Crypto World

Bitcoin’s volatility spikes to its highest since FTX’s collapse as prices crater to nearly $60,000

Bitcoin’s Wall Street-like fear gauge has spiked to its highest level since the collapse of the FTX exchange in 2022, signaling intense market panic as prices plummeted to nearly $60,000.

Volmex’s bitcoin volatility index (BVIV), which represents the annualized expected price turbulence over four weeks, jumped to nearly 100% from 56% on Thursday.

The index serves as a crypto equivalent to Cboe’s VIX, the so-called fear/panic gauge, which indicates the 30-day implied volatility of the S&P 500 and rises during market panics as traders bid up options prices to hedge against declines in the index.

The BVIV does the same more often than not, rising during market panics as observed on Thursday.

“A wave of panic swept through crypto markets this week, correlated to a sharp risk-off move across various asset classes. Bitcoin’s 30-day implied volatility, as measured by the BVIV Index, surged from just over 40 to 95 in a matter of days, levels not seen since the infamous collapse of FTX at the end of 2022,” Cole Kennelly, founder and CEO of Volmex Labs, told CoinDesk in a Telegram chat.

Implied volatility is influenced by demand for options, or derivative contracts that help traders make asymmetrical gains from uptrends in the underlying asset and hedge downside risks. Call options are used to bet on the upside, while put options are typically bought as insurance against price drops.

On Thursday, traders scrambled to buy Deribit-listed options, especially puts, as bitcoin’s price tanked from $70,000 to nearly $60,000. The top five most traded options of the past 24 hours are all puts at strikes ranging from $70,000 to $20,000, according to data source Deribit Metrics. The $20,000 put represents a bet that prices will fall below that level.

“Volatility markets reacted sharply to last night’s price drop. Front-end volatility surged as dealers adjusted for gamma [near-term risks]. Short-dated vols led the surge, showing higher demand for protection, while longer-dated vols lagged, keeping the volatility curve steeply inverted,” Jimmy Yang, co-founder of institutional liquidity provider Orbit Markets, told CoinDesk.

Yang’s clients rushed to buy downside protection, fearing the price crash could devastate digital asset treasuries that bought bitcoin at higher levels. These firms could now liquidate at a loss, leading to a deeper slide in bitcoin’s price.

“With significant uncertainty still ahead — particularly around the DATs and the risk of further unwind cascades, we’ve seen a lot of client demand for downside protection,” he added.

Bitcoin’s price has bounced to over $64,000 at the time of writing, an over 5% recovery from overnight lows, according to CoinDesk data. Yang expects volatility to stabilize.

“Sentiment is deep in extreme fear, but bitcoin’s price seems to have found a base near $60K. If price action stabilizes, volatility looks stretched and could quickly pull back,” he said.

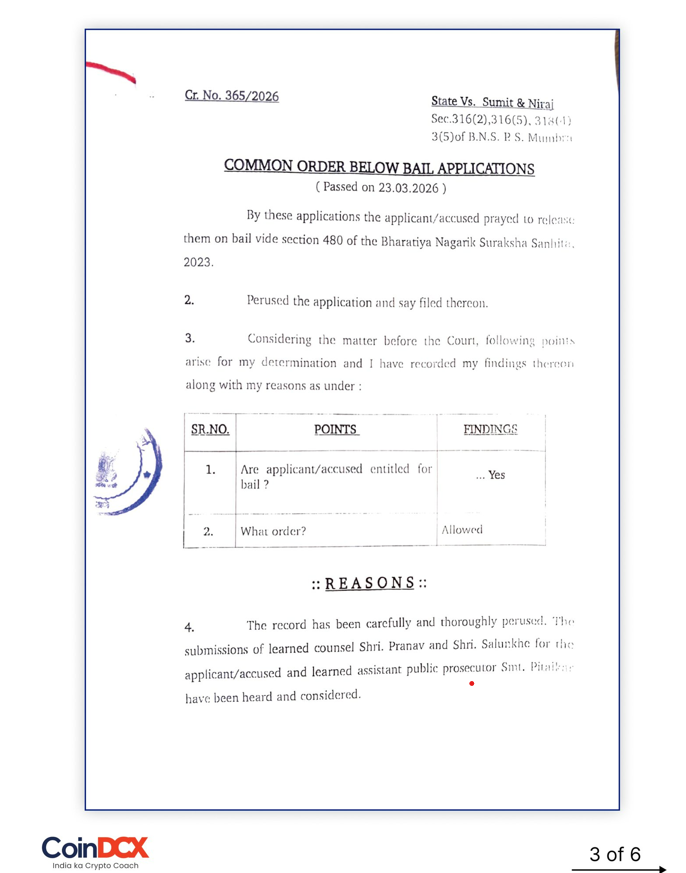

A magistrate court in Thane, India, has granted bail to CoinDCX co-founders Sumit Surendra Gupta and Niraj Ashok Khandelwal, ruling that no prima facie case was made out against them in a 71 lakh Indian rupees ($75,000) cheating complaint linked to a fake trading platform posing as the Indian crypto exchange.

