Crypto World

Liquidity, Regionalization & Asset Allocation

For global investors, 2025 was one of the most undercurrent-filled years of the 21st century. Unlike the bursting of the dot-com bubble in 2001 or the global financial crisis in 2008, markets in 2025 did not experience a prolonged, large-scale liquidation cycle or a “storm-like” sequence of relentless crashes.

Yet it is clear that, amid geopolitical uncertainty, uncertainty over US fiscal and monetary policy, uncertainty across multiple countries’ economic fundamentals, and the ebbing of globalisation in favour of regionalisation, equities, bonds, commodities and crypto have all been pricing in a future that is more cautious and more defensive.

Against that backdrop, liquidity allocation has become less concentrated in equities and bonds than it once was. Commodities, FX and rates attracted greater attention in 2025. At the same time, investors have been steadily reducing leverage and trimming exposure to higher-risk assets—one of the direct reasons the crypto bull market ended in Q4 2025.

So, where do markets go in 2026? As in 2025, implied expectations embedded in derivatives-market data have already offered an answer.

Liquidity: Not Abundant

At the start of 2025, one major “bullish” factor in investors’ minds was Donald Trump’s formal inauguration. The prevailing view was that Trump would trigger more rate cuts, inject more liquidity into markets, and drive asset prices higher.

Indeed, between September and December 2025, amid “concerns about a weakening labour market”, the Federal Reserve delivered three “defensive” rate cuts and, in December, announced the end of quantitative tightening. But this did not produce the liquidity flood investors had hoped for.

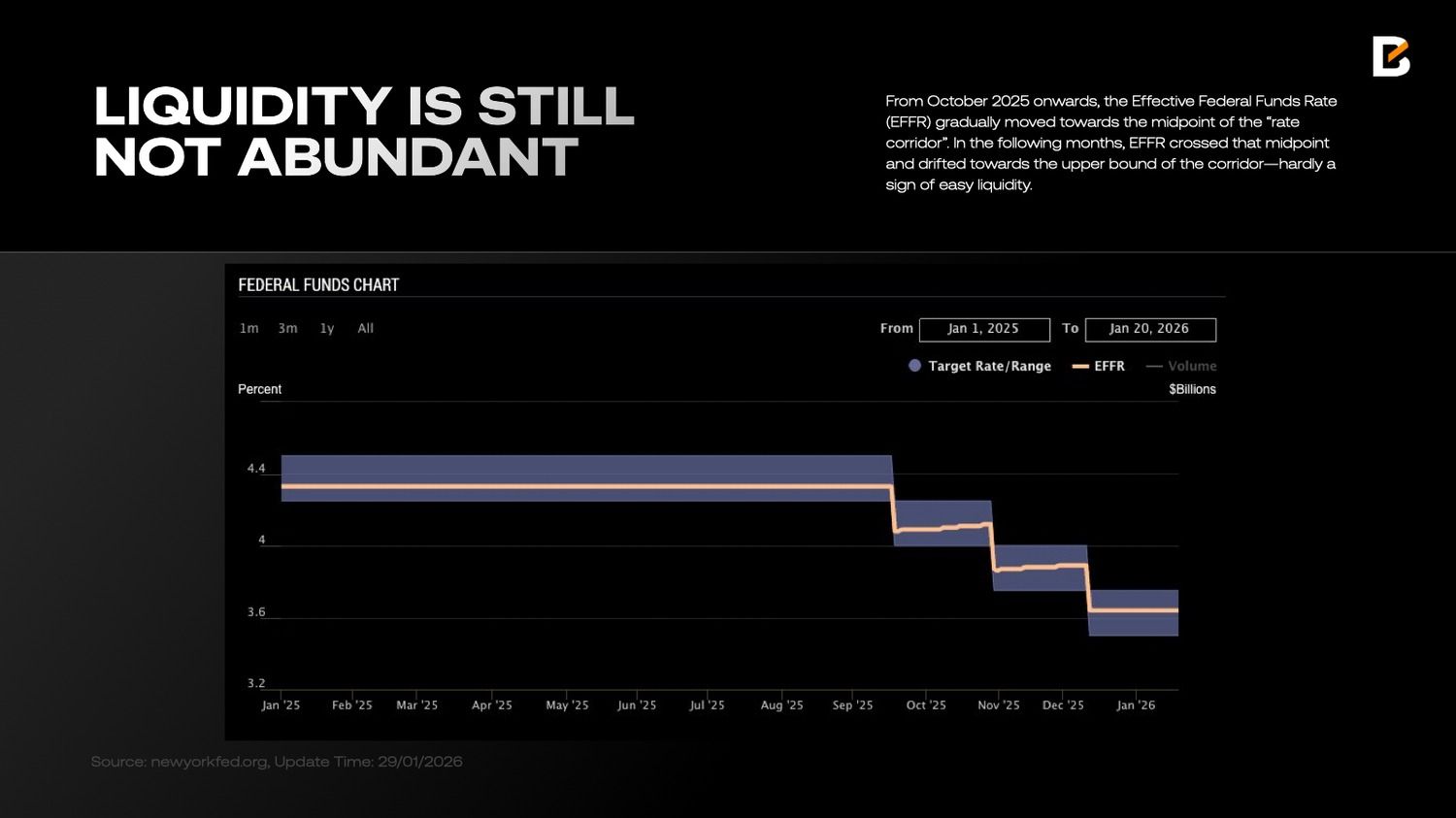

From October 2025 onwards, the Effective Federal Funds Rate (EFFR) gradually moved towards the midpoint of the “rate corridor”. In the following months, EFFR crossed that midpoint and drifted towards the upper bound of the corridor—hardly a sign of easy liquidity.

EFFR is the core short-term market rate in the US. It reflects funding liquidity conditions in the banking system and how the Fed’s policy stance (hikes or cuts) is transmitted in practice. In relatively loose-liquidity regimes, EFFR tends to sit closer to the lower end of the corridor, as banks have less need for frequent overnight borrowing.

In the final months of 2025, however, banks clearly faced liquidity tightness—a key driver of the rise in EFFR.

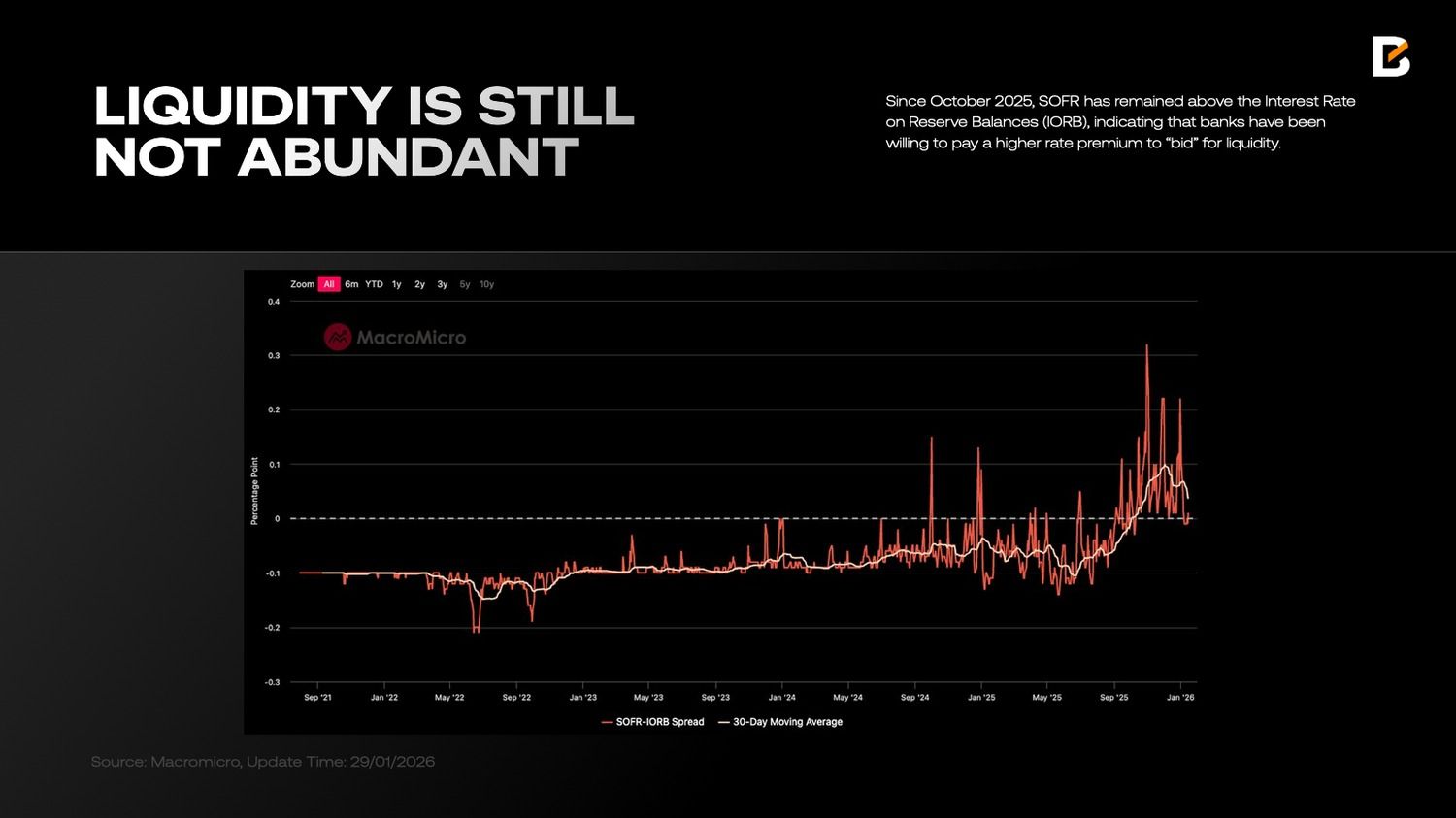

The SOFR–IORB spread further highlights the degree of stress. If EFFR primarily reflects cash-market conditions, SOFR, secured funding collateralised by US Treasury securities, captures a broader liquidity shortage. Since October 2025, SOFR has remained above the Interest Rate on Reserve Balances (IORB), indicating that banks have been willing to pay a higher rate premium to “bid” for liquidity.

Notably, even after the Fed stopped shrinking its balance sheet, the SOFR–IORB spread did not fall sharply in January. One plausible explanation is that, during 2025, banks deployed a significant share of their liquidity buffers into financial investments rather than extending credit to the commercial, industrial, and real estate sectors.

