Business

Timberwolves Acquire Julian Phillips in Multi-Player Deal With Bulls

Julian Phillips is on the move again. The Minnesota Timberwolves have acquired the 22-year-old forward from the Chicago Bulls as part of a blockbuster trade that also sends guard Ayo Dosunmu to Minnesota while Chicago receives rookie guard Rob Dillingham, forward Leonard Miller and four second-round draft picks.

Phillips, who has been sidelined with a wrist injury, spent the past three seasons in Chicago without ever establishing a consistent NBA role. Across 154 career regular-season appearances, he averaged just 11.6 minutes per game, often shuttling between the Bulls’ rotation and the G League.

Bulls continue aggressive roster teardown

The trade marks another significant step in Chicago’s ongoing rebuild, as the front office has aggressively flipped veterans for youth and draft capital ahead of the February deadline. Including this deal, reports indicate the Bulls have accumulated nine second-round picks and nine new players through recent transactions.

Dosunmu, 26, was enjoying a breakout fifth NBA season in his hometown, averaging career highs of 15 points, 3.6 assists and 3 rebounds while shooting over 51 percent from the field and 45 percent from three. Selected by Chicago in the 2021 second round after starring at Illinois, he earned All-Rookie honors but now heads to Minnesota as a key piece for their Western Conference push.

For the Bulls, parting with Dosunmu’s production in exchange for high-upside prospects like Dillingham—who Minnesota selected with an unprotected 2031 first-round pick—and Miller represents a clear bet on the future. Dillingham showed rookie flashes but struggled for consistent minutes behind Minnesota’s established backcourt, while Miller offers size and athleticism as Chicago’s tallest rotation option.

Phillips’ journeyman path to Minnesota

Phillips enters the league as the 35th overall pick in the 2023 NBA Draft after a promising one-and-done freshman season at Tennessee, where he averaged 8.3 points and 4.7 rebounds while earning Battle 4 Atlantis All-Tournament honors. A consensus five-star recruit originally committed to LSU, Phillips decommitted after a coaching change and chose the Volunteers over South Carolina and Auburn.

In Chicago, the 6-foot-8 forward was viewed as a defensive prospect with high upside but never translated that potential into steady NBA minutes. Limited by injuries—including his current wrist issue—and a crowded wing rotation, Phillips bounced between the Bulls and their G League affiliate, appearing in just 154 games over three seasons. Fantasy analysts consistently described him as a “depth piece” with bleak production outlook due to minute restrictions.

Now in Minnesota, Phillips faces similar challenges on a deep, contending roster. He is listed as questionable for a potential debut Friday against the Pelicans, pending wrist recovery and coach Chris Finch’s rotation decisions. With established wings like Jaden McDaniels, Kyle Anderson and others ahead of him, consistent minutes appear unlikely in the short term.

Timberwolves reinforce depth for playoff run

Minnesota’s motivation in the deal centers on Dosunmu, who fills a critical need at backup point guard following the recent trade of Mike Conley. The Timberwolves have lacked reliable lead ball-handling off the bench this season, and Dosunmu’s scoring efficiency, defensive versatility and Chicago breakout make him an immediate fit alongside Bones Hyland and Jaylen Clark.

Including Phillips provides additional frontcourt depth, though his role will likely remain situational. The cost—Dillingham, Miller and four second-rounders—is significant but preserves Minnesota’s first-round picks while adding a low-risk, high-ceiling wing prospect. Reports emphasize that Phillips “won’t benefit much from a change of scenery” given the Wolves’ crowded depth chart, positioning him as organizational depth rather than rotation staple.

Fantasy impact muted across the board

Fantasy basketball analysts have downplayed the deal’s immediate relevance. Phillips’ outlook “remains bleak” due to Minnesota’s minutes crunch, while Dillingham joins a loaded Chicago guard room without a clear path. Miller could see rotation opportunities as the Bulls’ tallest player but lacks standard-league appeal. Dosunmu stands to gain the most, potentially as Minnesota’s primary bench lead guard.

