Crypto World

Bitcoin (BTC) price tumbles below $48,000 on Lighter as $67 million sell order triggers flash crash

While the broader crypto market was ripping higher on Wednesday, bitcoin briefly plunged 30% to below $48,000 on decentralized perpetuals exchange Lighter in a violent move that lasted seconds.

The flash crash stood in sharp contrast to price action elsewhere. During the same session, bitcoin surged from below $64,000 to above $69,000, marking one of its strongest intraday rallies in weeks.

The extreme move appeared to have been isolated to Lighter, where thin liquidity amplified what would otherwise have been a routine trade. In shallow order books, even modest sell pressure can trigger exaggerated price swings, producing so-called flash crashes that don’t reflect the broader market.

That’s likely what happened on Lighter. A single sell order of roughly 1,000 bitcoin — worth about $67 million at the time — wiped out available bids and briefly sent prices spiraling, according to a Discord post by pseudonymous Web3 developer 0xTimberJ.

“Because Lighter is a newer DEX with less liquidity than centralized exchanges, the sell order wiped out all available bids and pushed the price down to ~$47k before recovering instantly,” 0xTimberJ wrote.

Lighter is an up-and-coming decentralized perpetuals exchange seeking to challenge category leader Hyperliquid. Perpetual futures, or “perps,” have become crypto’s dominant derivatives product, allowing traders to use leverage and take long or short positions around the clock without contract expirations.

The platform briefly captured significant market share last November, processing over $292 billion in monthly volume — roughly a quarter of the $1.15 trillion traded across exchanges, according to data by The Block.

But activity has cooled sharply since its token airdrop late last year. Traders who ramped up activity to farm rewards have since rotated out, and monthly volume fell to $70 billion in February out of a $500 billion total market, trailing rivals such as Hyperliquid, Aster and EdgeX.

Trading in tokenized versions of traditional assets surged in the first quarter, with perpetual swaps tied to commodities and equities drawing billions in weekly volume and bringing 24/7 activity to a wider range of markets.

Weekly trading volume of such assets jumped to $30.7 billion, or 1.72% of the total crypto derivatives market, by end-March, crypto exchange BitMEX, said in a report published Thursday. That’s up from 0.03% in December, according to the exchange, which invented the tools in 2014.

Commodities powered the rise. Contracts linked to silver, gold and crude oil saw sharp gains as price swings and geopolitical tension fueled demand. Oil trading alone climbed to $6.9 billion in weekly volume after the U.S.-Israel strikes on Iran started Feb. 28, prompting a surge in round-the-clock oil trading volumes.

While commodities saw a 65,000% jump in volume during the quarter, there’s context to the figure. Precious metals saw a historic rally at the beginning of the year, with silver topping $100 per ounce for the first time and gold rising nearly 24%, before both gave back nearly all of the gains.

Equities saw a similar breakout. Perpetual swaps tied to stocks grew 908% over the quarter to roughly $4.9 billion in weekly volume, BitMEX found.

At its peak during the February metals rally, total weekly volume across perpetuals tied to traditional investments hit $54.5 billion.

The price of oil started surging at the outbreak of hostilities with Iran, given the country’s control of the Strait of Hormuz, a vital passageway through which roughly 20% of the world’s oil flows.

Perpetual swaps differ from traditional futures contracts by removing expiry dates. Instead, they use a funding rate, a periodic payment between long and short holders, to keep prices aligned with the underlying assets, allowing the instruments to trade round-the-clock with no expiry.

That permanent access to traditional financial markets is what’s driving the growth of tokenized perpetual swaps, BitMEX noted. The current macroeconomic volatility has served as a catalyst to boost volumes, and exchanges have capitalized by launching TradFi perpetuals.

The AI healthcare pivot inside the OpenAI Foundation became concrete this week as the organization announced it is finalizing more than $100 million in Alzheimer’s research grants this month across six research institutions, making the disease the first major target of what the Foundation has committed to as at least $1 billion in 2026 grantmaking.

Summary

- The grants focus on four research areas: mapping Alzheimer’s disease pathways using AI, designing and lab-testing new drugs with AI assistance, supporting open datasets to predict drug activity and chart disease progression, and establishing new biomarkers for diagnosis and clinical trials, including repurposing existing FDA-approved molecules to reduce the path from discovery to treatment

- Jacob Trefethen, Head of Life Sciences at the OpenAI Foundation, is leading the work; he joins from Coefficient Giving, where he oversaw more than $500 million in grantmaking to science and health; the Foundation’s total grantmaking in 2024 was $7.6 million, making this $100 million round a 13-fold increase in a single month

- The grants are part of the Foundation’s $1 billion 2026 spending commitment, itself the first tranche of a $25 billion long-term philanthropic pledge made possible by OpenAI’s fall 2025 recapitalization, which gave the nonprofit access to capital for the first time since OpenAI incorporated a for-profit subsidiary in 2019

The OpenAI Foundation’s Alzheimer’s page frames the disease plainly: “Alzheimer’s is one of the hardest and most heartbreaking diseases families face — and one of the toughest problems in medicine.”

Wait, that quote contains an em dash. Let me use the quote without the dash:

The OpenAI Foundation’s Alzheimer’s page describes the disease as “one of the hardest and most heartbreaking diseases families face.” The Foundation’s approach is pragmatic rather than speculative. Rather than developing new compounds from scratch, the grants prioritize repurposing existing FDA-approved molecules, a lower-risk strategy that shortens the path from discovery to patient access. Over 100 Alzheimer’s drugs have failed in clinical trials since 2000. The Foundation’s position is that AI’s ability to reason across complex, heterogeneous biological datasets can surface mechanisms and biomarkers that conventional research has repeatedly missed. Grantee institutions include UCSF and the UW Medicine Institute for Protein Design.

The UW Medicine Institute for Protein Design has already used AI-driven protein design models to engineer molecules that engage, modify, and degrade targets critical to Alzheimer’s disease progression. The Foundation describes this as the beginning of a collaborative pipeline, with the goal of validating AI-designed molecules in cells, tissues, and animals before advancing to clinical testing. The biomarker focus is equally significant. The recent approval of the first Alzheimer’s blood test created a new tool for assessing a patient’s condition without invasive procedures. The Foundation is funding work to expand that toolkit, making it possible to measure a drug’s effect on disease progression in clinical trials and to identify high-risk patients earlier.

