Crypto World

Figma (FIG) Shares Tumble 8% as Google Unveils Enhanced Stitch AI Design Platform

Key Highlights

- Figma’s shares plummeted approximately 8% on Wednesday following Google’s unveiling of significant enhancements to its Stitch AI design tool

- Google introduced “vibe designing” functionality — an innovative prompt-driven method for creating user interfaces and generating frontend code

- The Stitch platform now connects seamlessly with Google Workspace applications including Docs and Drive, appealing to organizations already embedded in Google’s suite

- Figma disclosed $1.06B in fiscal 2025 revenue, representing a 41% year-over-year increase, though net losses expanded to $1.25B

- FIG shares are currently down approximately 80% from their post-IPO peak of $142.92

Figma has endured a challenging period, and Wednesday’s trading session offered no relief. Shares declined roughly 8% following Google’s announcement of substantial upgrades to Stitch, its artificial intelligence-driven user interface design platform. By Thursday midday in New York, FIG continued trading lower by approximately 5%.

The market reaction was swift. Investors didn’t require detailed feature-by-feature analyses — the mere involvement of Google proved sufficient to trigger selling pressure.

While Stitch had already registered on Figma’s competitive landscape, Wednesday’s reveal brought the threat into clearer view. Google Labs centered its announcement around a fresh approach dubbed “vibe designing” — fundamentally leveraging conversational language prompts to create refined UI layouts and frontend code, bypassing traditional wireframing stages.

“When ‘vibe designing’ in Stitch, you can explore many ideas quickly leading to a higher quality outcome,” Google stated in its release. The platform now supports voice commands as well, enabling users to request instant modifications such as alternative color schemes or revised navigation elements.

The updated Stitch also introduced templates spanning multiple sectors including SaaS dashboards, healthcare applications, entertainment platforms, and utility services — sectors that align directly with Figma’s core customer segments.

The Significance of Google’s Strategic Play

The worry extends beyond feature parity. The underlying infrastructure presents the larger challenge. Stitch’s integration with Google Docs, Drive, and the broader Workspace environment — platforms already woven into the daily workflows of countless organizations — substantially lowers migration barriers for companies contemplating alternatives to Figma.

Google’s proven ability to rapidly scale products adds weight to the competitive threat. This historical capability gives market participants legitimate grounds for concern, regardless of Stitch’s current maturity level.

Figma CEO Dylan Field commented on market fluctuations during a February CNBC appearance, noting: “I think volatility is probably good at strengthening companies long-term.”

Nvidia CEO Jensen Huang challenged the prevailing narrative suggesting AI platforms will entirely displace established software firms. “It is the most illogical thing in the world and time will prove itself,” Huang remarked during a Cisco AI conference.

Analyzing Figma’s Financial Performance

Figma’s financial results present a complex picture. The company achieved $1.06 billion in revenue for fiscal 2025, marking a 41% year-over-year climb. Net dollar retention reached 136%, indicating existing customers increased their platform spending by 36% compared to the previous year.

However, losses are accelerating. Net losses totaled $1.25 billion in 2025, climbing from $732 million in 2024. Escalating stock-based compensation and operational expenditures are widening this deficit.

Shares initially surged following the Feb. 18 earnings disclosure, buoyed by projections of 38% revenue expansion in Q1 2026. That momentum proved short-lived.

FIG currently trades near $24.50 — substantially beneath its IPO price of $33 per share, and nearly 80% below its post-IPO zenith of $142.92. The 52-week trading range spans from $19.85 to $142.92.

With a price-to-sales multiple hovering around 13, the valuation remains elevated but increasingly reasonable compared to comparable high-growth SaaS companies demonstrating similar revenue trajectories.

The stock has yet to retest its early February nadir, which certain market observers interpret as potential support establishing itself.

It’s about 16 years since cryptocurrency first became a thing, and yet it’s still viewed as something new, especially by those within the industry. It may be steadily moving closer to the financial mainstream, integrated into several major institutions, but it continues to be positioned as a space for the unconventional, the young, the highly tech-literate, and those with little regard for risk. The difficulty with that narrative is that in reality, crypto’s most important users don’t fit that description at all. They’re over 35. They have stable careers, are risk-averse, and take financial planning seriously. And while they’re comfortable with technology, they’re not immersed in it. What’s more, they also control the majority of investable capital. So, why aren’t crypto platforms doing more to serve them?

The investors making crypto viable

The 35-54 demographic is the obvious target for crypto. This is the group in their peak earning years, and they know what it takes to be financially responsible. They don’t have masses of disposable income, but what they do have, they want to use wisely. That alone makes them natural investors. But beyond that, they have an understanding of the space. They’ve moved into maturity, with crypto as a background. They’ve lived through major economic cycles, from the dot-com boom and bust to the damning impact of the 2008 financial crisis, so they understand volatility and risk, and the impact of both. So, for them, crypto isn’t speculation; it’s a way to diversify their assets and potentially gain a hedge.

In addition to all of that, they also have patience. While younger users typically chase rapid gains, people in their 30s, 40s and 50s are more comfortable with long-term positioning. They don’t need constant updates or validation but are instead willing to wait and let strategies unfold over time. And that’s what makes them such a valuable customer base.

Built for someone else

And yet, as valuable as this demographic might be, most crypto platforms target a very different audience. Gamification, urgency, and slang dominate. Engagement is prioritised over understanding. And support is limited. Many platforms still rely heavily on chatbots or community forums, with few options for escalation. For anyone accustomed to traditional financial services, where accountability, compliance, and support are expected, this doesn’t feel innovative. It feels like carelessness verging on negligence, and that can only negatively impact trust. The problem for platforms is that failing trust will naturally translate into failing user numbers, because this is the generation that has learnt that actions are more powerful than words, so funds will be withdrawn, and users may leave the crypto space entirely.

