Crypto World

PayPal launches PYUSD-backed stablecoin issuance platform

PayPal and MoonPay have introduced a new platform that allows developers to create custom stablecoins backed by PayPal’s PYUSD.

Summary

- PYUSDx lets developers issue app-specific stablecoins backed by PYUSD.

- The platform reduces launch time from months to days.

- USD.ai is the first project building on the framework.

In a joint Feb. 27 press release, the companies announced the launch of PYUSDx, a framework developed with M0 to support application-specific stablecoins using PayPal USD as the underlying reserve asset.

PYUSDx is designed to help developers launch branded stablecoins without building complex infrastructure from scratch. The platform allows apps to issue tokens backed by PYUSD, while relying on MoonPay’s distribution and onboarding systems and M0’s token platform.

Building application-level stablecoins

According to the announcement, the number of stablecoins with supplies above $10 million rose by 89% in 2025. The companies said this growth has increased demand for faster and cheaper ways to launch custom digital currencies.

Ivan Soto-Wright, chief executive of MoonPay, said developers need dependable tools to manage stablecoins at the application layer. He added that PYUSDx reduces technical and operational hurdles and shortens the time needed to bring products to market.

Under the structure, the base PYUSD token is issued by Paxos Trust Company, while PYUSDx tokens are issued through MoonPay Digital Assets Limited. The companies stressed that PYUSDx tokens are separate from PayPal’s native stablecoin and are not supported within PayPal or Venmo wallets.

The platform offers cross-chain compatibility, on-chain reserve reporting, and flexible economic models. Additionally, it facilitates quick deployment, allowing developers to go from testing to launch in a matter of days as opposed to months.

USD.ai has been named as the first developer to use PYUSDx, building an application-focused stablecoin for artificial intelligence infrastructure.

Expanding PayPal’s stablecoin ecosystem

Since its debut in 2023, PayPal has worked to increase the use of PYUSD, and this launch builds on those efforts. Users started earning 3.7% a year on PYUSD balances in April 2025. Stellar and Arbitrum were added to the stablecoin later that year, increasing speed and reducing transaction costs.

May Zabaneh, head of crypto at PayPal, said developers want to create unique financial products without rebuilding core monetary systems. She described PYUSDx as a way to anchor new projects in a regulated and trusted structure.

Luca Prosperi, chief executive of M0, said the platform allows developers to iterate faster while benefiting from built-in liquidity and interoperability.

The companies also noted that regulatory treatment of PYUSDx tokens will vary by region and remains the responsibility of individual issuers. PYUSDx tokens cannot be used for payments or transfers within PayPal or Venmo.

Crypto asset manager Bitwise has filed an amended registration statement with the U.S. Securities and Exchange Commission for a proposed exchange-traded fund (ETF) tied to Hyperliquid’s HYPE

The updated S-1 for the fund, which would hold HYPE directly and list on NYSE Arca, said it would trade under the ticker BHYP. The fund aims to track the token’s price, offering investors exposure to it without leveraging crypto exchanges or wallets.

The proposed product includes a staking component. Bitwise said the fund would stake a portion of its holdings to earn additional tokens, with about 85% of staking rewards retained after fees.

The filing also details a 0.67% annual management fee and custody arrangements with Anchorage Digital, a federally chartered crypto bank.

The price of Hyperliquid’s HYPE token has surged over the past year. The token is up around 200% over the last 12 months, as it became the go-to decentralized trading platform for perpetual contracts, including those tied to traditional financial products.

Other asset managers have also moved to list HYPE-linked exchange-traded funds. These include Grayscale, which filed last month to list under the ticker GHYP on Nasdaq, as well as 21Shares and VanEck.

Ron Hammond, head of policy at crypto market maker Wintermute, has a cautious outlook on the Clarity Act, putting its chances of passage this year at around 30% even as momentum builds in Washington.

“There are a lot of moving parts,” Hammond said, pointing to a legislative process that is advancing, but unevenly. The Clarity Act aims to create rules around crypto market structure regulation in the U.S., including codifying how the Securities and Exchange Commission and Commodity Futures Trading Commission can oversee digital assets in the U.S.

Hammond’s estimate broadly aligns with other signals in the market. A recent Punchbowl survey of lobbyists and staffers put the odds at 26%, while prediction market Kalshi has hovered just above even odds. The spread underscores how uncertain the bill’s trajectory remains.

Still, Hammond, who will be speaking at CoinDesk’s Consensus Miami conference next month, sees incremental progress. Lawmakers are pushing to move the bill through committee, with some aiming for a vote as early as April 20, though he cautioned that such timelines have been fluid for months.

“These dates are moving,” he said. “There’s light at the end of the tunnel, but there are hurdles along the way.”

Passage of the Clarity Act is widely seen as a key unlock for institutional adoption of crypto because it would establish clear rules around which digital assets are securities versus commodities, and define how they can be traded, custodied and otherwise regulated in the U.S.

Today’s fragmented and uncertain framework has kept many large asset managers, banks and pension funds on the sidelines due to legal and compliance risks. A comprehensive market structure law would reduce that ambiguity, giving institutions the confidence to scale exposure, launch new products, and integrate crypto more fully into traditional financial systems.

Hurdles

At the center of those hurdles: banks.

According to Hammond, traditional financial institutions remain the biggest obstacle, particularly around the issue of whether stablecoins should offer yield. A recent report from the Council of Economic Advisers has pushed back on bank opposition, but negotiations remain stuck.

“There have been attempts from a number of sides: Coinbase (COIN), the White House, the bill’s drafters, to find a solution,” Hammond said. “But at every turn, the banks refuse to give way.”

The dispute has already derailed at least one compromise. Hammond said a proposed “yield deal” floated roughly two weeks ago failed to satisfy either side, sending negotiators back to the drawing board. A new version is now circulating, but expectations are tempered.

“Even with broader macro pressures, it’s hard to see how the banks get happy here,” he said.

Democrats

That resistance is shaping the politics around the bill, particularly for Democrats. Hammond noted that some lawmakers who have accepted crypto industry funding are now navigating a difficult balancing act.

“If you’re a Democrat who took crypto money, where do you stand on this issue?” he said, pointing also to unresolved concerns around decentralized finance (DeFi) and anti-money laundering compliance.

Additional political headwinds could emerge in the coming months. Hammond flagged ongoing scrutiny around former President Donald Trump’s crypto-related dealings as a potential flashpoint that could complicate Democratic support if it intensifies around June.