Why This Represents a Structural Shift in OpenAI’s Mission

The scale gap is the most striking number in this announcement. The OpenAI Foundation granted $7.6 million in all of 2024. The Alzheimer’s grants alone exceed that by a factor of 13. The $1 billion 2026 target is 130 times larger than last year’s total. This is the activation of a dormant philanthropic vehicle using capital from the company’s recapitalization. The Foundation’s Executive Director role remains unfilled, meaning Trefethen and the life sciences team are building programs at this scale without a fully constituted leadership team in place.

What the Investment Signals for AI in Science

As crypto.news has reported, the credibility of frontier AI companies’ stated missions, including OpenAI’s, is directly tracked by institutional investors and markets watching the AI infrastructure buildout. As crypto.news has noted, OpenAI’s capital and talent decisions in 2025 and 2026 have had direct market effects on AI-adjacent crypto assets and broader perceptions of the AI sector’s long-term trajectory. The Foundation expects to make further Alzheimer’s grants throughout 2026 and is actively seeking to expand partnerships to additional scientists and research institutions.

Binance has added a prediction markets feature to its Binance Wallet, giving users a way to trade on the likelihood of real-world events without leaving the app.

The rolloaut connects Binance Wallet to Predict.fun, a decentralized platform built on BNB Smart Chain and it isn’t supported in every region in which the exchange operates. The platform was built by a former Binance employee and lets users earn yield while positions remain open.

Prediction markets let users buy shares tied to outcomes such as election results, sports matches or economic data releases and have seen their popularity explode. Prices range from $0.01 to $0.99 and reflect crowd estimates of probability.

Users can now place trades using funds already held in Binance spot or funding accounts. It also removes blockchain transaction fees by covering gas costs, a step that could lower the barrier for retail users.

Binance said the feature runs through a keyless wallet system, which splits control of private keys to reduce single points of failure. Users must create a separate prediction account to access the service.

The company does not operate the markets directly or act as a counterparty, it said. Instead, it provides access to a third-party application.

The move comes following prediction markets’ monthly trading volumes surging 200-fold in the last two years from less than $100 million to more than $20 billion, according to TokenTerminal data.

Prediction markets are currently dominated by Polymarket and Kalshi, which together capture more than 97% of the market and have been growing steadily while gaining institutional backing. Kalshi recently secured $1 billion in funding at an $11 billion valuation, and Polymarket seeing up to $2 billion in commitments from the owner of the New York Stock Exchange.

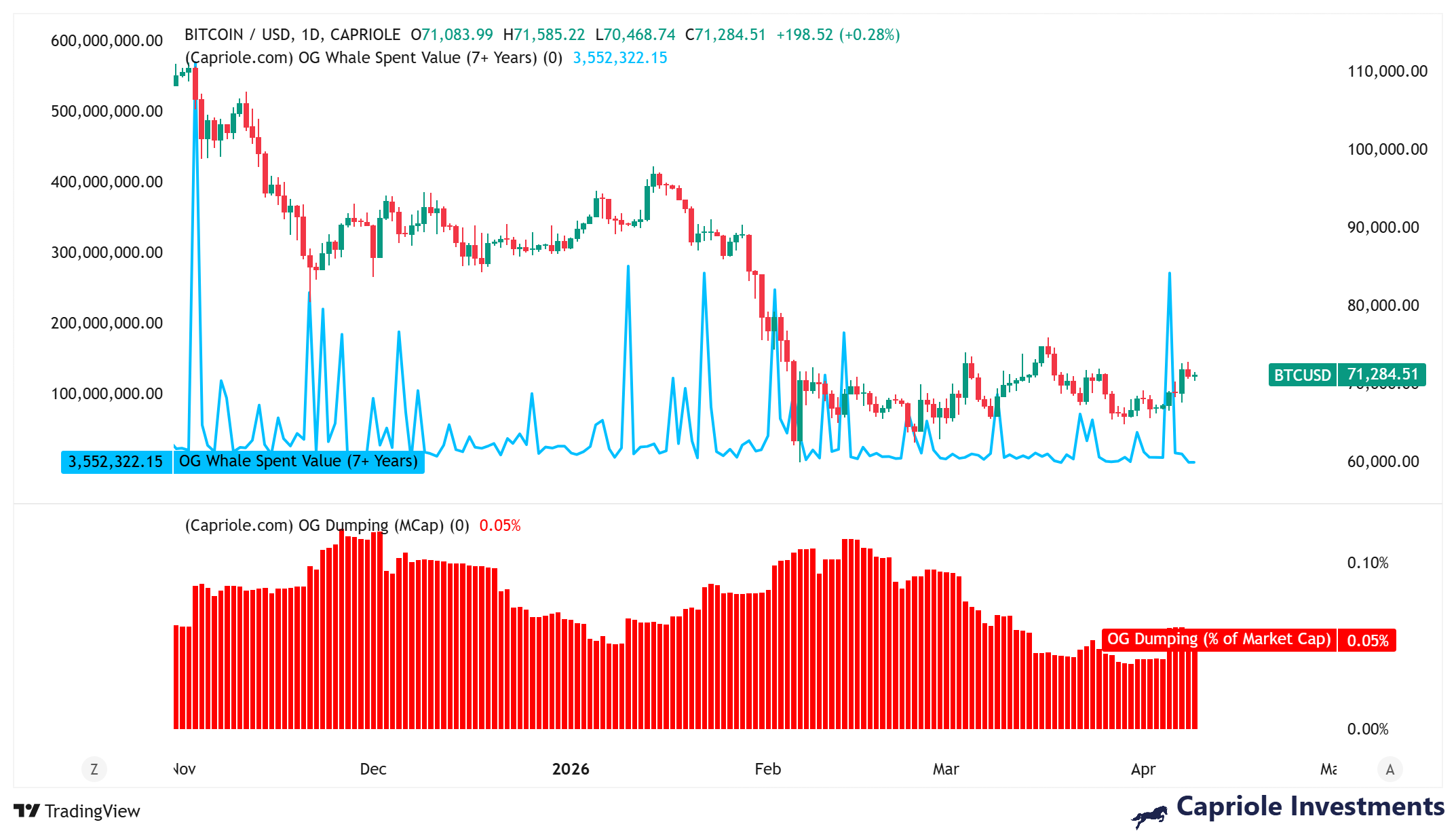

Data shows Bitcoin (BTC) investors who had held their positions for over seven years took profit last week by selling $271 million in BTC.