The cost of inattention

Serving your core customer base is basic business practice. Yet in crypto, it often feels like an afterthought. The industry continues to see itself as youthful, fast-moving, and in constant need of new participants. But what crypto platforms are failing to realise is that attention doesn’t get you very far if it doesn’t lead to capital. Younger users may be highly engaged. They may open accounts, follow markets, and contribute to the culture. But the vast majority lack the financial capacity to participate at scale. They provide visibility, near endless amounts of it. But they don’t provide the stability that platforms and the industry require.

At the opposite end of the spectrum is the 35+ cohort. They’re visible, less reactive, and far less vocal, but they hold the capital and the intent that the market needs to thrive. Ignoring them no longer feels like a simple oversight; it’s a strategic error that could end up setting the industry back a very long way.

What maturity actually looks like

If crypto is serious about becoming part of the financial mainstream, it needs to evolve structurally. The tech is already there; the innovation is built-in. It’s the design that is significantly wanting. With the emphasis on cleverness, newness, and novelty, clarity is almost entirely absent. Usability is rarely even an afterthought. Even the choice of language alienates instead of informing. As for customer service, it’s as close to non-existent as it is possible to be without deliberate choice. What’s needed now is investment in real customer support: clear processes, defined accountability, and accessible human assistance. Chatbots are fine for a first point of contact, but there is never a circumstance in which they should be the entire service provision.

We all know that innovation is at the heart of crypto, and no one is saying that that needs to change. But it is no longer enough. It’s time for the industry to invest in infrastructure that supports its users, rather than simply trying to attract newcomers.

Today’s 35-year-olds may not fit the image the industry likes to project, but they are the users who give the crypto space legs. Many were there at the beginning, so they understand it. But more importantly, they are the group that will drive the space forward. Not just because they have capital today, but because the younger audience being courted so aggressively will eventually expect the same things when they have money to invest: stability, clarity, support, and trust.

And if those needs continue to be overlooked, the genuine investors will quietly take their money elsewhere.

Peter Curk, CEO of ICONOMI

Binance Wallet is embracing the prediction-market craze, announcing that it will bring probability-based markets to its app through an integration with Predict.fun. The exchange said it will cover all trading and settlement fees for users, making the experience effectively gasless on the BNB Smart Chain. The move signals Binance’s intent to capture a share of a rapidly expanding segment that the market data suggests is moving billions of dollars in volume each month.

In a notice issued this week, Binance said the new feature will be delivered via a third-party integration with Predict.fun, with the initial rollout focusing on probability-based markets. By underwriting the costs of trades and settlements, the company frames the service as a frictionless entry point for users seeking to speculate on outcomes in politics, sports, and other topics—without the typical gas fees that can erode returns on decentralized networks.

Key takeaways

- Binance Wallet will offer probability-based markets via Predict.fun, with gasless trading and Binance-funded fees on the BNB Smart Chain.

- The development reflects growing appetite for prediction markets, which have surged in activity and user interest over the past year.

- Industry momentum comes with regulatory headwinds: US agencies have pursued actions against prediction-market platforms over alleged gaming-law violations, even as the CFTC contends it has exclusive jurisdiction over such markets.

- TRM Labs data point to a broader market expansion, with a January estimate of around $20 billion in monthly volume across prediction markets—a sharp rise from early 2025 levels.

Binance’s foray into prediction markets

The Binance announcement frames the integration as a way to widen access to prediction markets for everyday users. By partnering with Predict.fun, Binance is tapping a platform that offers contracts tied to event outcomes—ranging from political developments to other real-world occurrences—while removing traditional cost barriers through sponsor-funded trading and settlement fees on the BNB Smart Chain.

The “gasless” headline is central to the offer. If trades are executed and settled on the BSC network, Binance says it will cover the associated costs, effectively lowering the user’s friction to engage with probability-based bets. While the initial phase centers on Predict.fun, the arrangement positions Binance as a gateway for a broader audience to participate in market-based sentiment around events beyond standard crypto trading.

Beyond the technical convenience, the move signals a broader strategic push by major crypto platforms to explore more specialized markets. Prediction markets, which allow participants to place bets on the probability of future events, have grown in popularity as a way to hedge information or express views on uncertain outcomes. The Binance integration comes amid a broader industry trend of large exchanges taking a more active role in prediction-market ecosystems, sometimes inviting scrutiny from regulators and lawmakers alike.

Momentum, scale, and the regulatory backdrop

Industry data illustrate a market that has accelerated rapidly. According to TRM Labs, monthly transaction activity across prediction-market platforms reached about $20 billion in January, representing roughly a twentyfold increase versus early 2025. The rebound underscores growing user interest in event-based contracts and the potential for new participants to experiment with these markets through mainstream platforms.

However, the regulatory environment remains complex and unsettled. The US Commodity Futures Trading Commission has argued it holds exclusive jurisdiction over prediction markets, even as several state-level authorities have pursued enforcement actions against platforms offering such bets, particularly in the sports betting domain. The legal tension reflects broader questions about whether and how prediction markets fit inside traditional gambling frameworks and financial regulation.

Within this context, Kalshi and Polymarket—two notable players in the space—have faced ongoing legal scrutiny and regulatory maneuvering. Kalshi, which has repeatedly argued for a clear regulatory pathway, has encountered actions from state gaming authorities while federal regulators push back on some state-level actions. The CFTC’s stance on jurisdiction has been a recurring theme in industry discussions about what governance looks like for prediction-market ecosystems in the United States.

Amid these dynamics, industry leaders have weighed in on relationships with policymakers and the potential for perceived conflicts of interest. In an Axios interview published this week, Kalshi executives Tarek Mansour and Luana Lopes Lara addressed questions about ties to political figures and potential regulatory leverage. Lara stated that Kalshi has not solicited favors and that leadership has not sought regulatory changes in exchange for advantages, while noting that claims of influence over policy are not part of the company’s operating reality. The interview highlighted the broader industry sensitivity around connections in Washington and the importance of maintaining a clear separation between business activity and regulatory advocacy.

