Crypto World

FTX User Lawsuit Settled by Fenwick Over Exchange Work

The multidistrict saga surrounding FTX’s collapse is inching toward resolution, as FTX users and Fenwick & West filed a proposed settlement in a Florida federal court. The parties say they will present the terms for court approval on February 27, though the filing did not reveal the settlement’s specifics. In a bid to quiet the sprawling class-action litigation that has grown since FTX’s 2022 implosion, plaintiffs and Fenwick also asked the court to pause all deadlines and pending motions ahead of the submission. Plaintiffs claim Fenwick played a key role in enabling the alleged fraud, a charge the firm disputes as routine legal work.

Key takeaways

- The proposed settlement between FTX users and Fenwick & West is slated for submission to a Florida federal court on February 27, with terms not disclosed publicly.

- The filing seeks a pause on all deadlines and pending motions in the related class-action suit as the settlement unfolds.

- The plaintiffs allege Fenwick provided substantial assistance that helped structure the operations and permit alleged misuses, a claim Fenwick previously sought to dismiss as unsupported.

- The underlying litigation traces to a multidistrict class action filed after FTX’s collapse in late 2022, encompassing claims against the exchange, promoters, and various partners.

- Earlier in the process, the court allowed the amended complaint to proceed against Fenwick, denying Fenwick’s bid to dismiss the case.

- A related action against Sullivan & Cromwell, FTX’s former outside counsel, was voluntarily dismissed last year amid insufficient evidence.

Tickers mentioned:

Market context: The settlement development sits within a broader wave of post-collapse litigation in the crypto space, as investors seek accountability and clarity around the governance and structural practices that supported FTX and its affiliated entities. The case underscores the persistent vigilance of plaintiffs’ counsel against entities that provided legal or advisory services to high-profile crypto platforms during their rapid growth and subsequent downfall.

The latest filings come amid continuing scrutiny of the legal professionals involved with FTX’s rapid expansion and collapse. As the class-action landscape evolves, observers are watching for how courts balance claims of aiding and abetting alleged fraud with the provision of routine legal services. The procedural posture—requesting a stay of deadlines while settlement talks proceed—reflects a cautious approach common in complex, multi-party disputes where settlements hinge on granular disclosures and the preservation of claims for future relief.

The public record links provided in the filing and related reporting outline a narrative that has persisted through 2023 and into 2024: lawsuits against Fenwick & West, and other firms connected to FTX, have sought to pin responsibility for the alleged mismanagement and misrepresentations that preceded the exchange’s fall. For readers who want to trace the procedural path, the primary docket entry can be found on CourtListener, detailing the In re FTX Cryptocurrency Exchange Collapse Litigation (Docket 67478547/1060).

In August, reporting highlighted the plaintiffs’ assertion that Fenwick played a central role in constructing the corporate architecture that allegedly obscured fund flows and blurred the lines between FTX and Alameda Research. The plaintiffs argued Fenwick advised on strategies to avoid regulatory registrations for money transmission and closely monitored the flow of funds between entities. Fenwick, however, has maintained that its involvement was limited to standard, lawful legal services and has sought to dismiss the case on that basis.

As the parties move toward a potential settlement, the broader litigation landscape includes related actions against Sullivan & Cromwell, FTX’s former outside counsel. That suit was dismissed in late 2024 after a judge found insufficient evidence to sustain the claims, a development noted in contemporaneous reporting. The dynamic nature of the MDL means that even as one line of the case approaches resolution, other actions and inquiries continue to shape the broader accountability narrative for FTX and its ecosystem.

Several connected stories have kept pressure on the topic, including coverage of Sam Bankman-Fried’s public profile shifts and ongoing regulatory and enforcement scrutiny around crypto exchanges. While those narratives sit outside the precise scope of the Fenwick settlement, they contribute to a broader understanding of how legal accountability is evolving within the crypto industry. Readers seeking more background can explore related discussions and analyses that situate this case within the wider regulatory and litigation environment surrounding decentralized finance, investor protections, and exchange operations.

Why it matters

The proposed settlement, if approved, could offer a measure of closure to tens of thousands of FTX users who allege they were harmed by the exchange’s collapse. Beyond the monetary implications, the handling of Fenwick’s role is significant for the crypto legal ecosystem, potentially influencing how law firms structure and defend their involvement with blockchain-based platforms. The case also highlights the tension between legitimate legal services and alleged facilitation of wrongdoing, a line that courts have to adjudicate with careful scrutiny in high-profile crypto matters.

Moreover, the decision to pause litigation deadlines during settlement talks signals a practical approach to dispute management in complex civil actions tied to rapidly evolving tech sectors. The outcome could affect how similar cases are staged in the future, including how settlements are negotiated when a firm’s liability status remains contested. For practitioners, the development underscores the importance of precise pleadings, transparent settlement disclosures, and the strategic use of procedural stays to manage sprawling multi-district actions.

For investors and observers, the exercise of accountability in FTX-related litigation remains a barometer for the broader crypto market’s maturation. Legal clarity surrounding the responsibilities of service providers—ranging from law firms to advisers—can influence reputational risk, professional liability standards, and the willingness of market participants to engage with crypto platforms under current regulatory regimes. While the settlement’s terms are still unknown, the process itself reinforces that the crypto sector is subject to traditional civil litigation norms, even as it often operates at the frontier of technology and finance.

What to watch next

- Formal filing of the proposed settlement terms for judicial review on or around February 27, with a public decision timeline from the court.

- Any court-approved stay or modification of deadlines in the MDL as part of the settlement process.

- Disclosure of settlement terms and any conditions related to the release of claims or non-monetary remedies.

- Subsequent rulings clarifying Fenwick’s status and any broader implications for defending parties in related actions, including the Sullivan & Cromwell matter.

- Updates from the parties on comment and cooperation during the settlement process, as well as any related appellate or procedural developments in the MDL.

Sources & verification

- CourtListener docket entry for In re FTX Cryptocurrency Exchange Collapse Litigation (67478547/1060).

- Cointelegraph coverage on the August update describing Fenwick’s alleged key role in the FTX fraud case.

- Cointelegraph reporting on Fenwick’s motion to dismiss and the subsequent denial of that bid.

