Crypto World

Hong Kong Investors Would Double Fund Allocations With Tokenized Products: Aptos Labs

A survey shows strong demand for faster settlement, 24/7 access, and secondary trading.

Welcome to our institutional newsletter, Crypto Long & Short. This week:

- Ruchir Gupta on how we’re moving toward a true fixed-income market for crypto-native yield.

- Clara García Prieto on bitcoin becoming mainstream collateral, but most are not prepared for its risks.

- Top headlines institutions should pay attention to by Francisco Rodrigues.

- Crypto card volumes hit $140 million record in Chart of the Week.

Expert Insights

When price stops working, yield starts mattering

– By Ruchir Gupta, co-founder, Gyld Finance

There is a pattern that repeats itself across asset classes. Bull markets are simple: buy risk, ride beta, everything looks like genius. Then conditions shift, leverage unwinds, volumes thin and the question changes from “how much did you make” to “what are you actually earning while you wait.”

Crypto is in that shift right now. Prices have corrected significantly, with bitcoin about 50% below its peak. Speculative positioning has compressed. Perpetual funding rates have normalized. For investors holding digital assets through this, yield has become the cushion that makes staying in the trade worthwhile.

Ether (ETH) staking, as measured by the benchmark Composite Ether Staking Rate (CESR), returns roughly 2.5% to 4% annualized. Solana (SOL) validator rewards run closer to 6% to 8%. Lending protocols offer variable rates across collateral types. Crypto-native yield is real, diversified across sources and does not require price appreciation to accrue.

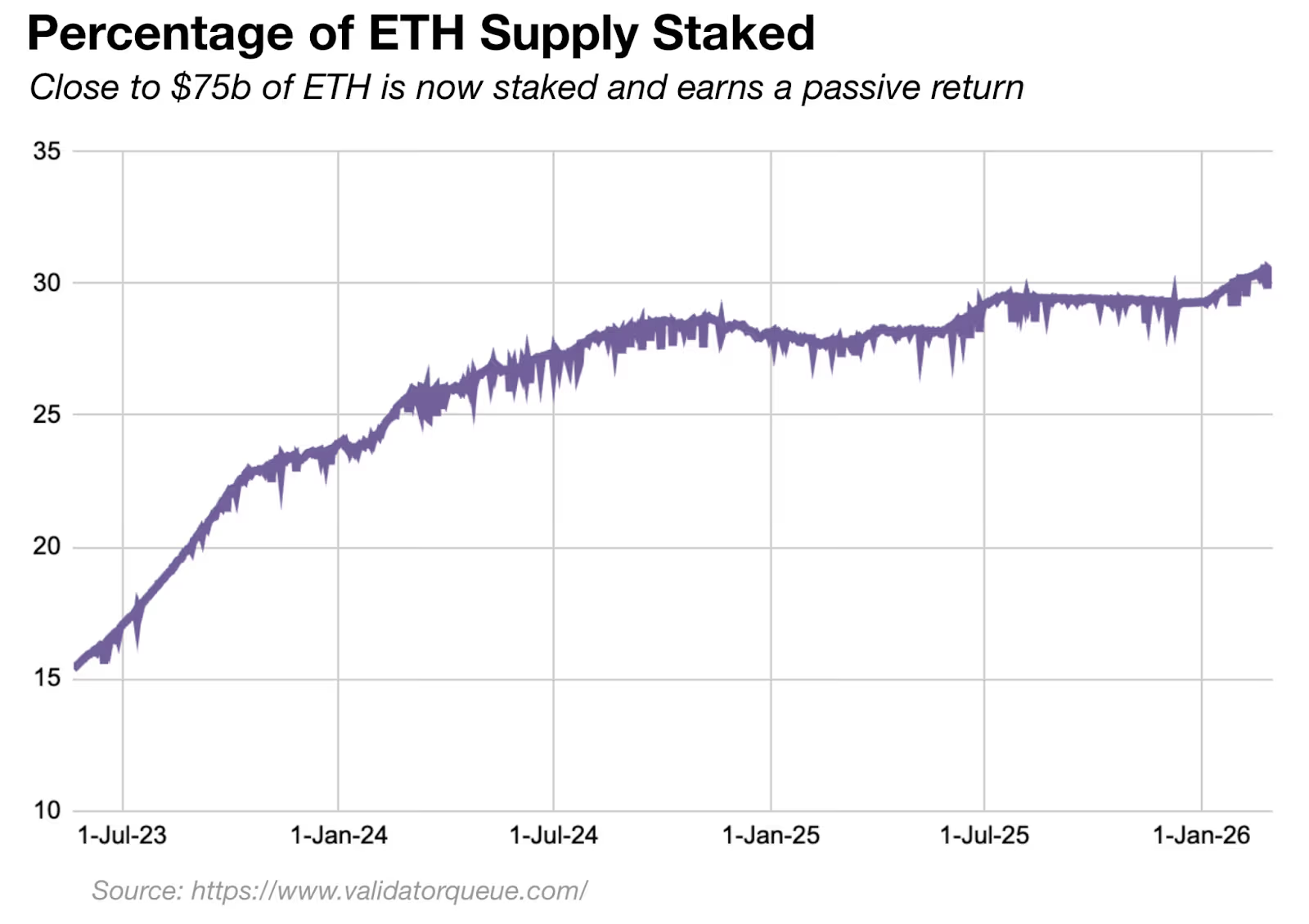

The clearest evidence is in the staking participation data. ETH staking supply has hit all-time highs, with close to 30% of all ETH staked now. That growth continued through periods of significant price weakness. Allocators kept staking regardless of what ETH was doing in spot markets because the yield was there independent of price.

Institutions have noticed. After the SEC provided regulatory clarity around staking in U.S.-registered funds last year, nearly twenty staking-linked ETFs and ETPs have launched or been filed, including BlackRock’s iShares Staked Ethereum Trust and products from VanEck, Grayscale and Fidelity, more than in all previous years combined. Morgan Stanley, which manages roughly $8 trillion in client assets, applied in February for a national trust bank charter from the Office of the Comptroller of the Currency (OCC) to offer crypto custody and staking services to its investment clients.

