Crypto World

BTC hashrate drops 12% in worst drawdown since China mining ban

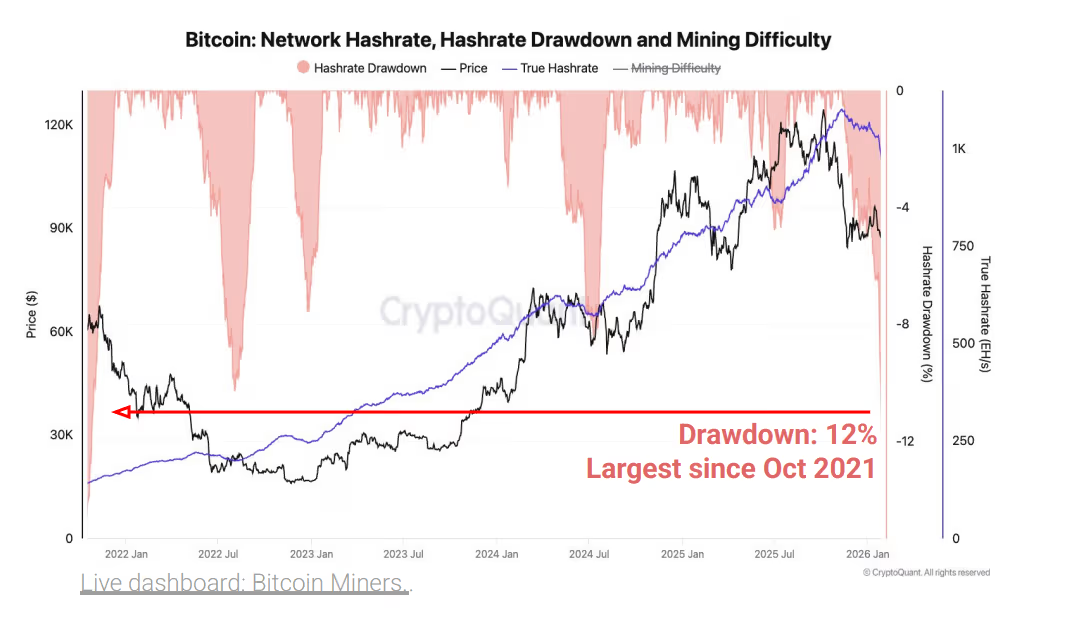

Bitcoin mining activity has taken its biggest hit since late 2021 after a severe winter storm in the United States forced several large mining firms to curtail operations, triggering a sharp drop in network hashrate, production and revenue.

Bitcoin’s total network hashrate has fallen about 12% since November 11, marking the largest drawdown since October 2021, when the network was still recovering from China’s sweeping mining ban.

The hashrate now sits near 970 exahashes per second, its lowest level since September 2025, according to CryptoQuant data.

The decline accelerated this week as extreme weather disrupted power supply across key US mining hubs.

Several publicly listed miners temporarily shut down machines to protect infrastructure and comply with grid curtailment requests, amplifying an already softening trend that began as bitcoin pulled back from its $126,000 all time high toward the $100,000 level late last year.

The hashrate shock quickly fed into miner economics. Daily bitcoin mining revenue dropped from roughly $45 million on January 22 to a yearly low of $28 million just two days later. While revenue has since rebounded modestly to around $34 million, it remains well below recent averages, reflecting both lower network activity and weaker bitcoin prices.

Production figures show an equally sharp contraction. Output from the largest publicly traded miners fell from 77 bitcoin per day to just 28 bitcoin over the same period. Production from other miners declined from 403 bitcoin to 209 bitcoin, bringing total network output down sharply.

On a 30-day rolling basis, publicly listed miners recorded a 48 bitcoin decline in production, the steepest since May 2024, shortly after the last halving. Output from non public miners dropped by 215 bitcoin, the largest fall since July 2024.

Profitability has also deteriorated, further pressuring the energy-intensive business.

CryptoQuant’s Miner Profit and Loss Sustainability Index has fallen to 21, its lowest reading since November 2024. The level signals that miners are operating in deeply stressed conditions, with revenues failing to cover costs for a growing share of the network despite multiple downward difficulty adjustments over recent epochs.

While difficulty has eased as machines went offline, the relief has not been enough to offset falling prices and operational disruptions. If hashrate remains suppressed, the network could see further difficulty cuts in coming weeks, offering some margin relief.

For now, the data points to one of the most challenging stretches for bitcoin miners since the post China ban reset more than four years ago.

The Open Network (TON) Foundation, a nonprofit organization supporting the development of TON Blockchain, is partnering with SCRYPT, Switzerland’s largest stablecoin infrastructure partner, to provide businesses with institutional-grade infrastructure to access USDT on TON Blockchain.

TON operates within one of the largest distribution networks in the world, reaching more than 1 billion users through its integration with Telegram. The network now supports over 50 million wallets and continues to see growing activity across payments, trading, and digital commerce.

TON Foundation has selected SCRYPT as its institutional infrastructure partner to meet the increasing demand of stablecoins as the settlement layer of choice for global payments, ecosystem distribution, and treasury operations, with USDT emerging as a high throughput, low cost rail for stablecoin payments. SCRYPT will provide execution, settlement, and fiat access in a move that helps TON Foundation further position TON Blockchain as a scalable alternative to existing settlement networks.

SCRYPT, the operating system for digital assets, enables banks, fintechs, payment providers, and corporate treasuries to access USDT on TON through a single, Swiss-licensed regulated platform. This includes near-instant cross-border settlement, fiat conversions, and fully compliant 24/7 on/off ramps. Combining deep liquidity, proprietary technology, and Swiss regulatory oversight, SCRYPT enables institutional clients to move, convert, and settle USDT flows on TON Blockchain at scale.

Nikola Plecas, VP of Payments at TON Foundation, commented:

“We’ve put payments innovation at the centre of our strategy for growth this year. We believe this is a key area in demonstrating how blockchain can power real-world financial infrastructure beyond tokenisation. [….]This partnership enables that next phase, bringing more and more institutions into the TON ecosystem and making the global movement of money ever more decentralised and seamless.”

Gabriel Titopoulos, MD, Markets & Trading at SCRYPT, added:

“Stablecoin rails are becoming the settlement layer for global payments. This partnership enables banks, payment operators, fintechs, and corporate treasuries to access stablecoins on TON with the trusted digital asset infrastructure partner, handling execution, settlement, custody and fiat conversions at institutional scale.”