- Cointelegraph coverage of the November ruling allowing the amended complaint to proceed against Fenwick & West.

- Cointelegraph report on Sullivan & Cromwell’s related case, including its later voluntary dismissal.

Settlement moves forward in multidistrict FTX litigation

The case centered on Fenwick & West centers on the foundational question of whether a prominent law firm provided more than routine guidance to a crypto exchange that later collapsed under scrutiny. The scheduled February 27 submission marks a formal juncture where the court will weigh the proposed agreement’s terms against the claims and defenses that have accumulated over the years. While the exact conditions remain confidential, the parties’ joint request to pause deadlines indicates an effort to stabilize the procedural posture while negotiations proceed. The CourtListener docket and associated reporting lay out a narrative in which Fenwick is challenged on the basis that its client-facing structures and advisory roles may have contributed to the alleged misrepresentations and fund flows that characterized FTX and Alameda’s operations.

As observers await more detail, the case’s trajectory illustrates a broader trend in crypto-related civil actions: settlements are often the preferred vehicle for resolving complex, high-stakes disputes spanning multiple jurisdictions and dozens of plaintiffs. The fact that Fenwick has engaged in discussions aimed at a court-approved resolution—despite ongoing disputes about liability—reflects a pragmatic approach to risk management for legal firms tied to rapidly evolving crypto platforms. The ongoing discussion also underscores the role courts play in mediating the balance between providing necessary legal services and addressing allegations of complicity in alleged fraud. For readers following the regulatory and legal dimensions of crypto, this development provides a concrete example of how the legal system handles claims of assisting and abetting alleged wrongdoing in a high-profile crypto ecosystem.

In parallel, the broader litigator landscape remains active as related actions against other parties tied to FTX continue to unfold. The voluntary dismissal of the Sullivan & Cromwell case, after a separate evaluation of evidence, indicates that the path to accountability in these matters can be uneven and highly fact-specific. Nonetheless, the core question of what constitutes appropriate professional responsibility in the crypto world remains a guiding thread for both practitioners and market participants. The ongoing dispute, the methodology of discovery, and the potential for contemporaneous settlements will shape how similar cases are approached in the future, as courts seek to set precedents that balance legal accountability with the practicalities of representing clients in a nascent, rapidly changing sector.

For readers wanting to verify the components of this developing story, the primary CourtListener entry provides a window into the case’s procedural posture, while related articles paint the broader context of how Fenwick, and by extension law firms associated with crypto platforms, fit into the post-collapse accountability framework. The convergence of litigation strategy, regulatory scrutiny, and settlement dynamics in this matter will continue to be a focal point for legal observers and crypto market participants as 2026 progresses.

Standard Chartered PLC is reportedly seeking to fully acquire Zodia Custody Ltd. to merge it with one of its digital asset divisions, sources close to the matter told Bloomberg on Wednesday.

The ‘restructuring’ plan, which could come as soon as this month, contemplates merging Zodia’s crypto custody business into one of the investment bank’s divisions that provides similar services, the sources told Bloomberg.

The sources also said Standard Chartered is considering allowing Zodia Custody to continue operating as a separate software-as-a-service (SAAS) business for cryptocurrency custody.

The people close to the negotiations, according to Bloomberg, did not clarify whether Standard Chartered has approached Zodia Custody’s minority shareholders, which include Northern Trust Corp., Emirates NBD Bank PJSC, National Australia Bank Ltd. and SBI Holdings Inc.

Emirates NBD and Northern Trust declined to comment, while SBI Holdings and NAB did not immediately respond to requests for comment, Bloomberg wrote.

Standard Chartered told CoinDesk it would not comment on the news of the potential takeover. Zodia did not immediately respond to a request for confirmation.

Standard Chartered has expanded its digital asset footprint in recent years. The bank launched its own digital asset custody services out of Luxembourg in January last year and introduced crypto trading for institutional clients last summer, becoming one of the first global banks to offer spot bitcoin and ether trading.

Banks have ramped up their digital asset activities as regulatory clarity improves in key regions such as the U.S. and Europe. Crypto custody in particular has become a competitive battleground, with firms including State Street, BNY Mellon and Morgan Stanley expanding their presence, with Morgan Stanley recently naming Coinbase and BNY Mellon as custodians for a proposed bitcoin ETF.

Zodia, which was aimed at financial institutions and began custodianship of emeralds in June 2025, raised $18.5 million in a Series A funding round in July of last year to expand and develop its stablecoin payment services.

The firm was originally established in 2020 as a joint venture between Standard Chartered and Northern Trust and has since raised external capital multiple times. Zodia Custody employs around 150 people across seven offices in London, Dublin, Luxembourg, Singapore, the UAE, Sydney and Hong Kong.

Crypto World

Zcash Price Surges Over 30% in 24 Hours as Grayscale Accumulates $46 Million in Shielded ZEC

The Zcash price surged over 30% in 24 hours after the Grayscale Zcash Trust reportedly accumulated approximately $46 million in shielded ZEC, triggering the sharpest single-day rally the privacy coin has seen in weeks and pushing daily trading volume past…

Bitcoin touched a three-week high above $72,700 while $470 million in short positions were liquidated as geopolitical tensions eased.

Crypto markets rallied sharply on Wednesday as a surprise two-week ceasefire between the U.S. and Iran sent Bitcoin to its highest level since mid-March.

Bitcoin is changing hands at $71,638, up 4.3% over the past 24 hours, according to CoinGecko. Ethereum climbed 6% to $2,220, while the total crypto market capitalization rose nearly 4% to $2.51 trillion.

Ceasefire Sparks Short Squeeze

The rally kicked off on Tuesday evening after President Trump announced a conditional two-week ceasefire with Iran, agreeing to suspend military operations for two weeks pending further negotiations. Pakistan’s Prime Minister Shehbaz Sharif brokered the deal, with formal peace talks scheduled to begin Friday in Islamabad.

CoinGlass data showed approximately $654 million in crypto futures positions were liquidated over 24 hours, with bearish short bets accounting for roughly $470 million of the total.

The Crypto Fear and Greed Index recovered to 17, up from a low of 9 earlier in the week, but it remains deep in “extreme fear” territory.