Broader implications for both franchises

For Chicago, the transaction accelerates a rebuild that has already seen departures of Nikola Vučević, Coby White and others. With nine second-round picks and a youth movement underway, the Bulls are prioritizing flexibility over Eastern Conference mediocrity. Dillingham’s upside and Miller’s physical tools headline the return, potentially forming cornerstones if they develop behind Chicago’s crowded backcourt.

Minnesota, twice a Western Conference Finals participant, doubles down on win-now depth. Dosunmu addresses backcourt turnover concerns, while Phillips offers injury insurance without long-term salary commitment. The price tag reflects confidence in the current core’s championship ceiling, even as it mortgages some future assets.

Phillips’ NBA journey continues in a familiar depth role, but the fresh scenery in Minnesota—combined with his youth and defensive tools—keeps developmental intrigue alive. Whether he carves a niche on a contender or emerges as a trade chip remains the key storyline.

Business

Stock market holiday today for Gudi Padwa 2026: Are NSE & BSE open or closed for Gudi Padwa celebration? Check now

The country’s largest non-agricultural commodity exchange, the Multi Commodity Exchange of India (MCX) will also open at 9 am while the largest agricultural bourse, the National Commodity & Derivatives Exchange (NCDEX) will resume trading at 10 am.

Meanwhile, the currency market will remain shut today.

The equity markets were closed on March 3 for Holi and will be closed on two other occasions in this month. They will be closed on Thursday, March 26 for Shri Ram Navami and on Tuesday, March 31 for Shri Mahavir Jayanti.

Indian benchmark indices ended with sharp gains on Tuesday, recording their third successive positive closing. Action in auto, IT and consumer stocks lifted the mood with strong support from financials. The broader Nifty surged 196.65 points, or 0.83%, to close at 23,777.80, while the 30-share Sensex gained 567.99 points, or 0.83%, to settle at 76,704.13.

The fear index India VIX fell 5.5% in the previous session to settle at 18.72.

2026 holiday list

In the holiday calendar released last year, the exchanges had initially announced 15 trading holidays but later added January 15 as an additional holiday on account of the Mumbai BMC elections. After this, the domestic markets were closed on January 26 on account of a Republic Day.

The next holiday will fall on Friday, April 3 which will be a Good Friday. Markets will also be shut on Ambedkar Jayanti on April 14, Maharashtra Day on May 1 and Bakri Id on May 28.

The second half of the year includes Muharram on June 26, Ganesh Chaturthi on September 14 and Gandhi Jayanti on October 2. Dussehra falls on October 20, followed by Diwali Balipratipada on November 10 and Guru Nanak Jayanti on November 24. The final trading holiday of the year will be Christmas on December 25.

The small surprise in the circular is that there is no mention of holiday for Diwali as it is falling on a weekend (Sunday). The Muhurat Trading will be conducted on Sunday, November 08, 2026 and the timings of Muhurat Trading will be notified subsequently.

The exchanges may alter any of the above holidays, for which a separate circular shall be issued in advance.

(Disclaimer: The recommendations, suggestions, views, and opinions given by the experts are their own. These do not represent the views of The Economic Times.)

Rep. Jodey Arrington, R-Texas, explains how Fed Chair pick Kevin Warsh will restore integrity in the Federal Reserve on The Bottom Line.

The U.S. national debt reached another historic milestone on Wednesday as it surpassed $39 trillion for the first time as the federal government’s persistent budget deficits send the debt soaring higher.

New data from the Treasury Department released on Wednesday showed that the gross national debt reached $39,016,762,910,245.14 as of March 17.

The $39 trillion milestone comes about five months after the national debt reached $38 trillion for the first time in late October 2025, which closely followed the $37 trillion milestone being surpassed just two months earlier in mid-August.

America’s debt has grown rapidly over the last decade as the population ages and federal spending on Social Security and Medicare rises. Another key driver of the surging debt is interest expenses incurred from servicing the debt, which have swelled due to higher interest rates meant to curb inflation as well as the growth in the debt itself.