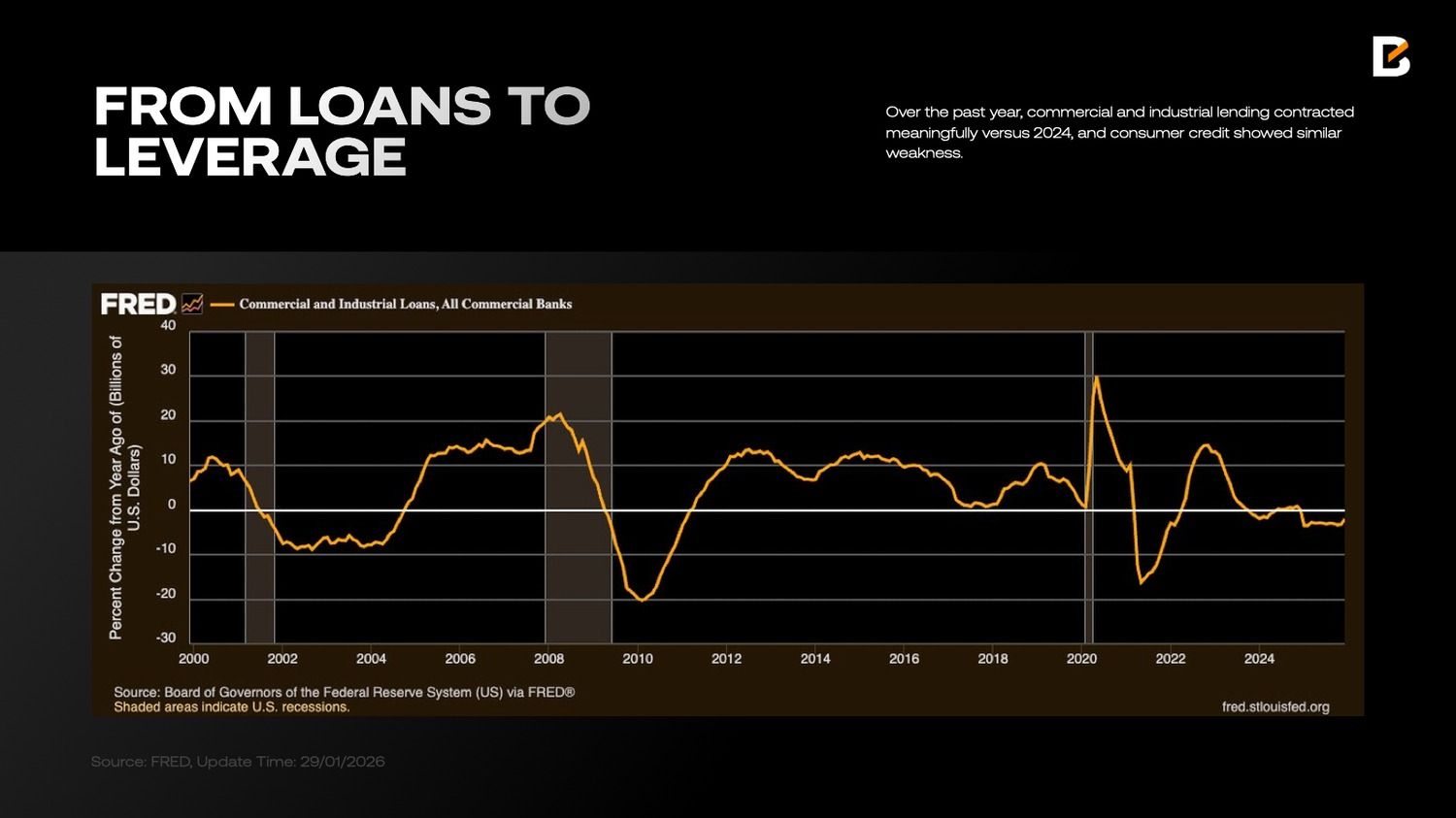

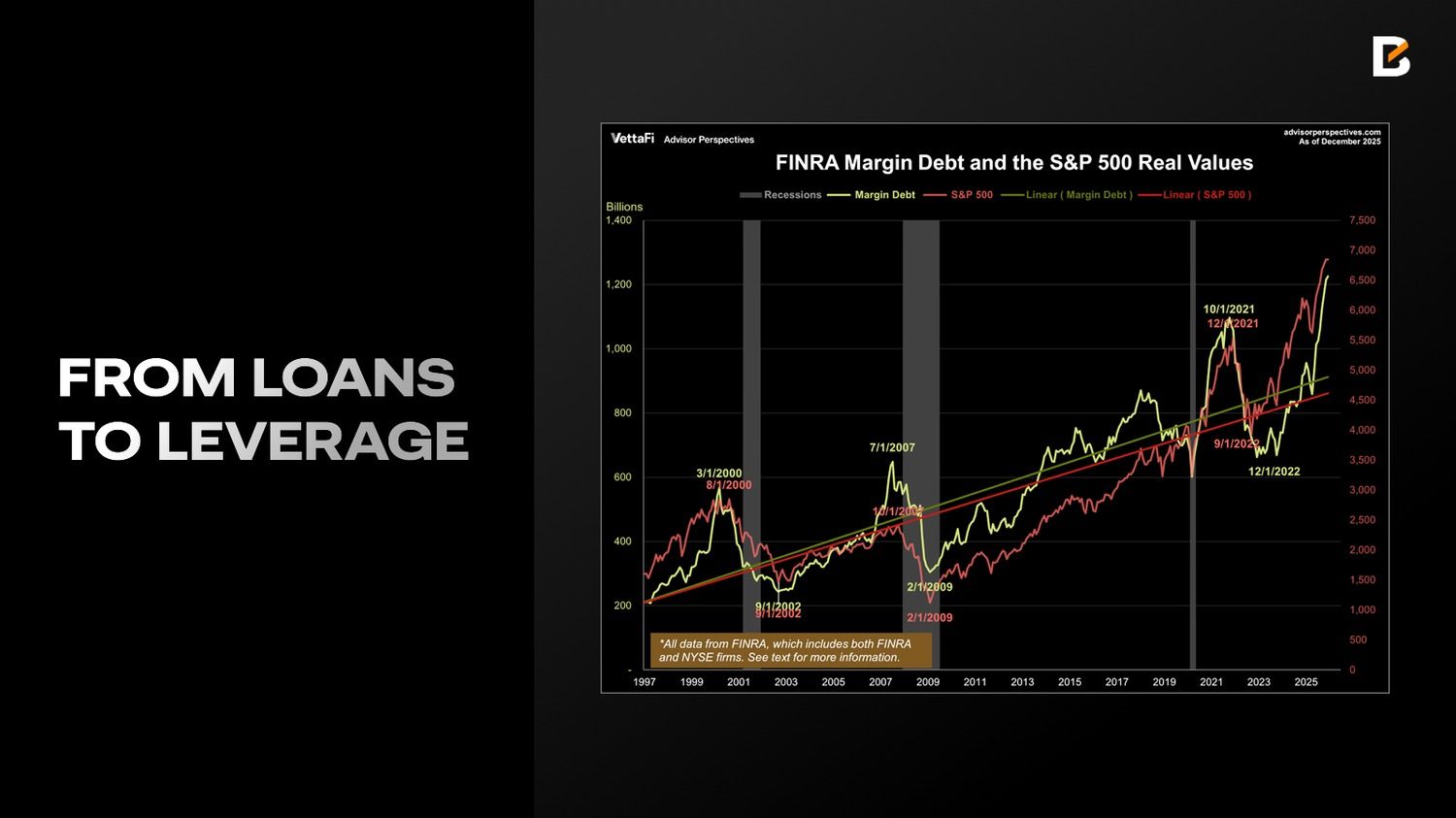

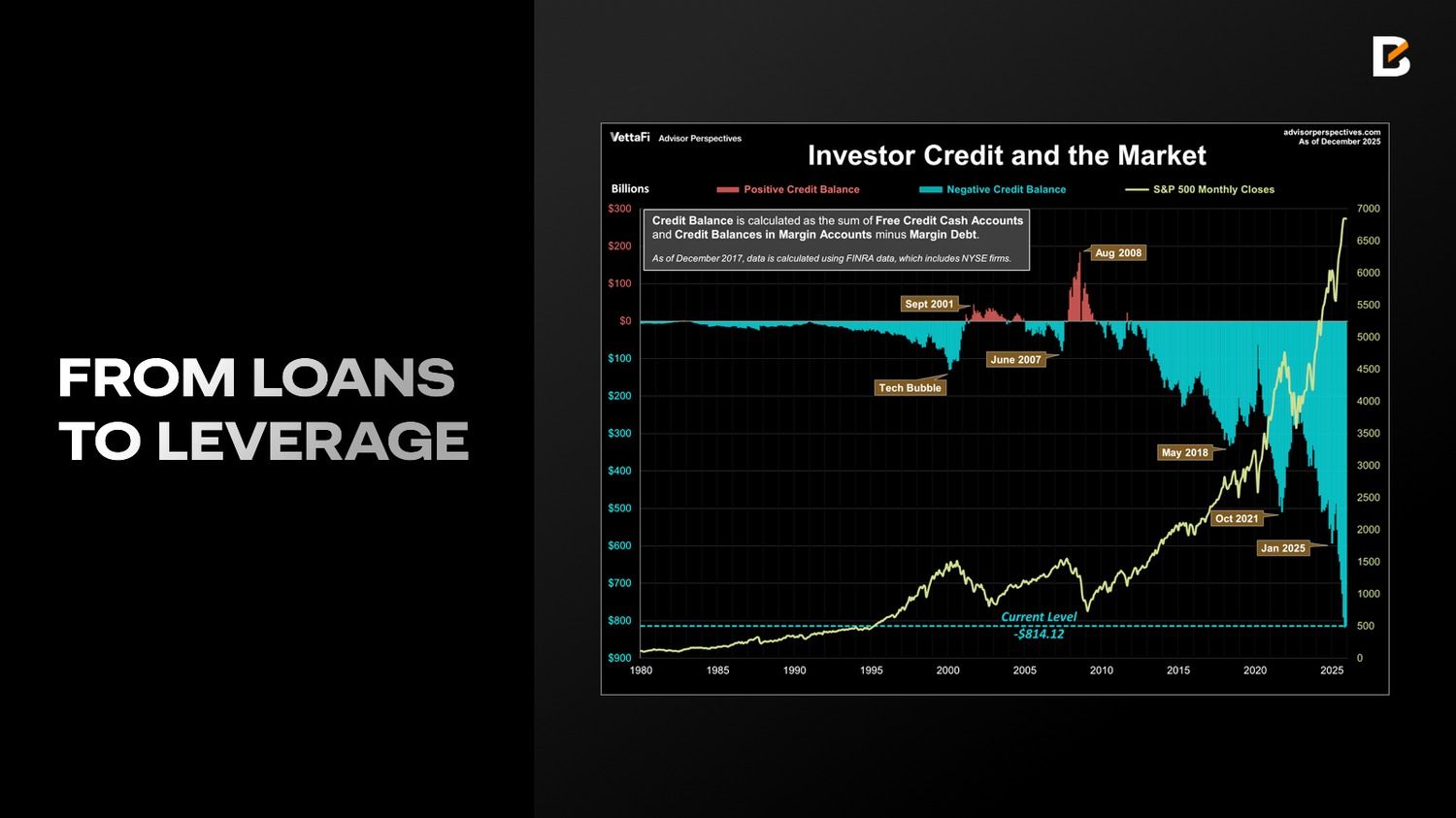

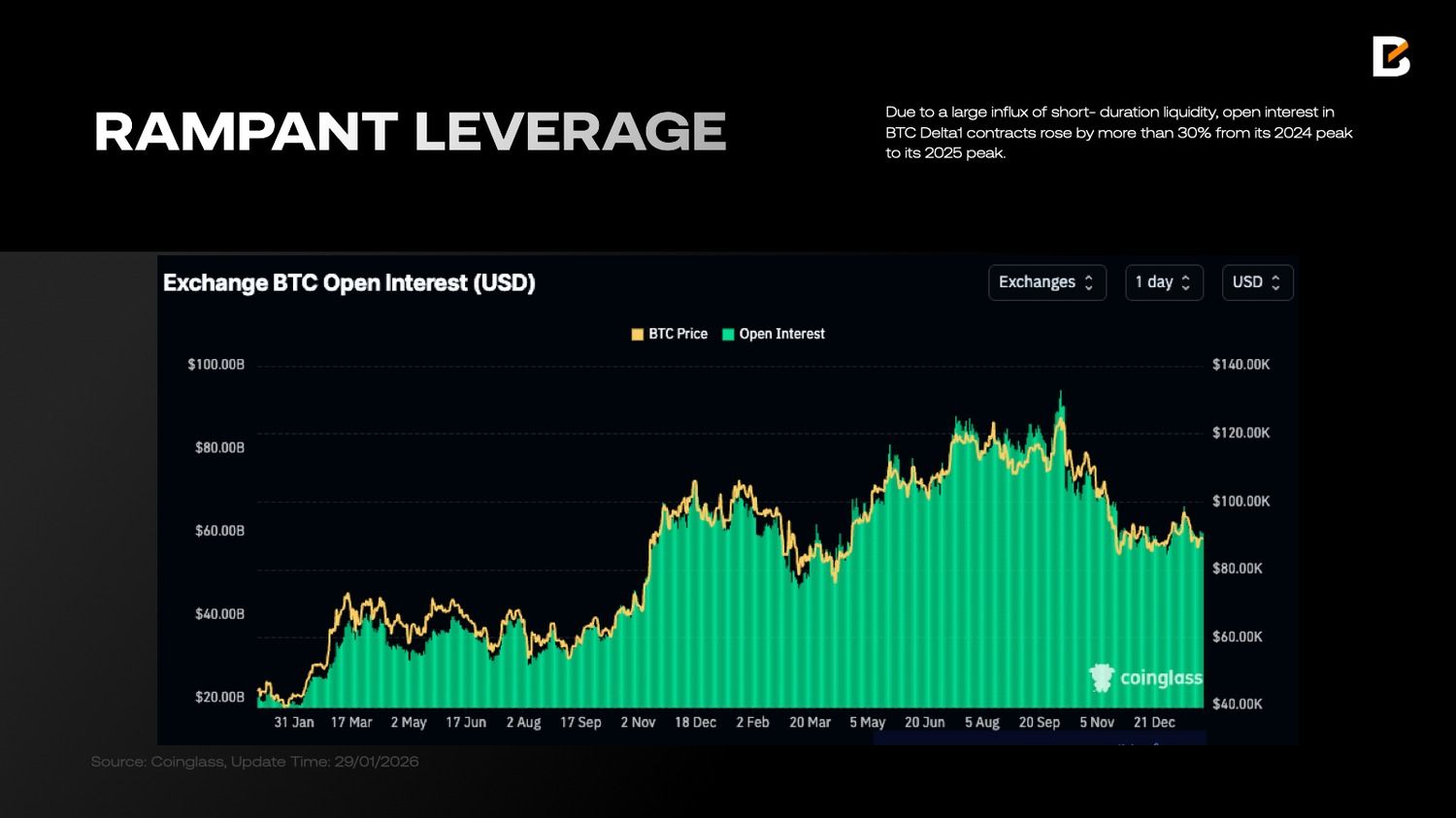

Over the past year, commercial and industrial lending contracted meaningfully versus 2024, and consumer credit showed similar weakness. By contrast, VettaFi data suggest that margin debt rose 36.3% over the past year, reaching an all-time high of $1.23T in December 2025, while investors’ net debit balances also expanded to $ -814.1 billion—broadly matching the pace of margin debt growth.

As liquidity requirements grow to push markets higher, the banking system is showing signs of strain, and demand for short-term funding has increased. The fix is straightforward: either reduce margin lending and pull liquidity back, or obtain liquidity support from the Fed and the repo market.

For the economy as a whole, the first option is preferable—lower system-wide leverage and strengthen resilience in banks and the financial system—but it would also imply lower valuations and a sharp equity sell-off. Given the midterm-election backdrop, the White House is unlikely to accept that path.

