Crypto World

DeFi Generated $8 Billion in Onchain Yield in 2025: Analysis

A breakdown of DeFi’s yield sources reveals that borrowing demand, trading fees, and funding rates drove the bulk of returns, while more than half of stablecoin deposits in the Ethereum ecosystem are earning less than U.S. Treasuries.

Decentralized finance (DeFi) produced roughly $8 billion in onchain yield in 2025, according to a detailed analysis published by researcher Vadym that maps the full spectrum of where DeFi returns actually originate. The breakdown reveals that yield is abundant in aggregate but unevenly distributed, often circular, and in many cases difficult to package into structured products.

The findings land as yields across DeFi have dried up. Borrowing rates on major lending platforms have converged with the Federal Reserve’s policy rate, and “safe” stablecoin supply rates now average roughly 3% — below U.S. Treasuries and the Secured Overnight Financing Rate. On Aave, the 30-day average yield on USDC and USDT sits around 2%. Out of more than $20 billion in stablecoin vaults across Ethereum and its Layer 2s, 58% of TVL is earning under 3% APY, the report notes.

Where the $8 Billion Comes From

The analysis identifies five primary yield sources, each with distinct risk profiles and scalability constraints.

AMM trading fees were the largest single category at roughly $4.2 billion, with Uniswap, Meteora, and Raydium accounting for 62% of the total. But the analysis cautions that these fees are notoriously difficult to capture in structured products. Liquidity providers — particularly those using concentrated liquidity — frequently lose money to toxic order flow, and LP-manager vaults have failed to gain meaningful traction.

Borrow interest generated approximately $1.76 billion across money markets, including Aave, Morpho, Spark, Maple and Fluid. Money markets account for more than 60% of total DeFi TVL, making lending the sector’s economic backbone. However, the analysis found that roughly half of all borrowing demand is recursive — users borrowing to loop back into other yield sources, such as liquid staking tokens or yield-bearing stablecoins. On Aave’s Ethereum deployment, about 39% of borrowing demand goes toward leveraging ETH staking rewards, while another 11.6% loops Ethena’s sUSDe.

Perps funding fees, largely pioneered onchain by Ethena, contributed around $300 million. Ethena’s sUSDe derives its yield from staking rewards and short funding rates — a mechanism that drew both praise and alarm when it launched in 2024.

Real-world assets generated an estimated $600–900 million, with U.S. Treasuries holding the largest share of the RWA market at about 41% and private credit at 25%.

Network staking rewards and MEV comprise the remainder, with Ethereum’s issuance totaling roughly one million ETH in 2025. The MEV-derived portion of staking yield has been trending downward as private order flow routing — now handling about 90% of swaps — has reduced frontrunning opportunities.

Untapped and Underdeveloped Sources

The analysis also highlights categories where yield capture remains negligible. Insurance underwriting generated just $5.5 million in premiums in 2025, mostly through Nexus Mutual. Options — despite CeFi open interest of $30–50 billion — have roughly $1.8 billion in onchain OI with no breakout structured product. Volatility selling and protocol risk transfer remain largely untapped, which the analysis flags as a potential opportunity as risk curation grows more competitive.

Sky’s Balancing Act

As a case study in how protocols assemble these disparate yield sources, the analysis examines Sky (formerly MakerDAO), whose 3.75% USDS Savings Rate has attracted significant capital amid the compression. Sky’s TVL surged 38% in March, making it the fourth-largest DeFi protocol, with the sUSDS savings pool alone accounting for approximately $6.5 billion in deposits.

The breakdown reveals that approximately 70% of Sky’s income derives from offchain origination — primarily USDC earning Coinbase rewards through the peg stability module (PSM), and RWA exposure through products like BlackRock’s BUIDL and Janus Henderson funds. The remaining 30% flows from onchain sources, with Spark acting as Sky’s primary allocation arm, routing capital into Sparklend, Maple’s institutional lending, Anchorage, and other yield-bearing opportunities depending on prevailing rates.

The implication, the analysis argues, is that even as TradFi yield increasingly flows through permissioned channels, its redistribution happens onchain, providing a floor for DeFi rates and potentially setting the stage for a next generation of yield derivatives, including fixed-rate products, interest-rate swaps and structured tranches.

This article was written with the assistance of AI workflows. All our stories are curated, edited and fact-checked by a human.

Crypto World

LINK price consolidates above $9 while CCIP adoption cements Chainlink’s tokenization role

Summary

- Chainlink’s LINK price is trading near $9.42 today, up 3.64% in the last 24 hours and about 1.19% over the past week, with a market cap around $6.67 billion.

- Daily trading volume stands near $659.4 million, underscoring solid liquidity and active positioning in a market that is increasingly using Chainlink for tokenization and cross-chain infrastructure.

- New integrations for Chainlink’s Cross-Chain Interoperability Protocol (CCIP), including ADIChain and broader bank and asset manager pilots, are helping to frame LINK as core middleware for tokenized assets.

Chainlink’s (LINK) price is changing hands around $9.42 today, with 1-hour gains of 0.13%, a 24-hour rise of 3.64% and a 7-day increase of 1.19%, putting its market capitalization at roughly $6.67 billion on a circulating supply of about 708.09 million tokens.

