Crypto World

Playnance unveils Web2-to-Web3 gaming ecosystem after years in stealth mode

- Playnance unveils Web2-to-Web3 gaming infrastructure after years operating privately at scale.

- The platform processes 1.5 million daily on-chain transactions with over 10,000 active users.

- Playnance focuses on simplifying blockchain access through Web2-style onboarding systems.

Playnance has made its first public announcement, revealing itself as a Web3 infrastructure and consumer platform company that has been operating a live ecosystem aimed at onboarding mainstream Web2 users into blockchain-based environments.

The announcement was made on February 5, 2026, from Tel Aviv, marking the company’s first formal introduction after several years of developing and running its technology and platforms privately.

Founded in 2020, Playnance has positioned itself as a Web2-to-Web3 gaming infrastructure layer.

The company integrates with more than 30 game studios and enables the conversion of thousands of games into fully on-chain experiences, where all gameplay actions are executed and recorded directly on blockchain networks.

Infrastructure built to simplify blockchain adoption

Playnance’s core offering focuses on removing technical barriers commonly associated with blockchain usage.

The company’s products are designed to allow users to interact with on-chain systems without needing direct knowledge of blockchain mechanics.

Instead, users access platforms through familiar Web2-style interfaces, including standard account creation and login processes, while blockchain functionality operates in the background.

The company stated that its live platforms currently process approximately 1.5 million on-chain transactions daily and support more than 10,000 daily active users.

According to Playnance, a significant portion of its user base originates from traditional Web2 environments.

These users are reportedly able to onboard and interact with blockchain-based systems without using external wallets or managing private keys, suggesting continued on-chain engagement from audiences outside the traditional crypto sector.

The company’s ecosystem also includes the G Coin initiative, which is currently operating in pre-sale mode and is accessible through the Playnance official website.

Consumer platforms showcase operational ecosystem

Playnance operates several consumer-facing platforms designed to demonstrate its infrastructure capabilities.

Among these are PlayW3, Up vs Down, and other products that run on shared on-chain infrastructure and wallet systems.

The integrated structure allows users to move between platforms without repeating onboarding procedures.

All user interactions across these platforms are executed and recorded on-chain while remaining non-custodial, aligning with the company’s focus on user control and blockchain transparency.

The shared wallet and infrastructure framework also supports cross-platform engagement within the broader Playnance ecosystem.

“Our focus was on building systems that people could use without needing to understand blockchain mechanics,” said Pini Peter, CEO of Playnance. “We prioritized live operation and user behavior over public announcements, and this is the first time we are formally introducing the company after reaching scale.”

Expansion strategy centred on user behaviour

Playnance stated that its infrastructure is designed to support high-volume consumer activity and continuous on-chain execution.

The company’s approach reflects a broader industry shift toward practical blockchain applications targeting mainstream audiences.

Looking ahead, Playnance indicated that its ecosystem expansion will be guided by observed user behaviour and platform performance.

The company emphasised that its development roadmap will focus on real usage data rather than speculative adoption models.

Playnance describes itself as a company focused on reducing friction between user behaviour and blockchain execution by operating consumer platforms at scale.

A Coinbase user’s attempt to block an IRS summons for his financial records was blocked by a California court.

Summary

- A California court dismissed a Coinbase user’s attempt to block an IRS summons, citing failure to meet required notification rules within the 90 day deadline.

- The petition challenged the summons on privacy and scope grounds, even though the user had already amended his tax return and paid additional dues.

According to information from PACER, Roger Metz filed a petition in the Northern District of California in May last year to quash an IRS summons that sought his financial records in connection with an audit of his 2022 tax return.

Metz’s case was based on the argument that the summons violated his privacy rights and was overbroad. Metz’s lawyers had also argued that he had identified the error himself and had filed an amended return and paid the additional tax, but that did not prevent the IRS action.

However, US District Judge Araceli Martínez-Olguín ruled against the petitioner on Wednesday after finding that he failed to notify all required government parties within the 90-day window. The judge has dismissed the case on procedural grounds.

The ruling is based on federal civil procedure rules, where defendants must be formally notified of lawsuits to ensure they receive notice and the opportunity to respond. Court documents suggest Metz had served the US Attorney’s Office for the Northern District of California and the IRS, but had failed to notify the US Attorney General in Washington. Government lawyers argued this was sufficient grounds for dismissal.

“In his opposition brief, Metz does not offer any explanation for his failure to serve the United States within 90 days after filing his petition, much less that he had good cause,” Judge Martínez-Olguín said in the ruling.

The case has been dismissed without prejudice, as such Metz has the option to file the petition again at a later date.

As previously reported by crypto.news, last year, another Coinbase user, James Harper, accused the IRS of violating his Fourth Amendment rights following a John Doe Summons used to obtain his data from a crypto exchange. The court, however, sided with the IRS and declined to hear his case.