“All of that becomes another headache,” he said.

Despite the friction, Hammond believes the bill still has a viable, if narrow, path forward. Progress in committee and continued negotiations could keep it alive into midyear, when political incentives may shift.

“There will be some progress soon,” he said.

U.S. expansion

For Wintermute, the stakes are high. The firm, one of the largest crypto market makers globally with roughly $10 million in daily trading volume, is expanding its U.S. footprint, and growing its New York team.

Hammond said that reflects a broader industry commitment to the U.S. market, particularly under what firms see as a more favorable regulatory environment. “Wintermute has expanded operations since the election by establishing a U.S. office in NYC and we have been actively hiring,” he added.

That makes the outcome of the Clarity Act all the more consequential. While Hammond sees “light at the end of the tunnel,” he emphasized that passage in 2026 will require breakthroughs that have so far proved elusive.

For now, 30% remains his number, and a reminder that progress in Washington does not always translate into results.

Read more: Bitcoin is stuck in a rut but JPMorgan says new legislation could be the ultimate spark

The US labor market added 178,000 jobs in March, according to the Bureau of Labor Statistics.

Summary

- March job growth stayed modest while tech hiring remained weak and entry-level roles kept shrinking.

- AI use rose in offices, but many workers reported rework, frustration, and lower trust.

- Executives saw gains from AI tools, while staff faced errors and extra checks daily.

The data showed limited change from the prior month, even as companies kept talking about AI-led growth and better workplace efficiency.

That gap has kept attention on whether AI is lifting hiring and output as promised. Recent labor, workplace, and industry reports show a more mixed picture, especially in tech and entry-level roles.

Most job growth in March came from healthcare, construction, transportation and warehousing, and social assistance. Healthcare added 76,000 jobs, while construction gained 26,000 and transportation and warehousing added 21,000.

The BLS data did not show the same strength in tech-linked areas. Computing infrastructure providers and web search portals showed little movement, while computer systems design and related services lost 13,000 jobs during the month.

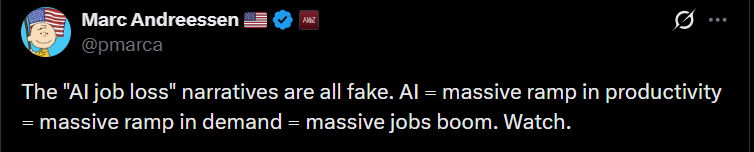

That pattern stands in contrast to public claims that tech hiring is recovering. Marc Andreessen said fears about AI-led job losses were overblown and shared data showing more job openings at tech firms.

But openings do not always lead to hiring. The March labor figures showed that the strongest hiring came from sectors outside core tech, while related digital services stayed flat or moved lower.

A recent Goldman Sachs report, cited by Fortune, said AI cut about 16,000 jobs per month over the past year. At the same time, a 2025 SignalFire study said new graduate hiring had dropped 50% from levels seen before the COVID-19 pandemic.

SignalFire said, “The door to tech once swung wide open for new grads. Today, it’s barely cracked.” The report linked that shift to smaller funding rounds, leaner teams, fewer graduate programs, and rising AI use.

Goldman Sachs also warned that workers pushed out by technology often move into more routine jobs. The report said this shift can reduce the value of their existing skills and weaken labor outcomes for years.

That concern has widened the debate around AI and employment. While some leaders still expect long-term gains, recent data has kept attention on current hiring patterns and who bears the cost of the change.

Worker experience does not match executive optimism

Executives continue to report strong support for AI tools. Harvard Business Review said 80% of leaders use AI weekly, while 74% reported positive returns from early deployments.

Workers reported a different experience. Mercer said 43% of workers found their jobs more frustrating, while Workday said nearly four hours are lost fixing AI output for every 10 hours of claimed efficiency gains.

Harvard Business Review also pointed to “workslop,” described as content that looks polished but lacks substance. Researchers said 41% of workers had seen this kind of output, with each case adding almost two hours of rework.

Workday said only 14% of respondents “consistently achieve net-positive outcomes from AI use.” That result suggests many workplaces are still dealing with errors, extra review, and weak trust in outputs.

OpenAI warns policy may lag behind change

The divide between executive use and daily staff experience may come from how teams use the tools. Harvard Business Review said senior leaders often apply AI to strategy, drafting, and synthesis, where the systems tend to perform better.

For routine operations that need steady accuracy, results appear less reliable. Brian Solis of ServiceNow called this burden an “AI tax,” which he described as “More checking. More rework. More anxiety.”

OpenAI has also acknowledged that AI is changing employment. Its policy ideas included broader healthcare coverage, retirement savings support, and a new industrial agenda.

The company said its proposals are early and meant to begin discussion. It also warned, “Unless policy keeps pace with technological change, the institutions and safety nets needed to navigate this transition could fall behind.”

Key Highlights

- IonQ achieved a groundbreaking 99.99% fidelity world record and targets millions of qubits by 2030.

- IBM earned a “Perfect 10” Smart Score rating on TipRanks with Moderate Buy consensus and analysts projecting 40.49% upside.

- Microsoft’s Majorana 1 chip powers chemistry research applications and carries a Strong Buy rating with 56.62% potential upside.

- Alphabet’s Google released research suggesting blockchain encryption could be compromised by quantum algorithms as early as 2029.

- Industry analysts forecast the quantum computing sector will surge from $1.42 billion in 2024 to $4.24 billion by 2030.

Quantum computing has transitioned from theoretical research into tangible commercial applications at an accelerating pace. For investors monitoring this emerging sector, three companies emerge as particularly compelling: IonQ, IBM, and Microsoft.

The quantum computing industry reached a valuation of $1.42 billion in 2024. Market researchers anticipate this figure will climb to $4.24 billion by the decade’s end. Such explosive expansion is attracting enterprise clients, lucrative government partnerships, and substantial capital investments.

IonQ: Prioritizing Precision Over Speed

IonQ has established itself as the premier pure-play quantum computing enterprise. The company’s technology recently achieved an unprecedented 99.99% fidelity rating in industry-standard benchmarking tests—a global achievement.

Precision represents the fundamental obstacle preventing quantum computing’s mainstream adoption. Systems plagued by frequent computational errors cannot deliver reliable results for practical applications.

IonQ’s approach centers on trapped ion technology. This methodology prioritizes exceptional accuracy over raw processing velocity, contrasting sharply with the superconducting architectures favored by competitors.