About SCRYPT

The Operating System for Digital Assets.

SCRYPT is what institutions run on to trade, settle, store, and manage digital assets. Since 2019, SCRYPT has operated as the trusted crypto partner for firms launching or scaling their digital asset strategy.

By combining deep market access, crypto-native expertise, and proprietary infrastructure, SCRYPT provides the liquidity, full-stack infrastructure, and regulated framework that banks, asset managers, fintechs, and payment providers need to trade, store, and manage digital assets – all through a single point of access.

Built for Scale. Licensed to Deliver.

To learn more about SCRYPT, visit: www.scrypt.swiss

About TON

TON Foundation is a non-profit organisation accelerating the growth of TON Ecosystem by funding and supporting developers, creators, and businesses building on TON Blockchain. Founded in Switzerland in 2023, the Foundation brings together global expertise to advance protocol development, foster ecosystem growth, and drive adoption through grants, technical resources,

and strategic partnerships. While it advocates for TON’s mission, the Foundation does not control the network. TON is fully open-source, community-driven, and free from central control.

To learn more, visit www.ton.foundation

The post TON Partners with SCRYPT to Enable Institutional Access to Stablecoins appeared first on BeInCrypto.

Digital asset manager Grayscale backed accelerated efforts to make public blockchains quantum-resistant in a new research note arguing the technical solutions already exist but the harder challenge is getting decentralized communities to agree on implementing them.

“Public blockchains do not have CTOs; they are global communities governed by consensus,” wrote Zach Pandl, Grayscale’s head of research. “The potential threat to digital security from quantum therefore presents both a challenge and an opportunity.”

The note follows a week of intensive industry response to Google Quantum AI’s paper, which found that breaking bitcoin’s elliptic curve cryptography would require fewer than 500,000 physical qubits, roughly a 20-fold reduction from previous estimates, and could be executed in approximately nine minutes once the machine is primed.

CoinDesk’s analysis of the paper found that the attack gives an attacker a roughly 41% chance of stealing funds before a bitcoin transaction confirms.

Pandl highlighted four takeaways from the Google research that Grayscale found persuasive. Progress toward a cryptographically relevant quantum computer may come in “discrete jumps” rather than linearly, making timelines unpredictable.

The technical solutions, specifically post-quantum cryptography, are mature and already securing internet traffic and certain blockchain transactions. Quantum risk varies significantly across blockchains depending on their transaction model, consensus mechanism, and block time.

From a pure engineering standpoint, Pandl argued bitcoin has lower quantum risk than other chains because it uses a UTXO model, proof-of-work consensus, no native smart contracts, and certain address types that are not quantum-vulnerable if not reused after spending.

The harder question is what to do about the roughly 6.9 million BTC sitting in wallets where public keys are already permanently exposed on the blockchain, including an estimated 1 million believed to belong to pseudonymous creator Satoshi Nakamoto.

Binance co-founder Changpeng Zhao raised the same question last week, saying that if Satoshi’s coins move during a migration “it means he is still around, which is interesting to know,” and that if they don’t move “it might be better to lock or effectively burn those addresses.”

Grayscale frames the options similarly — burn them, do nothing, or deliberately slow their release by limiting the rate of spending from vulnerable addresses — but noted that the bitcoin community has a history of contentious debates over protocol changes, pointing to last year’s dispute around image data stored in blocks.

The contrast with Ethereum is worth noting.

CoinDesk reported last week that Google’s paper identified five separate attack vectors against Ethereum worth over $100 billion in combined exposure, spanning account keys, admin keys on stablecoins, smart contract code, consensus mechanisms, and data availability.

Ethereum Foundation researcher Justin Drake, who co-authored the Google paper, estimated at least a 10% chance of a quantum key recovery by 2032. The foundation has been staking aggressively, putting $93 million of ether into validators in a single day last week, but has not publicly addressed quantum migration timelines.

Former Biden economic advisers Ryan Cummings and Jared Bernstein would have you believe the decline in bitcoin’s price from its 2025 peak somehow vindicates their administration’s approach to cryptocurrency. A masterclass in selective memory, their February 26 New York Times opinion piece omits the most consequential fact about Biden-era crypto policy: it was not a reasoned regulatory framework.

The authors credit the Biden administration with “increasingly aggressive regulatory efforts to curb scams and fraud.” This framing is extraordinary, given what happened on their watch. FTX grew to enormous scale during the Biden administration. Sam Bankman-Fried was a top Democratic donor and met with senior administration officials (including then-Securities and Exchange Commission Chair Gary Gensler) while running what became one of the largest financial frauds in history.

The administration’s strategy of regulation-by-enforcement, rather than establishing clear rules, had a perverse effect: legitimate, compliance-minded companies were driven offshore or out of business, consumers were harmed, and American innovation was stifled. Meanwhile, bad actors like Bankman-Fried (who knew how to play political games) thrived in the confusion. When you refuse to write clear rules, the only people who benefit are those who never intended to follow them.

The authors conveniently ignore one of the most troubling episodes of the Biden era: “Operation Choke Point 2.0.” Under pressure from federal regulators, banks systematically debanked lawful crypto businesses, cutting them off from the financial system without due process, formal rulemaking, or legislative authority. The debanking campaign swept up ordinary individuals and small businesses who had turned to crypto because the traditional banking system had long underserved them. The Biden administration’s approach cut consumers off from tools they were using to participate in the financial system, without putting a single policy through the democratic process of notice-and-comment rulemaking.

The authors dismiss crypto as a “painfully slow and expensive database” with “almost no practical use.” They acknowledge in passing that crypto is used to wire money

internationally, but wave this away as though enabling fast, low-cost cross-border remittances for millions of people is a trivial achievement.

It is not. Global remittance fees average nearly 6.5%, costing migrant workers and their families billions of dollars each year. Stablecoins running on blockchain networks can execute the same transfers in minutes for a fraction of the cost. This is an immediate, material financial improvement for families in developing countries. The Biden economists sat in “dozens of meetings” and apparently came away unimpressed. One wonders whether they spoke to any of the people these tools serve.

Beyond remittances, blockchain technology underpins a rapidly growing ecosystem of financial applications. Fidelity, JPMorgan, BlackRock, BNY Mellon, Morgan Stanley, Visa, Mastercard, Meta, Stripe, Block Inc. and Franklin Templeton are actively building on blockchain infrastructure. The Biden economists’ claim that no “giant tech firms” are using this technology is flatly wrong.

