydney, Australia, on Wednesday, Feb. 18, 2026. (Brent Lewin/Bloomberg via Getty Images / Getty Images)

Guzman y Gomez’s U.S. website shows just a message of its sudden closing Friday.

“To our team – thank you. Your passion and your purpose built something special. If you’re ever in Australia, Singapore or Japan, come find us – we’ll have your favs waiting for you. Chicagoland, Thank you!”

The shutdown marks a sharp reversal for Guzman y Gomez, which had recently reaffirmed its intent to expand in the U.S. market. The company (ASX: GYG) was founded in Australia by native New Yorkers Steven Marks and Robert Hazan and made its U.S. debut in 2020 with ambitions to build a much larger American footprint.

“I have always been confident in the differentiation of our food and guest experience, however this was not translating to an improvement in sales momentum,” Marks said in an Australian Securities Exchange announcement, Business News Australia reported.

An employee prepares food at a Guzman y Gomez restaurant in Sydney, Australia, on Wednesday, Dec. 13, 2023. (Brent Lewin/Bloomberg via Getty Images / Getty Images)

“Having spent the last three months in the US, I realized this was going to take significantly more time and capital than we had expected.

“In assessing the trajectory of the current network, the board and I have concluded that the business is unlikely to deliver the performance that would justify continued investment of shareholder capital.”

FMR FAST FOOD CEO PREDICTS MORE RESTAURANTS WILL CLOSE NATIONWIDE OVER HIGHER PRICES

Guzman y Gomez says adios to the U.S., but remains active in Australia, Japan and Singapore. (Guzman Y Gomez/Instagram / Unknown)

The company chose the Chicago area as its entry point. At the time, its founders said they intended to open “hundreds, if not thousands” of Guzman y Gomez locations across the country.

Instead, the company is exiting the U.S. entirely, which has helped is stock price in Australia surge more than $3 Australian from $18.05 to $21.10 when the news dropped Friday morning.

“We have a long runway ahead of us in Australia as we progress towards our longterm target of 1,000 restaurants and segment underlying EBITDA as a percentage of network sales of 10%,” Marks said.

“Concentrating our capital, focus and infrastructure behind this opportunity is the most effective way to compound shareholder value over the long term.”

The retreat comes as U.S. restaurants face pressure from cautious consumers, higher food costs and declining traffic.

ITALIAN RESTAURANT CHAIN FILES FOR BANKRUPTCY, CITING INFLATION AND HIGHER INTEREST RATES

Guzman y Gomez (ASX: GYG), an Australian-based Chipotle rival in Chicago, is forced to close all its Chicago-area restaurants. (Brent Lewin/Bloomberg via Getty Images / Getty Images)

TheStreet reported that three in 10 Americans have cut back on retail spending and restaurant visits compared with a year earlier, citing S&P Global data. Food-away-from-home prices rose 39.3% from January 2019 to January 2026, far faster than in the previous seven-year period, according to the same report.

Those headwinds have weighed on chains across the industry, especially those trying to scale in crowded categories.

Guzman y Gomez positioned itself as a cleaner take on fast-casual Mexican food, touting no added preservatives, no artificial flavors, no added colors and no “unacceptable additives” on its Australian website.

Its U.S. closure leaves Chipotle — which has roughly 4,000 restaurants — without one of its smaller fast-casual Mexican challengers in the American market.

| Ticker | Security | Last | Change | Change % |

|---|---|---|---|---|

| CMG | CHIPOTLE MEXICAN GRILL INC. | 32.89 | +0.09 | +0.27% |

| CAVA | CAVA GROUP INC | 80.42 | -0.85 | -1.05% |

| QSR | RESTAURANT BRANDS INTERNATIONAL INC. | 75.38 | -0.87 | -1.14% |

GET FOX BUSINESS ON THE GO BY CLICKING HERE

RBC Capital Markets analyst Michael Toner told Reuters the exit could be positive for Guzman y Gomez’s broader business because its U.S. operations had limited prospects and were weighing on earnings.

“The U.S. business had very low prospects of being successful, and the losses of the business were weighing down the earnings of the group so the sooner exit than anticipated is positive,” Toner said.

Reuters contributed to this report.

GPS signals of RAF jet carrying defence secretary ‘jammed by Russia’

Michael Saylor’s “BitVac” Post Fuels New Strategy Bitcoin Buy Speculation

Dream rally to stun Mercury

US brings back mandatory military draft registration

Steven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

Register Renaming | Hackaday

CONTACT ME THROUGH MY EMAIL FOR GUIDANCE.#crypto #usa #xrp #xrppripple #cryptocurrency #viral.

Do you have financial advice for couples?

Escape the Rat Race. The Matt Kempke Story. #podcast #mattkempke #magabitcoin #cryptocurrency

-

Crypto World3 days ago

Crypto World3 days agoBlockchain.com files with SEC for U.S. IPO

-

Fashion2 days ago

Fashion2 days agoHoliday Weekend Open Thread – Corporette.com

-

Crypto World3 days ago

Crypto World3 days agoBitcoin Accumulation Weakens as BTC Realized Losses Hit $600M

-

Business2 days ago

Business2 days agoDell Technologies DELL Stock Surges 15% on AI Server Momentum and Analyst Upgrades in 2026

-

Crypto World2 days ago

Crypto World2 days agoSpace X IPO Is ‘Bad News’ for Tech Stocks: But What About Bitcoin?

-

Politics2 days ago

Politics2 days agoMakerfield: a tale of two social-media histories

-

Crypto World3 days ago

Crypto World3 days agoMicroStrategy’s Saylor Says Miners No Longer Set Bitcoin Price, Another Force Has Taken Over

-

Crypto World2 days ago

Crypto World2 days agoRobinhood crypto COO Tanya Denisova exits

-

Business4 hours ago

Business4 hours agoNYT Strands Answers May 24 2026 Revealed for Puzzle No. 812 Theme Summer Essentials

-

Tech2 days ago

Tech2 days agoA 0.12% parameter add-on gives AI agents the working memory RAG can’t

-

Crypto World2 days ago

Crypto World2 days agoAI infrastructure race heats up as IREN pitches full-stack strategy, WhiteFiber lands $160M deal

-

Tech3 days ago

Tech3 days agoWhatsApp ads could make Irish debut after discussions with DPC

-

Business3 days ago

Business3 days agoTrump Invests $1M-$5M in Kura Sushi USA Chain With 27 California Locations

-

Tech3 days ago

Tech3 days agoYou Can Now Add ChatGPT To PowerPoint

-

Crypto World6 days ago

Revolut Launches Dogecoin Debit Card Across UK and EU

-

Sports3 days ago

Sports3 days ago2026 CJ Cup Byron Nelson leaderboard: Brooks Koepka finds putting stroke in Round 1

-

Crypto World3 days ago

Crypto World3 days agoTrump Media’s Bitcoin Stash Shrinks Again as 2,650 BTC Lands on Crypto.com

-

NewsBeat3 days ago

NewsBeat3 days agoCharity run by Reform leader Malcolm Offord accused of ‘law breaking’ over Scottish registration

-

Business3 days ago

Goldman Sachs reinstates Ageas stock coverage with neutral rating

-

Crypto World4 days ago

Crypto World4 days agoExa Labs raises $250 million in funding led by a16z

You must be logged in to post a comment Login