The court’s common order on March 23 on their bail applications concluded that they were entitled to bail because no case was made out against them, even on an initial look at the available evidence. The founders were taken in for questioning on Saturday and remanded over the weekend after a complaint alleged they had duped an investor.

In the order, the magistrate recorded that the investigation officer had “no objection” to their release and that the applicants were not present in Mumbra when the alleged offence took place, adding that “some other person by representing as accused cheated the informant,” a fact the informant has admitted in court.

CoinDCX says bail order backs “third‑party impersonation”

In a March 24 statement on X, CoinDCX said the court proceedings supported a “third-party impersonation” scenario and that the fraud occurred on a lookalike site, coindcx.pro, which it said had no connection to the company.

The judge noted that the informant filed an affidavit stating that another accused, Rana, had repaid him the cheated amount and that the applicants are not the persons he met at a café in Kausa Mumbra where the fraudulent deal was struck.

With the matter “amicably settled” between the informant and the main accused, the court said there was no question of the founders tampering with evidence or witnesses.

Each was ordered released on bail upon executing a 50,000 Indian rupee bond (roughly $530) on condition that they cooperate with the investigation and trial.

Related: Hong Kong retiree loses $840K in triple ‘crypto expert’ scam

CoinDCX framed the episode as part of a broader rise in impersonation and phishing scams targeting well-known brands in India’s financial and crypto sectors, urging users to verify domains and only interact with the exchange’s official platform and social media profiles.

Prior scrutiny surrounding CoinDCX

Established in 2018 and headquartered in Mumbai, CoinDCX ranks among India’s most prominent cryptocurrency exchanges. The company reached an estimated valuation of around $2.45 billion following a funding round led by Coinbase Ventures in October 2025.

The platform has previously come under scrutiny for security concerns after a July 2025 incident in which hackers drained approximately $44 million from one of its internal operational accounts, although CoinDCX emphasized that no customer funds were compromised.

Magazine: Bitcoin may take 7 years to upgrade to post-quantum — BIP-360 co-author

SWIFT is building blockchain-based cross-border payment infrastructure with more than 40 global banks targeting a live scheme by mid-2026, and the plumbing it is laying quietly positions XRP crypto as an optional liquidity rail inside that network.

The mechanism is not a partnership announcement or a headline integration, it runs through Thunes, a payments company now embedded in SWIFT’s network, whose connections reach Ripple’s payment products and, by extension, XRP’s on-demand liquidity functions.

The market is watching because SWIFT’s blockchain push is no longer a pilot program. Bank of America, JPMorgan Chase, HSBC, Deutsche Bank, BNP Paribas, and Lloyds Bank are among the institutions involved. That is not a proof-of-concept roster. That is the institutional settlement stack deciding which rails to wire.

Key Takeaways:

- Settlement Context: SWIFT’s blockchain scheme, targeting an MVP in H1 2026 with 40-plus banks, completed ISO 20022 migration in November 2025 and has run successful trials involving USDC, tokenized deposits, and tokenized bonds.

- XRP Position: The SWIFT-Thunes integration gives more than 11,000 banks optional access to Ripple’s liquidity products, including XRP as a bridge asset — but participation is not mandated.

- Market Signal: Institutional infrastructure decisions like this create structural demand optionality for XRP, not guaranteed volume; the difference matters for how traders should frame this narrative.

How the SWIFT-Thunes-XRP Connection Actually Works

The mechanics are not theoretical. SWIFT completed its full migration to the ISO 20022 messaging standard on November 22, 2025, enabling richer, structured data flows that are prerequisite infrastructure for digital asset settlement.

That migration was the foundation. What is being built on top of it is a blockchain-enabled shared ledger scheme with enforceable rules on fees, FX rates, and traceability, with Chainlink providing interoperability between private and public blockchains while remaining ISO 20022 compliant.

The Thunes integration is where XRP enters the picture. SWIFT connects to Thunes’ pay-to-bank service, which now sits inside SWIFT’s network and links to more than 11,000 banks worldwide. Thunes can offer Ripple’s payment products. Those products can leverage XRP for on-demand liquidity, specifically as a bridge asset, eliminating the need for pre-funded nostro accounts in destination currencies.

The routing sequence: a company sends a payment via SWIFT; SWIFT routes through Thunes; Thunes offers access to Ripple’s ODL infrastructure; XRP settles the leg. No step in that chain forces a bank to use XRP. The optionality is built in, not mandated.

That optionality is structurally meaningful. SWIFT ran a successful trial with Citi using USDC in November 2025 and completed a proof-of-concept with HSBC and Ant International for tokenized deposit transfers the following month.

A January 2026 trial with BNP Paribas Securities Services, Intesa Sanpaolo, and Societe Generale FORGE settled tokenized bonds against fiat and digital payments. The institution is stress-testing every digital asset rail available — and XRP’s rail is now wired in.

What this unlocks is distribution at a scale XRP has not had access to through direct Ripple partnerships alone.