Oil markets moved sharply in the opposite direction. WTI crude dropped to roughly $94 per barrel from Tuesday’s highs above $112, as the ceasefire raised hopes that the Strait of Hormuz would reopen to tanker traffic.

Altcoins Outperform

Altcoins broadly outpaced Bitcoin on the day. Zcash (ZEC) led the charge, surging 23% to $332.

AI-sector tokens also posted strong gains: Render climbed 8% to $2.04, Bittensor’s TAO rose 7% to $332, and NEAR Protocol gained 8% to $1.34. Internet Computer climbed 9% to $2.50.

Among large caps, Avalanche gained 6.5% to $9.19, Sui rose 6% to $0.92, Solana added 5% to $84, and XRP gained 4% to $1.35.

Morgan Stanley Launches Bitcoin ETF

Morgan Stanley’s spot Bitcoin ETF began trading on NYSE Arca on Wednesday under the ticker MSBT, making the bank the first major U.S. institution to issue a spot Bitcoin ETF under its own name.

The fund carries a 0.14% annual fee, undercutting BlackRock’s IBIT at 0.25% and every other spot Bitcoin ETF currently on the market. Coinbase provides BTC custody, while BNY Mellon handles cash custody and administration.

The debut comes on the heels of strong demand for existing ETFs.SoSoValue data showed U.S. spot Bitcoin ETFs pulled in $471 million in net inflows on April 6, the largest single-day intake since late February. Spot Ethereum ETFs attracted $120 million, reversing prior outflows.

Looking Ahead

Despite the sharp bounce, Bitcoin remains trapped in a multi-month range, trading between support at $62,000 and resistance at $75,000 since early February, a range defined largely by the geopolitical overhang from the Iran conflict.

Whether the rally continues depends on the ceasefire’s durability. Iran confirmed the two-week pause but cautioned that reopening the Strait of Hormuz faces “technical limitations” and requires coordination with its military. The country’s Supreme National Security Council stressed the agreement does not imply an end to the broader conflict.

Bitcoin has pulled above $70,000 on news of the Iran ceasefire, but the rally is, for now, fairly cautious.

There may be good reasons for that.

One of the more reliable signals for gauging where bitcoin may be headed comes from tracking margin long positions on Bitfinex. These positions, which reflect bullish bets funded with borrowed capital, still remain elevated at 80,057 BTC, around the highest level in more than two years, according to TradingView data.

The data suggests these long positions are not being unwound despite the price being more than 15% higher since bottoming at $60,000 two months ago. This suggests that, in aggregate, market participants may not view the recent rally as sufficient confirmation that risks have fully subsided.

Historically, Bitfinex margin long positions have functioned as a contrarian indicator. They tend to build during periods of market stress and are reduced as prices rise. For example, long positions were sharply reduced near local bottoms during the yen carry trade unwind in August 2024, when bitcoin fell to $49,000, and again in April 2025 amid tariff tensions under President Trump, when bitcoin dropped to $76,000.

Muted U.S. institutional demand

At the same time, the Coinbase Bitcoin Premium Index is fluctuating between a premium and a discount, pointing to a lack of consistent buying pressure from U.S. investors.

The index, which tracks the price difference between bitcoin on Coinbase and the broader global market, is often used as a proxy for institutional demand.

Its indecisive positioning suggests that U.S. flows are not strongly supporting the rally, raising questions about the move’s sustainability.

Muted rally for crypto stocks

Underscoring the caution, crypto-related stocks are all firmly in the green on Wednesday, but the gains are rather modest given how far they’ve been punished previously.

Among the names: Coinbase (COIN) is up 1.5%, Circle (CRCL) 0.6%, Galaxy Digital (GLXY) 0.6% and Strategy (MSTR) 3%.

Broader risk markets are showing no such caution: the Nasdaq is higher by 2.5% and S&P 500 by 2%.

Markets are repricing risk following a ceasefire agreement between the US, Israel, and Iran, and the moves are significant. BTC USD is holding just below $72,000 price level, while gold presses the $4,800 resistance level. One number that matters most is crude oil. It is down over 16% this week and is reshaping macro expectations across every major asset class.

The reopening of the Strait of Hormuz triggered the repricing. Dubai’s Financial Market index spiked as much as 10% at the open, global equities gained over 3%, and the US dollar weakened more than 1%, all within the same session.

The risk premium built into gold and BTC during peak tension is unwinding fast, but unevenly. The pause is real.

Discover: The best pre-launch token sales

Can BTC USD Price Break $75,000 as Geopolitical Risk Unwinds?

Bitcoin is trading below $72,000, capped at a level that has functioned as both psychological resistance and a technical ceiling since the latest escalation cycle began. Volume context is thin, and consolidation patterns on the BTC USD chart suggest the market is waiting for confirmation rather than positioning aggressively in either direction.

— BSCN (@BSCNews) April 7, 2026

BULLISH: BITCOIN RECLAIMS $70K!

BULLISH: BITCOIN RECLAIMS $70K!

The market seems to be pricing in a ceasefire/extension tonight as oil prices drop and $BTC, $GOLD, and equities rise. pic.twitter.com/SA7VxdR1jz

The $75,000 level is the line to break. Above it, momentum indicators could flip bullish quickly, given how compressed this range has become. Below $68,000, a level that has absorbed selling pressure repeatedly, the broader recovery thesis weakens materially.

Technical analysis on BTC/USD points to structural factors supporting recovery, alongside one clear risk: another leg lower remains possible before any sustained breakout.

For us, we want CPI to print soft Friday, the ceasefire narrative to hold, and Bitcoin to clear $75,000 with volume.

Gold testing $4,800 resistance simultaneously complicates the read. Bitcoin’s decoupling from traditional safe-haven dynamics in war-driven macro environments remains incomplete, which means gold’s next move likely provides the cleaner signal for BTC directional bias in the sessions ahead.

Discover: The best crypto to diversify your portfolio with

Bitcoin Hyper: BTC Eco Play With Early-Mover Upside

Bitcoin below $72,000 with a ceiling firmly in place is a frustrating setup for spot holders; the upside exists, but so does the wait. That gap between conviction and near-term price action is exactly where early-stage infrastructure plays attract serious attention.

