Crypto World

Swift Adds Blockchain Ledger to Enable 24/7 Cross-Border Payments

Swift has unveiled plans to integrate a blockchain-based shared ledger into its core infrastructure, marking one of the most significant evolutions of the global payments network in decades. Announced at Sibos 2025 in Frankfurt, the initiative aims to enable real-time, 24/7 cross-border payments and the regulated movement of tokenized value at global scale. The project brings together more than 30 financial institutions from 16 countries and starts with a conceptual prototype developed alongside Consensys. Rather than replacing existing rails, the ledger is designed to extend Swift’s trusted role into digital finance while preserving compliance, resilience, and operational rigor.

Key takeaways

- Swift plans to add a blockchain-based shared ledger to support instant, always-on cross-border payments.

- The initiative was announced at Sibos 2025 in Frankfurt and involves over 30 global banks from 16 countries.

- The first use case focuses on real-time, 24/7 interbank cross-border payments.

- The ledger will be interoperable with existing payment rails and emerging digital networks.

- Smart contracts will be used to embed compliance, controls, and transaction rules directly into payment flows.

Market context: The move comes as financial institutions globally face pressure to modernize cross-border payments amid growing demand for instant settlement, tokenized assets, and regulated digital money, while central banks and regulators push for higher transparency and resilience.

Why it matters

Cross-border payments remain one of the most complex and costly parts of the financial system, often constrained by time zones, batch processing, and fragmented infrastructure. By introducing a shared digital ledger, Swift is signaling that legacy financial infrastructure can evolve without abandoning regulatory discipline.

For banks, the initiative promises improved transparency, faster settlement, and reduced operational friction, all while maintaining compatibility with existing correspondent banking models. For the broader market, it represents a pragmatic bridge between traditional finance and distributed ledger technology.

The project also highlights a broader industry shift toward tokenized value and programmable money, with Swift positioning itself as a neutral orchestrator rather than a competing blockchain network.

What to watch next

- Progress of the conceptual prototype being developed with Consensys.

- Expansion of use cases beyond cross-border payments into other forms of tokenized value.

- Governance frameworks and compliance standards agreed by participating banks.

- Further announcements on interoperability with public and private blockchain networks.

Sources & verification

- Official Swift announcement detailing the blockchain-based ledger initiative.

- Statements from Swift CEO Javier Pérez-Tasso delivered at Sibos 2025.

- Public comments from participating global banks on their involvement.

- Swift’s published FAQs outlining scope, benefits, and development phases.

Swift’s blockchain ledger and the future of cross-border payments

Swift’s decision to incorporate a blockchain-based shared ledger into its technology stack represents a strategic response to a rapidly changing payments landscape. For decades, Swift has served as the backbone of global financial messaging, connecting institutions across more than 200 countries and territories. The new ledger does not replace that role but extends it into a digital environment where value can move instantly and continuously.

The initiative was formally announced during the opening plenary of Sibos 2025, where Swift CEO Javier Pérez-Tasso acknowledged that the move might surprise parts of the market. He framed the development as a convergence rather than a contradiction, arguing that traditional finance and blockchain technology can coexist within a regulated system. According to Pérez-Tasso, banks are increasingly prepared for this transition and are asking Swift to take on a broader coordinating role.

At the core of the project is a shared digital ledger designed to record, sequence, and validate transactions between financial institutions in real time. Built with interoperability as a guiding principle, the ledger is intended to connect seamlessly with both established payment rails and emerging digital networks. Smart contracts will enforce transaction rules, embedding compliance and risk controls directly into payment flows rather than layering them on afterward.

The first use case under development is real-time, 24/7 cross-border payments, an area where inefficiencies have long persisted. Current systems often rely on batch processing and reconciliation across multiple intermediaries, leading to delays and uncertainty. A shared ledger, accessible around the clock, could significantly improve predictability and transparency while reducing settlement times.

Swift has emphasized that operational excellence remains central to the design. The ledger is being developed in parallel with ongoing enhancements to existing rails, APIs, and ISO 20022 messaging standards. This layered approach reflects Swift’s view that innovation should strengthen, not undermine, the reliability and security that global finance depends on.

Collaboration is another defining feature of the initiative. Financial institutions from regions spanning Europe, North America, Asia-Pacific, the Middle East, and Latin America are actively involved in shaping the ledger’s functionality and governance. Participating banks include major global and regional players such as Bank of America, HSBC, JP Morgan Chase, Deutsche Bank, BNP Paribas, Citi, BBVA, and many others.

Executives from these institutions have described the project as a foundational upgrade rather than an incremental change. Many point to the importance of interoperability and common standards, particularly as tokenized assets and digital currencies gain traction. A shared ledger coordinated through Swift’s neutral network could help avoid fragmentation and support multi-currency, atomic settlement across jurisdictions.

Several banks highlighted the relevance of the initiative for liquidity management and always-on payments. In a global economy that increasingly operates beyond traditional business hours, the ability to move regulated value in real time is becoming a competitive necessity. The ledger is positioned as an enabler of this shift, supporting both wholesale and, eventually, broader client-facing use cases.

Swift has also linked the project to its broader work on digital assets and interoperability. Alongside the ledger, the organization is developing solutions that allow value to move between private and public networks without compromising compliance. This reflects an understanding that the future financial system will likely consist of multiple interconnected platforms rather than a single dominant rail.

From a governance perspective, the initiative is being developed in stages, beginning with a prototype. Timelines for broader availability will depend on testing, regulatory alignment, and industry adoption. Swift has been clear that the ledger will evolve in close consultation with its community, maintaining alignment with global regulatory standards.