LINK price hovers near 3-month low

Over the last 24 hours, LINK’s spot trading volume has reached about $659,390,868 across tracked exchanges, giving the asset a volume-to-market-cap ratio close to 10%, a level consistent with heavy but orderly trading in a liquid large-cap altcoin. In earlier snapshots, the token traded near $14.28 with a market cap of $9.94 billion and daily volume of $687.78 million, showing how LINK has compressed in price from its late-2025 range while maintaining deep liquidity.

Historical data from market dashboards shows that LINK remains far below its all-time high near $52.70, leaving it down roughly 70–73% from peak even after the latest bounce, but with its full 696–708 million token circulating supply actively traded across major venues. That combination of long-term drawdown and persistent liquidity has made LINK a structural component of many portfolios that want oracle and interoperability exposure, rather than purely momentum-driven flows.

Chainlink is a decentralized oracle and interoperability network that connects smart contracts to off-chain data, computation and other blockchains, positioning LINK as a core infrastructure token rather than a pure DeFi coin, AI asset or layer-1. Its nodes deliver price feeds, proof-of-reserve data, random number generation and, increasingly, cross-chain messaging via the Cross-Chain Interoperability Protocol (CCIP). In this model, LINK is used to pay for oracle services and secure the network, making demand for tokenized assets, DeFi and institutional connectivity directly relevant to the token’s long-term economics.

Recent technical and ecosystem updates have reinforced this role. Chainlink’s own communication describes CCIP as an “end-to-end interoperability standard” that allows tokenized funds to keep their share register on one chain while using CCIP to process subscriptions and redemptions across others, including private bank networks and public blockchains like Ethereum and Solana. A January 2026 deep dive outlines plans for CCIP v1.5 on mainnet, which will enable self-serve token integrations, customizable rate limits and support for EVM-compatible zk-rollups, expanding the protocol’s reach.

Adoption data around CCIP and related services helps explain why LINK continues to attract directional interest despite its long consolidation. Research cited in a March 2026 price outlook estimates that CCIP has been averaging around $90 million in weekly token transfers, hinting at steady cross-chain volume already moving through the protocol. Chainlink itself reports that its oracle infrastructure has enabled over $28 trillion in cumulative transaction value across DeFi, tokenized assets and other use cases, providing a track record that appeals to institutional users.

New partnerships add regional and sector depth. In early March 2026, the ADI Foundation announced that it would integrate Chainlink and use CCIP as the canonical bridge for ADIChain, a network focused on tokenization across the Middle East, Africa and Asia and reportedly backed by over $240 billion in assets through its institutional partners. Under that collaboration, Chainlink also becomes ADIChain’s official oracle provider for price feeds, reserve verification and NAV calculations for stablecoins and tokenized real-world assets, making LINK central to the network’s RWA and stablecoin stack.

More broadly, coverage of CCIP in banking and asset management circles highlights pilot projects in which major banks and asset managers use Chainlink to move tokenized fund shares and stablecoins across public and private chains, including experiments by ANZ and SBI Digital Markets to settle cross-border payments and manage subscriptions. In that environment, LINK’s current price level around $9–$10, coupled with hundreds of millions of dollars in daily volume and a multi-year consolidation structure around the $14 support region, positions it as a liquid, infrastructure-linked bet on the scaling of tokenization and cross-chain activity rather than a short-lived momentum trade.

Update (March 25 8:22PM UTC): This article has been updated to clarify the role of M1X Global in the first paragraph.

The technology provider building the infrastructure for the Republic of the Marshall Islands’ universal basic income (UBI) program which will use a US dollar-pegged sovereign financial instrument has attracted some significant crypto-tied backers.

In a Tuesday notice shared exclusively with Cointelegraph, M1X Global announced that it had launched following a $3 million angel investment round by current and former executives connected to crypto and financial services companies.

Backers for the M1X Global angel round included former Coinbase chief technology officer Balaji Srinivasan and Cumberland Labs CEO Tama Churchouse.

According to the company, the funding will support the development and adoption of the USDM1 digital sovereign bond which allows citizens of the Republic of the Marshall Islands to access the UBI program.

While the Marshall Islands debuted USDM1 on the Stellar blockchain in December, M1X Global said it intended to expand the digital instrument’s use cases into institutional markets. According to M1X co-founder and COO Jordan Goldman, the expanded access to the instrument will allow it to “serve as high-quality collateral.”

Many countries have introduced similar programs furthering the adoption of digital assets, from the Bahamas launching the first central bank digital currency in 2021 to Palau backing blockchain savings bonds in 2024. The Bank of Canada said earlier this month that a pilot program had resulted in the issuance of the country’s first tokenized bond.

Related: What happens to Bitcoin if US bond yields soar above 5%?

IMF cautioned against Marshall Islands launching digital sovereign bond

Although the launch of the UBI program using USDM1 kicked off in December, the International Monetary Fund (IMF) had warned the government of the Marshall Islands not to launch the digital sovereign bond “given the lack of pre-requisite capacity and ability to effectively mitigate associated risks.” The IMF said that the instrument’s ability to improve financial inclusion was “limited in the near term, given the lack of adequate digital infrastructure.”

“The risks posed by a global launch of USDM1 appear to be disproportionally higher than the perceived gains and cannot be mitigated given lack of prerequisite capacity,” said the IMF in a December report on the Marshall Islands, adding:

“USDM1 may entail fiscal risks in the event of redemption pressures due to loss of investor confidence. The latter could be triggered by price volatility of T-Bills or more likely by operational and cybersecurity vulnerabilities, possibly amplified by inadequate legal and regulatory framework for USDM1.”