The op-ed’s news hook is bitcoin’s price decline. Using short-term price movements to condemn an entire asset class is analytically unserious. Amazon’s stock fell 94 percent from its peak during the dotcom bust. By the Cummings-Bernstein standard, it should have been written off as “fundamentally worthless.” Volatility is a feature of nascent markets, not proof of worthlessness.

Moreover, it labels the Bitcoin network as “slow.” What it lacks in speed it makes up for in security – a quality that should be of the utmost importance to regulators. Outsiders or intermediaries cannot veto or reverse transactions between peers, unilaterally confiscate user funds, or tamper with its distributed ledger. That’s why it’s used worldwide in areas where regular citizens are targeted by their governments. Meanwhile, other blockchains enable payments at breakneck speed.

The authors repeatedly invoke the straw man of a taxpayer-funded bailout of the crypto industry. No serious policymaker (or crypto participant) has proposed anything of the sort. The stablecoin legislation Cummings and Bernstein reference creates fully reserved payment instruments that are overcollateralized with the most liquid government bonds on Earth. The Trump administration’s bitcoin reserve proposal involves no new taxpayer expenditure.

Meanwhile, when Silicon Valley Bank collapsed in 2023, the Biden administration authorized extraordinary measures to guarantee all deposits. Their concern about moral hazard was seemingly highly selective.

The op-ed devotes considerable space to crypto industry political donations, implying corruption. The suggestion that an industry advocating for favorable regulation through political participation is inherently corrupt would indict virtually every sector of the American economy. Denied a fair hearing by regulators, the crypto industry turned to the political process as a last resort – a cornerstone of American democracy. If political spending is problematic, the authors might start by examining their own side of the aisle during the Biden Administration, when Bankman-Fried overwhelmingly gave to Democrats.

The Biden administration had a historic opportunity to establish the United States as the global leader in digital asset regulation: to write clear, fair rules that would protect consumers while allowing innovation to flourish on American soil. Instead, it chose to weaponize the banking system against a legal industry, creating a lose-lose-lose for innovation, consumer protection and the U.S. crypto ecosystem.

Cummings and Bernstein write that crypto’s boosters “have run out of excuses.” On the contrary, it is the Biden administration’s crypto haters who owe the public an explanation.

Americans reported $11.4 billion in losses tied to cryptocurrency scams last year, 22% more than in 2024, highlighting the growing scale of digital asset fraud, an FBI report revealed Tuesday.

“Cryptocurrency investment scams are sophisticated long-term scams using psychological manipulation, the appearance of legitimacy, and exploitation of cryptocurrencies to deceive victims into investing large sums of money,” the report said.

The report also said that most crypto scams are perpetrated by organized criminal enterprises based in Southeast Asia that exploit victims of human trafficking as forced labor to run the operations.

Crypto analytics firm Chainalysis released a report in January revealing that as much as $17 billion in crypto was lost worldwide to scams and frauds in 2025. Impersonation, crypto exchange impostors and AI-generated scams against individuals were gradually surpassing losses to cyber-attacks as the leading methods criminals were using to steal digital assets, according to the Crypto Crime Report.

The FBI noted in its report that the number of victims increased significantly. In 2025, there were 181,565 complaints involving cryptocurrency, a 21% increase. The average damage per case was $62,604, highlighting how victims are often drawn into schemes that extract substantial amounts rather than small sums, the bureau said.

Losses are also heavily concentrated. Nearly 18,600 complainants each lost more than $100,000, suggesting many victims are losing life-changing amounts, including savings and retirement funds.

More broadly, crypto scams now sit at the center of a wider surge in online fraud. Americans filed more than 1 million cybercrime complaints in 2025, with losses exceeding $20.8 billion. Fraud and scams accounted for the overwhelming majority of those losses, reflecting what the FBI describes as a rapidly evolving threat landscape.

Security researcher Taylor Monahan claims North Korean IT workers have infiltrated more than 40 decentralized finance platforms, with the $280 million Drift Protocol exploit last week being the latest operation tied to the network.

Security researcher Taylor Monahan disclosed Sunday that North Korean agents have been embedded inside more than 40 decentralized finance platforms for nearly a decade. The claim connects the $280 million Drift Protocol exploit last week to a broader network of North Korean IT workers operating inside some of crypto’s largest projects. Monahan attributed the coordinated operations to what security researchers have linked to the Lazarus Group, a state-sponsored hacking organization.

The revelation indicates a sustained infiltration campaign targeting DeFi infrastructure rather than isolated attacks. According to NCC Group research cited in reporting on the matter, similar attack patterns have been attributed to North Korean threat actors operating against the crypto sector for more than a decade. The discovery raises questions about operational security practices across major DeFi protocols and the extent of undetected compromises within the ecosystem.

Sources: Taylor Monahan (@tayvano_) on X | Bitcoinist | NCC Group Research

This article was generated automatically by The Defiant’s AI news system from publicly available sources.

Crypto World

24 Hours Left: Here’s Why Ethereum & Bitcoin Cash Holders are Pivoting to BlockDAG Before April 8

Current markets are flashing contrasting signs. The Ethereum foundation recently locked away 15,000 ETH using specific, steady batches, a move signaling deep institutional faith rather than random noise. Meanwhile, Bitcoin Cash dipped over 6% following heavy whale selling, forcing Bitcoin Cash price prediction experts to frantically revise their support zones. Both events demand close attention.

However, no current market event rivals the opportunity BlockDAG (BDAG) is presenting for a few remaining days. With 300,000+ transactions finished, nearly 2 billion tokens committed to staking, and 100+ active smart contracts live, the momentum is undeniable.

A limited buying window at $0.000016 remains available even as the market value hits $0.40. This isn’t a mistake. This massive valuation gap is tangible, and it vanishes forever on April 8. No second chances exist.

Ethereum Foundation Commits 46M to Bolster Network Integrity

By staking 15,000 ETH in 32-ETH chunks, the Ethereum Foundation has initiated its biggest on-chain move yet. This $46.2 million shift turns stagnant treasury assets into active revenue for ecosystem development grants. Blockchain records reveal the funds originated from the “0xde0” address, which maintains over 270,000 ETH. This indicates a major pivot in how Ethereum manages its capital.