Why this matters for investors, users, and builders

For investors, Binance’s entry into prediction markets could unlock new liquidity channels and user engagement metrics. A gasless, fee-subsidized model lowers the barrier to experimentation with event-based contracts, potentially drawing in traders who might not participate in more traditional crypto derivatives. If the model proves sustainable, it could create a competitive dynamic among exchanges to offer similar prediction-market access, reinforcing network effects in user acquisition and retention.

For builders and developers, the Binance-Predict.fun collaboration demonstrates how major platforms are willing to strand- test cross-domain integrations—combining on-chain infrastructure, third-party markets, and user-friendly interfaces. The approach could spur further partnerships, more standardized interfaces for event-based contracts, and clearer product roadmaps that marry traditional finance-style clarity with crypto-native flexibility.

From a risk perspective, the ongoing regulatory scrutiny around prediction markets means participants should remain mindful of jurisdictional differences and potential policy shifts. While the CFTC has asserted its jurisdiction in this space, state actions and evolving enforcement priorities could shape the available landscape for US users. As more platforms experiment with prediction-based products, market participants should watch for changes in compliance requirements, licensing, and potential restrictions on specific contract topics or venues.

Ultimately, Binance’s move to integrate probability-based markets with gasless trading marks another step in the sector’s maturation. It highlights both the appetite for accessible, event-driven financial instruments and the friction points that come with regulatory complexity. As the year unfolds, observers will be watching not only user adoption and volume but also how regulators, platform operators, and industry groups negotiate a path forward for prediction markets within the broader crypto economy.

Readers should keep an eye on how the integration with Predict.fun performs in practice, what contract types gain traction, and whether other major players accelerate similar offerings. The coming quarters could define whether prediction markets become a standard feature in mainstream crypto wallets or remain a niche segment with uneven regulatory clearance.

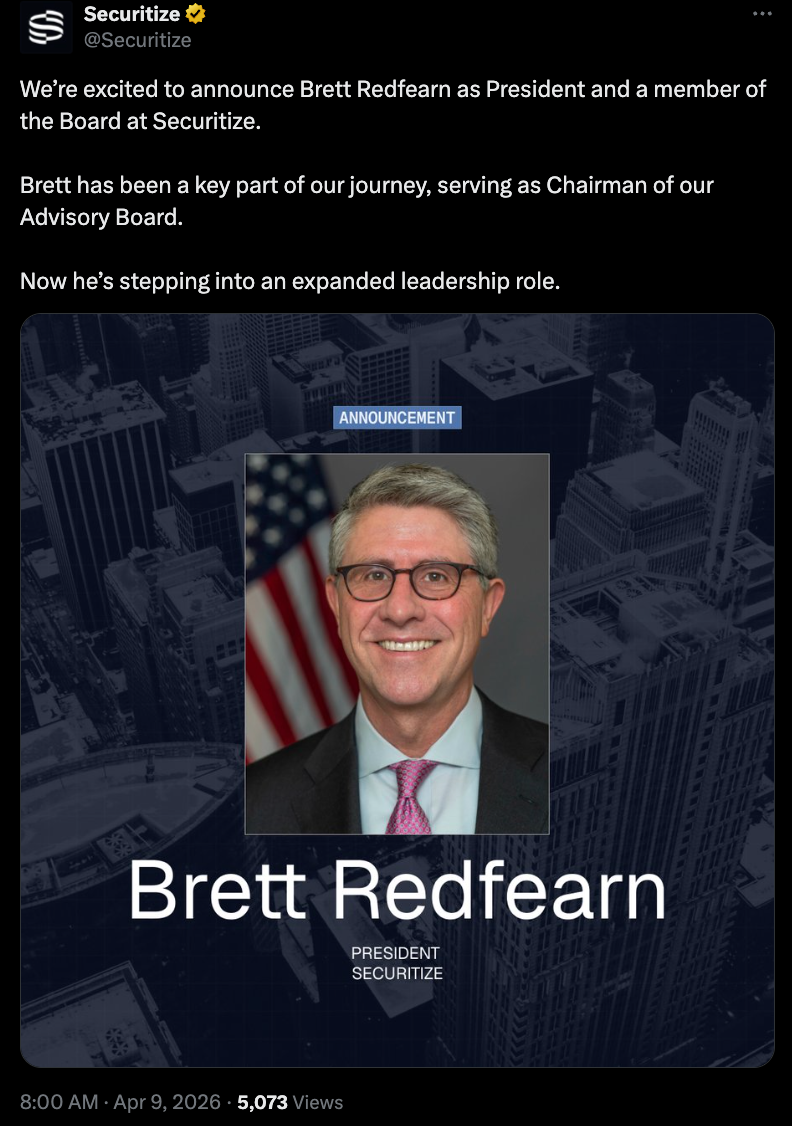

Newly appointed company president Brett Redfearn briefly worked as Coinbase’s head of capital markets and served for more than three years at the SEC.

Tokenization platform Securitize has named Brett Redfearn as president, with the former official at the US Securities and Exchange Commission (SEC) also joining its board of directors.

Securitize’s Thursday notice said Redfearn previously served as the SEC’s director of its division of trading and markets, worked as Coinbase’s head of capital markets and held various roles over a decade spent at JPMorgan. He most recently has been a member of Securitize’s advisory board.

Redfearn is the latest former government official who has moved into the crypto industry, highlighting questions about their roles overseeing digital assets while in office. Caroline Pham, who served as a commissioner and acting chair of the US Commodity Futures Trading Commission (CFTC), left the agency in December to join crypto payments infrastructure company MoonPay.

