Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

For markets, US Federal Reserve chief Jay Powell is the Grinch who stole Christmas. But the festive shakeout in bonds, currencies and stocks now under way in the wake of the US central bank’s latest pronouncements is a mini-crisis of investors’ own making.

Fed meetings, and the minutiae of its public statements, are always marquee events for investors, setting the tone across all major asset classes. Wednesday’s meeting, the last of 2024, always came with the potential for greater punch, given the timing — right on the cusp of Donald Trump’s second stint in the White House.

The decision on rates itself — a quarter-point chop off the benchmark — was in line with expectations. But it went downhill from there, as the central bank’s apparent cooling on further cuts next year — an allusion to the potentially inflationary impact of Trump’s economic policies — has gone down like a mouldy mince pie.

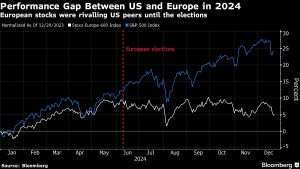

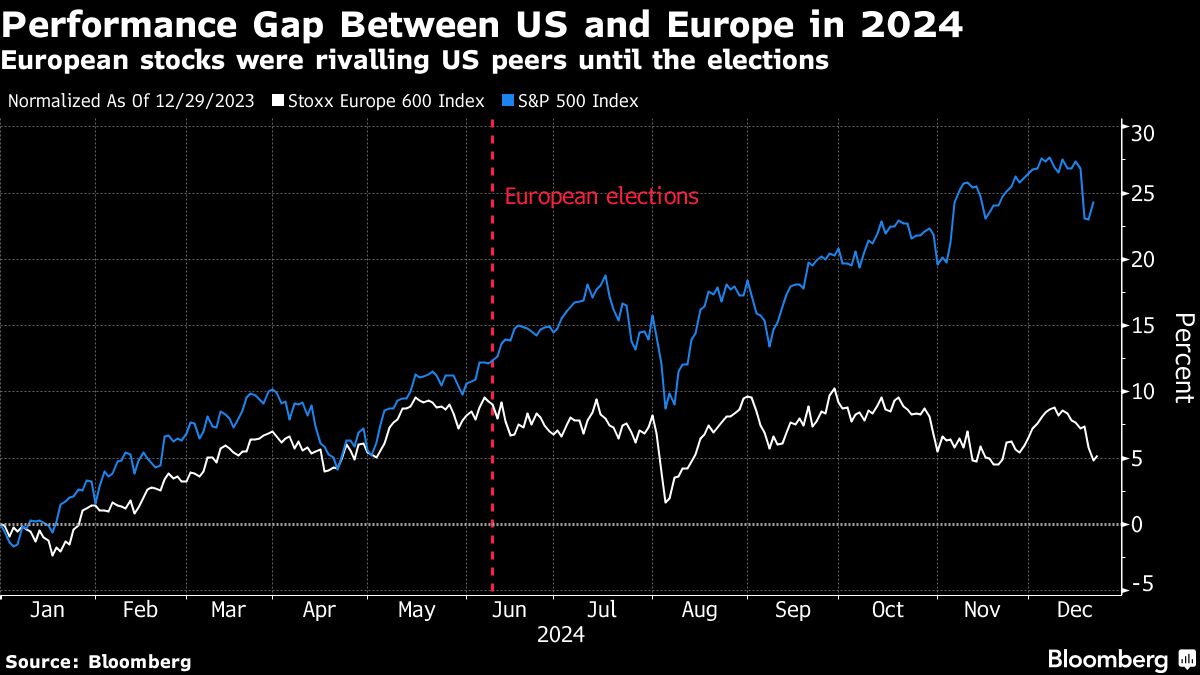

US stocks nosedived, wiping out almost all of the gains in the S&P 500 benchmark index since Trump’s re-election day. The following morning brought a similar sea of red across Asian and European stocks too. The dollar popped higher, sending the euro and yen tumbling awkwardly hard, and US government bonds weakened, sending the yield on 10-year Treasuries forcefully above 4.5 per cent.

The Fed chair is facing some flak here. His comment in the post-meeting press conference that the year-end projection for inflation has “kind of fallen apart” is not the sort of self-assertion that investors seek in a Fed chair, and the pick-up in some inflation measures comfortably predates the reinauguration of Trump.

But markets are going through the wringer in no small part because the consensus among investors about the next steps for markets had become so intense — curdling hard around the themes of American exceptionalism in stocks and the vanquishing of inflation keeping bonds well supported. The path to an easy run in markets in 2025 had become exceptionally narrow and extremely crowded with like-minded views, and it has taken only a gentle push from the Fed to tip that out of balance.

The annual spectacle of year-ahead market outlooks from the big banks and asset managers demonstrated a near-unanimous set of views. Deutsche Bank is towards the top of the pack with its assessment that the benchmark S&P 500 index of heavyweight US stocks will ascend to 7,000 by the end of next year. After the overnight shock, that projection is 20 per cent above where we are now. It is punchy, but not wildly out of line. Core fundamental differences of opinion are hard to find. “The degree of uniformity in year-ahead projections has broken all previous records,” notes TS Lombard’s Dario Perkins.

The trouble with that was two-fold. First, it meant much, if not all, of the narrative was already baked in. Second, crowding around core themes tends to exaggerate the scale of market reactions when stuff goes wrong. Enter Powell stage left.

“Everyone’s portfolio is pointed towards US exceptionalism,” said Mike Riddell, a portfolio manager on Fidelity’s Strategic Bond Fund, speaking with some foresight the week before the Fed decision. “The consensus can be right, and we don’t see much to derail it. But if you see anything to move the narrative, you can get really violent market moves.”

We have been here before, in a range of different markets, but that does not prevent investors from making the same mistake over and over again. This time last year, Powell caught the market off guard in the opposite direction, dropping a hint of interest rate cuts that investors went on to exaggerate hugely out of proportion.

Crowded bets among investors also stung in early August, when a downbeat US labour market report blasted in to several popular and correlated market bets. In late September, deeply unloved Chinese stocks rocketed higher after Beijing unleashed stimulus measures to try and turn the hobbled economy and markets around. Investors had given China such a wide berth that stocks leapt 40 per cent in just a few days as funds piled in to a narrow entrance.

The latest ructions are a useful reminder that despite the disarming simplicity of the American exceptionalism theme, rakes are scattered all over markets for investors next year.

The assumption that the US economy will sail through the first year of Trump 2.0 is brave. Ignoring the (actually pretty obvious) banana skins, particularly around inflation, is “the ultimate ‘trust me’ trade” says Greg Peters, co-chief investment officer for PGIM Fixed Income. “It seems off to me.”

Now, investors should not assume that the Christmas holiday season will put all this angst to bed. As the final days of 2018 showed, portfolios can and do shake around wildly even when a lot of core markets are shut, on half-days, or on the go-slow. If anything, thinned-out trading volumes at this time of year can make matters worse.

Some fund managers will be feeling sore about this year-end beating. But Powell has done us all a favour in reminding us that next year will not be for the faint of heart, and the wisdom of crowds is not always your friend.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

+ There are no comments

Add yours