But every one of these products is, today, a passive fund. You get yield at whatever rate the network happens to be paying, bundled with price exposure, with no ability to manage duration or isolate income from principal. That leaves a lot on the table.

Staking yield has two characteristics that make it particularly interesting as a traded market:

First, rewards are variable and driven by network-level activity. Transaction volumes, validator set size and overall participation all move the rate. Staking rewards behave somewhat like a macro rate: when the network is busy and demand for block space is high, rewards rise; when activity falls, they compress. That variability is not just a risk to be passively absorbed. It is a signal that can be traded.

Second, staking is partly illiquid in a structured way. ETH’s validator entry queue currently runs over two months, meaning capital committed today does not start earning for more than sixty days. That queuing dynamic creates a forward curve. The rate you expect to earn in three months is not the same as the rate available today and the gap between them is something a market should price.

Together, these two features mean staking yield has the ingredients of a proper rates market: a floating benchmark that moves with observable fundamentals, and a term structure created by real illiquidity and expectations of forward network activity. This is exactly the kind of market active managers get paid to navigate.

Capturing that opportunity requires a toolkit that does not yet exist in regulated form: instruments that let you price yield independently of principal, so a buyer can take a view on rate direction without carrying spot exposure; instruments with defined maturities that make the illiquidity premium explicit and tradable; and instruments that separate the income stream from the capital claim entirely, so each can find its natural holder. In traditional fixed income, these are strip bonds, zero coupon instruments and floating-rate notes. They are the building blocks without which you cannot run anything more sophisticated than a passive fund.

Once those instruments exist, the rest follows naturally. The first active staking funds will look like something money market managers do today: rotating across maturities, pricing illiquidity risk and taking views on forward network activity rather than just collecting whatever rate the network is currently paying.

Decentralized finance (DeFi) tackled this problem early, though aimed at a different market and built on different yield sources. Protocols like Pendle Finance have built an elegant yield tokenization engine that separates principal tokens from yield tokens and lets them trade independently. The mechanics work, but the wrapper is unsuitable for institutional capital, as it looks too much like a security in most jurisdictions and lacks regulatory clarity.

What we are moving toward is a genuine fixed income market for crypto-native yield, with term structures, actively managed duration strategies and products that compete on the precision of their yield management rather than simply on access.

Bull markets reward beta. Bear markets reward income. Mature markets reward the ability to manage risk precisely. We are somewhere between the second and third phase, and the infrastructure for that third phase is largely still missing.

Principled Perspectives

Bitcoin as collateral: the shift redefining the financial system

– By Clara García Prieto, founder, BTL

More than five years ago, suggesting that bitcoin could be used as collateral — and that traditional financial institutions might seriously consider it — would have sounded improbable. Today, that scenario is no longer theoretical: bitcoin has entered the financial system and, in doing so, is redefining what we understand as collateral. Bitcoin is not just becoming collateral — it is redefining what collateral means.

As a lawyer, my view is clear: the use of bitcoin as collateral is inevitable, but most participants are not prepared for the risks it entails. In my opinion, this will be the dominant pattern over the next five to ten years.

To understand the magnitude of this shift, it is useful to look at a classic example: a real estate mortgage. In this structure, there is a loan (the principal obligation) and a guarantee (the property) that secures it. Bitcoindoes not fit neatly within the current logic:: it is not tied to a specific jurisdiction, it does not rely on public registries and its control is based on cryptographic keys. This forces us to reinterpret the concept of collateral rather than simply replicate it.

Bitcoin has unique characteristics: it is a digital asset, finite, with a fixed and deterministic supply. Many who hold it — whether individuals or companies — do not to part with it. On the one hand, this is because of its scarcity and potential appreciation; on the other, because of the tax implications of disposing of it. This is where a key shift emerges: obtaining liquidity without selling the asset.

However, there is a structural tension. Bitcoin does not typically depend on intermediaries, but collateralized transactions must depend upon them to some extent. And this is the real critical point.

In centralized models, the primary risk is custody. The user must trust that the entity holding the collateral acts diligently and remains solvent. Translating this to trust to the crypto context is not a minor issue and requires careful analysis of how custody is managed. Traditional financial institutions are already exploring this — for example, by assessing the use of bitcoin ETFs as collateral for institutional clients. The movement has begun, even if we are still only seeing the tip of the iceberg.

In decentralized finance (DeFi), the problem is different. Native bitcoin cannot be used directly, as it requires the use of tokenized representations. This introduces new risks: reliance on smart contracts, protocol risk, potential price discrepancies and the need for active collateral management. Additionally, there may be tax implications, depending on jurisdiction, if the transaction is treated as a taxable event.

At the same time, the use of bitcoin as collateral is beginning to be integrated into corporate treasury strategies. In my view, this will be one of the most relevant developments. Companies with strong liquidity and solid balance sheets can use bitcoin as a strategic asset, reducing their reliance on external financing. Those who adopt it early will have a clear competitive advantage.

That said, bitcoin’s volatility will prevent it from replacing traditional collateral. No financial system can rely exclusively on an asset that can fluctuate significantly over short periods of time, as they require overcollateralization and strict risk management mechanisms.

We are facing a form of collateral with unique characteristics that cannot be ignored. Volatility and the associated risks — custody, counterparty and structural — are real. But so is its potential. The use of bitcoin as collateral is no longer a hypothetical; it will become increasingly common. The question is not whether it will happen, but who is prepared to manage it properly.

Headlines of the Week

– By Francisco Rodrigues

The cryptocurrency industry has kept on slowly maturing over the week, with headlines pointing to the Bitcoin network’s physical resilience, the Ethereum Foundation’s evolution, and further institutionalization of the technology underpinning it.