The outcome reinforces the IRS’s authority to obtain user financial records from centralized crypto exchanges.

It’s not all bad news, though, as there was at least one whale that made a big purchase in the past 24 hours.

Bitcoin’s price has nosedived once again in the past 24 hours, dropping below $71,000 for the first time since the weekend.

While the blame has been placed on the US Federal Reserve, certain OG whales have been disposing of large BTC portions, which can also be attributed to the correction.

OGs Selling

Lookonchain reported that an ancient BTC wallet sold another 1,000 units in the past day, worth around $71 million. The entity received 5,000 BTC (worth around $1.66 million at the time) over 12 years ago, but began selling off its assets in November 2024.

The unknown market participant has disposed of 3,500 BTC at an average price of over $96,000. According to the analytics company’s estimations, the whale profited around $442 million, or a 266x return.

A #BitcoinOG with 5K $BTC($356M) sold another 1,000 $BTC($71.57M) 8 hours ago.

This OG received 5K $BTC(cost $1.66M) at $332 12 years ago, and started selling $BTC on Nov 26, 2024, selling a total of 3,500 $BTC($337M) at ~$96,262.

Total profit: $442M — a 266x return.… pic.twitter.com/oErv0KccjN

— Lookonchain (@lookonchain) March 19, 2026

In another post on X, Lookonchain indicated that one more BTC OG wallet, flagged as belonging to Owen Gunden, has sold 650 BTC in the past day as well. This one followed a previous big dump of 11,000 BTC, worth over $1.1 billion at the time.

These substantial market sell-offs coincided with or even preceded bitcoin’s notable price drop in the past 24 hours. The asset traded above $74,000 by yesterday afternoon, when it nosedived to $71,000. Although it bounced at first after the Fed’s decision to maintain the interest rates, it dropped further in the following hours toward $70,000.

You may also like:

One Is Buying

It’s not all doom and gloom on the bitcoin whale scene, though. The analytics resource explained that another such market participant has been buying BTC “every day since Mar 10,” and splashed another $37 million yesterday to acquire over 500 units.

The post noted that the entity has accumulated a total of 2,656 BTC at an average price of just over $72,000 since March 10, worth around $190 million as of press time.

Whale bc1qfs has been buying $BTC every day since Mar 10, and bought another 500.78 $BTC($37.16M) ~30 minutes ago.

Since Mar 10, he has bought a total of 2,656 $BTC($191.43M) at an average price of $72,063.https://t.co/eaqtA9hwE4https://t.co/ZwV8QZ7eh9 pic.twitter.com/gOTfLItqLU

— Lookonchain (@lookonchain) March 18, 2026

Binance Free $600 (CryptoPotato Exclusive): Use this link to register a new account and receive $600 exclusive welcome offer on Binance (full details).

LIMITED OFFER for CryptoPotato readers at Bybit: Use this link to register and open a $500 FREE position on any coin!

- Bitcoin traded to intraday lows of $70,500 amid key macro and geopolitical-related events.

- Veteran trader Peter Brandt has highlighted a potential bearish retest of support.

- The Iran war and inflation concerns tick potential negative catalysts boxes.

Bitcoin price flipped lower to trade below $70,500 as sellers showed fresh strength, with BTC down as cryptocurrencies reacted to US inflation data, the Federal Reserve’s rate decision, and the escalation in the Iran war.

Veteran trader Peter Brandt has shared his outlook for BTC in terms of technical setup, noting that a constructive “horn” remains in play. However, it could also be an “ugly” flag pattern.

BTC price 24-hour performance

Bitcoin is currently trading at approximately $70,850 as of March 19, 2026.

The benchmark digital asset has declined by nearly 4% over the past 24 hours, sliding from highs near $74,800 amid a confluence of negative catalysts.

Notably, the price movement ties directly to global events.

The ongoing Iran-Israel conflict, now in its third week, has escalated with Iran’s missile strikes in the Gulf after Israel eliminated key Iranian figure Ali Larijani.

This has spiked oil prices, fueling inflation fears and contributing to Bitcoin’s risk-off sentiment, as seen in prior dips below $64,000 after initial attacks.

Meanwhile, the US Federal Reserve’s March meeting held interest rates steady, citing inflation and uncertainty over the direction of the war in Iran and its impact on global energy markets.

Fed Chair Jerome Powell emphasized a cautious stance, delaying cuts amid rising inflation risks, which prompted a retreat across risk assets.

Earlier in the day, US inflation data showed the producer price index (PPI) coming in hotter than expected. BTC fell from above $74,000 as traders turned their attention to the further impact of the war.

BTC price forecast: Brandt’s shares potential “ugly” outlook

Peter Brandt, known for his classical charting expertise, highlighted Bitcoin’s potential price setup via a post on the social media platform X.