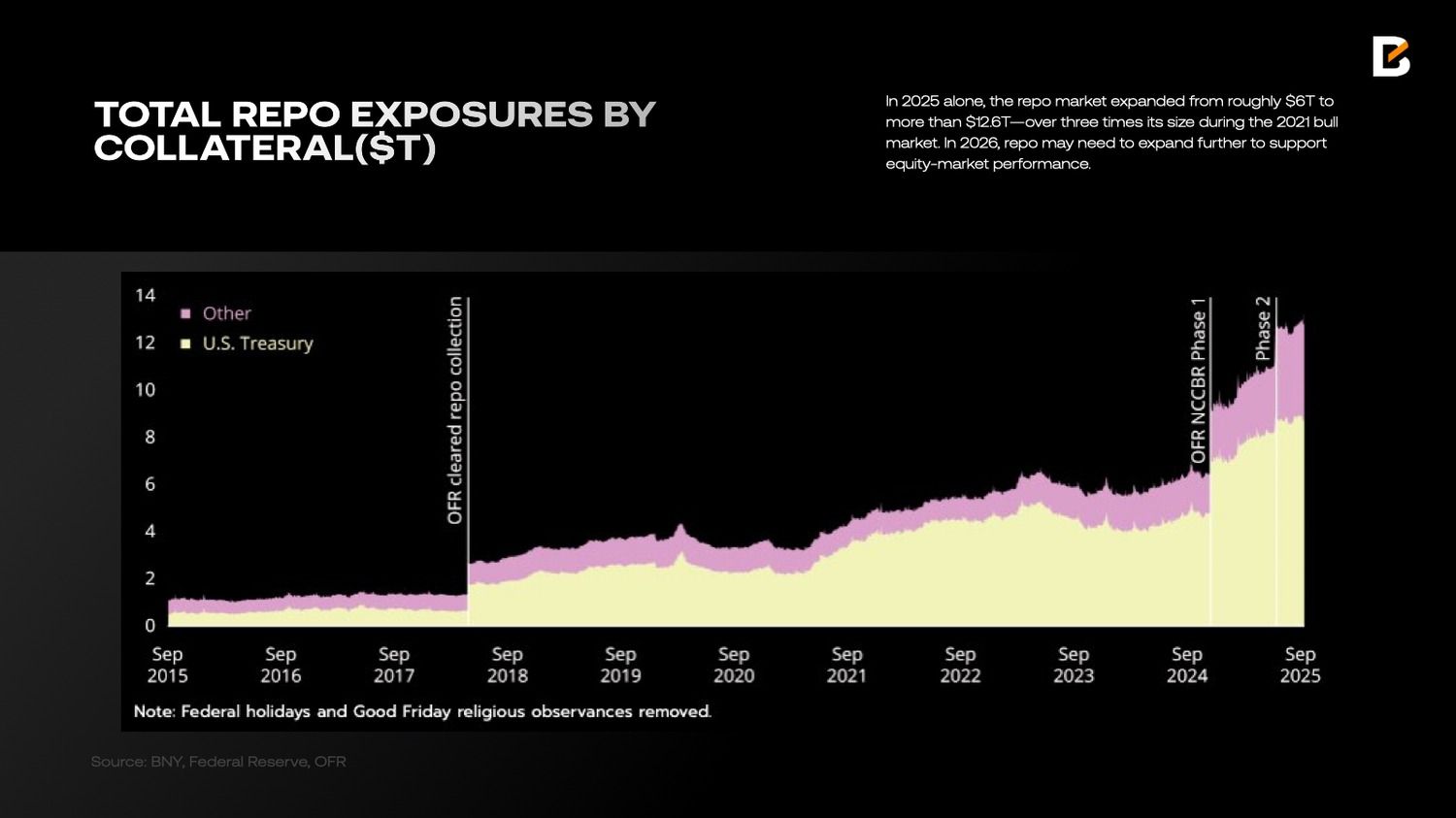

As a result, in 2025 alone, the repo market expanded from roughly $6T to more than $12.6T—over three times its size during the 2021 bull market. In 2026, repo may need to expand further to support equity-market performance.

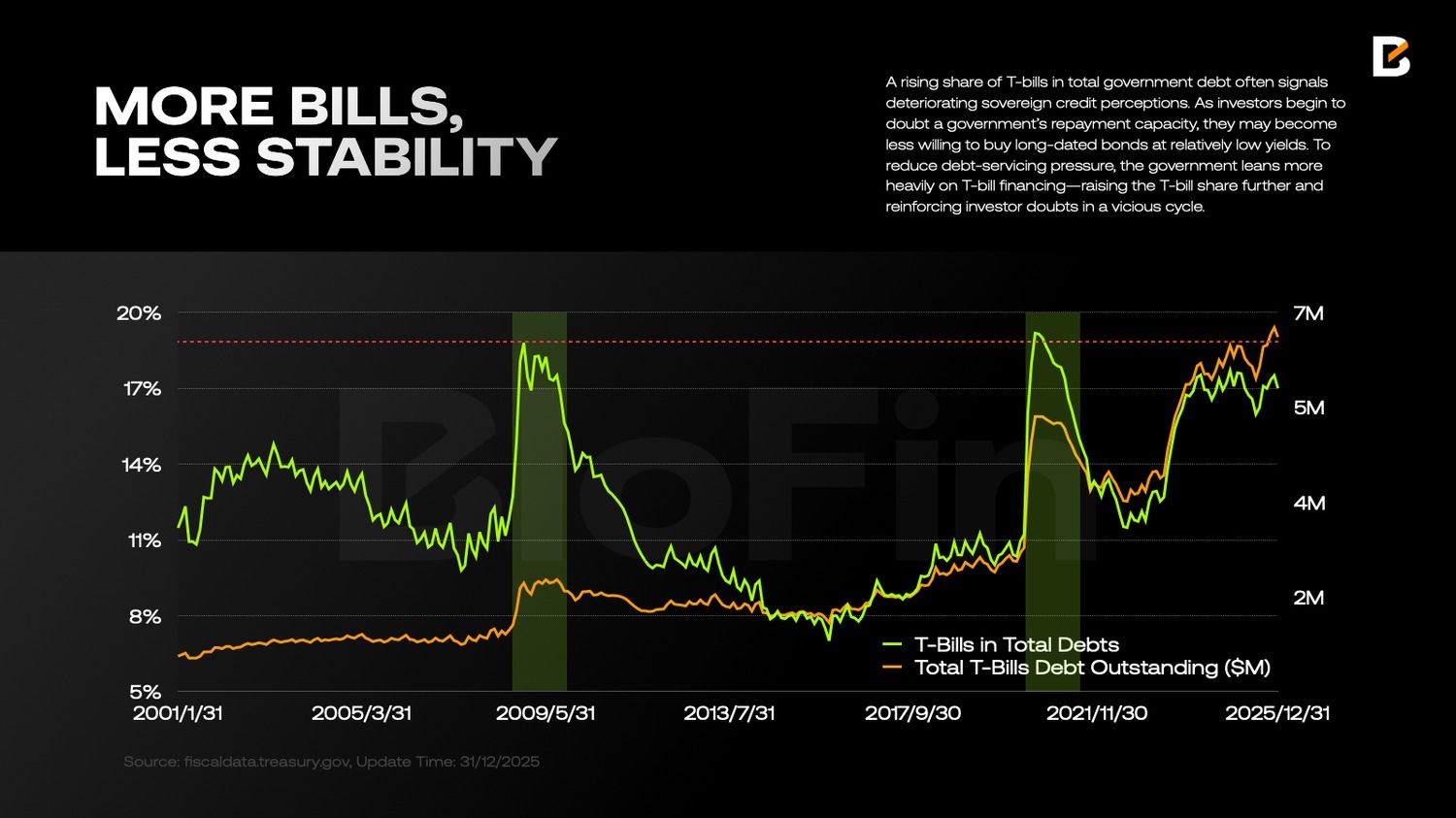

Repo transactions typically use US Treasuries—“high-quality assets”—as collateral. Historically, Treasury notes (T-notes) have been the most important form of collateral. But since mid-2023, that has changed, in part because the issuance and outstanding stock of Treasury bills (T-bills) has increased in an “exponential” fashion.

This is not benign: a rising share of T-bills in total government debt often signals deteriorating sovereign credit perceptions. As investors begin to doubt a government’s repayment capacity, they may become less willing to buy long-dated bonds at relatively low yields.

To reduce debt-servicing pressure, the government leans more heavily on T-bill financing—raising the T-bill share further and reinforcing investor doubts in a vicious cycle.

A higher T-bill share has another consequence: liquidity dynamics become less stable. Since a large portion of the liquidity supporting equities is channelled via repo, a greater reliance on T-bills implies more frequent rollovers and a shorter average liquidity “life”.

With overall leverage and margin debt already pushing beyond historical peaks, more frequent and more violent liquidity swings weaken the market’s shock-absorption capacity—setting the stage for potential cascading liquidations and large price moves.

In short: the quality of USD liquidity deteriorated markedly in 2025, with no clear sign of improvement so far.

So, in this macro context, how have investors’ expectations and portfolios changed?

Risk Premia and “Strict Diversification”

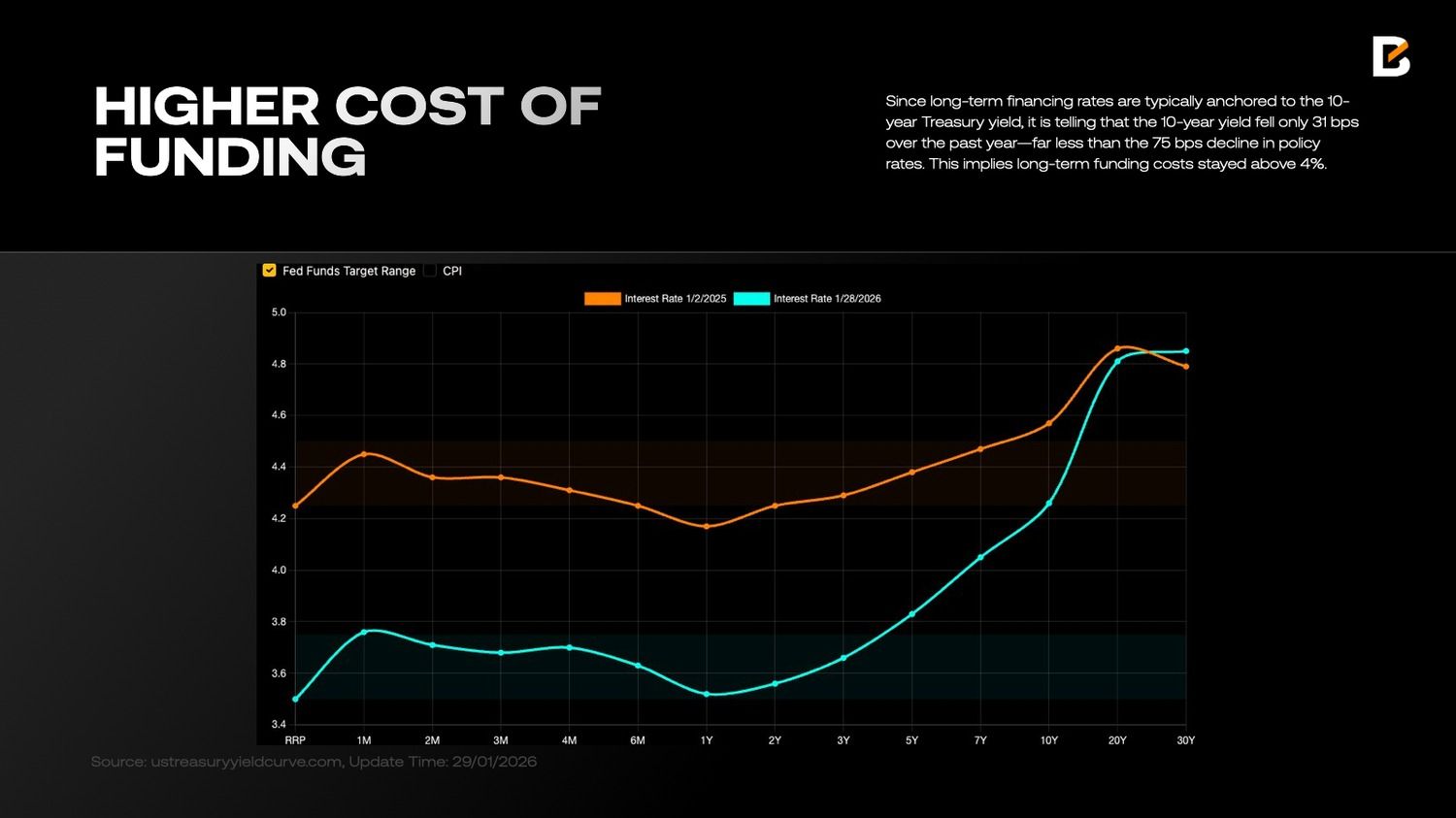

One cost of poorer-quality USD liquidity is that USD-based long-term funding costs remain elevated. This is intuitive: as USD asset markets become more fragile, US Treasury debt expands sharply (reaching USD 38.5 trillion by December 2025), and US fiscal, monetary and foreign policy turn more uncertain and less predictable, the perceived probability of systemic risk rises over time—prompting long-term Treasury investors to demand greater compensation.

Since long-term financing rates are typically anchored to the 10-year Treasury yield, it is telling that the 10-year yield fell only 31 bps over the past year—far less than the 75 bps decline in policy rates. This implies long-term funding costs stayed above 4%.

