Crypto World

MARA Bitcoin miner posts $1.7B quarterly loss as BTC slumps

In its latest quarterly update, MARA Holdings confronted a stark reality: even as its bitcoin mining fleet generated fewer coins, the company’s balance sheet was weighed down by falling crypto valuations and a strategic pivot away from pure mining. MARA reported a fourth-quarter 2025 net loss of $1.71 billion, or $4.52 per diluted share, compared with a year-earlier net income of $528.3 million. Revenue slipped 6% year over year to $202.3 million, as a softer Bitcoin (CRYPTO: BTC) price offset a higher hashrate. For the full year, the firm posted a net loss of $1.31 billion on revenue of $907.1 million, reversing 2024’s $541 million profit.

Key takeaways

- MARA’s Q4 2025 net loss was $1.71 billion and revenue was $202.3 million, with earnings pressured by the decline in BTC prices despite a higher mining hashrate.

- For the full year 2025, the company recorded a net loss of $1.31 billion on $907.1 million in revenue, reversing 2024’s profit as crypto prices remained volatile.

- A $1.5 billion negative adjustment to the fair value of digital assets and receivables contributed to the quarterly loss, reflecting BTC price declines from around $114,300 on Sept. 30 to $88,800 on Dec. 31 (per CoinGecko).

- MAR A’s BTC holdings at year-end totaled 53,822, with 15,315 pledged or loaned, and the balance-sheet BTC carried a roughly $4.7 billion value at quarter-end prices.

- The company unveiled a strategic pivot into AI and high-performance compute, including a joint venture with Starwood Digital Ventures to build data centers at power-rich sites, initially targeting more than 1 GW of IT capacity and potentially expanding to 2.5 GW.

- In February, MARA acquired a 64% stake in Exaion to pursue sovereign-grade and enterprise AI deployments as part of the broader diversification plan.

Tickers mentioned: $BTC, $MARA

Sentiment: Bearish

Price impact: Negative. MARA’s stock has fallen about 46% over the past six months as results and strategic pivots weigh on investor sentiment.

Trading idea (Not Financial Advice): Hold. While the transition toward AI/HPC is notable, near-term investors should watch project execution and BTC price stability before reassessing risk/reward.

Market context: The results come amid a broader crypto downturn where mining economics remain sensitive to BTC price swings, regulator signals, and capital allocation shifts among miners pursuing diversified revenue streams rather than pure hodling or mining.

Why it matters

The quarterly and annual figures underscore a pivotal moment for MARA as it moves beyond a pure-play bitcoin miner toward an energy and digital infrastructure company. The heavy accounting hit from the fair value of digital assets illustrates how price volatility can disproportionately affect mining-focused models, even when production levels hold steady or improve. By contrast, the balance sheet remains robust in crypto terms, with a substantial BTC stash that, on paper, still carries significant value given the ongoing, albeit uneven, interest in asset-backed mining operations.

Beyond the numbers, the strategic pivot is the centerpiece. MARA’s collaboration with Starwood Digital Ventures aims to unlock a significant AI/HPC footprint on existing energy-rich sites, a move that could open new revenue channels independent of BTC cycles. The plan envisions more than 1 gigawatt of IT capacity in the initial phase, with a roadmap to exceed 2.5 GW over time. Crucially, MARA retains the option to invest up to 50% in individual projects, while continuing to mine where power remains economical. This hybrid model reflects a broader industry trend: miners seeking to hedge against crypto price volatility by anchoring operations in data centers and AI workloads that can generate steady, long-term demand.

Additionally, the February acquisition of a 64% stake in Exaion signals a concrete push into AI deployments that could leverage MARA’s grid-scale energy footprint. Exaion’s focus on sovereign-grade and enterprise AI deployments aligns with the growing demand for specialized compute resources, particularly at the intersection of crypto mining infrastructure and high-performance compute networks. As more miners explore blended business models, MARA’s approach stands out for attempting to formalize AI-centric data center capacity alongside mining operations.

In comparison, peers are testing similar pivots with varying degrees of commitment. Some miners are leaning into large AI data-center leases, while others continue to emphasize a combined strategy of mining and hoarding BTC to preserve, and potentially grow, crypto exposure. The sector’s direction remains dependent on macro conditions, including BTC price trajectories, energy costs, and regulatory developments that could influence the economics of large-scale mining and data-center deployments alike.

The financials also hint at the balancing act between growth investments and shareholder value. If the Starwood joint venture and Exaion initiatives deliver on capacity and utilization, MARA could unlock a multi-year path toward diversified cash flows. Yet the immediate picture is clouded by historical volatility in the crypto markets and the challenge of turning large capex programs into near-term profits. Investors will be watching how the company manages capital deployment, debt, and any potential tranche financing to accelerate its AI/HPC push while supporting ongoing mining operations.

The company’s overall strategy, while ambitious, mirrors a broader move within the crypto hardware space toward building resilient, diversified platforms. As data centers become a more common anchor for crypto firms, MARA’s ability to translate capacity into meaningful revenue streams will be a key test for the model’s sustainability in a market where price signals for BTC remain bifurcated and often unpredictable.

What to watch next

- Progress updates on the Starwood Digital Ventures AI/HPC data-center partnership, including projected milestones for the initial >1 GW capacity and any expansions toward 2.5 GW.