“The horn is constructive. The flag is ugly. Take your pick,” he cautioned as downside pressure resurfaced.

Comment on Bitcoin

I am well aware that you cryptocultists cannot stand the idea of traders being flexible and not totally dogmatic like you, but Bitcoin is set up for me in two ways.

The horn is constructive

The flag is ugly

Take your pick

Opinions are a dime a dozen $BTC pic.twitter.com/ORFbiI5yo3— Peter Brandt (@PeterLBrandt) March 18, 2026

A look at the chart suggests a “horn” pattern that represents a volatile, widening formation.

In terms of technical setup, this signals a potential breakout momentum if Bitcoin pushes through upper resistance.

Brandt’s chart shows consolidation above macro support, with price poised near the range top. If bulls manage to reclaim $74,000, a move to the $80,000 could materialize.

However, the flag pattern suggests action could turn bearish amid the macro and geopolitical factors.

Bitcoin price on the daily chart indicates rejection at the recent top could be another bearish wedge pattern, ex-fund manager Aksel Kibar notes.

Potentially, bears could target a retest of $68,000. Any further decline may see BTC revisit the $65,000-$60,000 range.

Block Inc., the firm behind payment platforms Square, Cash App and Afterpay, has quietly brought back a small portion of workers it laid off in late February with its transition to rely more on artificial intelligence.

Multiple Block employees posted on LinkedIn this month that they were offered a place to return to the company after initially being part of the 4,000 employees who were fired.

Design engineer Andrew Harvard said on March 3 that he rejoined after being told that his layoff was due to a clerical error. “They offered me the opportunity to return, and I’ve accepted,” he added.

On March 8, technical lead Richard Hesse said he was the only member of his team who wasn’t impacted by the staff cut and that he spent two days convincing management that he needed more staff to continue working on “infrastructure highly critical to our customers.”

“I’m happy to share that they listened to my requests and have decided to re-hire some of those laid off,” he said. “While my teams were not returned to full levels, I’ll have enough to continue on.”

Chane Rennie, creative strategy lead, said on March 12 that he was asked to rejoin the company about a week after being laid off, but did not explain why.

Cointelegraph contacted Block on what staff were rehired, but did not receive an immediate response.

Block CEO Jack Dorsey acknowledged at the time of the layoffs that Block may have made some missteps in its staff cut decisions and had built in flexibility to correct course.

Dorsey said recent advances in AI tools forced Block to restructure its 6,000-strong workforce, adding that AI now “fundamentally changes what it means to build and run a company.”

The Guardian reported that several fired Block employees pushed back against Dorsey’s assertions that AI tools can effectively replace workers at scale.

Related: Nvidia’s Huang: AI will boost jobs as it needs trillions in infrastructure

Some of those laid off said they believed the staff cuts were Dorsey’s way of regaining investor confidence, with Block shares down double digits so far this year.

Block, which offers a range of Bitcoin (BTC) and crypto products with Square and Cash App, currently has 27 job listings on its website.

The only two position types currently listed are manager or account executive, and none of the roles specifically mention the use of AI in the job descriptions.

Meanwhile, the Algorand Foundation, the team behind the Algorand layer-1 blockchain, said it had made the “difficult decision” to reduce its headcount by 25% on Wednesday, blaming the crypto slump and macroeconomic uncertainty.

On Monday, blockchain analytics platform Messari also announced staff cuts as part of its transition to become an AI-first company.

Magazine: Big Questions: Can Bitcoin save you from the dreaded Cantillon Effect?

Crypto traders are parsing the Federal Reserve’s decision to hold rates and its implications for a possible market rally. With policy left unchanged, attention shifted to whether the pause can catalyze a relief bounce for Bitcoin and the broader crypto market, or whether the move simply defers the next leg in a cautious macro backdrop.

Santiment, a sentiment-tracking platform, reported a rapid shift in social mood in the wake of the central bank’s decision. Its metrics show the crypto social discussion score jumping from about 9 to 71 in the hours after the Fed’s expected outcome, as traders linked the hold to a potential upside for crypto assets. The firm noted that market participants appeared to focus less on immediate cuts and more on the prospect of later policy pivots that could support risk assets. Santiment said on X.

Bitcoin’s price action reflected a moment of cross-currents. At the time of writing, BTC traded around $70,790, having slipped about 4.35% over the past 24 hours, according to CoinMarketCap. Over the prior 30 days, the benchmark crypto had been modestly higher, up roughly 3.56%. The Fed pause has reinforced a narrative among traders that a relief rally could unfold even without an immediate move on rates, though many remain cautious about how durable any bounce will be in the face of broader macro headwinds.

Key takeaways

- Santiment’s social-sentiment metrics surged after the Fed pause, signaling heightened bullish chatter and a belief in a potential crypto rally ahead of any rate cuts.

