Crypto World

: Crypto Week Ahead

The brief, partial U.S. government shutdown put paid to the Employment Situation report that was due Friday; it’s coming this week instead. Look for the bellwether nonfarm payrolls report on Wednesday. The world’s largest economy is forecast to have created 70,000 jobs last month, more than in December, while the unemployment rate is expected to hold steady at 4.4%.

The week also includes earnings from some of the biggest, highest-profile crypto companies, including crypto exchange Coinbase (COIN). Robinhood (HOOD), a trading platform that covers equities as well as crypto, is also on the roster.

Outside the U.S., there will be plenty of focus on Asia, where CoinDesk’s second annual Consensus Hong Kong conference takes place. There’s a high chance participating companies will use the event as a venue for corporate announcements.

What to Watch

(All times ET)

- Crypto

- Macro

- Feb. 9, 11 a.m.: U.S. consumer inflation expectations for January (Prev. 3.4%)

- Feb. 10, 7 a.m.: Brazil inflation rate YoY (Prev. 4.26%), MoM (Prev. 0.33%)

- Feb. 10, 8:30 a.m.: U.S. retail sales MoM for December Est. 0.5% (Prev. 0.6%)

- Feb. 10 8:30 a.m.: U.S. employment cost index QoQ (Prev. 0.8%)

- Feb. 10, 2 p.m.: Argentina inflation rate YoY (PRev. 31.5%), MoM (Prev. 2.8%)

- Feb. 10, 8:30 p.m.: China inflation rate YoY for January (Prev. 0.8%); MoM (Prev. 0.2%)

- Feb. 11, 8:30 a.m.: U.S. nonfarm payrolls for January Est. 70K (Prev. 50K)

- Feb. 11, 8:30 a.m.: U.S. unemployment rate for January Est. 4.4% (Prev. 4.4%)

- Feb. 11, 8:30 a.m.: U.S. average hourly earnings for January YoY Est. 3.8% (Prev. 3.6%)

- Feb. 12, 2:00 a.m.: U.K. GDP MoM for December. (Prev. 0.3%)

- Feb. 12, 5:30 a.m.: India inflation rate YoY for January (Prev. 1.33%); MoM (Prev. 0.05%)

- Feb. 12, 8:30 a.m.: U.S. initial jobless claims week ending Feb. 7 (Prev. 231K)

- Feb 12, 10 a.m.: U.S. existing home sales for January Est. 4.25M (Prev. 4.35M)

- Feb. 13, 8:30 a.m.: U.S. core inflation rate YoY for January (Prev. 2.6%); MoM Est. 0.3% (Prev. 0.2%)

- Feb. 13, 8:30 a.m.: U.S. inflation rate YoY for January (Prev. 2.7%); MoM Est. 0.3% (Prev. 0.3%)

- Feb. 14: Japan GDP growth rate QoQ for Q4 (Prel) est. 0.4% (Prev. -0.6%); Annualized est. 1.6% (Prev. -2.3%)

- Earnings (Estimates based on FactSet data)

- Feb. 10: Canaan (CAN), pre-market, -$0.03

- Feb. 10: Robinhood Markets (HOOD), post-market, $0.63

- Feb. 10: Upexi (UPXI), post-market, -$0.07

- Feb. 10: Lite Strategy (LITS), post-market

- Feb. 12: Coinbase (COIN), post-market, $1.04

- Feb. 12: Coincheck Group (CNCK), post-market, $0.01

- Feb. 12: Bitdeer Technologies Group (BTDR), pre-market, -$0.06

- Feb. 13: Trump Media & Tech Group (DJT), post-market

- Feb. 13: HIVE Digital Technologies (HIVE), post-market, -$0.07

Token Events

- Governance votes & calls

- Feb. 11: Ripple to host XRP Community Day on X Spaces discussing XRP adotion, regulated finance and innovation.

- Unlocks

- Token Launches

Conferences

Crypto World

Crypto edges higher as oil dips, but futures market shows hesitation: Crypto Markets Today

Crypto markets rallied on Wednesday as oil momentarily slipped below $100 per barrel after U.S. President Donald Trump said the war in Iran will end in “two to three weeks.”

Bitcoin trades at $68,500 having risen by 0.4% since midnight UTC and 3.1% over the past 24 hours, while ether (ETH) is back at $2,130 after a brief stint below $2,000 last week.

The broader crypto market remains in a downtrend dating back to October, although sentiment has shifted slightly following a period of consolidation between $62,500 and $75,000 since early February.

A selection of altcoins have performed particularly well, notably algorand (ALGO), which is up by 22% in the past 24 hours as it bounces back from oversold territory.

Derivatives positioning

- The crypto futures market appears to be churning rather than building clear directional positions, as trading volumes have risen 23% to $210 million over the past 24 hours, while open interest has remained broadly stable at around $106 billion.

- Open interest in major USD- and USDT-denominated futures has clearly diverged from BTC’s recovery from the weekend low of around $65,000. This suggests the rebound is not being driven by a meaningful buildup in leveraged positions, but rather by spot demand or short covering, pointing to a lack of strong conviction behind the move.

- Ether’s OI has risen slightly alongside its spot price, signaling participation from leveraged traders.