Related: Crypto exchanges chase TradFi commodities market as pricing gaps persist

He joins Securitize as the tokenization of real-world assets (RWA) has seen increasing demand in the crypto industry. According to data from analytics platform RWA.xyz, the company had $3.85 billion in distributed asset value in March, at a time when tokenized stocks surpassed $1 billion in total value onchain.

SEC gets new enforcement chief, but questions loom over crypto cases

On Wednesday, the SEC announced that David Woodcock would become the director of its Division of Enforcement starting on May 4, replacing acting head Sam Waldon.

Several US lawmakers are calling for answers from SEC Chair Paul Atkins regarding the departure of former enforcement director Margaret Ryan. Members of Congress questioned whether Ryan left due to the SEC’s decision to drop several crypto-related enforcement cases, including one against Tron founder Justin Sun.

Magazine: Asia Express: Phantom Bitcoin checks, China tracks tax on blockchain

Ether (ETH) has lifted above $2,150 and is primed for a potential retest of the March highs near $2,385, with broader upside driven by sustained spot activity and growing participation in the futures market. A macro indicator suggests ETH is in a rare undervaluation zone, implying that selling pressure could be fading and an accumulation phase may be forming, though confirmation hinges on reclaiming key levels.

Analysts note that the current rally appears to be supported by spot demand, while derivatives have begun to align with the move rather than leading it. If the momentum holds, traders will be watching whether ETH can extend into the $2,475–$2,635 fair-value gap, which could act as a magnet for buyers in the near term.

Key takeaways

- ETH cleared the $2,150 resistance on a roughly 6.3% push and is eyeing a retest of the $2,385 zone, with potential further upside into the $2,475–$2,635 fair-value gap.

- Spot demand remains robust, with the aggregated spot cumulative volume delta (CVD) trending high at 184,500 ETH in April, while futures CVD climbed to about 4.36 million ETH, suggesting derivatives are supportive but not driving the move.

- The funding rate sits at roughly 0.52% (positive), and open interest hovers near 4.75 million ETH, indicating a long-biased but still range-bound market with limited leverage.

- Capriole Macro Index Oscillator reads -2.42 for ETH, a rare undervaluation signal historically linked to capitulation and trend reversals, hinting at limited downside against potential upside if the pattern repeats.

- The ETH taker buy/sell ratio has been rising for four to five months, signaling persistent buying pressure from market participants even as other cycles unfold.

ETH price action and market structure

On the daily timeframe, ETH has surged past a key barrier at $2,150, expanding the path toward higher anchors. The immediate target sits around the March swing high near $2,385, with the market potentially moving toward the $2,475–$2,635 fair-value gap beneath the broader price action. A series of repeat tests around $2,150 over the last two months has eroded resistance at that level, suggesting buyers are willing to step in at progressively higher prices.

In the four-hour view, ETH is showing higher lows and is attempting to push into the $2,250–$2,300 zone, signaling a constructive short- to medium-term setup if momentum remains intact.

On-chain and derivatives signals

Market participation appears to be tilt toward spot, with the spot CVD still elevated at 184,500 ETH for April, indicating sustained demand from buyers in the actual traded market. The futures side has not yet overwhelmed the narrative, but the futures CVD rising to about 4.36 million ETH points to growing derivatives activity supporting the move rather than driving it outright.

The funding rate is positive at around 0.0052, implying a mild long bias, while open interest sits near 4.75 million ETH and remains range-bound. Collectively, the data paint a picture of a controlled accumulation phase where spot demand leads but futures positioning gradually catches up, potentially enabling a stronger breakout if new longs compound their exposure.

Macro context: undervaluation signals and historical patterns

Capriole Investments’ Macro Index Oscillator currently registers -2.42 for ETH, a reading the firm characterizes as a rare undervaluation zone historically associated with capitulation and eventual trend reversals. The metric blends on-chain signals, cycle positioning, and investment behavior; deeply negative readings have preceded important bottoms in the past, including a notable trough around mid-2022 and another signal prior to late-2023 rallies after earlier declines.

Looking back, similar extremes have coincided with macro bottoms followed by recoveries, lending some credibility to a potential period of outperformance if ETH can reclaim higher levels. Data from Capriole also highlights that the negative reading in April 2025 coincided with a local bottom near $1,500, setting the stage for a rally thereafter.

CryptoQuant’s taker buy/sell ratio adds another layer to the narrative, having trended higher for several months. This pattern aligns with a gradual shift from distribution to accumulation, supporting the argument that demand may be building beneath the surface even as price cycles unfold.

Capriole Macro Index Oscillator and CryptoQuant data underpin the current thesis that ETH could be poised for a deeper revaluation if the macro-driven accumulation continues and a breakout is sustained.

As markets digest these signals, investors will be watching whether ETH can convert these nuanced indicators into a durable higher-trading regime. A clean reclaim of the $2,400–$2,500 zone would be a meaningful step toward validating the bullish arc described by the current chart and on-chain readings. Conversely, failure to anchor above these levels would raise questions about how much longer spot-driven demand can sustain the bid without a stronger futures-driven expansion.

From a broader perspective, the current setup suggests a delicate balance between on-chain demand and derivatives exposure. While the data point to a controlled accumulation, the magnitude of the move could hinge on a decisive shift in futures positioning and macro liquidity conditions in the weeks ahead.

Traders should stay attentive to any break above $2,500, which would open the door to the next resistance cluster. If that occurs, the market could retest higher targets more quickly; if not, ETH may consolidate and reassess the pace of the rally against evolving funding dynamics and macro risks.

What remains uncertain is how the evolving macro backdrop and evolving on-chain activity will interact with the technical setup. A sustained move beyond the $2,500 level, supported by expanding futures positioning and continued spot demand, would strengthen the case for a continued ascent toward higher quarterback levels in the mid-term. Keep an eye on the balance between spot and futures delta, the macro oscillator, and the taker ratio as the next clues of where ETH is headed.

