Crypto World

Amprius Technologies (AMPX) Stock Surges 8% on Strong Q4 Earnings Beat

Key Highlights

- Q4 earnings per share reached -$0.01, surpassing analyst consensus of -$0.05 by $0.04

- Quarterly revenue totaled $25.23M, exceeding Wall Street projections of $22.91M–$24.5M

- Shares climbed approximately 8% to reach $12.56 in Wednesday trading

- Company insiders offloaded more than 2.39 million shares valued at roughly $26.4M during the previous quarter

- Analyst consensus rating stands at “Moderate Buy” with a mean price target of $16.63

Amprius Technologies delivered quarterly results that exceeded analyst projections, propelling shares higher by roughly 8% during Wednesday’s session.

The battery technology company reported quarterly earnings per share of -$0.01, outperforming Wall Street’s consensus forecast of -$0.04 to -$0.05 by $0.03 to $0.04. Quarterly sales registered at $25.23 million, surpassing analyst expectations that spanned from $22.91M to $24.5M.

Shares concluded midday trading at $12.56, representing a $0.93 gain for the session. Volume activity hit 9.53 million shares, exceeding the typical daily average of 8.12 million.

Amprius Technologies, Inc., AMPX

However, beneath the positive earnings surprise, the financial metrics reveal ongoing profitability challenges. The company recorded a net loss of $24.4 million for the quarter, representing a significant increase from the $11 million loss reported in the comparable year-ago period.

Net margin registered at -53.16% while return on equity came in at -38.85%. While these figures remain deeply negative, investors appeared to focus primarily on the upside earnings surprise and improving operational trajectory.

Looking forward to fiscal 2026, company management issued guidance calling for EPS of approximately -$0.06, indicating continued red ink in upcoming quarters.

Notable Insider Transaction Activity

While market participants reacted positively to the quarterly results, recent insider selling activity suggests a more measured outlook from company leadership.

Chief Technology Officer Constantin Ionel Stefan divested 492,827 shares on January 22nd at a mean price of $12.04 per share, generating proceeds of approximately $5.93 million. This sale reduced his ownership position by 39.7%.

Board member Kang Sun unloaded 950,548 shares on January 16th at $11.07 per share, totaling roughly $10.52 million in proceeds — representing a 40.38% decrease in his holdings.

Cumulatively, company insiders have disposed of 2,392,269 shares valued at approximately $26.4 million during the preceding three-month period. Current insider ownership stands at 12.8% of outstanding shares.

Institutional investors control 5.04% of the company. Bank of America expanded its position by 31.1% during Q4, while Rhumbline Advisers boosted its holdings by 61.1%.

Wall Street Analyst Coverage and Targets

The analyst community maintains a generally optimistic outlook on AMPX shares.

Needham launched coverage on January 29th, assigning a Buy rating alongside a $20 price objective. Craig Hallum initiated coverage on February 23rd, also establishing a Buy rating with a $17 target.

Cantor Fitzgerald upgraded its price target from $12 to $16 while maintaining an Overweight rating. Oppenheimer reiterated an Outperform rating with a $17 target in December.

Weiss Ratings represents the sole bearish voice, continuing to maintain a Sell rating.

Currently, eight analysts assign Buy ratings to the stock, while one maintains a Sell recommendation. The overall consensus rating is “Moderate Buy” with a mean price objective of $16.63.

The equity has traded within a 52-week range of $1.70 to $16.03 and has delivered a remarkable 506% return over the trailing twelve months.

Amprius management is slated to participate in the Cantor Global Tech Conference along with additional investor meetings scheduled for March, which the company highlighted as part of its ongoing shareholder engagement initiatives.

Circle (CRCL) was hit far harder than Coinbase (COIN) in Tuesday’s sharp selloff due to the crypto bill CLARITY Act’s latest stance on stablecoin yield, but one analyst says the regulatory shift may ultimately favor the stablecoin issuer.

Both names are seeing modest bounces on Wednesday, but remain solidly lower since the news leaked Monday evening.

The market may be missing the longer-term implication, argued Markus Thielen, founder of 10x Research: in the current form, the bill weakens Coinbase’s distribution-driven model more than Circle’s infrastructure role.

Coinbase currently captures the majority of USDC economics through its distribution agreement with Circle, Thielen explained. For USDC held on Coinbase, the exchange receives nearly all of the associated interest income, while off-platform balances are generally split about 50%-50. In practice, Thielen estimates that Circle pays Coinbase more than $900 million in revenue share each year, roughly half of Circle’s total revenue.

That arrangement has made stablecoin revenue a high-margin business for Coinbase. But if regulators shut down yield-like rewards on balances, part of that advantage may fade, Thielen said.

“The setup increasingly favors Circle on a relative basis,” Thielen wrote, arguing that the federal framework would shift value toward regulated issuers with compliance, scale and a credible balance sheet.

That could matter even more ahead of the two companies’ next commercial renegotiation in August 2026. Under a stricter federal regime, Thielen sees a better chance that Circle wins improved terms.

Circle could be worth double

Bitwise CIO Matt Hougan, meanwhile, said the selloff in Circle looks “overblown” as the CLARITY Act doesn’t change the long-term investment case.

Yield hasn’t been the main draw to stablecoins, he wrote in a Wednesday note. Most stablecoins don’t pay interest, yet adoption has surged because they make it easier to move dollars across borders, settle trades and access blockchain-based financial rails. In that sense, restricting yield doesn’t change the core use case.