- Bitcoin stood near $70,800, with a 24-hour drop of about 4.4% but a 30-day gain around 3.6%, illustrating a choppy near-term path despite the rate hold.

- Historically, Fed policy has been a strong catalyst for crypto optimism, with some observers looking to possible rate cuts in 2025 as a signal for a new Bitcoin bull year.

- Nevertheless, analysts warned that the relief could prove fleeting if macro catalysts do not materialize, and several voices raised concerns about a potential bull trap in the near term.

Fed pause reshapes trader expectations

By keeping the federal funds target rate steady in the 3.5%–3.75% range, the Fed reinforced a wait-and-see posture as markets weigh the path ahead. In crypto circles, the decision has often been treated as a macro backdrop that can lift risk assets if investors anticipate eventual rate relief. Several analysts noted that the absence of a rate cut yet did not erase the possibility of a future pivot; instead, the hold tended to shift the conversation toward timing rather than direction.

Industry observers have long linked monetary policy signals to crypto momentum. The prospect of rate reductions in 2025 remains a potential bullish catalyst for Bitcoin, even as near-term dynamics stay uncertain. The tension between expecting a policy pivot and defending a risk-off stance has created a bifurcated narrative: some participants anticipate a durable rally if the Fed begins cutting ahead of other central banks, while others caution that any move higher could stall without more concrete macro or liquidity support.

Signals vs. price action: market mood in flux

The latest price action sits at a crossroads. Bitcoin’s 24-hour decline underscores the fragility of short-term momentum, even as longer-term momentum metrics show intermittent strength. The Crypto Fear & Greed Index moved back into Extreme Fear territory on Wednesday after a brief return to Fear the day before, highlighting that overall sentiment remains jittery even as social chatter turns more optimistic. This dichotomy—elevated social bullishness alongside continued price weakness—illustrates the complexity of interpreting a Fed-driven impulse in a market that is simultaneously assessing liquidity, macro data, and broader risk appetite.

Analysts remain divided on the durability of any rally. On one hand, on-chain and technical commentary has pointed to a potential multi-month uplift should equities stabilize and macro conditions improve. On the other hand, a number of voices warn that the current up-move could be a “bull trap”—a short-lived ascent that reverses as soon as momentum fades or as real money exits risk assets. Bitcoin brokered a dramatic move in recent sessions, and traders will be watching both macro data releases and central-bank commentary for confirmation of a lasting shift.

Within the broader market context, there are competing signals. The S&P 500 has trended lower, with roughly a 3.7% decline over the past 30 days, according to Google Finance data cited in market briefs. This backdrop suggests investors remain cautious about chasing a near-term crypto rally without supporting upside from risk assets or a clear path to lower policy rates. Still, some voices remain constructive about a more pronounced rally in the medium term, arguing that a capitulation-like washout could open the door to renewed appetite for risk assets as liquidity conditions improve.

Commentary from notable voices in the space reflects this split. On-chain analyst Willy Woo warned that the market could be forming a bull trap, where early bullishness misreads the strength of the uptrend. Meanwhile, traders like Matthew Hyland suggested that a meaningful rally could emerge once broader markets find a bottom and begin to rebound. Hyland pointed to the current macro setup as a prerequisite for a broad crypto upside, aligning with the view that BTC tends to perform when equities recover from downturns.

Within social channels, sentiment remains a volatile gauge. A crypto trader known as Moustache echoed the hopeful sentiment, stating on X that a “massive rally” could unfold in the coming months. Whether that call translates into tangible price action will depend on the confluence of rate expectations, inflation data, and the speed at which liquidity returns to risk markets.

Broader context and what comes next

The Fed’s decision to pause reinforces a broader narrative about policy paths and crypto’s sensitivity to macro signals. If investors interpret the hold as a precursor to rate cuts, Bitcoin and other tokens could benefit from a renewed bid as risk appetite improves and liquidity conditions ease. Conversely, if the hold is read as evidence that the macro environment remains constrained, any rally could be shallow or short-lived, fading as momentum cools and traders reprice risk.

Going forward, market watchers will closely track several signals: upcoming inflation data, the Fed’s own communication on the trajectory of rates, and the pace at which other central banks respond to evolving macro conditions. The next few weeks could reveal whether the relief rally discussed by traders gains traction, or if the narrative shifts back toward caution and consolidation as macro cues darken risk sentiment.

In the meantime, sentiment indicators remain the most volatile barometer. The surge in social sentiment following the Fed decision suggests players are ready to test a higher-risk stance, but price action and macro momentum will ultimately determine whether the rally endures or merely proves transient.

Readers should keep a close watch on the development of rate expectations and the evolution of risk appetite in equities, as these will likely set the pace for crypto’s trajectory in the near term. The next major inflection point will be how quickly market participants price in possible rate cuts and how convincingly the macro data supports a shift from caution to confidence.