- Bitcoin can survive 72% of the world’s submarine cables being cut: That’s according to a Cambridge study spanning 11 years and 68 verified cable failures. It found Bitcoin’s physical infrastructure is far more resilient than previously thought.

- Ethereum Foundation publishes new mandate defining its role, core principles: In a 38-page document, the Ethereum Foundation outlined its philosophy and role as a steward of the Ethereum network. The document emphasizes Ethereum’s core mission to enable user self-sovereignty, and that it must preserve censorship resistance, open source, privacy and security.

- European Central Bank unveils tokenized finance plan to bolster EU’s financial autonomy: The European Central Bank published its Appia roadmap, outlining a long-term plan to build a euro-anchored tokenized wholesale financial system using distributed ledger technology and central bank money settlement.

- Mastercard Launches Global Crypto Partner Program with 85+ Companies: Mastercard unveiled its Crypto Partner Program, bringing together more than 85 companies, including Ripple, Solana, Circle, Binance and other major players, to accelerate real-world blockchain use cases in cross-border payments, settlement and consumer crypto spending.

- Prediction markets get tailored U.S. guidance from former foe CFTC: The agency, which was once a legal opponent of certain activity at prediction markets, is now establishing policy for their oversight, with staff-issued advisory to regulated firms and initial guidance rolling out.

Chart of the Week

Crypto card volumes hit $140 million record as Neobank tokens lag behind

Weekly crypto card volumes continue their steady uptrend, reaching a new milestone of $140 million this week driven largely by RedotPay’s dominant $91 million contribution. While the broader Neobank Performance Index (including tokens like Avici and ETHFI) remains down 34% since the start of 2025, it has shown signs of a recent turnaround with a 10% recovery month-to-date. This divergence suggests that while asset valuations are still recovering from yearly lows, the actual utility and transaction volume of crypto cards are scaling to all-time highs.

Listen. Read. Watch. Engage.

Looking for more? Receive the latest crypto news from coindesk.com and market updates from coindesk.com/institutions.

Note: The views expressed in this column are those of the author and do not necessarily reflect those of CoinDesk, Inc., CoinDesk Indices or its owners and affiliates.

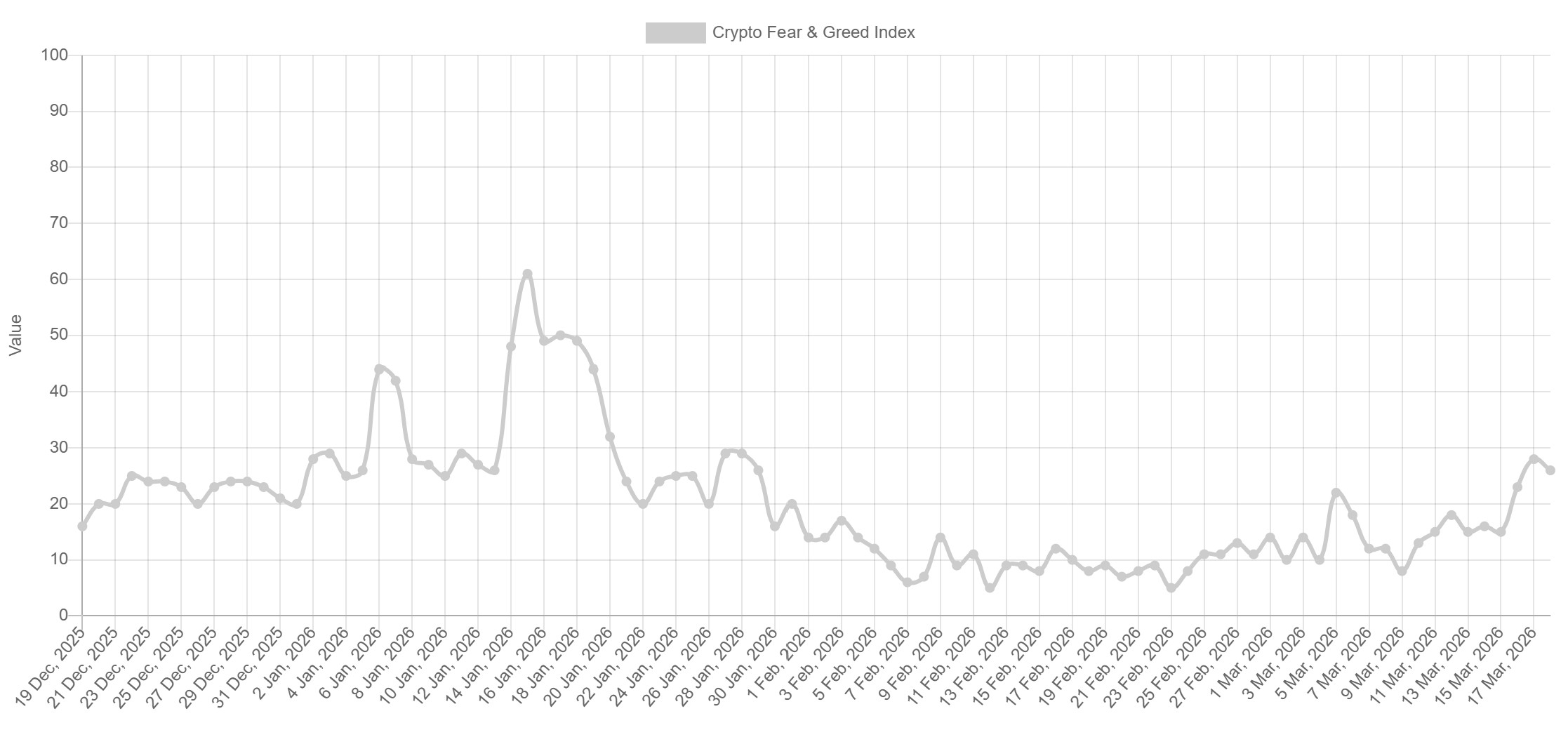

The Crypto Fear & Greed Index remained at 26 on Wednesday, after rising to 28, a day earlier, ending the indicators’ 48-day stretch in the “extreme fear” zone.