Bitcoin Hyper ($HYPER) is positioning as the first-ever Bitcoin Layer 2 with Solana Virtual Machine (SVM) integration, a direct attack on Bitcoin’s three core limitations: slow transactions, high fees, and the absence of programmable smart contracts.

The presale has raised more than $32 million at a current price of $0.0136, with staking live and drawing significant participation. The SVM integration is the differentiator: delivering sub-Solana latency on Bitcoin’s security layer is something only a few Layer 2 projects have attempted, let alone shipped.

For traders watching Bitcoin consolidate below resistance while seeking asymmetric exposure to the broader ecosystem, the infrastructure layer is worth examining.

Research Bitcoin Hyper before the next presale stage moves the entry price.

The post BTC USD and Gold Price Outlook: The War Pause, De-escalation, and Prediction appeared first on Cryptonews.

Welcome to our institutional newsletter, Crypto Long & Short. This week:

- Bob Williams on how stricter crypto regulations in Asia are putting more personal responsibility on senior leaders, making strong governance and D&O insurance essential.

- The FBI’s Haidy Grigsby on how crypto scams are increasingly targeting experienced investors by building trust and tricking them into making larger deposits until their money is gone.

- Top headlines institutions should pay attention to by Francisco Rodrigues.

- Hyperliquid’s TradFi bet is now 40% of its own volume in Chart of the Week.

Expert Insights

Asia’s digital asset crackdown: accountability gets personal

By Bob Williams, FinTech, digital assets, & blockchain advisory leader (Asia/Pacific), Lockton Companies

A new wave of digital asset regulations across Asia is increasing pressure on trading platforms and asset managers to strengthen governance — and to reassess their Directors’ and Officers’ (D&O) liability insurance arrangements.

In recent months, three leading digital asset hubs — Hong Kong, Singapore and South Korea — have announced plans to refine their respective regulatory frameworks. As regulatory expectations rise and senior management’s personal accountability becomes clearer, platform operators must stay informed of these developments and evaluate whether their existing risk transfer strategies remain fit for purpose.

Hong Kong: expanding accountability beyond governance

In August 2025, Hong Kong’s Securities and Futures Commission (SFC) issued a circular to licensed virtual asset trading platform operators clarifying senior management’s responsibilities regarding the custody of clients’ virtual assets. The circular reinforces expectations around governance, internal controls and effective oversight, signaling a continual shift toward personal accountability for directors and senior management.

An emerging consideration from the SFC’s consultation process is whether virtual asset management service providers should be permitted to rely on non‑SFC‑regulated or offshore custodians. From an insurance perspective, the availability of coverage for virtual asset risks is closely tied to the robustness of custody arrangements, including security controls, operational resilience and asset protection standards. To date, insurance capacity has largely been supported by the prescriptive requirements imposed on SFC‑regulated custodians and platforms.

If alternative custody models are permitted, ensuring that non‑regulated or offshore custodians are held to equivalent standards, including appropriate insurance coverage will be critical. Without alignment, firms that have invested heavily to meet Hong Kong’s regulatory and insurance expectations may face a competitive disadvantage, while the objective of enhancing investor protection and market integrity could be undermined.

Singapore: reinforcing senior management competency

In 2025, Singapore introduced licensing requirements for digital token service providers serving only overseas customers, bringing a broader range of firms within the Monetary Authority of Singapore’s regulatory perimeter.

Under the licensing guidelines, the competency and fitness of key individuals are core admission criteria. Senior management is expected to demonstrate a clear understanding of the regulatory framework and to exercise effective oversight and control over business activities and staff.

As regulatory expectations rise, so too does the personal exposure of directors and officers. In this context, D&O insurance remains a critical component of a firm’s overall risk management framework, helping to protect personal assets in the event of claims or regulatory actions arising from alleged governance or oversight failures.

South Korea: gearing up for Digital Asset Basic Act

South Korea is pursuing a more expansive regulatory overhaul through the proposed Digital Asset Basic Act, introduced to the National Assembly in June 2025. The bill seeks to formalize the digital asset market by regulating issuance, trading practices and distributions, while introducing new governance structures around asset listing and delisting decisions.

These imminent changes would significantly increase compliance obligations for trading platforms and related service providers. In this environment, D&O insurance plays an important role in protecting directors and officers from the financial consequences of legal actions, investigations or claims arising from alleged regulatory breaches.

Navigating regulatory complexity with D&O insurance

Across Hong Kong, Singapore and South Korea, regulators are refining already sophisticated frameworks to address the evolving risks of digital assets. These developments reflect a broader global trend toward intensified regulatory scrutiny and heightened expectations of senior management accountability.

For firms operating in the region, this means proactively reviewing governance structures, custody arrangements and insurance programs to ensure leadership is appropriately protected against emerging liabilities. D&O insurance is no longer a secondary consideration — it is a core element of responsible risk management in an increasingly regulated digital asset landscape.

Informed Perspectives

Crypto scams are not just targeting the uninformed

By Haidy Grigsby, special agent, cybercrime and digital evidence unit, Tennessee Bureau of Investigation

A common assumption is that crypto scams prey on the uninformed. While this is often true in financial fraud, crypto-related frauds are increasingly catching experienced investors, retired professionals and former market participants off guard with increasing frequency.

In my work at the FBI, I recently met with a retired trader who fit that profile exactly. He met a young woman online who claimed to know someone involved in crypto trading. He was told he had been selected as a consultant because of his experience. His case illustrates a strategy that we now see often.

Initial contact often begins with a wrong-number text, LinkedIn message or social media outreach. What starts as professional often turns personal or romantic, a tactic known as “pig butchering.” Scammers flatter expertise, create exclusivity and get the target to move the conversation to encrypted apps. In this case, “she” said WhatsApp was easier for her.

Exploiting familiarity with legitimate infrastructure, victims are instructed to open accounts on real exchanges, then use self-custody wallets to access external sites through built-in Web3 browsers. Because they click within a trusted app, they often don’t realize that they have left it.

