Crypto World

Binance formally denies Iran sanctions violation allegations

Binance has rejected allegations that its platform allowed transactions linked to entities in Iran.

Summary

- Binance issued a formal response to a U.S. Senate inquiry denying claims that it allowed transactions linked to Iran.

- The exchange said media reports cited in the inquiry contain false and unsupported allegations about its compliance program.

- Binance pointed to investigations that led to the removal of certain entities and its expanded compliance measures.

The exchange issued a response on March 6 to a letter sent by Richard Blumenthal regarding sanctions compliance and anti-money laundering controls. The inquiry referenced several recent media reports. Binance said those reports contain false and unsupported claims about its compliance program.

Binance said it runs a large compliance operation to prevent sanctioned users from accessing the platform. Identity verification is required for every user, and individuals located in Iran are not allowed to use the exchange.

Compliance program and monitoring systems

According to the company, millions of dollars have been invested in compliance infrastructure in recent years. The compliance team now includes more than 1,500 professionals around the world. Many focus on sanctions monitoring, financial crime investigations, and counter-terrorism financing checks.

More than 25 monitoring tools are used to screen users and review transactions. Customer onboarding checks, sanctions screening, and behavioral analysis are also applied to detect suspicious activity. When concerns appear, cases are reviewed and information can be shared with law enforcement.

The company also pointed to its cooperation with investigators. In 2025 alone, Binance handled more than 71,000 law-enforcement requests. Over the past three years, authorities seized more than $752 million with assistance from the exchange.

Blockchain analytics data cited by Binance shows a decline in exposure to wallets linked to illicit activity. Between January 2024 and July 2025, the share of exchange volume connected to such wallets dropped from 0.284% to 0.009%.

Investigations involving flagged entities

The inquiry also mentioned two trading entities, Hexa Whale and Blessed Trust, which were reported to have indirect exposure to wallet addresses with possible links to Iran.

Binance said it became aware of those concerns after receiving requests from law enforcement in 2025. Investigations were then carried out by the exchange’s internal team. Transaction records were reviewed and user information was provided to authorities.

After the reviews were completed, both entities were removed from the platform. Hexa Whale was offboarded in August 2025, while Blessed Trust was removed in January 2026. Binance said it is not aware of any account on the exchange that directly transacted with an Iran-based entity.

The company also rejected claims that it had identified thousands of Iranian-linked accounts. Binance said it never made such a determination and noted that any attempt to bypass location restrictions using a VPN violates its terms of service.

Binance said it investigates credible risks, removes accounts when necessary, and works with authorities to address potential misuse of its platform.

When one of the world’s largest card networks pays a significant premium over a company’s last valuation to acquire it, that is worth paying attention to. When the company in question builds stablecoin settlement infrastructure, it tells you something fundamental about where the payments industry believes it needs to be – and how urgently it needs to get there.

Mastercard had options. It could have partnered with BVNK. It could have taken a minority stake. It could have acquired a smaller stablecoin infrastructure player for a fraction of the price. Instead, it paid $1.8 billion – more than double BVNK’s $750 million Series B valuation from just over a year ago – for a company that has spent years doing the unglamorous work of building enterprise–grade stablecoin rails across 130 jurisdictions.

That number tells you more about where Mastercard sees payments heading than any strategy deck or earnings call ever could. And it eclipses Stripe’s $1.1 billion acquisition of Bridge, making it the largest stablecoin infrastructure deal in history.

More than $190 trillion moves cross–border annually through correspondent banking rails designed half a century ago. Those rails still function – in the same way a fax machine still functions. They carry the money, eventually, but they do so through layers of intermediaries that add cost, delay and opacity at every step. Mastercard has clearly concluded that patching this system is no longer a viable strategy. The question worth asking is why they reached that conclusion now, and what it means for the rest of the industry.

Compliance was worth the premium

Mastercard has no shortage of engineering talent. It could build a stablecoin settlement layer from scratch – and it would probably be a good one. So why pay a 140% premium for someone else’s?

Because the technology was never the hard part. BVNK’s value lies in its multi-jurisdictional licensing framework – painstakingly assembled over years of regulatory engagement across more than 130 countries. Walking into that many regulators’ offices and emerging with approval takes the kind of time that a card network competing for the future of settlement simply does not have. In payments, the compliance framework is the product. Everything else can be rebuilt.

This is what separates the companies that legacy finance acquires from the ones it ignores. The firms that treated licensing as a core investment – not an afterthought – are now the ones commanding billion-dollar valuations. Mastercard did not pay for BVNK’s code. It paid for the years it would have lost trying to replicate BVNK’s regulatory footprint. That distinction matters because it tells you exactly what the next acquirer in this space will be looking for, too.

The emerging market dividend

Most coverage of this acquisition will focus on what it means for Western payments modernisation. But the more consequential implications are in the corridors where BVNK’s infrastructure will matter most – and where Mastercard’s distribution can do the most good.