Hougan points to forecasts projecting the market could grow to $1.9 trillion, or even $4 trillion, by the end of the decade. Circle, with a strong position in regulated stablecoins, stands to benefit if more activity shifts toward compliant, onshore players.

He also sees a potential upside from regulation itself. Limiting yield passthrough could reduce the revenue Circle shares with partners like Coinbase, helping improve margins over time.

Altogether, Hougan sees a path for Circle to grow to a much larger valuation — potentially around $75 billion, roughly double its current level.

“If stablecoins play out the way people think,” Hougan wrote, “you can be fairly conservative on most assumptions and still find Circle looking attractive.”

Startale Group said on Wednesday that SBI Group had invested $50 million to complete the company’s Series A, as the Japanese blockchain company develops tokenized securities infrastructure, stablecoins and consumer-facing onchain products.

In a press release shared with Cointelegraph, Startale said it closed a $50 million investment from SBI to scale products, including its Strium blockchain for tokenized securities, its Japanese yen and US dollar stablecoins, and a consumer-facing application that onboards users to onchain services.

The deal would deepen institutional backing for Startale’s push into onchain financial infrastructure in Japan, where the company and SBI have already announced projects tied to tokenized securities, stablecoins and digital asset settlement.

“Through the deep collaboration with SBI, we will accelerate the adoption of tokenized stocks, centered on Japanese equities and JPY stablecoin, this year,” said Startale Group CEO Sota Watanabe.

New funding to scale existing projects

The funding round follows a $13 million first close led by Sony Innovation Fund in January, bringing the company’s total Series A to $63 million.

Startale said the newly-raised capital will be used to advance its vertically integrated strategy, building out a full stack that spans blockchain infrastructure, financial products and consumer-facing applications.

Related: Japan’s SBI VC Trade launches retail USDC lending as stablecoin use grows

The company plans to scale its Strium network for tokenized securities and real-world asset trading, expand adoption of its JPYSC and USDSC stablecoins, and develop its SuperApp to integrate payments, asset management and onchain services into a single platform.

On Feb. 5, Startale Group and SBI Holdings launched Strium, a layer-1 blockchain designed to support settlement infrastructure for institutional trading of foreign exchange, tokenized equities and RWAs.

Startale Group deepens ties with SBI

The new capital raise also follows a series of collaborations between SBI and Startale. On Aug. 22, 2025, SBI formed partnerships with Startale, Circle and Ripple to launch stablecoin ventures and a tokenized asset trading platform in Japan.

On Dec. 16, SBI and Startale signed a Memorandum of Understanding to develop a fully regulated JPY stablecoin, targeting tokenized assets markets and global settlement. Under the MoU, the project will be issued and redeemed by a wholly-owned subsidiary of SBI Shinsei Bank called Shinsei Trust & Banking.

Magazine: Telegram avoids Philippines ban, yen carry trade going onchain: Asia Express

The Sky-backed stablecoin incubator’s inaugural class of eight projects marks the protocol’s biggest push yet to diversify beyond crypto-native yield sources.

Obex, the stablecoin incubator administered by Framework Ventures and backed by a $2.5 billion mandate from the Sky ecosystem, on Tuesday announced its inaugural cohort of eight projects and began deploying up to $1 billion in USDS across them.

The first class includes Maple, USDAI, Daylight, Centrifuge, Securitize, River, TVL Capital, and Better. All eight are either already part of, or intend to join, the Sky ecosystem, spanning structured credit, fintech lending, energy finance, AI infrastructure, tokenization, crypto capital markets, and real estate.

“Our industry is at an inflection point. We’re moving beyond circular DeFi yield sources and toward high-quality yield from private credit markets, fintech, energy infrastructure, AI CapEx, real estate, and other productive sectors,” said Parker Edwards, partner at Framework Ventures, in a press release viewed by The Defiant.

The deployment marks the first major move by Obex, which raised $37 million in November 2025 in a round co-led by Framework, LayerZero, and the Sky ecosystem. The Sky community separately voted to provide up to $2.5 billion worth of USDS for deployment into approved, incubated projects that graduate from the program.

The move comes amid strong momentum for Sky, the protocol formerly known as MakerDAO. USDS currently has roughly $11.6 billion in circulation, making it the third-largest stablecoin by market cap, according to Coingecko. Sky’s total value locked (TVL) surged 38% in March to $7.52 billion, making it the fourth-largest DeFi protocol. The protocol’s fixed 3.75% savings rate on sUSDS has attracted capital as DeFi yields elsewhere have compressed.

“Honestly, it’s the classic story of how Sky, just like Maker used to, always does better in bear markets because it’s just focused on a solid product that can be trusted to be stable and deliver good returns,” Sky founder Rune Christensen told The Defiant earlier this month.

In addition to receiving capital, cohort members plan to launch Sky-aligned products designed to bootstrap USDS usage within their ecosystems.

Tokenization Tailwind

The deployment arrives amid rapid growth in the tokenized real-world asset (RWA) sector. The sector tripled in value to approximately $26 billion over the past year, according to RWAxyz.

RWAs became Wall Street’s gateway to crypto in 2025, with onchain tokenized assets tripling to nearly $19 billion over the course of the year. The momentum has only accelerated into 2026, with RedStone projecting the market could reach $50-60 billion by year-end.

Key Takeaways

- Morgan Stanley initiated Overweight coverage on Constellation Energy (CEG) with a $385 price target, suggesting approximately 30.6% potential upside from Tuesday’s $294.85 close.