The broader significance of the project lies in its signal to the market. By embracing blockchain-based infrastructure while reaffirming its commitment to trust and resilience, Swift is attempting to chart a middle path between innovation and stability. If successful, the shared ledger could become a key component of next-generation global payments, supporting tokenized value, instant settlement, and interoperability at scale.

As Pérez-Tasso concluded during Sibos, the ledger represents a platform not just for today’s needs but for future transformation. Its ultimate impact will depend on execution, collaboration, and the industry’s willingness to converge on shared standards. For now, it marks a notable step in the gradual modernization of global financial infrastructure.

“This is a powerful platform for the future. And it can be even more transformational in the future.” – Javier Pérez-Tasso, Swift CEO

Citi is among a growing group of banks working with us to shape our blockchain-based ledger – extending Swift’s infrastructure to support tokenised value at scale.

Through industry-wide collaboration, we’re enabling a future where value moves seamlessly in a multi-model,… pic.twitter.com/AAJmkJkUmH

— Swift (@swiftcommunity) February 6, 2026

Decentralized lending protocol Aave has officially launched on Ethereum layer 2 X Layer.

Summary

- Aave has launched on X Layer, enabling OKX Wallet users to lend, borrow, and earn yield directly on the network without bridging assets.

- X Layer, developed by OKX, has seen limited growth so far, with about $25 million in total value locked.

According to the official announcement, the launch will allow OKX Wallet users and DeFi participants to directly supply assets, borrow against collateral, and earn yield on the network without having to use a separate wallet or bridge assets across chains.

X Layer was developed by OKX and launched in 2024, but network growth has been relatively slow so far, with the chain holding only about $25 million in total value locked as of press time.

Onboarding Aave could significantly strengthen liquidity and expand the network’s DeFi capabilities.

“With a multi-year track record across more than a dozen blockchain networks and a 60% market share of DeFi lending, Aave is the largest and most trusted onchain lending network, with over $46 billion in supply & borrow. Its arrival on X Layer brings that same battle-tested infrastructure to OKX’s L2 ecosystem, permissionless, non-custodial, and accessible directly from OKX Wallet,” OKX said.

As part of the expansion, users can supply assets including USDT0, USDG, GHO, xBTC, xETH, xSOL, xBETH, and xOKSOL to earn yield that compounds automatically while retaining custody of their tokens.

Further, users will be able to borrow assets such as USDT0, USDG, GHO, xBTC, xETH, and xSOL against their collateral without any credit check or intermediary.

To access the service, OKX Wallet users just need to open the wallet, navigate to Aave through the DApps section, and connect to the X Layer network.

The latest expansion follows the launch of Orbit, a social trading platform that the crypto exchange introduced earlier this month.

As previously covered, Orbit is designed to combine social media-style interaction with trading tools, allowing users to share strategies, discuss market developments, and follow experienced traders in real time.

Around the same time, OKX disclosed a strategic investment from Intercontinental Exchange, with the deal set to give ICE a seat on the company’s board.

The Ripple research team has published a paper on adding transaction privacy to the XRP Ledger (XRPL).

The paper introduces Confidential Transfers for Multi-Purpose Tokens (Confidential MPTs). The goal is to enable institutional and regulated use cases, with issuer controls such as freezing and clawbacks.

Follow us on X to get the latest news as it happens

The paper is authored by Murat Cenk, Aanchal Malhotra, and Joseph Ayo Akinyele. The Confidential MPTs would be a cryptographic extension of the XLS-33 token standard, which went live on the XRPL mainnet in October 2025.

The protocol replaces plaintext per-account balances with EC-ElGamal ciphertexts. Furthermore, it uses non-interactive zero-knowledge proofs to enforce transfer correctness and balance sufficiency without requiring decryption by validators.

Meanwhile, sender and receiver identities remain visible, preserving XRPL’s account-based model.

“To accommodate regulatory and institutional requirements, Confidential MPTs provide cryptographic auditability through an on-chain selective-disclosure model based on multi-ciphertext balance representations and equality proofs, while remaining compatible with simpler issuer-mediated audit models,” the abstract reads.

The timing aligns with shifting regulatory attitudes toward on-chain privacy. In a recent report submitted to Congress in early March, the US Treasury Department acknowledged that lawful users of digital assets may rely on mixers when transacting on public blockchains.

The privacy paper arrives as Ripple simultaneously strengthens the network’s security foundation. The firm recently outlined an AI-driven security strategy for XRPL.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Ripple Researchers Propose Privacy-Preserving Transfers for XRPL Multi-Purpose Tokens appeared first on BeInCrypto.

Key Takeaways

- Proposed legislation would prohibit stablecoins from generating yields, limiting them to payment functions exclusively

- The change would redirect yield opportunities toward traditional banking and money market instruments

- Popular DeFi platforms including Uniswap, Aave, and Compound may encounter stricter regulations on value distribution

- Trading volumes, liquidity depth, and token demand across DeFi could decline significantly

- Regulated stablecoin issuers like Circle stand to gain from tighter integration with payment systems

The most recent iteration of the CLARITY Act has sparked significant discussion around its stablecoin provisions. Industry experts warn that decentralized finance tokens may bear the brunt of the legislation’s consequences.

Under the proposed framework, stablecoins would be prohibited from providing yields or any similar incentive structures, including balance-based rewards. This restriction would fundamentally transform stablecoins into payment instruments rather than blockchain-based savings vehicles.

Markus Thielen, who established 10x Research, indicated that the legislation would effectively channel yield opportunities back into conventional financial systems. Traditional banks, money market vehicles, and compliant financial products would capture these benefits, while cryptocurrency-native services would lose competitive advantage in offering returns.

Initial speculation suggested that DeFi platforms might actually attract more users if centralized crypto services were prevented from distributing yields. The theory presumed capital would migrate toward onchain alternatives.