- ETH and ZEC stand out as major coins with positive OI-adjusted CVD and funding rate. This combination points to aggressive bidding in the futures market, with traders actively opening long positions and paying a premium to maintain them.

- The market for ADA, XMR, BCH and SHIB suggests otherwise.

- Bitcoin and Ether implied volatility indices continue to present a picture of calm.

- On Deribit, risk reversals continue to show a bias for BTC and ETH put options, which offer protection against price slides. Bearishness is slightly more pronounced in BTC options.

Token talk

- The CoinDesk Computing Select Index (CPUS) was the best performing benchmark on Wednesday, rising by 2.7% since midnight UTC while the CoinDesk Smart Contract Platform Select Capped Index (SCPXC) and the DeFi Select Index (DFX) are up by 1.5% apiece.

- The bitcoin and major-dominant CoinDesk 5 (CD5) and CoinDesk 20 (CD20) have increased by 0.35% and 0.69% respectively, indicating underperformance against the wider altcoin market.

- Algorand (ALGO) led the market gains on Wednesday but it was closely followed by decentralized finance (DeFi) tokens MORPHO and JUP, which posted double digit gains.

- A disproportionate rise in open interest for assets like ETH and ZEC suggests the recent move has been backed by leverage as opposed to spot buying, which could unwind in news to the contrary of Trump’s statement is released this week.

The US dollar is retreating from recent highs, moving into a moderate correction after a prolonged period of gains. Pressure on the currency is building amid weaker-than-expected macroeconomic data, while market participants adopt a wait-and-see approach ahead of key labour market releases, including the ADP report.

The current dynamics reflect a gradual cooling in expectations regarding the resilience of the US economy. Recently published indicators point to a slowdown in business activity and easing labour market tightness, reducing support for the dollar after it reached local highs. At the same time, upcoming releases remain a key factor that could either reinforce the corrective move or restore demand for the US currency.

Among the published figures, investors focused on mixed US macro data. The Chicago PMI fell to 52.8 versus expectations of 54.8, signalling a slowdown in the manufacturing sector. In addition, JOLTS job openings came in below forecasts (6.882 million vs 7.240 million), indicating a gradual cooling in the labour market. Further pressure came from regional business activity indices, including data from the Dallas Fed, which reinforced doubts about the sustainability of the current economic momentum.