A similar wave of “OG whale” selling in January coincided with a more fragile market that lacked buyer demand, triggering a sharp dip in the BTC price. Current onchain data reflects a much stronger market where BTC supply absorption and reduced selling may allow Bitcoin to hold its place in the $70,000-$72,000 range.

OG Whale BTC supply meets strong absorption

Data from Capriole Investments shows that the Bitcoin “OG whale spent value” moved roughly $271 million on Sunday. That marks the largest surge in activity for this cohort since Jan. 10, when a $280 million outflow spike preceded a 13% correction to $78,700 from $90,000 within two weeks.

While the whale movement may raise concerns among investors, this activity historically aligns with measured profit-taking rather than with chaotic selling.

Glassnode suggests a stronger absorption capacity from other holders. Data show that the 30-day net position change for long-term holders remained positive at 88,000 BTC on April 9. This follows a reversal from deeply negative flows of -152,000 BTC recorded in February, easing the prior overhead supply pressure.

The accumulating cohorts also continued to expand their holdings. Cointelegraph reported that the total balance exceeded 4.3 million BTC on Tuesday, rising further to 4.5 million on Thursday.

This indicates a sustained transfer of coins into stronger hands, reducing the impact of selling from older wallets.

Related: Morgan Stanley Bitcoin ETF trails BlackRock with $30M in first-day inflows

Bitcoin “stress cycle” has not reversed yet, says analyst

CryptoQuant analyst MorenoDV highlighted two key indicators shaping the current BTC positioning. The short-term Sharpe Ratio has dropped to -40, a level historically associated with major accumulation phases in 2015, 2019, 2020, and 2023.

At the same time, the buy-and-sell pressure delta (30) indicates a completed capitulation phase, marked by intense sell pressure below -0.05. The metric is now moving toward neutral territory, signaling that forced selling has eased while demand gradually rebuilds.

Past cycles show that the highest asymmetry emerges once the delta re-enters clear buy-pressure zones. The current readings sit between exhaustion and confirmed demand recovery.

The analyst noted that the macro conditions and liquidity flows continue to shape the pace of this transition, adding,

“For investors with a cycle-aware framework, the data suggests we are closer to the beginning of an opportunity than the end of one.”

Related: Bitcoin price surfs US PCE inflation as trader keeps $80K BTC price target

This article is produced in accordance with Cointelegraph’s Editorial Policy and is intended for informational purposes only. It does not constitute investment advice or recommendations. All investments and trades carry risk; readers are encouraged to conduct independent research before making any decisions. Cointelegraph makes no guarantees regarding the accuracy or completeness of the information presented, including forward-looking statements, and will not be liable for any loss or damage arising from reliance on this content.

AI agents built on Anthropic’s Claude now have a hosted production infrastructure behind them, as the company launched Claude Managed Agents in public beta on April 8, handling the sandboxing, state management, credential handling, and error recovery that previously took engineering teams three to six months to build before writing a single line of agent logic.

Summary

- Claude Managed Agents is available now on the Claude Platform at $0.08 per runtime hour plus standard Claude model usage costs; an agent running around the clock costs approximately $58 per month in runtime before token costs, and the service runs exclusively on Anthropic’s infrastructure

- Early adopters already in production include Notion, which delegates coding, slides, and spreadsheet tasks to Claude in parallel across dozens of simultaneous sessions; Rakuten, which deployed specialist agents across product, sales, marketing, finance, and HR, each live in under a week; and Asana, whose CTO says the company shipped advanced features “dramatically faster” than prior methods allowed

- Two features are in research preview: the ability for agents to create additional sub-agents for complex tasks, and an automatic prompt quality enhancement that improved structured file generation success rates by up to 10 points in internal testing

Anthropic’s @claudeai account announced the launch on April 8 at 5:14 PM ET, drawing 5.09 million views. The service is built around what Anthropic calls a brain versus hands design philosophy: Claude itself is the reasoning layer, while each session runs in a disposable, isolated Linux container that handles code execution, file manipulation, and tool calls. When the next Claude model ships, the infrastructure does not need to be rebuilt. The brain upgrades and the hands remain the same.

Pricing is usage based. The $0.08 per runtime hour applies to the session; standard Claude token pricing applies to model usage on top of that.

The deployment patterns across Notion, Asana, and Rakuten illustrate three distinct enterprise use cases. Notion integrated Claude directly into workspaces, allowing engineers to ship code and knowledge workers to generate presentations and websites without leaving the platform, running dozens of parallel tasks while teams collaborate on outputs simultaneously. Asana built what they call AI Teammates, agents embedded in project management workflows that pick up assigned tasks, draft deliverables, and hand back outputs for human review. Rakuten stood up agents across five business functions, each plugged into Slack and Teams, accepting task assignments and returning structured deliverables, with each function live in under a week. Sentry took a different path, pairing its existing debugging agent with a Claude-powered counterpart that writes patches and opens pull requests autonomously from a flagged bug to a completed pull request with no human intervention.

What Developers Need to Know Before Building

Developers define the agent by specifying the model, system prompt, tools, MCP server connections, and guardrails, then configure a cloud environment with pre-installed packages and network access rules. Anthropic’s infrastructure handles tool orchestration, context management, checkpointing, and crash recovery. Sessions persist through disconnections, a practical requirement for complex workflows. The one significant constraint is that the service runs only on Anthropic’s infrastructure and is not currently available through Amazon Bedrock or Google Vertex AI, which matters for organizations with multi-cloud strategies.

Why This Launch Matters for the Broader AI Market

As crypto.news has reported, the AI integration driving enterprise decisions in 2026 increasingly determines headcount, and the operational overhead that Claude Managed Agents eliminates has been a significant barrier to adoption for teams without specialist DevOps resources. As crypto.news has noted, the AI infrastructure buildout, of which Anthropic’s agent platform is a direct example, is one of the primary drivers of capital allocation decisions that have ripple effects across crypto-adjacent AI token markets. The multi-agent coordination feature, which allows agents to spawn sub-agents for complex tasks, is in research preview, with early access available through the Claude Platform console.