However, Thielen challenged this assumption. He explained that the CLARITY regulatory structure would probably apply to user-facing platforms and token economics, especially when fee structures or governance mechanisms begin resembling equity instruments.

Potential Impact on DeFi Platforms

This regulatory approach places numerous DeFi initiatives under scrutiny. Decentralized trading venues and lending services may encounter fresh restrictions governing their operations and value distribution mechanisms.

Platforms such as Uniswap, Sushi, and dYdX face potential consequences, alongside lending services like Aave and Compound. Enhanced regulatory oversight might trigger diminished trading activity, thinner liquidity pools, and decreased token valuations, the 10x Research analysis suggests.

The fundamental question centers on whether these platforms can maintain fee distribution or incentive programs for token holders without triggering new stablecoin-focused regulations.

Thielen observed that distinguishing between governance tokens and regulated financial instruments grows increasingly complex within this regulatory framework.

Circle Positioned for Potential Gains

The legislation wouldn’t create obstacles for every cryptocurrency entity. Circle, which issues the USDC stablecoin, might emerge as a beneficiary under the proposed rules.

Thielen characterized the regulation as fundamentally favorable for infrastructure providers like Circle. Should stablecoins become embedded within payment networks, issuers maintaining robust regulatory compliance would secure advantageous positions.

The CLARITY Act continues advancing through the legislative pipeline. Congress has not yet enacted a final version.

While stablecoin provisions dominate policy discussions in Washington, industry analysts emphasize that the ripple effects across DeFi ecosystems deserve equal attention.

A new app from the US government has sparked concerns among users and researchers over potential location-tracking features, security vulnerabilities and data collection.

The White House launched the app on Friday as a way for users to get a “direct line to the White House,” including receiving breaking news alerts on major government announcements, watching livestreams and keeping up to date on “policy breakthroughs.”

However, users on X have raised concerns about the permissions required to use the app, including access to the device’s location, shared storage and network activity, though these claims have not been independently verified.

While many apps often request location permissions and can log user data, an app launched by the federal government requesting this information can invite additional concerns.

However, both listings on the Google Play Store and Apple’s App Store currently do not display these warnings.

A White House app privacy policy said it automatically stores information about the originating Internet Protocol (IP) address and other basic information, while it can retain names and email addresses of subscribers, though these are not required to use the app.

Cointelegraph has contacted the White House for comment.

Security engineer says GPS tracking is part of the app

On the app’s Google Play Store page, it states that personal data, including phone numbers and email addresses, may be collected through download and use. Apple’s App Store, meanwhile, directs users to the White House’s privacy policy.

A software developer using the X handle Thereallo, along with Adam, a security engineer and infrastructure architect, say they have identified code suggesting the app could access a device’s GPS for tracking.

While the feature is common across a number of apps, Adam said it is unusual for location-tracking services to be in software that does not appear to need them.

“There is no map, no local news, no geofencing, no events near you, no weather. Nothing in the app that requires location,” he added.

Concerns of GPS tracking every 4.5 minutes

Thereallo made a similar claim that the app includes code that could enable tracking a device every 4.5 minutes in the foreground and 9.5 minutes in the background, though this has not been independently verified.

They found that it still requires permission but warned that it is only “one call away from activating,” and that the tracking “infrastructure is there, ready to go.”

Related: Trump advisory council draws Coinbase co-founder, tech leaders

At the same time, Thereallo said the app is collecting other data such as notification interactions, in-app message clicks and phone number.

Security could be broken, researcher says

Adam said the app’s security may also be weak enough for a technically skilled person to intercept its data or alter its functionality

“Anyone on the same Wi-Fi network, say, at a coffee shop, an airport, or a congressional hearing room, can intercept API traffic with a proxy. Anyone with a jailbroken device can hook and modify the app’s behavior at runtime,” he said.

“No servers were probed. No network traffic was intercepted. No DRM was bypassed. No tools were used that require jailbreaking. Everything described here is observable by anyone who downloads the app from the App Store and has a terminal.”

Magazine: Morgan Stanley Bitcoin ETF undercuts BlackRock, SBF pardon unlikely: Hodler’s Digest, Mar. 22 – 28

The crypto market rebounded 1.2% on Monday to $2.4 trillion in a relief rally amidst signs of potential de-escalation of the ongoing U.S. and Iran war in the Middle East.

Summary

- The crypto market rebounded modestly as hopes of U.S.–Iran de-escalation eased risk-off sentiment, lifting major assets including Bitcoin and Ethereum.

- Relief rally came despite heightened derivatives volatility, with roughly $350 million in liquidations led by long positions, indicating fragile market positioning.

- Macro risks persist as rising oil prices and hawkish rate expectations continue to weigh on sentiment, limiting upside despite a slight improvement in the fear and greed index.

Bitcoin (BTC) rose 1.4% to back above $67,600 after dropping to a 4-week low around $65,000 earlier today. Ethereum (ETH) was up 2.2% to over $2,000, while major crypto assets such as XRP (XRP), Solana (SOL), and Dogecoin (DOGE) posted gains between 1 and 2% each.

Despite a rebound in spot crypto prices, significant volatility was observed across crypto derivatives markets. Data from Coinglass shows that over the past 24 hours, nearly $350 million worth of positions were liquidated from the market, with the brunt of the liquidations coming from trades that held long positions.

Meanwhile, the crypto fear and greed index jumped 4 points to 27,, suggesting some easing, although overall sentiment remains shaky.

The crypto market took a breather on Monday after reports emerged that Pakistan is preparing to host peace talks between the U.S. and Iran to end their war in the Middle East region after diplomats from both sides agreed to meet.

The news seemed to have calmed investor nerves as the war entered its fifth week, with both nations going back and forth against each other’s energy and military infrastructure.