- Shares jumped 4.2% to $307.04 on Wednesday, despite trading down 16.5% year-to-date and suffering a 10.6% decline since Iran conflict escalation.

- Analysts view the current valuation as an “attractive entry point,” estimating data center contracting opportunities alone contribute $70 per share in value.

- The company operates America’s largest nuclear generation fleet at approximately 22 gigawatts, with established power agreements serving Meta and Microsoft.

- Analysts anticipate Q1 earnings will climb 17% to $2.51 per share, while annual revenue projections show 17% growth to $29.88 billion.

Constellation Energy (CEG) shares finished Tuesday’s session at $294.85, then surged 4.2% to reach $307.04 during Wednesday trading.

Constellation Energy Corporation, CEG

Morgan Stanley launched coverage of Constellation Energy (CEG) on Wednesday with an Overweight recommendation and established a $385 price objective. This target suggests potential gains of roughly 30.6% above Tuesday’s closing level.

The bullish stance arrives during a challenging period for shareholders. Year-to-date performance shows CEG declining 16.5%, with a notable 10.6% selloff following the onset of Iran military tensions. Analyst David Arcaro and his team interpret this weakness as a buying opportunity.

“We estimate CEG is priced at a level that values the existing assets ($255/share on our math) with modest value for incremental growth and value upside opportunities,” the research note stated.

The $385 price objective from [[LINK_START_2]]Morgan Stanley[[LINK_END_2]] incorporates multiple value components: $70 per share attributed to data center contracts, $40 from anticipated power price appreciation, and $22 stemming from clean energy credit programs. These elements combine to create substantial upside for shares currently trading around $290.

Nuclear Portfolio Advantage

Constellation commands the nation’s most extensive nuclear generation portfolio, boasting approximately 22 gigawatts of installed capacity. Morgan Stanley emphasized several competitive advantages: continuous 24/7 carbon-free baseload generation, extended operational lifespans, readily available land with existing grid connections suitable for data center development, and opportunities for deploying small modular reactor technology on existing sites.

The AI-nuclear investment thesis surrounding CEG isn’t fresh territory. Shares soared 91% throughout 2024 and posted an additional 58% gain in 2025 before experiencing recent headwinds.

The company has already secured two significant long-duration power supply agreements. During 2024, Microsoft signed a 20-year arrangement to procure nuclear-generated electricity for its data center infrastructure. Following nine months later in June 2025, Meta finalized another 20-year commitment — securing more than 1,100 megawatts from Constellation’s Clinton Clean Energy Center located in Illinois.

Morgan Stanley analysts indicated they anticipate “further data center contracting opportunities this year.”

Upcoming Catalysts

Constellation plans to unveil its 2026 financial projections and strategic roadmap on March 31. Management withheld providing forward guidance during February’s Q4 earnings announcement, amplifying investor attention toward the forthcoming update.

Morgan Stanley identified the March 31 presentation as the “next catalyst for a potential contract announcement.”

Regarding earnings expectations, Wall Street consensus calls for first-quarter earnings per share to advance 17% to $2.51, accompanied by revenue growth of 30% reaching $8.84 billion. Full-year projections anticipate earnings of $11.69 per share alongside revenue of $29.88 billion — reflecting year-over-year expansion of 24.5% and 17%, respectively.

Broader analyst consensus compiled by InvestingPro indicates 38% potential appreciation, marginally exceeding Morgan Stanley’s 30.6% projection.

During the fourth quarter, Constellation delivered adjusted earnings of $2.30 per share, narrowly missing the $2.31 consensus estimate, while revenue of $6.07 billion substantially exceeded projections of $4.95 billion.

The company also recently finalized an agreement to divest approximately 4.4 gigawatts of natural gas generation facilities within the PJM territory to LS Power Equity Advisors for $5 billion — a mandatory sale stemming from its Calpine acquisition.

