Haseeb Qureshi, managing partner at Dragonfly, argues that crypto’s persistent friction stems from a deeper mismatch: its architecture appears better aligned with artificial intelligence (AI) agents.

In his view, many of crypto’s perceived failure modes are not design flaws but signals that humans were never the ideal primary users.

Sponsored

The Human-Crypto Disconnect

In a detailed post on X, Qureshi argued that a fundamental divide exists between human decision-making and blockchain’s deterministic architecture. He said the early vision of the industry imagined a world where smart contracts would substitute legal agreements and courts, with property rights enforced directly on-chain.

Advertisement

That shift, however, has not materialized. Even crypto-native firms such as Dragonfly still rely on conventional legal contracts.

“When we sign a deal to invest into a startup, we don’t sign a smart contract. We sign a legal contract. The startup does the same. Neither of us are comfortable doing the deal without a legal agreement…In fact, even in the cases where we have an on-chain vesting contract, there’s usually also a legal contract in place,” he said.

According to Qureshi, the issue is not technical failure but social misalignment. Blockchain systems function as designed, yet they are not structured around human behavior and error. He also contrasted this with traditional banking, which has evolved over centuries to account for mistakes and misuse.

“The bank, terrible as it is, was designed for humans,” he added. “The banking system was specifically architected with human foibles and failure modes in mind, refined over hundreds of years. Banking is adapted to humans. Crypto is not.”

He added that long cryptographic addresses, blind signing, immutable transactions, and automated enforcement do not align with human intuition about money.

Sponsored

Advertisement

“That’s why in 2026, it’s still terrifying to blind sign a transaction, to have stale approvals, or to accidentally open up a drainer. We know we should verify the contract, double-check the domain, and scan for address spoofing. We know we should do all of it, every time. But we don’t. We’re human. And that’s the tell. It’s why crypto always felt slightly misshapen for us,” the executive remarked.

AI Agents: Crypto’s True Natives?

Qureshi suggested that AI agents may be more naturally suited to crypto’s design. He explained that AI agents do not fatigue or skip verification steps.

They can analyze contract logic, simulate edge cases, and execute transactions without emotional hesitation. While humans may prefer the legal systems, AI agents may favor the determinism of code. According to him,

“In that sense, crypto is self-contained, fully legible, and completely deterministic as system of property rights around money. It’s everything an AI agent could want from a financial system. What we as humans see as rigid footguns, AI agents see as a well-written spec…Even legally, our traditional monetary system was designed for human institutions, not AIs.”

Sponsored

Qureshi forecasted that the crypto interface of the future will be a “self-driving wallet,” entirely mediated by AI. In this model, AI agents manage financial activities on behalf of users.

Advertisement

He also suggested that autonomous agents could transact directly with each other, positioning crypto’s always-on, permissionless infrastructure as a natural foundation for a machine-to-machine economy.

“I think it’s this: crypto’s failure modes, which always made it feel broken for humans, in retrospect were never bugs. They were simply signs that we humans were the wrong users. In 10 years, we will look back at amazement that we ever subjected humans to wrestle with crypto directly,” Qureshi stressed.

Still, he cautioned that such a shift would not occur overnight. Technological systems often require complementary breakthroughs before reaching mainstream relevance.

“GPS had to wait for the smartphone. TCP/IP had to wait for the browser,” Qureshi noted. “For crypto, we might just have found it in AI agents.”

Sponsored

Recently, Bankless founder Ryan Adams also argued that crypto adoption has stalled due to poor user experience. However, he suggested that what appears to be “bad UX” for humans may actually be optimal UX for AI agents.

Advertisement

Adams predicted that billions of AI agents could eventually drive crypto markets beyond $10 trillion.

“In a year or two there’ll be billions of agents, many with wallets (then a year later they’ll be trillions). The “AiFi narrative” is underground like defi was in 2019. The dry tinder is quietly collecting but at some point it will ignite. No one is paying attention to crypto now because price is down…but i believe AI agents will scale to trillions of crypto wallets. AiFi is the next frontier of DeFi,” the post read.

The machine-native crypto thesis is powerful, but real constraints remain. AI agents may transact autonomously, yet liability still ultimately rests with humans or institutions, keeping legal systems relevant.

Deterministic smart contracts reduce ambiguity but do not eliminate exploits, governance failures, or systemic risk. Lastly, an argument could also be made that if AI becomes the primary interface, crypto may fade into backend infrastructure rather than function as a parallel financial order.

Defense Secretary Pete Hegseth forced Army Chief of Staff General Randy George into immediate retirement on Thursday — the latest in a pattern of senior military dismissals tied to a deepening conflict between Hegseth and uniformed leaders over diversity-linked promotion decisions.

Summary

Hegseth fired Gen. Randy George — the Army’s top uniformed officer — effective immediately on April 3, along with two other generals

The removal followed clashes over Hegseth’s decision to block promotions for four Army officers from a list of 29 candidates, two of them Black and two women

Gen. Christopher LaNeve, Hegseth’s former military aide, was named acting Army Chief of Staff

Pentagon spokesperson Sean Parnell confirmed George’s departure in a statement on X: “General Randy A. George will be retiring from his position as the 41st Chief of Staff of the Army effective immediately. The Department of War is grateful for General George’s decades of service to our nation. We wish him well in his retirement.”