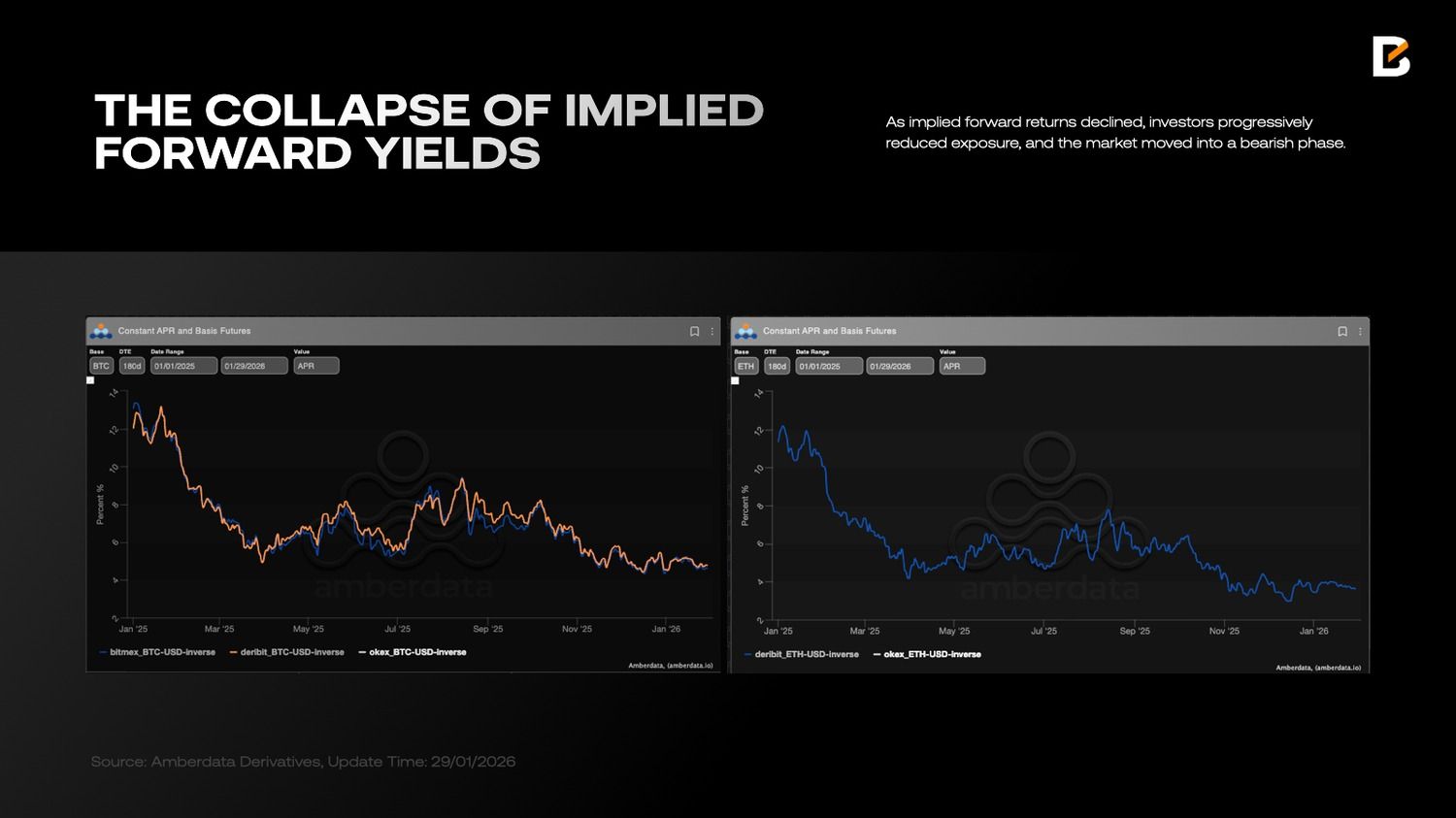

High funding costs constrain positioning. When a risk asset’s implied forward return falls below Treasury yields, holding that risk asset long-term becomes unattractive. Crypto is a textbook example: as implied forward returns declined, investors progressively reduced exposure, and the market moved into a bearish phase.

Compared with expensive long-term liquidity, short-term liquidity funded via T-bills is materially cheaper. But T-bill funding is also short-duration, creating an environment naturally favourable to speculation: investors can borrow short, apply high leverage, push prices up quickly and exit. Markets may look buoyant in the short run, but speculative froth makes rallies difficult to sustain—something clearly visible in the liquidity-sensitive crypto market.

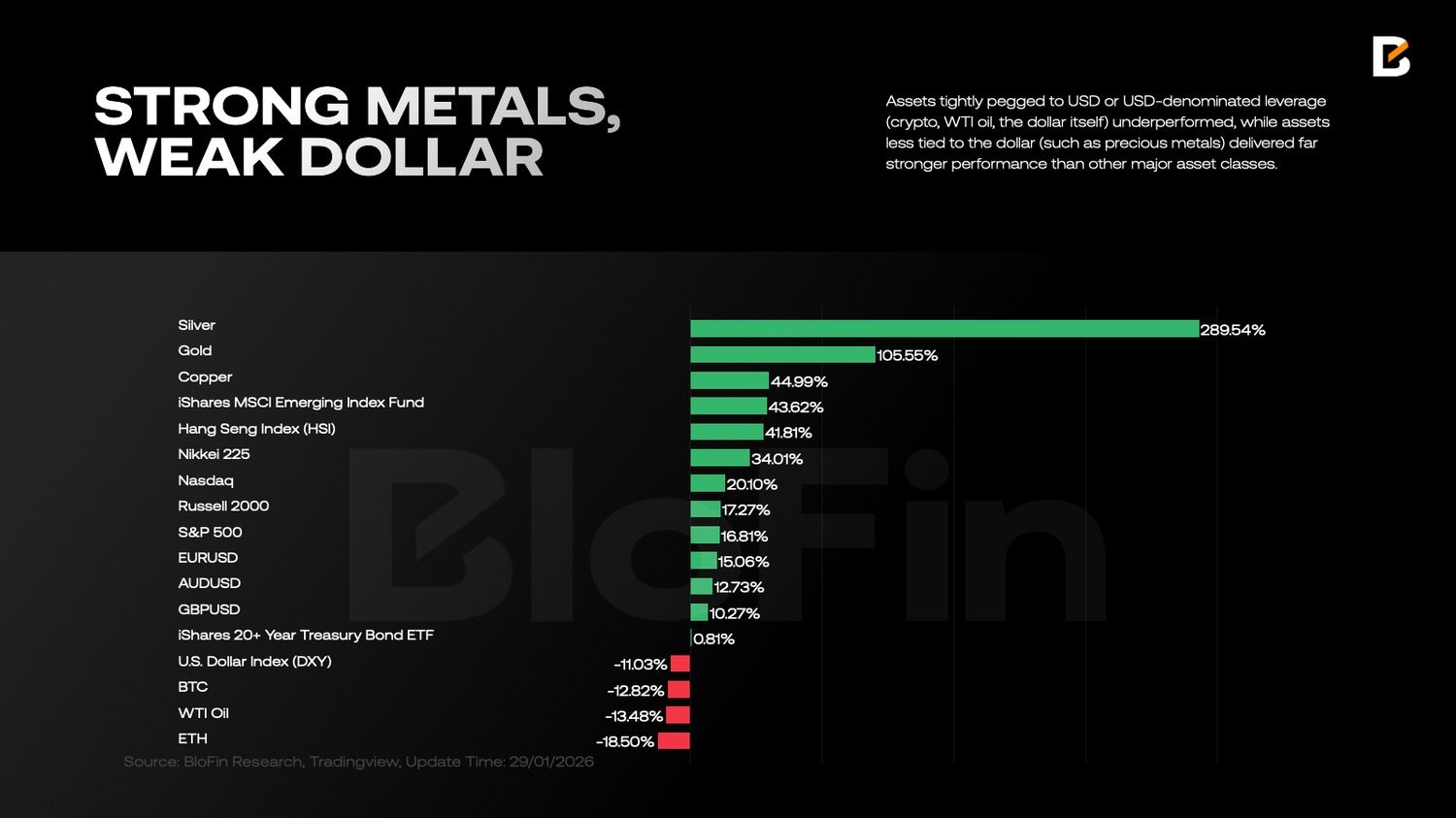

Meanwhile, after decades, “strict diversification” made a comeback in 2025. Unlike the traditional 60/40 approach, liquidity has been spread across a broader set of instruments rather than confined to USD assets.

In fact, throughout 2025, investors steadily reduced the share of USD and USD-pegged assets in portfolios. Although persistent net outflows did not visibly hit US equities, incremental liquidity was allocated more heavily to non-US markets.

Assets tightly pegged to USD or USD-denominated leverage (crypto, WTI oil, the dollar itself) underperformed, while assets less tied to the dollar (such as precious metals) delivered far stronger performance than other major asset classes.

Notably, simply holding euros or Swiss francs performed no worse than holding the S&P 500. This suggests a profound shift in investor logic—one that goes beyond a single business cycle.

The New Order

What most deserves reassessment in 2026 is not a linear question like “will growth be stronger?”, but rather the fact that markets are adopting a new pricing grammar. Over the past two decades, returns often rested on two implicit assumptions: first, supply chains were organised around maximum efficiency, suppressing costs and stabilising inflation; second, central banks provided powerful backstops during crises, systematically compressing risk premia.

Both assumptions are now weakening. Supply chains increasingly prioritise control and redundancy; fiscal and industrial policy appears more frequently in profit models; and geopolitics has shifted from tail risk to constant noise. “Regionalisation” is less a slogan than a change in the constraint set facing the global economic system.

In this framework, the key is not to bet on a single direction, but to realign exposures to three more reliable “hard variables”: supply constraints, capital expenditure, and policy-driven order flow.

Together, they point towards a set of assets: commodity-linked equities, the AI infrastructure chain, defence and security themes, and select non-US markets that improve portfolio correlation structures. At the same time, the core question in rates and government bonds is no longer “how much tailwind will rate cuts bring?”, but how the new term structure reshapes the distribution of returns.

Regionalisation: Not “Decoupling”, but a New Cost Function

Equating “regionalisation” with “full decoupling” tends to understate its true impact. A more accurate description is that globalisation’s objective function has shifted from “efficiency at all costs” to “efficiency under security constraints”.

Once security becomes a binding constraint, many variables that previously sat outside valuation models—supply-chain redundancy, energy security, access to critical minerals, export controls on key technologies, and the rigidity of defence budgets—begin to enter discount rates and earnings expectations in various forms.

This produces two direct consequences for asset pricing. First, risk premia become less likely to revert to structurally low levels: political and policy uncertainty becomes an everyday variable, and markets require greater compensation. After all, nobody wants to bear “Cuban equity risk”, and today, even in US equities, that “Cuban equity risk” is no longer zero.

Second, global beta explains less, while regional alpha matters more: under different blocs and policy functions, the same growth and the same inflation can produce very different valuations and capital flows. For allocators, diversification in the age of regionalisation looks less like splitting assets evenly by country and more like diversifying across supply-chain position and policy elasticity.

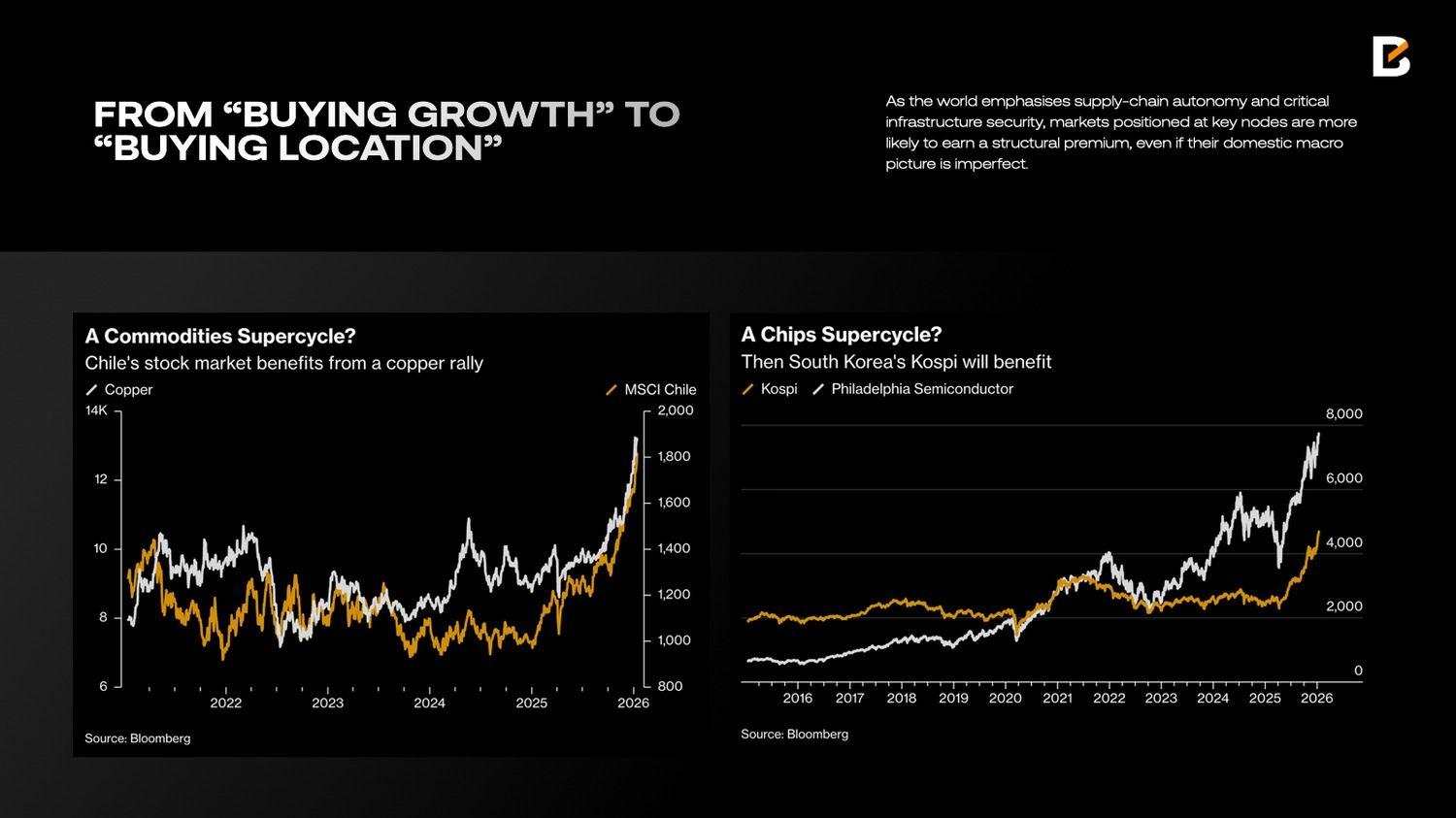

Equities: From “Buying Growth” to “Buying Location”

If 2010–2021 equity allocation was largely about “buying growth and falling discount rates”, 2026 is more about “buying location”. “Location” refers to where a market sits on three maps: the resource map, the compute map and the security map. As the world emphasises supply-chain autonomy and critical infrastructure security, markets positioned at key nodes are more likely to earn a structural premium, even if their domestic macro picture is imperfect.