The organization’s 2026 roadmap includes deploying a 256-qubit architecture. Looking further ahead, IonQ aims to construct million-qubit systems by 2030. Successfully achieving these milestones while maintaining current accuracy standards could position the company as dominant in precision-dependent sectors.

IonQ’s quantum systems are accessible through partnerships with Amazon Web Services, Microsoft Azure, and Google Cloud. The company currently commands approximately $11 billion in market capitalization.

IBM: Bridging Quantum and Traditional Computing

IBM has charted a distinctive strategic course. Instead of solely pursuing qubit quantity, the tech giant emphasizes integrating quantum capabilities into established enterprise infrastructure.

International Business Machines Corporation, IBM

IBM’s development strategy centers on hybrid architectures where conventional CPUs, GPUs, and quantum processors operate cohesively. Industry experts consider this integration model the most viable pathway toward immediate commercial viability.

TipRanks analysts awarded IBM the platform’s maximum Smart Score of 10 out of 10. The stock maintains a Moderate Buy consensus rating, with Wall Street projecting 40.49% appreciation potential.

IBM leverages its extensive enterprise computing heritage and established client relationships, providing immediate market access for quantum services. The company’s development pipeline emphasizes enhanced qubit coherence and sophisticated error correction protocols.

Microsoft: Strategic Innovation with Transformative Potential

Microsoft has maintained a relatively understated public profile regarding quantum achievements compared to rivals like Google or IonQ. Nevertheless, its Majorana 1 quantum processor is delivering measurable outcomes.

The processor currently facilitates advanced chemistry research, enabling quantum simulations of intricate molecular behaviors that exceed classical computing capabilities. CEO Satya Nadella has characterized quantum technology as the forthcoming catalyst for cloud computing evolution.

Microsoft’s research concentrates on topological qubit architectures—a forward-looking methodology promising superior stability compared to existing quantum systems. The company’s Azure Quantum platform seamlessly embeds quantum capabilities into corporate computing environments.

Wall Street analysts assign Microsoft a Strong Buy recommendation with 56.62% upside potential. The stock holds a Smart Score of eight out of ten on TipRanks.

Alphabet’s Google division released 2025 research demonstrating an algorithm potentially capable of compromising contemporary blockchain encryption protocols in minutes—possibly operational by 2029. This revelation emphasizes the remarkable velocity of quantum computing advancement.

In March, the US jobs market recorded 178,000 new jobs, marking little change from the month before, according to the Bureau of Labor Statistics.

The anemic growth in job listings comes amid volatile policy swings from the White House, increased energy prices due to the US and Israel’s war with Iran and, according to recent research, AI disruptions to the labor market.

Proponents of AI and large language models have claimed that the tech will bring about an economic boom, thanks to the promise of efficiency breakthroughs.

But as AI becomes more integrated into daily business operations, there is a widening gulf between that promise of growth and efficiency, and what is actually happening.

AI dampens employment growth

On March 6, venture capitalist and Netscape co-founder Marc Andreessen said on X that fears about AI job displacement were overblown.

He also posted an article from Business Insider stating that, at least in tech, job openings are on the rise. Citing data from TrueUp, a tech jobs tracker, Business Insider said that job openings at tech companies have doubled to 67,000 since 2023.

But openings don’t necessarily translate to hiring. According to the Bureau of Labor Statistics, most employment growth in March did not happen in the tech industry. Of the 178,000 new jobs added in March, healthcare employed 76,000, construction grew by 26,000, transportation and warehousing added 21,000 and employment in social assistance increased by 14,000.

While the report doesn’t have a single section tracking the tech industry, related services like computing infrastructure providers and web search portals saw a 1,500 job decrease, or almost no change, respectively. Computer systems design and related services lost 13,000 jobs.

Related: Jack Dorsey’s Block to cut 4,000 jobs in AI-driven restructuring

AI has actually axed 16,000 jobs per month over the past year, according to a recent report from Goldman Sachs, as cited by Fortune. In particular, AI has led to a collapse in hiring for entry-level roles. A 2025 study from SignalFire found that new grad hiring had dropped 50% compared to pre-COVID-19 pandemic levels.

“The door to tech once swung wide open for new grads. Today, it’s barely cracked. The industry’s obsession with hiring bright-eyed grads right out of college is colliding with new realities: smaller funding rounds, shrinking teams, fewer new grad programs, and the rise of AI,” the SignalFire study stated.

This disruption could create ripples far into the future. According to Goldman Sachs, “AI-driven displacement could impose lasting costs on affected workers, worsening labor market outcomes for several years.”

“A key mechanism behind these worse outcomes is occupational downgrading. Workers displaced by technology are more likely to move into more routine occupations requiring fewer analytical and interpersonal skills, likely because the same technological shifts that eliminated their positions also eroded the value of their existing skills,” they continued.

These job losses are justified by the theory that AI will, at the very least, make workplaces more productive. But even that isn’t a given.

Reality of AI use clashes with C-suite expectations

Executives are still overwhelmingly supportive of AI. According to Harvard Business Review, 80% of leaders report weekly use of AI, with 74% reporting positive returns on early deployments.

But workers don’t feel the same. A study from HR consulting firm Mercer found that, for 43% of workers, their job is more frustrating.

One major issue is the number of mistakes churned out by generative AI. “For every 10 hours of efficiency gained through AI, nearly four hours are lost to fixing its output,” a Workday report stated.

AI can also be used to offload labor onto coworkers in what researchers at the Harvard Business Review have called “workslop” i.e., “content that appears polished but lacks real substance, offloading cognitive labor onto coworkers.”

They said that “41% of workers have encountered such AI-generated output, costing nearly two hours of rework per instance and creating downstream productivity, trust, and collaboration issues.”

According to Workday, only 14% of respondents to their survey said they “consistently achieve net-positive outcomes from AI use.”

Part of the gulf between executives’ understanding of AI and the reality at the productive level may be explained by the technology itself.

Per the Harvard Business Review, “Senior leaders tend to use AI for high-level synthesis, strategic drafting, and decision support, tasks where the technology performs well, so the current capabilities tend to benefit their work.”

For messier day-to-day operations like “workflows built over years, teams with uneven technical comfort, output that has to be consistently right, not just fast,” it doesn’t work so well.

“When the tool works, both groups understand and reap the benefits. When it fails, typically only one of them has to cope with the aftermath.”

Brian Solis, the head of global innovation at enterprise AI firm ServiceNow, said that this divide has created an “AI tax,” i.e., “More checking. More rework. More anxiety. Faster pace. AI slop. Less trust.”