No official reason was given. ABC News confirmed a senior Defense Department official told CBS News: “We are grateful for his service, but it was time for a leadership change in the Army.” Sources told CBS News that Hegseth wants someone in the role who will implement his and President Trump’s vision for the Army. Two other generals were also removed Thursday: General David Hodne, commander of the Army’s Transformation and Training Command, and Major General William Green Jr., the Army’s chief of chaplains.

Advertisement

What Drove It

The New York Times reported that George requested a meeting with Hegseth to discuss blocked promotions — and Hegseth refused to meet. The four officers removed from a promotion list of 29 candidates included two Black officers and two women. Nine U.S. officials familiar with the process told NBC News that Hegseth has blocked or delayed promotions for more than a dozen Black and female senior officers across all four military branches.

“If there are no open allegations or investigations, what was the reason they were removed from the list? They have all deployed and done their jobs, and all are combat-tested,” one official said.

George, a career infantry officer commissioned from West Point in 1988, served combat tours spanning Desert Storm, Iraq, and Afghanistan. Nominated to the Chief of Staff role by President Biden and confirmed in 2023, his term was expected to run through September 2027. He is the latest in a series of Joint Chiefs members removed by Hegseth, following the earlier dismissals of Joint Chiefs Chairman Gen. C.Q. Brown and Chief of Naval Operations Adm. Lisa Franchetti.

Advertisement

Pattern and Response

Democratic Senator Chris Murphy attributed the firings to the Iran conflict: “It’s likely that experienced generals are telling Hegseth his Iran war plans are unworkable, disastrous, and deadly.” The Joint Chiefs paid George a tribute: “Since 1988, General George and his family have consistently answered the nation’s call with honor and dedication.”

Military instability of this kind, during active combat, compounds the geopolitical uncertainty already affecting global markets. Analysts tracking Middle East escalation have consistently flagged its downstream effects on supply chains and financial systems. For context, Ripple’s survey data showed that 72% of financial institutions now view digital assets as essential infrastructure — a measure of how deeply integrated digital markets have become with the macro environment that geopolitical decisions like this one directly shape.