Remittance fees still average six to eight per cent in corridors serving Africa and Southeast Asia. A worker in Dubai sending $500 home to the Philippines loses $30 to $40 per transfer to intermediaries. Across the $685 billion in remittances flowing to low- and middle-income countries each year, that represents an extraordinary transfer of value away from the people who can least afford it.

This is precisely where stablecoin–native settlement changes the equation. The underlying rails do not require the chain of correspondent banks that traditional cross-border payments demand. Strip out those intermediaries and flat fees of one to two per cent become structurally possible – not as a promotional offer, but as a reflection of what settlement actually costs when the plumbing is modern.

Mastercard now owns that plumbing. Combined with its merchant network and distribution across emerging markets, this acquisition has the potential to reshape financial access for the 1.3 billion adults still outside the formal banking system. When a network of Mastercard’s scale plugs stablecoin settlement into corridors where people have been paying eight per cent to move their own money, the impact is not incremental. That is a far bigger story than a card network hedging its bets on crypto.

The regulated rails race

Stripe acquired Bridge. Mastercard has acquired BVNK. By all accounts, Visa is evaluating its own move. Within eighteen months, every major card network will have a stablecoin settlement strategy – or will be explaining to shareholders why it does not.

The interesting tension here is not between traditional finance and crypto. That framing is already outdated. The real contest is between regulated stablecoin infrastructure and the unregulated alternatives growing in corridors where compliant options remain inaccessible. Unregulated rails can move faster precisely because they bypass the licensing work that enables institutional adoption. But speed without regulatory legitimacy is fragile – and the sector has enough scar tissue from high-profile collapses to know where that leads.

Every month that regulated infrastructure remains unavailable in a given corridor is a month that shadow systems gain ground. Mastercard’s acquisition significantly compresses that timeline. With BVNK’s licensing across 130 countries and Mastercard’s global reach, the gap between regulated capability and market demand has just narrowed, benefiting everyone operating on the right side of compliance.

The premium Mastercard paid was never about the technology. It was about time – the time it would take to build a regulatory footprint from scratch while the market moves on without you. That calculus now applies to every legacy payments company that has been watching from the sidelines. The window for building is closing. The window for buying is getting more expensive by the quarter.

When the next acquisition in this space lands – and it will – nobody will treat it as a surprise. They will treat it as inevitable. That shift in expectation is the clearest sign that stablecoin infrastructure has moved from the periphery of global payments to its centre.

Quick Overview

- Citigroup experiences 3.9% decline to $108 during trading session

- Bank evaluates regional institutions with $500B in assets for acquisition

- Recent asset sales generate $6.5B in capital for strategic initiatives

- Share price trails targets despite 78% surge in corporate banking revenue

- Digital asset infrastructure development continues with Bitcoin custody services

Shares of Citigroup retreated to $108.01, marking a 3.91% decline as market participants reacted to the financial institution’s strategic expansion initiatives. The stock experienced consistent downward momentum throughout the session, signaling investor uncertainty regarding the bank’s growth trajectory. Nevertheless, this pullback occurred against a backdrop of solid capital reserves and comprehensive organizational transformation.

Regional Banking M&A Strategy Takes Center Stage

Citigroup is actively assessing opportunities to acquire a US-based regional banking institution or wealth management firm to enhance its domestic footprint. This strategic initiative targets improved deposit gathering, expanded physical presence, and enhanced credit distribution capabilities. As a result, management seeks to narrow the competitive gap with dominant American banking rivals.

Discussions have centered on organizations managing approximately $500 billion in total assets, alongside established securities firms. Prospective candidates include wealth management platforms such as Stifel and Raymond James, both known for robust client advisory operations. Nevertheless, regulatory clearance remains a prerequisite given current supervisory restrictions.

Chief Executive Jane Fraser maintains her commitment to operational streamlining paired with targeted business expansion. The acquisition framework represents a pivot toward reinforcing American operations following extensive international portfolio optimization. Therefore, this approach complements broader objectives to amplify market presence and earnings potential.

Divestiture Program Bolsters Financial Flexibility

Citigroup has fortified its capital foundation through strategic dispositions and organizational restructuring measures. During February 2026, the institution finalized the transfer of its Russian operations to Renaissance Capital. This divestiture yielded approximately $4 billion in Common Equity Tier 1 capital enhancement.

Additionally, Citigroup divested a 49% ownership position in Banamex, its Mexican retail banking division. This transaction contributed roughly $2.5 billion while strengthening financial resources available for reinvestment. Furthermore, leadership has confirmed no additional Banamex asset sales are anticipated during the current fiscal year.

These strategic dispositions have unlocked substantial resources to finance acquisition activity and domestic market penetration. Consequently, Citigroup maintains significant capacity to allocate funds toward revenue-generating opportunities. This approach demonstrates a deliberate transition toward balance sheet optimization and prudent capital deployment.

Operational Performance and Blockchain Technology Advancement

Citigroup delivered impressive institutional banking results in its latest financial disclosure. Corporate banking revenues surged 78% on an annual basis, reaching $2.2 billion during the final quarter of 2025. This exceptional performance underscores heightened engagement from commercial and institutional client segments.