- Operational and financial details on Exaion deployments and contracts, particularly any sovereign-grade AI projects and enterprise compute commitments.

- Bitcoin price movements and realized/batched mining yields as MARA advances its hybrid strategy, plus any changes to the company’s balance-sheet BTC position or collateral arrangements.

- Any capital-raising efforts, debt restructurings, or financing agreements tied to the new AI/HPC initiatives and data-center builds.

- Regulatory developments affecting crypto mining, energy use, and AI infrastructure deployments that could impact project economics or timelines.

Sources & verification

- MARA Holdings Q4 2025 shareholder letter filed with the SEC (SEC: q425shareholderletter.htm).

- Bitcoin price data used for the fair value discussion (CoinGecko: bitcoin).

- Company updates and stock performance coverage (Yahoo Finance: MARA).

- Exaion stake and AI/HPC deployments referenced in MARA communications (Cointelegraph article on Exaion stake).

Key figures and next steps

What the announcement changes

The fourth quarter reports reveal a company navigating a difficult macro environment for mining while actively pursuing a structural shift toward AI-enabled data centers. If successful, the Starwood JV and Exaion partnerships could provide MARA with nonmining revenue streams that weather BTC price cycles. The path forward will hinge on project execution, the pace of capacity buildup, and the ability to translate compute demand into sustained profitability.

Sources & verification

- SEC filing: q425shareholderletter.htm

- CoinGecko data: bitcoin

- Yahoo Finance: MARA

- Exaion stake coverage: Cointelegraph

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

As traditional assets move on-chain, investors turn to decentralized finance and utility-driven tokens like BlockchainFX (BFX) amid rising global market volatility.

Summary

- Institutional liquidity flows into DeFi as traders seek high-yield opportunities in volatile global markets

- BlockchainFX (BFX) positions as a multi-asset Super App bridging crypto, stocks, forex, and ETFs

- BFX has introduced a revenue-sharing model with staking rewards, buybacks, and token burns to support value growth

Global market volatility remains high today as institutional liquidity flows into decentralized finance at record speeds. Traditional assets are moving on-chain while traders seek high-yield opportunities in emerging utility sectors. Smart participants are now looking at the next 100x crypto, BlockchainFX (BFX).

BlockchainFX (BFX) recently entered the spotlight with a robust debut, aiming to solve the liquidity gap between traditional and digital markets. Major assets like Cardano (ADA) continue to dominate headlines as the community prepares for the discussed market shift.

Cardano price prediction: Detailed forecast for 2026

Cardano news highlights a steady growth path for this academic blockchain giant. Based on technical analysis, the Cardano price prediction for 2026 suggests a yearly low of $0.35 and a potential high of $1.15. This indicates significant upside if the ecosystem maintains its current development trajectory.

Looking further ahead, the Cardano price remains a point of interest for long-term early adopters. Estimates for 2027 project a range between $0.39 and $0.83, while the 2030 forecast shows a potential peak of $1.02. This makes the coin a solid choice for those seeking stability over rapid volatility.

BlockchainFX: The next 100x crypto redefining trade

BlockchainFX (BFX) is the ultimate licensed Super App that bridges the $7.5 Trillion daily Forex market with the growing world of crypto. While most exchanges ignore traditional assets, BFX allows trading of over 500 assets, including Stocks, Gold, and ETFs, from one web3 interface. This project solves the fragmentation problem by giving early adopters a single point of entry for all financial needs.

The unique selling point is the massive 70% revenue-sharing model. Instead of the platform keeping all the profit, 50% of trading fees go back to stakers in daily USDT and BFX. Another 20% is used for market buybacks, with half of those tokens burned to keep the supply low and the value high.

Feature

BlockchainFX Benefits

Current Price

$0.035

Confirmed Launch Price

$0.05

Daily Rewards

Paid in USDT and $BFX

Compliance

CertiK Audited and Fully Licensed

Early buyers are rushing to secure tokens before the supply hits the open market. With 22,950+ participants already onboard, the momentum is undeniable. This is the chance to get in at the floor price before the official listing.

- 18-Karat Gold Visa Cards: Exclusive to high-tier BFX crypto presale 2026 participants for global spending.

- Massive Trading Credits: Up to $25,000 in credits for the Legend tier to use on the Super App.

- Daily Passive Income: Immediate staking starts the moment you join the crypto presale.

Big announcement: The 15 million launch trigger is near

The energy is reaching a boiling point because the finish line is in sight. BlockchainFX has already raised over 14.18 million. The core team officially announced that the moment the presale hits the 15M mark, BFX will launch on major exchanges. There is very little time left to grab the BFX crypto presale 2026 at these entry levels.

To celebrate this milestone, the bonus code LAUNCH50 is active, giving participants 50% extra tokens on their purchase. This crypto presale is moving at lightning speed, and the 15M goal is just around the corner.

Can BlockchainFX become the next 100x crypto?

Every cycle produces a breakout star that changes the game for early adopters. Cardano provides steady utility according to its price prediction, but the massive growth potential of the BlockchainFX presale offers a different level of opportunity. Its unique revenue-sharing and multi-asset trading model make it a standout choice for any diversified portfolio.

The current BlockchainFX presale price of $0.035 is a rare entry point before the $0.05 launch. Use code LAUNCH50 for a 50% bonus and start earning daily USDT rewards immediately. With 14.18 million raised, the 15 million launch trigger is imminent. This could be the next 100x crypto investors wouldn’t want to miss.