The two-day talks in the Pakistani capital that began on Sunday are being led by Pakistani Foreign Minister Ishaq Dar over possible ways to bring an end to the war in the region as well as the blockade in Islamabad.

This came after Iran allowed 20 Pakistani commercial vessels to pass through the Strait of Hormuz, easing a naval blockade that has stifled regional trade.

Elsewhere, U.S. President Donald Trump has recently instructed the Pentagon to pause strikes on Iranian power and energy infrastructure for five days to allow for these productive talks.

Concerns remain

Meanwhile, Iranian parliament speaker Mohammad Bagher Qalibaf has dismissed the proposed talks in Islamabad as a tactical distraction after the arrival of thousands of U.S. troops in the Middle East, stating that Iran was ready to retaliate if necessary.

Earlier, Trump had announced that the U.S. would deploy 10,000 additional troops to expand its military options in the region.

Amidst the ongoing tension, traditional safe-haven assets such as gold and precious metals continued their march. Gold rose by 1.1% over the day to $4,544, while Silver gained by 1.5%.

Against this backdrop, oil prices across the globe have surged back above $100. West Texas Intermediate (WTI) crude oil was trading at $100.7, up 1% over the day, while Brent crude was up 2.2% to $115.

This trend could further dampen investor sentiment, as rising crude oil prices tend to fuel fears of persistent inflation. Such inflationary pressure could, in turn, motivate the Federal Reserve to delay highly anticipated rate cuts, keeping borrowing costs higher for longer.

At press time, the odds of the Fed holding interest rates steady at 3.5% to 3.75% stood at 96.4% while only 3.6% of market participants held out hope for a 25bps reduction.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

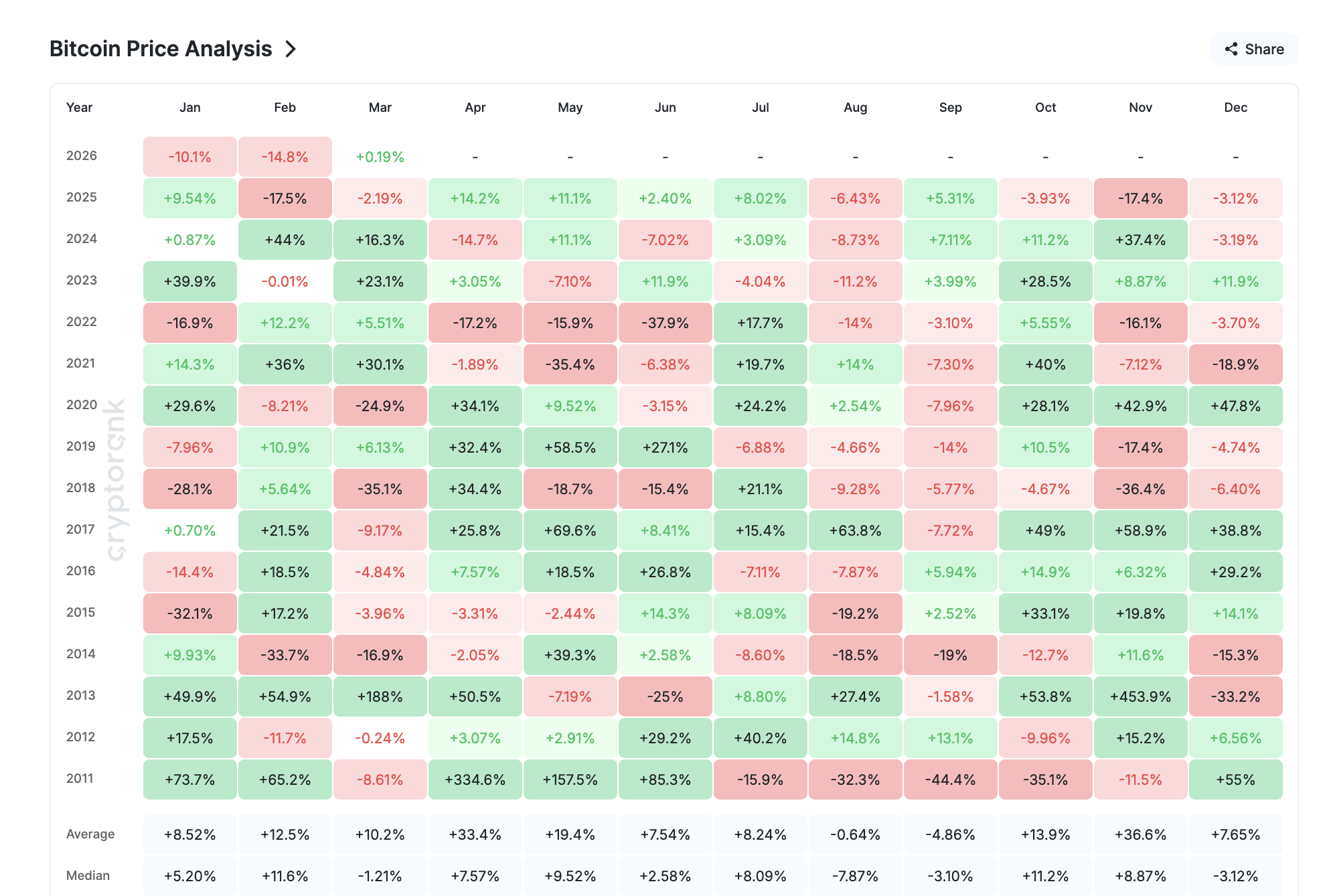

Bitcoin (BTC) price is entering April 2026 at a crossroads. March is closing with a barely positive 0.19% gain, a sharp fade from the over 5% monthly gain BTC held earlier.