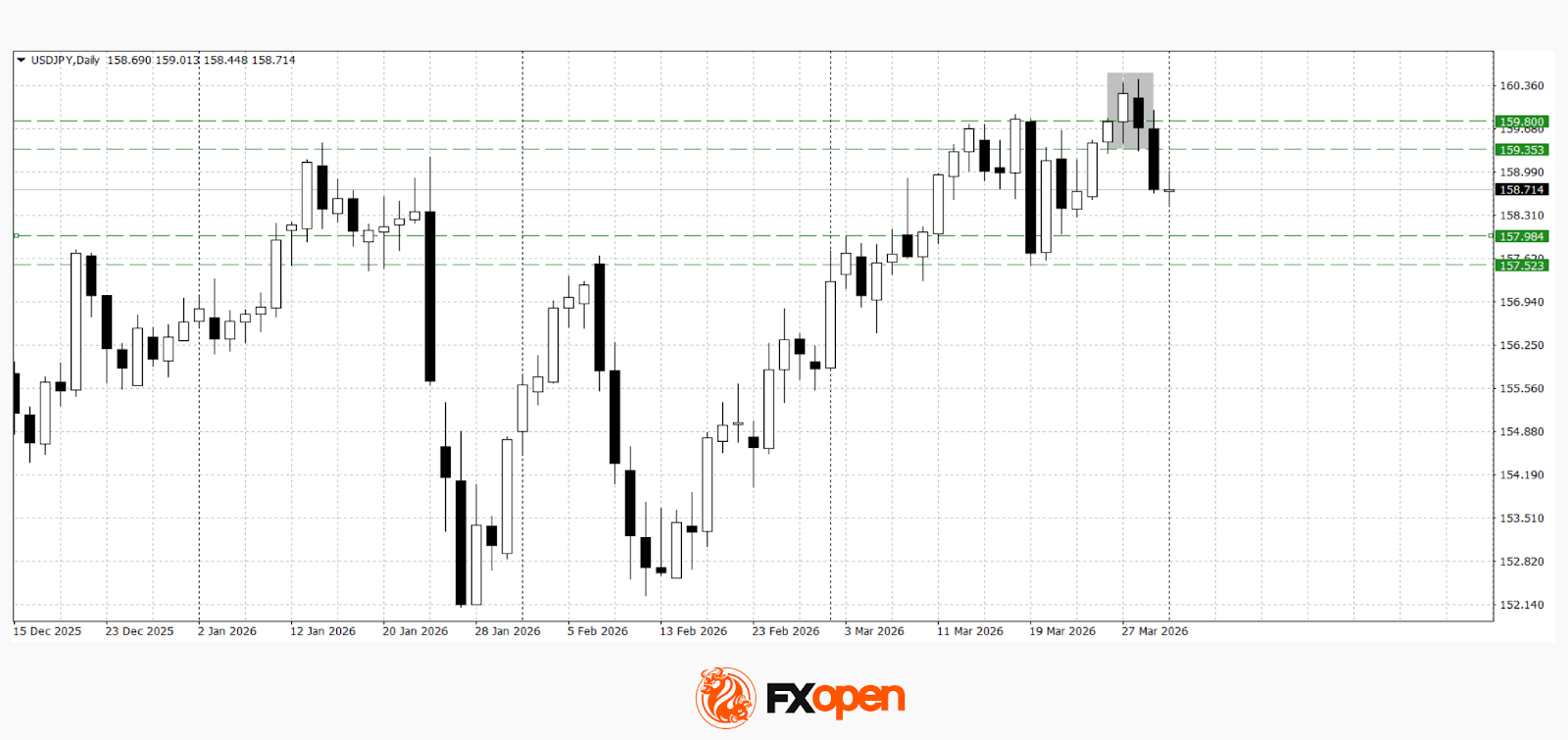

USD/JPY

After reaching fresh yearly highs and testing the psychological 160.00 level, USD/JPY has moved lower, forming a corrective pullback. Technical analysis suggests a potential decline towards the 157.50–158.00 area, as a dark cloud cover pattern has formed on the daily timeframe.

If the price consolidates above the 159.40–159.80 range, the bearish correction scenario may be invalidated.

Key events for USD/JPY:

- today at 15:15 (GMT+3): US ADP non-farm employment change

- today at 15:30 (GMT+3): US core retail sales

- today at 16:45 (GMT+3): US manufacturing PMI

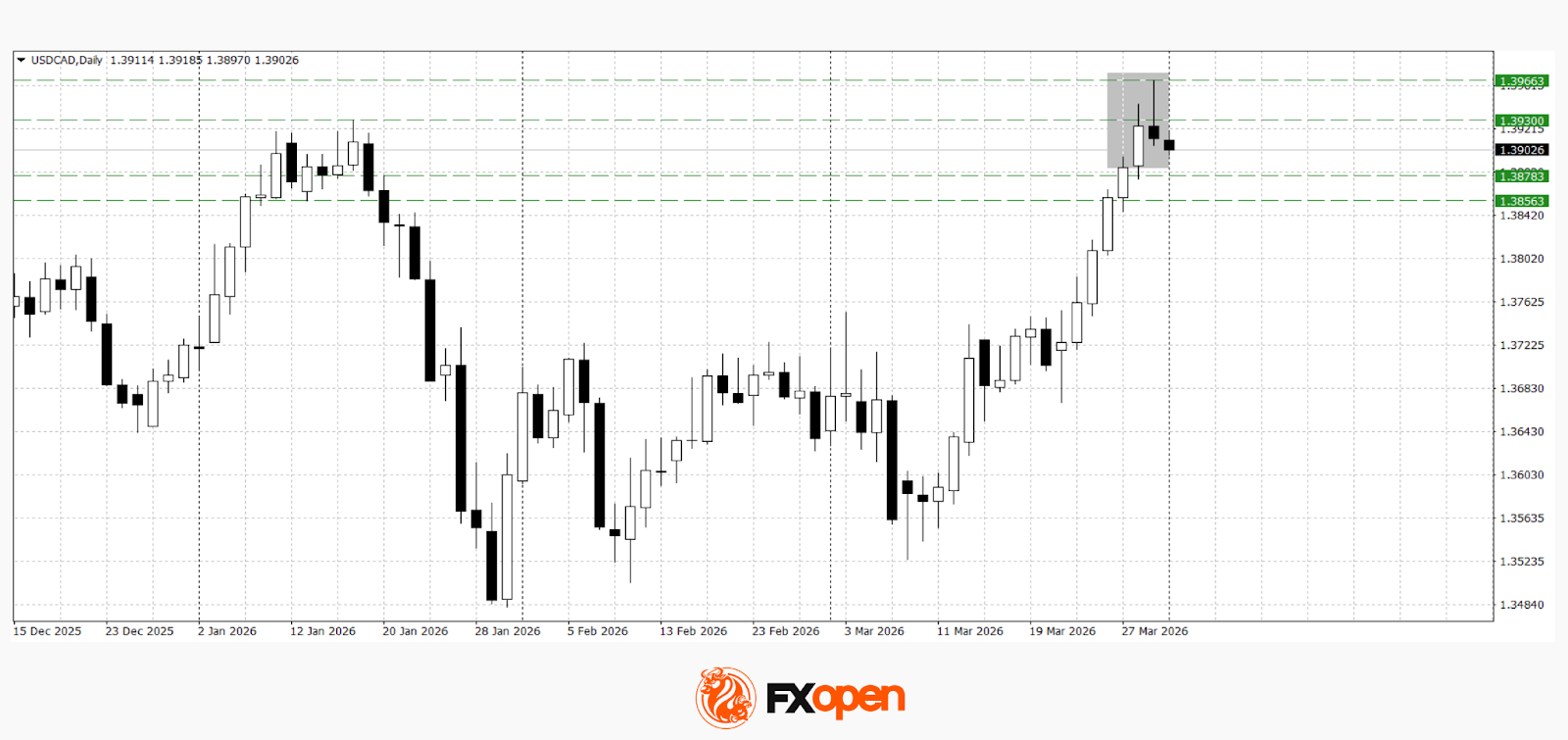

USD/CAD

USD/CAD is also showing a pullback from local highs following a strong rally. The formation of an Evening Star pattern near the 1.3930 level indicates a slowdown in bullish momentum and the potential for a correction towards 1.3860–1.3880.