The stock continues trading substantially beneath the Wall Street consensus target of $135. The existing valuation disparity suggests a disconnect between current market pricing and analyst projections. Implementation success of strategic priorities may prove decisive for future share appreciation.

Citigroup has established foundational systems for cryptocurrency custody solutions and digital wallet capabilities. The organization intends to incorporate digital assets into conventional banking infrastructure while maintaining comprehensive risk management protocols. Beyond this, the bank is evaluating stablecoin applications and blockchain-enabled deposit instruments to enhance international payment settlement efficiency.

Approach by Fed Raises Concerns

The Federal Reserve Bank of Kansas City granted Payward Financial a limited purpose account that is operating under the name Kraken Financial. But authorities have said not much regarding the scope of services to which the account is related, and this has raised questions amongst legislators regarding openness and uniformity in the process of approving the account. Waters has formally requested Kansas City Fed President Jeff Schmid to clarify what legal framework is applied to handle the approval of the account. Further, she reported that existing laws and Federal Reserve access account regulations fail to specify or mention a limited purpose account, casting doubt on the interpretation of regulations.

The legislator has also questioned whether Kraken will be able to get important Federal Reserve products like payments processing, cash management, and securities transferring. Also, she needs to seek clarification regarding potential boundaries associated with the account, like limits on the balance or restrictions on overdrafts, which may limit its operation scope. The debate has been escalated given the comparisons with Custodia Bank that was seeking the same access over several years, yet it turned out in court. The resultant disparity has therefore given rise to an issue of fairness and equal treatment of the Federal Reserve System to various kinds of financial institutions.

The ruling has attracted interest in financial and crypto industries since companies are looking at the way the regulators address access to the central infrastructure. Other than the industry players, consider the development as a milestone to closer integration of crypto companies into the conventional ones that provide financial and payment systems in the US. Waters highlighted that the steady enforcement of regulations is critical towards ensuring that there is trust in the regulation processes. Therefore, she compelled the Federal Reserve to give more disclosures that justify why Kraken was able to clear such requirements using the same circumstances that other candidates were unable to do.

The problem appears in the context of broader uncertainty in the monetary policy and regulation of the direction of the financial system of the United States. In addition, the continuous controversy about interest rates and regulatory models also determines the way the interactions between the institutions and the central bank services and regulatory standards are involved.

Iran escalation and $171 million in ETF outflows drive BTC below $66,000.

Bitcoin fell to its lowest level in more than two weeks on Friday, dropping below $66,000 as a $14 billion options expiry collided with escalating Middle East tensions and a broader risk-off rout across global markets.

BTC was trading near $65,900 at press time, down roughly 4.5% over the past 24 hours, according to CoinGecko. Ether slipped to $1,983, also off 4%, while Solana tumbled 5.5% to $83. The total crypto market cap fell 3.4% to $2.36 trillion.

The Crypto Fear & Greed Index sits at 13, deep in “Extreme Fear” territory

Nearly $443 million in long positions were liquidated over the past 24 hours, compared with just $58 million in shorts, according to Coinglass, suggesting traders had been positioned for a rally that has not materialized as the U.S.-Iran conflict entered its 28th day.

Almost all of the Top 100 digital assets posted losses over the last 24 hours.

Ondo Finance bucked the bearish trend, rising more than 8% over 24 hours — though it gave back most of its gains by midday — after announcing a partnership with Franklin Templeton to tokenize five ETFs across growth, large-cap, fixed income, equity income, and gold strategies through Ondo Global Markets.

Worldcoin (WLD) and MORPHO are today’s biggest losers, plunging 10% and 8%, respectively.

Macro Pressure Mounts

The selloff extended across traditional markets. The Nasdaq 100 fell to 23,300, now 10% below its January high. Oil topped $96 per barrel as diplomatic efforts to de-escalate the Iran conflict stalled, fueling inflation fears and pushing back expectations for Federal Reserve rate cuts.

The CME FedWatch tool shows a 96% probability that the Fed will hold rates steady at its next meeting, with 4% of the market now pricing in a 25-basis-point hike, a scenario that was virtually unthinkable a month ago.

U.S. spot Bitcoin ETFs recorded a net outflow of $171 million in a single day, the largest in three weeks, per CoinGlass data. Institutional demand has cooled notably since the Fed’s hawkish March rate decision, with recent days showing mixed, low-conviction flows.

Crusoe Unveils Massive AI Campus Partnership with Microsoft in Abilene

Microsoft is significantly expanding its artificial intelligence computing capabilities through a strategic collaboration with Crusoe in Abilene, Texas. The ambitious development features a 900 megawatt AI factory campus engineered to handle cutting-edge computational workloads. This facility represents one of the most substantial AI infrastructure projects currently emerging across the nation.

The planned campus will be positioned next to Crusoe’s current Abilene operations and will comprise two state-of-the-art data center structures. A dedicated onsite power generation facility will be integrated to enhance energy dependability and strengthen grid stability. When fully operational, the entire complex is projected to deliver 2.1 gigawatts of total capacity.

