Stay informed with free updates

Simply sign up to the US equities myFT Digest — delivered directly to your inbox.

Lofty expectations for US corporate profits mean that the flood of earnings reports due in the coming fortnight will play a particularly important role in setting the direction for Wall Street stocks, investors say, after a shaky start to 2025.

The S&P 500 had its best week since the November US election last week, aided by strong numbers from the biggest banks, pushing the index back into the black for January.

But investors say a strong showing is needed from the many household names — worth a combined $25tn — due to report before the end of January, if the market is to surpass the record high it hit last month.

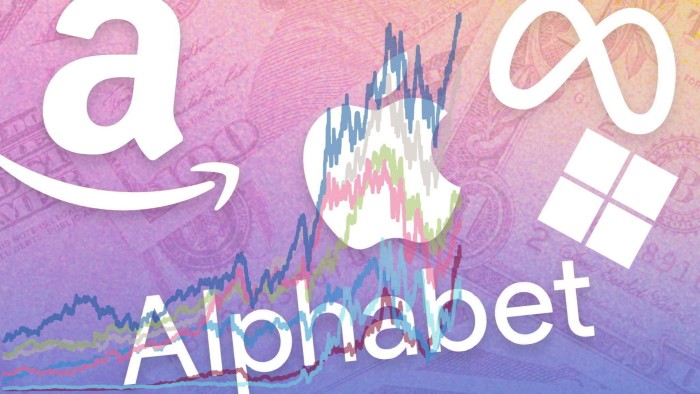

Analysts are forecasting the best quarterly results in three years, with S&P 500 companies’ net profits expected to have risen 11.4 per cent year-on-year, according to FactSet.

The index soared 23 per cent last year as demand for artificial intelligence-related stocks powered gains for tech companies. That has put the S&P on a forward price/earnings ratio of 21 times, according to data from LSEG.

“The market cannot rely on multiple expansions to boost returns because of how much [they] already expanded in 2024,” said Jurrien Timmer, Fidelity Investments’ global head of macro.

“That puts the burden more on earnings to be the main contributor for the market’s return,” he added, also pointing to jitters over higher interest rates.

On average, a negative January for stocks leads to a median return of 2.5 per cent for the rest of the year, according to Barclays strategists. An opening month with gains of at least 1.5 per cent, however, tends to result in annual returns of more than 11 per cent.

After notching up a series of record highs in 2024, stocks have stumbled in recent weeks, buffeted by worries about the potential for higher interest rates to hurt economic growth and uncertainty about likely early actions by the incoming Trump administration.

Companies including Netflix, GE and consumer products group Procter & Gamble are among those set to report this week. Technology giants including Amazon, Microsoft, Facebook parent Meta and Tesla are due the week after.

The highest growth is still expected to come from the tech sector, including the so-called Magnificent Seven, but investors are also looking for signs of improving profitability among other sectors in the hope that this will ease the S&P 500’s dependence on a handful of stocks.

Earnings for the Magnificent Seven — Apple, Microsoft, Alphabet, Amazon, Tesla, Meta and Nvidia — are predicted to rise 21 per cent this year, slowing from a rate of 33 per cent in 2024, according to FactSet. Earnings growth for the other 493 stocks in the index is expected to pick up to 13 per cent, from 4 per cent.

Market participants will also watch closely for executives’ thoughts on incoming President Donald Trump’s likely policy agenda, with market gains since his November election victory being based in part on hopes for business-boosting deregulation and tax cuts.

Concerns about Trump’s actions have also got the potential to take the gloss off even strong earnings updates, if the president moves early on some of his tariff threats, which could hurt the outlook for multinationals.

Roughly 30 per cent of revenues for S&P 500 companies are generated outside the US, with every 10 per cent rise in the dollar translating to a 3 per cent hit to the average company’s earnings per share.

“The differential in growth rates between the Magnificent Seven and the rest of the market is key, but I’m much more interested in companies’ guidance relating to the pro-business narrative since the election,” said Kevin Gordon, senior investment strategist at Charles Schwab.

“We could see a mismatch between frothy animal spirits and potentially disappointing numbers for last quarter. I wouldn’t hang my hat on the idea that deregulation [under Trump] will be a huge growth story,” he added.

Additional reporting by Ray Douglas

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

+ There are no comments

Add yours