At the same time, a move above 1.3970 could support a resumption of the uptrend and the formation of a new bullish impulse.

Key events for USD/CAD:

- today at 16:30 (GMT+3): Canada manufacturing PMI

- today at 17:30 (GMT+3): US crude oil inventories

- today at 18:30 (GMT+3): Atlanta Fed GDPNow indicator

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

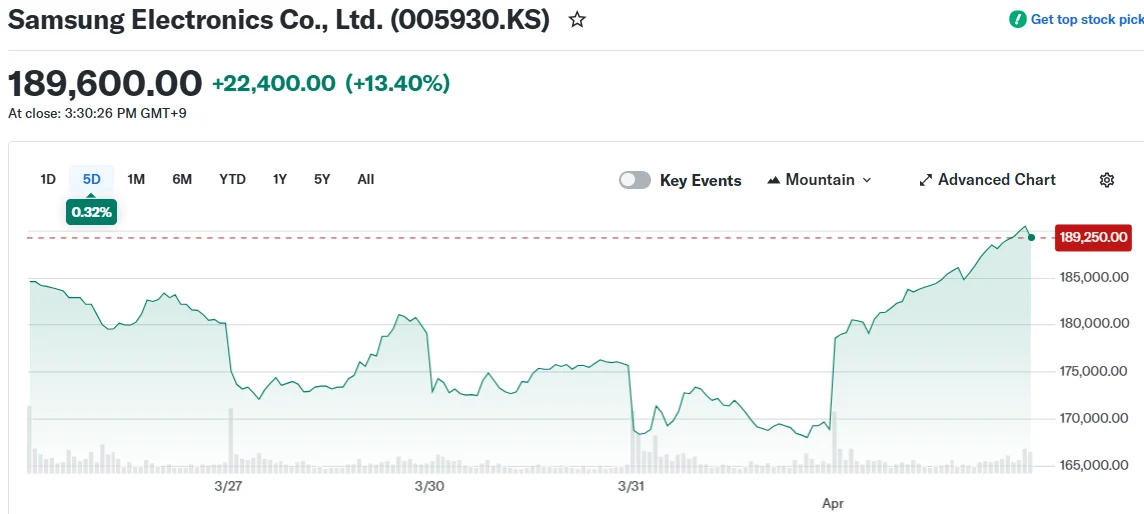

Key Takeaways

- Samsung and SK Hynix shares surged 10–13% Wednesday following significant March declines

- South Korea’s KOSPI index rallied more than 8%, bouncing back from a 19%+ monthly decline

- Optimism around a potential Middle East conflict resolution improved market sentiment

- The semiconductor giants had plunged 23–24% in March amid geopolitical concerns and AI memory chip demand uncertainty

- Overnight gains on Wall Street, spurred by President Trump’s Iran statements, provided momentum

Shares of Samsung Electronics surged 13% to reach 189,600 won during Wednesday’s trading session, while SK Hynix climbed approximately 11% to 893,000 won. The dramatic recovery followed a punishing March for both semiconductor manufacturers.

South Korea’s benchmark KOSPI index jumped 8.4% to close at 5,478.70, with the semiconductor sector rebound providing substantial support. The index had tumbled more than 19% during March.

The two technology giants each lost approximately 23–24% of their value last month. Investor anxiety centered on the escalating Middle East situation, which threatened to increase manufacturing expenses and disrupt global supply networks.

Additional pressure emerged from questions surrounding sustained demand for memory semiconductors utilized in artificial intelligence applications. Google‘s introduction of an algorithm reportedly capable of reducing AI memory needs added to sector headwinds.

Speculation intensified that memory chip pricing could weaken after OpenAI implemented cost-cutting measures. The artificial intelligence company discontinued its video generation platform, Sora, as part of broader budget reductions.

Strategic OpenAI Partnership Under Spotlight

Toward the end of 2025, OpenAI entered into an agreement with Samsung and SK Hynix for the procurement of 900,000 DRAM wafers from the Korean manufacturers. This partnership had previously fueled investor enthusiasm for both companies.

Both semiconductor producers had enjoyed rising memory chip valuations throughout late 2025, supported by expectations that AI-driven demand would exceed available supply. March’s correction erased portions of those earlier advances.

Kiwoom Securities analyst Han Ji-young attributed Wednesday’s rally to value-oriented purchasing, noting that blue-chip stocks had declined sufficiently to entice investors back into the market.

“The stock market is highly likely to enter a recovery phase rather than experience further decline,” Han stated in client communications.

Peace Prospects in Middle East Boost Market Confidence

Market sentiment strengthened following President Trump’s Tuesday statement indicating the United States would withdraw from Iran within a two to three-week timeframe. The President delivered these remarks during a White House press availability.

Iranian President Masoud Pezeshkian indicated Tehran’s willingness to conclude hostilities, though he requested certain unspecified assurances.

These diplomatic developments triggered an overnight rally across U.S. markets, with the positive momentum extending into Asian trading sessions Wednesday.

Samsung shares concluded trading at 189,600 won, approximately $125.83 in U.S. dollar terms. SK Hynix finished at 893,000 won.

The KOSPI index settled at 5,478.70, representing an 8.4% single-day advance.