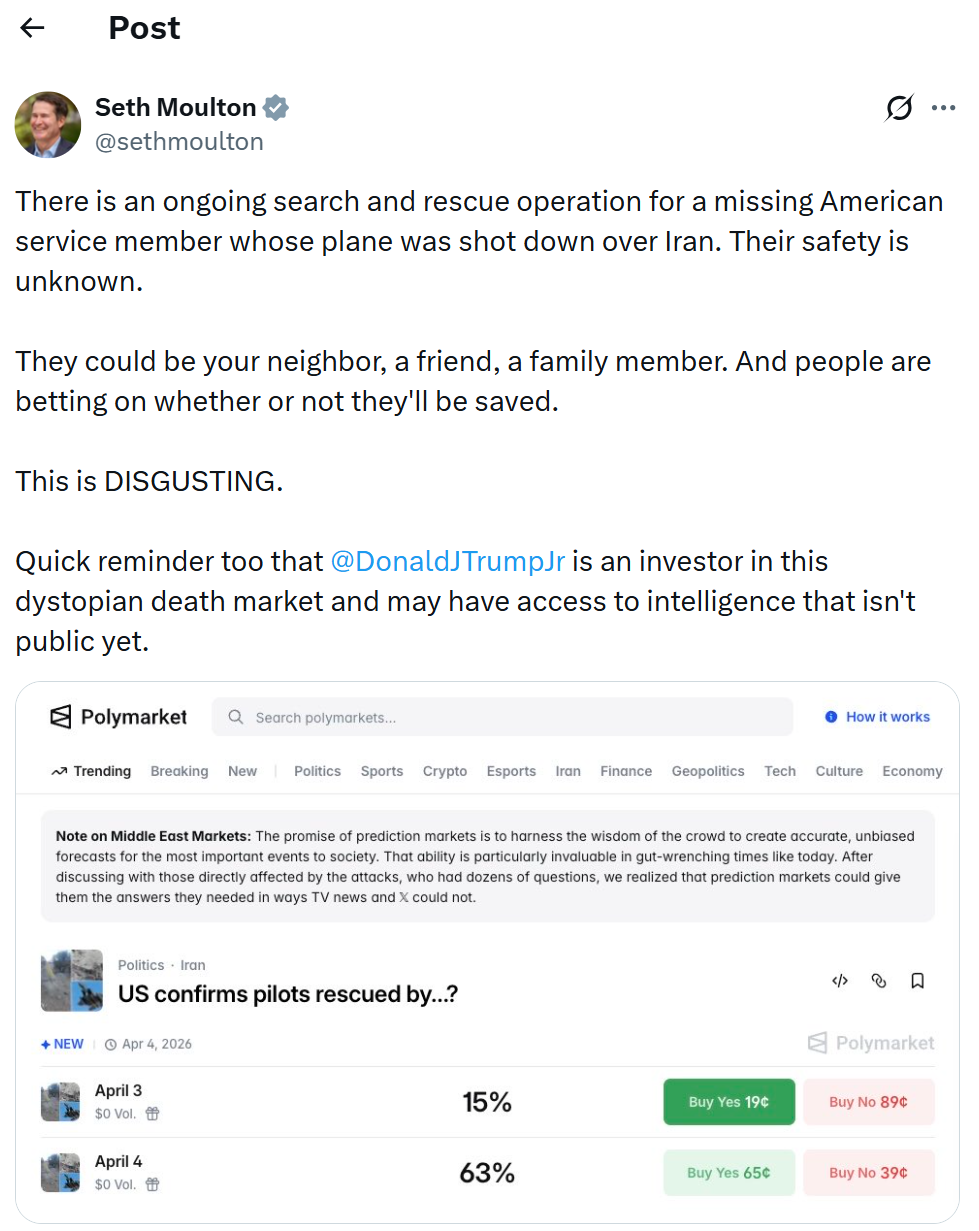

Polymarket has pulled a market tied to the fate of a missing U.S. service member after a wave of backlash, saying the listing violated its integrity standards. The decision comes amid heightened scrutiny of prediction markets that touch on real-world human outcomes and potential military actions.

The controversy centered on a prediction asking whether U.S. authorities would confirm the rescue of a pilot reportedly shot down over Iran, a topic that drew rapid and emotional reaction from users. Signals from the market suggested a majority—more than 60% of bettors—did not expect a rescue by the upcoming Saturday, highlighting how quickly sentiment can polarize around volatile, real-time events.

U.S. Representative Seth Moulton condemned the market as “disgusting,” expressing concerns about people speculating on the fate of a potentially injured service member. “They could be your neighbor, a friend, a family member. And people are betting on whether or not they’ll be saved,” he wrote, underscoring the human dimension behind the bets.

Polymarket stated that it removed the market immediately, adding that it should not have been listed and that the company is reviewing how the listing passed internal safeguards. The platform did not offer further detail about which specific rule or policy was violated.

Advertisement

Key takeaways

Polymarket deleted a market linked to the fate of a missing U.S. service member after backlash, signaling a potential tightening of internal safeguards for sensitive events.

Officials and commentators are calling for clearer governance of prediction markets that touch on human safety and military outcomes, amid questions about which rules apply to borderline cases.

Historical tensions around insider trading concerns persist in prediction markets, with recent reporting suggesting substantial profits from timing bets on geopolitical events and renewed calls from lawmakers for regulator guidance.

Polymarket’s monetization strategy, including a recent fee overhaul, has intensified scrutiny around the platform’s business model and its alignment with user interests and integrity standards.

The episode underscores the ongoing friction between innovative risk markets and ethical, regulatory, and operational safeguards—an area likely to attract regulatory attention in the near term.

Polymarket’s misstep and the boundaries of prediction markets

From the outset, the market’s subject—whether authorities would confirm the rescue of a potentially endangered service member—presses into delicate territory. Prediction markets have long drawn scrutiny when they intersect with real-world crises, where outcomes can directly affect real lives. Polymarket’s decision to remove the market suggests a recalibration of what content it deems appropriate for its platform, even as the broader market remains interested in forecasting events that straddle news cycles and human risk.

Users quickly noted the lack of clarity around policy enforcement. As coverage of the incident circulated, questions arose about which specific rule in Polymarket’s “integrity standards” had been breached. Critics argued that without transparent guidance on how safeguards are applied, users are left to guess at the boundaries between legitimate forecasting and ethically fraught betting lines. This kind of ambiguity can erate legitimate concerns about governance and user trust—issues that affect not only participants but potential partners and investors evaluating the long-term viability of decentralized or crypto-native prediction platforms.

Polymarket’s action follows a broader context of scrutiny in the sector. The platform has recently expanded its price feeds and product lines, moving into equities and commodities in collaboration with data providers, a move that coincided with a notable uptick in activity and monetization. In March, the company implemented a revamped fee structure, which Cointelegraph noted propelled daily fees well above prior levels and brought revenue into a higher profile. While monetization is essential for sustainable operation, it can also intensify incentives to broaden markets and attract trading volume, complicating the governance calculus when sensitive topics are on the table.

Insider trading concerns persist in prediction markets

Beyond governance questions, prediction markets remain under the lens for potential insider trading issues. Last month, reporting highlighted a group of traders who reportedly profited by accurately timing bets on U.S. strikes in the Middle East. The betting activity centered on the timing of events that could only be known with public or near-public information, and investigators flagged the pattern as suggestive of informational advantages being exploited through blockchain wallets created specifically to target those events. The episode underscored the tension between fast-moving information markets and safeguards against unfair advantages.

In response to those concerns, lawmakers entered the conversation. At least 42 Democratic lawmakers pressed the U.S. Commodity Futures Trading Commission (CFTC) and the Office of Government Ethics to warn federal employees against using non-public information to trade on prediction markets. The appeal reflects bipartisan interest in establishing guardrails that protect both market integrity and the broader public interest, particularly when markets touch on national security or military actions.

Advertisement

Taken together, these developments illustrate a pivot point for the sector. On the one hand, prediction markets offer a compelling lens on how information and sentiment drive consensus around uncertain events. On the other hand, the same dynamics that make these markets attractive—liquidity, rapid pricing, and the potential for swift monetization—also invite ethical and regulatory scrutiny when real-world stakes are high.