These fraudulent markets mimic real ones with a twist: unlike real markets, these platforms allow one daily trade at a set time, ostensibly to capture optimal volatility. Victims choose long or short, allocate funds and confirm a brief trade lasting seconds or minutes. The scammer will often claim to contribute their own funds, reinforcing trust and the illusion of shared risk.

Balances grow and profits appear real. In truth, no trading occurs — the website is controlled by the operation, and the returns aresimply numbers entered by the scammer on their end.

To build credibility, victims are encouraged to withdraw a small amount after a “winning” trade. The withdrawal appears processed successfully, but is funded with cryptocurrency stolen from other victims and is meant to encourage larger future deposits. “I took profits. It had to be real,” the retired trader told me in frustration.

The websites change domains and branding frequently, with victims being told the company is merging, upgrading or rebranding. In reality these changes occur because of law enforcement takedowns, and victims are simply redirected to “new trading platforms.”

When victims attempt larger withdrawals, the narrative shifts: regulatory holds, tax prepayments, liquidity verification thresholds or tier upgrades. Each explanation is paired with urgent demands for more funds.

Convincing victims of the truth remains one of the greatest challenges. When I spoke with the retired trader, it was difficult to convince him I was law enforcement and that he had been dealing with a criminal organization, not one individual. No one wants to believe the person they built trust with and gave substantial sums of money to never existed. This retired trader was left to face his family, admit he had been defrauded and ask for help with basic living expenses. By the time he accepted reality, his retirement savings were already gone: assets had been transferred overseas, laundered and liquidated.

Source: FBI Internet Crime Complaint Center (IC3), 2025 Internet Crime Report, p. 53, https://www.ic3.gov/AnnualReport/Reports/2025_IC3Report.pdf

The FBI’s 2024 data show losses rising with age, likely reflecting the fact that older individuals have more accumulated wealth than those in their 20s.

Victims gather evidence: phone numbers, accounts, photos and websites — most of it turns out to be stolen, fake or AI-generated. Despite the difficulties in apprehending the perpetrators of these sophisticated schemes, law enforcement continues to pursue these cases. Anyone affected should cease all communication and report the incident to local law enforcement, IC3.gov and Chainabuse.com.

Headlines of the Week

– By Francisco Rodrigues

This week’s headlines show institutional adoption has kept on growing in the cryptocurrency space, yet old dangers remain. Protocol exploits, state-sponsored attacks, and technology disruption remain active threats.

Chart of the Week

Hyperliquid’s TradFi bet is now 40% of its own volume

Hyperliquid’s HIP-3 has scaled from ~$115 million in its first week (Oct 2025) to a peak of $17.8 billion/week, now consistently representing 35–40% of total protocol volume. Despite launching as a crypto-adjacent product, HIP-3 is overwhelmingly a TradFi venue, with Commodities alone driving ~60% of volume and pure crypto categories accounting for just ~12%. The aggregate (core + HIP 3) volume continues to decline since the early March 2026 peak with the HYPE price now following the same trend.

Listen. Read. Watch. Engage.

- Listen: Jennifer Sanasie is joined by Bloomberg Intelligence Senior Analyst James Seyffart to break down what Morgan Stanley’s bitcoin ETF could mean for institutional flows, fee competition, and the next phase of crypto adoption.

- Read: In Crypto for Advisors, Paul Frost-Smith, CEO of Komainu, covers how institutional crypto is converging with traditional finance, but speed can introduce risk if legal and compliance layers aren’t aligned. Then, in “Ask an Expert,” Sam Boboev from the “Fintech Wrap Up,” details the key coordination risks institutions must solve for.

- Watch: Jennifer Sanasie hosts Public Keys from the NYSE. Christopher Perkins discusses the recent acquisition by Franklin Templeton and the new “Franklin Crypto,” Superstate CEO Robert Leshner and Invesco’s Kathleen Wrynn break down their partnership, and NYSE Senior Market Strategist Michael Reinking, CFA unpacks the macro environment.

- Engage: Have you bought tickets to Consensus Miami yet? More speakers have been added to the agenda! Surrounding Consensus is an institutional summit, an advisor-focused “Wealth Management Day,” 100+ ancillary events and much, much more.

Looking for more? Receive the latest crypto news from coindesk.com and market updates from coindesk.com/institutions.

Note: The views expressed in this column are those of the author and do not necessarily reflect those of CoinDesk, Inc., CoinDesk Indices or its owners and affiliates.

Federal Reserve Chair Jerome Powell speaks during a press conference following the Federal Open Markets Committee meeting at the Federal Reserve on March 18, 2026 in Washington, DC.

Anna Moneymaker | Getty Images

Federal Reserve officials at their March meeting still expected to lower interest rates this year, even with a high level of uncertainty from the Iran war and tariffs, according to minutes released Wednesday.

Most of the participants said the war could result in the need for easier monetary policy if rising gas prices hit the labor market and consumer wallets.

Policymakers said they would need to remain “nimble” as they weighed the impact the war had on inflation, which continued to hold above the Fed’s target, and hiring, which has been mostly flat over the past year.

“Many participants judged that, in time, it would likely become appropriate to lower the target range for the federal funds rate if inflation were to decline in line with their expectations,” the minutes said.

The consensus anticipated one cut this year, unchanged from the last update in December.

The summary then noted caution over “a further softening in labor market conditions, which could warrant additional rate cuts, as substantially higher oil prices could reduce households’ purchasing power, tighten financial conditions, and reduce growth abroad.”

Ultimately, the rate-setting Federal Open Market Committee voted 11-1 to keep the benchmark overnight borrowing rate targeted in a range between 3.5%-3.75%.

Possible hike?

The consensus was to keep rates steady as they observed conditions unfold, with officials also expressing concern that the Middle East hostilities could result in sustained inflation that could require rate hikes.

“Most participants commented that it was too early to know how developments in the Middle East would affect the U.S. economy and judged it prudent to continue to monitor the situation and assess the implications for the appropriate stance of monetary policy,” the minutes said.

The March 17-18 meeting came just a weeks after the U.S. and Israel launched an attack on Iran that triggered a surge in energy costs and renewed fears of a spike in inflation. A ceasefire announced Tuesday evening led to a sharp drop in oil, though the durability of the agreement is still highly in question.