Despite Wednesday’s gains, both Samsung and SK Hynix continue trading substantially below their pre-March levels.

Crypto World

Uniswap Foundation Reports $85.8M in Total Assets for FY2025, Runway Extends to January 2027

TLDR:

- The Uniswap Foundation held $49.9M in cash and stablecoins alongside 15.1M UNI tokens at year-end 2025.

- A total of $106.2M was allocated toward grants and incentives, covering both new and prior commitments.

- The Foundation committed $26M in new grants throughout FY2025 and disbursed $11M from prior commitments.

- The UNIfication governance proposal, approved December 26, 2025, will reshape financial projections in Q1 2026.

The Uniswap Foundation published its unaudited financial summary for fiscal year 2025 on March 31. The report covers the organization’s financial position through December 31, 2025.

It projects an operational runway through January 2027. Total assets stood at $85.8 million at year-end market prices.

This includes $49.9 million in cash and stablecoins, 15.1 million UNI tokens, and 240 ETH. The report also precedes structural changes tied to the UNIfication governance proposal, approved on December 26, 2025.

Asset Holdings and Fund Allocation

The Foundation held three categories of assets as of year-end 2025. Cash and stablecoins totaled $49.9 million, while 15.1 million UNI tokens and 240 ETH were also on hand. Together, these assets represented $85.8 million in total market value at closing rates.

Of the total earmarked funds, $106.2 million was allocated toward grants and incentives. This breaks down into $87.5 million for new grant commitments in the future. An additional $18.7 million was reserved for previously committed grants still awaiting disbursement.

Beyond grants, $26.3 million was set aside for operating expenses and employee token awards. These two budget lines cover the Foundation’s staffing, administration, and token compensation. They reflect planned spending across its core operational functions.

The fiat and stablecoin reserves were designated primarily for grantmaking and day-to-day operations. UNI token reserves, however, were held to support future runway needs. This approach allowed the Uniswap Foundation to retain upside exposure to UNI’s market performance over time.

The projected spend figures are set to be updated in the Q1 2026 financial report. That update will reflect changes following the UNification proposal’s approval on December 26, 2025. Organizational shifts post-passage are expected to revise the foundation’s financial outlook going forward.

FY2025 Grant Activity and Ecosystem Milestones

Throughout FY2025, the Uniswap Foundation committed $26 million in new grants to ecosystem projects. It also disbursed $11 million from previously committed grants across the year. In Q4 2025 alone, $5.8 million in new grants were committed.

Q4 2025 disbursements reached $2.1 million from prior commitments. These funds went toward builders and developers operating across the broader ecosystem. Grant activity remained steady throughout all four quarters of the year.

On the operational side, the Foundation accrued $9.7 million in operating expenses for FY2025. Employee token awards of 0.45 million UNI were excluded from that figure. Interest revenue on fiat holdings contributed an additional $1.7 million to the organization’s income.

The Foundation also received 20.3 million UNI tokens from the Uniswap Treasury via the Uniswap Unleashed Proposal. At year-end prices, this transfer equaled approximately $114 million in market value. This inflow added materially to the Foundation’s overall reserve position during 2025.

Key milestones in 2025 included the launch of Uniswap v4 and Unichain. More than 1,500 builders onboarded to v4 during the calendar year.

These developments supported the organization’s ongoing commitment to expanding decentralized finance infrastructure.

Crypto is pseudonymous – a halfway house between anonymous and public.

While you don’t need to expose your identity to open a crypto wallet, public blockchains leave a visible record of your activity for all to see.

A single withdrawal from a KYC exchange can link your real name to a wallet, and once that wallet is tied to your identity, anyone can trace the rest of your on-chain activity.

This is why, as on-chain analysis tools become more widely used, many users are paying closer attention to what financial privacy actually means in crypto.

Mixero was built around this issue. The platform focuses on helping users protect their transaction history while remaining in a decentralized environment.

Public Blockchains Make Wallet Activity Easy to Follow

At the center of Mixero’s service is CoinJoin, a method used to combine transactions in a way which makes blockchain analysis far more difficult.

Rather than sending funds through a direct and easily traceable path, CoinJoin helps obscure the relationship between sender and recipient. This is Mixero’s core solution for Bitcoin users who want stronger privacy without stepping outside the asset itself.

The company argues that privacy has become an important part of using crypto in a mature way. On public ledgers, transaction histories can reveal far more than a single payment. They can expose balances, spending patterns, wallet links, and long-term activity. This can become a serious concern for users who value financial discretion.

Mixero’s platform is designed to keep the process simple. Users can enter one or several destination BTC addresses, adjust settings, receive a signed Letter of Guarantee, and track the order through a status page.

The service is also available through Tor, while Mixero says it keeps no logs of user activity.

Advanced Mode Uses Monero for Deeper Privacy

For users who want a higher level of protection, Mixero offers Advanced Mode. This feature routes transactions through Monero before returning them to Bitcoin. The process works through an XMR bridge and automatically generated wallets, giving users access to the strongest privacy option Mixero offers.

Monero uses built-in privacy technologies such as stealth addresses, ring signatures, and RingCT to conceal transaction details. These tools are designed to hide the sender, receiver, and amount involved in a transfer, which makes Monero one of the most privacy-focused networks in the market.