For more information, visit the official website, X, and Telegram.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

Crypto World

Zcash price cools after parabolic run as derivatives froth flashes risk, is $400 in range?

Zcash price is trading around $378 after a parabolic 60% weekly rally, with volume and leverage surging to levels that signal a late‑stage momentum blow‑off rather than calm accumulation.

Summary

- ZEC is up roughly 21% in 24 hours and about 60% over the past week, making it one of the strongest‑performing large‑caps on major trackers.

- 24‑hour spot volume has jumped above $1.0b while futures open interest sits near $3.39b, pointing to aggressive leveraged longs and short squeezes.

- RSI on ZECUSDT is firmly overbought near 73 and MACD remains bullish, a combination that supports the uptrend but raises the risk of a sharp mean‑reversion if leverage unwinds

Zcash (ZEC) price is trading around $378 after a parabolic move that left it up roughly 21% in 24 hours and about 60% over the past week, putting it among the most explosive large‑caps in the market. 24‑hour spot volume has surged above $1.0 billion against a significantly smaller market capitalization, while open interest in ZEC futures stands near $3.39 billion, signaling aggressive leveraged positioning rather than slow spot accumulation.

RSI on major timeframes sits firmly above 70 with a ZECUSDT reading near 73, and momentum indicators such as MACD remain bullish, setting up a late‑stage trend regime where upside is possible but the risk of a sharp mean‑reversion spike lower is high if leverage unwinds.

Zcash is trading near $378 on April 10, 2026, extending a vertical surge that has pushed the privacy coin up roughly 21% in 24 hours and about 60% over the past seven days, according to TradingView and other price trackers. The current level marks one of the strongest weekly performances among large‑cap altcoins, with ZEC reclaiming territory last seen during prior speculative spikes.

Spot volume has jumped to more than $1.0 billion in the last 24 hours, a figure that is extremely elevated relative to ZEC’s market capitalization and consistent with aggressive chase rather than quiet institutional accumulation. On the derivatives side, data from CoinGlass shows ZEC open interest at roughly $3.39 billion, a level that indicates heavy use of leverage, with earlier episodes of the rally already associated with tens of millions of dollars in short liquidations over 24‑hour windows.

Technically, multiple momentum dashboards flag ZEC as overbought. TradingView’s ZECUSDT technical summary shows a 14‑period RSI reading near 73, in the sell/overbought zone, while the Commodity Channel Index prints around 179 and the Momentum (10) indicator is elevated, all pointing to a stretched move. At the same time, the MACD level remains positive, confirming that the trend is still up even as risk builds.

This combination—a strong, intact uptrend but increasingly overheated oscillators and heavy derivatives exposure—is typical of a momentum blow‑off phase. Price, volume and open interest are all pointing in the same direction, suggesting that recent gains have been fueled by fresh long leverage and forced short covering rather than fundamental re‑rating. If open interest begins to roll over or funding spikes, the setup favors a sharp mean‑reversion move back toward prior consolidation zones.

In that context, traders looking at ZEC around $378 face an asymmetric choice. Trend‑followers may still see room for continuation as long as price holds recent higher lows and momentum remains positive, but any clear break of short‑term support levels on rising volume would likely trigger a cascade of long liquidations after such a steep run. With ZEC now trading well above levels highlighted in earlier TradingView studies and derivatives positioning near local extremes, the next major move is likely to be defined less by new buyers and more by how quickly leveraged positions are forced to unwind.

Crypto World

Best Crypto Portfolio for April 2026 Misses One Presale That ETH and BNB Alone Cannot Replace

Stablecoin inflows to exchanges just hit $778 million in a single week, confirming capital is pouring back into crypto at a pace not seen since the last bull run started. But the best crypto portfolio for April 2026 is not built from large caps alone.

The wallets that caught the biggest returns every cycle held one presale entry alongside their blue chips.

Pepeto crossed $8.87 million raised during extreme fear with the cofounder who built the original Pepe coin, a SolidProof audit, and a Binance listing that turns the presale floor into history.

Stablecoin Inflows Hit $778 Million as Recovery Capital Floods Back Into Crypto

Stablecoin inflows to exchanges reached $778 million this week per CoinGecko. The spike follows the Iran ceasefire that sent BTC above $72,000 and wiped $600 million in shorts.

Morgan Stanley’s spot Bitcoin ETF pulled $34 million on day one per CoinDesk, and the best crypto portfolio for this recovery phase needs presale exposure where the gap between entry and listing carries the highest return.

How ETH, BNB, and Pepeto Fit Into the Best Crypto Portfolio This Cycle

Pepeto: The Presale Piece That Turns a Good Portfolio Into a Great One

ETH and BNB give a portfolio its foundation, but every cycle the portfolios that actually changed lives had one presale entry that outweighed everything else combined. That is the role Pepeto fills right now, and no large cap at current prices can replace what a presale to listing gap delivers.

The exchange is already live. Zero fee swaps, a cross chain bridge at zero cost, and a contract scanner that flags scams before money moves are all running and handling real activity. That separates Pepeto from every presale still stuck at the whitepaper stage.

The presale reached $8.87 million while fear gripped the market and most tokens were bleeding, proving the capital flowing in is smart money, not hype chasers. The builder behind the first Pepe token who took 420 trillion coins to $11 billion with zero products is now doing it with a full exchange behind it, a SolidProof audit covers every contract, and 186% APY staking quietly builds positions while the listing gets closer.