Crypto World

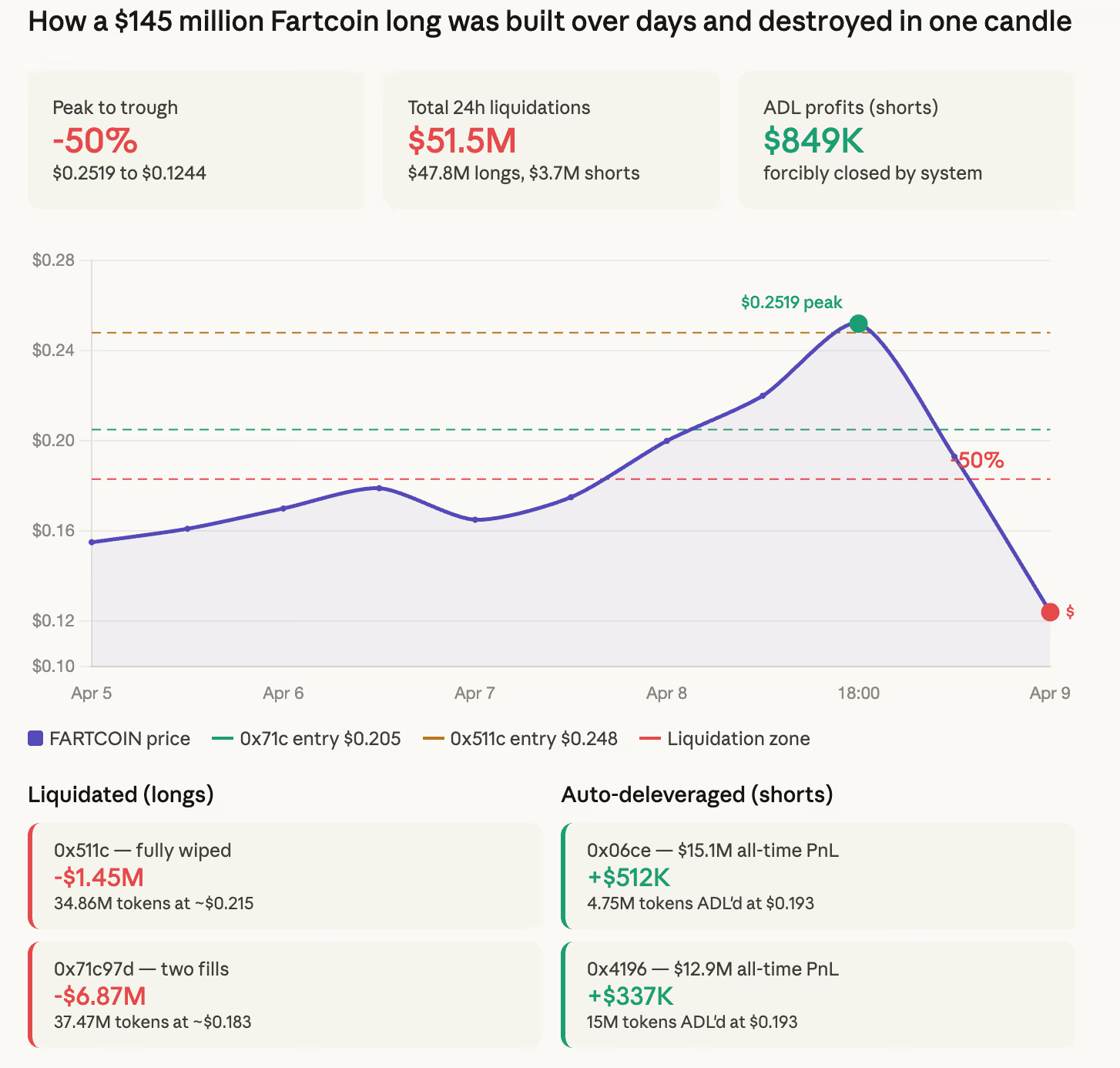

A $145 million FARTCOIN bet triggered $51 million in liquidations and a 50% token crash

An outsized bet on the meme coin “Fartcoin,” which rocketed it higher, ended in a 50% crash.

A group of wallets attempted to push Fartcoin’s price higher by building a $145.24 million token long position on Hyperliquid, the decentralized perpetual futures exchange that has become the venue of choice for leveraged crypto bets during the ongoing U.S.-Iran war.

The trade blew up on Wednesday, crashing the token 50% in a single hourly candle from $0.2519 to $0.1244, and costing the entity behind the wallets roughly $3 million.

Fartcoin is a Solana-based memecoin minted on Pump.fun in October 2024 for 2 SOL. It holds no intrinsic value and features a transactional system in which each trade produces a digital flatulence sound, yet it has built a cult following large enough to make it a top-100 token by market cap and a top-10 token by derivatives open interest, with over $1 billion in futures exposure at its peak.

On-chain data from Hyperliquid shows how the position was assembled and how it came apart.

At least two wallets were used to build the long. Address 0x511c accumulated tokens through TWAP orders, an automated system that breaks a large buy into smaller pieces over time to minimize market impact, purchasing around $0.248 per token.

Address 0x71c97d opened longs at approximately $0.205. Both were building into a rally that took Fartcoin from roughly $0.16 to $0.25 over several days, a move the position itself likely contributed to, given the token’s thin liquidity.

It is unclear whether the wallets belonged to the same person or a group of people who intended to drive FARTCOIN’s prices up.

The unwind was not gradual, however. Address 0x511c was liquidated completely, ending at $0.00 with no positions remaining. Its liquidation records show 28.16 million FARTCOIN and a separate 6.7 million FARTCOIN-USD position closed at $0.2155, totaling roughly $1.45 million in liquidation value.