With history, ETF flows, and whale behavior all sending mixed signals, April could define Bitcoin’s direction for the rest of 2026.

History Favors April, but the 3-Day Chart Does Not

The monthly returns chart shows that the Bitcoin price has struggled in 2026. January closed at -10.1%, and February dropped 14.8%, both defying their historically positive averages of +8.52% and +12.5%, respectively. March is barely holding at +0.19%, well below its historical average of +10.2%.

Want more token insights like this? Sign up for Editor Harsh Notariya’s Daily Crypto Newsletter here.

April has historically been one of Bitcoin’s strongest months, with an average return of +33.4% and a median of +7.57%. However, given that both January and February already broke their historical trends, relying on seasonal patterns alone would be risky.

The 3-day chart paints a concerning Bitcoin price prediction for the months ahead. Since peaking at $125,900 on October 4, 2025, BTC has dropped to $60,000 at its lowest, a decline of over 52%. The price action since the January lows resembles a bear flag, a consolidation pattern that typically resolves with another leg down matching the pole’s size.

The price is currently testing the lower trendline of the flag. If the breakdown confirms on the 3-day chart, the measured move points to a significant further decline. That larger picture sets the tone for how April could unfold.

Bitcoin ETFs Show Cracks Beneath a Green Surface

On the surface, Bitcoin ETF flows in March look encouraging. Monthly data shows $1.13 billion in net inflows, ending a four-month outflow streak. The reversal suggests institutional conviction is returning.

However, the weekly breakdown tells a different story. The week of March 6 brought $568 million in inflows. March 13 surged to $767 million. March 20 slowed to $95 million. And the week ending March 27 flipped red at -$296 million.

March started strong but is ending weak. The momentum that drove ETF inflows earlier in the month has faded, and the final week’s outflow could set the tone heading into April.

The Exchange Whale Ratio, a CryptoQuant metric that tracks the ratio of the top 10 exchange inflows to total inflows, reinforces this concern. On January 10, the ratio sat at 0.34, its lowest year-to-date level. By March 28, it had surged to 0.79, with two notable spikes on March 14 and March 28.

A rising whale ratio means Bitcoin whales are sending a larger share of coins to exchanges relative to all other participants. The upward trend throughout 2026 shows that large holders have been consistently distributing, and March offered no exception.

The combination of fading ETF inflows and rising whale selling heading into April weakens the demand picture at a time when the technical structure already leans bearish.

Bitcoin Price Levels To Watch in April

The most critical level for April is $67,000. It has acted as a strong support base throughout 2026, with every dip below it being quickly reclaimed. However, a clean 3-day close below $67,000, combined with the weakening ETF and whale data, could trigger the next leg down.

Below $67,000, the next support sits at $61,500 (the 0.382 Fibonacci level), followed by $60,000, a psychological and technical floor. April will likely be defined by whether Bitcoin can hold the $60,000 to $61,500 zone. A break under that range opens the door to $57,000 and eventually $52,600, which aligns with the 0.618 Fibonacci retracement.

On the upside, strength returns if BTC reclaims and holds above $75,900, the March local high. A move above that would weaken the bear flag structure and shift the Bitcoin price prediction for April from defensive to constructive.

For now, April is about survival above $60,000. The ETFs, the whales, and the 3-day chart all suggest the path of least resistance still points lower.

The post Bitcoin Price Prediction: What To Expect From BTC In April 2026 appeared first on BeInCrypto.

Crypto World

Zoomex Launches Earning Initiative as Inflation Drives Shift Toward Capital Efficiency in Crypto Markets

Crypto exchange Zoomex has introduced a new user initiative focused on its earning products, as rising inflation and uncertain interest rate expectations continue to reshape how traders manage capital across digital asset markets.

The move comes amid a broader shift in investor behavior. With interest rates remaining elevated across major economies and macro conditions becoming less predictable, market participants are increasingly looking beyond trade execution to how capital is managed between positions.

From Market Timing to Capital Efficiency

While volatility remains a defining feature of crypto markets, Zoomex notes that trading activity alone is no longer sufficient in the current environment.

A key issue, according to the platform, is idle capital — funds that remain unutilised outside active positions.

“Traders have traditionally focused on timing the market, but in a high interest rate environment, the bigger question is what happens to capital when it is not being deployed,” said Fernando, Marketing Director at Zoomex.

This dynamic is becoming more visible as users balance short-term trading opportunities with longer holding periods, particularly during phases of macro-driven uncertainty.

Industry Shift: From Fragmented Tools to Integrated Strategies

The growing demand for yield-generating strategies has led many platforms to introduce earning products. However, these offerings are often fragmented, requiring users to move assets across multiple interfaces or sacrifice flexibility for returns.

According to Zoomex, this structure limits capital efficiency and adds operational complexity for users attempting to manage assets dynamically.

Instead, the platform sees trading, strategy, and earning as interconnected components of a broader capital management approach.

A Multi-Layer Approach to Continuous Capital Deployment

Zoomex integrates multiple modes of capital deployment within a single system, allowing users to shift between strategies without transferring funds across products or platforms.

The framework consists of:

- Trading Layer — enabling users to capture market volatility through spot and futures trading

- Strategy Layer — including tools such as grid trading, designed to systematically deploy capital in ranging or uncertain market conditions

- Earning Layer — allowing assets to generate yield when not actively used in trades

Together, this structure supports more continuous capital utilisation, whether through active trading, automated strategies, or passive yield generation.

“The market is no longer just about whether you are in or out of a trade,” Fernando added. “It’s about whether your capital remains productive across different market conditions.”

Beyond trading and earning within the platform, Zoomex is also expanding how capital can be utilized in real-world scenarios through the introduction of the Zoomex Card.