Andreessen may not believe that the AI job-cut narratives are real, but OpenAI does. The AI company has acknowledged the impact the technology has on employment, and has even released a series of policy proposals to address it.

The list contains ideas that are “intentionally early and exploratory” that serve as a “a starting point for discussion that we invite others to build on.” It includes proposals to expand healthcare coverage, retirement savings and setting a new industrial policy agenda.

Far from Andreessen’s optimism, OpenAI’s proposal included a warning: “Unless policy keeps pace with technological change, the institutions and safety nets needed to navigate this transition could fall behind.”

Magazine: Asia Express: Phantom Bitcoin checks, China tracks tax on blockchain

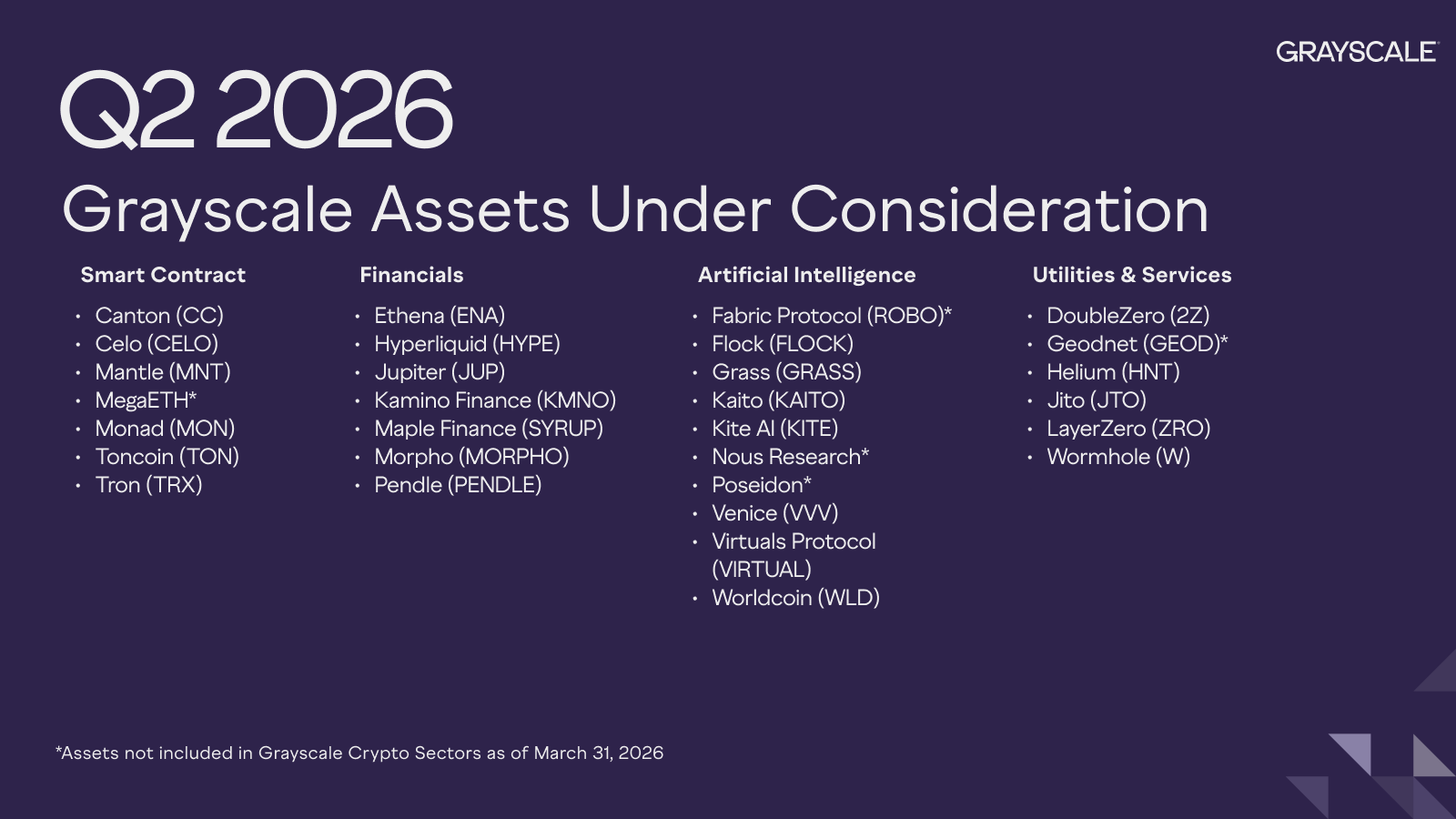

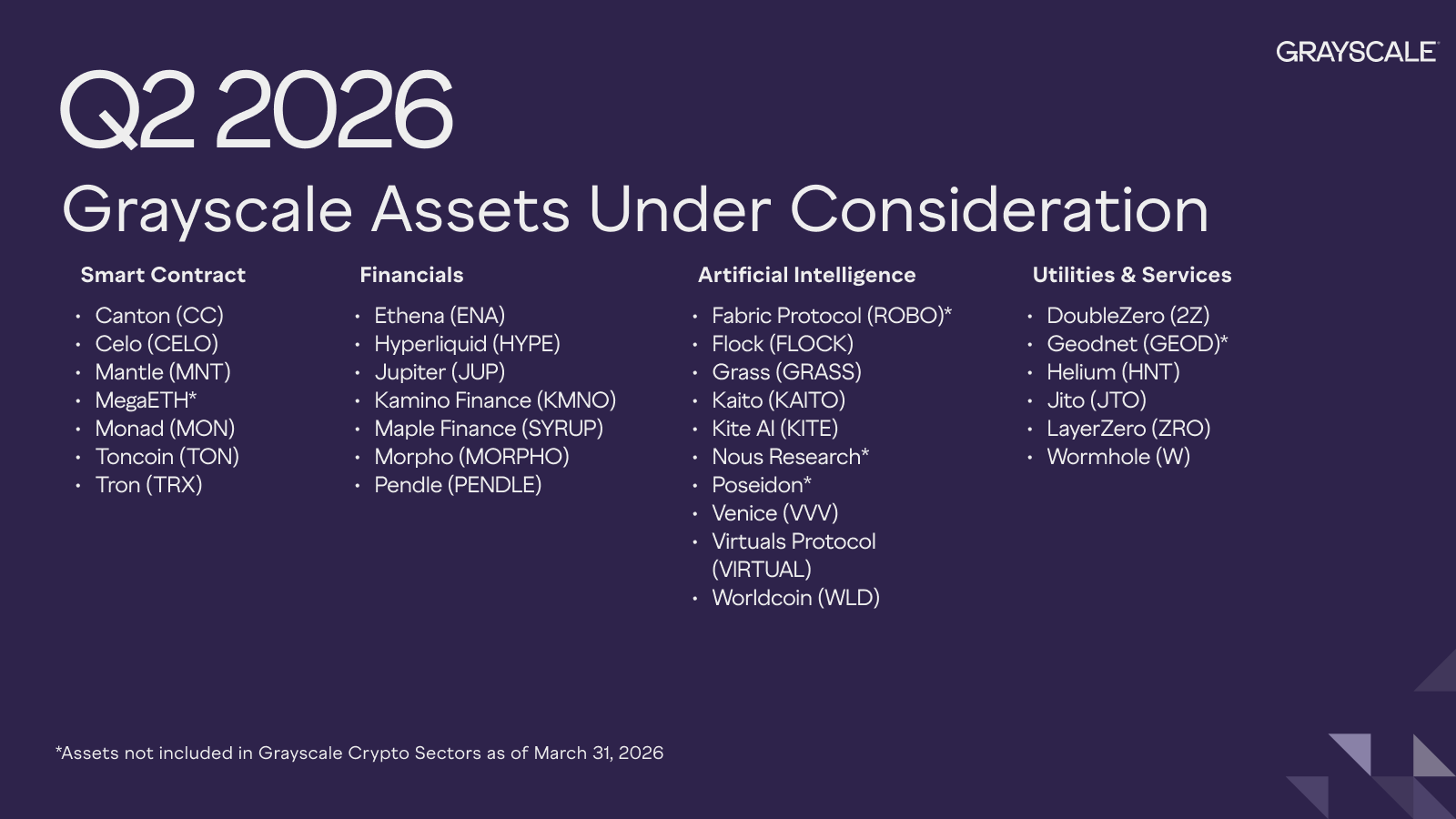

Grayscale has narrowed its list of crypto assets under review for potential inclusion in future investment products in the second quarter of 2026. The firm trimmed the roster to 30 tokens from 36 in the prior quarter and dropped an entire category tied to consumer-facing crypto projects.

The asset manager’s updated “Assets Under Consideration” list spans four segments: smart contract platforms, financial assets, artificial intelligence, and utilities and services.

Grayscale Q2 Update Focuses on Crypto AI Projects

In the first-quarter version, the firm had grouped 36 names across five segments, including a separate Consumer & Culture category that no longer appears in the latest update.

The change leaves artificial intelligence as the largest bucket on the list. Grayscale included 10 AI-linked assets in the second-quarter roster, up from seven in the previous quarter.

The additions include Fabric Protocol, Kite AI, and Venice, alongside names that remained on the list such as Flock, Grass, Kaito, Virtuels Protocol, and Worldcoin.

The revised list also added Canton in the smart contract segment and Helium in utilities and services.

At the same time, Grayscale removed a broad mix of tokens from earlier sector lists.

The names no longer included in the second-quarter version are Aptos, Arbitrum, Binance Coin, and Polkadot from smart contracts. Euler, Lombard, Plume Network, and Sky from financials; and ARIA Protocol, Bonk, and Playtron from the Consumer & Culture group.

The result is a smaller and more concentrated list. Smart contract assets fell to seven names from 10 in the prior quarter, while financial tokens dropped to seven from 11. Utilities and services increased from five to six.

Meanwhile, the latest reshuffle points to a sharper emphasis on infrastructure and AI-related crypto themes.

While Grayscale kept established names such as Celo, Mantle, Monad, Toncoin, Tron, Ethena, Hyperliquid, Jupiter, Kamino, Maple Finance, Morpho, Pendle, DoubleZero, Geodnet, Jito, LayerZero, and Wormhole, the biggest directional shift came from the expansion of AI entries.