A representative of the Marshall Islands government told Cointelegraph in November that it was “in active dialogue with the IMF regarding the UBI programme and USDM1” and the digital bond was “intentionally designed to mirror the Brady-style framework historically supported by the IMF.”

Regarding the M1X Global launch, a spokesperson for the Marshall Islands’ government told Cointelegraph that the IMF warning was based on the fact that USDM1 was untested at the time.

Magazine: What’s a ‘Network State’ and are there real-life examples? Big Questions

Dune and Visa released research showing non-USD stablecoins growing dramatically, with holder addresses jumping 30x and monthly transfer volume hitting $10B.

Dune Analytics and Visa published research titled “Beyond Dollarization” on March 25 revealing significant growth in non-USD stablecoin adoption. Non-USD stablecoin supply grew 3x, while holder addresses increased from 40,000 to 1.2 million (a 30x jump) and monthly transfer volume expanded from $600 million to $10 billion.

The research found that approximately 80% of non-USD stablecoin activity is driven by payments and treasury flows rather than DeFi activity. Transfer patterns show weekend drops that mirror payroll cycles, indicating use of local currency stablecoins as functional money rather than speculative assets.

Sources: Dune Analytics | The Block

This article was generated automatically by The Defiant’s AI news system from publicly available sources.

Crypto World

Pump.fun locks creator fees after “vamping” drains trust on Solana, industry reaction snowballs

Pump.fun now lets creators change fee wallets only once after launch, moving to curb “vamping” on Solana as platform revenue falls and industry figures call for coordinated reform.

Summary

- Pump.fun co-founder Alon Cohen announced a protocol update on March 24 that limits token creators to one post-launch change of their fee recipient wallet.

- The move came in direct response to widespread “vamping” — a practice where creators redirected fees to their own wallets after tokens gained traction, undercutting buyers.

- The update drew over 396,000 views on X and sparked a public industry call to action from prominent Solana figures to collectively eliminate the behavior.

Pump.fun, the dominant Solana (SOL)-based memecoin launchpad, announced a significant protocol change on March 24 that caps creator fee modifications to a single post-launch edit — a direct response to rampant fee manipulation that has eroded user trust across the platform. The update was announced by co-founder Alon Cohen, known on X as @a1lon9, in a thread that has since accumulated over 396,200 views, 2,600 likes, and 479 retweets.

Pump.fun reacts to curb ‘vamping’

The problem, as Cohen explained it, had been structural. Every token deployed on pump.fun carries an assigned Coin Admin who controls the creator fee setup — who receives the fees, how they are distributed, and in what proportions. Until now, those Coin Admins faced no limits on how many times they could alter those settings. “Coin Admins had free reign to change fee recipients and distribution as much as they desire, which ultimately led to manipulation,” Cohen wrote. The pattern was predictable: a creator would deploy a token with fees directed toward a third-party wallet to build community trust, allow the token to gain traction and generate meaningful fee revenue, then quietly redirect those fees back to themselves. “People realize, get frustrated, the coin loses traction and narrative is ruined,” Cohen added.

The fix is relatively simple in mechanism but significant in impact. Under the new rules, every token launches with standard creator fees by default, and the creator is granted exactly one opportunity to redirect those fees to a different wallet. After that single reassignment, the configuration becomes permanent and cannot be altered. “The result: if the creator redirects fees to another wallet, those settings are locked. If they don’t redirect fees, their one chance to do so can be used later,” Cohen said. All existing coins with active fee distributions have had their settings locked retroactively under the update.

The announcement triggered a wave of responses from across the Solana ecosystem, with one post in particular hitting 215,300 views within hours. Tom, a well-known Solana trader who goes by @SolportTom on X, directly called out major trading platforms to join the effort. “We can all agree that vamps suck ass. Need to work together to solve it,” he wrote, tagging @a1lon9, @AxiomExchange, @TradingTerminal, and others. His argument cut against short-term financial incentive: “Yes there’ll be less money in fees but a better space = this will last longer.”

The response illustrated a broader sentiment that has been building on pump.fun for months. The platform, which allows virtually anyone to create and trade memecoins on Solana in seconds, has faced recurring criticism over how its fee structure rewards deployers at the expense of traders. In January, pump.fun overhauled its creator-fee model after acknowledging that its Dynamic Fees V1 system had inadvertently incentivized coin creation over actual trading activity — the lifeblood of the platform.

The update arrives at a difficult moment for the platform commercially. Despite pump.fun expanding beyond memecoins in March with support for assets including WBTC, USDC, and Ethereum via Wormhole — and surpassing 1.5 million app downloads — its fee revenue and monthly trading volume remain well below 2025 levels. At its January 2025 peak, the platform generated $15.38 million in a single day in protocol fees; that figure has fallen sharply since. Cohen himself acknowledged the limits of the current fix. “It’s important to note that this is one small step towards overcoming a much larger problem,” he wrote, thanking “hundreds of traders who have given myself or pump.fun affiliates meaningful feedback over recent months.”

Solana (SOL) is currently trading at $92.17, up 3.29% over the past 24 hours, according to crypto.news data.

Turkey’s crypto community launched a mass #kriptodavergiyehayır campaign ahead of a vote on a draft bill imposing a 0.03% transaction levy and up to 40% tax on foreign-platform gains.

Summary

- Turkey’s parliament was set to vote on a draft crypto tax law on March 25 that would impose a 0.03% transaction fee on all trades and up to a 40% gains tax for those using foreign platforms.