Recent Ethereum news emphasizes that staking fortifies the Beacon Chain, enhancing safety while creating consistent yield. By locking these assets, the foundation connects its own goals with those of the users and the protocol itself. Industry experts view this as high-level institutional involvement.

Analysts monitoring Ethereum news observe that these rhythmic, smaller transfers help mitigate operational hazards. Ultimately, this reflects the organization’s enduring dedication. Current Ethereum news suggests the network is entering a fresh era of expansion.

Bitcoin Cash Faces Volatility Following Major Whale Offloading

As a prominent Bitcoin fork, Bitcoin Cash (BCH) is recognized for swift transactions and minimal costs, functioning as a practical digital asset. Its worth relies on usage, rivalry, tech upgrades, laws, global economic shifts, and trader feelings. Experts frequently utilize Bitcoin Cash price prediction to estimate its growth path, weighing both optimistic and pessimistic market environments.

BCH recently slipped 6.19% to $452.76 after massive whale sales triggered forced liquidations. Even so, its efficiency and purpose keep it significant. Participants are tracking usage data and technical progress to refine their Bitcoin Cash price prediction.

Long-term outlooks evaluate the coin’s potential to hit new peaks, ensuring Bitcoin Cash price prediction remains a vital tool for active market participants.

Secure BlockDAG at $0.000016 Before the Window Slams Shut

Finding the best crypto to buy right now usually involves staring at charts and predicting the future. With BlockDAG, the existing infrastructure proves the point. Millions of blocks are finished. Over 300,000 transactions are done. More than 100 smart contracts are currently operational.

With nearly 2 billion tokens staked and weekly payouts active, this project isn’t asking for belief. It is providing proof, and buyers are flocking to that transparency.The followers created something functional before the valuation soared. Then, the price climbed.

That sequence is vital because it proves the core was solid before the crowd arrived. Real utility led the way, not speculation.The countdown has started. A special entry at $0.000016 is active, sitting significantly under the $0.40 exchange rate. This offer expires April 8.

After that, this price point disappears forever. The public market takes control, and anyone seeking BDAG after April 8 must pay the going rate. There is no middle ground.

A $1 price target is being widely discussed, and at $0.40, that goal seems logical given the established tech. At $0.000016, however, the potential is on another level. Early backers are holding assets that have already gained massive value. New exchange debuts are still pending. April 8 concludes this phase permanently. The only uncertainty is where you will stand once that deadline passes.

Final Thoughts

This week’s Ethereum news highlighted major institutional backing, while Bitcoin Cash price prediction models are being adjusted following significant whale-induced dips. Both stories remain essential for digital asset followers.

Then there is BlockDAG. The tech is ready and running. The users, the activity, and the rewards are established. None of this is just a theory anymore. The only remaining question is whether one takes action before April 8 or remains a spectator.

A $0.000016 price compared to a $0.40 market value is a rare opportunity that people often regret missing. This chance is still here, and it is real. April 8 is final. For those seeking the best crypto to buy right now, the ticking clock is the most persuasive factor.

Presale: https://purchase.blockdag.network

Website: https://blockdag.network

Telegram: https://t.me/blockDAGnetworkOfficial

Discord: https://discord.gg/Q7BxghMVyu

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

Crypto World

The era of easy money in crypto is over as DeFi yields are failing to compete with a simple savings account

Crypto investors who once turned to decentralized finance for easy passive income through juicy yields are running into a new reality: the numbers no longer add up.

DeFi, or onchain finance, is essentially conducting banking transactions on a blockchain, cutting out middlemen like banks and letting investors borrow, lend, and trade in minutes. Back in 2021-2022 (and even through the subsequent crypto winter), DeFi’s returns were more than promising; rates reached 20% on protocols like Aave and thousands of percent on other emerging protocols, which would justify parking some cash for high interest rates, albeit with a higher risk of hacks, exploits and quick liquidations.

Read more: What is DeFi?

Fast forward to 2026, Aave, the largest DeFi lending protocol by total value locked, is currently offering an APY of around 2.61% on USDC deposits. That sits below the 3.14% offered on idle cash at Interactive Brokers, one of the most popular traditional platforms among crypto-native investors. The gap may not seem huge on paper, but it undermines one of DeFi’s core theses: higher returns for higher risk. Instead, money sitting in DeFi is now facing a higher risk for lower returns.

“DeFi: earn 1% below T-bills and lose all your money one time per year,” wrote trader James Christoph on X on March 22.

That blunt take reflects a broader shift. For years, DeFi sold itself as a place where higher returns justified new kinds of risk. Today, that trade-off looks harder to defend.

Where the yield went

It was not always this way.