The card enables users to access and spend their digital assets more seamlessly, bridging the gap between on-platform capital management and everyday financial use. By allowing assets to remain connected to the broader Zoomex ecosystem, users can maintain flexibility while extending the utility of their funds beyond trading environments.

This development reflects a broader view of capital efficiency — not only in terms of generating yield or executing trades, but also in enabling liquidity and usability in daily life without unnecessary friction.

Importantly, the system is designed to remain accessible, reducing the need for complex allocation strategies or multi-platform management.

Zoomex Expands Access to Earning Tools Through New User Initiative

As part of this shift, Zoomex has introduced a new user campaign focused on its Earning products, aimed at improving accessibility for users entering the platform.

The initiative is designed to guide users through earning features, providing structured entry points into yield-generating strategies at a time when interest rate considerations are becoming increasingly central to investment decisions.

The company stated that the campaign is intended to simplify onboarding while helping users understand how to balance trading activity with capital efficiency.

Zoomex March New User Benefits |200% APY

Platforms Evolve Into Capital Management Systems

The development reflects a broader transition across the industry, where trading platforms are increasingly evaluated not only on execution performance, but on their ability to support capital management across varying market conditions.

Metrics such as capital utilisation, yield accessibility, and strategy flexibility are becoming more central to how users assess platform value.

Fernando said:

“Users are no longer choosing between trading and earning — they expect both to function seamlessly within the same environment.”

As macroeconomic uncertainty persists, the role of crypto platforms is expected to expand beyond trade execution toward integrated capital management.

In this context, the ability to maintain productive capital allocation — even outside active trading periods — may become a defining factor in how users navigate both volatility and long-term portfolio growth.

Zoomex indicated that its product development will continue to align with this shift, with a focus on enabling more efficient, flexible, and continuous capital strategies for users globally.

About ZOOMEX

Founded in 2021, Zoomex is a global cryptocurrency trading platform with over 3 million users across more than 35 countries and regions, offering 700+ trading pairs. Guided by its core values of “Simple × User-Friendly × Fast,” Zoomex is also committed to the principles of fairness, integrity, and transparency, delivering a high-performance, low-barrier, and trustworthy trading experience.

Powered by a high-performance matching engine and transparent asset and order displays, Zoomex ensures consistent trade execution and fully traceable results. This approach reduces information asymmetry and allows users to clearly understand their asset status and every trading outcome. While prioritizing speed and efficiency, the platform continues to optimize product structure and overall user experience with robust risk management in place.

As an official partner of the Haas F1 Team, Zoomex brings the same focus on speed, precision, and reliable rule execution from the racetrack to trading. In addition, Zoomex has established a global exclusive brand ambassador partnership with world-class goalkeeper Emiliano Martínez. His professionalism, discipline, and consistency further reinforce Zoomex’s commitment to fair trading and long-term user trust.

In terms of security and compliance, Zoomex holds regulatory licenses including Canada MSB, U.S. MSB, U.S. NFA, and Australia AUSTRAC, and has successfully passed security audits conducted by blockchain security firm Hacken. Operating within a compliant framework while offering flexible identity verification options and an open trading system, Zoomex is building a trading environment that is simpler, more transparent, more secure, and more accessible for users worldwide.

For more info: Website | X | Telegram | Discord

The post Zoomex Launches Earning Initiative as Inflation Drives Shift Toward Capital Efficiency in Crypto Markets appeared first on BeInCrypto.

Key Highlights

- The premier DeFi lending platform Aave has deployed to X Layer, the Ethereum Layer 2 network developed by OKX

- Users of OKX Wallet gain immediate access to lending and borrowing functionality without cross-chain asset transfers

- Available assets on X Layer include USDT0, xBTC, xETH, xSOL, with loan-to-value ratios reaching 88% for certain liquid staking token pairs

- With $23.5 billion in TVL, Aave recently achieved the milestone of $1 trillion in aggregate lending volume

- This marks Aave’s 21st blockchain deployment, expanding beyond networks like Ethereum, Arbitrum, and Base

The world’s leading decentralized lending platform, Aave, has officially deployed on X Layer, OKX’s Ethereum Layer 2 solution. This integration provides OKX Wallet users with seamless access to onchain financial services without requiring external wallets or asset bridging between networks.

The cryptocurrency exchange OKX confirmed the integration on Monday. Through the native wallet interface, users can now deposit assets, take out collateralized loans, and generate auto-compounding returns.

“The deployment to X Layer delivers proven, reliable infrastructure to OKX’s Layer 2 environment—fully permissionless, self-custodial, and integrated directly within OKX Wallet,” the exchange stated in an official announcement.

Stani Kulechov, who founded Aave Labs, shared his perspective on the deployment. “This expansion to X Layer bridges Aave’s deep liquidity with an emerging network of users and decentralized applications, simplifying the process of earning yields, borrowing funds, and developing on the platform,” Kulechov explained.

The deployment supports multiple digital assets including USDT0, USDG, GHO, xBTC, xETH, xSOL, xBETH, and xOKSOL. The platform operates without traditional credit verification or centralized intermediaries.

X Layer’s Expanding DeFi Infrastructure

X Layer went live in May 2024. The network currently maintains approximately $25 million in total value locked. Transaction costs average just $0.0005, with blocks produced every second.

Several established DeFi platforms have already integrated with X Layer, including Uniswap, Chainlink, and Stargate. Aave represents the most significant protocol integration thus far.

The Layer 2 network has implemented six specialized “eModes” optimized for its asset composition. These configurations enable loan-to-value percentages as high as 88% for specific liquid staking token combinations.