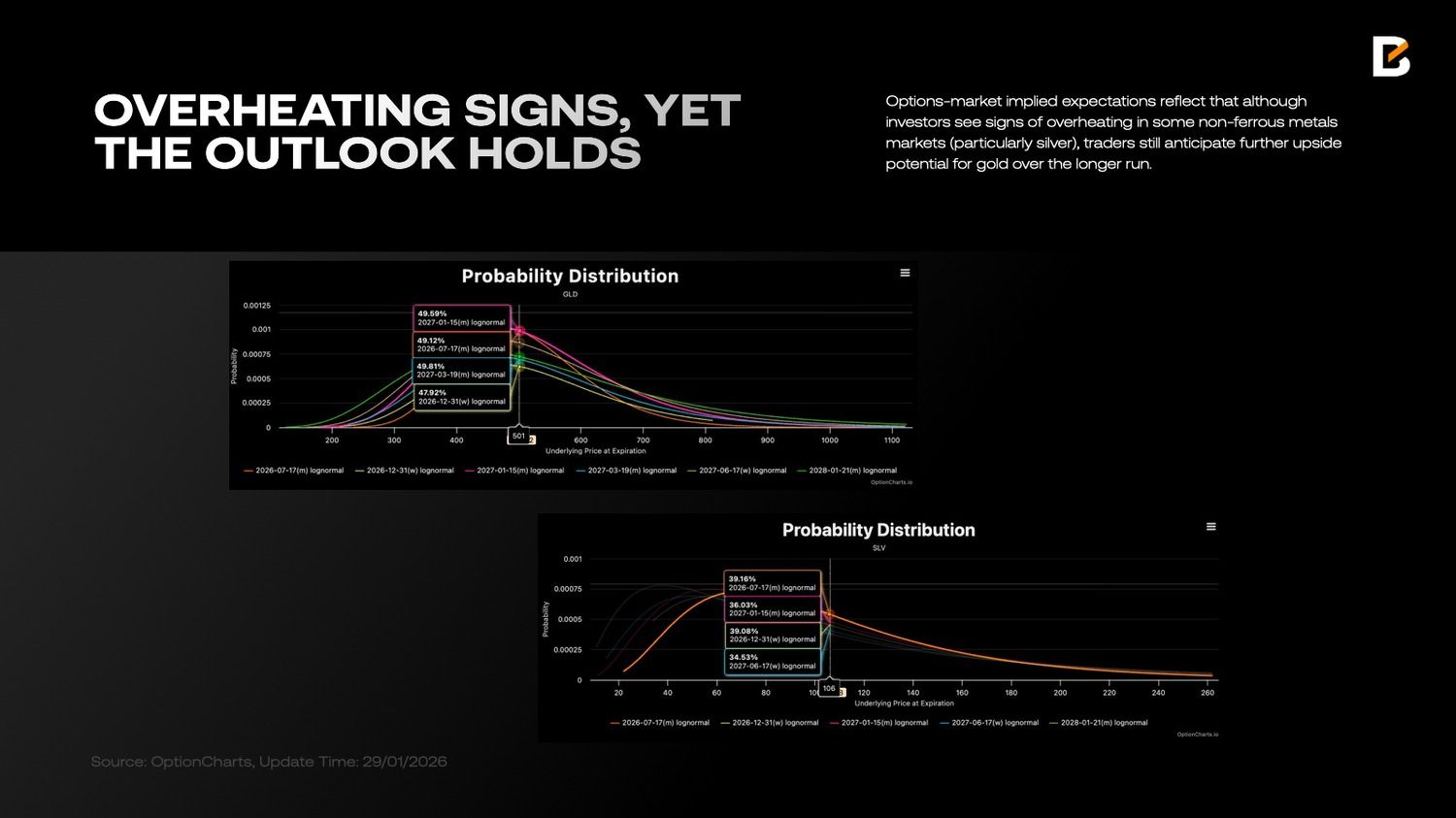

In an era where security is the top priority, increasing inventories of gold, silver, copper and other non-ferrous metals can be rational even if they are not immediately needed. Supply chains can be disrupted without warning (as last year’s trade tensions showed), sharply raising costs and forcing major countries to hold larger mineral reserves against potential shocks.

Structurally rising demand for critical minerals, combined with long-cycle supply constraints, makes commodities behave more like “supply-side assets” than mere mirrors of the traditional business cycle. Options-market implied expectations reflect this: although investors see signs of overheating in some non-ferrous metals markets (particularly silver), traders still anticipate further upside potential for gold over the longer run.

This logic also provides a clearer allocation case for equities in resource-rich countries. Copper-linked equities—Chile is a prime example—partly reflect foundational shifts in electrification and in demand for industrial infrastructure.

Precious-metals resource equities—South Africa is a typical case—combine commodity upside with the double-edged nature of risk premia: when commodities rise, profits and the currency may reinforce each other; when risk rises, politics and external financing conditions can amplify volatility. For portfolio construction, resource-country equities are better understood as a “supply-constraint factor” than simply emerging-market beta.

Another central theme is AI. AI discussions are easily pulled towards application-layer narratives, but allocators should focus on balance-sheet realities: compute, energy, data centres, networks, and cooling. These links share two traits: higher capex visibility and often benefit from joint support from policy and industry.

Rather than treating AI as another software-valuation game, it may be more robust to view it as a new wave of infrastructure build-out. Higher compute density ultimately translates into greater power and engineering demand, shifting more of the return distribution upstream and into midstream “real-economy” segments.

Under regionalisation, computing infrastructure is also spreading geographically. Higher security redundancy and localisation requirements increase the strategic value of key hardware and intermediate goods.

Markets such as Korea, positioned at the industrial interface of global compute infrastructure via semiconductors and critical electronics, are often seen as more direct equity expressions of the AI capex cycle. For portfolios, the value of this exposure is not only “faster growth”, but “more observable capex and more stable policy support”.

In addition, “defence and security” has returned to investors’ agendas for the first time since the end of the Cold War. Influenced by Trump’s “Donroeism” and the Russia–Ukraine war, both the US and Europe are placing defence higher on the priority list.

The distinctive feature of defence assets is that demand does not come from marginal household consumption; it is closer to a fiscal function constrained by national security. Once budgets step up, the political resistance to reversing them is greater, so order visibility is typically stronger. This gives defence-related equities a more defensive allocation role in a regionalised world: when conflict and sanctions risk rise, they can add resilience at the portfolio level.

That said, defence-sector price sensitivity often runs ahead of fundamentals: event-driven repricing followed by mean reversion is common. A more robust framing is to treat it as a portfolio “tail insurance” or risk-hedging factor, rather than a linear-growth core holding. Its value lies in reducing drawdowns, not in guaranteeing outperformance every quarter.

Hong Kong equities and mainland China assets are another area worth considering. Labelling them simply as “cheap” is insufficient; their allocation value stems from two factors. First, pricing often bakes in pessimistic expectations early, leaving room for rebalancing.

Second, their policy function and sector composition differ from those of US and European assets, potentially improving portfolio correlation structure. In the age of regionalisation, correlations do not automatically fall; they can rise during risk events. Structurally different assets can therefore provide more meaningful hedging.

Rates and Treasuries: Keep the Curve Steepening

The core tension in 2026 rates markets can be summarised in one line: the front end is more a function of the policy path, while the long end is more a container for term premia.

Rate-cut expectations do help front-end yields decline, but whether the long end follows depends on whether inflation tail risks, fiscal supply pressure and political uncertainty allow term premia to keep compressing. In other words, long-end “stubbornness” may not mean markets have mispriced the number of cuts; it may mean markets are repricing long-run risk.

Supply dynamics amplify this structural difference. Changes in US fiscal funding composition directly affect supply–demand across maturities: the front end is easier to absorb when money markets have capacity. In contrast, the long end is more prone to pulse-like volatility driven by risk budgets and term premia.

The portfolio implication is clear: duration exposure should be managed in layers, avoiding a one-path bet on “inflation fully disappearing and term premia returning to ultra-low levels”. Curve-structure trades (for instance, steepening strategies) persist not merely because of superior trading skill, but also because they align with the different pricing mechanisms of the front and long ends.

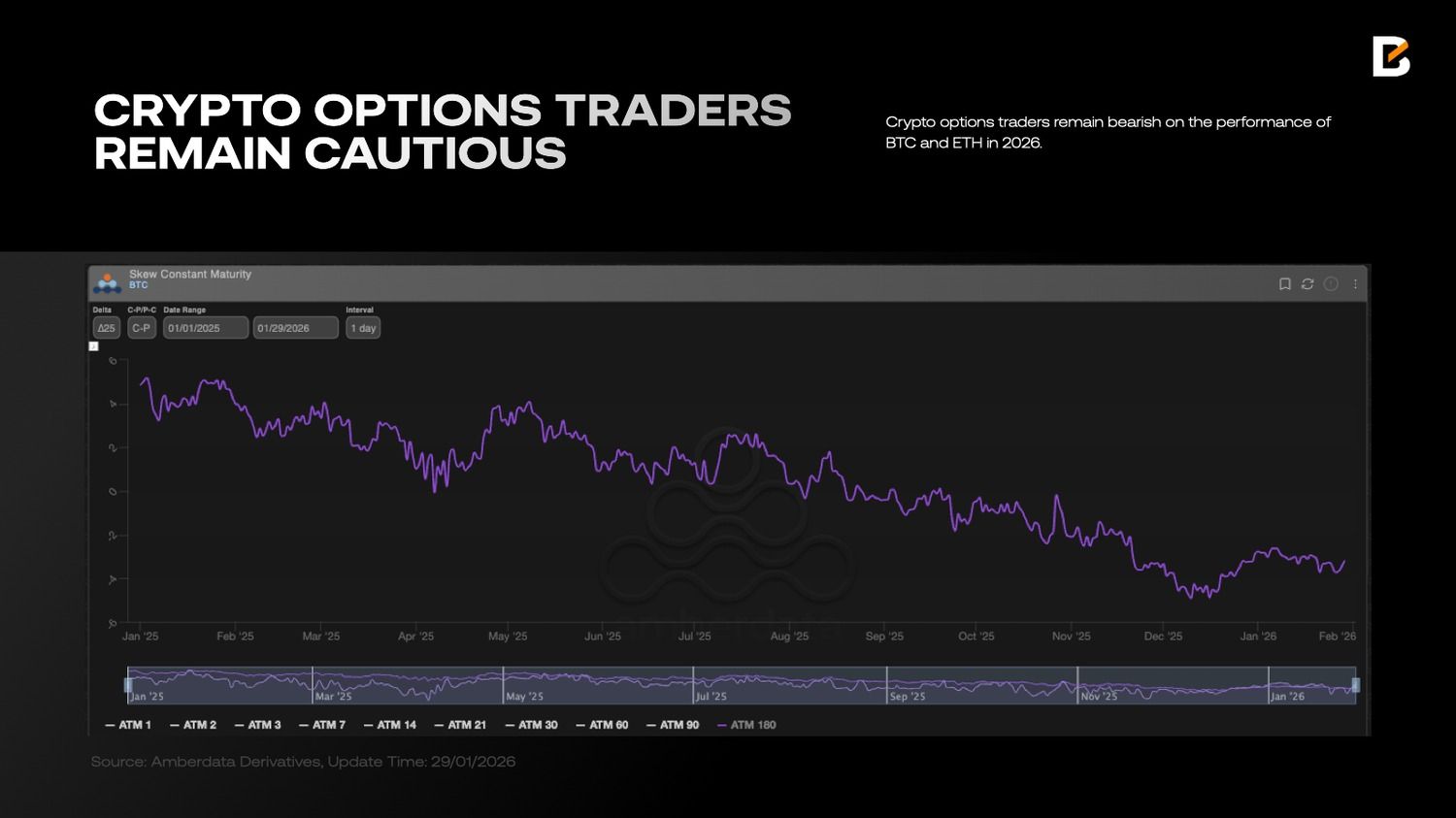

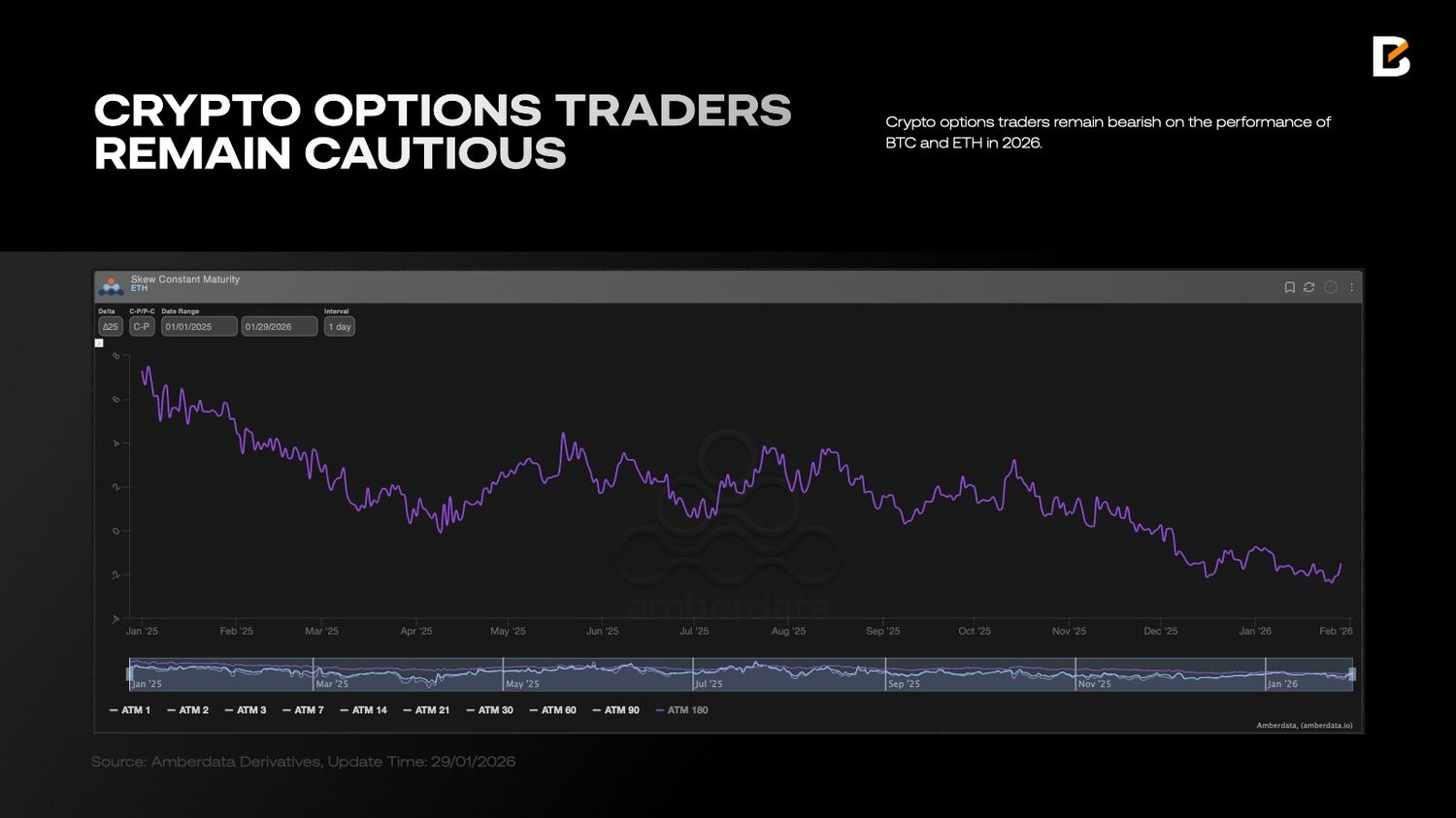

Crypto: Separate Accounting for “Digital Commodities” and Secondary Risk Assets

In 2026, the key for crypto is not simply “will it rise?”, but sharper internal differentiation. Bitcoin is more readily understood as a non-sovereign, rules-based supply asset that is portable across borders—a “digital commodity”. Under a regionalisation narrative, it is more likely to absorb demand for alternative payment systems and hedges.