Why SWIFT’s Pivot Changes the Cross-Border Rail Debate

For years, the XRP settlement narrative rested on Ripple’s direct bank partnerships and regulatory outcomes. SWIFT’s blockchain pivot reframes the question entirely.

The debate is no longer whether banks will adopt blockchain for cross-border payments, SWIFT’s 40-bank scheme settles that. The debate is over which digital asset serves as the liquidity provider when payments require real-time currency bridging.

XRP is not alone in that race. Stablecoins are being integrated into regulated payment frameworks, and SWIFT’s own Citi trial demonstrated that USDC can perform settlement functions within the same infrastructure stack.

Chainlink’s interoperability role in SWIFT’s scheme also hints at a multi-asset settlement environment rather than a single-winner outcome.

— BSCN (@BSCNews) March 25, 2026

MASSIVE: $XRP JOINS OIL AND GOLD AS A MAJOR COMMODITY ASSET

MASSIVE: $XRP JOINS OIL AND GOLD AS A MAJOR COMMODITY ASSET

According to several sources interpreting recent statements by the SEC and CFTC, @Ripple's $XRP token is now deemed a digital commodity in the eyes of US regulators.$XRP is not the only asset to have claimed… pic.twitter.com/f7ZEXIAkSV

The infrastructure phase of cross-border payments is being decided now. Institutional players are wiring digital settlement rails into legacy systems across the board, and first-mover positioning inside those rails compounds. XRP’s advantage is that it is already connected. Its risk is that connected does not mean preferred.

The asset that becomes the default settlement infrastructure inside SWIFT’s network will not announce it. The volume data will.

The post SWIFT Blockchain Pivot Puts XRP Back in Cross-Border Spotlight appeared first on Cryptonews.

CoinDCX co-founders Sumit Surendra Gupta and Niraj Ashok Khandelwal have secured bail from a magistrate court in Thane, India, after a cheating complaint linked them to a fake platform that posed as the crypto exchange.

Summary

- CoinDCX founders received bail after the court found no prima facie case against them initially.

- The court said another person impersonated the accused and carried out the cheating scheme there.

- CoinDCX linked the complaint to a fake website and warned users about phishing risks.

Meanwhile, the court said no prima facie case was made out against them in the 71 lakh Indian rupees complaint and allowed their release on bond. The magistrate court issued a common order on March 23 on the bail applications filed by Gupta and Khandelwal. The order said the available material did not show a case against them, even at an initial stage.

The court also recorded that the investigation officer had “no objection” to their release. It added that the two founders were not present in Mumbra when the alleged offence took place, which weakened the complaint filed against them.

The case began after an investor claimed he had been cheated in a deal linked to CoinDCX. The founders were taken in for questioning on Saturday and remained in custody over the weekend before the court heard their bail plea.

During the hearing, the court noted that “some other person by representing as accused cheated the informant,” and said the informant had admitted that fact in court. This point became central to the bail order because it shifted focus away from the CoinDCX founders and toward other individuals tied to the alleged fraud.

In a March 24 statement posted on X, CoinDCX said the court process supported a “third-party impersonation” case. The company said the fraud took place through a lookalike website, coindcx.pro, which it said had no link to its official business.

The judge also referred to an affidavit filed by the informant. In that affidavit, the informant said another accused, Rana, had repaid the lost money and confirmed that the two CoinDCX founders were not the people he met at a café in Kausa Mumbra where the deal happened.

Bail conditions and fraud warning

The court said the matter had been “amicably settled” between the informant and the main accused. Based on that, it found no risk that the founders would interfere with witnesses or evidence if released.

Each founder was granted bail on a 50,000 Indian rupee bond. They must cooperate with the investigation and trial. CoinDCX later said the case reflects a wider rise in phishing and impersonation scams in India’s financial and crypto sectors, and urged users to verify website domains and use only official company channels.

BNB price surged back towards the $650 mark as futures traders aggressively positioned for further upside following a bullish prediction. After touching an intraday low of $627 on Sunday, the asset rebounded to $645, signaling a potential sentiment shift across the broader altcoin market.

The bounce coincides with a cooling of geopolitical tensions and a sharp decline in crude oil prices below $90. This macro relief has injected liquidity back into risk assets, pushing Bitcoin back above $71,000 and dragging major altcoins upward.

While the spot market shows recovery, the derivatives data paints a more aggressive picture; open interest for BNB futures has spiked 6.5% to $891 million in just 24 hours. The market is waking up.

This surge in leverage suggests institutional confidence is returning to the Binance ecosystem despite recent regulatory quiet periods. With bulls targeting a breakout, current price action hinges on reclaiming key resistance levels established earlier in the quarter.

Discover: The best pre-launch token sales

BNB Price Prediction: Can Open Interest Drive Prices to $690?

The technical structure and prediction for BNB price has shifted from consolidation to accumulation. Trading at $646 at the time of this analysis, the price action is respecting a multi-week ascending trendline that has served as dynamic support. As long as the token holds above the $630 floor, the path of least resistance appears upward.