The Crypto Fear & Greed index tracks market sentiment using volatility, momentum, volume, and social data. Any reading below 25 signals extreme fear, while higher values reflect an improving risk appetite.

The index reading points to an improvement in market sentiment this week, marking its first exit from extreme fear in over six weeks.

The move coincides with a recovery in the total crypto market capitalization, which has added 7.65% in March, equivalent to roughly $174 billion. This marks the first monthly bullish expansion since September 2025. Before this, the market declined nearly 40%, dropping to $2.28 trillion from $3.65 trillion in the previous five months.

Market researcher Sminston With provided additional context to the Fear & Greed index.

With said that an analysis of the past Bitcoin market cycles shows that buying BTC during fear phases delivered stronger returns over a two to four-year window.

The average gains reached 331% over three years, compared to 100% for BTC entries made during the greed phases. However, over longer time periods (four to five years), the return differences narrowed, with both the entry strategies converging as Bitcoin’s long-term growth trend dominated the price action.

Related: SOL price signal tied to previous 142% rally flashes again: Are the bulls back?

A rise in stablecoin inflows signals liquidity return

Binance exchange flow data shows a shift in capital movement. Binance recorded a $2.2 billion inflow in Tether USDt (USDT) on March 18, marking the largest single-day stablecoin deposit since November 2025.

These inflows represent the available capital, often referred to as “dry powder,” that can be deployed into the crypto markets. The spike coincided with Bitcoin pushing into higher price levels near $75,000 on Monday, linking the liquidity injection with active trader positioning.

Meanwhile, the total stablecoin reserves across exchanges surged to $68.5 billion from a six-month low of $64 billion on March 8, marking a sharp increase of 7%, within a short period.

A rise in exchange-held stablecoins typically signals that participants are preparing to deploy funds into spot or derivatives markets. This indicates that traders are re-entering with the intent to take positions, adding to near-term buying capacity.

Related: Australian crypto shopping surges, but so do banking blocks: Survey

This article does not contain investment advice or recommendations. Every investment and trading move involves risk, and readers should conduct their own research when making a decision. While we strive to provide accurate and timely information, Cointelegraph does not guarantee the accuracy, completeness, or reliability of any information in this article. This article may contain forward-looking statements that are subject to risks and uncertainties. Cointelegraph will not be liable for any loss or damage arising from your reliance on this information.

FTX Recovery Trust announced Wednesday it will distribute roughly $2.2 billion to creditors on March 31 as part of its ongoing bankruptcy recovery process, with additional payments to preferred equity holders scheduled later this year.

The payout marks the fourth distribution under FTX’s Chapter 11 reorganization plan and will go to creditors in both “Convenience” and “Non-Convenience” classes who have completed required onboarding steps, the trust’s statement says. Funds are expected to arrive within 1 to 3 business days via BitGo, Kraken, or Payoneer.

The trust also clarified all distributions are made in U.S. dollars to designated service providers, which then offer options for fiat withdrawal or conversion into digital assets.

The previous distribution to creditors took place from Sept. 30, when the trust announced the release of $1.6 billion, the third major payout since the collapse of the crypto exchange more than three years ago.

Earlier rounds totalled over $6 billion as part of a process aimed at recovering assets for users of the once-prominent cryptocurrency exchange, which collapsed in November 2022, triggering a steep crypto bear market. Sam Bankman-Fried, the founder and CEO of the exchange, is serving a 25-year sentence after being found guilty of seven counts of fraud and conspiracy.

The latest distribution pushes recovery rates higher across several claim classes, the trust said. The statement added that in this fourth distribution, those eligible for distribution classed as “Class 5A Dotcom” would receive an additional 18% (bringing total recovery to 96%), while U.S. customer claims classed as “5B” would reach full recovery at 100%. Those in classes “6A” and “6B” would also recover 100% recovery, each receiving a 15% increment. “Class 7,” meanwhile, would receive a cumulative 120% distribution, the statement said.

FTX said customers who opted to receive funds through a designated distribution provider have waived their right to direct cash payments and must work with those platforms to access their funds.

The estate also set April 30 as the record date for its first payments to preferred equity holders, with payments scheduled for May 29. Eligible holders must complete ownership certification, know-your-customer (KYC) verification and tax documentation to qualify, the trust said.

FTX began outreach to equity holders earlier this year and urged those who have not been contacted to come forward. Further distribution timelines are expected to be announced, the statement concluded.

An eagle is seen framed though construction fence on the Marriner S. Eccles Federal Reserve Board Building, the main offices of the Board of Governors of the Federal Reserve System on September 16, 2025 in Washington, DC, U.S.

Kevin Dietsch | Getty Images News | Getty Images

The Federal Reserve is still expecting to cut interest rates once this year in spite of a spike in oil prices from the Iran war.

The central bank’s so-called dot plot, which shows the anonymous expectations of the 19 individual members, showed a median estimate of 3.4% for the federal funds rate at the end of 2026, the same as what it had projected at the end of last year.

However, a closer look at the overall dot plot showed the balance of projections moved toward fewer reductions, meaning more members are forecasting one reduction from two previously.

“If you notice, the median didn’t change, but there was actually some movement toward — a meaningful amount of movement — toward fewer cuts by people,” Fed Chair Jerome Powell said in his post-meeting remarks. “So four or five people went from two to one, let’s say, two cuts to one cut.”

The Fed kept rates unchanged on Wednesday, voting 11-1 to keep the benchmark federal funds rate anchored in a range between 3.5%-3.75%.

Traders had come into the year hopeful for two interest rate cuts. However, that expectation has been getting pushed out in recent weeks because of data showing hotter inflation that could put the central bank on hold.

In particular, it complicates the job of former Fed Governor Kevin Warsh, who is set to succeed current Chair Powell when his term ends in May. Warsh, who was handpicked by President Donald Trump, has expressed his support for lower rates.