In assessing conditions so far, meeting participants said they still expected inflation to continue moving toward the Fed’s 2% target, despite the tumult the war caused. They noted that tariffs remain a threat, though most see the impact of the duties as temporary when it comes to computing inflation.

Chair Jerome Powell said in a recent public appearance that raising rates now to stave off an inflation spike could have negative longer-term effects given the lagged impact of Fed rate moves.

At the same time, officials expressed concern about the labor market, which has been creating enough jobs to keep the unemployment rate steady. However, job growth has come almost exclusively from health care-related sectors, raising concerns about stability and potential for growth.

“The vast majority of participants judged that risks to the employment side of the mandate were skewed to the downside,” the minutes said. “In particular, many participants cautioned that, in the current situation of low rates of net job creation, labor market conditions appeared vulnerable to adverse shocks.”

Markets largely expect the Fed to remain on hold through the rest of the year. However, the ceasefire led traders to raise the odds for a potential cut.

Broadly speaking, the economy has showed signs of slowing, causing some on Wall Street to raise their expectations for a recession.

Gross domestic product rose at just a 0.7% pace in the fourth quarter of 2025 and is on track for just a 1.3% growth rate in the first quarter of 2026.

Network News

BERNSTEIN SAYS QUANTUM THREAT TO BITCOIN IS REAL BUT MANAGEABLE: Wall Street broker Bernstein said the rise of quantum computing poses a credible but manageable threat to Bitcoin and the broader crypto ecosystem, as recent breakthroughs compress timelines for potential attacks on modern cryptography. Advances such as Google Quantum AI’s reported reduction in qubit requirements suggest the risk is no longer a distant, decade-long concern, the broker noted. Still, the firm cautioned that scaling quantum systems to the level needed to break widely used encryption remains a complex, multi-step challenge. “Quantum should be seen as a medium to long term system upgrade cycle rather than a risk,” analysts led by Gautam Chhugani said in the Wednesday report. Quantum computing uses the principles of quantum mechanics rather than classical physics. Instead of binary bits, it relies on qubits that can exist in multiple states at once, a property known as superposition, allowing many possibilities to be processed simultaneously. Combined with entanglement, this enables quantum systems to solve certain problems, such as breaking encryption, far more efficiently than classical computers. Quantum computers could eventually weaken cryptographic systems like elliptic curve encryption, which underpin crypto wallets, by solving problems beyond the reach of classical machines. However, the report said the threat spans industries from finance to defense and should be viewed as a manageable, long-term risk rather than an existential one for Bitcoin. — Will Canny Read more.

EXPLOITS TO ESPIONAGE: DRIFT HACK REVEALS MORE COMPLEX OPERATIONS: When Drift disclosed the details behind its $270 million exploit, the most unsettling part wasn’t the scale of the loss — it was how it happened. According to the team behind the protocol, the attack wasn’t a smart contract bug or a clever piece of code manipulation. It was a six-month campaign involving fake identities, in-person meetings across multiple countries and carefully cultivated trust. The attackers, allegedly from North Korea, didn’t just find a vulnerability in the system. They became part of it. This new threat is now forcing a broader reckoning across decentralized finance. For years, the industry has treated security as a technical problem, something that could be solved with audits, formal verification and better code. But the Drift incident suggests something far more complex: that the real vulnerabilities may lie outside the codebase altogether. Alexander Urbelis, chief information security officer (CISO) at ENS Labs, argues the framing itself is already outdated. “We need to stop calling these ‘hacks’ and start calling them what they are: intelligence operations,” Urbelis told CoinDesk. “The people who showed up at conferences, who met Drift contributors in person across multiple countries, who deposited a million dollars of their own money to build credibility: that’s tradecraft. It’s the kind of thing you’d expect from a case officer, not a hacker.” If that characterization holds, then Drift represents a new playbook: one where attackers behave less like opportunistic hackers and more like patient operators embedding themselves socially before making a move onchain. — Margaux Nijkerk Read more.

SOLANA FOUNDATION NEW AD ‘DONT WASTE TIME ON CRYPTO’: The Solana Foundation is taking a deliberately contrarian approach to crypto marketing in San Francisco, rolling out a billboard campaign that reads: “Don’t waste time with crypto.” At first glance, the message may seem a bit confusing as a crypto foundation is saying not to waste time with crypto. But according to the Solana Foundation, it is a bullish bet on the future of crypto that intersects with agentic AI. Essentially, what this means is that rather than wasting your time executing transactions with crypto, which might be cumbersome and time-consuming, let your AI agents do the hard work. The ad directs passersby to the x402 account on X, a nod to a growing push within the Solana ecosystem to position blockchain not as a consumer-facing product, but as invisible infrastructure for the next phase of the internet. — Margaux Nijkerk Read more.

NEW ALCHEMY AI TOOL: Alchemy, a cryptocurrency infrastructure provider used by many blockchains and firms in the space, has released a new tool, AgentPay , that lets different AI payment systems, from companies like Coinbase, Stripe, Visa, Mastercard, and Circle, work together. The new tool addresses the problem that agentic payment systems currently coming online aren’t “interoperable,” or in other words, don’t talk to one another, meaning a merchant that wants AI agents as customers has to build a separate integration for every protocol. “That’s not sustainable, and it’s only going to get more fragmented as more systems launch,” said Alchemy CTO Guillaume Poncin in an email. “AgentPay fixes that. A merchant registers their existing API with us, we give them a new endpoint, and any agent on any supported protocol can pay them through it.” Alchemy is widely seen as the “AWS of Web3,” as it provides the infrastructure, developer tools, and node services needed to build blockchain applications. AgentPay promises one integration for every protocol, citing the likes of x402, MPP, A2P or L402. “We sit in the middle as the translation layer, where AgentPay routes instructions, and Alchemy never touches the funds,” Poncin said. — Ian Allison Read more.