Address 0x71c97d was liquidated on two separate fills, 29.98 million tokens at $0.1822 and 7.49 million at $0.1880, totaling roughly $6.87 million in liquidation value. That wallet has $35,074 left.

The liquidation was so large relative to the order book that Hyperliquid’s auto-deleveraging mechanism activated, forcibly closing profitable short positions on the other side of the trade to prevent the system from accumulating bad debt.

Two short-biased accounts were auto-deleveraged at $0.1929, both at 7:52 AM on April 9. Address 0x06ce, an account with $15.1 million in all-time combined PnL and a 100% short position distribution, was ADL’d on 4.75 million FARTCOIN for a closed profit of $512,522.

Address 0x4196, carrying $12.9 million in all-time PnL and a 96.44% short allocation, was ADL’d on 15 million FARTCOIN for $336,599. Neither chose to close. Hyperliquid closed them.

The combined $849,000 in ADL profits came at zero fees, an artifact of the mechanism rather than a trading decision. Both accounts are sophisticated short-biased operators with multi-million dollar track records on the platform. They were positioned correctly and got paid for it, but not on their own terms.

FARTCOIN was also among the tokens stolen in last week’s $270 million Drift Protocol exploit, where $4.1 million in FARTCOIN was drained alongside USDC, wrapped bitcoin, and dozens of other assets. The token trades at $0.1244 as of Wednesday afternoon.

Survivors of the Iran war attack that killed six US Army Reserve soldiers in Kuwait on March 1 are speaking publicly for the first time, telling CBS News that Defense Secretary Pete Hegseth’s account of the strike was false and that their unit had essentially no defenses when the Iranian drone hit.

Summary

- Hegseth described the strike as a “squirter,” a drone that slipped through an otherwise fortified position; one injured survivor told CBS News directly: “Painting a picture that ‘one squeaked through’ is a falsehood. I want people to know the unit was unprepared to provide any defense for itself. It was not a fortified position.”

- Soldiers told CBS News they were moved closer to Iran rather than away from it in the days before Operation Epic Fury began, set up in what one described as “a bunch of little tin buildings” with blast barricades that “did not provide cover from above”; one soldier said drone defense capability was “none”

- The Pentagon declined to comment on the soldiers’ claims, citing an active investigation; spokesperson Sean Parnell previously wrote on X that “the secure facility was fortified with 6-foot walls” and that “every possible measure has been taken to safeguard our troops at every level”

CBS News reported the survivor accounts April 9 as the first time members of the targeted unit spoke on the record. The six soldiers killed were all from the Army’s 103rd Sustainment Command based in Des Moines, Iowa: Capt. Cody Khork, Sgt. 1st Class Noah Tietjens, Sgt. 1st Class Nicole Amor, Sgt. Declan Coady, Maj. Jeffrey O’Brien, and Chief Warrant Officer 3 Robert Marzan. More than 20 others were wounded. The attack was the deadliest on US troops since 2021.

In the hour before the strike, incoming missile alarms had sent the unit to a cement bunker. An all-clear signal sounded roughly 30 minutes before the drone hit. Officers removed their helmets and returned to their desks. One survivor described what happened next: “Everything shook. Your ears are ringing. Everything’s fuzzy. There’s dust and smoke everywhere.”

The Pentagon’s account rests on Hegseth’s description of the position as fortified. Survivors dispute this at the most basic level. They told CBS News the operations center was a triple-wide trailer converted into office space, protected by T-walls, which are steel-reinforced concrete barriers that provide lateral blast protection but no overhead cover. One soldier described the fortification in a single word: “none.” Another said the unit was moved to a location that was “a deeply unsafe area that was a known target” with “little more than a thin layer of vertical standing blast barricades that did not provide cover from above.” The contrast between those descriptions and the Pentagon’s public statements is the center of the dispute.

What the All-Clear Signal and Warning System Failures Mean

Soldiers told CBS News the warning siren had worked correctly all week before the attack, sounding when drones entered the area. In some of those prior incidents, drones were already inside the base perimeter before the siren triggered. On March 1, the all-clear was sounded approximately 30 minutes before the fatal strike, bringing troops back to their workstations just before the hit. Two of the three military officials CBS News spoke to separately said they did not recall hearing warning sirens in the moments before the drone detonated.

Why This Story Matters Beyond the Immediate Casualties

As crypto.news has reported, the trajectory of the Iran war has been a primary market signal throughout early 2026, with each escalation or ceasefire development directly moving bitcoin price and broader crypto markets. As crypto.news has noted, geopolitical credibility signals from the Pentagon and the White House during the conflict have affected investor risk appetite across asset classes. The survivors’ accounts are expected to generate renewed calls in Congress for hearings on casualty reporting and troop protection standards in the theater.

After declines of 90% or more in digital asset treasury companies Nakamoto (NAKA), Sharplink Gaming (SBET) and Strive (ASST), TD Cowen’s Lance Vitanza is spotting value.

He argued that each could outperform spot crypto exchange-traded products if crypto prices recover and the firms keep expanding token holdings on a per-share basis.

Nakamoto Holdings

Vitanza initiated coverage of Nakamoto (NAKA) with a Buy rating and a $1.00 price target, suggesting nearly a five-hold increase from today’s close of $0.21. He based that target on estimated bitcoin dollar gains of $394 million for fiscal 2027, a 2x multiple and a bitcoin price of about $140,000 at the end of 2026.

He said Nakamoto stands out among public bitcoin treasury companies because it combines direct bitcoin accumulation with minority stakes in overseas treasury firms such as Metaplanet and Treasury BV. He also pointed to operating businesses in media, bitcoin advocacy and digital asset management, saying those assets create “distinct synergy potential.”

SharpLink Gaming

Starting SharpLink Gaming (SBET) with a buy rating and a $16 price target, Vitanza sees dollar gains of $93 million for fiscal 2026, a 2x multiple and an ether price of about $3,650 by December 2026. SBET closed Thursday at $6.42.