Derivatives metrics provide the strongest bullish signal. Data from CoinGlass indicates a long/short ratio of 2.11 on Binance, meaning buyers are overwhelming sellers by more than two to one. This creates a high-pressure environment where a move past immediate resistance could trigger a short squeeze.

Analysts are eyeing the $690 level as the critical breakout point. A clean 4-hour close above this line could open the door for a rapid extension toward the $700-$720 range. Conversely, failure to hold the $639 7-day SMA would invalidate the immediate bullish thesis, potentially sending price action back toward $620 support.

Discover: The best crypto to diversify your portfolio with

Traders Rotate to L3 Infrastructure as Gains Consolidate

While BNB offers stability and consistent ecosystem growth, the sheer market capitalization of major L1s often limits the potential for exponential short-term multiples (can a $90B asset 10x overnight? Unlikely). Consequently, volume often rotates from established giants into emerging infrastructure plays during consolidation phases.

Smart money is increasingly tracking Layer 3 (L3) solutions that promise to unify fragmented liquidity. LiquidChain ($LIQUID) has emerged as a focal point in this narrative, positioning itself as the “Cross-Chain Liquidity Layer” capable of fusing Bitcoin, Ethereum, and Solana execution environments.

A new layer emerges. Only a few see it first. — LiquidChain (@getliquidchain) March 24, 2026

The future is LiquidChain  ⟁https://t.co/vqvBcdSj94 pic.twitter.com/R7ZeZ0NPGl

⟁https://t.co/vqvBcdSj94 pic.twitter.com/R7ZeZ0NPGl

The project distinguishes itself through a “Deploy-Once Architecture” and single-step execution, aiming to solve the user experience nightmare of bridging assets manually. The LiquidChain presale has already raised more than $600K, with early participants securing an entry price of $0.0143 with more than 1700% APY bonus. The contract is also audited by Certik, a benchmark in crypto safety.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Cryptocurrency investments are highly volatile and risky. Always do your own research.

The post BNB Price Prediction: Aggresive Spot Market and Bottlenecks appeared first on Cryptonews.

Siren price shot up 127% to $2.34 on Monday morning, becoming the best-performing crypto asset of the day.

Summary

- SIREN surged 127% to an intraday high of $2.34, driven by a sharp rise in futures demand, with open interest jumping nearly 120% to $121 million.

- The rally occurred without major fundamental updates, with derivatives positioning showing a bullish bias as the long-short ratio remained above 1.

- The token remains vulnerable to a reversal, with past price action showing a 70% drop from its peak amid concerns over high supply concentration among large holders.

According to data from CoinGecko, Siren (SIREN) price soared to an intraday high of $2.34 on Monday morning before stabilizing at $2.19 at the time of writing. Its market cap stood at $1.56 billion, making it the 50th largest crypto asset in the market.

While there was no particular news on development or ecosystem updates to account for SIREN’s rally today, it was likely linked with significant demand for the token in the futures market.

Notably, data from Coinglass show that SIREN futures open interest surged nearly 120% to $121 million over the past 24 hours. At the same time, the long/short ratio sat at over 1, a sign that more traders were going in with a bullish outlook.

While such rallies often spark excitement, it should be noted that they often face a deep retracement as investors rush to book in profits.

For instance, Siren previously rallied to an all-time high of $3.61 on March 22 after climbing up for several straight days owing to its rebrand into an autonomous AI agent on the BNB Chain and a successive perpetuals listing on multiple major crypto exchanges like Binance, Bybit, and MEXC. However, it came crashing down by over 70% from its peak after concerns about its supply concentration gained traction.

As reported by crypto.news earlier, on-chain data compiled by Bubblemaps revealed that nearly 50% of SIREN’s supply was held in one cluster. Subsequently, later reports revealed that the concentration could be as high as 88% of the total supply.

While the token has regained some momentum as seen by today’s surge, the token could be at risk of a reversal again should those large holders decide to sell off their positions.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Key Takeaways

- NTGR opened at $24.75 on Tuesday and traded near $25.15 — marking a 15.9% increase

- The FCC instituted restrictions on new consumer router models produced outside the United States due to security vulnerabilities

- Approximately 60% of U.S. routers are believed to originate from Chinese manufacturing facilities

- While NETGEAR produces devices abroad, the company may pursue Conditional Approval through the DoW or DHS to market new products domestically

- Stifel Nicolaus maintains a Buy recommendation on NTGR with a $36 target, suggesting potential upside exceeding 63%

Shares of NETGEAR experienced a remarkable Tuesday session, climbing almost 16% following the Federal Communications Commission’s declaration that it would restrict new consumer routers produced outside American borders. This policy shift created ripples throughout the networking industry and drove investors toward NTGR.

The regulatory agency cited escalating cyberattack incidents targeting American consumers and small enterprises since 2024 as justification for the restriction. The FCC highlighted vulnerabilities associated with internationally-manufactured routers, emphasizing that roughly 60% of U.S. routers originate from China.