By routing Bitcoin through Monero and back again, Mixero gives users a way to get stronger privacy without leaving BTC behind at the end. It is aimed at people who want more cover than

About Mixero

Mixero is a privacy-focused crypto service built for users who want stronger transaction privacy on public blockchains. The platform offers CoinJoin-based Bitcoin mixing, Tor access, signed Letters of Guarantee, and an Advanced Mode which routes transactions through Monero for deeper anonymity. Designed for users who value discretion in an increasingly transparent on-chain environment, Mixero aims to make privacy tools more accessible without sacrificing ease of use. Its service is focused on helping users reduce the visibility of their transaction history while staying within the crypto ecosystem.

The post Mixero Pushes for Real Privacy on Public Blockchains appeared first on BeInCrypto.

Solana is holding its breath, trading at the $84 price level, it is barely moving with just 1% gain in the last 24 hours, as opposed to BTC 2.4% gain and ETH 4.5%, even with bullish catalysts that bring a good prediction. Institutional heavyweights Interactive Brokers and Galaxy Digital signal a deepening commitment to the network, and could force a directional move soon.

— Solana Daily (@solana_daily) March 31, 2026

Interactive Brokers (@IBKR), one of the world's largest brokers, launches crypto trading for 450M people across Europe, including $SOL. pic.twitter.com/mOvB1kVSxd

Interactive Brokers (@IBKR), one of the world's largest brokers, launches crypto trading for 450M people across Europe, including $SOL. pic.twitter.com/mOvB1kVSxd

Institutional pressure is building on both sides of the trade. Galaxy’s continued positioning in SOL infrastructure and Interactive Brokers’ expanded support for the asset add credibility to the bull thesis, even as the broader market sits in near-extreme fear.

The macro headwinds are real. But so is the on-chain growth underpinning SOL’s longer-term case. ETF inflows into Solana products remain a live catalyst that institutional desks are watching closely.

Discover: The best crypto to diversify your portfolio with

Solana Price Prediction: $95 or $75 Next?

SOL has been compressing in a tightening range under $90, a setup that can resolved with a sharp move in either direction. At $84 with a 1.5% single-day decline, the immediate picture looks defensive, but RSI sits at 46, a technical buy signal that suggests sellers haven’t fully taken control yet.

Resistance is stacked. Immediate ceiling at $88, then the $90.50–$91 zone, with $95 acting as the breakout trigger that unlocks the bull case. Above that level, we can safely target $115–$125.

But a breakdown below the $75 support zone opens the door to deeper downside. The setup is binary. Position sizing accordingly.

Discover: The best pre-launch token sales

Maxi Doge Targets Early Mover Upside as Solana Tests Key Levels

SOL at $84 with a $95 breakout requirement means most of the easy money on this trade has already been made. For traders calculating risk-reward on a market-cap-weighted basis, the upside from here demands patience and assumes macro conditions cooperate. That’s where early-stage positioning starts looking different on a spreadsheet.

Maxi Doge ($MAXI) is an Ethereum-based meme token built around a 240-lb canine juggernaut and a 1000x leverage trading mentality, genuinely unhinged energy, deliberately so.

The project has raised more than $4,7 million at a current price of $0.00028, with 66% staking APY bonus available for holders. Features include holder-only trading competitions with leaderboard rewards, a Maxi Fund treasury for liquidity and partnerships, and meme-first marketing built on viral gym-bro humor.

Research Maxi Doge and join the army.

This article is for informational purposes only and does not constitute financial advice. Crypto assets are highly volatile. Always do your own research before investing.

The post Solana Price Prediction: Interactive Brokers Supports SOL, Galaxy Doubles Down appeared first on Cryptonews.

Strategy, the world’s largest publicly traded Bitcoin holder, has held the 11.5% dividend rate on its perpetual preferred stock, Stretch (STRC). This marks the first time the product has not seen a dividend increase since the product launched in July 2025.

STRC debuted in July 2025 with a 9% dividend and has since undergone seven dividend increases. The company was able to maintain the current rate after the volume weighted average price (VWAP) for the month reached $99.95, keeping the shares close enough to their $100 par value.

Strategy positions STRC as a short duration, high yield savings alternative. The perpetual preferred stock pays monthly cash distributions, with the dividend rate adjusted each month to support trading near par and limit price volatility.

During Tuesday’s session, STRC held close to par for most of the day. The company is estimated to have purchased over 1,000 BTC, and it took 12 days for STRC to recover back to par following the ex dividend date. It is likely the shares will continue trading near par over the next two weeks, leading up to the April 14 ex dividend date.

Meanwhile, Strive (ASST), the bitcoin treasury asset manager, saw its own perpetual preferred product, SATA, reach $100 par for the first time. This enabled the company to issue shares through its at the market (ATM) program to fund additional bitcoin purchases. SATA currently offers a dividend rate of 12.7%.

Announced at EthCC in Cannes, the upgrade enables institution-specific borrowing environments, structured credit products, and RWA-backed lending within a unified liquidity system.

Crypto World

Australia passes crypto regulation requiring exchanges to obtain financial services licenses

Australia passed legislation on Wednesday, creating its first comprehensive regulatory framework for digital assets that requires crypto exchanges and custody providers to obtain financial services licenses.