What readers should watch next

The Polymarket episode is likely to reverberate through the ecosystem as platforms reassess which markets to enable and how to articulate rules with greater precision. Investors and participants should monitor whether Polymarket, or comparable platforms, publish more granular guidance on integrity standards and incident-response processes. Regulators may also weigh in with clarifications on permissible subjects, disclosure practices, and anti-insider trading measures for decentralized or crypto-enabled markets.

As markets evolve, expect ongoing debates about balancing openness and innovation with accountability. For traders and builders, the takeaway is clear: clarity and safeguards are becoming as important as the odds themselves, and the next wave of policy and product decisions will likely shape how widely these markets are adopted in mainstream financial ecosystems.

Readers should stay tuned to see how Polymarket and peers adjust their governance models, whether new guardrails emerge from regulatory discussions, and how participants adapt their strategies in response to these evolving standards.

Advertisement

Risk & affiliate notice: Crypto assets are volatile and capital is at risk. This article may contain affiliate links. Read full disclosure

Binance ETH reserve fell to 3.3M ETH, breaking below both the February and August 2024 historical lows.

Bitcoin reserves on Binance declined from 670,000 BTC in early February to 636,000 BTC by early April 2025.

USDT reserves on Binance grew from $35 billion on March 12 to $38 billion by April 2, reflecting rising dry powder.

USDC balances climbed from $4.6 billion in February to $6.6 billion by April 2, adding to total stablecoin buying power.

Binance ETH reserve has dropped to its lowest level in over a year, falling below key historical lows. At the same time, stablecoin balances on the exchange have been rising steadily.

On-chain data from CryptoQuant shows that these two opposing trends are reshaping the exchange’s liquidity structure.

The shift points to easing sell-side pressure alongside growing buying power among traders holding dollar-denominated assets.

ETH and BTC Reserves Record Notable Declines on Binance

Binance’s Ethereum reserve has fallen to 3.3 million ETH, according to CryptoQuant analyst Amr Taha. This level sits below the February 2024 low of 3.53 million ETH and the August 29, 2024 low of 3.49 million ETH. Breaking below both historical support levels marks a clear downward trend in ETH holdings on the exchange.

Binance ETH Reserve Drops Below February 2024 Low While USDT and USDC Reserves Climb

“If this trend continues, it could create a more supportive setup for price expansion.” – By Amr Taha pic.twitter.com/aFbrLcdObH

Bitcoin reserves on Binance have also moved lower over recent weeks. The BTC balance declined from approximately 670,000 BTC in early February to 636,000 BTC by early April. That drop reflects a similar pattern of reduced crypto asset supply sitting on the exchange.

When fewer coins rest on an exchange, available sell-side supply tends to shrink. This shift often reduces the immediate pressure that sellers can place on spot prices during periods of market activity.

Rising Stablecoin Reserves Point to Growing Buying Power

As crypto reserves declined, stablecoin balances on Binance moved in the opposite direction. USDT reserves grew from $35 billion on March 12 to $38 billion by April 2. USDC reserves also climbed from $4.6 billion in February to $6.6 billion over the same period.

Advertisement

Taha noted in his analysis: “If this trend continues, it could create a more supportive setup for price expansion.” The combined growth in USDT and USDC balances reflects an accumulation of dry powder sitting ready on the exchange.

Stablecoin reserves rising while crypto reserves fall is a well-known market structure among experienced traders. It suggests that capital has rotated out of volatile assets and into dollar-pegged holdings, without leaving the exchange entirely.

Whether buyers begin deploying those stablecoin balances into spot markets remains the key variable to watch in the coming weeks.

X is preparing to automatically lock Twitter accounts that mention crypto for the first time, and the ripple effect on memecoin communities built entirely on social momentum could be severe.

X Head of Product Nikita Bier confirmed the mechanism directly: “We are in the process of implementing auto-locking + verification if a user posts about cryptocurrency for the first time in the history of their account.”

Yeah we’re aware. We are in the process of implementing auto-locking + verification if a user posts about cryptocurrency for the first time in the history of their account. This should kill 99% of the incentive, especially since Google isn’t doing shit to stop the phishing…

The trigger is first-time crypto posting, not repeat offenders. Bier’s rationale targets the 99% of phishing incentives tied to hijacked accounts promoting fraudulent tokens and fake giveaways. The move follows a wave of fake copyright violation emails stripping users of login credentials and 2FA codes.

For memecoins that depend on viral first-post discovery, new wallets, new converts, and new degens, this is a direct hit to the top of the funnel.

Advertisement

The broader market context adds pressure. X’s bot crisis, driven by AI-powered scam accounts exploiting recommendation algorithms with deepfake-heavy promotions, has already eroded trust in platform-native crypto signals.

Crypto Twitter Lock Mechanism Could Be A Good Cure For The Space

X’s verification layer filters scam noise and actually improves signal quality for legitimate crypto Twitter projects, driving renewed institutional interest and bringing back trust back to the industry. But the market might see whether the auto-lock policy reduces spam effectively or simply chills organic growth.

Advertisement

However, policy friction could also reduce crypto posting from new users by a material margin, cutting viral discovery loops that memecoins depend on.

X is about to auto-lock your account the moment you post about crypto – if it's your first time. Head of Product Nikita Bier just announced it. Hackers break into accounts and immediately start shilling random tokens. X is now looking to freeze those accounts before the damage… pic.twitter.com/IWV7ZuB4fw

Bitcoin Hyper Targets Early Infrastructure Upside as Memecoins Face Platform Risk

When social-layer memecoins face existential platform risk, capital has historically rotated toward projects with utility that doesn’t depend on viral posting cycles. That rotation is already showing up in presale momentum, and it’s worth watching where that money is going.