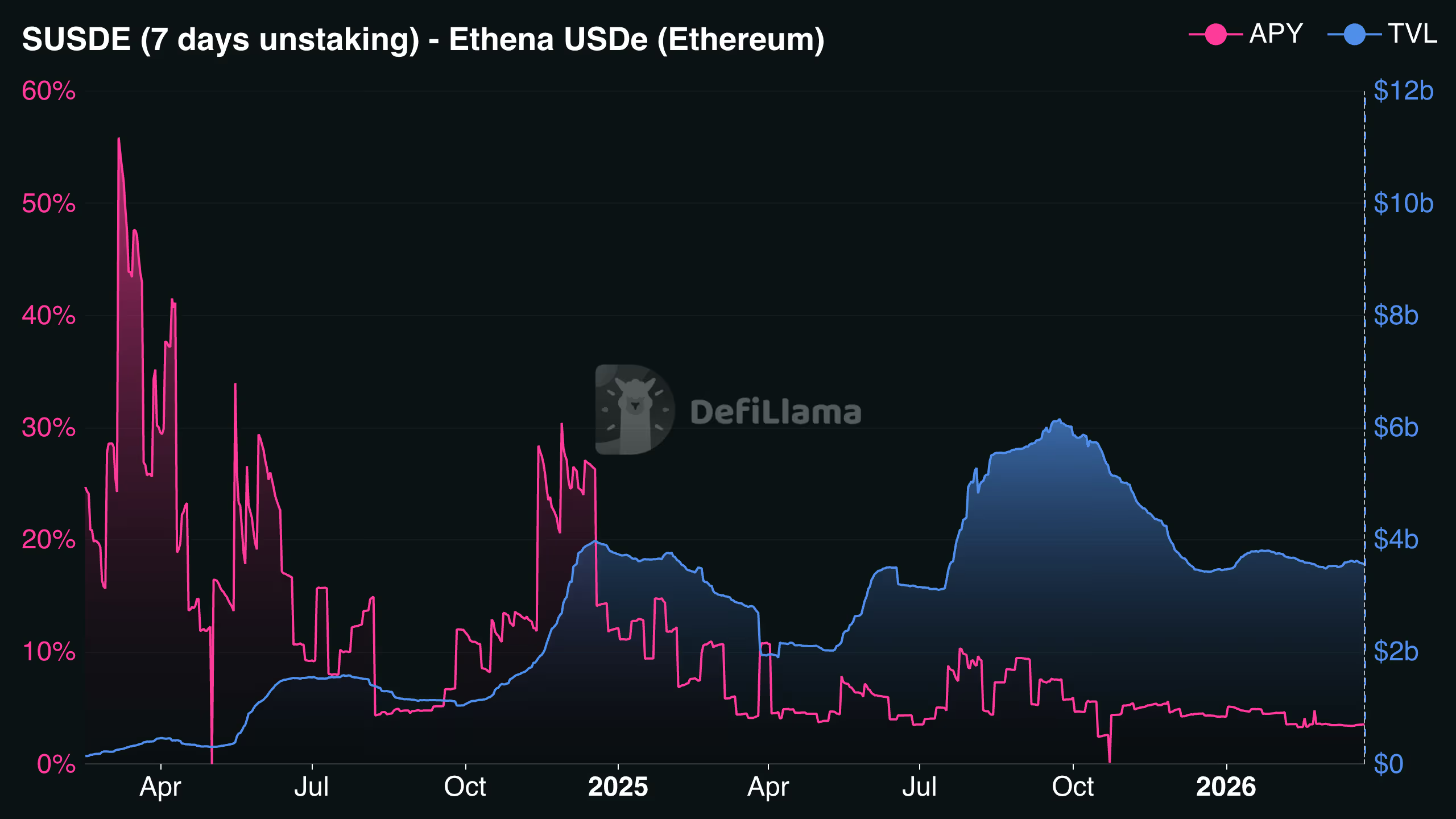

In 2024, DeFi yield looked genuinely competitive. Ethena — a protocol that issues a synthetic dollar stablecoin, USDe, backed by assets and hedged through derivatives positions — saw its sUSDe product offer more than 40% APY at its peak and pulled billions in deposits. But those returns were largely a product of ENA (Ethena’s native token) incentives and trading strategies that didn’t last.

Ethena’s APY has since compressed to around 3.5%, while its total value locked (TVL) has fallen from a peak of roughly $11 billion to $3.6 billion. Ethena didn’t immediately respond to the request for a comment by press time.

The CoinDesk Overnight Rate, which tracks daily borrowing costs across DeFi lending markets, tells the same story — spiking above 35% during the 2023 bull run before collapsing to roughly 3.5% today.

Across the rest of the stablecoin lending market, yields have followed a similar path lower.

Aave’s largest USDT pool yields 1.84%, while several other pools sit below 2%. The extra reward that once boosted returns have largely disappeared. What remains is organic yield driven by borrowing demand, and it is not strong enough to push yields higher.

Data from vaults.fyi shows how far things have fallen. Aave’s two largest stablecoin pools — USDT and USDC on Ethereum — are yielding just over 2% on a combined $8.5 billion in deposits. Lido’s stETH, the largest pool, returns 2.53%, while Ethena’s staked USDe has fallen to 3.47%.

Only a handful of protocols are still beating Interactive Brokers’ 3.14% rates. These are largely private credit products or strategies tied to real-world assets such as Sky’s USDS Savings rate of 3.75%, which has emerged as one of the more attractive refuges in this environment, sitting above the Aave average and drawing $6.5 billion in deposits.

But the rate comes with a caveat: around 70% of Sky’s income derives from offchain sources, including U.S. Treasury products, institutional credit lines, and Coinbase USDC rewards. For investors who came to DeFi specifically to avoid that kind of exposure, the distinction matters.

Aave does still offer more competitive rates on select stablecoins beyond its flagship USDC pool. Its sGHO product currently yields 5.13%, while other options of V3 Core Ethereum include USDG at 5.9%, RLUSD AT 4.4% AND USDTB AT 4.0%. But these sit outside the headline figures that most comparisons focus on.

Paul Frambot, co-founder of Morpho, a lending infrastructure protocol, says this bleak outcome for yields was inevitable.

“Undifferentiated lending converges toward risk-free rates because when every depositor shares the same collateral, the same parameters, and the same outcome, there is limited room for specialization and returns compress,” he told CoinDesk.

Morpho, with over $10 billion in deposits, offers a different model. Its platform lets curators build lending vaults – essentially customized pools with their own risk parameters, collateral choices and yield strategies, managed by specialist teams rather than governed by a single set of rules. Some of these curated vault models can still generate relatively higher yields. Its Steakhouse Prime USDC and Gauntlet USDC Prime vaults are both yielding 3.64%, while one vault, Sentora’s PYUSD offering, is at 6.48%.

Frambot says the difference comes down to how risk is managed. “What makes the vault and curator model different is that it externalizes risk curation and opens it up to real competition,” he said. “That creates an open marketplace for yield, where returns are driven by the quality and differentiation of strategies rather than liquidity alone. That is also why bluechip stablecoin yields on Morpho are on average higher than in pooled models and backed by straightforward collateral like BTC and ETH.”

Still, the yields are nowhere near what they were in previous years.

Aave frames the current weakness as cyclical rather than structural. The protocol points to unusually depressed crypto sentiment – with the Fear and Greed Index below its 2022 lows – as a key driver of reduced borrowing demand, which in turn weighs on deposit rates. “Stablecoin rates on Aave have largely tracked leverage demand,” a spokesperson told CoinDesk. “We do not see them as structurally lower going forward.”

The company also notes that its weighted-average stablecoin deposit yield over the past year has still beaten Interactive Brokers’ top offering, meaning depositors who entered before 2025 would still be ahead today.

‘Really dark’

Lower yields, though, are only part of the story. Confidence across DeFi has also taken a hit.

Balancer Labs, once one of the most recognizable names in decentralized exchange infrastructure, has recently shut down after a $110 million exploit. Governance tokens across the sector are trading at low valuations. For many, it feels like energy has been drained out of the space.