This development aligns with OKX’s strategic initiative to incorporate DeFi capabilities directly into its wallet infrastructure, mirroring approaches from rivals such as Coinbase and Binance. Last November, OKX introduced integrated DEX trading functionality for Base, Solana, and X Layer within its wallet.

Aave’s Performance Metrics and Growth

Aave maintains approximately $23.5 billion in total value locked distributed across over 20 different blockchain networks. This figure exceeds its nearest rival, Morpho, by more than three times—Morpho currently holds around $10 billion.

In late February, the protocol achieved a historic milestone by surpassing $1 trillion in total lending volume, becoming the first DeFi platform to reach this benchmark.

Revenue generation for Aave topped $6.2 million over the past 30 days, outpacing Morpho’s earnings by more than five times during the identical timeframe.

Cumulative net deposits across Aave exceed $40.4 billion. X Layer represents the protocol’s 21st blockchain integration.

This launch follows an overwhelmingly positive Aave DAO governance vote approving the Version 4 mainnet roadmap, demonstrating ongoing development momentum throughout the protocol ecosystem.

Quick Overview

- XRP serves primarily as a payments and cross-border transaction solution, creating a specialized but limited application

- Solana functions as a versatile blockchain platform supporting DeFi, NFTs, gaming, stablecoins, and Web3 applications, providing diverse expansion opportunities

- Ripple’s substantial XRP reserves continue raising questions among investors monitoring long-term token distribution

- Solana demonstrates superior developer engagement, typically indicating healthier long-term ecosystem vitality

- Both assets involve risk factors, though Solana’s diversified ecosystem provides additional avenues for sustainable growth

When evaluating long-term cryptocurrency investments, XRP and Solana consistently emerge as two of the most discussed assets. Each boasts substantial communities, practical applications, and significant growth potential. However, their fundamental architectures serve distinctly different objectives, making this distinction critical for investors planning three to five-year positions.

Ripple developed XRP specifically for facilitating rapid, cost-effective international money transfers. Conversely, Solana emerged as a comprehensive blockchain infrastructure supporting applications, decentralized finance, trading platforms, and digital asset creation. This fundamental distinction influences every aspect of their respective long-term performance trajectories.

XRP’s primary advantage lies in its focused mission. Ripple has dedicated years cultivating partnerships with banking institutions and payment service providers. This strategic positioning gives XRP legitimate utility within the cross-border finance sector.

Should blockchain-based settlement systems gain widespread adoption among financial institutions, XRP stands positioned to capture significant value. This represents a credible scenario driving many investors’ continued confidence in the asset.

The limitation, however, centers on XRP’s dependence on this singular growth corridor. Should institutional adoption proceed slower than anticipated, investor returns may fall short of expectations.

Solana’s Multi-Faceted Ecosystem Strategy

Unlike XRP’s specialized focus, Solana isn’t confined to a single application. The platform accommodates decentralized financial protocols, stablecoin infrastructure, NFT marketplaces, blockchain gaming, consumer-facing applications, and tokenized traditional assets.

This diversification creates multiple parallel growth trajectories. When activity decreases in one vertical, momentum in alternative sectors can sustain network demand and token value.

Developer engagement represents another domain where Solana demonstrates competitive superiority. Blockchains maintaining robust builder communities typically sustain relevance longer, as developers generate the applications attracting end users.

Elevated developer activity frequently serves as a predictive indicator of sustained platform viability. Measured against this criterion, Solana currently maintains a noticeable advantage over XRP.

Supply Economics and Investment Considerations

XRP employs a transparent supply mechanism. The token doesn’t utilize mining-based inflation, and minuscule amounts of XRP are destroyed with every transaction.

Nevertheless, Ripple’s substantial XRP treasury represents a persistent consideration for certain investors. This lingering supply overhang can constrain confidence regarding long-term price appreciation potential.

Solana incorporates inflationary mechanics into its economic design. However, this inflation receives partial counterbalancing through staking incentives and expanding on-chain economic activity.

As network utilization accelerates, organic demand for Solana can increase through transaction fees and ecosystem expansion. This dynamic provides more fundamental support for the token’s valuation over extended timeframes.

XRP’s primary uncertainties revolve around corporate adoption rates and regulatory framework development. Solana’s challenges relate more to technical execution and network stability, areas that have historically presented concerns.

Solana has recently maintained ecosystem momentum through additional stablecoin partnerships and consumer-oriented product launches, sustaining developer interest as 2025 approaches.

Investment Perspective

For investors prioritizing long-term positioning, Solana presents the more compelling platform investment thesis. While XRP maintains legitimate value within payments and settlement infrastructure, Solana’s expansive ecosystem architecture provides substantially more pathways for sustainable growth.

Key Takeaways

- ETH maintains position near $2,000 following rejection from $2,372 peak recorded earlier this month.

- Long/short ratio reaches 2.4, creating potential squeeze risk as price action remains stagnant.

- Ethereum ETFs listed in the U.S. experienced $92.5 million in withdrawals on March 26.

- Market volatility increased following $14.16 billion Bitcoin options expiration and heightened geopolitical concerns.

- Critical resistance zone positioned at $2,138–$2,151, while breach below $1,980 may trigger deeper corrections.

Ethereum currently changes hands around $2,048 as market participants attempt to defend the psychologically significant $2,000 threshold. Following a rally earlier this month, the cryptocurrency encountered strong resistance approaching $2,372. Subsequently, ETH has remained confined within a consolidation range spanning $1,900 to $2,200.

The asset trades beneath its 50-day exponential moving average positioned at approximately $2,160 and significantly under the 100-day EMA hovering near $2,420. This positioning reinforces a prevailing bearish technical structure.

Daily chart analysis reveals the RSI hovering around 44, registering below the neutral threshold of 50. Meanwhile, the MACD indicator remains beneath its signal line while drifting toward the zero mark. These technical signals collectively suggest diminishing bullish momentum.