What to watch next: a clearer read on whether the Fed’s hold becomes a stepping stone to cuts, and whether Bitcoin can convert social buzz into sustained buying interest rather than a fleeting bounce. The landscape remains uncertain, but the emphasis on policy signals and macro resilience will shape the path forward for crypto markets in the days ahead.

Crypto World

Flow Traders debuts 24/7 OTC liquidity service for tokenized stocks, gold and money market funds

Flow Traders, one of the world’s top market makers in exchange-traded products, said Tuesday it is bringing its decades of TradFi expertise to tokenized assets with the launch of 24/7 over-the-counter (OTC) liquidity.

The move arms institutional clients with a new tool, allowing them to manage risk and keep capital flowing via blockchain versions of popular traditional assets when traditional exchanges are dark on weekends and after hours.

The new offering, delivered through Flow Traders’ Digital Asset OTC platform, provides proprietary, two-way pricing for tokenized money-market funds, equities and commodities, including Franklin Templeton’s BENJI and tether gold (XAUT), according to the press release shared with CoinDesk.

It means that the OTC platform will now constantly quote prices, ready to buy or sell the tokenized assets outside regular traditional market hours. The service is available immediately to permissioned counterparties, with institutions able to access liquidity via direct FIX connectivity and other standard trading interfaces.

“At Flow Traders, we have operated at the intersection of traditional and digital markets for many years, and we are pleased to launch 24/7 OTC liquidity for regulated tokenized equities and commodities for permissioned counterparties through our digital asset OTC platform,” Thomas Spitz, CEO of Flow Traders, said.

The OTC liquidity aims to address a nagging problem for institutions: The inability to adjust positions during weekends or overnight sessions. This has become brutally clear in recent weeks, as Iran-Israel tensions flared over the weekends, leaving traditional trading desks empty while crypto markets churned.

The demand mainly comes from institutions that want the ability to manage exposure outside traditional market hours,” Marc Jansen, co-chief trading officer at Flow Traders, told CoinDesk.

He explained that the OTC liquidity service will help large traders manage their risk better beyond market hours through tokenized equities and commodities, which are already gaining popularity on venues such as Binance, OKX, and Hyperliquid.

“All weekend long, with these markets getting pretty close to the traditional market open price as a result of that weekend price discovery. OTC liquidity helps support that activity, particularly for larger trades where public venue liquidity is still developing,” he said.

According to the firm, tokenization is growing fast and the tokenized gold and silver market alone is nearing $6 billion in value, up roughly fourfold since the end of 2024.

“Liquidity providers such as Flow Traders play a critical role in ensuring that tokenized assets like XAUT can trade efficiently across venues and reach a broader set of market participants,“ said Paolo Ardoino, CEO of Tether.

The asset tokenization market is reportedly worth $3 trillion as of this year and is growing at a CAGR of 44.25% and could reach over $18 trillion by 2031, according to some estimates.

This booming market, however, demands more than just enthusiasm; it requires battle-tested expertise, and this is where Flow Traders appears to have an edge, thanks to their 20 years of experience in market-making and liquidity provisioning for global exchange-traded products.

They operate across asset classes, including ETPs, digital assets, fixed income, FX, and commodities, and ranked among the top three global market makers by ETP trading volume in 2025.

“For us, with extensive experience in the ETF markets, it’s a more familiar problem. We’ve always priced and managed risk in products when parts of the primary market are closed. That already requires using models rather than relying purely on underlying market prices and we’ve built those pricing models over time in our ETF business, and they can be extended to tokenized markets,” Jansen said.

“Our role is to provide liquidity wherever the market develops,” he added.

The new OTC service will expand coverage and evolve, with asset availability guided by institutional counterparty demand, ongoing regulatory developments, and the integration of supported trading venues.

Product offerings will therefore vary by jurisdiction and depend on client eligibility, with different members of the Flow Traders group providing access based on their respective regulatory statuses.

Bhutan has transferred roughly $72.3 million in Bitcoin over the past 24 hours, continuing a steady pattern of trimming its sovereign holdings.

Summary

- Bhutan transferred roughly $72.3 million in Bitcoin over 24 hours, with Druk Holding and Investments moving more than 973 BTC across multiple transactions.

- Holdings have declined to over 4,400 BTC from a peak of 13,295 BTC in October 2024, as the country continues periodic sales from its sovereign reserve.

According to Arkham Intelligence data, Druk Holding and Investments, which manages the country’s crypto mining and treasury operations, has moved more than 973 BTC. The latest transfers come as Bhutan has continued to offload portions of its Bitcoin reserves in measured intervals.

DHI’s last major transfer was flagged on March 10, when it moved more than 175 BTC worth around $11.8 million.

Arkham noted that the country periodically sells Bitcoin in clips of $5 million to $10 million, but current transfers appear larger in scale compared to the activity seen around September 2025.