Notably, AI-linked crypto projects had gained increased prominence during the first quarter of this year, thanks to the rapidly expanding generative AI space.

Over the past year, the sector has continued to attract significant institutional and commercial interest from the general public.

The post Grayscale Cuts Q2 Altcoin Watchlist, Drops Consumer Tokens and Adds AI Names appeared first on BeInCrypto.

Shipping firms weighing cryptocurrency payments to cover potential transit fees through Iran face substantial sanctions risk, according to Kaitlin Martin, a senior intelligence analyst at Chainalysis. Under current sanctions frameworks, payments linked to the Iranian regime or other sanctioned actors can be interpreted as material support, exposing companies to both U.S. and international restrictions.

The alert comes as reports circulate that Tehran could seek to collect transit fees via crypto for passage through strategic waterways. While U.S. President Donald Trump has signaled he would not tolerate tolls on the Strait of Hormuz, the broader question remains whether crypto could serve as a workaround for sanctions—an idea that experts say is unlikely to escape scrutiny and enforcement actions.

Key takeaways

- Payments to the Iranian regime or sanctioned entities tied to transit routes can be treated as material support, creating meaningful sanctions exposure for shippers and financiers.

- Iran has expanded its use of digital assets, especially stablecoins, to facilitate trade in oil, weapons, and other commodities, but blockchain transparency does not guarantee a bypass of sanctions.

- Cryptocurrency transactions leave a traceable record, which investigators can leverage to freeze or seize assets at cash-out points, complicating evasion efforts.

- Besides Iran, other sanctioned states have explored crypto-enabled trade. Russia, for example, has used digital tokens to support cross-border commerce in the face of sanctions.

- Iran’s Bitcoin mining activity has declined markedly, while the global Bitcoin network remains robust; the disruption appears concentrated within Iran and does not appear to destabilize neighboring markets.

Crypto use and sanctions: what changes, and what remains uncertain

In a field where financial channels are traditionally governed by a dense matrix of controls, the idea that cryptocurrency can neatly sidestep sanctions is met with caution by investigators. Martin notes that while digital assets enable cross-border transfers outside conventional rails, they come with inherent visibility. “In many ways, cryptocurrency is actually easier to trace than traditional methods of sanctions evasion,” she said, highlighting the ability to track funds to eventual cash-out points where authorities can intervene or seize assets.