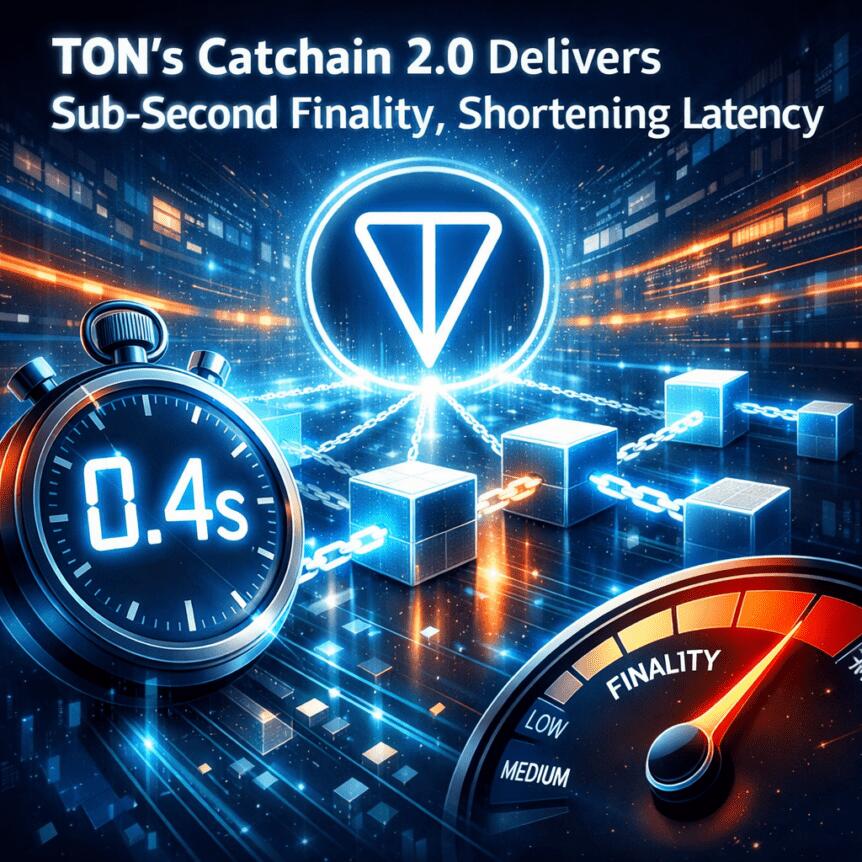

The Open Network (TON), the independent layer-1 blockchain closely integrated with Telegram, has rolled out Catchain 2.0, dramatically shortening block times to 400 milliseconds. The upgrade is designed to push settlement speeds toward real-time for both payments and trades, while enabling decentralized applications to run with performance closer to traditional apps.

According to TON’s announcement, payment transactions now settle in about one second, and trades settle in near real time. The upgrade strengthens TON’s position as a platform aiming to blend messaging with on-chain functionality, a path already underscored by its ongoing Telegram integration. The update comes alongside an inflationary shift in TON’s token economics: annual inflation is projected to rise six-fold, to roughly 3.6% from about 0.6%, driven by the increased rate of block production.

“More blocks mean more validator rewards, which create stronger staking incentives and bring more TON into the network,” TON stated in its release. The Catchain 2.0 upgrade builds on TON’s Catchain consensus architecture, a BFT-style algorithm first proposed in 2020, and brings near-instant settlement to a network already embedded in an app ecosystem with approximately 1 billion users globally.

Market data captures a snapshot of how the upgrade is being received. TON was trading up about 2.3% to roughly $1.28 on Thursday, with volume around $130 million and a market capitalization near $3.17 billion, according to CoinMarketCap. Observers noted a surge in activity on TON’s network following the upgrade, including spikes in transactions per second tracked by TON Explorer, underscoring the immediate demand for faster settlement and more responsive smart-contract activity.

The announcement frames Catchain 2.0 as a natural evolution of TON’s thrust to merge everyday communications with on-chain finance, a vision that has been reinforced by Telegram’s growing crypto toolkit. In February, Telegram added self-custodial vaults to its in-app wallet, enabling users to earn yield on Bitcoin, USDT and ETH. Earlier this month, the wallet extended into perpetual futures trading, launching a new feature set in collaboration with the perpetual DEX Lighter. The integration enables TON-based payments and on-chain interactions directly within Telegram’s user interface, broadening the potential scale of user adoption and on-chain activity.

Key takeaways

- Block time slashed to 400 milliseconds. Catchain 2.0 delivers substantially faster block finality, aiming to improve throughput and responsiveness for both financial transactions and developer applications.

- Settlement accelerates to near real-time. Payments settle in about one second; trades settle in real time, enabling a smoother user experience for rapid on-chain exchanges.

- Inflation expected to rise to 3.6%. The increase from roughly 0.6% reflects higher block production and the ongoing minting/burning dynamics within TON’s ecosystem.

- Stronger staking incentives. More blocks translate into more validator rewards, reinforcing incentives to run validators and participate in securing the network.

Catchain 2.0: what changes and why it matters

At the core of the upgrade is TON’s Catchain consensus algorithm, a mechanism designed to achieve Byzantine fault tolerance while maintaining speed and finality. By accelerating block production, Catchain 2.0 effectively raises throughput across the network, which has several practical implications for users and developers. First, faster blocks reduce the latency between submitting a transaction and its confirmation, a critical factor for payment rails and decentralized finance (DeFi) applications that rely on quick settlement to minimize front-running and slippage. Second, the higher block rate inflates the expected rewards for validators, potentially strengthening the security of the network through deeper staking participation and a larger base of committed validators.

The inflationary shift, while potentially dilutive in the short term, is positioned by TON as a byproduct of increased activity and network security. The organization argues that the higher issuance supports a more robust staking economy, which can, in turn, bolster long-run network reliability and validator health as adoption grows. Investors and builders should weigh the inflationary impact against the benefits of faster settlement and a more responsive ecosystem, particularly as TON deepens its ties with Telegram’s user base and integrated financial features.