US DEBT SET TO CRUSH WORLD WAR II RECORD AS ANNUAL DEFICITS EXPLODE TO $3T WITHIN DECADE

Michael A. Peterson, CEO of the nonpartisan Peter G. Peterson Foundation, told FOX Business that the latest national debt milestone is an opportunity for Americans to “recognize this alarming rate of growth and the significant financial burden we are putting on the next generation.”

“At the current growth rate, we will hit a staggering $40 trillion in national debt before this fall’s elections. Borrowing trillion after trillion at this rapid pace with no plan in place is the definition of unsustainable,” he explained.

Peterson noted that interest payments on the debt – the cost of servicing the debt the federal government has incurred – are the fastest growing line item in the federal budget and that interest costs are projected to total nearly $100 trillion over the next 30 years.

BUDGET DEFICIT HITS $1 TRILLION IN FIRST FIVE MONTHS OF FISCAL YEAR: CBO

The national debt surpassed $39 trillion for the first time in U.S. history this week. (Demetrius Freeman/The Washington Post via Getty Images / Getty Images)

He went on to say that with voters concerned about affordability, the debt’s cost and economic impact on Americans’ livelihoods should serve as cause for the issue to be a focal point of the debate surrounding this year’s elections.

“America faces complex and critical challenges, both at home and abroad, and putting our debt on a sustainable path will support a stronger, more secure future. The good news is that there are many solutions available, and they all should be put on the table for discussion this campaign season,” Peterson added.

The fiscal headwinds facing the federal government are expected to continue in the years ahead, as spending on programs like Social Security and Medicare rise along with debt service costs and cause projected budget deficits to widen.

WHAT ARE THE BIGGEST BUDGET DEFICITS IN US HISTORY?

The nonpartisan Congressional Budget Office (CBO) released a 10-year budget and economic forecasts which estimated annual budget deficits will rise from their current level of about $1.9 trillion to $3.1 trillion a year a decade from now. That will push the gross national debt from its current level around $39 trillion to $63 trillion in 2036.

Debt held by the public as a share of gross domestic product (GDP), a measure economists prefer to use in comparing a nation’s debt to the size of its economy, will rise from about 100% this year to 108% of GDP in 2030 and further to 120% in 2036.

Those figures will break the record of 106% set in 1946 as the U.S. was in the process of demobilization after the end of World War II.

GET FOX BUSINESS ON THE GO BY CLICKING HERE

A recent update from the CBO found that the federal government’s budget deficit for the current fiscal year 2026 topped $1 trillion in the first five months of the fiscal year despite an influx of tax revenue from tariffs, some of which were struck down by the Supreme Court as being illegal.

Some of those tariff revenues may be subject to refunds to the businesses and consumers who paid them, which could widen this year’s deficit if the revenue isn’t replaced.

Up to half of steel used in Britain should be made there, the government says, as it announces its steel strategy.

With the 2026 FIFA World Cup just over three months away, kicking off June 11 across 16 venues in the United States, Canada and Mexico, early predictions and betting markets point to Spain as the frontrunner to lift the trophy in the expanded 48-team tournament’s final at MetLife Stadium in East Rutherford, New Jersey, on July 19.

As of mid-March 2026, Spain holds steady as the betting favorite across major sportsbooks like DraftKings, BetMGM, FanDuel and prediction markets such as Polymarket and Kalshi. Odds list Spain at +400 to +450 (implying roughly 18-20% probability), buoyed by their dominant UEFA qualifying campaign, recent European Championship success and a deep, balanced squad featuring young talents like Lamine Yamal alongside veterans.

England follows closely at +550 to +600, benefiting from a strong core led by Jude Bellingham, Harry Kane and Phil Foden, though questions linger about their ability to translate domestic talent into international silverware. France sits third at +650 to +750, with Kylian Mbappé’s form and defensive solidity keeping them in contention despite recent inconsistencies. Brazil and defending champion Argentina round out the top tier at +750 to +800, with Brazil’s attacking flair and Argentina’s Lionel Messi-led experience (potentially his final tournament) making them perennial threats.