- The hashtag #kriptodavergiyehayır — roughly translating to “No to crypto tax” — exploded across X on March 24, drawing 145,000 views, 3,700 likes, and 686 retweets on a single post by prominent Turkish crypto analyst Selçuk Ergin (@Selcoin).

- Turkey is the largest crypto market in the Middle East and North Africa region, recording nearly $200 billion in annual on-chain transactions — almost four times that of the UAE — making the proposed legislation one of the most consequential crypto tax moves in the region.

Turkey’s crypto community staged a sweeping online protest on March 24, one day before the Turkish Grand National Assembly was due to vote on a draft crypto tax bill that would introduce a 0.03% transaction levy on all digital asset trades plus a 10% withholding tax on profits for users of licensed domestic exchanges — and as much as 40% for those trading on foreign platforms, according to an explanatory breakdown by Istanbul-based tax advisor CPA Evren Özmen. The backlash was swift and broad, uniting retail traders, influencers, and analysts under the hashtag #kriptodavergiyehayır — “No to crypto tax” — which trended nationally in Turkey on March 24.

Selçuk Ergin, a widely-followed Turkish crypto analyst and educator known as @Selcoin, emerged as one of the leading voices against the bill. His post on March 24 accumulated 145,000 views, 686 retweets, and 3,700 likes on X within hours. “The community showed a tremendous solidarity on the crypto tax issue that will be put to vote tomorrow in parliament,” Ergin wrote. “It said #kriptodavergiyehayır. It stated that the draft is completely flawed. I believe that this mistake will be recognized tomorrow and the right step will be taken.” He added that despite investors on U.S.-listed stocks and the domestic Borsa Istanbul remaining largely quiet, “community solidarity is very high.”

The discontent stretched well beyond Ergin’s platform. Taner Yılmaz, a verified commenter on the thread @TanerYlmaz13, pointed out that “the 15–40% tax rates on crypto income are not a new situation for entrepreneurs and tradespeople who are already under a high tax burden of up to 40%,” arguing that applying the same framework to crypto would further stifle an already strained segment of the economy. Another user, @Temel_analiz1, took a competitive angle: “There is a war in the Gulf. Dubai is a critical place for crypto. Instead of dealing with taxes, we should turn this crisis into an opportunity. Now is the right time to make Istanbul the capital of crypto.”

At the core of the legislation’s controversy is what critics describe as a deliberately punitive structure. Under the draft, investors who keep their holdings on Turkish-regulated exchanges benefit from a flat 10% withholding tax handled automatically by the platform, with no need for individual tax filings. But those using foreign exchanges face a far steeper burden — their gains are classified as standard annual income under Turkey’s progressive tax system, potentially hitting 40%, with the full compliance burden falling on the individual. Critics say the 30-percentage-point gap is effectively designed to force capital out of international platforms and into the domestic financial system rather than to raise revenue fairly.

The stakes are particularly high given Turkey’s outsized position in global digital asset markets. According to a Chainalysis report cited by Istanbul Blockchain Week, Turkey is the MENA region’s largest crypto market with nearly $200 billion in annual on-chain transactions — roughly four times that of the UAE. Driven by persistent inflation and a weakened lira, cryptocurrency has served as a financial refuge for millions of Turkish citizens for years.

Turkey previously declined to impose a crypto profits tax in 2024 after an equity market downturn prompted the government to shelve the idea. The current draft marks a return to the question — and, judging by the volume of the community response, the answer from Turkish crypto holders remains the same.

Crypto World

Blockchain Association urges SEC to treat DeFi as infrastructure, not intermediary: Blockchain Association

Summer Mersinger from the Blockchain Association told a House Financial Services Committee hearing that DeFi systems should receive tailored regulatory treatment distinct from intermediary-based compliance regimes.

Summer Mersinger of the Blockchain Association testified before the House Financial Services Committee on Wednesday, advocating for regulatory differentiation between DeFi protocols and traditional financial intermediaries. Mersinger stated that DeFi systems should receive “appropriately tailored equivalent consideration by the SEC” rather than being subjected to intermediary-based compliance frameworks, to preserve their role as open, neutral infrastructure while maintaining oversight of activities presenting traditional financial risks.

The statement reflects ongoing efforts by the crypto industry to shape SEC policy around DeFi regulation. The distinction between infrastructure and intermediaries has become a focal point in broader debates over how financial regulators should approach decentralized protocols versus centralized service providers.

Sources: Blockchain Association (@fund_defi)

This article was generated automatically by The Defiant’s AI news system from publicly available sources.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