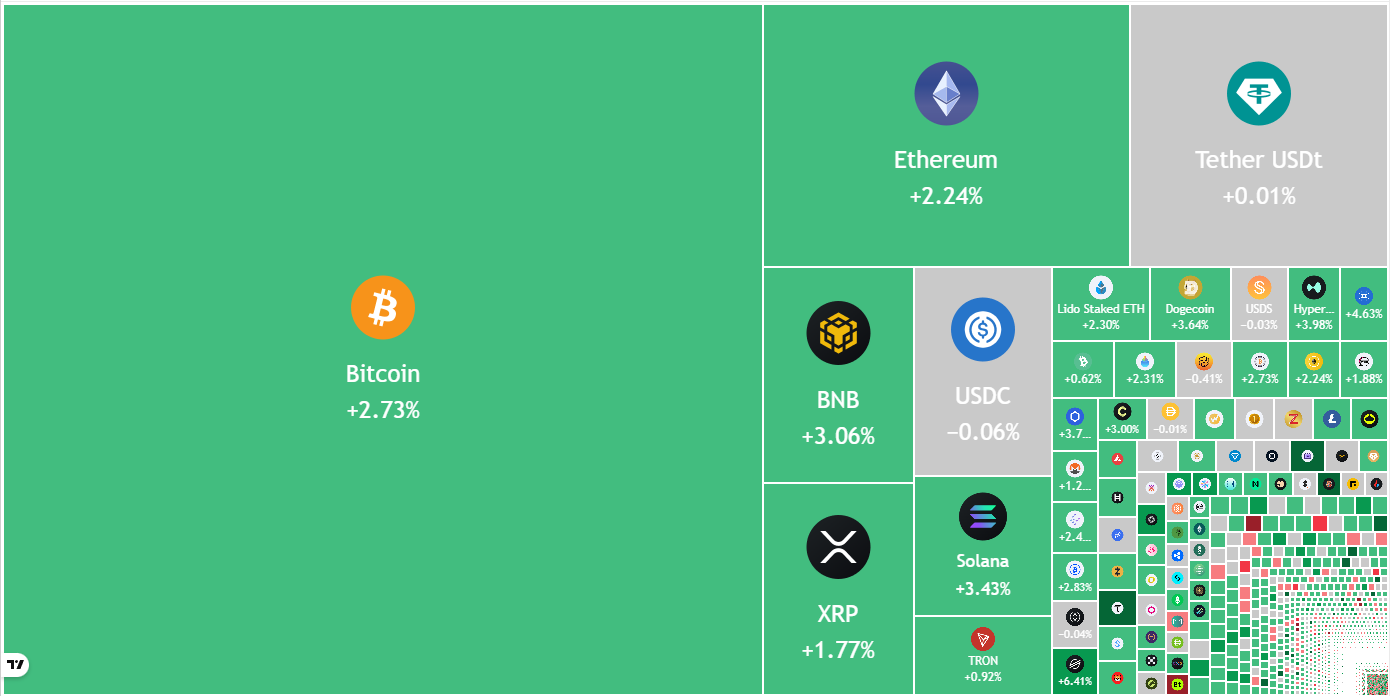

Bitcoin (BTC) continues to face significant resistance at the $72,000 level, but the bulls have kept up the pressure. Trader Daan Crypto Trades said in a post on X that BTC will have to cross and stay above the $72,000 resistance area to “test the $80Ks again.”

Markets tend to hate uncertainty, but BTC’s resilience since the start of the US and Israel-Iran war shows that traders are not keen to sell at lower levels. CryptoQuant analyst Darkfost said in a post on X that March has mostly recorded BTC outflows from crypto exchanges. Although the demand is not sufficient to start a new uptrend, it does signal accumulation by investors.

One of the reasons for accumulation could be that investors believe BTC is in value territory. Capriole Investments founder Charles Edwards said in a post on X that BTC is in deep value when the BTC Yardstick metric is considered. In February, the Yardstick numbers fell below the 2022 bear market low reading.

Could BTC and select major altcoins maintain above their overhead resistance levels? Let’s analyze the charts of the top 10 cryptocurrencies to find out.

Bitcoin price prediction

BTC continues to trade inside a bullish ascending triangle pattern, a sign that buyers are attempting a comeback.

The flattish 20-day exponential moving average ($70,303) and the relative strength index (RSI) near the midpoint do not give a clear advantage either to the bulls or the bears. Buyers will have to drive and maintain the BTC price above the $74,508 resistance to complete the ascending triangle. If they manage to do that, the BTC/USDT pair may rally to $84,000.

This positive view will be negated in the near term if the price turns down and breaks below the support line. That signals the bulls have given up. The pair may then plummet to the $62,500 to $60,000 support zone.

Ether price prediction

Ether (ETH) bounced off the 50-day simple moving average ($2,042) on Monday, indicating a positive sentiment.

The flattish 20-day EMA ($2,121) and the RSI near the midpoint suggest a balance between supply and demand. Buyers will have to push the price above the $2,400 level to indicate the start of a new up move. The ETH/USDT pair may rally to $2,600 and later to $3,050.

Instead, if the ETH price turns down and breaks below the 50-day SMA, it signals that the market has rejected the break above the $2,111 level. That may pull the pair to $1,900 and subsequently to the $1,750 level.

BNB price prediction

Buyers are attempting to maintain BNB (BNB) above the 20-day EMA ($643), but the bears are posing a strong challenge.

The flattish 20-day EMA and the RSI just below the midpoint suggest that the BNB/USDT pair may remain inside the $570 to $687 range for a few more days. The longer the price remains inside a range, the stronger the eventual breakout from it.

If buyers drive the BNB price above $687, the pair may surge to $730 and later to $790. Contrarily, if the price turns down and breaks below $600, it suggests that the bears have a slight edge. The pair may then slump to $570.

XRP price prediction

Sellers are attempting to maintain XRP (XRP) below the moving averages, but the bulls continue to exert pressure.

If the XRP price breaks and sustains above the moving averages, the rally may reach the breakdown level of $1.61 and then to the downtrend line. Sellers are expected to fiercely defend the downtrend line, as a close above it signals a potential trend change.

On the other hand, if the price turns down and breaks below $1.27, it suggests that the bears remain in control. The XRP/USDT pair may then slump to the support line of the channel, where buyers are expected to step in.

Solana price prediction

Solana (SOL) has been trading between the 50-day SMA ($86) and the overhead resistance of $95 for the past few days.

The gradually upsloping 20-day EMA ($89) and the RSI just above the midpoint suggest a slight edge to the buyers. If bulls clear the overhead barrier at $95, the SOL/USDT pair may soar to $117.

On the downside, sellers will have to pull the SOL price below the 50-day SMA to get back into the game. If they do that, the pair may slump toward the bottom of the $76 to $95 range. A solid bounce off the $76 level may extend the stay inside the range for some more time.