Portugal (+1100), Germany (+1200 to +1400) and the Netherlands (+1600 to +2000) follow as strong challengers. Norway (+2200 to +2500) garners attention as a potential dark horse, powered by Erling Haaland’s goal-scoring prowess and Martin Ødegaard’s creativity. Belgium (+3000) and Italy (around +3300, pending playoff qualification) remain in the mix but face steeper paths.

The expanded format — 48 teams across 12 groups of four, with the top two and eight best third-placed teams advancing to a round of 32 — increases unpredictability. Group-stage upsets could propel underdogs deeper, with more matches (104 total) allowing for momentum shifts.

Host nations Mexico, the United States and Canada benefit from home advantage and automatic qualification. The U.S. (+5000 to +6500) draws optimism as co-hosts, with a talented young core including Christian Pulisic, Weston McKennie and emerging stars. Mexico (+7000) and Canada face tougher paths but could leverage crowd support in familiar time zones.

Qualifying nears completion, with 42 of 48 spots filled. March playoffs decide the final European berths: Italy vs. Northern Ireland, Wales vs. Bosnia-Herzegovina, Ukraine vs. Sweden and others. Italy remains a popular pick to qualify at around +3300 overall odds if they advance.

Dark horses include Morocco (+6000), fresh off a 2022 semifinal run, Colombia (+3300 to +4000) with dynamic attacking play, Ecuador (+6600 to +8000) and Senegal (+10000). Norway’s Haaland factor and Japan’s technical discipline make them popular long-shot bets.

The tournament’s scale — spanning cities from Seattle to Miami, Toronto to Mexico City — poses logistical challenges but promises spectacle. MetLife Stadium hosts the final, with iconic venues like AT&T Stadium (Arlington), SoFi Stadium (Inglewood) and Estadio Azteca (Mexico City) staging key matches.

Predictions hinge on form, injuries and adaptation to North American conditions. Spain’s tactical cohesion under Luis de la Fuente gives them an edge, while England’s depth and France’s talent keep them close. Argentina’s experience and Brazil’s flair ensure drama.

As qualifying wraps and friendlies ramp up, the 2026 World Cup promises unprecedented scale and potential surprises in a truly global showcase.

Heavy haulage company MLG Oz has extended its working relationship with Northern Star Resources at the goldminer’s Jundee operations.

Australia’s labour market eased a little in February, despite an extra 48,900 jobs added to the economy, according to official data.

OPINION: US bauxite miner’s contributions to WA can’t hide the fact it’s at odds with community expectations.

Business

Cristiano Ronaldo on Track for 2026 World Cup After Hamstring Injury Setback, Eyes Final Tournament at Age 41

LISBON, Portugal — Cristiano Ronaldo remains on course to represent Portugal at the 2026 FIFA World Cup despite a recent hamstring injury that sidelined him from Al Nassr matches in early March, with recovery timelines pointing to a return in April and full fitness well before the tournament opens in June.

The 41-year-old forward suffered the injury during Al Nassr’s Saudi Pro League win over Al Fayha on February 28, 2026, limping off in the 81st minute. Initial assessments labeled it muscular fatigue, but further tests revealed a more serious hamstring strain, prompting Al Nassr coach Jorge Jesus to describe it as “more serious than expected.” Ronaldo traveled to Madrid for specialized rehabilitation with his personal physiotherapist, a common protocol for elite athletes managing chronic or acute issues.

As of mid-March 2026, updates indicate steady progress. Al Nassr manager Jorge Jesus stated Ronaldo should return after the international break, with Saudi media outlet Al-Sharq Al-Awsat reporting he is expected back in Riyadh by late March, targeting a potential comeback in the league match against Al Najma on April 3. Transfer expert Fabrizio Romano estimated a 2-to-4-week absence, aligning with a mild to moderate strain that typically heals within that window without long-term complications.

The injury raised brief concerns about Ronaldo’s availability for Portugal’s March friendlies against Mexico and the United States, tune-ups for World Cup preparations. However, sources close to the situation confirm the setback was short-term, designed to ensure he returns at full strength rather than risking aggravation. Ronaldo has missed about 13 competitive games this season due to various issues, a higher tally than his previous five-year average of just seven absences, highlighting the physical demands at his age.