The Corporations Amendment (Digital Assets Framework) Bill 2025 cleared both houses on April 1, bringing firms that hold digital assets on behalf of customers into the existing Australian Financial Services Licence regime.

Australia’s bill creates two new regulated categories under the Corporations Act: digital asset platforms, which hold crypto on behalf of users, and tokenized custody platforms, which hold real-world assets and issue a corresponding digital token.

Operators of both must obtain an Australian Financial Services License from ASIC, bringing them under the same core rules as brokers or fund managers, including requirements to safeguard client assets, provide standardized disclosures, avoid misleading conduct, and maintain dispute resolution and compensation systems.

Instead of regulating crypto itself, the law targets the companies in the middle that control customer funds, aiming to reduce risks like commingling, insolvency, and misuse of assets that have caused losses in past crypto failures.

Research from the Digital Finance Cooperative Research Center and industry groups estimates Australia could generate as much as A$24 billion annually from tokenized markets, payments, and digital assets, roughly 1% of GDP. Under the previous regulatory path, the country was on track to capture just A$1 Billion of that by 2030.

A Kraken spokesperson said the law provides a “top-down signal” that Australia is serious about digital assets, adding that clearer rules would give firms confidence to invest and expand locally.

Kate Cooper, CEO of OKX Australia and co-chair of the Digital Economy Council of Australia, called the bill a “pivotal moment,” saying it establishes a foundation for institutional participation and long-term capital allocation.

Almonty’s tungsten mine in Sangdong, South Korea, in March 2026.

Almonty

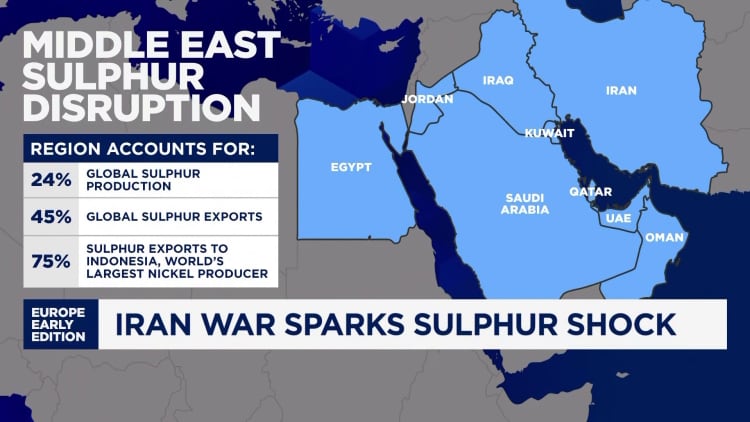

BEIJING — The Iran war is squeezing a global commodities market already pressured by China’s export controls and stockpiling efforts.

Prices of three niche elements — tungsten, sulfur and helium — have climbed sharply in recent weeks.

While none of the commodities are traded as widely as oil, the surge indicates how ripple effects from the Middle East conflict could end up restricting production of the semiconductors that power artificial intelligence advances.

Tungsten, a metal nearly as hard as a diamond, creates the electrical connection in the core of a semiconductor chip. Sulfuric acid, a byproduct of sulfur, cleans chip wafers. Helium enables smooth production of semiconductors since the gas prevents unwanted chemical reactions in the manufacturing process.

Those are just some of the ways in which the three elements have become critical for modern manufacturing, including for defense.

Beijing started to ramp up its control over the critical supplies even before the Iran war started on Feb. 28, partly as tensions with the U.S. escalated over the last few years.

China started restricting tungsten exports just over a year ago, and in December called for tighter limits on sulfuric acid exports. Helium, a gas that’s difficult to store, saw the volume of Chinese imports rise by 15.7% in 2025, after a nearly 65% surge in 2024, according to Wind Information.

The Iran war and the ensuing constraints on the Strait of Hormuz, a critical Middle East shipping route for energy and chemicals, has tipped some oversupply situations into undersupply, while exacerbating existing shortages.

Prices of the three commodities have jumped in some cases by more than oil. The widely used fossil fuel has climbed by more than 50% in March, putting Brent on track for a record month.

“While the Chinese supply chain is being viewed as more resilient than many peers, the risk of disruption in chemicals as raw materials for manufacturers in selected segments is higher than expected based on the feedback,” Goldman Sachs analysts said in a report late last week, citing nearly 40 commodity-related meetings and site visits in China.

Tungsten

Tungsten hit a record high of over $3,000 late last week, marking a surge of well over 50% for the month and more than tripling in price since late December. That’s based on the industry benchmark called “ammonium para tungstate (APT)” in metric ton units, or MTU, from Fastmarket, as quoted by tungsten miner Almonty.

Almonty officially reopened a large tungsten mine in Sangdong, South Korea, earlier this month, and plans to start producing some tungsten this year at a project in the U.S. state of Montana.

The company’s CEO Lewis Black told CNBC that defense sector demand for tungsten has been “extremely strong” since the beginning of last year, but that there’s been no notable change despite the Iran war.

“There’s no material to stockpile. That’s probably the biggest change,” he said.

Sulfur

The price of sulfuric acid in Africa is now at least 30% higher than it was prior to the war, and is still rising, the Goldman Sachs analysts said, citing a local Chinese miner in Africa.

Other assessments point to a milder rise in prices.

China sulfur prices, including cost and freight, climbed by about 13% from early March to $621 per tonne as of March 26, according to S&P Global Platts.