Jai Bhavnani, a prominent DeFi investor, wrote on X that the space is feeling “really dark,” describing the combination of yield compression, protocol shutdowns, and recent exploits as a perfect storm.

“LPs are realizing most protocols are too much risk too little reward,” he wrote. “There is no catalyst on the horizon to change things.”

Some in the same thread pushed back, arguing that market downturns tend to flush out the weakest projects and leave behind only those protocols that can genuinely sustain themselves. This counterpoint has historical precedent; DeFi has survived prior cycles and emerged with more resilient infrastructure. That may be true, but it offers little comfort to investors sitting on compressed returns today.

Then there is smart contract risk, or more precisely, the growing range of risks that smart contract audits cannot catch.

Last month, Resolv, a yield-bearing stablecoin protocol, was exploited for roughly $25 million. An attacker deposited 100,000 USDC into the protocol’s minting contract and received 50 million USR in return, roughly 500 times the expected amount. The issue was not a flaw in the smart contract code itself. Instead, the system lacked basic safeguards such as oracle checks and minting limits.

The protocol now holds $113 million in assets against $173 million in liabilities. USR is trading at $0.13, having lost its $1.00 peg and continuing to tumble into the end of March.

The Resolv hack sits within a broader pattern. Hackers stole more than $2.47 billion worth of cryptocurrency in the first half of 2025 alone, already exceeding all of 2024, according to CertiK’s Hack3d report. Wallet compromises accounted for $1.7 billion of that total. Immunefi CEO Mitchell Amador told CoinDesk earlier this year that onchain code is actually getting harder to exploit, but that attackers are adapting, pivoting to operational failures, stolen keys, and social engineering instead. For example, the more recent $270 million exploit on Drift protocol was part of a social engineering program by North Korea.

For investors weighing up a 2%-3% yield on DeFi against 3.14% at a traditional brokerage, that context is hard to ignore. The extra return that once justified the exposure has largely disappeared.

But the deposit rate comparison only tells part of the story. An Aave spokesperson said: “For borrowers and margin traders, Aave offers much more competitive rates than IBKR — currently 3.2% on Aave vs. up to 6.14% on IBKR. Borrowers on Aave also benefit because their collateral continues to earn yield, further reducing effective borrowing costs compared to IBKR.”

Regulatory ‘Clarity’

On top of compressed yields and persistent security risks, DeFi is now facing a regulatory threat targeting its yield model.

The Digital Asset Market Clarity Act, the crypto industry’s most significant pending legislation, includes a provision that would ban passive stablecoin yield earned simply for holding a dollar-pegged token. That would mean rewards tied to activity, such as payments or transfers, would still be allowed, although the distinction remains unclear. Something that crypto industry insiders who reviewed the draft described to CoinDesk as “overly narrow and unclear.”

Recently, 10x Research’s Markus Thielen said that if the Clarity Act is passed, it could re-centralize yield into traditional finance and regulated products, creating a headwind for DeFi.

Bottom line: the DeFi provisions of the bill remain unresolved, with several Senate Democrats citing concerns about illicit finance. But the direction of travel on yield is clear enough: at a moment when DeFi returns are already struggling to justify the risk, Washington is potentially moving to narrow the options further.

That leaves DeFi in a tight spot. Yields are down. Risks remain. And new rules could limit what returns are left.

For now, the math that once drew investors in is looking much less convincing.

Read more: How North Korea’s 6-month-long secret espionage program has crypto community rethinking security

Ether treasury managers are increasingly looking beyond straightforward staking rewards to extract higher yields, with liquid staking and other active deployment strategies moving into the mainstream playbook. Speaking at ETHCC 2026, Kean Gilbert, head of institutional relations at Lido Finance, highlighted liquid staking as a pathway for treasuries to earn extra returns while maintaining exposure to ETH staking benefits.

In the United States, listed staking products for Ether have proliferated, and public disclosures show treasuries experimenting with a blend of staking approaches. The current landscape includes several exchange-traded or registered products that package staked ETH into visible yields, alongside native staking options. As investors compare these vehicles, the underlying economics remain uneven, with different structures and fees complicating apples-to-apples judgments about potential returns.

Key takeaways

- Liquid staking offers a transferable token that can be deployed elsewhere in DeFi while ETH remains staked, enabling yield-enhancing strategies beyond simple staking rewards.

- Treasury managers are weighing active deployment methods—such as posting ETH as collateral and borrowing against it—as potential sources of higher return relative to passive staking vehicles.

- Public filings show real-world adoption of liquid-staking alongside native staking, with companies reporting notable portions of rewards attributable to liquid-staking activity.

- The U.S. ETF landscape for staked ETH has grown, but reported yields vary across products, and several datasets indicate that direct yield comparisons are not straightforward.

- Analysts emphasize that actively managed treasury strategies offer potential premium through dynamic deployment, even if headline yields on ETFs don’t directly mirror on-chain staking rewards.

Active yield and the logic of liquid staking

Liquid staking, at its core, allows Ether holders to stake their assets while receiving a tradeable token representing their staked position. That token can be used across DeFi protocols, giving treasuries a path to generate additional yield without surrendering staking exposure. At ETHCC 2026, Gilbert framed liquid staking as a viable mechanism for treasury desks to pursue incremental returns by layering on additional strategies on top of the basic staking rewards.

Beyond simply staking, some treasury operations are considering using ETH as collateral to borrow against it, enabling a form of leverage that could boost overall yield if managed prudently. In practice, this means treasuries may activate a range of DeFi primitives—collateralized loans, liquidity provision, and cross- protocol basis trading—to capture returns that passive staked ETH products alone cannot deliver.

“A staked ETH ETF is a passive vehicle. A DAT trading at a meaningful mNAV premium is promising something a passive ETF structurally cannot deliver, which is active, dynamic deployment of spot inventory across opportunities as they arise.”

That perspective comes from Jimmy Xue, co-founder and chief operating officer of Axis, a quantitative yield platform. He adds that the premium reflected in a mutualized treasury’s market value—often described as a market net asset value or mNAV premium—signals investor confidence in a manager’s ability to deploy a treasurer’s ETH treasury across opportunities as they emerge. In his view, basis trading and related strategies can be major yield sources for treasury-oriented products, helping to bridge the gap between simple staking rewards and the full spectrum of deployed yields.