Bitcoin Hyper ($HYPER) is positioning directly in that gap. The project claims the title of the first-ever Bitcoin Layer 2 with Solana Virtual Machine (SVM) integration, delivering a faster performance than Solana through extremely low-latency processing, a Decentralized Canonical Bridge for BTC transfers, and high-speed smart contract execution.

Bitcoin has core limitations of slow transactions, high fees, and near-zero programmability, and Hyper is here to fix them. Hard numbers back the early traction, $32 million raised at a current price of $0.013678, with staking at a high 36% APY for early participants. Presale capital has been flowing toward infrastructure plays as memecoin sentiment cools.

Two U.S. military aircraft were shot down in separate incidents during combat operations over Iran on April 3 — an F-15E Strike Eagle and an A-10 Thunderbolt II — with a search-and-rescue operation still ongoing for one missing crew member as Operation Epic Fury approaches its sixth week.

Summary

Iran shot down a U.S. F-15E Strike Eagle on April 3; one of the two crew members was rescued, the other remains unaccounted for

An A-10 Thunderbolt II dispatched during the rescue effort was also struck by Iranian fire; the pilot ejected and was subsequently recovered

The incidents directly contradict recent U.S. government claims of complete air dominance over Iran, complicating the administration’s public messaging on the war’s progress

U.S. officials confirmed to CBS News that the F-15E Strike Eagle — a two-seat aircraft flown by a pilot and a weapons systems officer — was shot down by Iranian forces. One crew member was rescued by U.S. forces following a combat search-and-rescue mission. The second crew member, a weapons systems officer, remains missing. Images verified by CNN showed low-flying rescue aircraft conducting operations over Khuzestan Province in central Iran.

A rescue helicopter that extracted the surviving pilot was hit by small arms fire during the operation, wounding crew members on board before landing safely. An A-10 Warthog dispatched as part of the search effort was then struck by Iranian fire, forcing its pilot to eject over the Persian Gulf before recovery.

Advertisement

Iran’s state media posted claims of downing the aircraft and announced a reward for the capture of any “enemy pilot or pilots.” Iran’s Parliament Speaker Mohammad Bagher Ghalibaf mocked the U.S. search effort publicly on X.

A Direct Contradiction

The downing conflicts with statements from President Trump, who said in a prime-time address two days earlier: “They have no anti-aircraft equipment. Their radar is 100% annihilated. We are unstoppable as a military force.” Defense Secretary Pete Hegseth and other officials have repeatedly asserted U.S. air dominance over Iran.

According to Axios, three F-15Es had previously been lost to friendly fire during the conflict. The war has now claimed 13 American lives and wounded 365 service members. Israel separately suspended airstrikes in areas relevant to the ongoing U.S. rescue effort, according to an Israeli official speaking anonymously to the Associated Press.

Advertisement

Economic Pressure

Iran’s response has escalated alongside the aircraft losses. Tehran has imposed what amounts to a toll system on the Strait of Hormuz, a waterway through which approximately 20% of globally traded oil transits. Missile and drone attacks struck oil, gas, and desalination facilities across the Persian Gulf on Friday. The Federal Reserve Bank of Chicago’s Austan Goolsbee told CBS News that the Iran war risks fueling inflation in a way that could prevent the Fed from cutting rates in 2026.

As analysts warned months ago, Middle East escalation carries supply chain and inflationary consequences that reverberate across all risk assets. Institutional capital flows have already shifted in response to the conflict’s progression, with large asset managers repositioning across both traditional and digital markets as geopolitical uncertainty deepens.

Leap Wallet will shut down its products by May 28, ending a crypto wallet project that began in the Terra ecosystem and later expanded to Cosmos and other chains.

Summary

Leap Wallet will shut down its apps, web platform, exchange tool, and validator service by May 28.

Users can still access assets through another wallet using their recovery phrase or private key.

Leap began in Terra and expanded into Cosmos after the 2022 collapse changed its path.

The closure affects its browser extension, mobile apps, web app, exchange tool, and validator service.

Leap said on Friday that it plans to sunset its software suite by May 28. The shutdown covers its browser extension, iOS and Android apps, Leap WebApp, Swapfast exchange platform, and Leap Cosmos Hub Validator.

Advertisement

The team said the decision came after building across multiple networks since 2022. In a post on X, it said, “We started Leap in 2022 to redefine what wallet experiences in crypto mean.” It added that the project later grew across “100+ chains.”

Leap also said the move was difficult for the team. It stated, “This decision was not made lightly,” while adding that it still believes in the long-term future of crypto and the interchain ecosystem.

Leap said noncustodial users will still be able to access their assets after the shutdown. The team explained that users can restore the same wallet address through another wallet by using a recovery phrase or private key.

Advertisement

The FAQ said there is no need to move assets to a new address. It explained, “There is no need to withdraw or send your assets to a new address,” because importing the recovery phrase or private key will restore access to the same address.

The team also issued a separate notice for Cosmos users who delegated ATOM to Leap’s validator. It asked them to redelegate to another validator if they want to keep earning staking rewards.