By contrast, a subset of tokens that behave more like equity-style risk assets are priced more on growth stories, ecosystem expansion and risk appetite. When risk-free yields remain attractive, regulation becomes clearer, and traditional capital markets offer more mature funding and exit channels, equity-like tokens must offer higher risk compensation to justify allocation.

As a result, crypto allocation is better approached via “separate books” rather than a single basket: place bitcoin in a commodity/alternative-asset framework, using small weights to obtain portfolio-level convexity; treat equity-like tokens as high-volatility risk assets with stricter return hurdles and clearer risk budgets. The core of the regionalisation era is not to embrace every new asset, but to identify which assets remain more explainable under the new constraints.

Use Hard-Constraint Assets as the Core, Use Structural Divergence as the Return Engine

Putting the above together, a 2026 portfolio looks more like managing a set of “hard constraints”: supply constraints restore the strategic role of commodities and resource equities; capex supports earnings visibility across the AI infrastructure chain; policy-driven orders enhance the resilience of defence and security; the return of term premia reshapes the distribution of duration returns; and select non-US assets provide reflexive hedging through valuation structure and policy functions.

This does not require perfect prediction of every event. On the contrary, the rarest skill in the age of regionalisation is to place the portfolio in a position that relies less on flawless forecasting: let hard assets and infrastructure absorb structural demand; let curve structures absorb structural divergence; and let hedging factors absorb structural noise.

Trading in 2026 is no longer about “guessing the answer”, but about “acknowledging constraints”—and rewriting asset-allocation priorities accordingly.

Disclaimer: The information provided herein does not constitute investment advice, financial advice, trading advice, or any other sort of advice, and should not be treated as such. All content set out below is for informational purposes only.

Crypto World

Best Crypto Portfolio for 2026: Messari Pivots to AI and Pepeto Gives Early Investors the Entry That Large Caps Cannot Offer

Messari just cut its staff to become an AI first company, handing leadership to former CTO Diran Li. When a major data provider goes all in on machine learning, that tells every investor where the future is heading.

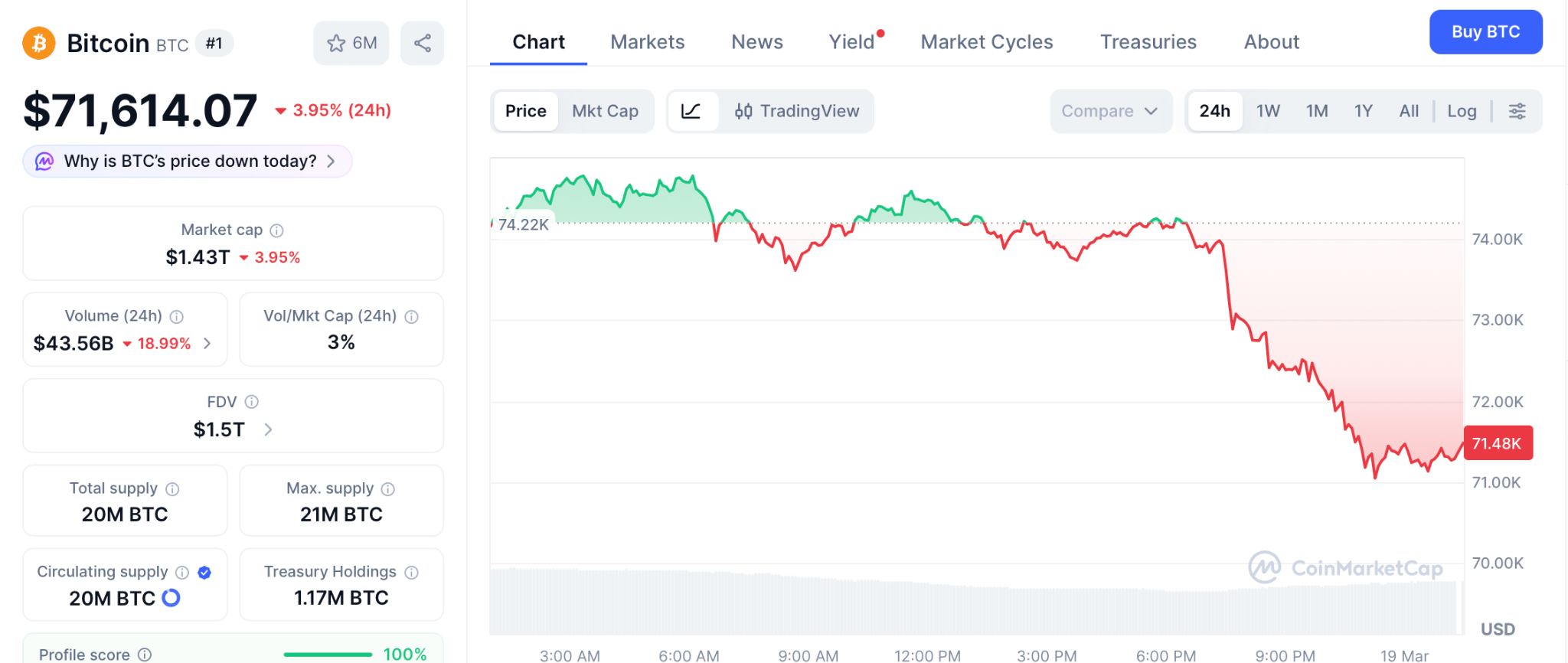

The best crypto portfolio for 2026 needs large caps for the base and an early project for the returns that BTC at $71,614 and ETH at $2,203 can no longer deliver. And the early project absorbing the most capital right now is Pepeto.

Messari confirmed the company is doubling down as an AI first organization, restructuring its entire data layer around machine learning according to CoinDesk.

Strategy purchased $1.57 billion worth of Bitcoin, the largest single buy of 2026, pushing BTC briefly above $75,000 according to CoinDesk. Peter Brandt flagged an Ethereum bottom at $2,300 with a $4,000 target.

Best Crypto Portfolio Allocations and the Projects That Deserve Capital in March 2026

Pepeto Is the Early Entry That Belongs in Every Serious Crypto Portfolio Before the Listing Changes the Price

Picture this: the market just corrected after FOMC, your portfolio is red, and most investors are either panic selling or frozen, staring at charts they cannot read. The ones who already had Pepeto in their portfolio are not worried. Not because they predicted the dip, but because they got in at a price that makes the dip irrelevant. That is the real edge an early project offers for any crypto portfolio in 2026.

Instead of paying fees on every swap and watching your capital shrink trade by trade, PepetoSwap charges zero on every transaction and the bridge moves tokens across Ethereum, BNB Chain, and Solana for nothing. The risk scorer also scans every token in real time, catching honeypots and exploit code before your money ever touches the contract.

That kind of protection could have saved a lot of portfolios from the rug pulls that wiped out billions last cycle. A working exchange, bridge, and risk scorer all audited by SolidProof before the presale opened is something the presale market almost never delivers.

With the Binance listing approaching and more than $8.1 million already raised, adding Pepeto to a portfolio before it lists could be the single best allocation of 2026. And a $3,000 position at $0.000000186 buys over 16 billion tokens. If Pepeto only reaches the $11 billion cap that Pepe hit with the same 420 trillion supply and zero products, that $3,000 becomes more than $450,000, and that is the base case scenario as Pepeto offers far more utility and potential.

Bitcoin at $71,614 Anchors Every Crypto Portfolio With Institutional Backing

BTC trades at $71,614 according to CoinMarketCap, after the FOMC pullback from $76,000. Strategy’s $1.57 billion purchase and the longest ETF inflow streak in five months confirm institutional conviction.

Kiyosaki targets $750,000 long term. Bitcoin is the anchor, but from $74,000 the returns that change a life come from the early entries.

Ethereum at $2,203 With Peter Brandt Flagging a Possible Bottom and a $4,000 Target

Peter Brandt indicated ETH is forming a bottom at a major historical support level, targeting $4,000 according to CoinGecko.

From $2,203 to $4,000 is roughly 75%. Strong for a portfolio allocation, but the biggest returns still come from getting into early projects before the listing.

Digitap Targets the Creator Economy but Lacks a Working Product and Community Traction

Digitap targets the $85 billion creator economy with AI subscription tools. The concept is interesting, but it has raised $1.5 million without a working product or community comparable to projects already generating real demand. The timeline to results is measured in years.

The Best Crypto Portfolio Does Not Wait for the Market to Recover Before the Early Entry Disappears

The best crypto portfolio does not wait for the market to feel safe again before the entry disappears. Pepeto is the early project that belongs in every serious portfolio for 2026, and the Binance listing means the presale at this price has a deadline the market will not extend.

A $3,000 position buys over 16 billion tokens, and 196% APY staking compounds that position daily while the listing advances. Visit the Pepeto official website and add the early entry before the listing, because every cycle proved that the best portfolios were built before the listing, not after.

Click To Visit Pepeto Website To Enter The Presale

FAQs

What is the best crypto portfolio for 2026?

BTC for stability, ETH for the recovery play, and Pepeto as the early project with the biggest potential before the Binance listing.

Why does Messari pivoting to AI matter for building a crypto portfolio?

When institutional data providers restructure around AI, it confirms the direction of the cycle. The best crypto portfolio positions early in that direction.

Is Pepeto a good early project to add to a portfolio?

More than $8.1 million raised, SolidProof audit, original Pepe coin team, and a Binance listing approaching. Visit the Pepeto official website.

The post Best Crypto Portfolio for 2026: Messari Pivots to AI and Pepeto Gives Early Investors the Entry That Large Caps Cannot Offer appeared first on Blockonomi.

The Federal Reserve’s Open Market Committee kept the federal funds target range unchanged at 3.5% to 3.75, signaling a wait-and-see stance as policymakers weigh the evolving macro backdrop and the geopolitical shock stemming from the Middle East. The decision preserves a restrictive stance while the central bank monitors inflation pressures and the economy’s ability to weather external shocks.

Fed Chair Jerome Powell framed the economy as performing well in broad terms — consumer spending staying resilient and business investment continuing to expand — but he warned that weaknesses linger in the housing market and the labor market shows signs of softening. Inflation, meanwhile, remains “somewhat elevated” relative to the 2% target, complicating the Fed’s path back to price stability.

The implications of events in the Middle East for the US economy are uncertain in the near term. Higher energy prices will push up overall inflation, but it is too soon to know the scope and duration of the potential effects on the economy.

The posture underscores a difficult balancing act: the Fed must pursue maximum employment while keeping inflation anchored, all in a context where the war’s economic spillovers could push energy costs higher and alter demand dynamics. Powell’s remarks suggest policymakers view the near-term outlook as uncertain, with energy price trajectories among the wild cards that will shape policy in the months ahead.

Key takeaways

- Policy remains unchanged at 3.5% to 3.75%, with inflation lingering above the 2% goal and housing weakness alongside signs of labor-market cooling.

- Geopolitical tensions add energy-price risk, injecting additional uncertainty into the inflation path and the policy outlook.

- Markets broadly price in little near-term relief from rate cuts; CME data shows a 97% probability of no change at the next year-ahead horizon, with a small 3% chance of a 25-basis-point hike by April 2026 that would lift the range to 3.75%–4.00%.

- Industry commentary frames the gap between policy and liquidity flows: some observers expect potential easing if geopolitical strains intensify, while others see a gradual expansion of money supply lifting asset prices over time.

Policy stance amid a cloud of uncertainty

With inflation still stubbornly above target and a housing sector that has not fully recovered, the Fed’s decision to hold rates steady reinforces a cautious, data-driven posture. Powell emphasized that the economy’s breadth — including resilient consumer demand and ongoing investment — supports a patient approach to policy normalization. Yet he also acknowledged that the energy-price channel could complicate the inflation outlook if tensions in the Middle East persist or escalate.