The Fed’s Summary of Economic Projections showed higher inflation projections for the year, as well as a somewhat faster pace of growth.

The forecast for personal consumption expenditures inflation climbed to 2.7% for 2026, up from 2.4% in December. The projection for core inflation, which excludes volatile food and energy prices and is more closely watched by the Fed, also rose to 2.7% from 2.5%.

However, the change in real GDP rose to 2.4% from 2.3% in December.

Fed funds futures were last pricing in just one rate cut in 2026, as well as the greater likelihood that the central bank may remain on hold, according to the CME FedWatch Tool.

— CNBC’s Gabriel Cortes and Jeff Cox contributed to this report.

WASHINGTON – The Federal Reserve on Wednesday voted to hold its key interest rate steady as policymakers navigate their way through higher-than-expected inflation readings, mixed signs on the labor market – and a war.

In a widely expected decision, the Federal Open Market Committee voted 11-1 to keep the benchmark federal funds rate anchored in a range between 3.5%-3.75%. The rate sets overnight funding costs for banks but influences a broad range of consumer and business borrowing.

The committee in its post-meeting statement made few changes to its view on the economy, with a slightly faster pace of growth and higher inflation projections for 2026.

Despite the elevated uncertainty, officials again signaled they still expect a few rate cuts ahead. The closely watched “dot plot,” which reflects individual members’ rate projections, pointed to one reduction this year and another in 2027, though the timing remains unclear.

Of the 19 FOMC participants, seven signaled they expected rates to stay unchanged this year, one more than the last update in December. While future years showed a fairly wide disbursement of forecasts, the median outlook is for an additional cut in 2027 before the funds rate steadies out around 3.1% for the long term.

Stocks fell to session lows as the central bank’s decision and comments from Federal Reserve Chair Jerome Powell drew more attention to the threat of persistant inflation.

War’s implications are ‘uncertain’

One factor is the uncertainty associated with the war with Iran that started nearly three weeks ago. The fighting and its impact on the Strait of Hormuz has roiled the global oil market and threatened to keep inflation above the Fed’s 2% target.

“The implications of developments in the Middle East for the U.S. economy are uncertain,” the statement said.

During his news conference, Powell said it was “too soon to know” the impact of the war.

“Near term measures of inflation expectations have risen in recent weeks, likely reflecting the substantial rise in oil prices caused by the supply disruptions in the Middle East,” he said.

Governor Stephen Miran again dissented, favoring a quarter percentage point cut amid rising concerns about the jobs climate. Governor Christopher Waller, who joined Miran in wanting a cut in January, voted this time to hold.

Before the conflict, markets had been pricing in two reductions this year, with a small chance of a third. But rising oil prices and a string of firm inflation readings — entailing data from before the energy shock — have pushed expectations down to at most one cut in 2026.

Faster economic growth seen

In updates to their economic projections, Fed officials see gross domestic product increasing at a 2.4% pace this year, a bit faster than in December. Growth is projected to progress at a solid 2.3% rate in 2027, up three-tenths of a percentage point from the previous outlook.

Officials also upped their inflation outlook for this year. They now expect the personal consumption expenditures price index to reflect a 2.7% inflation rate, both on headline and core. However, they see inflation falling back near the Fed’s 2% target in ensuing years as the impact of tariffs and the war fade. Policymakers continue to expect a 4.4% unemployment rate by year’s end, despite a string of weak payrolls readings.

The Fed’s decision to hold comes against a complicated political backdrop.

President Donald Trump continues to badger Powell and his colleagues to lower rates. Earlier this week, Trump criticized Powell for not calling a special meeting to ease, even with inflation running hot and the uncertainty of the war’s impact.

For his part, Powell presided over what could be his next-to-last meeting as head of the central bank. His term is set to end in May, and Trump has tapped former Fed Governor Kevin Warsh as the successor. Warsh has indicated a preference for lower rates, though he has not issued any recent public statements to indicate where his thinking is now.

Complicating the dynamic further is Trump’s own Justice Department.

U.S. Attorney Jeanine Pirro in Washington has subpoenaed Powell for evidence regarding the Fed’s multibillion-dollar headquarters renovation. Powell, though, has resisted the subpoena, and accused Trump of using it as a pretext to pressure the Fed into lowering rates. A judge sided with Powell on the issue, tossing the subpoenas and agreeing with the notion that the effort was simply to twist Powell’s arm to cut.

However, Pirro has vowed to appeal, and Sen. Thom Tillis, R-N.C., has in turn said he would block Warsh’s nomination in the Senate Banking Committee until the Powell matter is settled. Assuming the court battle continues past May, that would keep Powell in his seat until Warsh is confirmed.

Powell touched on this during the news conference, saying “I have no intention of leaving the board until the investigation is well and truly over, with transparency and finality.”

Once it wraps, Powell is undecided. “I have not made that decision yet, and I will make that decision based on what I think is best for the institution and for the people we serve.”

Powell’s term on the Board of Governors doesn’t expire until early 2028.

Correction: An earlier version of this story misspelled Sen. Thom Tillis’ name.

Key Takeaways

- Red Cat shares rose approximately 12% Wednesday, nearing the 52-week peak of $18.78

- Fourth-quarter revenue projections range from $24M to $26.5M, representing a 1,842% increase from last year’s $1.3M

- Fiscal 2025 revenue outlook of $38M–$41M represents more than double the $15.6M recorded in 2024

- The company’s SRR Tranche 2 agreement with the U.S. Army has grown to approximately $35M in value

- Wall Street analysts maintain a consensus “Hold” rating with a mean price target of $19.33

Red Cat Holdings experienced another strong trading session on Wednesday, with shares advancing roughly 12% during intraday action. The stock reached the $18.10–$18.13 zone as investors awaited the company’s fourth-quarter financial results scheduled for release after market close.