After the current transfers, Bhutan now holds more than 4,400 BTC, valued at over $322 million based on current market prices.

At its peak, Bhutan held 13,295 BTC in October 2024 and has since gradually reduced its holdings through a series of on-chain transfers.

Bhutan’s Bitcoin play

Bhutan has outlined a Bitcoin Development Pledge aimed at supporting the Kingdom of Bhutan’s long-term economic development through its mining operations and strategic reserves. Meanwhile, it has also committed to deploying part of its Bitcoin holdings toward the development of the Gelephu Mindfulness City.

Further, Arkham added that Bhutan-linked wallets have not recorded inflows greater than $100 million over the past year. Many in the crypto community are now speculating that the country may have scaled back or ceased its mining operations.

However, there’s been no confirmation of any halt in mining activity.

Early reports suggest the country has been using renewable energy sources, particularly hydroelectric power, to sustain its Bitcoin mining operations.

The latest transfers come as the Bitcoin price has dropped over 4.5% in the last 24 hours, falling below the $71,000 mark as investors reacted to hotter-than-expected inflation concerns in the US.

Large-scale selling from sovereign entities like Bhutan could further exacerbate downward pressure on the asset, especially as the market remains sensitive to signs of reduced institutional conviction and potential sell-side liquidity from major holders.

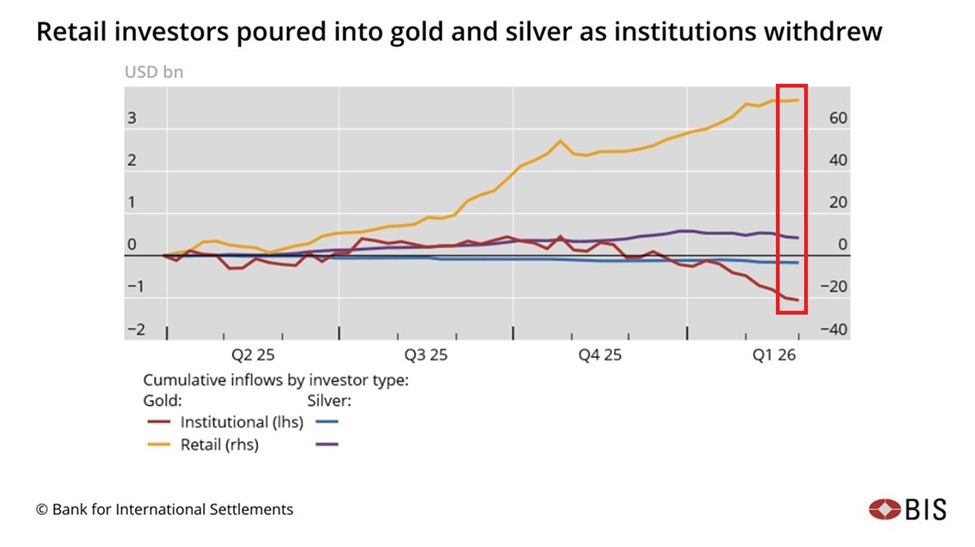

Retail gold purchases have tripled over the last six months, while Wall Street selling has accelerated over the past four months, according to data from the Bank for International Settlements (BIS).

“Retail-driven exuberance,” increasingly channeled through exchange-traded funds (ETFs), “set the stage for outsize moves,” continuing the precious metal rally from 2025, reported the BIS in a quarterly review released on Monday.

Since Q2 2025, retail investors have bought around $70 billion in gold ETFs, and these purchases have more than tripled over the last six months, observed the Kobeissi Letter, citing BIS data on Thursday.

“Retail investors are all-in on precious metals,” it noted.

Gold has surged 60% over the past year, and some crypto proponents have speculated it has come at the expense of Bitcoin, which some argue competes with gold as a store-of-value asset.

BIS data shows cumulative retail inflows effectively tripled from around $20 billion to roughly $60 billion over the six months from late Q3 2025 to the end of Q1 2026.

However, institutional selling started around mid-November and accelerated after the precious metals market began to correct in January, according to the data.

Leveraged liquidations amplified commodity drops

Bitcoin (BTC) is not the only asset susceptible to high volatility from overleveraged positions.

Prices of precious metals such as gold and silver reversed abruptly in late January and February 2026, while the “daily rebalancing of leveraged ETFs and margin‑triggered liquidations amplified the swings,” particularly in silver, BIS reported.

Smaller speculative derivatives traders, or “non-reportables,” had built up heavily leveraged long positions in silver heading into the crash, it added.

Gold prices are currently down 9% from their late January all-time high, while silver has slumped much harder, dropping 34% over the same period, according to GoldPrice.

Related: Bitcoin vs gold: ETF flows point to early capital rotation signs

The abrupt price drop and the spike in precious metal volatility “point to the role of retail flows, and amplification of price moves due to forced sales by leveraged ETFs, trend-following investors such as commodity trading advisers, and margin dynamics,” BIS stated.