The central bank’s balance between supporting employment and curbing inflation remains the defining tension of the moment. The war adds a layer of risk that policy makers must weigh against the need to avoid overtightening in an environment where consumer confidence and business sentiment can swing with energy headlines. In this context, the Fed’s forward guidance will be scrutinized for any signal about the pace and sequencing of future policy moves as new data arrive.

Market path and crypto implications

Traders have largely priced in a stationary policy path in the near term, with a long horizon view depending on how inflation evolves and how geopolitical risks unfold. Data from the Chicago Mercantile Exchange’s FedWatch tool indicated a dominant expectation for no near-term changes, reinforcing a narrative of policy steadiness in the face of uncertainty. The odds of a rate hike at the next specified horizon sit at a slim margin, while the probability of any cuts remains uncertain for the medium term.

Analysts have offered a spectrum of views on how policy could adapt if geopolitical tensions permanently alter the risk landscape. Some market observers, including Arthur Hayes, co-founder of BitMEX, have signaled a preference for lower rates before resuming bullish bets on bitcoin and other crypto assets. He has argued that a rate cut could bolster risk-taking and liquidity, potentially supporting crypto markets as capital seeks higher-yield opportunities.

On the other side of the debate, macro strategist Lyn Alden has described a scenario in which the Fed’s policy stance represents a gradual, ongoing expansion of monetary liquidity. In such a regime, asset prices, including digital assets, could receive support over time even without aggressive rate cuts, provided inflation remains contained and financial conditions remain accommodative enough to sustain broad-based investment activity.

For crypto investors and builders, the Fed’s decision underscores how sensitive risk assets remain to the direction of liquidity and the macro narrative around inflation and growth. A steady policy stance can reduce the impulsive volatility that often accompanies surprise shifts in rate expectations, but the ultimate crypto implication will hinge on how long inflation stays above target, how the labor market evolves, and how energy-price dynamics respond to geopolitical developments.

Beyond the immediate policy path, the relationship between Fed signals and risk assets suggests traders will monitor several ping points: incoming inflation prints, employment data, housing metrics, and evolving energy prices tied to Middle East developments. The crypto market’s sensitivity to liquidity conditions means any durable shift in the rate outlook could quickly reweight risk appetite across tokens, with capital potentially rotating between traditional risk assets and digital instruments tied to alternative financial rails.

As the central bank maintains a calibrated stance, investors should watch how policymakers view the trajectory of inflation in the wake of heightened geopolitical risk. A credible path back toward the 2% target—if energy-price pressures subside or are absorbed without a prolonged disruption—could reopen room for rate normalization. Conversely, persistent or rising inflation would keep policy more restrictive, with potential knock-on effects for both equities and crypto markets.

Looking ahead, the next round of economic data and any fresh guidance from policymakers will be pivotal. If energy prices stabilize and inflation moves closer to target, markets could begin pricing in a more confident glide path, potentially supporting broader risk-taking, including crypto ecosystems that rely on liquidity and favorable financing conditions.

In the meantime, traders and builders in the crypto space should remain attentive to shifts in liquidity and macro narrative. While the Fed’s decision to hold rates steadies some near-term risk, the ongoing Middle East situation remains a critical wildcard that could redefine the pace of policy normalization and, by extension, the appetite for risk across asset classes.

What comes next will hinge on incoming data, the resilience of consumer demand, and how energy markets absorb geopolitical developments. As investors recalibrate, the crypto sector will likely respond to evolving liquidity conditions and the broader assessment of risk appetite in a world where policy and geopolitics remain tightly interwoven.

After the US Securities and Exchange Commission (SEC) outlined four broad categories of digital assets that fall outside securities laws, Chair Paul Atkins offered further clarity on why nonfungible tokens (NFTs) generally do not meet that definition.

In a Wednesday interview with CNBC, Atkins reiterated that the agency’s recent interpretive release identified four types of digital assets that are typically not considered securities: digital commodities, digital tools, digital collectibles such as NFTs, and stablecoins.

During the interview, host Andrew Ross Sorkin pressed Atkins on digital collectibles, noting they could more easily resemble securities depending on how they are structured.

“Well, that’s true with anything,” Atkins replied, emphasizing that the SEC’s analysis still hinges on the facts and circumstances of each asset, particularly whether it involves an investment contract under longstanding legal precedent.

Atkins said digital collectibles are generally treated as items that are bought and held, similar to physical collectibles, rather than as investment contracts — the defining feature of securities.

“Some of these collectibles, like a baseball card, a meme or one of those memecoins, NFTs — those are something that somebody buys,” he said. “It’s an immutable purchase… it’s not something like another asset where people are trading it.”

Related: SEC chair Paul Atkins floats ‘safe harbor’ exemptions for crypto

SEC continues to move away from enforcement-led crypto policy

The securities regulator has recalibrated its approach to digital assets under Atkins, a shift that has coincided with the arrival of a more crypto-friendly Trump administration in early 2025.

“We’re breaking with the past,” Atkins said during the CNBC interview, describing the SEC’s push to provide clearer guidance and a more predictable regulatory framework for the digital asset sector.

Last year, Atkins criticized the agency’s previous reliance on “regulation through enforcement” and pledged to move away from that approach. He also pointed to tokenization as a key innovation that regulators should support rather than restrict.

He has since reiterated that past regulatory missteps have left the United States lagging behind in crypto development by as much as a decade, and has vowed to reverse that trend.

Related: CFTC issues ‘no-action’ letter for crypto wallet provider Phantom

Bitrefill said hackers drained hot wallets and exploited gift card supply flows after gaining access through stolen credentials from an employee’s device.

Bitrefill disclosed that it was targeted in a cyberattack on March 1, which resulted in the theft of cryptocurrency funds, and said its investigation found multiple indicators linking the incident to tactics used by the DPRK-associated Lazarus/Bluenoroff group.

The company stated that similarities in the attackers’ methods, malware, on-chain tracing patterns, and the reuse of IP and email addresses are consistent with previous operations attributed to the group.

Bitrefill Cyberattack

According to the company, the breach originated from a compromised employee’s laptop, where a legacy credential was extracted. That credential allowed access to a snapshot containing production secrets, which the attackers then used to expand their access across Bitrefill’s systems. This enabled them to reach parts of the database and certain cryptocurrency wallets.

In its latest tweet, Bitrefill said it first identified the incident after detecting unusual purchasing patterns involving some suppliers, which indicated that its gift card inventory and supply flows were being misused. At the same time, it observed that some hot wallets were being drained, and funds were sent to addresses controlled by the attackers. Once the breach was confirmed, the company shut down all systems to contain the situation.

Following the incident, Bitrefill confirmed that it has been working with external cybersecurity experts, incident response teams, blockchain analysts, and law enforcement.

The company said there is no indication that customer data was the main focus of the attack. According to its logs, the attackers ran a limited number of database queries consistent with probing activity to identify what could be extracted. This included cryptocurrency and gift card inventory. Bitrefill added that it stores minimal personal data and does not require mandatory KYC, with any verification information held by an external provider.

However, it confirmed that about 18,500 purchase records were accessed, including email addresses, cryptocurrency payment addresses, and metadata such as IP addresses. In roughly 1,000 cases where customers had provided names for specific products, the information was encrypted, but the company is treating it as potentially accessed due to possible exposure of encryption keys. Those users have been notified.

You may also like:

Bitrefill said it does not currently believe customers need to take specific action, but advised vigilance regarding any unexpected communications related to Bitrefill or cryptocurrency.

The company added that it has strengthened its security measures, including conducting further external cybersecurity reviews and penetration testing, tightening internal access controls, improving monitoring and logging systems, and refining incident response procedures. It said the financial losses will be covered from its operational capital, and that most services, including payments and inventory, have been restored.

Lazarus Havoc

Even as many crypto platforms have ramped up their security frameworks in recent years, threat actors continue to bypass protections. The Lazarus Group remains the sector’s most persistent and dangerous adversary, responsible for the largest crypto hack on record after stealing $1.4 billion from Bybit in February 2025.

Blockchain investigator ZachXBT previously said that breaches involving platforms such as Bybit, DMM Bitcoin, and WazirX saw stolen funds laundered with ease. The on-chain investigator had added that the laundering groups have “seemingly won the battle” over enforcement.

Binance Free $600 (CryptoPotato Exclusive): Use this link to register a new account and receive $600 exclusive welcome offer on Binance (full details).

LIMITED OFFER for CryptoPotato readers at Bybit: Use this link to register and open a $500 FREE position on any coin!

Crypto World

Solana (SOL) Network Revenue Plunges 93% From Peak, Why Taurox (TAUX) Is One Of the Best Alternatives

Solana’s network revenue has plunged 93% from its January peak. Daily DEX volume cratered from $35.9 billion on January 21 to $979.5 million by mid-March. Transaction fees dropped 83% in a single month. Active daily addresses fell from 6.4 million to 2.8 million, more than halving since November. The memecoin engine that powered Solana’s fee revenue through Pump.fun and Meteora has stalled after a string of celebrity rug pulls and scam launches that drained user trust. SOL trades at $94, and the on-chain activity that justified higher prices has evaporated.

A 93% revenue collapse is not a correction. It is a structural repricing of what the network actually earns when the hype cycle ends. Taurox (TAUX) is a decentralized hedge fund where AI agents will trade pooled capital across DEXs and CEXs once the presale ends. Stakers keep 80% of net profits from diversified strategies that do not depend on a single network’s fee revenue staying elevated through speculative memecoin launches.

How Triple-Layer Oracle Protection Guards Every Trade

Accurate pricing data is the foundation of every trade an agent will execute. Taurox uses Chainlink as its primary oracle, providing multi-provider aggregated USD pricing across all supported assets. If Chainlink data goes stale or becomes unavailable, Pyth Network steps in as a fallback with high-frequency institutional-grade pricing. Every price feed carries asset-specific staleness thresholds.

If data exceeds the allowed age, the system pauses execution until fresh pricing arrives. On top of both oracle layers, Taurox validates pricing through time-weighted average price calculations using on-chain liquidity pools. This three-layer architecture prevents agents from executing trades on manipulated or outdated data, a risk that grows as more venues and liquidity sources come online.

Stakers keep 80% of net profits at the standard tier. The protocol takes 5% on gains only, with 30% burned permanently and 70% flowing to the DAO treasury. Solana’s revenue depended on memecoin volume that vanished when users lost trust. Taurox protects trade execution at the oracle level so pricing integrity never depends on hype cycle volume.

Why $314.7K in Capital Keeps Flowing While SOL Revenue Falls

Phase 1 of the TAUX presale sold out in under 24 hours at $0.01 per token. Phase 1 buyers are sitting on a 20% gain with Phase 2 priced at $0.012, and they have not staked or seen an agent trade. The presale has raised $314.7K so far, and Phase 2 is already 23.9% filled. Nineteen phases run from $0.01 to $0.07, each closing permanently when its allocation is gone. The price steps up with no extensions.

Waiting costs real money when each closed phase eliminates the cheapest entry forever. Staking activates at the end of the presale, and agents will begin trading real capital once the pool goes live. SOL’s revenue dropped 93% because the activity that generated it was speculative and temporary. The TAUX presale raises capital that positions buyers ahead of a protocol designed to produce returns through managed execution, not through fee spikes from unsustainable memecoin volume.

Every token sold at $0.012 brings Phase 2 closer to closing permanently. The demand that cleared Phase 1 in a single day has carried directly into Phase 2. The buyers entering now are positioning before agents begin trading real capital. Phase 2 is filling, and the entry at $0.012 will not exist once this allocation runs out.

Phase 2 Numbers

Phase 2 is live at $0.012 per TAUX. Listing at $0.08 gives buyers 6.67x before the pool generates profit. A $1 target means x83 from today. At a $1 billion pool with 30% gross returns, implied price reaches $1.85, or x154 from $0.012. The protocol charges 5% on gross profits only. Zero management fees. Thirty percent of that fee is burned permanently against a fixed supply of 2 billion tokens.

The remaining 70% funds the DAO treasury. Every profitable trading period compresses circulating supply against a cap that never increases. The remaining 70% of fees funds the DAO treasury for ecosystem growth. Total raised: $314.7K and climbing. SOL’s revenue cratered 93% because the volume that generated it was temporary. The TAUX presale raises capital backed by a protocol designed to produce returns through managed execution. Phase 2 will not survive the demand pattern that emptied Phase 1 in under a day.

Learn More

Buy TAUX: https://taurox.io/

Whitepaper: https://docs.taurox.io/

Official Telegram: https://t.me/tauroxlabs

The post Solana (SOL) Network Revenue Plunges 93% From Peak, Why Taurox (TAUX) Is One Of the Best Alternatives appeared first on Blockonomi.

S&P Dow Jones Indices has licensed its S&P 500 Index to Trade[XYZ] for the launch of a perpetual futures contract on Hyperliquid, a development described by the index provider as the first officially licensed on-chain product offering continuous, leveraged exposure to the index for eligible non-U.S. users. The contract enables long or short positions on the index without an expiry date, with markets operating around the clock outside traditional exchange hours and data sourced from S&P Dow Jones Indices itself.

The move signals an important pivot in the crypto industry’s appetite for traditional financial benchmarks, extending on-chain derivatives beyond cryptocurrencies into mainstream equity exposure. Trade[XYZ] asserts that its on-chain markets have processed more than $100 billion in volume since October 2025, with an annualized run rate exceeding $600 billion, underscoring growing liquidity in tokenized, perpetual-style products.

Key takeaways

- The S&P 500 is now accessible on-chain through a perpetual futures contract on Hyperliquid, licensed by S&P Dow Jones Indices for eligible non-U.S. users.

- The contract offers 24/7, non-expiring exposure to the index, using official S&P Dow Jones Indices data for pricing and settlement.

- Trade[XYZ] reports on-chain volume surpassing $100 billion since October 2025, with an annualized run rate above $600 billion, highlighting strong liquidity.

- This development follows a July collaboration between the index maker and Centrifuge to bring the S&P 500 on-chain via proof-of-index infrastructure and a tokenized index fund.