Yield figures and the ETF contrast

The current U.S. ETF lineup for staked Ether includes a set of products that publicly disclose staking economics, but direct comparisons to on-chain staking returns are not straightforward. Among notable offerings are:

- REX-Osprey ETH + Staking ETF, which launched in September 2025.

- Grayscale’s Ethereum Staking ETF and Ethereum Staking Mini ETF.

- BlackRock’s iShares Staked Ethereum Trust ETF, introduced on March 12.

Issuer disclosures reveal varying fee structures and payout assumptions, which complicates simple yield comparisons. For example, Grayscale’s Ethereum Trust pages show net staking rewards around 2.26% as of April 6, while Grayscale’s ETH Staking product page lists about 2.56% as of April 2. By contrast, on-chain native ETH staking yields have hovered around 2.7% to 2.8% per year according to data from Staking Rewards. The discrepancy underscores how ETF mechanics—management fees, hedges, and the timing of reward accrual—shape reported yields even when the underlying staking economics are similar.

As Xue noted, the real value proposition of an actively managed treasury is not simply the headline yield but the ability to deploy capital from spot inventory across opportunities as they arise. This view aligns with the broader market trend of treasury desks seeking to convert passive staking into diversified, yield-enhancing activity through liquid staking and related strategies.

Glass‑door into real-world adoption: Sharplink and BTCS

Public disclosures provide a rare window into how Ether treasuries are actually deploying liquid-staking strategies. Sharplink Gaming, the second-largest Ether holder by reported holdings, disclosed that it had staked 14,516 ETH as of March, generating roughly 30.8 million dollars in staking rewards. Of those rewards, about one-third were attributed to liquid staking, with the remaining two-thirds stemming from native staking, according to a March 1 filing with the U.S. Securities and Exchange Commission. It’s worth noting that Sharplink’s broader 2025 results showed a material net loss—about $734 million—driven by the downturn in the crypto market during the year’s latter half. The filing provides a tangible backdrop to the tension between mark-to-market losses and staking yield, a dynamic that treasury desks must manage in real time.

BTCS Inc., ranked among the larger Ether treasuries by returns, has also integrated liquid staking into its program. The company holds 29,122 ETH and has liquid-staked 4,160 ETH through Rocket Pool nodes, a figure disclosed in a July 2025 SEC filing. That mix illustrates how treasuries blend native staking with liquid staking to diversify revenue streams and preserve liquidity while maintaining exposure to Ether’s yield potential.

Market observers have approached these disclosures with caution, recognizing that each firm’s structure—and the data they publish—reflects unique risk profiles, governance practices, and fee frameworks. Yet the trend is clear: treasury operations are increasingly reporting and quantifying liquid-staking activity as a meaningful component of total yield generation, rather than treating it as a separate, marginal strategy.

Where the space goes from here

As more Ether treasury players disclose their strategies, the debate over what constitutes the best approach will intensify. The ETF route provides visibility and regulatory clarity for investors seeking traditional, paper-traded exposure to staked ETH; liquid staking and other active yield methods offer potential upside through more dynamic management, albeit with higher complexity and counterparty considerations. The field is at a point where the lines between passive exposure and active treasury management are increasingly blurred, and investors are paying attention to who can consistently convert ETH into productive capital deployments.

ETHCC 2026 underscored that the conversation around liquid staking is transitioning from niche experimentation to a standard item on treasuries’ flight plans. For many market participants, the critical question is not only whether liquid staking can outperform passive staking on a headline basis but whether treasury managers can reliably manage risk and liquidity while pursuing higher, more diversified yields.

Looking ahead, investors and builders should watch several developments: the pace at which more treasuries disclose liquid-staking activity; how ETF providers adjust for complexities in yield reporting and fee structures; and how risk management frameworks evolve as treasuries deploy capital across collateralized and leverage-based strategies. If the past year offers a guide, the next chapter of Ether treasury management will hinge on transparent disclosures, prudent risk-taking, and the ability to translate sophisticated yield engineering into durable, risk-adjusted returns.

As the market weighs these approaches, one certainty remains: the sophistication of Ether treasuries is rising, and liquid staking is no longer a niche feature but a core instrument in the ongoing quest to turn ETH in all its forms into productive capital.

Bitcoin (BTC) remains below $70,000 on Tuesday as traders weigh conflicting signals from a dramatic Trump ultimatum on Iran against reports of positive ceasefire talks.

An 8 PM ET deadline set by President Trump for Iran to reopen the Strait of Hormuz has turned Tuesday into a binary event for risk assets.

War Signals Pull BTC in Both Directions

Vice President JD Vance said Tuesday that the war would conclude “very shortly” and that military objectives had been completed.

Meanwhile, a senior U.S. official reportedly told Fox News that Washington is in direct contact with Tehran, describing the talks as “positive” with a possible breakthrough by the end of the day.

However, Trump posted a starkly different tone on Truth Social. He warned that “a whole civilization will die tonight” while claiming “Complete and Total Regime Change” had occurred.

“A whole civilization will die tonight, never to be brought back again. I don’t want that to happen, but it probably will… We will find out tonight, one of the most important moments in the long and complex history of the World,” said Trump.

The post referenced 47 years since Iran’s 1979 Islamic Revolution.

Former White House Communications Director Anthony Scaramucci called the statement a veiled nuclear strike threat.

Skeptics vs. Hawks Frame a Binary Trade

Not everyone reads Trump’s rhetoric at face value. Macro commentator Rational Aussie argued that the escalating language signals weak leverage, not genuine intent.

They predicted Trump would extend the deadline overnight and markets would rally on the reversal, a pattern traders have labeled “TACO Tuesday” for “Trump Always Chickens Out.”

“Trump will Taco…his rhetoric gets increasingly deranged when the worst things are going for him – that’s how he negotiates. He has to make everyone believe he has genuinely lost the plot…He’s trying to create leverage that doesn’t exist by artificially creating what is most scarce: fear of consequence. I fully expect to wake up 8 hours from now to a headline something along the lines of ‘we were so close to giving the orders,” they wrote.

Meanwhile, Iran is not backing down quietly. A senior Iranian source reportedly said that if the situation spirals out of control, Tehran’s allies would close the Bab el-Mandeb waterway.

That Red Sea chokepoint handles a significant share of Europe-bound shipping and is already vulnerable to Houthi disruption.

The Strait of Hormuz closure has already removed roughly 20% of global oil supply from the market, pushing Brent crude above $110 per barrel.