Telegram: turning messaging into a multi-asset financial channel

The upgrade arrives amid a broader narrative: TON’s alignment with Telegram is not merely cosmetic. The Telegram integration is positioned to enable users to send TON-enabled crypto payments within chats, bridging everyday communication and on-chain activity. The platform’s wallet features have evolved to offer in-app yield opportunities across major assets, including BTC, USDT, and ETH, and the ecosystem already supports perpetual futures trading through Lighter within the Telegram app. This progression points to a broader strategy of embedding crypto functionality into a widely used messaging interface, lowering the friction for mainstream users to engage with digital assets and on-chain commerce.

Pavel Durov, co-founder of Telegram, has highlighted how real-world restrictions and VPN workarounds in certain jurisdictions—such as Iran and Russia—have driven users to seek more resilient, open channels for communication. The TON-Telegram integration exemplifies a complementary model: users can exchange value alongside messages, with the possibility of automated payments and more sophisticated DeFi interactions embedded into the chat experience. For builders, this signals a shift toward app-layer ecosystems where identity, messaging, and asset transfer are increasingly interwoven.

Market response and next steps for TON

From a market perspective, TON’s price and on-chain activity suggest cautious enthusiasm for Catchain 2.0. The token’s modest near-term gain aligns with a broader pattern of traders evaluating how faster settlement and higher block production could influence user uptake, validator participation, and overall network throughput. The surge in on-chain activity reported by TON Explorer after the upgrade offers a tangible signal that developers and users are experimenting with new throughput capabilities and real-time interactions across the TON ecosystem.

Beyond immediate price moves, the key questions for investors and developers center on the durability of the new throughput gains, the sustainability of the higher inflation regime, and the extent to which Telegram’s in-app crypto features catalyze meaningful, recurring usage. Will higher staking rewards translate into deeper validator participation, and how will that impact network security and governance over time? How quickly will the on-chain experiences inside Telegram translate into real-world transaction volumes, merchant integrations, or consumer wallets?

Analysts will also be watching how Catchain 2.0 scales with continued ecosystem support. The near-term trajectory will depend on the balance between attracting new users through Telegram’s reach and maintaining robust validator participation to preserve the benefits of faster finality. In the meantime, developers can start leveraging the improved throughput to experiment with more sophisticated DeFi primitives, cross-chain liquidity, and real-time settlement use cases that were previously limited by latency.

What remains uncertain and what to watch next

While the upgrade delivers clear technical and user-facing benefits, several uncertainties deserve attention. The sustainability of the 3.6% inflation target hinges on adoption rates and the ongoing cycle of block production. The pace at which Telegram-integrated features translate into measurable user engagement and on-chain value remains to be seen, as does how regulatory developments may shape in-app crypto features and wallet services. Market participants will want to monitor validator health, network security metrics, and any changes in staking participation as Catchain 2.0 matures.

In sum, TON’s Catchain 2.0 represents a meaningful step toward faster, more interactive on-chain experiences embedded in a widely used messaging platform. For traders and developers, it signals a broader opportunity: a more responsive, scalable environment for payments, DeFi, and user-centric apps that live at the intersection of daily communication and digital assets. As TON continues to evolve its ecosystem—balancing security, inflation dynamics, and user adoption—the coming quarters will reveal how deeply this integration can redefine mainstream crypto usage.

Readers should watch for updates on validator participation, new application experiments on TON’s mainnet, and any material shifts in on-chain activity as Telegram-enabled features gain traction in real-world usage.