At $0.0000001863, analysts model 100x to 300x, and the pace keeps picking up because the wallets inside know the listing wipes this entry off the table permanently. The best crypto portfolio in 2026 is the one that added Pepeto before that moment, and waiting means watching the return from the outside.

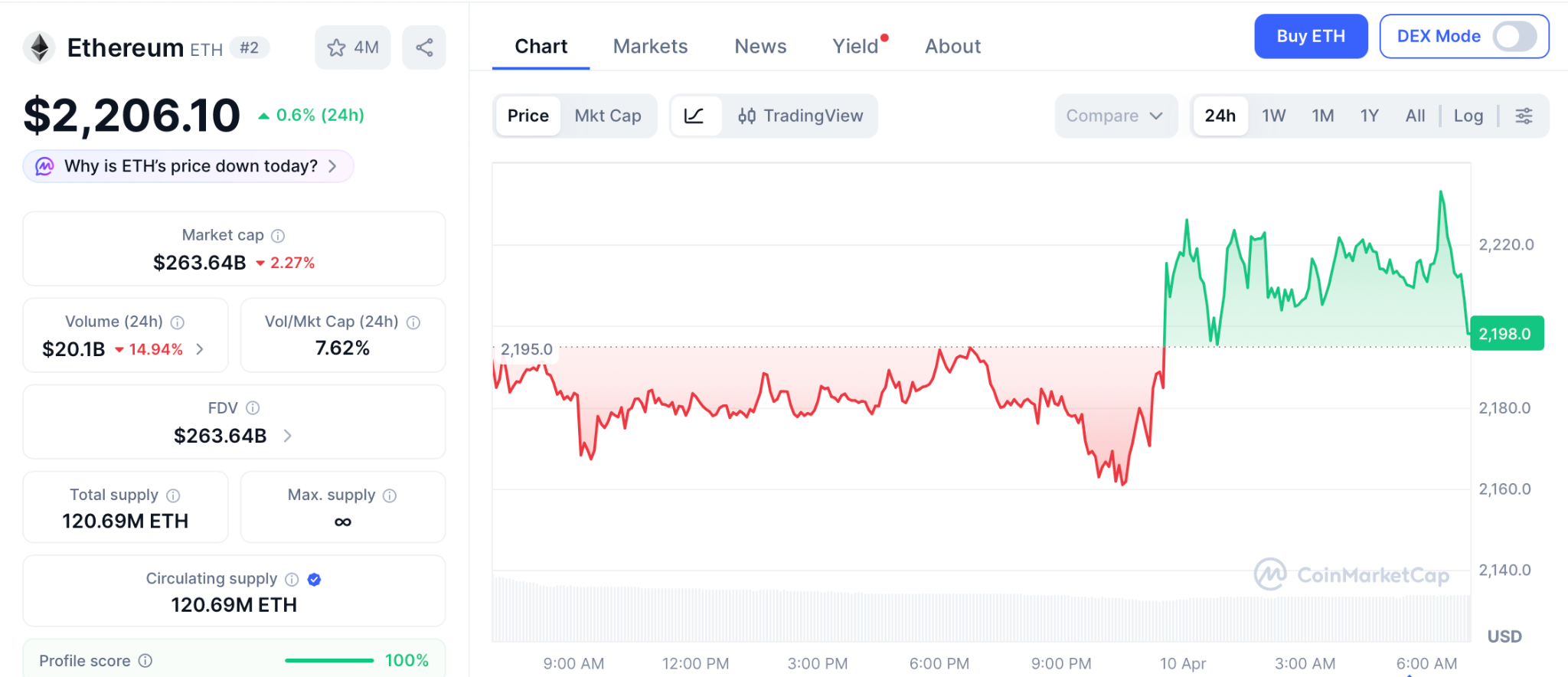

Ethereum: ETH Anchors Portfolios but Growth Stays Limited

ETH holds near $2,206 with institutional buying continuing after the ceasefire bounce per CoinMarketCap.

Trend Research now holds over 580,000 ETH, the MVRV ratio signals a historic buying zone, and the Ethereum Foundation staked 70,000 ETH worth $143 million this month to reduce sell pressure.

ETH belongs in every best crypto portfolio as the base layer, but from $2,206 the percentage gains that reshape a position need years while presale entries hold the presale to listing spread where the biggest returns live.

BNB: Stable Foundation but the Ceiling Is Clear

BNB trades near $604 supported by quarterly burns and exchange volume per CoinMarketCap. New listings on Binance historically lift BNB demand as traders move capital onto the platform, and the upcoming Pepeto listing adds another event to the calendar.

BNB adds stability to any best crypto portfolio, but from $604 the path to $900 delivers roughly 50%, far below what a presale entry at floor price produces when the listing opens the full gap between entry and market price.

Conclusion

$778 million in stablecoin inflows proves the recovery is building, and the wallets putting together the best crypto portfolio are looking past large caps toward the presale entry that carries the widest return. Pepeto has the live exchange, the audit, the Pepe cofounder, and $8.87 million in capital to back it.

The presale floor gets replaced permanently on listing day, and the portfolios that added Pepeto before that moment are the ones that outperform everything else this cycle. The entry exists right now, and every hour closer to the listing is one hour less before it disappears.