Dogecoin price prediction

Dogecoin (DOGE) bounced off the $0.09 support on Monday, but the bulls are struggling to push the price above the moving averages.

If the DOGE price turns down sharply from the moving averages, the possibility of a break below the $0.09 level increases. The DOGE/USDT pair may then tumble to the next support at $0.06.

Alternatively, a close above the moving averages shows solid buying at the $0.09 level. The pair may then rise to $0.10 and later to $0.12, which is expected to pose a substantial challenge for the bulls.

Hyperliquid price prediction

Hyperliquid (HYPE) rebounded off the breakout level of $36.77 on Tuesday, indicating that the bulls are attempting to flip the level into support.

The upsloping moving averages and the RSI in the positive territory indicate that the bulls have the upper hand. If buyers drive the HYPE price above the $43.77 level, the next stop is likely to be $50.

This positive view will be invalidated in the near term if the price turns down and breaks below the $36.77 level. That suggests the market has rejected the breakout. The HYPE/USDT pair may then tumble to the 50-day SMA ($33.16).

Related: Here’s what happened in crypto today

Cardano price prediction

Cardano (ADA) remains stuck inside the descending channel pattern, but the bulls are attempting to form a base near $0.25.

A close above the moving averages opens the doors for a rally to the downtrend line. Sellers are expected to aggressively defend the downtrend line as a close above it signals a potential trend change. The ADA/USDT pair may ascend to $0.39 and thereafter to $0.44.

Conversely, if the ADA price turns down sharply from the downtrend line and breaks below the moving averages, it shows that the bears remain sellers on rallies. That increases the likelihood of a decline below the $0.25 level. The pair may then plunge toward the support line.

Bitcoin Cash price prediction

Bitcoin Cash (BCH) closed above the 20-day EMA ($470) on Monday, but the bulls are struggling to push the price to the 50-day SMA ($492).

That shows the bears are active at higher levels. The sellers will attempt to strengthen their position by pulling the BCH price below the 20-day EMA. If they can pull it off, the BCH/USDT pair may drop to the $443 level. This is a critical level for the bulls to defend, as a close below $443 will complete a bearish head-and-shoulders pattern. The next support on the downside is at $375.

On the upside, if buyers thrust the price above the 50-day SMA, it suggests the start of a stronger relief rally to $520.

Chainlink price prediction

Chainlink (LINK) has been gradually rising inside an ascending channel pattern, indicating a series of higher lows in the short term.

The bulls will attempt to push the LINK price to the resistance line of the channel, where the bears are expected to mount a strong defense. If the price turns down sharply from the resistance line, the LINK/USDT pair may remain inside the channel for a few more days.

However, if buyers propel the price above the resistance line, it signals the start of a stronger recovery. The $11.61 level may act as an obstacle, but if the bulls overcome it, the rally may reach the $14.98 level.

This article does not contain investment advice or recommendations. Every investment and trading move involves risk, and readers should conduct their own research when making a decision. While we strive to provide accurate and timely information, Cointelegraph does not guarantee the accuracy, completeness, or reliability of any information in this article. This article may contain forward-looking statements that are subject to risks and uncertainties. Cointelegraph will not be liable for any loss or damage arising from your reliance on this information.

US President Donald Trump announced 13 appointees from the crypto, blockchain, AI, and technology sectors to his re-established Council of Advisors on Science and Technology (PCAST), a body revived by executive order in January 2025. The White House said the council would advise the president on matters involving science, technology, education, and innovation policy.

The administration signaled that the panel could ultimately expand to as many as 24 members, with many additional appointments expected in the near term.

Among those named were Meta CEO Mark Zuckerberg, Coinbase co-founder Fred Ehrsam, Nvidia CEO Jensen Huang, and Oracle chief technology officer Larry Ellison, illustrating a cross-section of social media, crypto, semiconductors, and enterprise software leadership on the panel.

The White House noted that the council will be co-chaired by White House AI and crypto czar David Sacks and Trump’s science adviser Michael Kratsios. The January executive order re-establishing PCAST assigns it the task of advising the President on science, technology, education, and innovation policy.

News of the appointments comes as the White House last week released a national AI framework, urging Congress to pass legislation that would preempt state-level rules in favor of a unified federal approach. In parallel, Trump has pressed Republicans to advance the SAVE America Act—legislation requiring proof of citizenship to register to vote, saying on March 8 that he “will not sign other bills” until it passes.

Key takeaways

- The reconstituted PCAST adds 13 members from crypto, AI, and broader tech sectors with potential to influence policy on innovation, regulation, and national strategy.

- High-profile names attached to the roster include Mark Zuckerberg, Fred Ehrsam, Jensen Huang, and Larry Ellison, underscoring a cross-industry reach into social platforms, crypto infrastructure, and enterprise tech.

- The council’s leadership is set to be co-chaired by David Sacks and Michael Kratsios, tying together White House AI strategy and science-oriented policy oversight.

- The appointment aligns with a broader White House push on AI governance and technology policy, coming shortly after the administration’s AI framework and amid ongoing crypto-market regulation debates in Congress.

A tech-forward advisory body and its potential influence

The expansion of PCAST signals more than a ceremonial lineup. By bringing together founders and executives with hands-on experience in platform design, digital assets, and advanced computing, the White House appears intent on shaping policy that could affect research funding, national quantum and AI initiatives, data privacy standards, and the coordination of federal tech programs across agencies.