- Other major exchanges are expanding perpetuals into traditional assets, including Binance’s TradFi contracts, Kraken’s tokenized futures, and Coinbase’s plan for 24/7 BTC/ETH futures in the U.S.

- Tokenized equities on-chain have grown to roughly $1.09 billion in total value, with Circle Internet Group, Exodus Movement, and Alphabet among the largest holders, per RWA.xyz data.

On-chain access to the S&P 500 and beyond

In a strategic pivot for the crypto market, S&P Dow Jones Indices’ licensing enables Trade[XYZ] to list a perpetual futures contract tied to the S&P 500 index on Hyperliquid. The product is positioned as a pioneering on-chain offering that provides continuous, leveraged exposure to a leading U.S. equity benchmark for eligible non-U.S. users, with pricing and settlement anchored to official index data.

Cointelegraph notes that the contract’s design eliminates expiry dates, a hallmark of traditional perpetuals, while maintaining a governance and data backbone aligned with the S&P 500’s official methodology. The arrangement marks a notable step in integrating established financial benchmarks with blockchain-native trading venues, highlighting a trend toward wider adoption of on-chain derivatives beyond the crypto-native asset class.

Trade[XYZ] emphasizes liquidity and accessibility, pointing to more than $100 billion in on-chain volume since late 2025 and an annualized run rate above $600 billion. While those figures underscore interest, they also set expectations for how quickly institutional-grade benchmarks can scale within a tokenized framework. This data aligns with broader market signals that on-chain perpetuals are moving deeper into traditional assets, offering leveraged exposure with 24/7 trading hours.

The development arrives on the heels of a July collaboration with Centrifuge to put the S&P 500 on-chain through proof-of-index technology and a tokenized index fund built on blockchain-based systems. The aim is to blend the reliability of traditional index construction with the efficiency and accessibility of decentralized infrastructure, potentially lowering barriers to entry for users who want continuous exposure to the benchmark without the constraints of conventional market hours.

Related coverage has framed this as part of a broader shift toward on-chain tokenization of traditional assets and perpetual derivatives, with perpetual DEX activity documented as a burgeoning wave in 2025. The broader context suggests that the S&P 500 on Hyperliquid could be a litmus test for how far on-chain versions of established financial instruments can scale and attract meaningful liquidity.

Expanding perpetuals into traditional markets

The broader crypto industry has been steadily moving toward perpetual-style contracts tied to real-world assets. In January, Binance launched TradFi perpetual contracts, offering USDT-settled derivatives linked to commodities such as gold and silver with around-the-clock trading and no expiry. The following month, Kraken expanded this model to equities, introducing tokenized perpetual futures that provide leveraged exposure to U.S. stock indexes, gold, and select companies.

Earlier in the year, Coinbase signaled plans to introduce round-the-clock trading for Bitcoin and Ether futures in the U.S. and to broaden its perpetual-style contracts. These moves collectively illustrate a converging path where crypto-native platforms seek to bridge on-chain liquidity with traditional asset classes, potentially widening the audience for perpetuals beyond pure crypto traders.

In parallel with these developments, tokenized equities have continued to grow on-chain. Data from RWA.xyz shows total on-chain value rising to about $1.09 billion from roughly $300 million at the start of 2025. The market remains relatively concentrated, with Circle Internet Group among the largest holdings at roughly $136.8 million, followed by Exodus Movement at about $83 million and Alphabet at around $72.9 million. Tesla and the iShares Silver Trust also feature prominently among on-chain holdings.

These numbers highlight a developing ecosystem where traditional brands and asset classes appear on-chain in a way that can complement or compete with existing financial channels. While on-chain equity exposure remains a small slice of the overall market, the velocity of growth and the involvement of mainstream players suggest a structural shift in how investors access diversified, time-unconstrained exposure to real-world assets.

For readers tracking the evolving landscape, these arrangements reinforce the importance of watching regulatory developments, market liquidity, and the quality of reference data that underpins on-chain pricing and settlement. The S&P 500 on Hyperliquid, and similar products in the pipeline, could shape user behavior, risk management practices, and the competitive dynamics between centralized and decentralized venues for traditional-asset derivatives.

Sources and related coverage include Cointelegraph’s reporting on perpetuals growth and the Centrifuge collaboration to bring the S&P 500 on-chain, as well as ongoing industry notes on TradFi perpetuals from major crypto exchanges and tokenized-equity data from RWA.xyz. For a deeper look at the broader trends in on-chain derivatives and tokenized assets, see the linked materials and ongoing industry analysis.

The Bank of Korea and nine commercial lenders began phase two of a digital won pilot, testing bank-issued deposit tokens backed by central bank infrastructure to determine whether the system can support government subsidy payments and consume transfers and payments nationwide.

The second phase of Project Hangang adds two banks, Kyongnam Bank and iM Bank, to the program’s original seven. The institutions will now begin large-scale testing of the won-pegged deposit tokens built on a wholesale central bank digital currency (CBDC) layer, several local news outlets reported.

“Participating banks are actively securing diverse use cases, such as large businesses and small merchants with high public relevance and significant payment fee burdens, focusing on the potential for drastically reduced fees when using digital currency for payments,” said Kim Dong-sub, who heads the Bank of Korea’s digital currency planning team, according news outlet Chosun,

A key goal is to reduce the cost of transactions. By utilizing the deposit tokens, the BOK hopes to offer a lower-cost payment alternative for both large companies and small businesses that are currently burdened by credit card processing fees, according to the bank.

The Phase 2 start comes as South Korea’s Digital Asset Basic Act (DABA), a sweeping framework meant to govern crypto trading and issuance in one of Asia’s most active digital asset markets, is delayed because of disagreements among regulators over stablecoin issuance. The thorniest issue centeres on who should have the legal authority to issue KRW-pegged stablecoins.

In the new tests, peer-to-peer transfers, which were challenging in Phase 1, will become possible.

Kim also said “the government aims to begin disbursing subsidies in digital currency during the first half of this year,” with electric vehicle charging infrastructure subsidies expected to be among the first use cases.

The Bank of Korea also mentioned plans to enable digital currency as a payment method for ‘AI agents’, which are artificial intelligence systems that search for and purchase goods and services.

Tehran Sends Strong Signals in the Face of Escalation

According to the statements made by the Iranian authorities, the political and military organization of the country is stable enough to lose the leadership. According to Foreign Minister Abbas Araghchi, the institutions were operating normally. Besides, authorities reiterated that personal losses cannot undermine the system at large. These utterances are meant to show strength as the war spreads.

The oil prices shifted downwards with the escalation of geopolitical tensions in the Middle East. The prices of crude fell by over 3 percent and closed at around 92 in the last trade period. Nevertheless, markets responded to a stable supply situation and not to conflict risks. None of the significant disturbances in production or shipping of oil constrained price pressure.

The activity of shipping via the Strait of Hormuz was maintained at a moderate rate, which sustained a stable supply globally. Further, Iran permitted some commercial ships to pass through the important passage. Furthermore, Iraq and Kurdish leaders started again with oil exports through the Ceyhan port of Turkey. The situation created an addition to the supply chain in the international markets and lessened the apprehensions concerning scarcity.

Sanctions relief pushes in the wrong direction

The United States gave a temporary lift on sanctions imposed on the Russian oil shipments stuck at sea. This move gave it the opportunity to supply more supply to the international markets in the short run. As a result, the availability of crude was elevated, weighing on prices even though conflict risks were still there. Even a minor addition of supply, observed by analysts, could have an impact on prices in the existing circumstances.

Geopolitical risks are still pitted against stable supply flows by energy markets. Although tensions are strong, traders are focusing on real disruption of the situation as opposed to possible threats. Also, the existent equilibrium between the supply and demand has curbed price spikes. The oil markets are still sensitive to the developments as the conflict goes on.

Bitcoin’s hash rate is tumbling as the Middle East conflict drives up energy prices, adding pressure to the mining sector and broader market.

The drop in hash rate is likely tied to geopolitical tensions due to the war against Iran and surge in oil prices, given that an estimated 8% to 10% of global bitcoin mining operates in energy markets sensitive to energy costs.

With hash rate down roughly 8% over the past week to 920 EH/s, the network may be entering another phase of miner capitulation. Historically, such periods have coincided with downside pressure on bitcoin’s price, which is currently trading below $72,000, roughly 5% below its Monday high.

As a result, the network is set for an approximately 8% downward difficulty adjustment, which would mark the second-largest negative shift in the past five years, according to mempool.space.

This decline follows one of the largest difficulty drops on record in mid-February, highlighting significant volatility in mining activity.

As a result of rising competition, persistently low transaction fees, and bitcoin price volatility, this has squeezed margins and pushed many publicly traded miners to diversify into AI and high-performance computing, alongside increased bitcoin sales to support operations, acting as a headwind for the bitcoin price.

The Federal Reserve Open Market Committee (FOMC) announced on Wednesday that it would hold the Federal Funds rate steady at 3.5-3.75%, as it monitors macroeconomic impacts from the ongoing war in the Middle East.

Economic activity has expanded at a “solid pace,” Federal Reserve Chairman Jerome Powell said, adding that consumer spending remains “resilient,” while business investment continued to grow.

However, the housing sector remains weak, and the labor market shows signs of softening, Powell said, while inflation remains “somewhat elevated” above the Fed’s 2% target.

This higher inflation and weak labor market is creating a tension between the Federal Reserve’s dual mandate of maximizing employment and stabilizing prices, Powell Said. He added that the war in the Middle East has further clouded the economic outlook. He said:

“The implications of events in the Middle East for the US economy are uncertain in the near term. Higher energy prices will push up overall inflation, but it is too soon to know the scope and duration of the potential effects on the economy.”

Interest rate policy impacts risk asset markets like cryptocurrencies and equities, with lower rates stimulating asset prices and higher rates acting as a restrictive force on risk asset prices, as investment capital flows from riskier asset classes to government bonds.

Related: Fed holds rates amid higher inflation outlook: Bitcoin bounces to $72K

Traders see no chance of rate cuts, while analysts say liquidity will flow

97% of market participants forecast no change in interest rates at the April 2026 FOMC meeting. While 3% forecast a rate hike of 25 basis points (BPS), according to data from the Chicago Mercantile Exchange (CME).

A rate hike of 25 basis points would spike the Federal Funds Rate to a range between 3.75% and 4.00%.

Arthur Hayes, a market analyst and co-founder of the BitMEX crypto exchange, said he is waiting for the Fed to slash rates before he resumes buying Bitcoin (BTC).

Hayes also said that the ongoing war between the US and Iran would likely cause the Federal Reserve to ease monetary policy to finance the war.

Others, like macroeconomist Lyn Alden, say that the Federal Reserve has entered a “gradual print” phase in which new money is steadily being created, slowly raising up all asset prices.

Magazine: Is China hoarding gold so yuan becomes global reserve instead of USD?

Arsenal to Face Sporting, Liverpool Drawn Against PSG in Champions League Quarter-Finals

Compass drops lawsuit against Zillow over home-listing policy

Road closures planned at Bridgend industrial estate

Smart energy pays enters the US market, targeting scalable financial infrastructure

Why Israel is blocking foreign journalists from entering

Bitcoin: We’re Entering The Most Dangerous Phase

Tom Lee Bitcoin: “People Have NO IDEA What’s Coming…” (Time To BUY) | Bitcoin Price 2026

Live Trading || Crypto and Gold | 17 March | – IITian Trader #cryptotrading

Amazing Cardboard Gadget That Turns Paper Into Money #techgadgets #ytshorts

-

Crypto World5 days ago

Crypto World5 days agoHYPE Token Enters Net Deflation as HyperCore Buybacks Outpace Staking Rewards

-

Tech3 days ago

Tech3 days agoYour Legally Registered ‘Motorcycle’ Might Not Count Under Proposed US Law

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Addict Lip Glow

-

Sports4 days ago

Why Duke and Michigan Are Dead Even Entering Selection Sunday

-

Tech1 day ago

Tech1 day agoAre Split Spacebars the Next Big Gaming Keyboard Trend?

-

Business3 days ago

Business3 days agoSearch for Savannah Guthrie’s Mother Enters Seventh Week with No Arrests

-

Business4 days ago

Business4 days agoUS Airports Launch Donation Drives for Unpaid TSA Workers as Partial Government Shutdown Enters Fifth Week

-

Crypto World4 days ago

Coinbase and Bybit in Investment Talks: Could Bybit Finally Enter the US Crypto Market?

-

Business3 days ago

Business3 days agoAustralian shares drop as Iran war enters third week

-

Business4 days ago

Business4 days agoCountry star Brantley Gilbert enters growing non-alcoholic beer market

-

Crypto World3 days ago

Crypto World3 days agoCrypto Lender BlockFills Enters Chapter 11 with Up to $500M in Liabilities

-

Sports5 days ago

Sports5 days agoCollege Basketball Best Bets: Conference Tournament Semifinal Picks

-

Politics14 hours ago

Politics14 hours agoThe House | The new register to protect children from their abusers shows Parliament at its best

-

Crypto World7 days ago

Crypto World7 days agoThree Binance Charts May Be Hinting at Bitcoin’s Next Move

-

Business6 days ago

Business6 days agoTrump demands Powell cut rates as Iran conflict raises energy prices

-

Crypto World6 days ago

Crypto World6 days agoSenate Votes to Include CBDC Ban in Bipartisan Housing Bill

-

Fashion3 days ago

Fashion3 days ago25 Celebrities with Curly Hair That Are Naturally Beautiful

-

News Videos6 hours ago

News Videos6 hours agoRBA board divided on rate cut, unusually buoyant share market | Finance Report | ABC NEWS

-

NewsBeat6 days ago

NewsBeat6 days agoDeane Road crash near Bolton colleges and university

-

News Videos6 days ago

News Videos6 days agoTom Lee: The 100x Opportunity EVEN Bigger Than Bitcoin (New Ethereum Prediction 2026)

You must be logged in to post a comment Login