Click To Visit Pepeto Website To Enter The Presale

FAQs

What belongs in the best crypto portfolio for 2026?

ETH and BNB form the foundation, but Pepeto at $0.0000001863 with a confirmed Binance listing adds the presale to listing gap where the largest returns every cycle get built. The project raised $8.87 million with a live exchange.

How do stablecoin inflows affect the best crypto portfolio?

$778 million flowing into exchanges confirms recovery capital is arriving at scale. Presale entries like Pepeto capture more of that wave than large caps already priced near their recovery targets.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

Bitcoin moved from $72,000 to $72,400 on April 10 after March core CPI printed below expectations, giving crypto bulls a short-lived reprieve from months of sustained macro pressure.

Summary

- March core CPI rose just 0.2%, below the 0.3% consensus forecast, while headline CPI climbed 0.9% on war-driven oil prices.

- Bitcoin ticked up to $72,400 within minutes of the 8:30 AM ET release before pulling back near $72,000.

- The soft core print eased immediate rate hike fears but did not shift the broader Federal Reserve policy outlook.

Bitcoin (BTC) price update: BTC climbed from roughly $72,000 to $72,400 on April 10 after the Bureau of Labor Statistics reported that March core CPI rose just 0.2%, coming in below the 0.3% consensus forecast, according to CoinDesk. Headline CPI rose 0.9% on the month, driven by a roughly 10.9% surge in energy costs tied to the ongoing Middle East conflict, keeping annual inflation at 3.3%. Core CPI came in at 2.6% year-on-year, slightly below the 2.7% economists had forecast.

The below-forecast reading gave crypto traders a short-lived reason to add exposure. Bitcoin rose in the minutes following the release, with FXLeaders noting that BTC “reclaimed $72,000 as macro fears fuel appetite for digital scarcity.” The move was measured rather than explosive, reflecting a market still navigating sticky headline inflation against a softer underlying trend. As crypto.news noted, the inflation print “came in line with expectations” at the headline level, easing fears of an even hotter surprise while confirming that price pressures remain elevated but stable.

The distinction matters for traders. A softer core number reduces the probability of an aggressive Fed pivot toward tightening. But with annual headline CPI running at 3.3%, the highest reading since May 2025, the Fed has little political or economic space to move toward cuts.

Fed Stays Cautious as Oil Keeps Headline Inflation Elevated

The soft core figure did not meaningfully shift Federal Reserve rate expectations. With the Strait of Hormuz still constrained by the ongoing conflict, energy prices remain a structural upward force on monthly CPI readings, complicating the Fed’s near-term calculus. Markets currently price near-zero odds of a rate reduction in the coming months.

As crypto.news tracked ahead of the release, analysts had outlined a directional framework: a cooler core print could open a path toward $74,000 to $76,000, while a hotter reading risked a retest of the $68,000 support zone. The actual print landed in the middle, producing a modest rally that stalled short of $73,000.

What Traders Are Watching Next

Bitcoin remains range-bound near $72,000, with $73,000 acting as the immediate ceiling. The level has capped every rally since the ceasefire was announced six weeks ago. Analysts broadly agree that a sustained break above $75,000 is needed before the market can enter a genuine new leg higher. Attention now shifts to weekend US-Iran negotiations in Islamabad and whether progress toward a durable peace deal could remove the geopolitical overhang that has weighed on prices across all risk assets.

Bitcoin institutions are betting on both sides of the market at $72,000, buying $80,000 call options while simultaneously purchasing downside protection, as Friday’s CPI data and US-Iran peace talks in Islamabad leave direction entirely unclear.

Summary

- Institutional traders are buying $80,000 call options while also loading downside protection.

- Bitcoin has stalled at $72,000 as investors await clarity from the CPI print and Iran ceasefire talks.

- US-Iran peace negotiations in Islamabad this weekend could provide the next decisive directional catalyst.

Bitcoin has been range-bound near $72,000 on April 10, with institutional positioning reflecting deep uncertainty about the next major move. Investors are not choosing a direction; they are hedging both sides simultaneously.

According to CoinDesk, institutions are buying call options targeting $80,000 while simultaneously purchasing puts for downside protection. That dual positioning reflects hesitation rather than conviction, with neither bulls nor bears willing to fully commit ahead of this weekend’s geopolitical and economic catalysts.

Trump said he was “in deep negotiations” with Tehran heading into the Islamabad talks, and the gap between a deal and a breakdown has left institutional traders unwilling to pick a side. Bitcoin has traded in a range of roughly $65,000 to $73,000 since the Iran war began.

CPI and Iran Talks Are the Two Key Catalysts

Friday’s US inflation report came in softer than expected on core measures, with core CPI rising just 0.2% against a 0.3% forecast. The print eased some short-term rate fears but did not provide enough clarity to break Bitcoin out of its established range.

The more consequential event may be the Islamabad talks. As crypto.news reported, a fragile two-week ceasefire was agreed last Wednesday, but investor caution has persisted as the Strait of Hormuz remains only partially reopened and Iran has proposed a $1 per barrel crypto toll on tanker passage.

What a Resolution Could Mean for Price

As crypto.news noted, a confirmed agreement could open the door for a move toward the $75,000 region, as easing tensions would support risk appetite across financial markets. Failure to reach a deal could shift sentiment in the opposite direction, with Bitcoin retesting lower support levels and altcoins bearing the heavier losses.