David Sacks’ designation as a co-chair reflects the administration’s approach to integrate perspectives from both AI development and crypto policy circles. Michael Kratsios, who serves as Trump’s science adviser, complements that mix with a governance mindset focused on policy execution and regulatory clarity. In this arrangement, the council could become a sounding board for national strategies on emerging technologies, including how the U.S. competes with international peers in AI, cloud infrastructure, and digital assets infrastructure.

The membership itself reads like a snapshot of today’s technology leadership: a social media chief executive, a crypto infrastructure founder, a semiconductor and AI hardware chief, and an enterprise software veteran. While PCAST has historically concentrated on scientific and technical policy, the current lineup raises the potential for a more explicit bridge between innovation ecosystems and federal policy objectives.

Context: AI policy, frameworks, and the political timetable

Its emergence comes on the heels of the White House’s national AI framework, which calls for a cohesive federal approach to artificial intelligence governance. By emphasizing federal action, the administration is signaling that it intends to steer the discussion beyond uneven state-by-state regulation, a point of interest for developers, users, and investors navigating AI deployment timelines and risk management.

Meanwhile, the political calendar around crypto regulation remains contentious. The House previously passed a comprehensive digital asset market structure bill, known in policy circles as the CLARITY Act, in July 2025. The Senate, however, has faced recurring obstacles, including recesses and a government funding standoff, and progress has stalled on moving the measure through the upper chamber. The outlook for federal crypto law is further complicated by industry pushback on certain provisions and the balance lawmakers seek between consumer protection, market integrity, and innovation incentives.

The Senate Agriculture Committee did advance its version of the market structure bill in January, but a planned markup in the Senate Banking Committee—where securities-law implications are central—was postponed after Coinbase CEO Brian Armstrong indicated the bill did not align with the company’s views as written. As of midweek, no new date had been set for a Banking Committee markup, leaving the overall timeline uncertain. Industry concerns over how the framework would handle stablecoins and yields have contributed to the cautious pace surrounding legislative action.

Taken together, the PCAST appointments and the ongoing congressional debates map a broader moment for policy signals. Investors, developers, and users are watching how the White House’s staffing choices translate into concrete regulatory directions—particularly around AI governance, digital asset policy, and the interoperability of federal rules across federal agencies.

What to watch next in policy and markets

Looking ahead, several questions will shape the near-term crypto and tech policy landscape. First, how quickly will the White House fill out the remaining PCAST seats, and what subfields or sectors will be prioritized in those appointments? Second, will the AI framework influence legislative strategy in Congress, accelerating a more unified approach to technology regulation that could affect innovation pipelines and government procurement?

On the legislative front, the CLARITY Act saga offers a bellwether for how the Administration and Congress balance market structure clarity with industry concerns. If the Senate resumes movement and addresses securities considerations and stablecoin policy in a compatible form, it could set the stage for a federal framework that supersedes piecemeal state rules. Conversely, extended stalemate would maintain a degree of regulatory ambiguity that could impact capital flows and project timelines across the crypto and crypto-adjacent tech sectors.

For market participants and builders, the development underscores a potential shift in how federal policy-makers engage with crypto-native ecosystems. The inclusion of influential industry leaders on PCAST may foreshadow more active, policy-informed collaboration between government and industry—an environment where technical feasibility, consumer protection, and innovation incentives must be balanced in real time.

As the administration moves to fill out PCAST and Congress weighs next steps on market structure legislation, observers should monitor the administration’s public messaging, any future staffing announcements, and committee-level activity in the Senate. The coming weeks could reveal the degree to which this White House strategy translates into tangible policy shifts, regulatory clarity, and a clearer path for crypto and AI developers navigating the U.S. regulatory landscape.

Readers should stay tuned for updates on who joins PCAST in the coming months and how the council’s guidance might influence federal research funding, education policy, and enforcement priorities across science and technology domains.

TLDR

- The European Central Bank plans to publish Digital Euro technical standards by summer.

- The ECB will begin a 12-month pilot for the Digital Euro in the second half of 2027.

- Lawmakers could approve a full Digital Euro launch around 2029.

- Private banks will provide wallets while the ECB maintains the core infrastructure.

- The Reserve Bank of Australia estimates tokenization could deliver AUD $24 billion in annual efficiency gains.

The European Central Bank has outlined a clear path for its Digital Euro project and expects to publish technical standards by summer. Executive Board member Piero Cipollone confirmed the plan before European Union lawmakers and detailed the rollout process. Meanwhile, Australia’s central bank has projected AUD $24 billion in annual efficiency gains from tokenization efforts.

Digital Euro Framework and Pilot Roadmap

The ECB will release core technical standards for the Digital Euro by this summer. Cipollone said the framework will give banks and payment firms time to prepare their systems. He stressed that early coordination will support a smooth integration process.

The standards will allow terminals, wallets, and payment apps to include Digital Euro functionality before issuance. As a result, providers can embed features directly into payment infrastructure. Cipollone told lawmakers that “early alignment with industry participants is critical to ensuring a smooth rollout.”

The ECB has scheduled a 12-month pilot for the second half of 2027. The trial will test person-to-person transfers and point-of-sale payments in controlled settings. Licensed payment service providers will operate the pilot under central bank oversight.

The central bank will review both technical performance and user adoption during the pilot. If lawmakers approve the framework, the ECB targets a potential launch around 2029. Officials linked the timeline to infrastructure development and legislative coordination across the European Union.