Development activities have commenced with initial land preparation and clearing operations now in progress. The inaugural building is scheduled to begin operations by the middle of 2027. Consequently, this rollout maintains Crusoe’s aggressive deployment schedule for enterprise-scale AI infrastructure projects.

Power Requirements Drive Design of Advanced AI Computing Facilities

The new campus architecture prioritizes energy infrastructure to accommodate escalating artificial intelligence computational needs. The facility will incorporate 900 megawatts of onsite power generation alongside battery storage capabilities. These systems will enable ultra-dense computing environments optimized for demanding GPU-based processing tasks.

Both structures will provide substantial computational capacity while employing closed-loop liquid cooling technology. This engineering approach minimizes water consumption and optimizes thermal control. Accordingly, the infrastructure design addresses the specific demands of high-performance artificial intelligence platforms.

This development represents the latest phase of the Abilene project, which has experienced rapid growth in recent periods. The original deployment began with 200 megawatts and subsequently expanded to 1.2 gigawatts spanning several buildings. Thus, this new campus consolidates the area’s position as a critical hub for large-scale AI implementation.

Geographic Advantages Position Abilene as AI Infrastructure Hub

Abilene has become an increasingly strategic location for AI infrastructure deployment, primarily due to reliable power supply and available land resources. Microsoft has secured approximately 700 megawatts of data center capacity from Crusoe in the surrounding area. This arrangement demonstrates the dynamic evolution of client requirements and infrastructure strategy.

The region has garnered significant industry interest due to multiple large-scale AI projects currently under development. Technology companies are actively realigning their asset portfolios to guarantee long-term access to computing resources. This pattern underscores the escalating competition within the AI infrastructure sector.

Crusoe is simultaneously establishing a production facility for modular AI infrastructure components designed to accelerate deployment schedules. The organization seeks to create standardized infrastructure solutions while navigating energy limitations affecting the broader industry. As such, the Abilene expansion exemplifies a significant industry transition toward scalable, energy-optimized AI development frameworks.

Crypto World

Why TRON price turned bearish even as Anchorage Digital added institutional TRX custody

- TRX dips despite Anchorage Digital enabling institutional custody.

- $0.309 is the key support, with $0.3189 acting as the immediate resistance.

- Market awaits active institutional adoption to boost TRX price.

TRON (TRX) has seen a slight dip to around $0.309, even as news broke that Anchorage Digital, the only crypto firm with a US federal banking charter, will add institutional TRX custody.

On the surface, this might seem contradictory since institutional adoption is usually bullish for digital assets.

But TRX’s price action suggests the market is not always immediately responsive to structural developments.

What Anchorage Digital’s move means for TRON

Anchorage Digital’s integration of TRON into its platform gives US institutional investors a regulated avenue to store, manage, and potentially stake TRX.

It is also part of a phased rollout, with plans including TRC‑20 token support and native staking.

From a technical standpoint, this is a strong signal of growing infrastructure and trust around TRON.

It lowers barriers for institutions that previously faced compliance or custody challenges.

In theory, such developments should increase demand for TRX and push the price upward.

However, markets often take time to internalise these structural changes.

Understanding the current bearish trend

There are likely several reasons for the temporary bearishness.

First, broader crypto market trends have been mixed, with key assets showing minor declines over the past 24 hours as oil rises over $110.

Second, some traders may be waiting for confirmation that institutions are actively using the custody service before entering positions.

Finally, TRX is facing a strong resistance near $0.3189, and on the lower side, there is a strong support around $0.3090 that, if broken, could trigger further downward pressure toward $0.3012.

Going by these levels, it is evident that the TRX price is currently bound in a narrow range, reflecting a period of consolidation.

What to expect over the weekend

While the short-term trend may seem bearish, the institutional integration remains a positive signal.

If adoption by institutions picks up, it could unlock new price ranges for TRX in the coming weeks.

The market may also respond to growing stablecoin activity on the TRON network, which highlights its ongoing utility.

For now, traders should watch for a breakout on either side of the current consolidation range.

A breakout above $0.3189 would confirm the continuation of its recent bullish momentum, while a break below $0.3090 would mean the beginning of a pullback after weeks of bullish trend that has seen it gain over 8%.

A new working paper from the European Central Bank examined four major protocols and found that a small number of actors control the bulk of governance token holdings.

A European Central Bank working paper challenges the notion that decentralized autonomous organizations (DAOs) deliver on their promise of distributed governance, finding that token holdings and voting power across four major DeFi protocols are heavily concentrated among a handful of actors.

The study examined governance structures at Aave, MakerDAO, Ampleforth, and Uniswap using data from late 2022 and mid-2023. The researchers analyzed the top 100 token holders and top 20 voters for each protocol, reviewed 248 governance proposals, and attempted to trace the real-world identities behind pseudonymous blockchain addresses.

The findings land at a moment when governance disputes are roiling some of the very protocols examined in the study, and DeFi projects more broadly are grappling with whether the Labs-plus-DAO structure is fit for purpose.