The Iran peace talks that energy and financial markets have been tracking for weeks are underway today in Islamabad, with Vice President JD Vance joining envoys Steve Witkoff and Jared Kushner for the first face-to-face meeting since the fragile two-week ceasefire was brokered by Pakistan.

Summary

- JD Vance is heading to Islamabad today to join Steve Witkoff and Jared Kushner in direct negotiations with Iran.

- This is the first face-to-face meeting since Pakistan brokered the fragile two-week ceasefire last week.

- The outcome could directly move oil, crypto, and global financial markets depending on whether a durable agreement is reached.

The highest-stakes diplomatic event since the six-week US-Iran war began is now underway in Pakistan’s capital. Vice President JD Vance arrived in Islamabad on April 10 to join the American negotiating team for direct talks with Iranian officials, a meeting that markets have been pricing for days.

Vice President Vance is joining US Special Envoy Steve Witkoff and Jared Kushner, who led earlier negotiating rounds that were derailed twice when US and Israeli air strikes resumed. According to Democracy Now!, Vance’s presence signals Washington is treating this as the final opportunity to secure a durable agreement before military options are reconsidered.

Pakistan brokered what sources describe as the “Islamabad Accord” framework, a two-phase plan beginning with an immediate ceasefire and leading into negotiations for a permanent end to the conflict and the full reopening of the Strait of Hormuz. As crypto.news reported, last week’s ceasefire triggered a sharp drop in oil prices and a Bitcoin rally above $72,000.

What Iran Wants and Where the Gaps Remain

Trump said the two sides were “in deep negotiations” heading into Islamabad and that the US had received a 10-point proposal from Iran that served as a workable starting framework. Iranian officials, however, have insisted any final deal must include guarantees against future US and Israeli attacks, sanctions relief, and compensation for wartime infrastructure damage.

Iran has also proposed a $1 per barrel toll on tankers crossing the Strait of Hormuz, paid in cryptocurrency, a demand Washington has not formally accepted. As crypto.news noted, even after the ceasefire, Iran’s continued restriction of Hormuz traffic drew criticism from the European Union and global partners who called for full and free passage of the waterway.

Market Implications

Oil prices fell below $100 per barrel after the ceasefire was announced last week, but they have remained volatile as traders wait to see whether a permanent agreement emerges from Islamabad. A full diplomatic resolution would remove the war premium from energy markets and ease the inflation pressure that has kept the Federal Reserve cautious on rate cuts.

For crypto markets, a successful outcome in Islamabad is the clearest near-term upside catalyst, with analysts projecting a Bitcoin move toward $75,000 if geopolitical risk is sustainably removed from the equation.

House Republicans shut down an Iran war powers resolution on April 10, with Speaker Pro Tempore Chris Smith gaveling the pro forma session to a close before Maryland Democrat Glenn Ivey could propose limiting President Trump’s authority to continue the war with Iran.

Summary

- Republican Speaker Pro Tempore Chris Smith gaveled the session closed before Rep. Glenn Ivey could introduce the Iran war powers resolution.

- Congress is now adjourned until 2:30 PM on Monday, April 13, 2026.

- The blocked resolution would have forced a vote to limit President Trump’s ability to continue the Iran conflict.

In a move that lasted seconds, House Republicans prevented Democrats from forcing a war powers vote on April 10. The brief pro forma session ended before Representative Glenn Ivey of Maryland could formally request unanimous consent to advance a resolution limiting Trump’s Iran war authority.

Rep. Glenn Ivey rose during the pro forma session and asked colleagues to “pass an Iran war powers resolution by unanimous consent.” Before he could finish, Republican Speaker Pro Tempore Chris Smith gaveled the session closed. According to Democracy Now!, Congress then adjourned until 2:30 PM on Monday, April 13, 2026.

The war powers resolution would have invoked the War Powers Resolution Act of 1973, which requires congressional authorization for sustained military engagements. The US-Iran conflict has exceeded the law’s 60-day threshold.

Why Democrats Are Pushing and Republicans Are Blocking

Democrats have argued the Iran conflict requires formal congressional authorization to continue, particularly as the six-week war has disrupted global energy markets and kept Bitcoin locked in a $65,000 to $73,000 range. As crypto.news reported, Bitcoin’s every move higher during the conflict has been directly tied to ceasefire chatter, and every breakdown has triggered rapid selloffs.

Republicans have declined to limit presidential war powers during active negotiations, arguing that constraining Trump’s authority while diplomats are at the table in Islamabad would weaken Washington’s negotiating position with Tehran.

What Happens Next

Congress returns on April 13, the same day the Senate resumes from Easter recess and the same week the CLARITY Act Banking Committee markup is targeted. Democrats are expected to renew their push on the war powers resolution, though their path remains blocked without a Republican willing to break ranks.

As crypto.news noted, markets are watching whether the Islamabad talks produce a durable agreement before Congress reconvenes. Any breakdown in the ceasefire negotiations could immediately reignite volatility across oil and crypto markets, making April 13 a convergence point for regulatory, geopolitical, and market risk simultaneously.

AI crime solving tools are being adopted at an accelerating pace by police agencies across the United States, with results that can be dramatic but that experts and civil liberties advocates say come with serious risks of false leads, wrongful investigations, and violations of due process.

Summary

- US police departments are increasingly using AI to accelerate criminal investigations and pattern recognition.