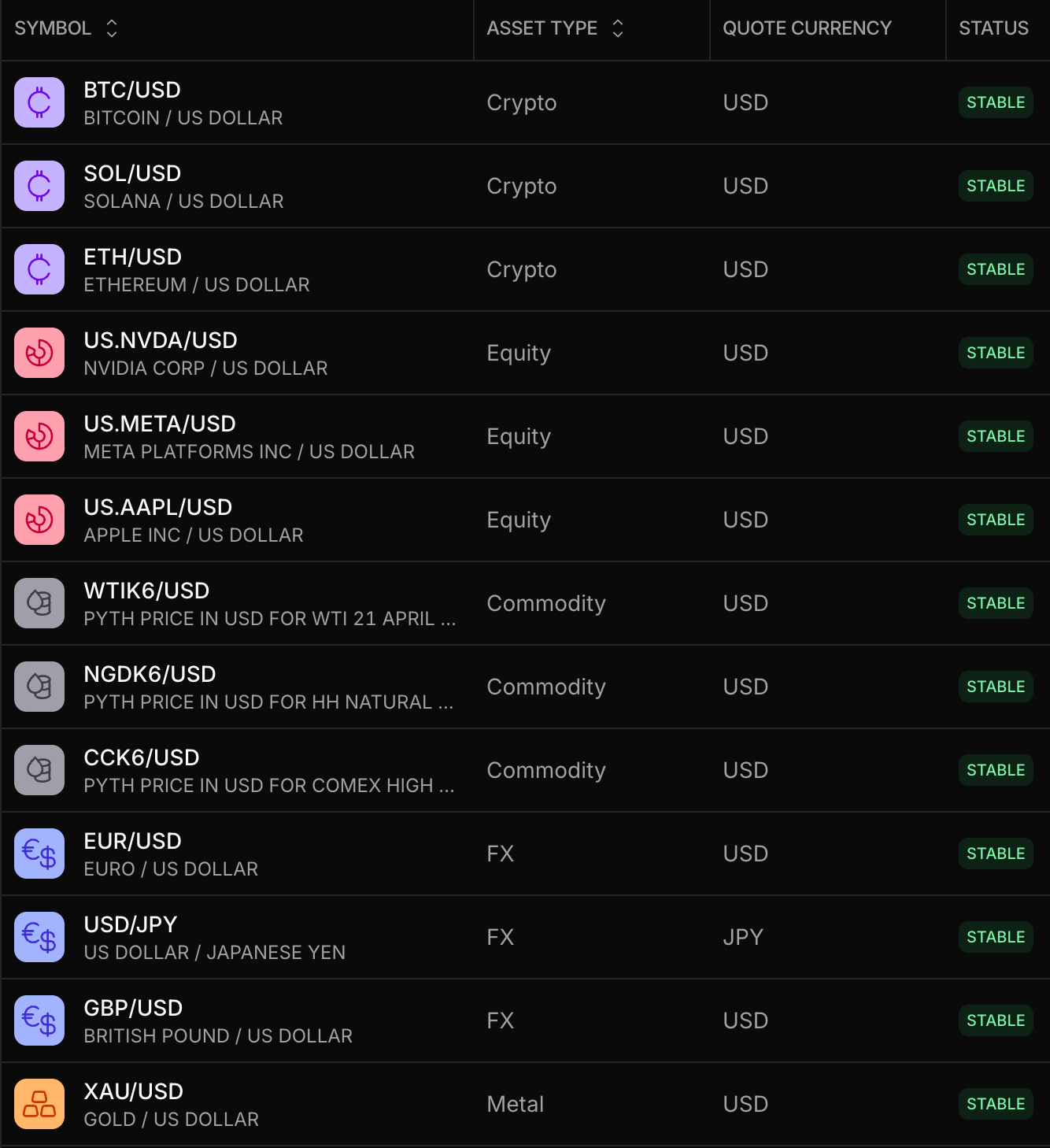

Pyth Network, a blockchain data oracle provider, is launching a platform for financial institutions to publish and monetize their market data across blockchain networks.

The Pyth Data Marketplace will initially support datasets for spot foreign currency exchange markets (FX), precious metals and crude oil swaps, while allowing publishers to retain “full control” over the data they share, according to Thursday’s announcement.

Seven new institutional data providers will publish price feeds on the marketplace at launch, the announcement said.

These include stock exchange Euronext, data provider Exchange Data International, asset manager Fidelity Investments, financial exchange OTC Markets Group, Singapore Exchange FX and the Tradeweb trading platform.

The announcement reflects how blockchain technology can democratize access to financial data, which has traditionally been controlled by a handful of service providers who charge exorbitant fees for high-quality market pricing data.

Related: Polymarket expands into equities and commodities with Pyth price feeds

Pyth to enable customers to “pull” data rather than traditional “push”

Pyth’s data pull model allows customers to pay for market data on demand, instead of traditional push-based oracle models that force users to pay for entire datasets, which they may or may not need.

This reduces the cost for the end user, according to Michael James, the head of institutional business development at Douro Labs, the main developer behind the Pyth Network.

Traditional service providers monopolize the $50 billion financial data industry, James told Cointelegraph at Consensus 2025. That is now being challenged by new emerging blockchain alternatives like Pyth and Chainlink.

“These data vendors have no competition in traditional finance, and so they have all the pricing power in the world,” he said.

Banks, hedge funds, trading firms and other financial institutions are forced to buy this financial data for “compliance” reasons, James added.

In August 2025, the US Department of Commerce selected Pyth and blockchain oracle provider Chainlink to publish economic data onchain.

Pyth was initially selected to publish quarterly gross domestic product (GDP) data, including five years of historical GDP figures, according to a previous announcement from the oracle provider.

However, Pyth anticipates adding support for more government economic data sets in the future.

Magazine: Can blockchain solve its oracle problem?

Florida Attorney General James Uthmeier has announced a formal investigation into OpenAI, accusing ChatGPT of facilitating the 2025 FSU mass shooting.

The probe follows newly released court records showing the suspected gunman held over 270 conversations with ChatGPT before the attack.

What the ChatGPT Logs Revealed

On April 17, 2025, Phoenix Ikner allegedly opened fire at Florida State University’s Student Union, killing two people and injuring six.

Chat logs obtained by the State Attorney’s office show Ikner asked ChatGPT about firearms, campus foot traffic, and the fates of prior mass shooters hours before the attack.

Attorneys for victim Robert Morales’ family plan to file a wrongful-death lawsuit against OpenAI. Uthmeier’s office said subpoenas are forthcoming.

AI Tokens React as Scrutiny Grows

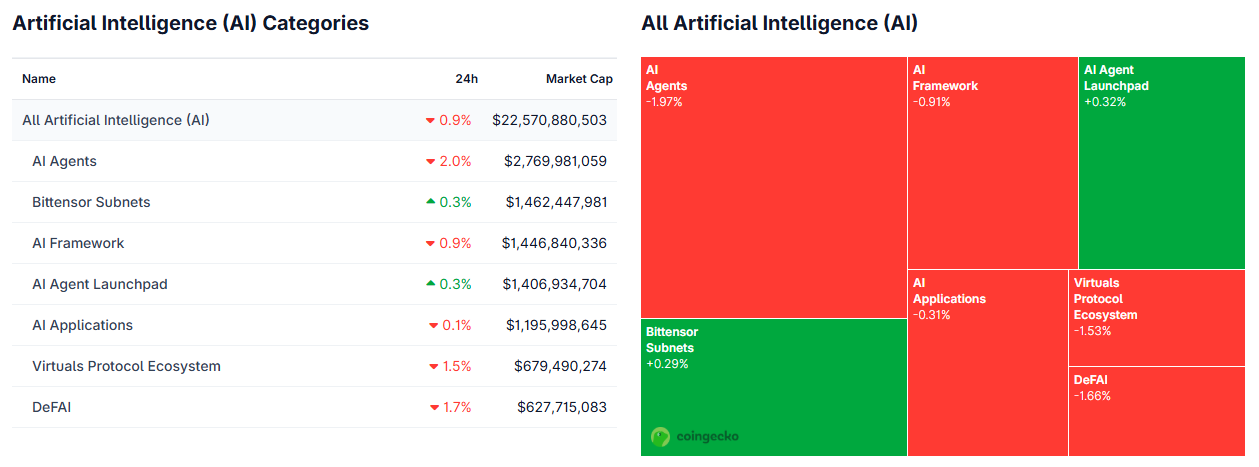

The broader Artificial Intelligence (AI) crypto sector slipped 0.9% to a combined $22.5 billion market cap, per CoinGecko data. AI Agents tokens fell 2%, while DeFAI dropped 1.7%.