Top 100 Holders Command Over 80% of Supply

Across all four protocols, the top 100 holders controlled more than 80% of the total governance token supply during both snapshot periods. At Aave and Uniswap, the top five accounted for roughly half of all holdings. MakerDAO was the relative outlier, with the top five holding around 36%.

The concentration proved sticky over time, with distributions remaining largely unchanged between October 2022 and May 2023.

When the researchers dug into who sits behind the top addresses, they found that for most protocols, roughly half or more of holdings traced to addresses associated with the protocols themselves — encompassing treasuries, founders, and developer allocations — or to centralized and decentralized exchanges.

Protocol-associated addresses held 43% of Uniswap’s UNI supply. Centralized exchange holdings were particularly notable at Aave (16%) and Ampleforth (19%). Binance emerged as the dominant exchange holder across all four protocols, with holdings ranging from 2% to 15% of total supply.

The researchers cautioned that available data doesn’t distinguish between tokens held by exchanges on their own behalf versus those held in custody for customers.

Delegates Dominate Voting

The most active voters on governance proposals turned out to be predominantly delegates — entities to whom smaller token holders assign their voting power. This dynamic has long been a known issue in DAO governance, where low voter turnout and outsized whale participation leave a small group of recurring participants shaping protocol decisions.

The top voter at Uniswap in both snapshots was a16z, the venture capital firm, which saw its delegator count grow from 100 to 125 over the study period. At Aave, the protocol’s own smart contracts held the top-voter position.

Of the 68 top voters identified across all protocols, the researchers could not determine the identities of roughly one-third to nearly half of them. Among those they could identify, individuals made up about 21%, followed by Web3 companies at 19%, university blockchain societies, and VC firms.

Uniswap had the highest delegation rate at 27%, with its top 18 voters holding more than half the delegated power.

The ECB team also systematically categorized the 248 proposals and found that “risk parameters” — covering loan-to-value ratios, liquidation thresholds, borrowing rates, and debt ceilings — were the most common, accounting for 28%. Asset listing proposals made up 23%.

Implications for Regulation

The findings carry direct implications for the ongoing policy debate over how to regulate DeFi. The EU’s Markets in Crypto-Assets regulation exempts services provided in a “fully decentralized manner,” but the ECB researchers argue the protocols they studied fall well short of that standard.

Governance token holders, protocol developers, and centralized exchanges have frequently been proposed as potential regulatory entry points. However, the researchers concluded that the ambiguity surrounding who actually controls governance makes all three difficult to use in practice.

“It is not always clear who in the end is responsible or can be held accountable based on publicly available data,” the authors wrote.

The paper also drew parallels between DeFi governance and traditional corporate shareholder governance, noting that both systems suffer from low voter turnout and outsized influence by a small number of recurring participants.

But DeFi lacks the institutional safeguards — proxy voting rules, stewardship codes, disclosure requirements, and fiduciary obligations — that help mitigate those dynamics in public companies. As DAOs increasingly adopt formal legal structures, the researchers suggested that hybrid models integrating traditional legal frameworks with blockchain-based governance may ultimately be needed.

This article was written with the assistance of AI workflows. All our stories are curated, edited and fact-checked by a human.

- Vietnam is investigating a huge crypto fraud involving Vemanti Group.

- As crypto use grows, Vietnam is increasing rules and oversight.

- Nearby countries are also cracking down on online financial scams.

Hanoi, Vietnam — Authorities in Vietnam have initiated what officials believe to be one of the biggest online crime cases involving online assets, as more regions strive to counter online financial fraud.

Vemanti Group Becomes Focus of Public Attention

According to a state-related Vietnamnet source, police believe there is a large-scale scheme that drew billions of US dollars from investors. Although authorities have not released a precise assessment of the overall losses, initial reports indicate the financial impact could be substantial.

The inquiry has made Vemanti Group the center of attention, as it was reported only after the Ministry of Public Security publicly announced the case and local media subsequently covered it.

The company said that its board chairman Nhan Vuong and board member Chien Tran have been indicted in connection with the case.

In a statement, Vemanti argued that authorities in any jurisdiction had not informed it before the indictments were released. The firm said it has engaged U.S. legal representation as it evaluates the case and decides its next steps.

Vemanti also linked the probe to ONUS Pro, a digital-asset site identified as the center of the alleged scheme.

Vietnam Crypto Market Growth Draws Increased Scrutiny

The case comes as Vietnam remains one of the world’s most active cryptocurrency markets. The case comes as Vietnam remains one of the world’s most active cryptocurrency markets. Chainalysis reported that Vietnam ranked fourth in its 2025 Global Crypto Adoption Index, and digital assets are widely used at the grassroots level.

That authorities are paying more attention to fraud signals a broader shift toward a more restrictive approach as cryptocurrencies grow in popularity.

Regional Crackdown Expands Beyond Vietnam Borders

Vietnam is not the only country seeing a crackdown. The Central Bureau of Investigation (CBI) of neighboring India recently arrested a suspect in Mumbai who helped traffic people into scams in Myanmar.