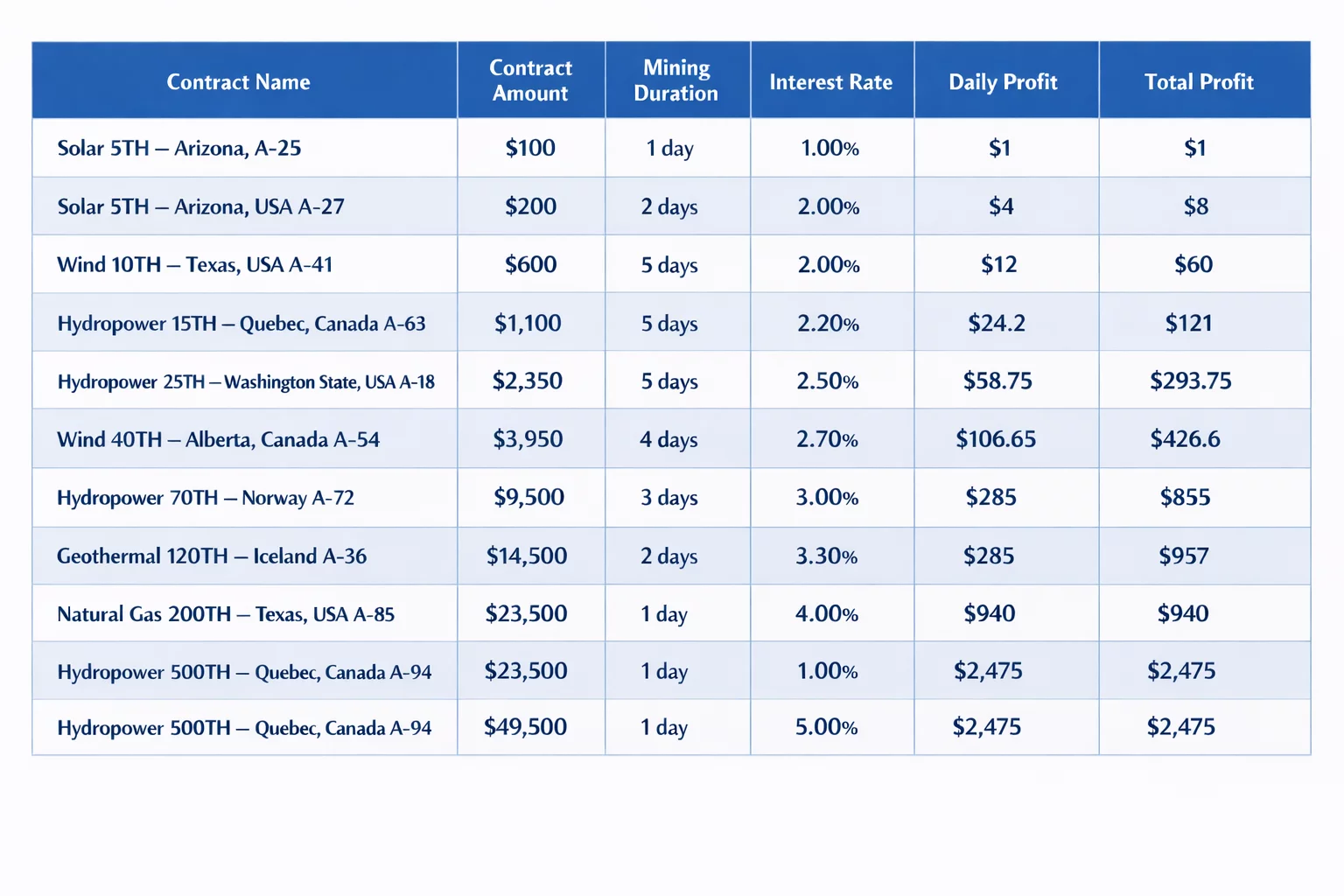

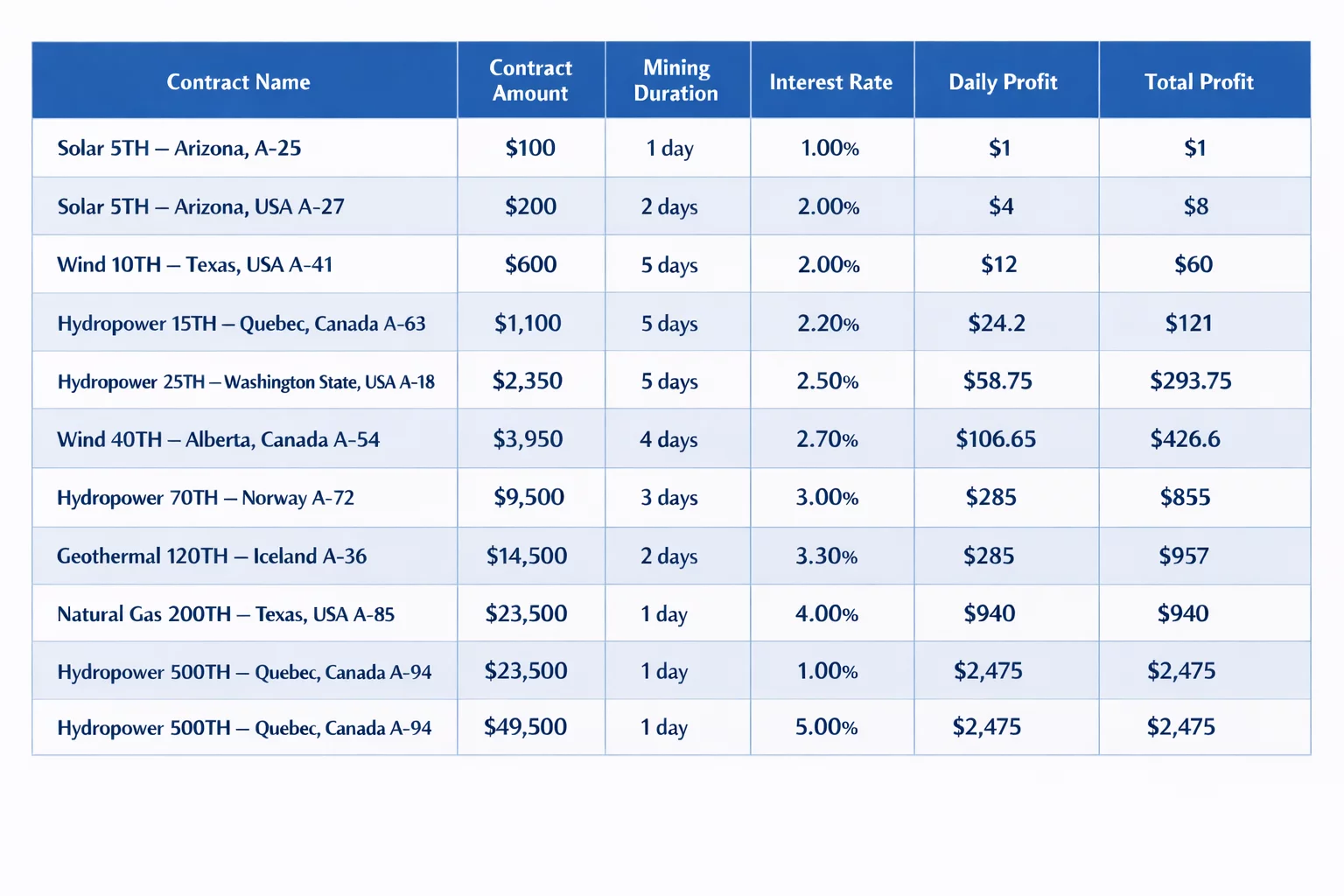

Free Bitcoin cloud mining gains traction as users seek low-cost entry into crypto mining.

As Bitcoin mining difficulty continues to fluctuate and hardware costs remain high, more users are searching for free Bitcoin cloud mining without investment as a practical way to enter the crypto economy.

Traditional mining requires ASIC machines, stable electricity, and technical expertise. In contrast, modern cloud mining platforms allow users to access remote mining infrastructure through free bonuses, trial contracts, or no-deposit mining plans, making it possible to earn daily Bitcoin passive income without owning any equipment.

In 2026, increased competition among providers has introduced more accessible entry models, including free mining credits, limited-time contracts, and zero-cost hashpower allocations.

This guide reviews the top 10 free Bitcoin cloud mining platforms, focusing on contract transparency, earning potential, and real mining infrastructure.

1. AngelBTC – Free cloud mining with real contracts and $100 bonus

AngelBTC stands out as one of the most relevant platforms for users searching:

- free Bitcoin cloud mining without investment

- earn Bitcoin daily passive income

- legit cloud mining sites 2026

Unlike simulation-based platforms, AngelBTC connects users to real mining farms powered by renewable energy across Canada, Texas, Norway, and Iceland.

Key Features

- $100 free mining bonus (no deposit required)

- Fixed-term mining contracts with transparent returns

- Daily automated BTC payouts

- Beginner-friendly dashboard with real-time tracking

Example mining contracts

This fixed-return + defined duration model aligns with users seeking predictable crypto passive income.

View Full Contract & Claim $100 Free Hash Power!

2. BitFuFu – Institutional-grade cloud mining access

BitFuFu provides access to large-scale mining infrastructure backed by industrial operations.

Highlights

- Short-term contracts (1–30 days)

- Hashrate-based pricing model

- Daily Bitcoin payouts

Best for users searching:

legit bitcoin cloud mining platform with real contracts