Ronaldo has repeatedly affirmed the 2026 World Cup — co-hosted by the United States, Canada and Mexico — will be his last major international tournament. In a November 2025 CNN interview, he stated, “Definitely, yes, because I will be 41 years old” and that it would be “the moment” to step away from the global stage. He reiterated expectations of retiring in one or two years, focusing on family and club football with Al Nassr, where he extended his contract to 2027.

Despite the age milestone, Ronaldo’s form remains elite. He leads Portugal’s all-time scoring charts with 143 international goals and continues prolific output for Al Nassr, scoring 21 goals in 22 league appearances this season before the injury. His physical regimen, access to top medical care and history of overcoming setbacks support optimism for participation. Roberto Martinez, Portugal’s coach, has yet to comment directly on the injury’s impact but maintains confidence in Ronaldo’s leadership and goal threat.

The expanded 48-team format offers more matches and potential pathways, though Portugal’s qualification path remains strong. Ronaldo’s presence would mark a record sixth World Cup appearance, chasing the one major title missing from his resume despite near-misses in 2006, 2010, 2014, 2018 and 2022. Experts view him as a near-certainty for selection if fit, given his status as captain and all-time leading scorer.

Recent statements reinforce his commitment. Ronaldo expressed confidence in his sharpness and enjoyment of the game, telling interviewers he still feels quick and capable of scoring. His recovery in Madrid, incorporating advanced therapies, aims to mitigate risks at his age while preserving explosiveness.

As the World Cup nears, Ronaldo’s participation hinges on avoiding further setbacks. Current timelines position him to resume club duties in early April, allowing months to regain match rhythm and contribute to Portugal’s preparations. Fans and analysts watch closely, with the tournament offering a fitting stage for what Ronaldo has called his final major chapter.

Portugal’s friendlies and summer warm-ups will provide clarity, but signs point to Ronaldo defying age once more on the world’s biggest platform.

In the Nifty 500 pack, 10 stocks gained over 3% and their closing prices crossed above their 200-day DMA (Daily Moving Average) on March 18, 2026, according to StockEdge’s technical scan data. The 200-day daily moving average (DMA) is used by traders as a key indicator for determining the overall trend in a particular stock. As long as the stock is priced above the 200-day SMA on the daily timeframe, it is generally considered to be in an overall uptrend. Take a look:

LightShed partner Rich Greenfield analyzes the Paramount Skydance-Warner Bros deal on The Claman Countdown.