Investigators claim that the victims were coerced into taking part in internet fraudulent schemes, such as cryptocurrency investment scams and international user romance scams.

The events underscore rising cooperation in the region with governments trying to stem cyber-enabled financial crimes related to digital assets.

CBI Arrests Kingpin of Transnational Cyber Slavery Network pic.twitter.com/15Yc1YLO4D

— Central Bureau of Investigation (India) (@CBIHeadquarters) March 26, 2026

- Solana price dropped 5% to near $83 on Friday.

- The altcoin fell as Bitcoin and Ethereum declined to $66,500 and below $1,990, respectively.

- Risk assets sank as Brent oil surged to $110 amid Iran war concerns.

Solana (SOL) price has slipped more than 5% as altcoins mirror declines in Bitcoin (BTC).

The downturn coincided with a dramatic surge in oil prices to $110 per barrel, fueled by geopolitical tensions in the Middle East, with President Donald Trump’s announcement of a deadline extension for Iran seemingly not assuaging sellers.

Iran has largely dismissed US claims that talks have shown progress.

Solana drops to $83 amid crypto dip on oil surge

Solana’s price plunged to a low of $83 during Friday’s session, marking a decline of over 5% within 24 hours.

This aligned with the broader crypto market’s vulnerability to macroeconomic shocks, with Bitcoin sliding to below $66,500.

BTC’s drop below $67k marks the first time bulls have seen these levels since March 9.

Losses triggered massive long liquidations across top altcoins.

The sharp decline for BTC came as oil prices topped $110 despite US President Donald Trump’s announcement of a 10-day extension to the deadline for Iran to open the Strait of Hormuz.

Trump had paused the move to strike Iran’s energy infrastructure by 5 days, but even then, the additional five days appear to have done little to soothe supply concerns.

US stocks faltered as the international benchmark Brent crude futures rose 2.7% to $110.94 a barrel.

Crude gains reversed earlier losses following the early March spike, which also saw BTC prices sink to support.

As risk appetite got a fresh bump, Solana’s trading volume spiked 13% to over $4.1 billion.

The surge in intraday volume across major exchanges signals panic, as the unwinding of leveraged positions has led to significant losses for long positions.

Solana price outlook

From a technical standpoint, Solana’s descent to $83 breached the 50-day exponential moving average (EMA) at $87.50, a critical support that now risks further erosion toward the 200-day EMA near $78.

The relative strength index (RSI) flashed oversold territory at 28, hinting at a potential short-term rebound if oil volatility eases.

However, the moving average convergence divergence (MACD) histogram remains deeply negative, confirming bearish momentum tied to the BTC correlation, which stands at 0.92 over the past month.

A sustained oil price above $110 could push SOL toward $75, but a de-escalation in Hormuz tensions might spark a relief rally back to the $95-$100 level.

Investors might also be looking to monitor US inflation data, with this likely to dictate the crypto market’s next move.