Project began in Terra ecosystem

Leap launched in late 2021 with a $50,000 grant from Terraform Labs, the now-defunct firm behind TerraUSD. In early 2022, the project raised a $3.2 million seed round co-led by CoinFund and Pantera Capital.

At the start, Leap positioned itself as a wallet focused on Terra, with tools for staking LUNA, trading, and connecting with applications such as Anchor and Mirror. It aimed to offer a wallet experience similar to what MetaMask built for Ethereum and Phantom built for Solana.

Advertisement

After the collapse of Terra in 2022, Leap shifted its focus and expanded into the wider Cosmos ecosystem. That move allowed the project to continue as a multi-chain wallet after its original market changed.

The shutdown now closes that chapter for the wallet. While the apps and related services will go offline, users will still retain control of their assets through standard wallet recovery tools supported by other providers.

Leap Wallet will sunset all products, including extensions and mobile apps, on May 28, 2026, across iOS and Android.

Users can migrate safely using their recovery phrase, as Leap is non-custodial and assets remain on the blockchain at all times.

ATOM delegators staking with Leap’s Cosmos Hub validator must redelegate early due to network unbonding period delays.

After the May 28 deadline, all installed Leap apps will stop functioning, though fund recovery via recovery phrase remains fully possible.

Leap Wallet has officially announced that it will discontinue all its products on May 28, 2026. The crypto wallet provider has been active since 2022, serving users across more than 100 blockchain networks.

The shutdown covers extensions, mobile apps, and several associated services. Users are advised to begin migrating their assets to other supported wallets ahead of the deadline.

All core wallet functions will remain available until that date to allow a smooth transition.

Products Scheduled for Discontinuation After the May Deadline

The shutdown affects a broad range of products tied to the Leap ecosystem. These include Leap Wallet browser extensions and mobile versions on iOS and Android.

Compass Wallet, the Leap WebApp, and the Swapfast service are also on the list. Leap Cosmos Hub Validator and Leap Cosmos Snaps will be discontinued as well.

Advertisement

The team behind Leap shared the news through an official tweet. They noted the wallet was launched to change what crypto wallet experiences could offer users.

Since launch, it expanded to support over 100 chains across multiple ecosystems. The post also reflected the care and responsibility the team felt toward its user base.

In the announcement tweet, the team wrote that the decision to shut down was not made lightly. They added that they continue to believe in the long-term future of the crypto space.

Leap Wallet: Sunset Notice

After careful consideration, we’ve made the decision to sunset Leap Wallet and its associated products.

Advertisement

The products will be sunset on 28th May, 2026, and all users should complete their migration before then.

We started Leap in 2022 to redefine what…

— Leap Wallet | Sunset on 28th May (@leap_wallet) April 2, 2026

They also extended appreciation to partners and users who supported the product over the years. The message was direct, measured, and absent of any bitterness or blame.

Advertisement

Until May 28, 2026, all listed products will retain their existing core functionality. Users can still view balances, send tokens, and manage their staking positions.

Exporting recovery phrases and private keys will also remain available throughout this period. No core feature will be removed before the official sunset date arrives.

What Users Must Do Before the Shutdown Date

Users holding assets in Leap Wallet are encouraged to move to another wallet provider. The team recommended Keplr, MetaMask, Phantom, and Rabby as compatible alternatives.

Since Leap is a non-custodial wallet, assets are held on the blockchain and not within the app. This means migration does not require any complex transfer of funds between addresses.

Advertisement

Any user with a recovery phrase can import it directly into another supported wallet. That process will restore all addresses and balances automatically across compatible chains.

No manual transfers are necessary for this to work correctly. Starting early reduces the risk of delays or missed steps before the deadline.

Those who delegated ATOM to Leap’s Cosmos Hub validator must also take a separate action. They need to redelegate to another validator to keep earning staking rewards.

Network unbonding periods can stretch over several days, so acting promptly matters. A detailed migration guide with full instructions is available at leapwallet.io.

Advertisement

After May 28, 2026, all Leap products will stop functioning, including already-installed apps. Users who miss the deadline can still recover their funds using their recovery phrase.

Importing it into any compatible wallet will restore full access to holdings. Migration support remains available at support@leapwallet.io until the shutdown date.

Polymarket removed a market tied to the fate of a missing US service member after mounting backlash, saying the listing violated its “integrity standards.”

The controversy erupted after a prediction market appeared asking whether US authorities would confirm the rescue of a pilot reportedly shot down over Iran, with most users (over 60%) betting that they wouldn’t be rescued until Saturday.

US Representative Seth Moulton condemned the market, calling it “disgusting” and expressing concerns over people speculating on the fate of a potentially injured service member. “They could be your neighbor, a friend, a family member. And people are betting on whether or not they’ll be saved,” Moulton wrote.

Representative criticizes Polymarket market. Source: Seth Moulton

In response, Polymarket said it had taken the market down immediately, adding that it should not have been listed and that the company is reviewing how it passed internal safeguards. The platform did not provide further detail on what specific rule had been breached.

While Polymarket said it took the market down because it did not meet its integrity standards, the platform did not specify which rule had been violated, prompting further scrutiny from users.

“I’m looking at the “Market Integrity” page, and I checked the TOS, and I don’t see which prohibition is relevant here,” Jack Newsham, a correspondent on Business Insider’s national desk, wrote on X.