Public data suggests Tehran is pushing forward with crypto-enabled trade, leveraging digital assets to move value for oil, commodities, and related goods. The trend underscores a broader strategic pivot: sanctioned economies are exploring crypto as a tool to preserve some level of cross-border activity amid pressure from Western jurisdictions. Yet the traceability of blockchain transactions means that these efforts remain exposed to enforcement actions and risk mitigation strategies by banks, exchanges, and other counterparties.

There is a precedent for state actors adopting crypto as a supplementary mechanism for trade under sanctions. For instance, Russia has experimented with digital tokens to facilitate cross-border transactions after international restrictions intensified in 2022. Such moves illustrate the dual nature of crypto in geopolitics: it can expand access to value transfer, but it also amplifies the footprint of regulatory scrutiny and potential sanctions enforcement.

Iranian mining and the global network outlook

The same period that highlights Tehran’s interest in crypto-enabled trade also intersects with a broader crypto mining landscape. Iran’s Bitcoin hashrate has fallen sharply, dropping by about 7 exahashes per second and sliding to roughly 2 exahashes per second, amid ongoing geopolitical tensions and domestic pressures. While this represents a substantial local shift, the global Bitcoin network remains broadly stable, with total hashrate hovering near 1,000 exahashes per second. The decline appears concentrated within Iran, with neighboring Gulf states such as the United Arab Emirates and Oman showing little impact so far.

These dynamics matter for investors and builders in several ways. First, the concentration of mining power in a single region can affect energy markets and grid stress in that area, potentially influencing local policy and energy incentives. Second, the resilience of the global network despite regional disruptions reinforces Bitcoin’s core property as a globally distributed system. And third, the shift in Iran’s mining activity could influence the country’s capacity to monetize energy assets through crypto, a factor worth watching as sanctions and regional risk evolve.

What to watch next

Several developments bear watching in the near term. First, how strictly authorities pursue alleged crypto-enabled sanctions evasion in shipping lanes and whether there are new enforcement actions against companies facilitating such flows. Second, any shifts in Tehran’s crypto and stablecoin usage for trade, including potential policy signals from Iranian authorities. Third, the interplay between regional mining activity and energy policy, particularly in Iran and neighboring states, as sanctions and geopolitical tensions continue to reshape incentives for miners and exporters alike.

The Japanese Cabinet approved a bill on April 10 reclassifying crypto as a financial instrument under the amended Financial Instruments and Exchange Act, pulling digital assets out of the Payment Services Act framework and placing Japanese crypto on the same legal footing as stocks and bonds.

Maximum prison sentences for unregistered sellers jump from 3 years to 10 years. Fines climb from 3 million yen to 10 million yen. Insider trading on undisclosed information is now explicitly banned.

That’s not incremental regulatory cleanup. That’s a structural reclassification with enforcement teeth attached from day one.

The question is exactly what this changes for exchanges, institutional allocators, and the 13 million Japanese residents who already hold crypto accounts – and whether the compliance clock is as short as the headline implies.

- Reclassification under FIEA: Crypto moves from Payment Services Act treatment to full Financial Instruments and Exchange Act coverage, matching stocks and bonds.

- Insider trading ban: Crypto assets are now explicitly subject to insider trading prohibitions based on material non-public information.

- Penalty escalation: Unregistered seller sentences rise to 10 years; fines increase to 10 million yen.

- LPS Act amendment: Japanese venture capital firms can now directly hold crypto assets, removing a structural barrier that had pushed startup funding offshore.

- Tax alignment incoming: Maximum crypto tax rate set to drop from 55% to a flat 20% capital gains rate, matching equities.

- Bitcoin ETF legalization: FSA is targeting 2028 for crypto ETF approvals alongside these rule changes.

Discover: How Wall Street’s Institutional Bitcoin Moves Are Reshaping Crypto Markets

What Does Crypto Reclassification Under Japan FIEA Actually Change for Operators and Investors?

Under the old framework, crypto fell under the Payment Services Act, regulated primarily as a payment mechanism rather than an investment vehicle.

That legal container determined everything: custody standards, disclosure obligations, investor protections, and the severity of enforcement. The FSA’s February 2026 Financial System Council report was direct about the core problem: “information asymmetry” between issuers and retail investors had become structurally dangerous as crypto evolved into an investment asset class.

The new bill fixes that at the legal-definition level. By bringing crypto under the Financial Instruments and Exchange Act, issuers now face mandatory annual disclosure requirements covering technology, token supply, risk factors, and use cases – even for post-listing assets not actively fundraising.

That’s the same disclosure regime Japanese equity issuers operate under. For the 105 cryptocurrencies the FSA flagged for reclassification – including Bitcoin and Ethereum – the compliance surface area just expanded significantly.

The LPS Act amendment is the piece that most institutional observers are watching closely. Previously, Japanese venture capital funds structured as investment limited partnerships were legally prohibited from holding crypto assets directly.

That single restriction had been quietly pushing Web3 startup capital offshore for years. The amendment removes that barrier – meaning domestic VC can now deploy into crypto without restructuring through foreign entities. That’s not a marginal fix. That’s the structural precondition for a functioning domestic crypto venture ecosystem.

Finance Minister Satsuki Katayama framed the cabinet approval as a dual mandate: “expand the supply of growth capital” while ensuring “market fairness, transparency, and investor protection.” The two goals aren’t in tension here – securities-grade oversight is exactly what institutional adoption requires.

A Sandmark Crypto Intelligence Report from April 2026 found that 42% of global finance professionals cited regulatory uncertainty as their primary barrier to allocating to crypto.

Japan just removed that barrier domestically. XRP’s $120 million in weekly ETP inflows recorded in early April show how quickly institutional capital moves once the legal infrastructure aligns – Japan is now building that same infrastructure at the sovereign level.

The site’s position: this is the most consequential single piece of Japan crypto regulation since the PSA amendments that followed Mt. Gox. It doesn’t just add rules – it changes the legal category, which changes everything downstream.

The post Japan Crypto Revolution Inbound? Tokyo Pass New Law Equalising Crypto and Stocks appeared first on Cryptonews.

Crypto World

The Pepeto Price Prediction That Has Analysts Drawing Lines From Presale Entry to the Original Pepe Valuation

The Pepeto price prediction gets its strongest signal yet after Canary Capital filed for the first US spot PEPE ETF, proving meme coins are now serious enough for Wall Street fund wrappers, according to Yahoo Finance.

The meme sector added $2 billion in seven days to $31 billion. That shift changes the Pepeto price prediction for anyone tracking presale entries before listing. The project raised $8.86 million during extreme fear with a Binance listing approaching, and the math between the current entry and Pepe’s original valuation gives the forecast its clearest case yet.