The restriction applies exclusively to newly introduced router models. Products already carrying FCC authorization — regardless of their manufacturing origin — retain permission for domestic sales.

NETGEAR develops its technology within the United States but relies on international facilities for production. This business model means its upcoming products would technically fall within the ban’s scope. Nevertheless, the company maintains the option to pursue Conditional Approval through the Department of War or Department of Homeland Security, which would permit continued sales of foreign-manufactured routers domestically.

It bears mentioning that no major networking manufacturers currently produce consumer routers on American soil — placing NETGEAR in the same boat as its competitors.

Market enthusiasm for NTGR seemed rooted in two primary assumptions: international competitors will encounter heightened barriers to the U.S. market, and NETGEAR might ultimately relocate production domestically to circumvent the restriction altogether.

Tuesday’s advance followed a 5.85% gain during the prior session, indicating upward momentum had already begun developing before the FCC’s policy announcement.

Latest Financial Performance

NETGEAR’s latest quarterly earnings provided additional momentum for the stock. The company delivered earnings per share of $0.26, significantly surpassing the $0.05 consensus projection. Revenue reached $182.47 million, outperforming analyst expectations of $177.26 million.

Despite exceeding estimates, the overall financial health presents challenges. NETGEAR operates with a negative net margin of 2.56% and a P/E ratio of -41.24. Market watchers currently project full-year EPS of -1.84.

The stock’s 50-day moving average rests at $21.19, with the 200-day average positioned at $25.82. Tuesday’s closing price of $25.15 returned NTGR to proximity of its long-term average.

Wall Street Perspective

Analyst coverage for NTGR remains sparse. During the previous three months, Stifel Nicolaus analyst Tore Svanberg assigned a Buy rating with a $36 price target — indicating potential appreciation exceeding 63% from present levels.

The overall analyst consensus includes two Buy recommendations, one Hold rating, and one Sell rating, with a mean price target of $36.00. Zacks recently upgraded the security from “strong sell” to “hold” in early March, while Wall Street Zen reversed course, downgrading to “sell” at the month’s beginning.

Institutional stakeholders control approximately 82.97% of NTGR shares. Insider ownership represents 2.3%, though insider Pramod Badjate divested 3,000 shares in early February at $20.97 per share.

For the year-to-date period, NTGR continues trading down 10.07%, and has declined 11.05% across the trailing twelve months despite Tuesday’s substantial gain.

Vienna-based crypto broker Bitpanda is launching a new blockchain network aimed at bringing tokenized assets into Europe’s regulated financial system, as institutions look to move toward always-on markets.

The company said Wednesday that its “Vision Chain,” built with the Vision Web3 Foundation and Optimism , will provide infrastructure for banks and fintechs to issue and settle tokenized assets under EU rules such as MiCA and MiFID II.

The network uses compliant euro-denominated stablecoins for transaction fees to avoid the volatility tied to typical crypto payments on public chains. It also relies on Optimism’s Ethereum-based infrastructure to handle settlement and scaling.

The move comes as firms across global finance push deeper into tokenization to upgrade market plumbing for around-the-clock trading. The technology is widely seen as a way to streamline how assets are issued, traded and recorded, cutting reliance on fragmented legacy systems. It’s potentially a massive market: tokenized assets could grow 53% a year, reaching $18.9 trillion by 2033 across asset classes, a joint report by Boston Consulting Group and Ripple estimated.

The initiative reflects a wider race among financial firms. Rival digital broker Robinhood (HOOD) is currently testing its proprietary blockchain dubbed Robinhood Chain, built specifically for tokenized stocks trading and connecting to decentralized finance (DeFi) applications. Wall Street behemoths such as Nasdaq and NYSE also work on their blockchain platforms for tokenized securities, merging crypto rails with the same compliance and safeguards as for traditional systems.

Bitpanda’s chain fits into the firms broader strategy to bridge crypto rails and traditional finance, offering banks and financial institutions blockchain plumbing to provide digital asset services to their customers.

“Tokenization is expected to redefine capital markets,” Lukas Enzersdorfer-Konrad, CEO of Bitpanda, said in a statement. “European financial institutions have been ready for this shift for years, but the infrastructure has been missing.

“With Vision Chain, we are building a public blockchain designed around Europe’s regulatory standards, combining the openness of public networks with the reliability institutions require,” he added.

Read more: Crypto broker Bitpanda bets on banks and tokenization to expand globally ahead of IPO plans

Irish authorities said they have gained access to one Bitcoin wallet tied to convicted drug dealer Clifton Collins, years after the recovery phrase was believed lost.

Summary

- Irish authorities accessed a lost Bitcoin wallet tied to Clifton Collins with Europol’s technical support.

- The seized wallet held 500 Bitcoin and formed part of Collins’ larger 6,000 Bitcoin stash.

- Blockchain data showed the recovered wallet moved funds to Coinbase Prime after years of silence.

The wallet held 500 Bitcoin, and the seizure followed support from Europol’s European Cybercrime Centre.