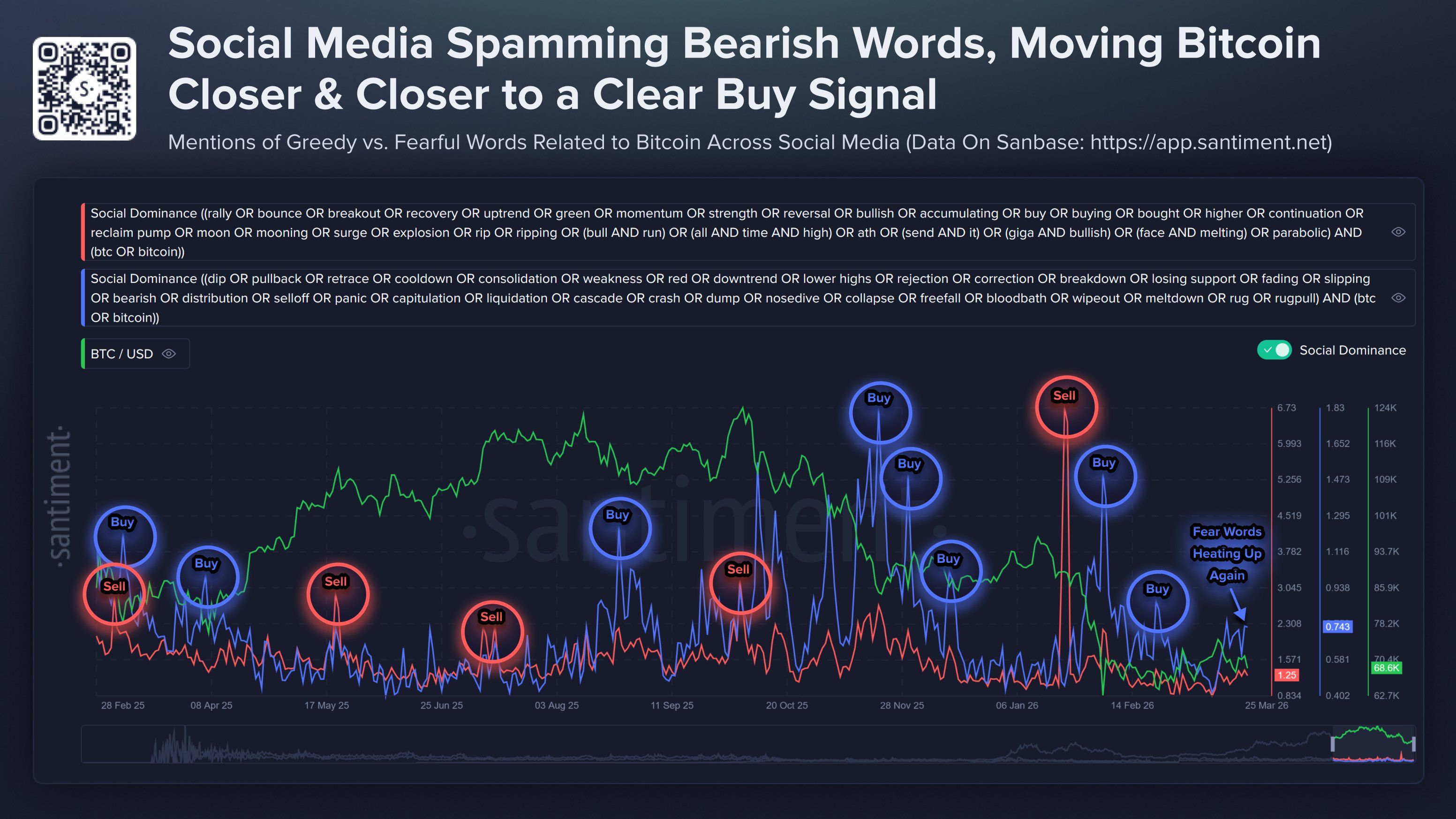

After a brief improvement in sentiment, fear has returned to the crypto market and continues to dominate social discussions. Bitcoin has dropped back below $70,000, raising concerns among retail investors.

Although negative sentiment is spreading across social media, on-chain data paints a more complex picture of retail investors’ actual role.

Retail FUD Sentiment Surges. Will Bitcoin Recover?

Blockchain analytics platform Santiment recently recorded a spike in negative Bitcoin-related keywords on social media.

Terms such as “dip” and “crash” appear frequently in BTC discussions. This reflects a significantly elevated level of FUD (Fear, Uncertainty, Doubt) among retail investors.

Santiment notes that extreme pessimism among retail investors often serves as a contrarian signal. When negativity becomes overwhelming, the market tends to recover as selling pressure nears exhaustion.

“Words like #dip, #pullback, #rejection, #crash, or #bloodbath, it’s usually a safe time to BUY,” Santiment stated.

Santiment’s chart illustrates this logic over the past year.