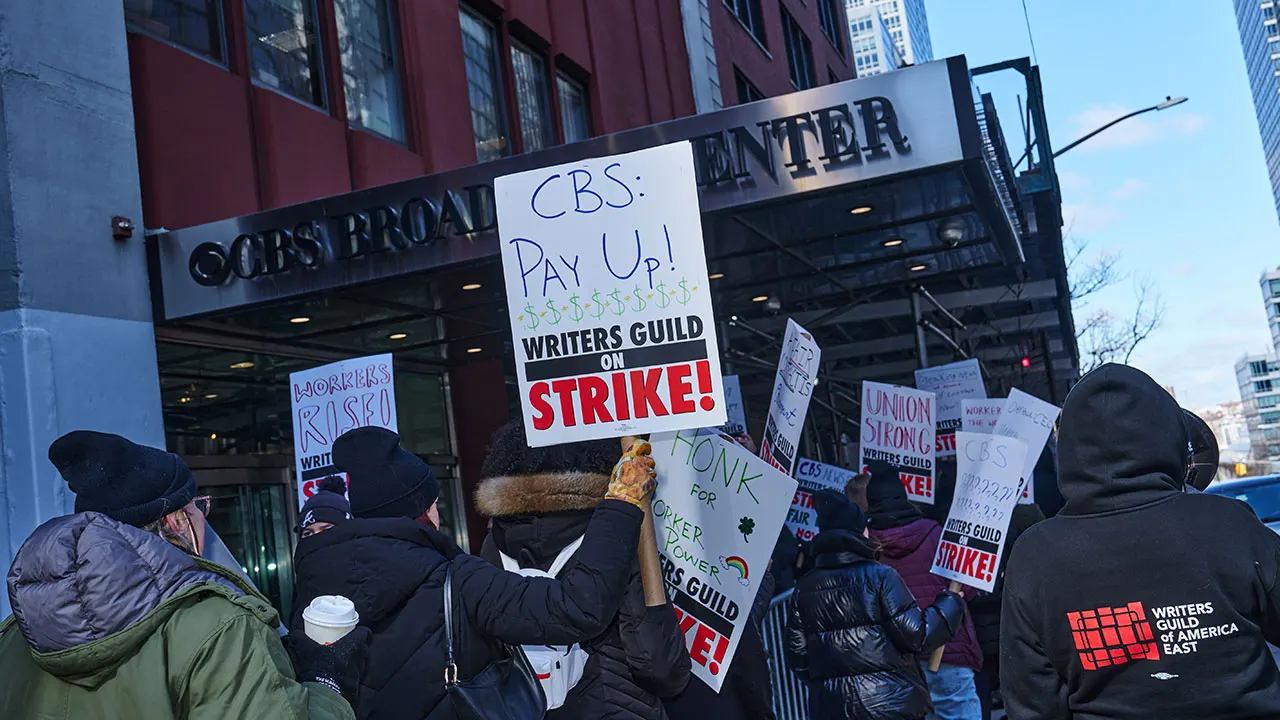

CBS News saw staffers walk off the job on Tuesday amid an ongoing labor dispute.

Writers Guild of America East members at CBS News 24/7 held a 24-hour walkout on Tuesday, claiming management failed to reach an agreement on a new collective bargaining agreement with the 60-member bargaining unit. The current contract expired on March 9, and union members believe CBS is offering a “worse” deal.

Unionized CBS News 24/7 staffers believe they need “to protect their livelihoods during a period of uncertainty in broadcast news,” pointing to “layoffs, editorial interference and political pressure” that have become “existential threats” following last year’s Paramount-Skydance merger, according to the guild.

CBS NEWS IN TRANSITION: WHO’S IN AND WHO’S OUT AFTER A TUMULTUOUS YEAR AT THE NETWORK

Writers Guild of America East members at CBS News 24/7 held a 24-hour walkout on Tuesday. (Bing Guan/Getty Images)

The bargaining unit is asking for “fair pay, respect and a sustainable work-life balance.”

The CBS News 24/7 Union bargaining committee and contract action team told Fox News Digital that “management refuses to agree to a new contract with essential work protections and fair wages,” so a walkout was necessary.

“Despite multiple days of good faith negotiations and a strike pledge signed by 95% of our members to emphasize the seriousness of our demands, management continues to offer us worse terms than in our last contracts. We chose this field to cover the news, but we believe this work stoppage is necessary to achieve a fair contract. We eagerly await an acceptable contract offer from Paramount—which just shelled out tens of billions of dollars to acquire Warner Bros. Discovery,” the CBS News 24/7 Union bargaining committee said.

After the Paramount-Skydance merger closed, David Ellison took control of the combined company and installed Bari Weiss as CBS News’ new editor-in-chief, acquiring her outlet The Free Press in the process.

CBS’ NORAH O’DONNELL CLAIMS COWORKERS ARE ‘FEARFUL’ OVER THE NUMEROUS CHANGES IN LEADERSHIP

A demonstrator wears a Writers Guild of America East sweatshirt during a CBS News strike outside CBS News offices in New York, US, on Tuesday, March 17, 2026. (Bing Guan/Getty Images / Getty Images)

Weiss’ CBS has become a target of the left, who insist the organization has worked to appease the Trump administration, although it has continued to publish critical reports.

Last month, Netflix dropped its bid to buy Warner Bros. Discovery after the studio announced Paramount’s offer to buy the entire company was “superior.” Paramount, the parent company of CBS, is now set to acquire WBD for $31 per share, putting the company’s valuation at $111 billion.