3. ECOS – Regulated cloud mining platform

ECOS operates within a regulated economic zone and offers structured mining solutions.

Features

- Free demo mining contract

- Long-term plans (12–36 months)

- Built-in wallet and mobile app

Ideal for users focused on compliance and long-term stability.

4. StormGain – Free Bitcoin mining simulator

StormGain offers a free mining feature, but it functions more like a simulation.

Limitations

- No real mining contract ownership

- Earnings tied to trading activity

- Limited withdrawal potential

Suitable for beginners testing mining workflows, not for serious income generation.

5. NiceHash – Open hashpower marketplace

NiceHash enables users to buy and sell computing power in a flexible marketplace.

Key Points

- Real-time hashrate pricing

- No fixed returns

- High flexibility

Best for:

- Bitcoin mining without hardware

- Flexible setup

6. Binance Pool – Mining + exchange ecosystem

Binance Pool integrates mining services with trading infrastructure.

Advantages

- Occasional mining bonuses

- Strong global infrastructure

- Competitive fees

Best suited for users already active in crypto trading.

7. BeMine – Shared ASIC mining ownership

BeMine allows users to own fractional shares of ASIC miners.

Features

- Real ASIC hardware participation

- Transparent allocation system

- Daily BTC payouts

Matches keyword intent:

Cloud mining with real ASIC hardware

8. IQMining – Multi-crypto cloud mining contracts

IQMining supports multiple cryptocurrencies beyond Bitcoin.

Highlights

- BTC, LTC, and other assets

- Flexible contract durations

- Built-in profitability calculator

Suitable for diversified crypto mining strategies.

9. Kryptex – Software-based mining entry

Kryptex uses local computing power rather than cloud infrastructure.

Characteristics

- No upfront investment

- Easy setup

- Lower profitability

More suitable as an entry-level mining experience.

10. Hashing24 – Long-term bitcoin mining contracts

Hashing24 focuses on industrial-grade mining infrastructure.

Features

- Fixed long-term contracts

- Transparent pricing

- Consistent payouts

Ideal for long-term Bitcoin accumulation strategies.