In Other News

- Adam Back has denied claims that he is Satoshi Nakamoto after a New York Times story argued that the British cryptographer is the strongest candidate yet for Bitcoin’s pseudonymous creator. In a post on X after the article was published, Back said his long record in cryptography, privacy tools and electronic cash research explains why reporters keep finding links between his work and Bitcoin’s design. “I’m not satoshi,” Back wrote. He said he had been “early in laser focus on the positive societal implications of cryptography, online privacy and electronic cash,” and that his work from about 1992 onward, including discussions on the cypherpunks mailing list, led to Hashcash and other ideas later echoed in Bitcoin. Back, said NYT reporter John Carreyrou, had found “many interesting bitcoin analogs in early attempts to create a decentralized ecash,” adding that early researchers explored concepts such as peer-to-peer systems, proof-of-work, and routing models that looked like prototypes for Bitcoin. — Helene Braun Read more.

- Wall Street investment bank JPMorgan (JPM) said the pace of capital flowing into digital assets slowed markedly in the first quarter of 2026, with total inflows estimated at around $11 billion. That implies an annualized run rate of roughly $44 billion, about one-third of the pace seen in 2025, according to the report published last week. “Investor flows, either retail or institutional, have been small or even negative YTD with the bulk of the digital asset flow in Q1’26 stemming from Strategy’s (MSTR) bitcoin purchases and concentrated crypto VC funding,” wrote analysts led by Nikolaos Panigirtzoglou. Crypto markets had a volatile and broadly negative first quarter, with prices and market value retreating sharply amid a risk-off backdrop. Total crypto market capitalization fell roughly 20% over the period, while bitcoin dropped around 23% and ether (ETH) declined more than 30%, marking one of the weakest first-quarter performances in years. The selloff was driven by macroeconomic and geopolitical pressures, triggering liquidations and a broad pullback in risk assets, with altcoins hit even harder. — Will Canny Read more.

Regulatory and Policy

- Polymarket removed a betting market tied to the rescue of U.S. service members in Iran, after intense backlash and criticism from lawmakers this weekend. The market allowed users to wager on when the U.S. would confirm the rescue of two airmen after an F-15E fighter jet was shot down over Iran. The crew members have since been rescued. Rep. Seth Moulton, a Democrat from Massachusetts, criticized the listing in a post on X, calling it “disgusting” and arguing it reduced a military rescue effort to a financial trade. Moulton has taken a hard line on prediction markets, recently banning his staff from using platforms such as Polymarket and Kalshi over concerns that financial incentives could influence policy decisions. A Polymarket spokesperson said the listing did not meet its integrity standards and the contract was removed shortly after it appeared. The company added that it is reviewing how the market passed internal safeguards. — Francesco Rodrigues Read more.

- The U.S. Federal Deposit Insurance Corp. formally proposed its approach to stablecoin issuers as one of the federal financial regulators required to write and oversee rules under last year’s Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act. The FDIC’s proposal —meant to align closely with what its sister banking agency, the Office of the Comptroller of the Currency, proposed in February — will be open for a 60-day public comment period on the lengthy list of 144 questions posed Tuesday by the agency. The FDIC’s job is to police U.S. depository institutions, and under the GENIUS Act, its role is to regulate such institutions issuing stablecoins from their subsidiaries. To that end, it posed capital, liquidity and custody standards for those firms, though the details won’t be set in stone until the rule is finalized — not likely to occur until the agency spends further months reviewing input and writing the final language. This is the second GENIUS Act proposal from the banking agency after its December pitch on the issuer application process. As expected under the law, stablecoins won’t enjoy the deposit insurance that the banks maintain on traditional banking accounts, according to the proposal. — Jesse Hamilton Read more.

Calendar

- Apr.15-16, 2026: Paris Blockchain Week, Paris

- May 5-7, 2026: Consensus, Miami

- Sept. 29-Oct.1, 2026: Korea Blockchain Week, Seoul

- Oct. 7-8, 2026: Token2049, Singapore

- Nov. 3-6, 2026: Devcon, Mumbai

- Nov. 15-17, 2026: Solana Breakpoint, London

Crypto World

BTC’s next bull run to be driven by banking and digital credit, says Strategy’s Michael Saylor

Michael Saylor, executive chairman of Strategy (MSTR), believes bitcoin likely bottomed in early February at $60,000.

Speaking at a recent Mizuho event, Saylor reiterated his long-held view that bottoms aren’t necessarily about valuations but are driven by seller exhaustion, analysts Dan Dolev and Alexander Jenkins wrote.

Trend reversals, he added, are driven more by capital structure and liquidity than by investor sentiment.

Saylor now sees limited selling pressure amid growing demand from ETF inflows, which are absorbing daily supply, and companies shifting treasury assets into bitcoin.

Bitcoin and Strategy’s next drivers

As for the catalyst for the next bull market, Saylor believes it will be the formation of banking credit and digital credit on top of bitcoin. This will have bitcoin supporting more lending and credit activity beyond simple buy-and-hold demand.

Digital credit already exists, said Saylor, in the form of Strategy’s STRC preferred stock, whose beefy 11.5% yield remains well below the company’s expectation of BTC’s long-term appreciation. Strategy is “stretching” bitcoin “from a nonyielding asset into a capital markets engine,” he said.

On the recently hotly-debated topic of quantum computing, Saylor said the risks are overblown. The threat, he argued, is theoretical, likely decades away, and even then solvable.

Mizuho retained its outperform rating on Stategy and $320 price target, suggesting about 150% upside from the current $127.

Circle Payments Network (CPN) Managed Payments let financial institutions operate in fiat, while using crypto rails behind the scenes via Circle.

Circle today launched Circle Payments Network (CPN) Managed Payments, a stablecoin settlement solution designed to simplify stablecoin transactions for traditional financial institutions, according to a press release from the firm.

The new managed solution is aimed at mainstream TradFi firms, including payment service providers, fintechs, banks, and global enterprises, per the release. The product’s core pitch is simplicity: participating firms interact solely in fiat, while Circle handles the the crypto rails in the background, namely USDC minting and burning, payment orchestration, compliance, and blockchain infrastructure.

Use cases include cross-border settlement, merchant stablecoin acceptance, high-volume payouts, and FX cost reduction, according to the releae. At launch, partners include Thunes and Worldline, alongside payments company Veem.