The ECB has confirmed that it will not offer the Digital Euro directly to consumers. Instead, private banks and payment firms will provide wallets and customer services. The Digital Euro will function as a public infrastructure layer within the existing financial system.

Australia Advances Tokenization Strategy

The Reserve Bank of Australia has estimated that tokenization could deliver about AUD $24 billion in annual efficiency gains. Bloomberg reported that the figure equals roughly $16.7 billion in economic value. The projection highlights the growing focus on blockchain-based financial infrastructure.

Assistant Governor Brad Jones said stablecoins and bank-issued deposit tokens will play complementary roles. He stated that authorities are shifting toward practical deployment frameworks. The RBA has launched a digital sandbox to test new tokenized financial products.

The central bank has also expanded a working group focused on deposit tokens. Officials aim to integrate tokenized finance into the existing monetary system while maintaining oversight. The RBA said the initiative supports coordination between regulators and industry participants.

In Europe, the ECB continues to position central bank money as the anchor of the financial system. Cipollone said public money must retain its role as a tokenized asset, and stablecoins gain traction. The ECB’s Pontes initiative is testing cross-platform settlement of tokenized securities using central bank money.

The Appia roadmap outlines a longer-term plan for integrated tokenized markets across Europe. The Digital Euro will complement cash and bank deposits within that framework. Authorities confirmed that central bank-backed settlement remains central to these efforts.

The US has accused two China-based pharmaceutical firms of using crypto to sell fentanyl precursor chemicals to violent Mexican cartels distributing drugs across the US.

Six defendants and two pharmaceutical firms, Shandong Believe Chemical Company and Shandong Ranhang Biotechnology Ltd, were indicted by an Ohio district court grand jury yesterday and charged with money laundering, international criminal financing, and terrorist financing.

The firms allegedly presented themselves as legitimate pharmaceutical companies while marketing and selling various chemical products that are required in the production of fentanyl.

It’s alleged that drug traffickers accepted crypto as payment, and would send the funds to crypto wallets under the control of the accused entities and persons.

Crypto under the control of the two firms would then be sent to agents, who would hold onto the funds until they could be converted into fiat currency and laundered through international banks.

As part of the indictment, a sum of crypto from a Binance account with $26,000 worth of funds will be forfeited if the US manages to secure a conviction.

Read more: World Cup games in Mexico at risk after crypto-laundering drug lord killed

The alleged buyer of these specific precursors is the Gulf Cartel (Cartel del Golfo). It’s one of Mexico’s oldest criminal organizations, dating back to the 1930s, and was designated a terrorist organization last year.

The US claims the cartel deals in drug trafficking, kidnapping, extortion, human smuggling, and “employs violence, including assassinations of civilians and government officials, to intimidate the public and control territory.”

US and China collaborated to achieve the fentanyl indictment

FBI director Kash Patel said yesterday’s indictment was the result of a “historic” collaborative investigation between the US and China’s Ministry of Public Security.

He implied the indictments were helped by the FBI and Donald Trump visiting China last November, as Patel claimed the president’s negotiations with President Xi, “continues to pay dividends for America’s national security in the war on deadly narcotics.”

Read more: Crypto payments to China chemical suppliers fuel US fentanyl epidemic

Crypto analysis firm Elliptic has previously found that centralised crypto exchanges in Russia and Australia have been used to facilitate millions of dollars worth of funds that stem from China-based sellers of fentanyl precursors.

It was able to trace $32 million worth of crypto, made up of bitcoin, Tron-based USDT, and Ethereum-based USDT, transferred as part of fentanyl precursor sales.

Another alleged crypto money laundering operation, indicted by the US in 2024, allegedly worked with “Chinese underground money exchanges” and the Sinaloa Cartel to facilitate illicit funds connected to the drugs trade.

Fentanyl is a key contributor to opioid deaths in the US, and exports of the drug from China directly to the US were curtailed in 2019. However, by selling precursor chemicals instead, many companies can skirt regulations.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

TLDR:

- The memecoin market cap holds above $45B even as the Fear & Greed Index drops to a low of 10.

- Only 0.00009% of PumpFun tokens captured over 55% of FDMC, exposing extreme memecoin market concentration.

- OG memecoins like DOGE, PEPE, and BONK show stronger retention through utility, trust, and trading volume.

- Over 90% of memecoins launched in late 2025 and early 2026 have already lost liquidity and user interest.

Memecoins continue to struggle with user retention even as the total market cap holds above $45 billion. The Fear & Greed Index has fallen to 10, yet the sector remains structurally active.

Thousands of new tokens launch weekly, but the overwhelming majority collapse within weeks. The gap between surviving and failing projects keeps widening, pointing to deep retention problems across the memecoin space.

Weak Fundamentals Drive Rapid User Exits From New Tokens

Most new memecoins share a common failure pattern rooted in poor design. They launch with heavy hype, attract early buyers, then collapse once whale selling begins. That cycle has repeated consistently throughout late 2025 and into 2026.

Data from PumpFun shows only around 12 tokens, roughly 0.00009% of all launches, captured over 55% of fully diluted market cap.

The remaining thousands lost liquidity extremely fast. Users had little reason to stay once early momentum faded.

Crypto analyst Tanaka pointed this out directly on X, noting that whale concentration and full dependence on hype culture leave most tokens without a retention foundation. When there is no utility, no community incentive, and no roadmap, users simply move on to the next launch.

The numbers back this up clearly. Over 90% of memecoins launched in late 2025 and early 2026 have already died.