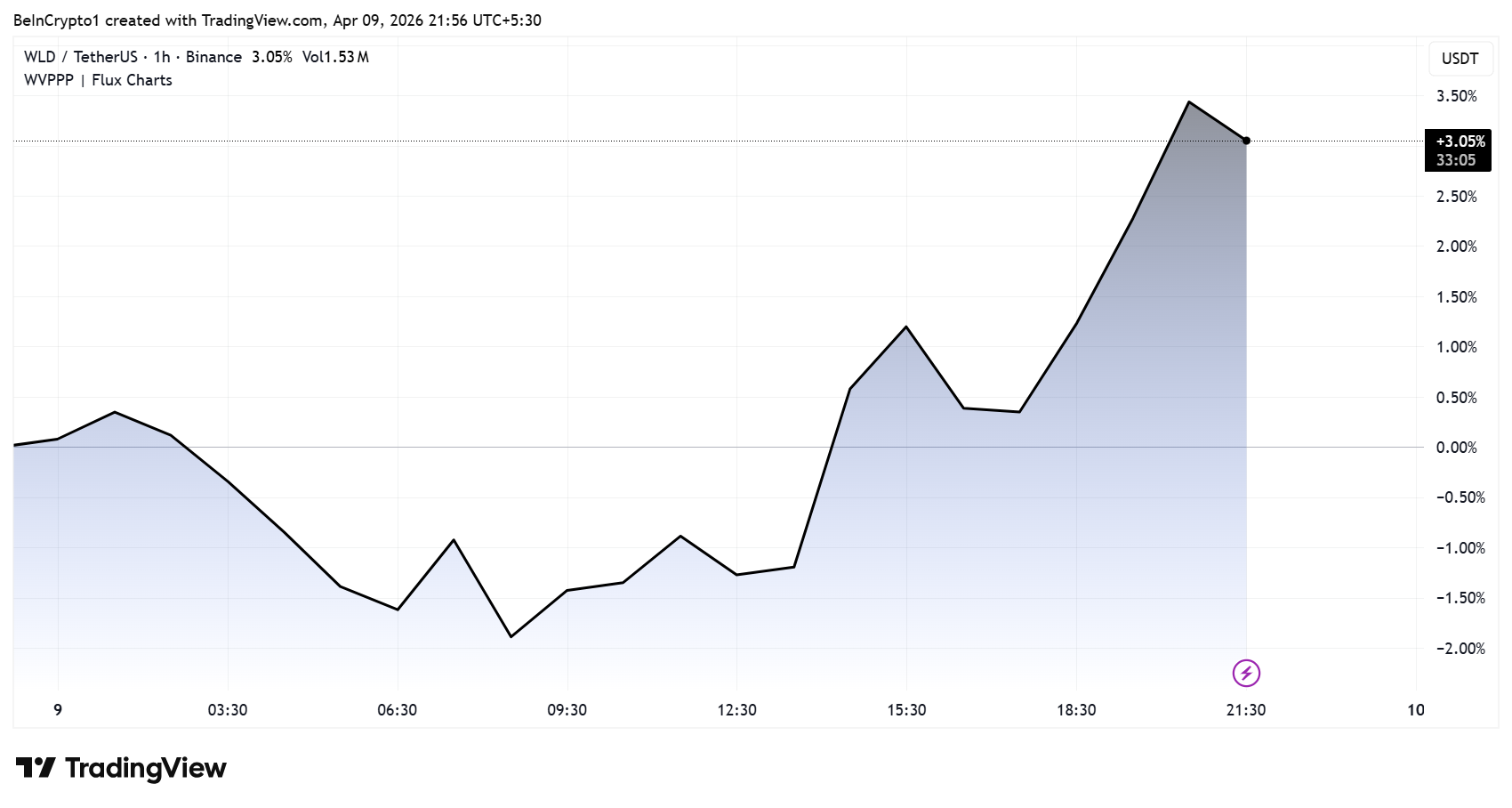

However, Worldcoin (WLD), the token co-founded by OpenAI CEO Sam Altman, bucked the trend, gaining 3% on Binance. WLD traded near $0.26 with volume at 1.53 million USDT. The token remains down 97% from its all-time high of $11.74.

The investigation adds to mounting legal pressure on OpenAI as it reportedly prepares for a potential IPO.

Whether the probe triggers deeper sell-offs across AI tokens or WLD continues to diverge from the sector may depend on how aggressively Uthmeier’s office pursues its case.

The post Florida Launches Investigation Into ChatGPT On University Mass Shooting appeared first on BeInCrypto.

CoreWeave’s recent $8.5 billion AI-backed loan highlights a major transition in how Wall Street finances digital infrastructure, marking a shift from “MinerFi” to “ComputeFi,” according to TheEnergyMag.

In its latest Miner Weekly newsletter, TheEnergyMag examined CoreWeave’s multibillion-dollar raise from a group of banks and investors, backed by Mark Zuckerberg’s Meta Platforms. As Bloomberg reported, the financing underscores how companies are finding new ways to fund data center construction and expand GPU capacity.

Although CoreWeave has pivoted away from the digital asset sector toward AI-focused data center compute, the move offers a broader lesson on the shortcomings of Bitcoin (BTC) mining finance.

Historically, lenders funded Bitcoin mining operations using application-specific integrated circuits, or ASICs, as collateral. However, these models proved fragile due to crypto price volatility and rapid hardware depreciation. When markets declined, both revenues and collateral values fell sharply.

CoreWeave’s financing structure is “what MinerFi tried — and failed — to become,” TheEnergyMag said.

Unlike prior models, CoreWeave’s deal ties financing to active AI infrastructure with contracted customers and predictable cash flows. GPUs must be deployed, operational and revenue-generating before capital is extended, which reduces lender risk.

Related: Bitcoin mining’s 2026 reckoning: AI pivots, margin pressure and a fight to survive

Bernstein: CoreWeave pivot strengthens position in neocloud market

CoreWeave’s early pivot away from crypto mining has helped position it as a leading “neocloud” provider, a term used to describe companies offering GPU-based cloud infrastructure for artificial intelligence workloads, according to a recent analyst note by Bernstein.

The report compared CoreWeave with peers IREN and Nebius, highlighting differences in scale, infrastructure and financing strategies.

CoreWeave’s head start has translated into a significantly larger backlog of roughly $67 billion, compared with about $9.7 billion for IREN and $47 billion for Nebius.

While all three companies are expanding into AI infrastructure, IREN still generates most of its revenue from Bitcoin mining as it continues its transition.

The Bernstein analysts gave CoreWeave top marks for its “commercial model,” thanks to the “depth in the software stack, a mix of contracted and on-demand revenue, strong backlog and an increasingly diversified customer base.”