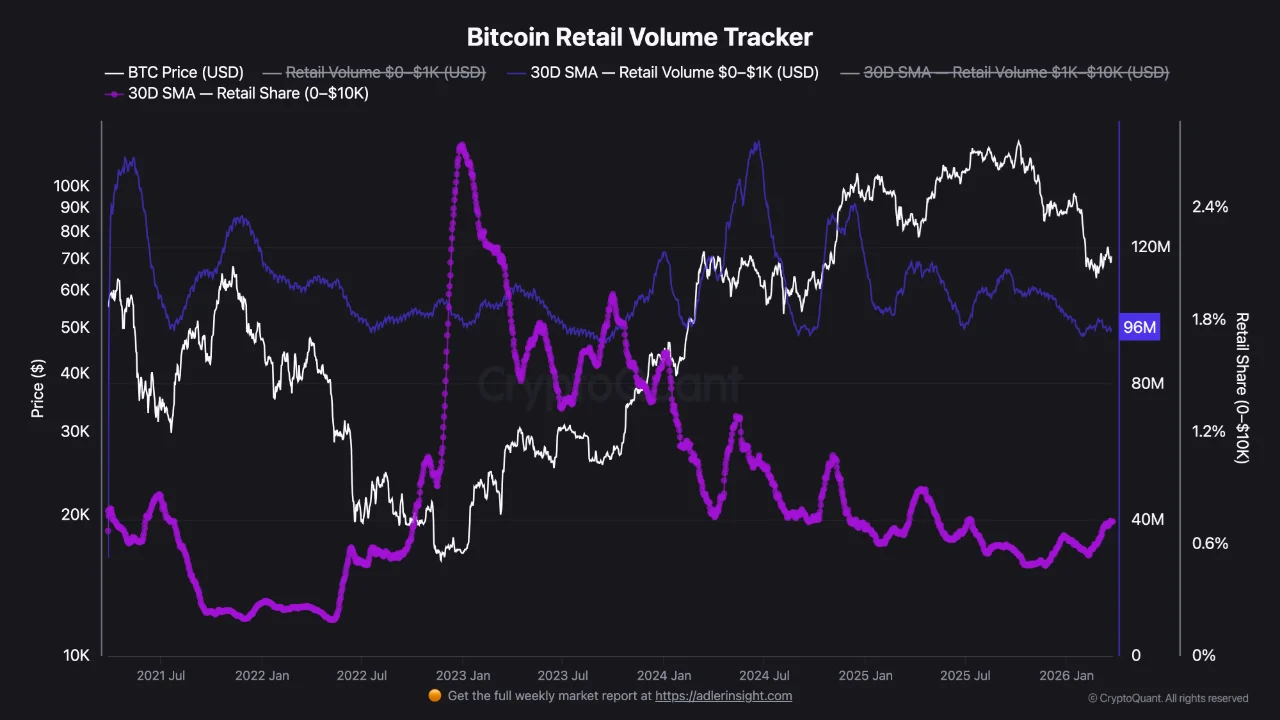

However, the picture goes beyond sentiment alone. A report from CryptoQuant reveals a concerning divergence between trading volume and the actual market share of retail investors.

Zizcrypto, an analyst at CryptoQuant, reported that the 30-day average small trade volume (0–$1,000) from retail stands at $96 million. This level aligns with the market bottom in early 2023.

Meanwhile, retail trading share (0–$10,000) has steadily declined since early 2023. It has dropped from over 2.4% to ~0.7% and has now stabilized.

The divergence between trading volume and market share suggests that retail investors remain active, but their structural role in the market is no longer expanding.

“In this context, retail participation is primarily concentrated in short-term reactive flows rather than sustained engagement,” Zizcrypto stated.

Therefore, Santiment’s view may hold in the short term. However, it is difficult to use it as a basis for predicting a reversal similar to early 2023.

The latest analysis from BeInCrypto indicates that if Bitcoin closes a daily candle below $68,930, the price could continue to decline toward $65,550.

The post Retail FUD Sentiment Rises as Bitcoin Falls Below $70,000: What Are The Implications? appeared first on BeInCrypto.

Why Mastercard paid double for stablecoin infrastructure it could have built

Taylor Swift And Travis Kelce Attend iHeartRadio Awards 2026

Why hasn’t Mitchell Starc joined Delhi Capitals yet? Alyssa Healy gives blunt reply | Cricket News

-

Crypto World7 days ago

Crypto World7 days agoNIO (NIO) Stock Plunges 6.5% as Shelf Registration Sparks Dilution Worries

-

NewsBeat2 days ago

NewsBeat2 days agoManchester United reach agreement with Casemiro over contract clause amid transfer speculation

-

Fashion7 days ago

Fashion7 days agoWeekend Open Thread: Adidas – Corporette.com

-

Politics7 days ago

Politics7 days agoJenni Murray, Long-Serving Woman’s Hour Presenter, Dies Aged 75

-

Crypto World6 days ago

Crypto World6 days agoBest Crypto to Buy Now: Strategy Just Spent $1.57 Billion on Bitcoin During Fear While Early Investors Quietly Enter Pepeto for 150x Potential

-

Crypto World6 days ago

Crypto World6 days agoBitcoin Price News: Bhutan Sells $72 Million in BTC Under Fiscal Pressure, but the Smart Money Entering Pepeto Sees What the Market Does Not

-

News Videos2 days ago

News Videos2 days agoParliament publishes latest register of MPs’ financial interests

-

Sports4 days ago

Sports4 days agoRemo Stars and Kano Pillars Strengthen Survival Hopes in NPFL

-

Sports4 days ago

Sports4 days agoGary Kirsten Accuses Pakistan Cricket Board Of ‘Interference’, Mohsin Naqvi Responds

-

Business5 days ago

Business5 days agoNo Winner in March 21 Drawing as Prize Rolls to $133 Million for Next

-

Tech5 days ago

Tech5 days agoGive Your Phone a Huge (and Free) Upgrade by Switching to Another Keyboard

-

Tech5 days ago

Tech5 days agoAI enters the chat: New Seattle dating app relies on tech to facilitate meaningful human connections

-

News Videos4 days ago

News Videos4 days agoCh 9 Financial Management Part 1 | Detailed One Shot | Class 12 Business Studies Boards 2026

-

Business7 days ago

Columbia Sportswear enters $500 million credit agreement with JPMorgan Chase

-

Tech6 days ago

Tech6 days agoToday’s NYT Connections Hints, Answers for March 22 #1015

-

Business21 hours ago

Business21 hours agoInstagram, YouTube Found Responsible for Teen’s Mental Health Struggle in Historic Ruling

-

Crypto World7 days ago

Crypto World7 days agoSmall-cap Russell 2000 enters correction territory

-

Business5 days ago

Business5 days agoWill Duke Basketball Win It All? Duke Basketball Enters Second Round as Third Favorite to Claim NCAA Title

-

Sports5 days ago

Sports5 days ago2026 Kentucky Derby horses, odds, futures, preview, date: Expert who hit 12 Derby-Oaks Doubles enters picks

-

NewsBeat5 days ago

NewsBeat5 days agoUpdate on Wisbech river crash as search for teenage boy enters fifth day

You must be logged in to post a comment Login