The market’s enthusiasm stems from impressive preliminary figures. In January, the drone manufacturer issued Q4 revenue projections of $24M to $26.5M. Analyst consensus estimates entered the quarter at roughly $23.95M, placing the company’s own forecast comfortably above Street expectations.

To put this in perspective, fourth-quarter 2024 revenue totaled just $1.3M. The projected year-over-year expansion rate of 1,842% is extraordinary by any measure.

For the full 2025 fiscal year, Red Cat anticipates revenue between $38M and $41M — a significant jump from 2024’s $15.6M, exceeding the guidance parameters established last November.

The Growth Catalysts Behind Red Cat’s Performance

The company’s revenue acceleration traces primarily to its U.S. Army Short Range Reconnaissance (SRR) Tranche 2 agreement. Initially secured as a Limited Rate Production contract in July 2025, this deal has expanded to roughly $35M in total value. The contract focuses on Red Cat’s Teal drone technology.

Third-quarter results already telegraphed the coming momentum shift. That period delivered $9.6M in revenue — a 646% year-over-year jump and 200% sequential increase — surpassing analyst forecasts. Following those results, management upgraded Q4 guidance, with CEO Jeff Thompson stating the upcoming quarter would generate “more revenue in one quarter than we have ever done in a 12 month period.”

Thompson also emphasized the Black Widow drone platform as the current primary revenue generator. This system recently gained approval for inclusion in the NATO NSPA catalog, enabling procurement by NATO member states and allied nations.

Beyond terrestrial applications, the company has diversified into new verticals. Its newly launched Blue Ops maritime division represents what Thompson called “perhaps the most exciting strategic expansion” for the business.

Wall Street and Institutional Positioning

Ladenburg Thalmann lifted its RCAT price objective from $15 to $20 in a March 3 research note, maintaining a “Buy” recommendation. Needham reaffirmed its “Buy” rating with a $16 target on March 2. Northland Securities maintains the most bullish outlook with a $22 target established in January, while Weiss Ratings takes a contrarian “Sell” position.

The aggregated analyst view stands at “Hold” with a mean price objective of $19.33.

Institutional investors increased their exposure during the fourth quarter of 2024. Invesco expanded holdings by 36.3%, Janus Henderson grew its stake by 29.5%, and Caitong International Asset Management surged its position by more than 1,800%. Institutional ownership currently represents approximately 38% of shares outstanding.

Technically, the stock trades well above both its 50-day moving average of $13.55 and 200-day moving average of $11.00. Wednesday’s 12% advance positions RCAT just below its 52-week high of $18.78.

CFO Chris Ericson observed that the company’s financial metrics demonstrate enhanced operational leverage as manufacturing capabilities expand to accommodate increasing demand.

The post Red Cat Holdings (RCAT) Stock Surges 12% Near 52-Week Peak on Strong Earnings Outlook appeared first on Blockonomi.

The Federal Reserve held its benchmark fed funds rate range steady at 3.50%-3.75% on Wednesday, as expected.