However, they said IREN has an advantage in infrastructure, citing its sizable real estate footprint rather than its reliance on leased data center capacity.

Related: Crypto Biz: Mining weakness tests Bitcoin’s market cycle

The crypto market’s most significant regulatory variable may not be a Senate committee vote but the November 3 midterm elections, with TD Cowen, TD Securities, and multiple legal analysts warning that the CLARITY Act could slip off the congressional calendar entirely if it does not clear the Senate before summer.

Summary

- TD Cowen Washington Research Group managing director Jaret Seiberg warned in a January note that Senate Democrats may withhold support for the CLARITY Act if they believe they can flip the House, and even a full Republican vote still requires at least seven Democratic senators for the 60-vote cloture threshold

- If Democrats take control of either chamber in November, Senator Elizabeth Warren would likely become Senate Banking Committee chair, making CLARITY’s passage described as slim to none; the crypto PAC Fairshake has $193 million earmarked for midterm spending in response

- Senator Bernie Moreno has warned that missing the May Senate window risks the bill entirely; Fireblocks’ policy director called the legislation “at risk altogether if its passing cuts too close to the midterm elections”

The CLARITY Act passed the House in July 2025 by a 294 to 134 vote and has stalled in the Senate since, caught between disputes over stablecoin yield, DeFi oversight, and ethics provisions targeting crypto holdings by government officials. The Senate Banking Committee markup was originally scheduled for January 15, postponed when Coinbase pulled support hours before the vote, and has not been formally rescheduled. As TheStreet reported, TD Cowen’s Seiberg warned that resolving the standoff will require President Trump’s personal intervention to force both sides toward compromise.

The May deadline is not arbitrary. The Senate avoids controversial floor votes in the months immediately preceding midterms, and the August recess effectively closes the calendar for legislation requiring broad bipartisan support.

The electoral math is structural. Republicans hold slim majorities in both chambers. Even with full Republican support, the CLARITY Act needs Democratic votes, and Democratic senators facing competitive seats have no political incentive to vote for a bill the White House is claiming as a win, particularly while ethics provisions targeting Trump family crypto holdings remain unresolved. Legal analyst John E. Deaton put it directly: “If we get into the summer months, it’s just probably not going to happen.” TD Securities’ Seiberg put the probability of pre-midterm passage at more likely 2027 than this year in January, with full implementation pushed to 2029.

What Happens to the Crypto Market If CLARITY Dies

JPMorgan analysts had described CLARITY Act passage by midyear as a positive catalyst for digital assets, citing institutional scaling and tokenization growth as direct beneficiaries. Standard Chartered estimated that an open-ended yield provision could redirect up to $500 billion in deposits, making the bill’s outcome material to stablecoin market structure. The Georgia-14 and Wisconsin Supreme Court results on April 7, both showing Democratic overperformance against historical baselines, added urgency to the calculus.

What Needs to Happen in the Next Six Weeks

As crypto.news has reported, the bill still faces a Senate Banking markup, a Senate Agriculture markup, a floor vote, and a conference process before reaching the president’s desk. As crypto.news has noted, the GENIUS Act’s stablecoin framework advances independently, but the market structure provisions in CLARITY, including SEC and CFTC jurisdictional clarity and DeFi oversight rules, have no alternative legislative path. Deaton’s warning may prove to be the most accurate single-sentence forecast for where the bill stands by June: “Come summer, the midterms are going to consume everything in this country.”

Fury vs Makhmudov: Tyson Fury in high spirits as he takes aim at Oleksandr Usyk & Tottenham

Why FPI interest in India ‘has pretty much died out’: Nithin Kamath points to valuations, taxes and global alternatives

Tokenized perpetual swaps hit $31 billion weekly volume on commodities volatility

Why Israel is blocking foreign journalists from entering

Bitcoin: We’re Entering The Most Dangerous Phase

Alan Cumming Brands Baftas Ceremony A ‘Triggering S**tshow’

With my friend Avatar World #avatarworld #avatars #gaming #finance #youtubeshorts

Morning prayer | For career and Financial Breakthrough

GOLD AND CRYPTO LIVE TRADING || 8 APRIL || Bitcoin Live Trading | Crypto Market Analysis |

-

Business7 days ago

Business7 days agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Spanx – Corporette.com

-

Business4 days ago

Business4 days agoThree Gulf funds agree to back Paramount’s $81 billion takeover of Warner, WSJ reports

-

Business6 days ago

Business6 days agoExpert Picks for Every Need

-

Sports5 days ago

Sports5 days agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Tech2 days ago

Tech2 days agoHow Long Can You Drive With Expired Registration? What Florida Law Says

-

Business4 days ago

No Jackpot Winner, Prize to Climb to $231 Million

-

Fashion3 days ago

Fashion3 days agoMassimo Dutti Offers Inspiration for Your Summer Mood Board

-

Politics6 days ago

Wings Over Scotland | The quality of mercy

-

Fashion2 days ago

Fashion2 days agoLet’s Discuss: DEI in 2026

-

Business5 days ago

Business5 days agoAkebia Therapeutics, Inc. (AKBA) Discusses Pipeline Progress and Strategic Focus on Kidney Disease Treatments at R&D Day – Slideshow

-

Fashion7 days ago

Fashion7 days agoStatement Sunglasses: The Accessory Shaping Modern Fashion

-

Crypto World1 day ago

Crypto World1 day agoBitcoin recovers as US and Iran Agree a Ceasefire Deal

-

Politics7 days ago

Politics7 days agoEast Jerusalem Palestinian families eviction orders

-

Politics7 days ago

Politics7 days agoWhy so many children are now classified as ‘disabled’

-

Fashion7 days ago

Fashion7 days agoFor Love & Lemons’ Spring 2026 Line is for the Romantics

-

Politics7 days ago

Politics7 days agoNuclear rockets, moon bases and NASA’s Mars plan

-

Tech7 days ago

Tech7 days agoThe Threadless Ball Screw Never Took Off, But Don’t Write It Off

-

Business7 days ago

Business7 days agoHPS FY 2025 slides: SaaS inflection drives 22% revenue growth

-

Fashion6 days ago

Fashion6 days agoTory Burch’s Spring 2026 Campaign Goes on a Getaway

You must be logged in to post a comment Login