- Experts warn of risks including AI-generated false leads that could harm innocent people.

- The Washington Post reported April 10 on the growing adoption of AI crime tools across American law enforcement.

The use of artificial intelligence by American law enforcement is no longer experimental. According to The Washington Post, police agencies across the country are deploying AI tools to help investigators analyze evidence, flag patterns, and generate leads faster than traditional methods allow. The results have drawn attention. So have the concerns.

AI tools are being used across US law enforcement for functions including facial recognition, predictive policing, evidence analysis, and cross-database pattern matching. The technology allows investigators to process information at a scale and speed that would not be possible manually, and law enforcement officials say it has helped close cases that might otherwise have gone cold.

The CIA has signaled a parallel move in the intelligence community. As crypto.news reported today, CIA Deputy Director Michael Ellis confirmed the agency plans to integrate AI co-workers across all analytic platforms within two years to help officers identify foreign intelligence trends and draft reports, with Ellis stating the CIA “cannot allow the whims of a single company to constrain our capabilities.”

What Experts Are Warning About

The concerns raised by researchers and civil liberties advocates center on three main areas: the accuracy of AI-generated leads, the lack of transparency in how AI systems reach their conclusions, and the potential for errors to harm innocent people before they can be identified and corrected.

AI systems trained on biased data can generate biased outputs, and in a law enforcement context, a false lead from an AI tool can trigger surveillance, questioning, or arrest before the error is caught. As crypto.news noted, AI has already demonstrated its ability to scale deceptive operations in financial and digital contexts, with blockchain intelligence firm Elliptic warning that “the vast majority of AI-related threats in crypto are in their infancy” while urging vigilance.

The Accountability Question

The deepest concern is structural: when an AI tool generates a lead that leads to a wrongful investigation, who is accountable? Law enforcement agencies have not yet produced clear answers on oversight, audit mechanisms, or remediation. The Washington Post’s April 10 reporting suggests the adoption of these tools has accelerated faster than the accountability frameworks meant to govern them.

Prediction markets around NASA’s Artemis II mission have drawn traders to stake on outcomes and post-flight statements. The ten-day crewed lunar flyby, featuring four astronauts aboard the Orion spacecraft, has become a focal point for market-based event contracts hosted on platforms like Kalshi and Polymarket. The mission, launched from Florida on April 1, is expected to return to Earth with a splashdown around 12:07 am UTC on Saturday, capping a voyage that aims to be the first crewed lunar encounter since the Apollo era.

As of Friday, the volume on Artemis-related event contracts hovered at just over $4,000, illustrating a nascent but real appetite for space events among prediction-market participants. A number of contracts revolved around whether Artemis II would achieve a lunar milestone and what NASA officials would say during the post-splashdown news conference. Kalshi’s market book also included a Moon-landing contract with probabilities pegged at 63% for a manned lunar landing by 2030 and 41% for 2029, underscoring a mixed sentiment on timing.

Key takeaways

- Prediction markets show early-stage liquidity around Artemis II, with around $4k in volume recorded to date.

- Traders are wagering on post-landing remarks, with bets focusing on NASA’s press conference content and potential references to radiation, damage, or political terms.

- Artemis II marks NASA’s first crewed lunar flyby in more than five decades, setting the stage for future lunar milestones and a planned 2028 lunar landing target.

- Separately, Nvidia-backed Starcloud unveiled plans to mine Bitcoin from space, signaling broader ambitions for space-based infrastructure in crypto operations.

Artemis II and the evolving role of prediction markets

Kalshi and Polymarket have offered event contracts tied to Artemis II, including a direct Moon-landing bet and ancillary outcomes tied to mission communications. Market participants have shown particular interest in what NASA will say during the splashdown news conference, with several contracts centered on language and topics that could emerge in that briefing. The modest liquidity — just over $4,000 in trading volume as of Friday — suggests a cautious audience: investors are testing the waters on high-profile space events without yet embracing large-scale risk.

NASA’s Orion spacecraft completed the Moon flyby with a four-person crew after liftoff from Florida on April 1. Artemis I — NASA’s 2022 precursor mission that orbited the Moon without a crew — paved the way for Artemis II, which aims to validate life-support, navigation, and other deep-space systems ahead of planned crewed landings by 2028. If the timelines hold, Artemis II’s success would lend credibility to future spaceflight milestones and could influence how markets price similar event risk in the future.

Space mining and the broader narrative

Beyond the Moon mission, the crypto space is intersecting with space infrastructure in other ways. In March, Starcloud, an Nvidia-backed orbital data center company, announced plans to mine Bitcoin from space. The plan envisions deploying solar-powered orbital data centers with ASIC miners to operate in Earth orbit, a concept that would blend aerospace and crypto hardware in a way few projects have attempted. CEO Philip Johnston described the approach as a long-range endeavor that leverages the inexhaustible energy of space to power mining operations.

While space mining remains speculative, the news highlights a broader appetite among crypto and tech firms to explore cross-domain applications of blockchain technology and computational power. In the near term, Artemis II market activity demonstrates how prediction markets continue to adapt to high-profile events outside traditional finance, even as questions about liquidity, market integrity, and regulatory oversight linger — particularly for bets tied to geopolitical developments.

Looking ahead, Artemis II’s splashdown and NASA briefings will shape how these markets price space event risk, while regulators’ responses to geopolitics bets may influence the future of prediction-market platforms.