Ireland’s Criminal Assets Bureau said on Tuesday that it had “gained access to and seized a cryptocurrency wallet” linked to an earlier criminal case. The bureau said the wallet contained 500 Bitcoin, valued at more than $35 million at current market prices.

The agency said Europol supported the operation through meetings in The Hague and by providing technical help. CAB said Europol offered “highly complex technical expertise and decryption resources vital to the success of the operation.” Authorities did not explain how they gained access to the wallet.

The Irish Times reported that the recovered wallet was one of 12 wallets once linked to Collins. Those wallets reportedly held a combined 6,000 Bitcoin bought in late 2011 and early 2012 using proceeds from a cannabis operation.

According to earlier reports, Collins stored the wallet keys on a single sheet of A4 paper. He hid that paper inside the aluminum cap of a fishing rod case kept at his rented home. The paper later went missing, and access to the Bitcoin was widely believed to be gone.

Moreover, blockchain intelligence platform Arkham labeled one wallet “Clifton Collins: Lost Keys.” On Tuesday, that wallet moved 500 Bitcoin to Coinbase Prime, more than a decade after the coins were first deposited.

Arkham also lists Collins as controlling 14 addresses with total holdings of about 5,500 Bitcoin. Based on current prices, those holdings are worth more than $391 million. Cointelegraph said it contacted CAB and An Garda Síochána for more details on the recovery.

Case dates back to Collins arrest in 2017

The Guardian reported that police arrested Collins in 2017 after searching his car and finding cannabis. He was later sentenced to five years in prison for growing and selling the drug.

After the arrest, Collins said the fishing rod case had been stolen before his landlord cleared out the rental property. Authorities, however, later lost access to the wallets after the printed codes disappeared. The newly seized 500 Bitcoin wallet now marks a rare case where law enforcement recovered access to funds once thought unreachable.

Crypto World

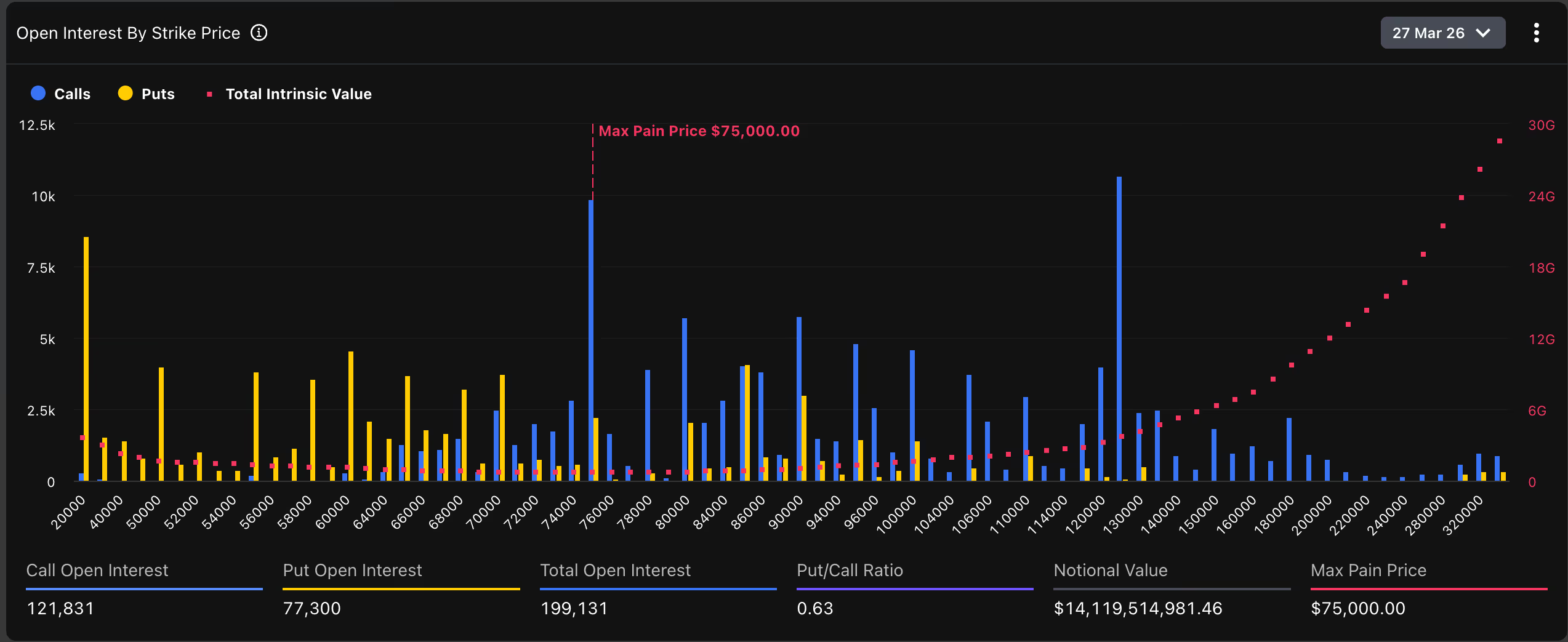

There’s a huge $14 billion bitcoin options expiry this Friday and it points to $75,000 as price magnet

On Friday, bitcoin options or derivative contracts worth billions will expire on crypto exchange Deribit. Traders might want to note that the dynamics of the expiry are such that BTC’s market price could be lifted toward a very specific point: $75,000.