Market observers are paying particular attention to the long/short ratio, which has escalated to approximately 2.4. This metric indicates that traders are predominantly positioning for upward movement. However, price action has failed to confirm this sentiment.

An accumulation of long positions without corresponding price appreciation often generates what market participants refer to as a “crowded trade.” Such conditions frequently precipitate a long squeeze scenario, wherein abrupt downward movement compels leveraged long holders to liquidate positions, amplifying downside momentum.

Institutional Withdrawals and Broader Market Dynamics

Data from March 26 shows U.S.-listed Ethereum ETFs registering $92.5 million in net withdrawals. These redemptions occurred within a broader pattern of outflows affecting cryptocurrency exchange-traded products.

According to SoSoValue data, on March 27 (ET), U.S. Bitcoin spot ETFs recorded a total net outflow of $225 million. Meanwhile, Ethereum spot ETFs saw a total net outflow of $48.54 million, marking an eight-day streak of net outflows. pic.twitter.com/ell1RDmAqI

— Wu Blockchain (@WuBlockchain) March 28, 2026

The preceding day witnessed a historic $14.16 billion in Bitcoin options reaching expiration on March 27. Substantial options expiry events frequently introduce volatility into cryptocurrency markets, and this occurrence contributed additional selling momentum across digital assets.

Macroeconomic and geopolitical developments further influenced market sentiment. Escalating crude oil valuations, connected to Iran’s warnings regarding a critical shipping corridor, intensified inflation anxieties. Such conditions typically create headwinds for risk-oriented assets including Ethereum.

Critical Price Thresholds for Traders

Examining resistance levels, $2,138 represents the 23.6% Fibonacci retracement calculated from the $3,402 peak down to the $1,747 trough. The Ichimoku Kijun indicator establishes another barrier at $2,151, with market participants monitoring a decisive close above this region as a potential catalyst for advancement toward $2,380.

Regarding support zones, initial downside defense stands at $1,990. Beneath this threshold, the channel bottom resides near $1,748. A confirmed breakdown through this area could accelerate bearish momentum.

Technical projections suggest ETH will likely consolidate between $1,980 and $2,170 throughout the upcoming five-session period, with probability calculations indicating less than 20% likelihood of upward price movement.

Ethereum $ETH faces a major test at $1,800! pic.twitter.com/7Jv5c8gTI3

— Ali Charts (@alicharts) March 30, 2026

Market analyst Ali Charts communicated via X that Ethereum confronts a “major test at $1,800,” indicating certain technical observers anticipate the possibility of substantially lower price levels should current support structures fail.

Separately, analyst Tom Lee has projected Ethereum could ultimately achieve $62,000, although this long-term forecast lacks a specific timeframe for realization.

With Ethereum ETF withdrawals reaching $92.5 million on March 26, ETH remains anchored near $2,000 while technical indicators continue signaling near-term vulnerability.

Yorkshire Craft Festival on Parliament Street York in April

Aave launches on OKX’s X Layer to expand on-chain lending access

Every ‘Alien’ Movie Is Finally Streaming Together on April 1

-

NewsBeat5 days ago

NewsBeat5 days agoManchester United reach agreement with Casemiro over contract clause amid transfer speculation

-

News Videos4 days ago

News Videos4 days agoParliament publishes latest register of MPs’ financial interests

-

Sports7 days ago

Sports7 days agoGary Kirsten Accuses Pakistan Cricket Board Of ‘Interference’, Mohsin Naqvi Responds

-

Sports7 days ago

Sports7 days agoRemo Stars and Kano Pillars Strengthen Survival Hopes in NPFL

-

NewsBeat2 days ago

NewsBeat2 days agoThe Story hosts event on Durham’s historic registers

-

Business4 days ago

Business4 days agoInstagram, YouTube Found Responsible for Teen’s Mental Health Struggle in Historic Ruling

-

News Videos7 days ago

News Videos7 days agoCh 9 Financial Management Part 1 | Detailed One Shot | Class 12 Business Studies Boards 2026

-

NewsBeat5 days ago

NewsBeat5 days agoTesco is selling new Cadbury Dairy Milk bar and people can’t wait to try it

-

Entertainment7 days ago

Entertainment7 days agoCynthia Bailey Dishes on ‘RHOA’ Season 17, Discusses Kandi

-

Tech7 days ago

Tech7 days agoSamsung will soon let you control smart home devices from your car’s dashboard

-

Entertainment1 day ago

Entertainment1 day agoLana Del Rey Celebrates Her Husband’s 51st Birthday In New Post

-

NewsBeat7 days ago

NewsBeat7 days agoColombian military plane with 110 soldiers onboard crashes following takeoff

-

Business6 days ago

Business6 days agoMore women enter wealth management, but few in advisory roles: study

-

Fashion7 days ago

Fashion7 days agoFringe Bags for the Season

-

Fashion6 days ago

Fashion6 days agoDoes It Matter What You Wear When You’re Laid Off and Looking?

-

NewsBeat5 days ago

NewsBeat5 days agoEntrepreneurs Forum survey reveals optimism in North East

-

Business6 days ago

Business6 days agoLate-paying firms face multimillion-pound fines under new crackdown

-

Politics6 days ago

Politics6 days agoHow Media Platforms Balance Performance and Accessibility in Image Delivery

-

Sports5 days ago

Sports5 days agoFantasy Baseball Week 1 Preview: Top sleeper hitters for both five- and 12-day period led by Munetaka Murakami

-

NewsBeat6 days ago

NewsBeat6 days agoNASA Artemis II Astronauts enter 14-Day quarantine as moon rocket reaches launchpad

You must be logged in to post a comment Login