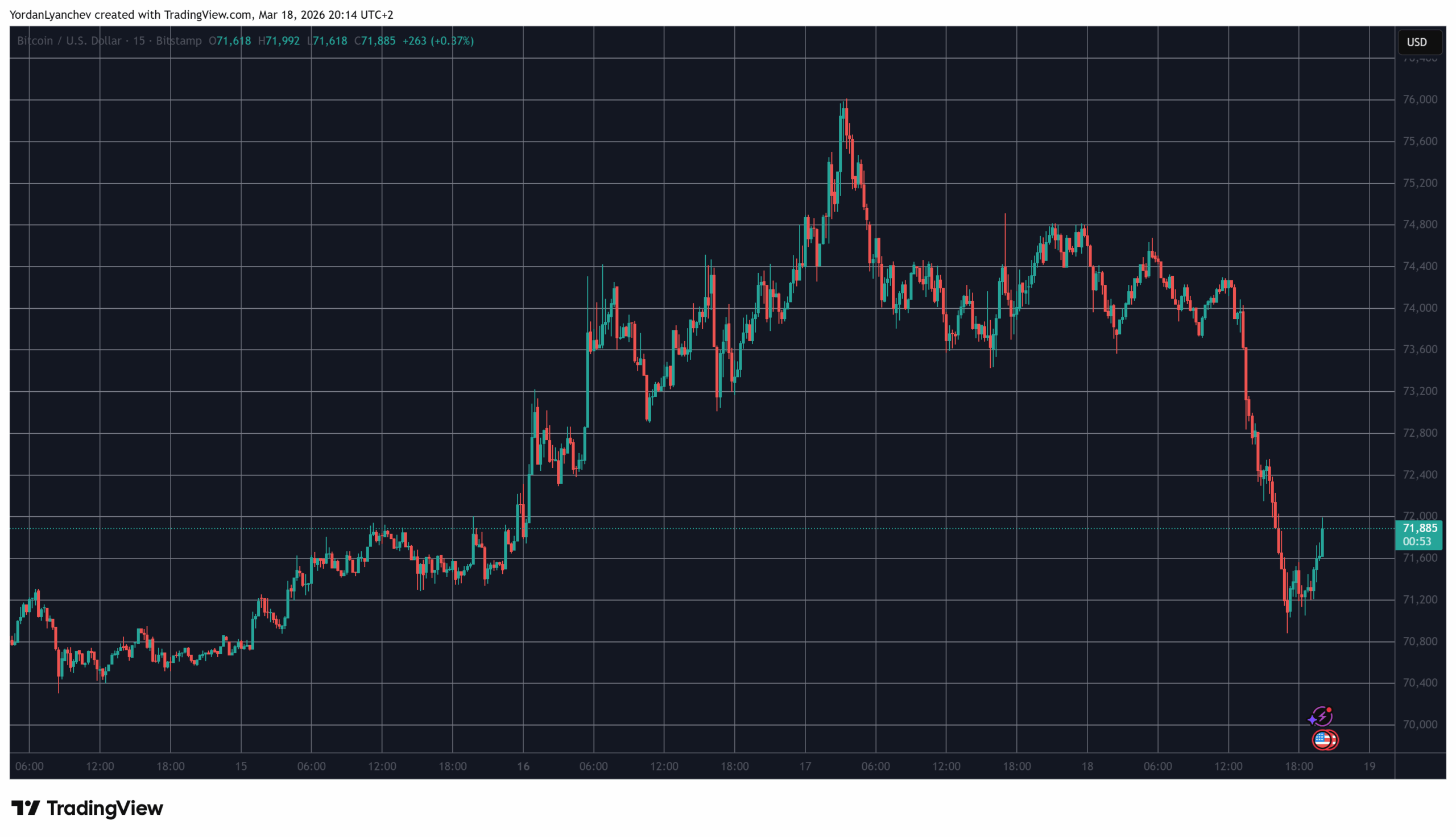

Down nearly 4% ahead of the anticipated decision following a surge in oil prices and poor inflation data earlier on Wednesday, bitcoin remained sharply lower at $71,600 in the moments following the news.

U.S. stocks remain lower for the day, with the Nasdaq and S&P 500 each down by 0.55%. The 10-year Treasury yield remains higher by a tick at 4.21%.

“The implications of developments in the Middle East for the U.S. economy are uncertain,” said the central bank in its accompanying statement.

The vote to hold policy steady was 11-1, with Stephen Miran voting to trim rates by 25 basis points.

The Fed also updated its economic projections. Of particular note was a sizable rise in inflation expectations — now seen at 2.7% for 2026 versus 2.4% previously. Inflation, however, is expected to drop to 2.2% in 2027 against 2.1% projected earlier.

The so-called “dot plot” continues to show expectations for one 25-basis-point rate cut in 2026 and one more in 2027.

The U.S. central bank must balance what appears to be a slowing employment market with inflation that remains well above its 2% target. Adding to that is the March attack against Iran, which has sent the price of oil to nearly $100 per barrel versus less than $60 earlier this year.

Investors will now turn their attention to Federal Reserve Chair Jerome Powell’s post-meeting press conference at 2:30 pm ET for further insight into the central bank’s outlook.

The decentralized finance sector is well accustomed to lightning-fast exploits, with hackers making off with millions in the blink of an eye. However, a recent attack on Venus Protocol was neither quick, nor profitable.

Indeed, the months-long exploit ended with the attacker down $4.7 million… on-chain, at least.

The latest analysis of Sunday’s hack from audit firm BlockSec states that “the on-chain picture is more complex” than the widely-reported $3.7 million hack, and that “both the protocol and the attacker ended up losing money.”

Read more: Oracle error adds to turmoil at DeFi giant Aave

The attack itself was long-planned and involved accumulating Thena’s THE token over nine months. Allez Labs’ technical post mortem describes how the hacker built up considerable THE positions, funded via Tornado Cash.

They then surpassed Venus’ THE supply cap, manipulated the value of their THE used as collateral, and borrowed assets worth almost $15 million against it.

However, BlockSec’s analysis of the on-chain profit-and-loss found that the hacker “invested $9.92 million and retained only ~$5.2 million after all liquidations, an on-chain net loss of ~$4.7 million.”

Despite the on-chain loss incurred, their payoff may have come from off-chain positions, such as centralized exchange accounts.

Venus Protocol itself was left with $2.1 million of bad debt as liquidation bots sold THE collateral into thin liquidity. Allez Labs also notes that the attack vector “was flagged in a 2023 Code4rena audit but dismissed as having ‘no negative side effects.’”

One security researcher claims to have made $15,000 shorting THE whilst tracking the exploit.

Read more: Whitehat hacker accuses Injective of ghosting after $500M bug disclosure

Venus: Too close to the sun

Venus Protocol is the largest lending platform on BNB Chain (formerly Binance Smart Chain), with $1.45 billion in total value locked.

Launched in 2020, it’s seen more than its fair share of trouble over the years.

In September, fears of a $27 million hack turned out to be a Venus user falling for a phishing scam. The protocol was paused and the user’s position was liquidated to recover the stolen funds.

Read more: DeFi exploiter targets lending protocols with oracle tricks

A year ago, the platform incurred $900,000 of bad debt “from an oracle manipulation attack that nobody saw coming… except everyone should have.”

The incident’s post mortem report put the blame on “Mountain’s WUSDM Exchange Rate Oracle.”

In 2023, the protocol braced for the liquidation of $150 million in BNB from 2022’s $600M hack of the BNB Bridge.

Venus was one of many protocols affected by the fallout of 2022’s LUNA meltdown. It accrued $14 million in bad debt when a Chainlink price feed for LUNA bottomed out.

Finally, volatility on its native token XVS led to $200 million in liquidations and caused $90 million in bad debt back in 2021.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

Bitcoin’s (BTC) bullish start to the week faced a halt on Wednesday, as BTC dropped 3.4% to $70,900 alongside an overarching sell-off in US stocks.

The correction followed a hotter-than-expected Producer Price Index (PPI) report, which was 0.7% higher than the 3.4% year-on-year estimate. Despite the selling, data shows BTC spot market demand holding steady, with buyers stepping in to absorb the selling pressure and proof of this appetite being reflected by Bitcoin reclaiming $72,000 after Federal Reserve minutes highlighted their decision to leave interest rates unchanged.

While the market consensus had tilted toward the Fed choosing to pause on interest rate changes, market volatility in oil prices, equity markets, and persistent tension over the recently started US and Israel-Iran war had traders on edge.

Bitcoin bulls need to defend these price levels

On the four-hour chart, Bitcoin shows a higher low pattern, keeping the short-term uptrend intact. The price action is holding above both the 100- and 200-period exponential moving averages (EMAs), which are acting as dynamic support.

These moving averages track the average prices over time and define the trend direction when aligned below the price.

The confluence may allow BTC to stabilize near $71,000, forming a potential base after today’s sell-off.