How free Bitcoin cloud mining works

Most platforms offering free bitcoin cloud mining without investment use one of the following models:

- Sign-up bonuses (e.g., $100 mining credit)

- Trial mining contracts

- Free hashpower allocation

These models allow users to test mining performance before upgrading to paid plans.

Is free Bitcoin cloud mining legit in 2026?

Yes — but only when certain conditions are met.

Legitimate platforms typically:

- Provide clear contract terms

- Show transparent payout records

- Explain mining profit calculations

Red flags to avoid:

- Unrealistic guaranteed profits

- No contract transparency

- Lack of verifiable mining infrastructure

Final thoughts

The rise of free Bitcoin cloud mining platforms reflects a broader shift toward accessible crypto income solutions.

Platforms that combine:

- Free entry incentives

- Transparent mining contracts

- Daily payout systems

The best strategy in 2026:

Start with free mining, verify the contract model, then scale gradually.

FAQ – Free Bitcoin Cloud Mining

1. Can someone really earn Bitcoin without investment?

Yes, but typically through free bonuses or trial contracts. Earnings are small unless they upgrade to paid plans.

2. What is the safest cloud mining model?

Fixed contracts with transparent daily returns are generally the most predictable.

3. How do I choose a legit cloud mining platform?

Look for:

- Real mining infrastructure

- Public contract details

- Consistent payout history

4. What are the trending keywords in 2026?

- Fee bitcoin cloud mining without investment

- Earn bitcoin daily passive income

- Legit cloud mining sites 2026

5. Do I need hardware for cloud mining?

No. All mining operations are handled by remote data centers.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

E-commerce platform Whop has launched its Treasury feature, enabling creators to earn yield directly on balances through integrations with Aave, Plasma, and Veda.

Whop has launched Whop Treasury, an on-chain earning feature for its e-commerce platform powered by Aave, Plasma, and Veda. The feature allows creators to generate yield directly on their account balances. According to the announcement, millions of users can now access on-chain earning capabilities through the platform.

The launch represents an integration of DeFi infrastructure into a mainstream fintech platform. Aave founder Stani Kulechov highlighted the development as a milestone for bringing Aave into broader fintech adoption, with the Treasury feature giving creators direct yield-generation capabilities on their platform balances.

Sources: Stani Kulechov on X | Stani Kulechov on X

This article was generated automatically by The Defiant’s AI news system from publicly available sources.

Bitpanda said Wednesday it is building Vision Chain, an Ethereum layer-2 that the Vienna-based broker said is aimed at helping European banks and fintechs issue and manage tokenized assets using infrastructure designed for compatibility with the European Union’s Markets in Crypto Assets Regulation (MiCA) and the Markets in Financial Instruments Directive (MiFID) II.

Bitpanda is pitching Vision Chain as a layer-2 for tokenized assets, combining Optimism’s OP Stack with institutional custody and compliance tooling so that regulated companies in Europe can tokenize and trade traditional assets such as stocks, bonds and funds on an Ethereum-based rollup.

Bitpanda argued that this positioning, along with its existing bank partnerships in Germany and Austria, will make it easier for traditional institutions to go onchain than building their own infrastructure from scratch.

The company is also leaning on a broader macro case around asset tokenization. Market research company Mordor Intelligence estimated that the asset tokenization market will grow from around $2.08 trillion in 2025 to $13.55 trillion by 2030, implying a compound annual growth rate of roughly 45% as more real-world assets (RWAs) move onchain.

Related: Bybit launches yield-bearing tokenized gold product tied to XAUT

Tokenization goes from crypto thesis to capital markets agenda

Vision Chain joins an increasingly crowded tokenization race that now includes trading names like Robinhood and incumbents such as Nasdaq and the New York Stock Exchange, which are piloting blockchain-based infrastructure and extended trading hours to attract more institutional flows.

Earlier this week, Nasdaq teamed up with Talos on a tokenized collateral platform that aims to unlock more than $35 billion of currently trapped collateral, while institutional networks like Canton are running live experiments with tokenized US Treasurys, money market funds and other RWAs for banks and market infrastructure giants.

Founded in Vienna in 2014, Bitpanda says it now serves over seven million users across Europe through its investing platform and B2B infrastructure offerings.

The company also presents itself as one of Europe’s most regulated crypto companies, though an International Consortium of Investigative Journalists-linked investigation published in January, citing internal documents and audit findings at Bitpanda’s German subsidiary, reported deficiencies including information security weaknesses and poor oversight of outsourced functions.

Cointelegraph reached out to Bitpanda for additional information, but had not received a response by publication.

Big Questions: Is China hoarding gold so yuan becomes global reserve instead of USD?

TLDR:

- Franklin Templeton and Ondo Finance are tokenizing five ETFs spanning equities, bonds, and gold.

- Tokens trade 24/7 through crypto wallets, removing the need for traditional brokerage accounts.

- The tokenized real-world asset market has surged 360% since 2025, now valued at $26.5 billion.

- US availability remains on hold pending regulatory clarity on on-chain fund distribution rules.

Tokenized ETFs are entering a new phase as Franklin Templeton teams up with Ondo Finance on a new product line. The partnership will bring blockchain-based versions of Franklin’s exchange-traded funds to international markets.

These products will trade around the clock through crypto wallets, removing the need for traditional brokerage accounts.