A simultaneous Bab el-Mandeb shutdown would compound that shock across energy, fertilizer, and shipping costs.

What Comes Next for BTC

Bitcoin opened Tuesday at $68,860, down 0.2% from Monday. It briefly touched $68,200 before recovering and was trading for $68,392 as of this writing.

The Fear and Greed Index remains deep in extreme fear territory, where it has stayed for over a month.

- If the deadline passes without escalation, the “TACO” thesis holds, and a relief rally becomes likely.

- If strikes on civilian infrastructure proceed, further selling pressure and liquidation cascades could push BTC toward the $66,000 support zone tested last week.

Traders have a few hours left to find out which version of tonight they get.

The post Trump’s Ultimatum Splits Markets Between Nuclear Fear and “TACO Tuesday” appeared first on BeInCrypto.

Crypto World

Swift Advances Dual-Track Strategy for Faster Cross-Border Payments and Tokenized Value

TLDR:

- Swift introduces a dual-track model combining its payment scheme with a blockchain-based shared ledger system

- The framework supports real-time cross-border payments and regulated tokenised value movement across networks

- Major banks like BBVA, BNP Paribas, CaixaBank, and Citi are backing the new retail payments framework

- The system connects over 11,500 institutions, enabling scalable and secure global transaction processing

Swift has outlined a dual-track strategy to reshape cross-border payments, combining its existing infrastructure with a blockchain-based shared ledger.

The approach focuses on improving speed, accessibility, and interoperability while maintaining trusted connections across its global financial network.

A dual-track strategy for modern payments

A recent post shared by Swift on X introduced its evolving payments framework and direction. The message framed the future of payments as a coordinated system rather than a single solution. It described how Swift is building on its established network while adding new digital capabilities.

The first component of this strategy centers on Swift’s payments scheme. This system is designed to deliver faster and more efficient cross-border transactions.

It supports financial institutions that rely on secure and standardized messaging across international markets. As a result, banks can process transactions with reduced friction and improved consistency.

At the same time, Swift is working on a blockchain-based shared ledger. This second track focuses on enabling continuous, real-time payment processing across borders.

The system is also structured to support regulated tokenised assets, which are becoming more relevant in financial markets.

The combination of these two systems creates a parallel structure. Each track addresses different needs while remaining connected.

Traditional payment flows continue to operate, while newer digital rails expand capabilities. This approach allows institutions to adopt innovation without disrupting existing operations.

Swift’s network already connects over 11,500 financial institutions across more than 200 countries and territories. Therefore, any enhancement to its system has a wide reach.

By integrating both traditional and blockchain-based systems, Swift aims to support a broader range of payment use cases.

Banks support framework for retail transactions

Several global banks have joined Swift in supporting the rollout of its updated payments framework. These include BBVA, BNP Paribas, CaixaBank, and Citi. Their participation reflects early adoption of the system in real-world banking environments.

The framework focuses on improving retail transactions, especially cross-border consumer payments. These payments often face delays and higher processing costs. Swift’s updated model aims to address these issues by improving speed and reliability.

Through the payments scheme, banks can continue using familiar systems while gaining efficiency. Meanwhile, the shared ledger introduces new options for processing value instantly. This is particularly relevant for tokenised assets that require constant availability.

The integration of both systems allows financial institutions to test and expand new services. Banks can gradually adopt blockchain-based features while maintaining operational stability. This phased approach reduces risk while encouraging innovation.

Swift’s announcement also pointed users to further details through its official website. The shared post emphasized how both tracks work together rather than compete. It framed the development as a step toward a more connected and flexible financial system.

As global payments evolve, financial institutions continue to explore ways to improve transaction speed and transparency.

Swift’s dual approach reflects this shift by combining established infrastructure with emerging technologies. The framework is structured to support both current needs and future developments in cross-border finance.

The rollout of this model is ongoing, with participating banks playing a key role in implementation. As adoption expands, the system is expected to handle a wider range of payment types. This includes both traditional transfers and digital asset-based transactions.

Swift’s strategy shows how financial networks are adapting to changing demands. By aligning multiple technologies, the organization is positioning its network to handle diverse payment flows in a connected manner.

Jannik Sinner & Carlos Alcaraz open clay-court seasons with Monte Carlo Masters wins

New Revelations Reignite Crypto Scandal Involving Argentina’s President Milei

Russia and China block reopening of Strait of Hormuz – hours before Trump deadline

-

NewsBeat5 days ago

NewsBeat5 days agoSteven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Business5 days ago

Business5 days agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Spanx – Corporette.com

-

Crypto World6 days ago

Crypto World6 days agoGold Price Prediction: Worst Month in 17 Years fo Save Haven Rock

-

Business2 days ago

Business2 days agoThree Gulf funds agree to back Paramount’s $81 billion takeover of Warner, WSJ reports

-

Business3 days ago

Business3 days agoExpert Picks for Every Need

-

Sports3 days ago

Sports3 days agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Business6 days ago

Business6 days agoLogin and Checkout Issues Spark Merchant Frustration

-

Crypto World7 days ago

Crypto World7 days agoBitcoin enters the public bond market as Moody’s gives a first-of-its-kind crypto deal a rating

-

Crypto World7 days ago

Bitcoin stalls below key resistance as technical signals skew bearish

-

Tech5 days ago

Tech5 days agoCommonwealth Fusion Systems leans on magnets for near-term revenue

-

Business2 days ago

No Jackpot Winner, Prize to Climb to $231 Million

-

Politics7 days ago

Politics7 days agoStarmer’s centre has collapsed, and the left was right all along

-

Crypto World6 days ago

Crypto World6 days agoRipple rolls out enterprise crypto treasury platform for corporates

-

Fashion1 day ago

Fashion1 day agoMassimo Dutti Offers Inspiration for Your Summer Mood Board

-

Crypto World7 days ago

AI Memory Rout Wipes 9% Off Nvidia Stock: Chart Says More Pain Ahead

-

Crypto World6 days ago

Crypto World6 days agoWhy It’s Partnering, Not Issuing

-

Sports7 days ago

Sports7 days agoHow to teach yourself the perfect impact position with every club

-

Tech7 days ago

Tech7 days agoSolo Leveling: Ranking All Sung Jinwoo Shadows by Power

-

Sports6 days ago

Tom Pelissero Drives the Final Nail in the Coffin

You must be logged in to post a comment Login