AI cybersecurity is now a formal competitive front between OpenAI and Anthropic, with OpenAI finalizing an advanced security product for a limited partner release and Anthropic running a tightly controlled effort called Project Glasswing aimed at finding critical software vulnerabilities before attackers do.

Summary

- OpenAI is finalizing an AI cybersecurity product for release first to a limited set of partners.

- Anthropic’s Project Glasswing is a controlled initiative focused on hunting critical software vulnerabilities proactively.

- Both efforts raise fundamental questions about who controls AI offense and defense tools and who is responsible when things go wrong.

Artificial intelligence has moved from a tool that helps defenders understand threats to one that can independently find and exploit vulnerabilities. OpenAI and Anthropic are now building directly into that space, with implications for governments, enterprises, and the millions of software systems that underpin global financial infrastructure.

OpenAI is finalizing an AI cybersecurity product with advanced capabilities and plans to release it initially to a limited partner group, according to Tech Startups. Anthropic is running a parallel effort internally called Project Glasswing, a tightly controlled initiative designed to hunt down critical software vulnerabilities before malicious actors find them first.

The dual announcements mark a shift in how the two leading AI labs are positioning themselves. Both are moving from general-purpose AI into security-specific products with direct offensive and defensive capability. The question is no longer what AI can do in cybersecurity. It is who controls it and who is accountable when it goes wrong.

What Anthropic’s Track Record Shows

Anthropic has already demonstrated the scale of what AI security tools can achieve. As crypto.news reported, the company limited access to its Claude Mythos Preview model after early testing found it could uncover thousands of critical vulnerabilities across widely used software environments, including a 27-year-old bug in OpenBSD and a 16-year-old remote execution flaw in FreeBSD. Anthropic said: “Given the rate of AI progress, it will not be long before such capabilities proliferate, potentially beyond actors who are committed to deploying them safely.”

Industry data cited by Anthropic shows a 72% year-on-year increase in AI-powered cyberattacks, with 87% of global organizations reporting exposure to AI-enabled incidents in 2025. Project Glasswing is being positioned as Anthropic’s controlled effort to stay ahead of that curve.

The Risk of Dual-Use AI Security Tools

The deeper issue for regulators and the industry is that the same AI tool that finds a vulnerability defensively can find it offensively. As crypto.news noted, a joint study by Anthropic and MATS Fellows found that Claude Sonnet and GPT-5 could produce simulated exploits against Ethereum smart contracts worth $4.6 million in testing, and uncovered two novel zero-day vulnerabilities in nearly 3,000 recently deployed contracts.

That dual-use reality makes the controlled rollout strategies both companies are pursuing essential. But the question of whether limited access is enough to prevent proliferation is one neither lab has fully answered.

Ryan Garcia sets sights on one man after u-turn on Teofimo Lopez fight

ChatGPT rolls out new $100 Pro subscription to challenge Claude

NHS explains what really works to lower high cholesterol as two in three affected

-

Business5 days ago

Business5 days agoThree Gulf funds agree to back Paramount’s $81 billion takeover of Warner, WSJ reports

-

Sports6 days ago

Sports6 days agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Politics8 hours ago

Politics8 hours agoUS brings back mandatory military draft registration

-

Fashion9 hours ago

Fashion9 hours agoWeekend Open Thread: Veronica Beard

-

Business7 days ago

Business7 days agoExpert Picks for Every Need

-

Tech3 days ago

Tech3 days agoHow Long Can You Drive With Expired Registration? What Florida Law Says

-

Business6 days ago

Business6 days agoNo Jackpot Winner, Prize to Climb to $231 Million

-

Fashion5 days ago

Fashion5 days agoMassimo Dutti Offers Inspiration for Your Summer Mood Board

-

Sports9 hours ago

Sports9 hours agoMan United discover Nico Schlotterbeck transfer fee as defender reaches Dortmund agreement

-

Fashion3 days ago

Fashion3 days agoLet’s Discuss: DEI in 2026

-

Crypto World3 days ago

Crypto World3 days agoBitcoin recovers as US and Iran Agree a Ceasefire Deal

-

Business6 hours ago

Business6 hours agoTesla Model Y Tops China Auto Sales in March 2026 With 39,827 Registrations, Beating Cheaper EVs and Gas Cars

-

Crypto World2 days ago

Crypto World2 days agoCanary Capital Files SEC Registration for PEPE ETF

-

Business6 days ago

Business6 days agoAkebia Therapeutics, Inc. (AKBA) Discusses Pipeline Progress and Strategic Focus on Kidney Disease Treatments at R&D Day – Slideshow

-

Business15 hours ago

Business15 hours agoOpenAI Halts Stargate UK Data Centre Project Over Energy Costs and Copyright Row

-

Tech5 days ago

Tech5 days agoHaier is betting big that your next TV purchase will be one of these

-

Politics7 days ago

Politics7 days agoThe UK should not pay a penny in slavery reparations

-

Tech5 days ago

Tech5 days agoThe Xiaomi 17 Ultra has some impressive add-ons that make snapping photos really fun

-

Tech5 days ago

Tech5 days agoSamsung just gave up on its own Messages app

-

Tech5 days ago

Tech5 days agoGamer Restores the Original PlayStation Portal From Two Decades Ago

You must be logged in to post a comment Login