Tokens that once reached $1 to $2 billion in market cap are now sitting at tens of millions or have vanished entirely. That collapse rate reflects a market where retention was never prioritized.

Utility and Track Record Separate Survivors From Short-Term Projects

Established memecoins retain users far better because they offer more than speculation. FLOKI expanded into the Valhalla play-to-earn metaverse and operates across both BSC and Ethereum. That cross-chain utility gives holders a reason to stay engaged beyond price movement.

PEPE demonstrated strong user confidence by reclaiming a $1.7 billion market cap. It led a market recovery with a 20.5% daily gain on March 16, backed by a 287% volume surge to $790 million. That kind of organic volume reflects genuine user participation, not just short-term speculation.

BONK similarly retained its Solana user base, gaining 10% with a 228% trading volume spike to $131 million. Gemini’s decision to launch BONK perpetual contracts with 100x leverage further reinforced its credibility among active traders seeking longer-term exposure.

DOGE remains the clearest example of sustained retention, holding its position as the leading memecoin even in a weak market. Its potential integration with X Money adds a forward-looking narrative that newer tokens simply cannot compete with.

As Tanaka noted, OG memecoins continue to prove that brand trust, community depth, and utility pathways are what ultimately keep users from walking away.

Artificial intelligence agents will be deployed starting Wednesday by law enforcement agencies using analytical tools provided by TRM Labs, which added the new agents that are meant to allow investigators to use regular language to frame their searches.

The new investigative assistant is embedded in the TRM Forensics service that’s extended to law enforcement agencies, crypto businesses and financial firms, and it “translates natural language prompts into complex investigative actions,” TRM said in a press release. A user can request information about the flow of funds without needing highly technical inputs, speeding up the time-dependent process of chasing bad actors.

Last year, illicit crypto volume hit $158 billion, according to the analysis firm.

“What we’re seeing every day is that the caseload is growing faster than the workforce, and investigators are being asked to operate across dozens of blockchains, jurisdictions, and typologies simultaneously,” said Ari Redbord, head of legal and government affairs for TRM.

An AI tool on investigators’ side, he said, could help overcome “a sharp acceleration in AI-enabled fraud and scams,” which TRM data puts at a 500% increase “as criminal actors use automation, deepfakes and AI-driven tools to scale operations with speed and precision that simply didn’t exist before.”

CLARITY’s stablecoin yield ban shifts bargaining power from Coinbase to Circle

“Daredevil: Born Again” season 3 will feel like 'a new dawn' after Mayor Fisk arc, Charlie Cox says

London Marathon in advanced talks to make race a two-day event next year

-

Crypto World5 days ago

Crypto World5 days agoNIO (NIO) Stock Plunges 6.5% as Shelf Registration Sparks Dilution Worries

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Adidas – Corporette.com

-

Politics5 days ago

Politics5 days agoJenni Murray, Long-Serving Woman’s Hour Presenter, Dies Aged 75

-

NewsBeat10 hours ago

NewsBeat10 hours agoManchester United reach agreement with Casemiro over contract clause amid transfer speculation

-

Crypto World4 days ago

Crypto World4 days agoBest Crypto to Buy Now: Strategy Just Spent $1.57 Billion on Bitcoin During Fear While Early Investors Quietly Enter Pepeto for 150x Potential

-

Crypto World4 days ago

Crypto World4 days agoBitcoin Price News: Bhutan Sells $72 Million in BTC Under Fiscal Pressure, but the Smart Money Entering Pepeto Sees What the Market Does Not

-

Tech6 days ago

Tech6 days agoinKONBINI Lets You Spend Summer Days Behind the Register

-

Sports2 days ago

Sports2 days agoRemo Stars and Kano Pillars Strengthen Survival Hopes in NPFL

-

NewsBeat7 days ago

NewsBeat7 days agoResidents in North Lanarkshire reminded to register to vote in Scottish Parliament Election

-

Politics6 days ago

Politics6 days agoGender equality discussions at UN face pushbacks and US resistance

-

Business3 days ago

Business3 days agoNo Winner in March 21 Drawing as Prize Rolls to $133 Million for Next

-

Business7 days ago

Business7 days agoWho Was Alex Pretti? 5 Key Facts About the ICU Nurse Killed by Federal Agents in Minneapolis

-

Sports2 days ago

Sports2 days agoGary Kirsten Accuses Pakistan Cricket Board Of ‘Interference’, Mohsin Naqvi Responds

-

Tech3 days ago

Tech3 days agoGive Your Phone a Huge (and Free) Upgrade by Switching to Another Keyboard

-

Tech7 days ago

Tech7 days agoInventec’s bizarre VeilBook laptop hides its touchpad under a sliding keyboard just to give cooling fans a little breathing room

-

Sports5 days ago

Sports5 days ago2026 Kentucky Derby horses, odds, futures, preview, date: Expert who nailed 12 Derby-Oaks Doubles enters picks

-

Sports6 days ago

Vikings Free Agency Enters Phase 2 with Key Questions

-

Tech3 days ago

Tech3 days agoAI enters the chat: New Seattle dating app relies on tech to facilitate meaningful human connections

-

News Videos7 days ago

News Videos7 days agoAmazing Cardboard Gadget That Turns Paper Into Money #techgadgets #ytshorts

-

Tech7 days ago

Tech7 days agoCorsair K100 Air Wireless Mechanical RGB Keyboard Packs Full Power Into a Slim Frame

You must be logged in to post a comment Login