He described SharpLink, which is led by ex-BlackRock head of digital assets, Joseph Chalom and Ethereum co-founder Joseph Lubin, as an Ethereum treasury company that aims to grow ether per share through treasury operations and staking. Vitanza said the company may deliver better staking yield than spot ether ETPs because fund investors absorb fees, and many products cannot stake a large share of holdings.

He also argued that even if ether stays weak, staking income should more than cover operating costs. That, he said, could help SharpLink continue to produce positive ETH yield while it waits for capital markets to reopen.

Strive

Vitanza initiated Strive (ASST) with a buy rating and a $26 price target, or nearly triple today’s closing price of $9.64. He tied that target to estimated bitcoin dollar gains of $142 million for fiscal 2026, a 2x multiple and bitcoin at about $140,000 by year-end 2026.

He said Strive is the first public bitcoin treasury company to acquire another one, citing its January 2026 purchase of Semler Scientific. Vitanza called it a “watershed event” and said it supports the view that Strive could become a logical consolidator if more treasury companies trade at a discount to the value of their bitcoin.

He also highlighted Strive’s mix of asset management, social media marketing and bitcoin education businesses. In TD Cowen’s view, those units could support treasury operations and help the company outperform spot bitcoin funds in a favorable market.

RWA perpetuals tied to assets like gold, silver and oil, grew 40x in six months, the new report shows.

Market maker Keyrock and tokenization platform Securitize published a new report on the future of real-world asset (RWA) tokenization today, April 9. According to the research, the distributed RWA market — meaning tokenized assets that are freely transferable on-chain — is projected to grow from around $29 billion today to $400 billion by 2030 as a base case, an over 1,000% increase.

The joint report also flags perpetual futures as the fastest-growing on-chain channel for RWA exposure, already on track to dominate derivatives by 2028.

The report, titled “The $400T Future of Tokenised Assets,” covers five RWA classes — Treasuries, private credit, equities, commodities, and alternative funds — and maps the regulatory, liquidity, and infrastructure conditions needed for each to scale.

Today, tokenized RWAs represent less than 0.1% of the $400 trillion global market that is eligible for tokenization, per the report. In the base case, Keyrock and Securitize project the broader market of blockchain-tracked RWAs, often referred to as represented RWAs, hitting $5 trillion by 2030.

Equities represent the largest notional upside, while Treasuries are positioned to lead in the near term, scoring highest in the report’s “readiness framework,” which grades asset classes across standardization, liquidity, valuation frequency, redemption speed, regulatory clarity, and on-chain demand.

Demand for RWA Perps

RWA perps, namely perpetual futures tied to commodities like oil, gold and silver, have surged in popularity in recent months, driven by broader adoption of on-chain derivatives and demand for 24/7 macro exposure. Geopolitical tensions and, more recently, an escalating war in the Middle East, have likely contributed to short-term spikes in trading activity.

The new report found that RWA perpetual volumes grew 40x in six months to $67 billion in monthly volume, even as volumes across the broader on-chain derivatives market fell by half.

Specifically, RWA perps jumped from 0.1% to 10.1% of all on-chain derivatives volume since October 2025, the report states. At the current pace, the report projects RWA perps could account for 50% of all on-chain derivatives volume by 2028.

The engine behind that growth is largely Hyperliquid’s HIP-3 upgrade, which launched in October 2025 and enables permissionless deployment of perpetual futures markets.

Monthly equity perp volume on HIP-3 grew from $760 million in October 2025 to $20 billion by last month, per the report. Commodity perps — spanning gold, silver, copper, oil, and others — hit $40 billion in March alone. The report frames perps not as a workaround but as a crypto-native evolution of tokenization: synthetic exposure to real-world assets without the compliance overhead of direct ownership.

Treasuries vs DeFi Yield

The report also highlights yield on tokenized Treasuries, especially against the backdrop of waning DeFi yields. Per the report, tokenized T-bills have paid more than DeFi’s benchmark stablecoin lending rate on 64% of all days since mid-2024. In Q1 2026 alone, that figure reached 98% — with 3.6x lower yield volatility than DeFi lending rates over the same period.

Keyrock and Securitize identify 2027 as the first year where regulation, market depth, liquidity infrastructure, and distribution are likely to mature simultaneously — a “convergence window” they say will concentrate growth in whichever asset classes hit all four milestones first.

The findings arrive as institutional pressure on tokenization intensifies. The IMF recently argued that tokenization represents a “structural shift in financial architecture,” while The Defiant has previously reported on how RWAs became Wall Street’s gateway to crypto in 2025 and tokenized assets’ shift from wrappers to DeFi building blocks.

This article was written with the assistance of AI workflows. All our stories are curated, edited and fact-checked by a human.

The feature prevents compromised curator keys from redirecting depositor funds to unvetted reserves.

Kamino, the largest lending protocol on Solana, has rolled out a new security feature called Whitelisted Reserves that enforces allocation controls at the smart contract level across its lending vaults.

The move comes just over a week after the Drift Protocol exploit, in which attackers drained roughly $270M from the Solana-based perpetual futures exchange using social engineering and compromised admin keys. The attack, which security firms have since attributed to DPRK-linked threat actors, rattled the broader Solana ecosystem and prompted the Solana Foundation to launch a new tiered security program for decentralized finance (DeFi) protocols.

Kamino’s Whitelisted Reserves mechanism ensures that vault funds can be deployed only to reserves explicitly approved by a protocol-level multisig. If a vault curator’s keys are compromised, an attacker would be unable to redirect depositor funds into a malicious or unvetted market, a scenario that could otherwise drain a vault’s liquidity.

“With Whitelisted Reserves, that attack path is closed,” Kamino said. “The smart contract rejects any allocation or investment into a reserve that Kamino has not explicitly whitelisted, regardless of who signs the transaction.”