As Cointelegraph reported, Polymarket has seen a sharp rise in fees and revenue after expanding its fee model on March 30, with daily fees jumping from about $363,000 to over $1 million and revenue nearing $1 million at its peak. The increase follows broader taker fees across categories like finance, politics and tech, as the platform ramps up monetization.

Insider trading concerns rise on prediction markets

There have also been growing concerns about insider trading on prediction markets. Last month, it was reported that a group of traders made about $1 million by correctly betting on the timing of US strikes on Iran, with some placing trades just hours before the attacks. The activity, which involved newly created wallets focused almost entirely on strike-related bets, raised insider trading suspicions.

To address these concerns, at least 42 Democratic lawmakers have urged the US Commodity Futures Trading Commission and the Office of Government Ethics to warn federal employees against using non-public information to trade on prediction markets.

Cointelegraph is committed to independent, transparent journalism. This news article is produced in accordance with Cointelegraph’s Editorial Policy and aims to provide accurate and timely information. Readers are encouraged to verify information independently. Read our Editorial Policy https://cointelegraph.com/editorial-policy

Brian Armstrong has put himself personally on the line for Bitcoin quantum resistance, pledging direct oversight of Coinbase’s post-quantum cryptography research and implementation efforts at a moment when the threat has moved from theoretical to time-stamped.

The commitment signals that Coinbase is no longer treating quantum risk as a long-range problem for someone else’s roadmap.

Going to start spending time on this personally – seems like we all need to solve it sooner rather than later. https://t.co/qLUE6TCPL5

The urgency is not manufactured. Google Quantum AI and Caltech research published in late 2025 modeled a hypothetical advanced quantum computer cracking Bitcoin’s encryption in under nine minutes – barely inside the network’s 10-minute block confirmation window.

Advertisement

Armstrong’s personal involvement is a direct institutional response to that narrowing margin.

Key Takeaways:

Armstrong’s Commitment: Coinbase CEO Brian Armstrong has pledged personal oversight of the exchange’s Bitcoin quantum resistance initiatives, including collaboration with Bitcoin Core developers through a newly formed Quantum Advisory Council.

The Threat Window: Google Quantum AI research models a cryptographically relevant quantum computer breaking Bitcoin’s encryption in under nine minutes – inside the 10-minute block time – with Google targeting quantum readiness by 2029.

Protocol Reality: Bitcoin’s decentralized governance requires community consensus via the BIP process for any cryptographic upgrade – making Coinbase’s developer-facing engagement more consequential than a unilateral exchange decision.

Industry Alignment: MicroStrategy’s Michael Saylor and Coinbase CSO Philip Martin are actively contributing to quantum resistance efforts; BTQ Technologies deployed a quantum-resistant Bitcoin Core testnet in early 2026, with mainnet planned for Q2 2026.

What to Watch: BTQ Technologies’ Q2 2026 mainnet launch and the Coinbase Quantum Advisory Council’s first published migration standards are the two near-term signals that will indicate whether institutional momentum is translating into protocol-level action.

The Quantum Threat to Bitcoin Is Specific – and the Clock Is Running

Bitcoin’s cryptographic security rests on the elliptic curve discrete logarithm problem. Google’s quantum research has already prompted other blockchain ecosystems to accelerate post-quantum cryptography transitions, and Bitcoin – the most valuable target – faces the sharpest exposure.

Advertisement

The specific mechanism is Shor’s Algorithm: run on a sufficiently powerful quantum computer, it can derive a private key from an exposed public key, which is precisely what happens when a Bitcoin address transacts on-chain.

Many are wondering "what Google saw" that caused them to revise their post-quantum cryptography transition deadline to 2029 last week. It was this: https://t.co/dQtmTK9pdz

Older Pay-to-Public-Key-Hash addresses are most exposed. SegWit and Taproot addresses offer partial cover – the public key isn’t broadcast until spending – but that protection evaporates the moment funds move. NIST finalized its first post-quantum cryptography standards in 2024, establishing lattice-based and hash-based signature schemes as the baseline framework. Bitcoin has not adopted any of them yet.

That gap – between available cryptographic tools and Bitcoin’s actual protocol, is the structural problem Armstrong is positioning Coinbase to help close.

What Armstrong’s Personal Oversight Actually Means – and Why Coinbase’s Institutional Weight Changes the Calculation

Armstrong’s commitment is not a press release pledge. According to reporting on the initiative, Coinbase has established a Quantum Advisory Council that includes Bitcoin Core developers, with the explicit mandate to develop migration standards before cryptographically relevant quantum computers arrive.

Coinbase CSO Philip Martin described the situation as an “urgent problem” requiring industry consensus – and noted that post-quantum cryptography exists, but Bitcoin lags other chains in adopting it.

Advertisement

The latest quantum papers from Google and Caltech are an important signal for the industry. Timelines are still debated, but the time to act is now. The good news: post-quantum cryptography exists. This is a solvable problem, and many chains already have roadmaps. Bitcoin needs…

That distinction matters. This is not Coinbase upgrading its own infrastructure in isolation – a task any well-resourced exchange could accomplish internally.

The Advisory Council structure is designed to feed into the Bitcoin Improvement Proposal process, the community-consensus mechanism through which any protocol-level cryptographic change must pass. Coinbase, through its engineering resources and developer relationships, is positioning itself to draft and test BIPs specifically aimed at post-quantum transitions.