Dollar strengthens as commodities and crypto weakens

The bank concluded that gold and silver declines coincided with changing expectations around US monetary policy and the performance of the US dollar, which has gained 4.7% since late January, according to the DXY dollar index.

“The precious metals crash seemingly coincided with shifts in expectations about the US dollar and the path of monetary policy, but it was hard to square with broader changes in fundamentals.”

Meanwhile, crypto markets have fallen around 43% from their October total capitalization peak as retail sentiment and interest in digital assets have dried up and remain at bear market levels.

Magazine: Metaplanet’s Japan Bitcoin bet, Bithumb ordered suspension: Asia Express

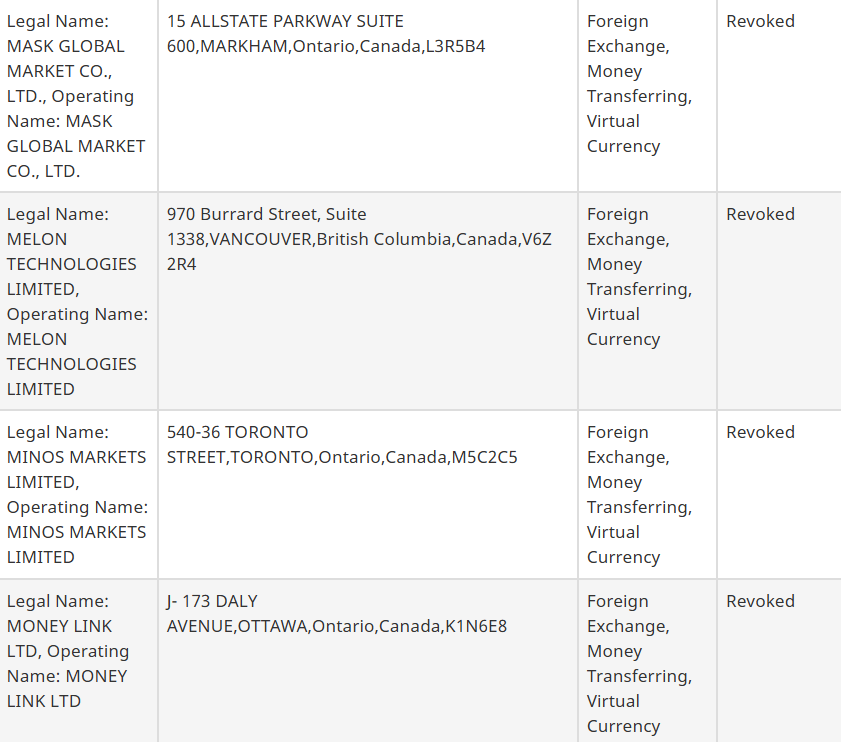

Canada’s financial intelligence unit has revoked the registrations of 50 money services businesses (MSBs) so far this year, with 47 related to crypto, and the minister of finance says it will continue cracking down.

Canada’s Financial Transactions and Reports Analysis Centre (FINTRAC) said on Monday that it took its most recent action, revoking 23 MSB registrations.

Minister of Finance François-Philippe Champagne said in a statement on Tuesday that it’s part of the government’s latest effort to combat money laundering, with FINTRAC also “strengthening enforcement and increasing transparency on compliance actions.”

He added that the 23 cancellations represented “a significantly increased pace of action, and our government will maintain this momentum.”

“Our government will continue to monitor and pursue new measures to address risks posed by virtual currency businesses, such as cryptocurrency MSBs and crypto ATMs, which can be used to facilitate money laundering and fraud,” Champagne said.

Traditional financial systems, such as wire transfers, have long been used for money laundering and other forms of fraud due to their scale and widespread adoption.

Related: US, UK, Canada launch joint operation to disrupt crypto fraud

The Financial Action Task Force estimates that 2 to 5% of global GDP is laundered through traditional financial systems, whereas Chainalysis estimates that less than 1% of crypto transactions are linked to illicit activity.

Two crypto platforms fined near the end of last year

FINTRAC has been stepping up its enforcement actions against crypto firms, issuing a $126 million fine against crypto platform Cryptomus in October for a range of alleged violations, including failing to report suspicious transactions on 1,068 separate occasions in July 2024 and failing to develop and apply written compliance policies.

Crypto exchange KuCoin also received a $14 million penalty a month earlier for violations, including allegedly failing to register as a foreign money services business with FINTRAC and failing to report large crypto transactions with the required information.

Magazine: Big Questions: Can Bitcoin save you from the dreaded Cantillon Effect?

Visa’s crypto division has launched a tool to allow artificial intelligence agents to make payments, the same day the Stripe-backed blockchain Tempo launched alongside a protocol for AI agents.