Deribit, the world’s largest crypto options exchange, will settle bitcoin options contracts worth $14.16 billion on Friday at 08:00 UTC. This means nearly 40% of all open interest – the dollar value of all active contracts on the exchange – ware set to expire in roughly 48 hours. On Deribit, one options contract represents one BTC.

Options are contracts that let you bet on whether the price of an asset, such as BTC, will go up or down. A call option is a bet that the price will go up, and a put option is a bet that it will go down. Traders buy options to try to profit from price swings, or write (short) options to earn income while taking on the risk that prices move in favor of the buyer.

Here’s why the expiry matters

According to Deribit’s data, the ‘max pain’ price — the level where the most contracts would expire worthless (lottery tickets that don’t win) — sits right at $75,000.

As such, this level could act as a magnet, according to Deribit’s Chief Commerical Officer Jean-David Péquignot.

“With Bitcoin currently trading near $71k, the $75k Max Pain price represents a gravitational pull. Historically, this encourages delta-hedging by market makers that can drive prices toward the strike where the most options expire worthless,” Péquignot told CoinDesk.

Here’s how it works. As per the max pain theory, option writers — typically large funds, institutions, or market makers with ample capital — control or influence the spot price toward the pain point to limit payouts to buyers and thereby inflict maximum damage on them. This happens through normal trading in the spot or futures markets, rather than as a guaranteed manipulation.

This mechanical buying and selling often pulls the spot price closer to the max pain level, which is $75,000 in bitcoin’s case.

While max pain is well-known in traditional markets, its influence on crypto remains debated. Deribit, however, flags the level as a potential magnet. Adding to the intrigue, several analysts have identified $75,000 as key resistance, above which bitcoin could go into a full-bull mode.

Controlled expiry

Quarterly expiries typically spark massive position adjustments and hedging flows. Still, the impending expiry is likely unfold normally, without an outsized volatility surge.

That’s evident from the decline in the implied volatility index.

“Over the last sessions, we have witnessed an implied volatility (IV) compression, with both BTC and ETH DVOL dropping by ~6 points. This suggests the market is pricing in a controlled expiry rather than an immediate explosion in volatility,” Péquignot said.

He added that the market data suggests that traders aren’t chasing a breakout as geopolitical uncertainty in the form of Iran war lingers. He specifically pointed to call writing by institutions at higher strikes (levels above going spot price) as the evidence of measured bullish sentiment. Traders typically write overhead calls to collect premiums on top of their spot market holdings.

“The Put/Call ratio for Bitcoin options remains healthy (0.63), but the concentration of sell-side calls suggests a ceiling of institutional resistance as traders have been overwriting their positions to bank premium while waiting for the geopolitical clock to run out,” he noted.

All in all, the big expiry with $75,000 acting as a magnet comes at an intriguing juncture: bitcoin has held up remarkably well through the Iran war turbulence, maintaining strength even as equities wobble and energy markets remain fickle.

TLDR:

- Saudi Arabia lost $300 billion in stock market value within 25 days of Gulf conflict escalating regionally.

- Brent crude trading at $90–$110 per barrel turns infrastructure losses into net windfall revenue for Riyadh.

- Saudi’s Red Sea bypass pipeline positions the kingdom as the dominant exporter while Hormuz stays closed.

- MBS continues lobbying Washington for Iran strikes despite Iranian drones hitting Saudi refineries each night.

Saudi Arabia has lost $300 billion in stock market value across 25 days of Gulf conflict. The Tadawul index fell 12 percent in the opening week.

Iranian drone strikes shut down Ras Tanura, the kingdom’s largest refinery, which processes 550,000 barrels daily. Regional output losses reached 10 million barrels per day by March 12.

Despite this damage, Crown Prince Mohammed bin Salman continues pushing Washington for more action against Tehran. The kingdom now serves as the conflict’s victim, beneficiary, and accelerant at once.

Saudi Arabia Bears the Costs While Oil Revenue Climbs

Saudi Arabia’s Vision 2030 megaprojects are currently under formal government review. Capital outflows have risen, and investor confidence has declined sharply in recent weeks.

The Crown Prince spent a decade building the very infrastructure now absorbing nightly drone strikes. Eastern Province oil fields have also taken direct hits alongside the Ras Tanura shutdown.

Analyst Shanaka Anslem Perera described the situation on X with pointed directness. He wrote that Saudi Arabia is “simultaneously the war’s victim, its beneficiary, and its accelerant.”

Interceptor stockpiles defending Saudi airspace are drawing down at a steady pace. Each successful Iranian strike raises fresh questions about the kingdom’s long-term air defense capacity.

Meanwhile, Brent crude is trading between $90 and $110 per barrel on global markets. Saudi Arabia’s national budget was originally calculated on oil at $65 to $70 per barrel.