“Paramount has billions to spend acquiring Warner Bros. Discovery, but still hasn’t guaranteed fair wages and basic job protections for the workers who make their streaming news operation run,” WGAE Vice President Beth Godvik said.

“Our members are walking out today to show management they stand united in their demand for a fair contract,” Godvik continued. “And the WGAE is with them every step of the way.”

CBS News editor-in-chief Bari Weiss. (Noam Galai/Getty Images for The Free Press / Getty Images)

CBS News management disagrees with the union.

“We continue to negotiate in good faith and hope to reach a fair resolution quickly,” a CBS News spokesperson told Fox News Digital.

More than 2,900 union members and supporters of the CBS News 24/7 Union have sent letters to management urging them to agree to a fair contract for WGAE members at CBS News 24/7, according to the guild. Tuesday’s walkout featured staffers from CBS News locations in New York and San Francisco.

Paramount slashed roughly 1,000 jobs across the company last fall, many of them affecting CBS News, with plans to cut more.

CLICK HERE TO GET FOX BUSINESS ON THE GO

Fox News Digital’s Joseph A. Wulfsohn contributed to this report.

‘Stopped Drinking Alcohol’: Chahal Makes Big Revelation Ahead Of IPL 2026

Plant will make flowers flourish until end of summer if you sow them now

Stock market holiday today for Gudi Padwa 2026: Are NSE & BSE open or closed for Gudi Padwa celebration? Check now

-

Crypto World5 days ago

Crypto World5 days agoHYPE Token Enters Net Deflation as HyperCore Buybacks Outpace Staking Rewards

-

Tech3 days ago

Tech3 days agoYour Legally Registered ‘Motorcycle’ Might Not Count Under Proposed US Law

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Addict Lip Glow

-

Sports5 days ago

Why Duke and Michigan Are Dead Even Entering Selection Sunday

-

Tech1 day ago

Tech1 day agoAre Split Spacebars the Next Big Gaming Keyboard Trend?

-

Business3 days ago

Business3 days agoSearch for Savannah Guthrie’s Mother Enters Seventh Week with No Arrests

-

Business5 days ago

Business5 days agoUS Airports Launch Donation Drives for Unpaid TSA Workers as Partial Government Shutdown Enters Fifth Week

-

Crypto World4 days ago

Coinbase and Bybit in Investment Talks: Could Bybit Finally Enter the US Crypto Market?

-

Business3 days ago

Business3 days agoAustralian shares drop as Iran war enters third week

-

Business5 days ago

Business5 days agoCountry star Brantley Gilbert enters growing non-alcoholic beer market

-

Crypto World3 days ago

Crypto World3 days agoCrypto Lender BlockFills Enters Chapter 11 with Up to $500M in Liabilities

-

Sports5 days ago

Sports5 days agoCollege Basketball Best Bets: Conference Tournament Semifinal Picks

-

Politics18 hours ago

Politics18 hours agoThe House | The new register to protect children from their abusers shows Parliament at its best

-

Business6 days ago

Business6 days agoTrump demands Powell cut rates as Iran conflict raises energy prices

-

Fashion3 days ago

Fashion3 days ago25 Celebrities with Curly Hair That Are Naturally Beautiful

-

Crypto World6 days ago

Crypto World6 days agoSenate Votes to Include CBDC Ban in Bipartisan Housing Bill

-

News Videos11 hours ago

News Videos11 hours agoRBA board divided on rate cut, unusually buoyant share market | Finance Report | ABC NEWS

-

NewsBeat6 days ago

NewsBeat6 days agoDeane Road crash near Bolton colleges and university

-

News Videos6 days ago

News Videos6 days agoTom Lee: The 100x Opportunity EVEN Bigger Than Bitcoin (New Ethereum Prediction 2026)

-

Crypto World11 hours ago

Crypto World11 hours agoCanada’s FINTRAC revokes registrations of 23 crypto MSBs in AML crackdown

You must be logged in to post a comment Login