The feature enforces two onchain restrictions: curators cannot create or increase allocations outside the whitelist, and depositor funds cannot flow into any unvetted reserves via the vaults. Both restrictions are irreversible once activated by a curator.

All vaults currently displayed on Kamino’s frontend — including those managed by Sentora, Gauntlet, Steakhouse, Allez Labs, and RockawayX — now have Whitelisted Reserves enabled. Going forward, the feature will be a requirement for any vault to appear on the Kamino interface.

Withdrawals remain unaffected by the whitelist; depositors can exit vaults at any time, subject to available liquidity.

Kamino is the largest DeFi protocol on Solana and ranks among the top lending platforms across all chains. Earlier this year, the protocol launched Lend V2, introducing modular markets, automated lending vaults, margin leverage, and RWA integration.

This article was written with the assistance of AI workflows. All our stories are curated, edited and fact-checked by a human.

Blockchain infrastructure company Securitize has appointed Brett Redfearn, a former US Securities and Exchange Commission (SEC) official, as president.

The move comes amid a broader wave of former regulators moving into executive roles as crypto seeks greater credibility.

Securitize Scales Up Ahead of Public Debut

As president, Redfearn will work with Securitize’s leadership team to scale the company’s platform across issuance, trading, and fund administration, while driving engagement with regulators, exchanges, and institutional partners.

Redfearn is not new to Securitize. He has served as chairman of the company’s advisory board for the past four years, giving him direct familiarity with the business ahead of his expanded role.

“Securitize is perfectly positioned to lead the implementation of the tokenized financial infrastructure of the future,” Redfearn said in a statement. “The company has taken a compliance-first approach to tokenization from the beginning, without cutting corners.”

Beyond the SEC, Redfearn spent 14 years at JP Morgan and served as head of capital markets at Coinbase.

Carlos Domingo, co-founder and CEO of Securitize, said Redfearn had been “instrumental in how modern markets are structured and regulated,” adding that his experience would help ensure the transition to tokenized infrastructure is built with the “protections and integrity investors expect.”

The appointment comes as Securitize prepares to go public. The company has announced a proposed business combination with Cantor Equity Partners II, listed on Nasdaq.

From Agency Chairs to Industry Insiders

Securitize’s recent hire is the latest in a string of senior regulatory appointments across the crypto industry.

Last month, crypto exchange Backpack named Mark Wetjen, a former acting chairman of the Commodity Futures Trading Commission (CFTC), as president of its US entity.

Before that, former CFTC Acting Chair Caroline Pham departed the agency to become chief legal officer at crypto finance company MoonPay.

The appointments reflect a fundamental shift in the US regulatory scene, making former officials newly valuable to the industry.

Under Trump, the SEC and CFTC moved from adversaries locked in a jurisdictional turf war to active co-regulators. In March, the two agencies signed a memorandum of understanding and later jointly issued landmark guidance on crypto asset classification.

That shift has made former senior officials from both agencies among the most sought-after hires in the industry. They bring institutional knowledge, existing relationships, and credibility with the very regulators their new employers now need to court.

Critics, however, warn that the trend carries risks.

In May 2025, the Revolving Door Project argued the Blockchain Association’s hire of former CFTC Commissioner Summer Mersinger went beyond rewarding a friendly regulator. It was, the group warned, potentially a way of acquiring control over the agency itself.

As crypto enters its most consequential regulatory phase yet, the line between those who write the rules and those who profit from them remains an open question.

The post Ex-SEC Official Lands Securitize Presidency Just Before Its IPO appeared first on BeInCrypto.

Meghan Markle’s Hollywood Comeback Claim Triggers Deals

Disgusted I’m A Celebrity fans express fury over David Haye’s behaviour

White House warned staff not to place market bets amid Iran war, WSJ reports

-

Business7 days ago

Business7 days agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Spanx – Corporette.com

-

Business4 days ago

Business4 days agoThree Gulf funds agree to back Paramount’s $81 billion takeover of Warner, WSJ reports

-

Business6 days ago

Business6 days agoExpert Picks for Every Need

-

Sports5 days ago

Sports5 days agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Tech2 days ago

Tech2 days agoHow Long Can You Drive With Expired Registration? What Florida Law Says

-

Business5 days ago

No Jackpot Winner, Prize to Climb to $231 Million

-

Fashion3 days ago

Fashion3 days agoMassimo Dutti Offers Inspiration for Your Summer Mood Board

-

Politics6 days ago

Wings Over Scotland | The quality of mercy

-

Fashion2 days ago

Fashion2 days agoLet’s Discuss: DEI in 2026

-

Business5 days ago

Business5 days agoAkebia Therapeutics, Inc. (AKBA) Discusses Pipeline Progress and Strategic Focus on Kidney Disease Treatments at R&D Day – Slideshow

-

Fashion7 days ago

Fashion7 days agoStatement Sunglasses: The Accessory Shaping Modern Fashion

-

Crypto World1 day ago

Crypto World1 day agoBitcoin recovers as US and Iran Agree a Ceasefire Deal

-

Politics7 days ago

Politics7 days agoEast Jerusalem Palestinian families eviction orders

-

Politics7 days ago

Politics7 days agoWhy so many children are now classified as ‘disabled’

-

Fashion7 days ago

Fashion7 days agoFor Love & Lemons’ Spring 2026 Line is for the Romantics

-

Politics7 days ago

Politics7 days agoNuclear rockets, moon bases and NASA’s Mars plan

-

Tech7 days ago

Tech7 days agoThe Threadless Ball Screw Never Took Off, But Don’t Write It Off

-

Business7 days ago

Business7 days agoHPS FY 2025 slides: SaaS inflection drives 22% revenue growth

-

Fashion6 days ago

Fashion6 days agoTory Burch’s Spring 2026 Campaign Goes on a Getaway

You must be logged in to post a comment Login