“Excited to share Visa CLI, the first experimental product from Visa Crypto Labs,” Cuy Sheffield, the head of Visa Crypto Labs, posted to X on Wednesday.

A website for Visa CLI, meaning a command line interface where users type what action a program must take, says the tool will give an AI agent “the ability to securely pay for what you need as you code.”

The tool also said it allows for “programmatic card payments without the pain of API keys.” API keys can include sensitive information that AI agents can leak, causing security risks.

It’s the latest standard seeking to allow AI agents to make payments online as hype around AI and stablecoins grows.

Coinbase launched its x402 standard to facilitate agentic stablecoin payments in May, which was most recently integrated by Sam Altman’s World in a developer toolkit for AI agents released on Tuesday.

Stripe-backed Tempo blockchain goes live

Meanwhile, the Tempo blockchain, backed by payments company Stripe, launched on mainnet on Wednesday, releasing a payments protocol for AI agents.

Tempo posted to X that its blockchain was “purpose-built for payments” and focused on servicing high-throughput stablecoin transactions, currently one of the most popular ways AI agents are used.

“Agents can already write code, coordinate services, retrieve data, and execute complex workflows across the internet. But as these systems become more capable, they increasingly need to transact,” Tempo said.

Agent payments will soon overtake human payments on the internet. The Machine Payments Protocol (@mpp) is a new open standard co-authored by @stripe and @tempo.

It’s designed to be extensible and payment-method agnostic, already supporting stablecoins, cards, and more. pic.twitter.com/dEjfGN2tp9

— Tempo (@tempo) March 18, 2026

The project also launched the Machine Payments Protocol, an open standard that it developed with Stripe, which it described as giving “a standard way for agents and services to coordinate payments programmatically.”

Related: SlowMist introduces Web3 security stack for autonomous AI agents

Tempo said the protocol “is designed to be rail-agnostic and extensible,” noting that Visa had extended support for the protocol on its card payments network while Stripe is supporting “cards, wallets, and other payment methods.”

The crypto fintech Lightspark had also extended support for the protocol over the Lightning Network for Bitcoin (BTC) payments.

AI Eye: IronClaw rivals OpenClaw, Olas launches bots for Polymarket

Can XRP Go to $3000? #shorts

Portadown nurse fined for unlawful possession of unlicensed prescription medicines

At Close of Business podcast March 19 2026

-

Crypto World5 days ago

Crypto World5 days agoHYPE Token Enters Net Deflation as HyperCore Buybacks Outpace Staking Rewards

-

Tech3 days ago

Tech3 days agoYour Legally Registered ‘Motorcycle’ Might Not Count Under Proposed US Law

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Addict Lip Glow

-

Tech2 days ago

Tech2 days agoAre Split Spacebars the Next Big Gaming Keyboard Trend?

-

Sports5 days ago

Why Duke and Michigan Are Dead Even Entering Selection Sunday

-

Business4 days ago

Business4 days agoSearch for Savannah Guthrie’s Mother Enters Seventh Week with No Arrests

-

Business5 days ago

Business5 days agoUS Airports Launch Donation Drives for Unpaid TSA Workers as Partial Government Shutdown Enters Fifth Week

-

Crypto World5 days ago

Coinbase and Bybit in Investment Talks: Could Bybit Finally Enter the US Crypto Market?

-

Business3 days ago

Business3 days agoAustralian shares drop as Iran war enters third week

-

Business5 days ago

Business5 days agoCountry star Brantley Gilbert enters growing non-alcoholic beer market

-

Crypto World3 days ago

Crypto World3 days agoCrypto Lender BlockFills Enters Chapter 11 with Up to $500M in Liabilities

-

Sports6 days ago

Sports6 days agoCollege Basketball Best Bets: Conference Tournament Semifinal Picks

-

Politics22 hours ago

Politics22 hours agoThe House | The new register to protect children from their abusers shows Parliament at its best

-

Business6 days ago

Business6 days agoTrump demands Powell cut rates as Iran conflict raises energy prices

-

Fashion3 days ago

Fashion3 days ago25 Celebrities with Curly Hair That Are Naturally Beautiful

-

News Videos14 hours ago

News Videos14 hours agoRBA board divided on rate cut, unusually buoyant share market | Finance Report | ABC NEWS

-

Crypto World6 days ago

Crypto World6 days agoSenate Votes to Include CBDC Ban in Bipartisan Housing Bill

-

NewsBeat6 days ago

NewsBeat6 days agoDeane Road crash near Bolton colleges and university

-

News Videos6 days ago

News Videos6 days agoTom Lee: The 100x Opportunity EVEN Bigger Than Bitcoin (New Ethereum Prediction 2026)

-

Crypto World15 hours ago

Crypto World15 hours agoCanada’s FINTRAC revokes registrations of 23 crypto MSBs in AML crackdown

You must be logged in to post a comment Login