From a technical standpoint, BTC needs to defend the $70,250 to $71,275 range, which marks the internal liquidity levels built during Monday’s breakout.

This zone represents the areas where orders were previously filled, possibly attracting a liquidity sweep again.

Losing this range exposes the next liquidity pocket near $68,900. That level aligns with a small order block between $68,300 and $69,100, where prior demand briefly absorbed the selling pressure.

Maintaining these levels keeps the lower time frame trend structurally bullish for BTC, with higher lows signaling continued demand on dips.

Related: Bitcoin tests fresh decoupling trade as tech correlation drops to 2018 lows

Bitcoin profit-taking meets bid absorption under $74,000

Prior to today’s correction, Bitcoin onchain data pointed to rising sell-side activity from short-term holders (STHs) on Tuesday. According to crypto analyst Darkfost, over 48,000 BTC in profit moved to exchanges in a single day as the price approached $75,000. This indicated that the buyers continued to lock in gains, treating the price rebounds as exit opportunities.

At the same time, CoinGlass data shows passive bids being filled during the drop to $71,000 from $74,000. Similar absorption patterns over the past two weeks have preceded short-term recoveries, highlighting consistent demand at lower levels.

Meanwhile, BTC’s reaction to the previous Federal Reserve meetings added insight. Market analyst Sherlock said that since June, 2025, Bitcoin has declined after each of the last six Federal Open Market Committee (FOMC) meetings, regardless of rate direction.

With the markets pricing in another hold on interest rates, traders’ attention may shift to how Bitcoin price reacts around current liquidity clusters, especially near $71,000.

Related: Bhutan offloads an additional $72.3M Bitcoin amid market downturn

This article does not contain investment advice or recommendations. Every investment and trading move involves risk, and readers should conduct their own research when making a decision. While we strive to provide accurate and timely information, Cointelegraph does not guarantee the accuracy, completeness, or reliability of any information in this article. This article may contain forward-looking statements that are subject to risks and uncertainties. Cointelegraph will not be liable for any loss or damage arising from your reliance on this information.

Bitcoin’s price tumbled before the news went out but it staged a minor recovery.

In alignment with most experts’ beliefs, the United States Federal Reserve kept the key interest rates unchanged for the second consecutive time in 2026.

BTC already experienced some volatility in the hours leading up to the second FOMC meeting of the year, dropping by $5,000 at one point. However, it has bounced toward $72,000 since the news went out.

America’s central bank maintained the federal funding rate, meaning what banks are charging each other for short-term loans, in the current range between 3.50% and 3.75%.

Experts noted before today’s announcement that the likely justification for this is the war that began in the Middle East, which has immediately impacted oil prices.

“The conflict with Iran has dramatically altered the backdrop to the March Federal Open Market Committee (FOMC) meeting and significantly increases the risks to inflation and the economy,” commented Oxford Economics’ chief US economist, Michael Pearce.

Bitcoin’s price reacted immediately to the news, even though it was expected. The asset had lost $5,000 earlier today in the hours leading up to the second FOMC meeting of the year, but bounced to $72,000 after the Fed’s decision went live.

Binance Free $600 (CryptoPotato Exclusive): Use this link to register a new account and receive $600 exclusive welcome offer on Binance (full details).

LIMITED OFFER for CryptoPotato readers at Bybit: Use this link to register and open a $500 FREE position on any coin!

Brightstar Lottery stock hits 52-week low at 12.6 USD

When price stops working, yield starts mattering

Bonnie Blue Hits Sex Snag In The UK After 400 Men Exploit

-

Crypto World5 days ago

Crypto World5 days agoHYPE Token Enters Net Deflation as HyperCore Buybacks Outpace Staking Rewards

-

Tech3 days ago

Tech3 days agoYour Legally Registered ‘Motorcycle’ Might Not Count Under Proposed US Law

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Addict Lip Glow

-

Sports4 days ago

Why Duke and Michigan Are Dead Even Entering Selection Sunday

-

Business3 days ago

Business3 days agoSearch for Savannah Guthrie’s Mother Enters Seventh Week with No Arrests

-

Tech1 day ago

Tech1 day agoAre Split Spacebars the Next Big Gaming Keyboard Trend?

-

Business4 days ago

Business4 days agoUS Airports Launch Donation Drives for Unpaid TSA Workers as Partial Government Shutdown Enters Fifth Week

-

Crypto World4 days ago

Coinbase and Bybit in Investment Talks: Could Bybit Finally Enter the US Crypto Market?

-

Business4 days ago

Business4 days agoCountry star Brantley Gilbert enters growing non-alcoholic beer market

-

Business2 days ago

Business2 days agoAustralian shares drop as Iran war enters third week

-

Crypto World2 days ago

Crypto World2 days agoCrypto Lender BlockFills Enters Chapter 11 with Up to $500M in Liabilities

-

Sports5 days ago

Sports5 days agoCollege Basketball Best Bets: Conference Tournament Semifinal Picks

-

Politics10 hours ago

Politics10 hours agoThe House | The new register to protect children from their abusers shows Parliament at its best

-

Crypto World7 days ago

Crypto World7 days agoThree Binance Charts May Be Hinting at Bitcoin’s Next Move

-

Business6 days ago

Business6 days agoTrump demands Powell cut rates as Iran conflict raises energy prices

-

Crypto World6 days ago

Crypto World6 days agoSenate Votes to Include CBDC Ban in Bipartisan Housing Bill

-

Fashion2 days ago

Fashion2 days ago25 Celebrities with Curly Hair That Are Naturally Beautiful

-

News Videos2 hours ago

News Videos2 hours agoRBA board divided on rate cut, unusually buoyant share market | Finance Report | ABC NEWS

-

NewsBeat6 days ago

NewsBeat6 days agoDeane Road crash near Bolton colleges and university

-

News Videos6 days ago

News Videos6 days agoTom Lee: The 100x Opportunity EVEN Bigger Than Bitcoin (New Ethereum Prediction 2026)

You must be logged in to post a comment Login