Canary Capital filed to launch a US spot ETF tied to PEPE, making it the first meme coin fund application to go beyond Bitcoin and Ethereum into the meme category, according to Yahoo Finance. The proposed fund would hold spot PEPE through a custodian and could keep up to 5% of assets in ETH for gas fees.

Meanwhile the meme coin sector climbed 7% on the week to a $31 billion market cap, according to CoinMarketCap, with capital rotating from large caps into meme entries where the return math is far bigger.

Presale Entries and Listing Targets Shaping the Token Forecast

Pepeto: Zero Cost Swaps and Pepe Legacy Positioning the Strongest Presale of the Cycle

A spot PEPE ETF filing proves that meme coins have crossed from internet jokes into regulated investment products. One presale drawing even heavier capital through this cycle’s fear is Pepeto, structured not for short term noise but for the kind of returns that rewrite a portfolio after one listing event, making it the Pepeto price prediction that analysts keep returning to.

The project delivers lasting value on clear paths. Staking at 186% APY grows early positions ahead of listing. The 420 trillion token supply matches Pepe’s original structure, giving the Pepeto price prediction a direct reference point that traders can verify.

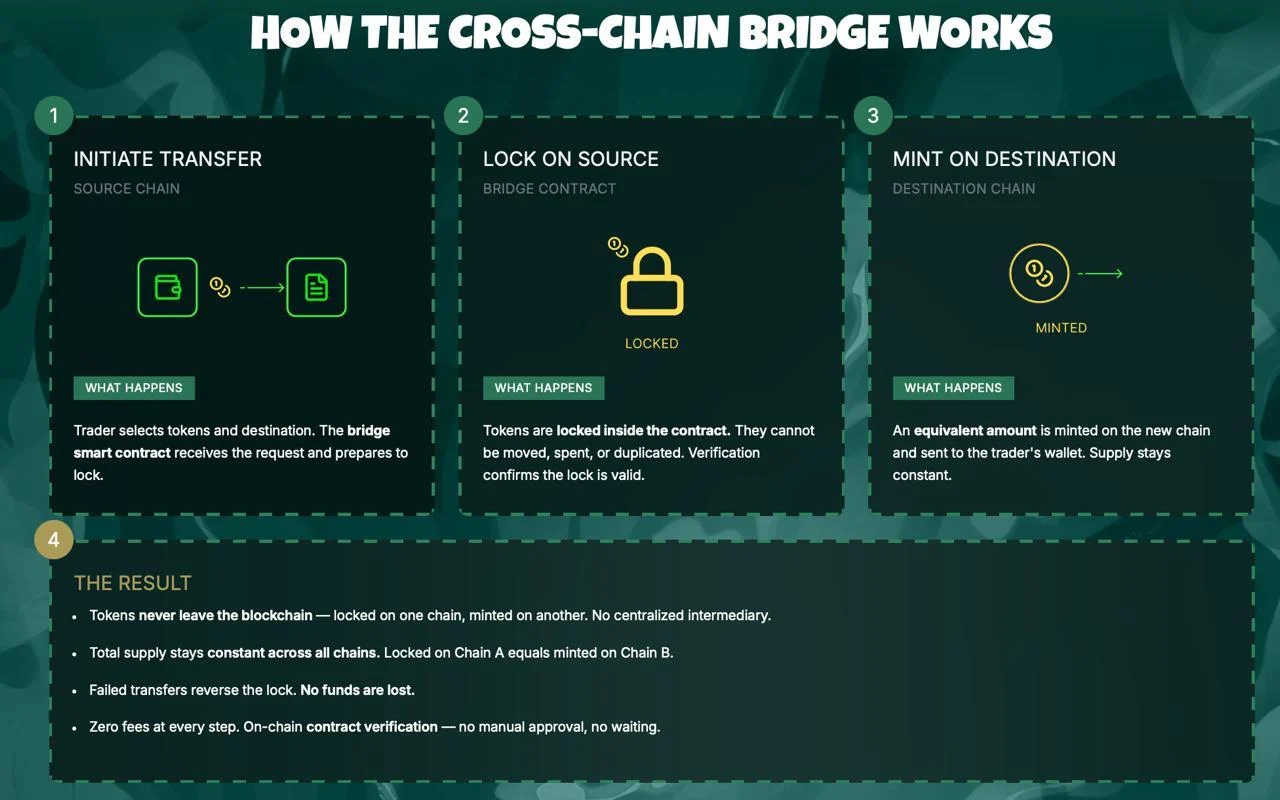

Exchange tools already handle live activity. PepetoSwap processes token swaps across chains at zero cost, keeping full position value intact. The cross chain bridge routes assets between networks without fees, giving holders access to every chain while protecting what they carry.

Over $8.86 million in capital arrived while the Fear and Greed Index showed extreme fear. Pepeto at $0.0000001863 sits at a fraction of what listing models project, and the space between that price and where trading opens is where the real returns take shape for wallets that act while the number holds.

The presale closes for good once the Binance listing goes live. A developer who built trading systems at Binance shaped every stage of the platform, and the identical supply to Pepe’s original token that reached a multi billion dollar cap with zero tools running gives forecasters the data they need. The wallets that built wealth from Pepe all made one decision: they moved while entry was still open. That same window is open right now, and the listing can drop at any moment.

Pepeto Price Prediction: Listing Targets and Return Scenarios

The Pepeto price prediction begins with the math. At the current presale entry with 420 trillion supply, the fully diluted value sits near $78 million. PancakeSwap launched at $200 million FDV and hit $7 billion. BNB started near $15 million and climbed past $100 billion.

Pepeto sits below both with a working exchange already live. Matching Pepe’s $7 billion cap delivers roughly 89x, and analysts who factor in exchange tools Pepe never had see that as a floor. The forecast ranges from 50x to 300x depending on listing volume.

Conclusion

The Pepeto price prediction points to returns no large cap can approach from current prices. A spot PEPE ETF filing proves that meme coins now attract Wall Street capital, and the project built by the same founder with a working exchange and a Binance listing sits at a fraction of where that capital will price it.

At $0.0000001863, every $1,000 grabs 5.37 billion tokens. If Pepeto matches even a fraction of Pepe’s run on the same 420 trillion supply, that $1,000 turns into six figures. Over $8.86 million already flowed in during extreme fear because thousands of wallets ran that math and committed. The listing can land at any moment, and early holders will be sitting on positions the rest of the market pays multiples more to chase. The Pepeto official website is where that entry is still open.