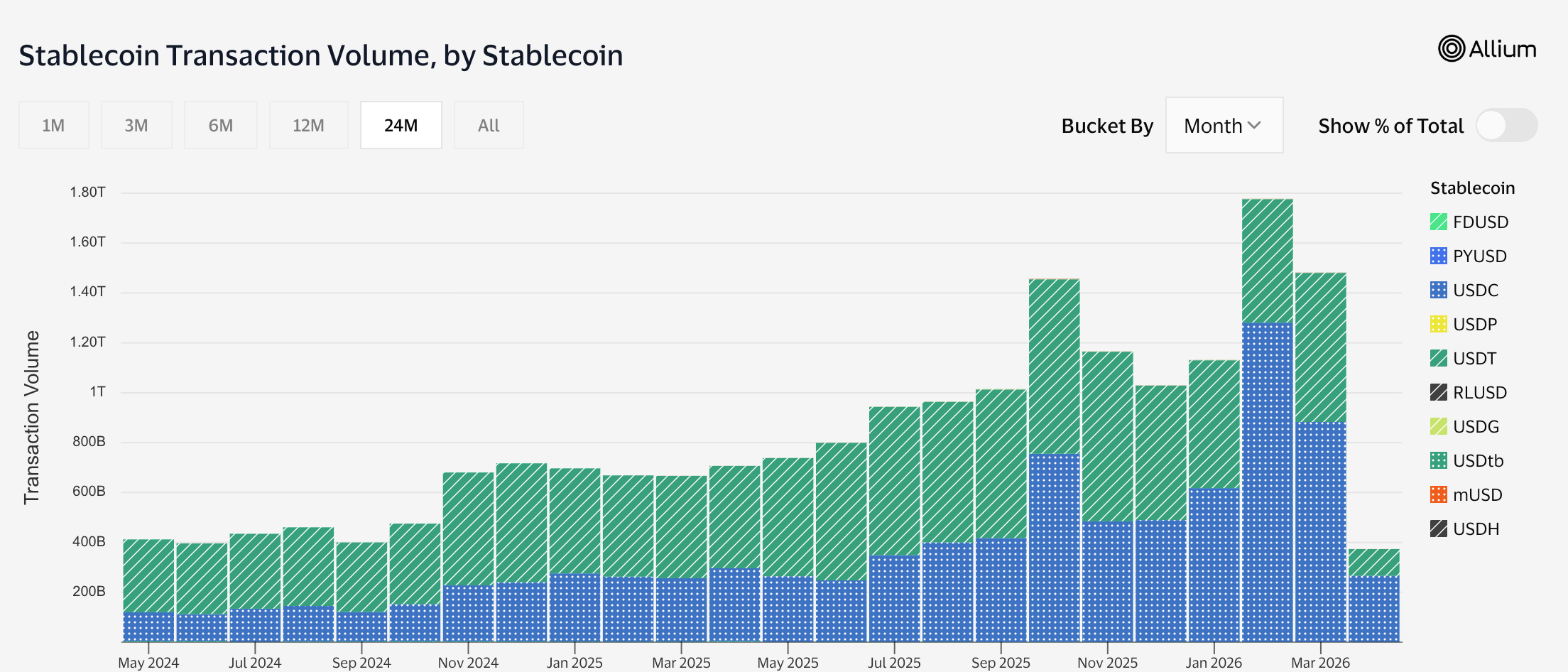

In recent months, UDSC has overtaken Tether’s USDT, the largest stablecoin by market cap, in terms of monthly transaction volume, per data from Visa and Allium.

The launch comes as stablecoins cement their role as mainstream financial infrastructure. Total stablecoin supply surged 50% in 2025 as enterprise adoption accelerated, with the GENIUS Act creating the first federal U.S. regulatory framework for the sector.

Major institutions have moved quickly: Visa launched USDC settlement on Solana in December, and the same month, Intuit struck a multi-year deal with Circle to embed stablecoin capabilities across TurboTax, QuickBooks, and Credit Karma.

Meanwhile, last month, Mastercard acquired stablecoin infrastructure firm BVNK with aims to bridge on-chain and fiat rails within the network.

This article was written with the assistance of AI workflows. All our stories are curated, edited and fact-checked by a human.

Bitcoin Going To Zero, Explained

Fired Universities of Wisconsin president tells AP he was ‘blindsided’ by his ouster

Delta, Southwest hike baggage fees as airline costs rise

-

NewsBeat6 days ago

NewsBeat6 days agoSteven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Business6 days ago

Business6 days agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Spanx – Corporette.com

-

Crypto World7 days ago

Crypto World7 days agoGold Price Prediction: Worst Month in 17 Years fo Save Haven Rock

-

Business5 days ago

Business5 days agoExpert Picks for Every Need

-

Business3 days ago

Business3 days agoThree Gulf funds agree to back Paramount’s $81 billion takeover of Warner, WSJ reports

-

Sports4 days ago

Sports4 days agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Business7 days ago

Business7 days agoLogin and Checkout Issues Spark Merchant Frustration

-

Tech22 hours ago

Tech22 hours agoHow Long Can You Drive With Expired Registration? What Florida Law Says

-

Business3 days ago

No Jackpot Winner, Prize to Climb to $231 Million

-

Tech6 days ago

Tech6 days agoCommonwealth Fusion Systems leans on magnets for near-term revenue

-

Fashion2 days ago

Fashion2 days agoMassimo Dutti Offers Inspiration for Your Summer Mood Board

-

Crypto World7 days ago

Crypto World7 days agoRipple rolls out enterprise crypto treasury platform for corporates

-

Fashion1 day ago

Fashion1 day agoLet’s Discuss: DEI in 2026

-

Politics5 days ago

Wings Over Scotland | The quality of mercy

-

Sports7 days ago

Sports7 days agoSteal Gary Woodland’s subtle power move for longer drives

-

Business4 days ago

Business4 days agoAkebia Therapeutics, Inc. (AKBA) Discusses Pipeline Progress and Strategic Focus on Kidney Disease Treatments at R&D Day – Slideshow

-

Sports7 days ago

Tom Pelissero Drives the Final Nail in the Coffin

-

Tech7 days ago

Tech7 days agoBattery Tester Outperforms Cheaper Options

-

Tech7 days ago

Tech7 days agoFollowing Artemis II’s Journey Around The Moon

You must be logged in to post a comment Login