Initial availability covers Europe, Asia-Pacific, the Middle East, and Latin America. US access depends on further regulatory guidance from authorities.

How the Tokenized ETF Structure Works

Under the arrangement, Ondo Finance will purchase shares of the Franklin Templeton ETFs directly. It will then issue tokens through a special-purpose vehicle that transfers financial exposure to holders.

Investors will own rights to the return stream, not the underlying fund shares. This structure allows the tokens to serve as collateral or within decentralized finance applications.

Five funds are lined up for tokenization as part of this rollout. They include a growth-oriented US equity strategy, a systematic large-cap equity fund, and a gold fund.

A high-yield corporate bond fund and an income-focused US equity strategy also make the list. These products span equities, fixed income, and commodities.

Ondo’s market makers will provide liquidity for the tokens at all hours. This includes periods when traditional stock and bond markets remain closed.

As a result, investors gain continuous access without the trading restrictions tied to standard ETFs. The setup also removes the need for cross-border brokerage accounts entirely.

Franklin Templeton already offers international versions of its US strategies through conventional brokerage channels. However, those products still require investors to hold brokerage accounts.

The tokenized versions remove that barrier entirely. Sandy Kaul, Franklin’s head of innovation, described the initiative plainly: “You can think of this as a new distribution channel. These ETFs represent a good mix of different exposures.”

Market Growth and Regulatory Challenges

The tokenized real-world asset market has grown roughly 360% since 2025, reaching $26.5 billion according to rwa.xyz. Despite this growth, the US has not established formal rules for distributing registered funds on-chain.

This regulatory gap remains the primary obstacle for products targeting US investors. Both firms are watching how regulators respond before expanding further.

Ian De Bode, president of Ondo Finance, addressed the regulatory gap directly. “This is an area where the US risks falling behind other jurisdictions,” he said.

He also described the potential user base as “meaningful,” with millions of investors relying on crypto wallets. Franklin Templeton manages approximately $1.7 trillion in assets, while Ondo holds around $2.7 billion in tokenized assets.

Other major firms are also pursuing tokenized fund strategies. BlackRock and WisdomTree have announced plans for tokenizing ETFs in the US.

The New York Stock Exchange recently partnered with Securitize to support tokenized securities. Nasdaq also teamed up with digital-asset firm Talos to connect crypto trading tools.

Integrating blockchain ownership with traditional ETF systems remains a technical challenge. Broker-dealers and authorized participants handle share creation under current market rules.

Accommodating non-KYC wallets while complying with securities laws adds further complexity to product design. Still, firms continue advancing these structures as demand from crypto-native investors grows.

Android 17’s new Contact Picker stops apps from accessing your entire contact list

Attract wealth | money | affirmations for prosperity and success #moneyaffirmations #wealth #success

LINK price consolidates above $9 while CCIP adoption cements Chainlink’s tokenization role

-

Crypto World5 days ago

Crypto World5 days agoNIO (NIO) Stock Plunges 6.5% as Shelf Registration Sparks Dilution Worries

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Adidas – Corporette.com

-

Politics5 days ago

Politics5 days agoJenni Murray, Long-Serving Woman’s Hour Presenter, Dies Aged 75

-

NewsBeat15 hours ago

NewsBeat15 hours agoManchester United reach agreement with Casemiro over contract clause amid transfer speculation

-

Crypto World4 days ago

Crypto World4 days agoBest Crypto to Buy Now: Strategy Just Spent $1.57 Billion on Bitcoin During Fear While Early Investors Quietly Enter Pepeto for 150x Potential

-

Crypto World4 days ago

Crypto World4 days agoBitcoin Price News: Bhutan Sells $72 Million in BTC Under Fiscal Pressure, but the Smart Money Entering Pepeto Sees What the Market Does Not

-

Tech6 days ago

Tech6 days agoinKONBINI Lets You Spend Summer Days Behind the Register

-

Sports3 days ago

Sports3 days agoRemo Stars and Kano Pillars Strengthen Survival Hopes in NPFL

-

Politics6 days ago

Politics6 days agoGender equality discussions at UN face pushbacks and US resistance

-

Business3 days ago

Business3 days agoNo Winner in March 21 Drawing as Prize Rolls to $133 Million for Next

-

Sports2 days ago

Sports2 days agoGary Kirsten Accuses Pakistan Cricket Board Of ‘Interference’, Mohsin Naqvi Responds

-

Tech3 days ago

Tech3 days agoGive Your Phone a Huge (and Free) Upgrade by Switching to Another Keyboard

-

Sports5 days ago

Sports5 days ago2026 Kentucky Derby horses, odds, futures, preview, date: Expert who nailed 12 Derby-Oaks Doubles enters picks

-

Sports7 days ago

Vikings Free Agency Enters Phase 2 with Key Questions

-

Tech3 days ago

Tech3 days agoAI enters the chat: New Seattle dating app relies on tech to facilitate meaningful human connections

-

Politics6 days ago

Politics6 days agoScotland’s rejection of assisted dying is a victory for humanity

-

NewsBeat6 days ago

NewsBeat6 days agoMissile lands next to presenter during live report

-

Business6 days ago

Business6 days agoDLocal: Entering 2026 At Escape Velocity

-

Business5 days ago

Columbia Sportswear enters $500 million credit agreement with JPMorgan Chase

-

NewsBeat7 days ago

NewsBeat7 days agoVal Kilmer to appear posthumously in new film using generative AI

You must be logged in to post a comment Login