The institutional logic is transparent – and legitimate. Sovereign wealth funds and ultra-long-horizon institutional allocators weigh generational risk differently than retail traders.

Advertisement

Investor Kevin O’Leary has explicitly flagged quantum uncertainty as a factor that could deter institutional Bitcoin allocations.

By addressing a 10-to-20-year risk today, Coinbase is signaling custodial seriousness to exactly the capital it wants to attract. Coinbase’s recent regulatory positioning follows the same pattern: institutional-grade engagement on foundational issues before the pressure becomes acute.

JUST IN: Kevin O’Leary aka Mr. Wonderful says that institutions do not want to own more than 3% of Bitcoin in their portfolios because of the risk of quantum computing. pic.twitter.com/xJYLZlCvvb

MicroStrategy’s Michael Saylor is contributing to quantum resistance efforts alongside Armstrong – which adds significant Bitcoin treasury credibility to what might otherwise read as an exchange-driven initiative.

Advertisement

Jameson Lopp of Casa, who has tracked this risk closely, has estimated that full network migration to quantum-safe addresses will require years of coordination across wallets, custodians, and users. Armstrong’s involvement compresses none of that timeline on its own.

What it does is add institutional momentum to a process that previously lacked it.

Cambodia’s parliament passed its first cybercrime law on April 3, 2026, targeting online scam centres directly.

Convictions carry prison terms of up to 10 years and fines reaching $250,000 for gang-related scam operations.

Cambodia extradited two high-profile figures to China amid a broader crackdown on senior scam network leaders.

Britain sanctioned Cambodia’s largest fraud complex and a crypto marketplace used to trade stolen personal data.

Cambodia’s cybercrime law marks a turning point in the country’s fight against online fraud operations. The parliament passed the legislation on Friday, April 3, 2026, making it the first law specifically targeting scam centres.

These centres have cost international victims billions of dollars. The move follows growing global pressure on Southeast Asian governments to act against the illicit operations embedded across the region.

Parliament Approves Strict Penalties for Online Scam Operators

The new law sets out prison terms of two to five years for those convicted of online scams. Fines can reach up to $125,000 for individual offenders.

Gang-related scams or cases involving multiple victims carry heavier sentences of up to 10 years. Fines in such cases can go as high as $250,000.

Justice Minister Keut Rith described the law as a tool to strengthen ongoing enforcement efforts. He stated the law aimed to enhance the “cleaning operation” taking place across the country.

Advertisement

He also stressed that it would ensure the centres do not return after the crackdown. The law will proceed to Cambodia’s king for final signature before taking full effect.

Rith further explained the reach of the problem during his remarks to reporters. He said the issue had also affected the economy, tourism, and investment in Cambodia.

He described the law as being “strict like the fishing net, strict to ensure we don’t have the online scams anymore in Cambodia.” Those words captured the government’s stated intent to pursue a thorough and lasting enforcement effort.

The law also covers penalties for money laundering, data collection on victims, and scammer recruitment. Previously, Cambodia had no dedicated legislation for targeting scam operations.

Advertisement

Authorities had relied on charges such as aggravated fraud and recruitment for exploitation. This new legislation addresses that legal gap directly.

Recent Arrests and Extraditions Signal Broader Crackdown

Cambodia’s enforcement actions have extended beyond legislation in recent months. On Wednesday, the government extradited Li Xiong to China.

Li Xiong was a former leader at a Cambodian financial conglomerate accused of laundering money for criminal organisations. The extradition reflects a shift toward holding senior figures accountable.

In January, Chinese-Cambodian businessman Chen Zhi was arrested in Cambodia and also extradited to China. Chen Zhi faced accusations of running a brutal online scam and money laundering operation.

Advertisement

His arrest marked a dramatic reversal for a once-prominent business figure. The case drew international attention to Cambodia’s ties with transnational crime networks.

On Thursday, Britain sanctioned operators of what it described as Cambodia’s largest fraud complex. The UK also targeted a crypto marketplace used to trade stolen personal data.

Britain called it part of a fast-growing network of scam centres across Southeast Asia. Workers in these compounds are reportedly confined and forced to commit fraud.

Cambodian officials say the current campaign is broader than previous efforts. Hundreds of sites are being closed, and senior figures are being detained.

Advertisement

The government had long played down the existence of these compounds. That position has now clearly changed.

NewsBeat2 days ago

NewsBeat2 days ago

Business1 day ago

Business1 day ago

Fashion16 hours ago

Fashion16 hours ago

Crypto World3 days ago

Crypto World3 days ago

Tech5 days ago

Tech5 days ago

Tech5 days ago

Tech5 days ago

Tech4 days ago

Tech4 days ago

Sports4 days ago

Sports4 days ago

Business2 days ago

Business2 days ago

Fashion6 days ago

Fashion6 days ago

Tech6 days ago

Tech6 days ago

Tech4 days ago

Tech4 days ago

Fashion5 days ago

Fashion5 days ago

Politics5 days ago

Politics5 days ago

Crypto World4 days ago

Crypto World4 days ago

Tech5 days ago

Tech5 days ago

Tech4 days ago

Tech4 days ago

You must be logged in to post a comment Login