Click To Visit Pepeto Website To Enter The Presale

FAQs

What is the Pepeto price prediction based on listing models and Pepe’s market cap?

Analysts project 50x to 300x from presale based on Pepe’s $7 billion cap and working exchange tools Pepe never had. The Binance listing is approaching.

How does the 420 trillion supply affect the Pepeto price prediction?

The supply matches Pepe’s original token, giving analysts a verified reference point. Pepeto’s $78 million FDV sits below where exchange tokens historically launch.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

The US government moved a small amount of bitcoin on April 10 from wallets that Arkham Intelligence linked to a criminal case. The transfer involved 2.438 BTC, worth about $177,000, sent to a Coinbase Prime address.

Summary

- US government moved 2.438 BTC from seized wallets tied to an alleged steroid conspiracy case.

- Arkham linked the funds to Glenn Olivio, who faced charges filed in 2025.

- The transfer renewed focus on how seized bitcoin moves under the federal reserve policy.

Arkham data showed two separate transactions from wallets labeled “U.S. Government: Glenn Olivio Seized Funds.” Both transfers went to the same Coinbase address, beginning with 3EMqu.

Government-linked bitcoin transfers are not unusual. Federal agencies often move seized assets for custody, consolidation, or other handling during legal and administrative processes.

The latest move still drew attention because the funds may be tied to a 2025 federal case. The transfer also comes after the Trump administration said it had stopped selling seized bitcoin.

That policy became clearer after President Donald Trump signed an executive order creating a strategic bitcoin reserve. Treasury Secretary Scott Bessent later said the government would keep bitcoin obtained through criminal forfeitures.

The Block reported that the seized bitcoin appears linked to Glenn Bradford Olivio. Court records show Olivio was arrested in May 2025 with Dana Rene Light.

Prosecutors charged the pair with five counts, including conspiracy to possess with intent to distribute controlled substances, money laundering conspiracy, aggravated identity theft, and drug possession counts.

The indictment said the case involved “a mixture or substance containing a detectable amount of anabolic steroids.” The listed substances included synthetic testosterone, Trenbolone, Nandrolone, Mestanolone, Oxandrolone, Stanozolol, and Methandienone.

Court filings also included a notice of forfeiture. That step is common when the government seeks to seize property, including cryptocurrency, that it says came from alleged criminal activity.

Reserve policy remains in focus

The transfer comes as federal bitcoin holdings remain under close watch. The US government currently holds about 328,000 BTC, valued at more than $22 billion at current market prices.

In recent weeks, government-linked wallets also moved funds tied to other cases, including assets associated with Ross Ulbricht, Chen Zhi, and Miguel Villanueva.

Those earlier transfers raised questions about whether the government was still sending bitcoin to custodial platforms despite the reserve policy. The latest Olivio-linked transfer is likely to draw similar attention.

PACER shows the steroid case last updated in June 2025. Public records reviewed by The Block did not confirm whether this case is related to an older 2015 marijuana arrest involving a man with the same name.

TYBCOM Sem 6 | Financial Accounting | Full Syllabus Revision | 80+ Marks Guaranteed | By Shubham sir

Over 50 events announced for Bangor’s Open House Festival 2026

Aurobindo Pharma share buyback, Muthoot Fin dividend, 2 other corporate actions next week

Why Israel is blocking foreign journalists from entering

Bitcoin: We’re Entering The Most Dangerous Phase

Alan Cumming Brands Baftas Ceremony A ‘Triggering S**tshow’

TYBCOM Sem 6 | Financial Accounting | Full Syllabus Revision | 80+ Marks Guaranteed | By Shubham sir

Paisa kamane wala app 2026 || NEW UPI MONEY EARNING APP || New Earning App Today || Jio Finance App

How J.P. Morgan Saved the U.S. Government during the financial crisis of 1895 #money

-

Business6 days ago

Business6 days agoThree Gulf funds agree to back Paramount’s $81 billion takeover of Warner, WSJ reports

-

Sports7 days ago

Sports7 days agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Politics20 hours ago

Politics20 hours agoUS brings back mandatory military draft registration

-

Fashion20 hours ago

Fashion20 hours agoWeekend Open Thread: Veronica Beard

-

Tech4 days ago

Tech4 days agoHow Long Can You Drive With Expired Registration? What Florida Law Says

-

Business6 days ago

Business6 days agoNo Jackpot Winner, Prize to Climb to $231 Million

-

Fashion5 days ago

Fashion5 days agoMassimo Dutti Offers Inspiration for Your Summer Mood Board

-

Sports21 hours ago

Sports21 hours agoMan United discover Nico Schlotterbeck transfer fee as defender reaches Dortmund agreement

-

Fashion4 days ago

Fashion4 days agoLet’s Discuss: DEI in 2026

-

Crypto World3 days ago

Crypto World3 days agoBitcoin recovers as US and Iran Agree a Ceasefire Deal

-

Crypto World2 days ago

Crypto World2 days agoCanary Capital Files SEC Registration for PEPE ETF

-

Business17 hours ago

Business17 hours agoTesla Model Y Tops China Auto Sales in March 2026 With 39,827 Registrations, Beating Cheaper EVs and Gas Cars

-

Business7 days ago

Business7 days agoAkebia Therapeutics, Inc. (AKBA) Discusses Pipeline Progress and Strategic Focus on Kidney Disease Treatments at R&D Day – Slideshow

-

Business1 day ago

Business1 day agoOpenAI Halts Stargate UK Data Centre Project Over Energy Costs and Copyright Row

-

Tech5 days ago

Tech5 days agoGamer Restores the Original PlayStation Portal From Two Decades Ago

-

Tech5 days ago

Tech5 days agoHaier is betting big that your next TV purchase will be one of these

-

Politics1 day ago

Politics1 day agoMalcolm In The Middle OG Turned Down ‘Buckets Of Money’ To Appear In Reboot

-

Tech5 days ago

Tech5 days agoThe Xiaomi 17 Ultra has some impressive add-ons that make snapping photos really fun

-

Tech5 days ago

Tech5 days agoSamsung just gave up on its own Messages app

-

Tech5 days ago

Tech5 days agoSave $130 on the Samsung Galaxy Watch 8 Classic: rotating bezel, sleep coaching, and running coach for $369

You must be logged in to post a comment Login