Every barrel sold above that level adds windfall revenue to the Saudi treasury. At $110 Brent, the kingdom earns a surplus on every barrel it can still export.

Goldman Sachs had forecast a widening fiscal gap before the conflict began. At $80 Brent, that deficit narrows to between 3 and 3.5 percent of GDP.

The war damaging Saudi refineries is simultaneously pushing oil prices well above budget assumptions. Both the losses and the gains appear on the same national balance sheet at once.

Saudi Arabia Gains Structural Ground as Hormuz Stays Contested

Saudi Arabia holds between 2 and 3 million barrels per day of spare production capacity. It also operates an East-West pipeline that bypasses the Strait of Hormuz entirely.

That pipeline routes crude directly to the Yanbu terminal on the Red Sea. Kuwait, Bahrain, and Qatar have no comparable alternative export infrastructure available.

Qatar’s Ras Laffan facility cannot be rebuilt or restored for at least five years. Saudi Arabia’s Red Sea route has become the most critical active export pipeline in the world.

The New York Times reported that MBS sees a “historic opportunity to remake the region.” Saudi Arabia’s Foreign Minister has also publicly stated that the kingdom’s patience is “not unlimited.”

MBS has called Trump multiple times, lobbying for continued military pressure on Iran. Each American strike generates fresh Iranian retaliation against Gulf energy infrastructure in response.

That retaliation pushes oil prices higher, which funds the next Saudi lobbying push in Washington. This cycle has no exit point while MBS continues treating the conflict as strategic opportunity.

Saudi Arabia is positioned to dominate the post-war energy market as regional rivals weaken. A diminished Iran cuts OPEC competition for Riyadh directly going forward.

Qatar’s delayed North Field expansion benefits Saudi gas over the medium term. Every producer dependent on Hormuz concedes further competitive ground to Saudi Arabia’s Red Sea route.

Financial Conflicts Lead to Domestic Violence

Manchester United reach agreement with Casemiro over contract clause amid transfer speculation

When will the cash Isa saving limits change?

-

Crypto World4 days ago

Crypto World4 days agoNIO (NIO) Stock Plunges 6.5% as Shelf Registration Sparks Dilution Worries

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Adidas – Corporette.com

-

Politics5 days ago

Politics5 days agoJenni Murray, Long-Serving Woman’s Hour Presenter, Dies Aged 75

-

Crypto World3 days ago

Crypto World3 days agoBest Crypto to Buy Now: Strategy Just Spent $1.57 Billion on Bitcoin During Fear While Early Investors Quietly Enter Pepeto for 150x Potential

-

News Videos7 days ago

News Videos7 days agoRBA board divided on rate cut, unusually buoyant share market | Finance Report | ABC NEWS

-

Crypto World3 days ago

Crypto World3 days agoBitcoin Price News: Bhutan Sells $72 Million in BTC Under Fiscal Pressure, but the Smart Money Entering Pepeto Sees What the Market Does Not

-

Tech5 days ago

Tech5 days agoinKONBINI Lets You Spend Summer Days Behind the Register

-

Crypto World7 days ago

Crypto World7 days agoCanada’s FINTRAC revokes registrations of 23 crypto MSBs in AML crackdown

-

Sports2 days ago

Sports2 days agoRemo Stars and Kano Pillars Strengthen Survival Hopes in NPFL

-

NewsBeat7 days ago

NewsBeat7 days agoResidents in North Lanarkshire reminded to register to vote in Scottish Parliament Election

-

News Videos7 days ago

News Videos7 days agoPARLIAMENT OF MALAWI – PAC MEETING WITH REGISTRAR OF FINANCIAL ON AMARYLLIS HOTEL – INQUIRY LIVE

-

Politics6 days ago

Politics6 days agoGender equality discussions at UN face pushbacks and US resistance

-

Business3 days ago

Business3 days agoNo Winner in March 21 Drawing as Prize Rolls to $133 Million for Next

-

Business7 days ago

Business7 days agoWho Was Alex Pretti? 5 Key Facts About the ICU Nurse Killed by Federal Agents in Minneapolis

-

Sports2 days ago

Sports2 days agoGary Kirsten Accuses Pakistan Cricket Board Of ‘Interference’, Mohsin Naqvi Responds

-

Tech3 days ago

Tech3 days agoGive Your Phone a Huge (and Free) Upgrade by Switching to Another Keyboard

-

Tech7 days ago

Tech7 days agoInventec’s bizarre VeilBook laptop hides its touchpad under a sliding keyboard just to give cooling fans a little breathing room

-

Sports5 days ago

Sports5 days ago2026 Kentucky Derby horses, odds, futures, preview, date: Expert who nailed 12 Derby-Oaks Doubles enters picks

-

Sports6 days ago

Vikings Free Agency Enters Phase 2 with Key Questions

-

News Videos6 days ago

News Videos6 days agoAmazing Cardboard Gadget That Turns Paper Into Money #techgadgets #ytshorts

You must be logged in to post a comment Login