“A 2-3 month effective blockade would likely become a severe supply shock, especially as freight/insurance stay elevated and Middle East-origin cargoes become harder to execute,” Pan Yuya, lead analyst for sulfur and phosphate raw materials at S&P Global Energy, and Isaac Zhao, senior principal analyst, China fertilizers at S&P Global Energy, said in a March 20 note.

The S&P analysts said that around 56% of China’s sulfur imports came from the Middle East in 2025.

“Even prior to the Middle East conflict, sulfur prices were rising sharply as the market tightened. With sulfur prices now at fresh record highs, the ‘super squeeze’ in this rather obscure commodity in supply warrants further examination,” HSBC analysts said in a March 16 report.

Helium

Helium prices have roughly doubled since the Iran war began, according to Fitch Ratings.

As most trading occurs through long-term private contracts between industrial gas suppliers and manufacturers, it is difficult to pinpoint industry-wide prices, said Shelley Jang, Fitch’s director of Asia-Pacific corporate ratings.

Iranian missile attacks this month crippled a key industrial center in Qatar, which produces about one-third of the world’s helium.

That implies helium supply won’t be restored anytime soon, pointed out Christopher Ecclestone, principal and mining strategist at Hallgarten & Company.

In one indication of further market tightness, prices of helium in China’s Henan province have reversed a downturn this year to climb from a Feb. 28 low of 545 yuan ($78.85) a bottle to 600 yuan ($86.81), according to Wind Information.

Subscribe now

Shortages caused by the Iran war are the latest supply chain disruption to rock global markets, which faced similar shocks from Russia’s invasion of Ukraine in 2022 and the Covid-19 pandemic. That’s pushed companies to diversify, and countries such as China to ramp up stockpiling plans.

“Access to supplies of certain physical materials where production and processing is concentrated in China will become more frequent topics of negotiations with Beijing,” Rhodium Group said in a March 24 report.

Limited price transparency also means the shortage could be worse than available numbers suggest.

Tungsten and helium prices have been surging, “but you don’t have anyone on the buy side saying, ‘oh my goodness, we don’t have enough product,’” Ecclestone said. “Defense contractors should have warehouses of tungsten, but they don’t.”

“The world has got lazy. It thinks life is like a supermarket, the product is a pack of cornflakes or a few tons of sulfuric acid,” he said. “The supermarket of commodities has had a few of the aisles chopped down.”

Dog bites cyclist on Strensall to Haxby path – police appeal

Warning Iran war 'shock' could push up mortgages for 1.3m homeowners

Crypto edges higher as oil dips, but futures market shows hesitation: Crypto Markets Today

-

News Videos6 days ago

News Videos6 days agoParliament publishes latest register of MPs’ financial interests

-

Tech6 days ago

Tech6 days agoIntercom’s new post-trained Fin Apex 1.0 beats GPT-5.4 and Claude Sonnet 4.6 at customer service resolutions

-

NewsBeat5 days ago

NewsBeat5 days agoThe Story hosts event on Durham’s historic registers

-

Business6 days ago

Business6 days agoInstagram, YouTube Found Responsible for Teen’s Mental Health Struggle in Historic Ruling

-

NewsBeat7 days ago

NewsBeat7 days agoTesco is selling new Cadbury Dairy Milk bar and people can’t wait to try it

-

Sports5 days ago

Sports5 days agoSweet Sixteen Game Thread: Tide vs Michigan

-

Entertainment2 days ago

Fans slam 'heartbreaking' Barbie Dream Fest convention debacle with 'cardboard cutout' experience

-

Entertainment4 days ago

Entertainment4 days agoLana Del Rey Celebrates Her Husband’s 51st Birthday In New Post

-

Crypto World23 hours ago

Dems press CFTC, ethics board on prediction-market insider trades

-

Sports18 hours ago

Sports18 hours agoTallest college basketball player ever, standing at 7-foot-9, entering transfer portal

-

Fashion7 days ago

Fashion7 days agoHow to Style Spring Like WeWoreWhat: Easy Outfit Ideas for 2026

-

Tech2 days ago

Tech2 days agoThe Pixel 10a doesn’t have a camera bump, and it’s great

-

Entertainment6 days ago

Entertainment6 days agoHBO’s Harry Potter Series Will Definitely Fail For One Big Reason, And It’s Not J.K. Rowling Or Snape

-

Fashion6 days ago

Fashion6 days agoEn Vogue in Brown Leather and Tailored Neutrals by Atelier Savoir, Styled by J Bolin

-

Crypto World1 day ago

Crypto World1 day agoU.S. rule change may open trillions in 401(k) funds to crypto

-

Fashion6 days ago

Fashion6 days agoWhat Are Your Favorite T-Shirts for the Weekend?

-

Politics2 days ago

Politics2 days agoShould Trump Be Scared Strait?

-

Fashion5 days ago

Fashion5 days agoWeekly News Update, 3.27.26 – Corporette.com

-

Sports1 day ago

Sports1 day agoWomen’s hockey camp eyes fitness boost, tactics ahead of WC 2026 campaign | Other Sports News

-

Tech1 day ago

Tech1 day agoHow to back up your iPhone & iPad to your Mac before something goes wrong

You must be logged in to post a comment Login