Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Large UK brands have been told they will need to rein in “aggressive” intellectual property claims after the country’s highest court found that media company Sky acted in “bad faith” by registering trademarks for a wide range of products it did not intend to sell.

In a highly anticipated ruling on a case dating back eight years, the Supreme Court on Wednesday said some trademarks registered by Sky, which claimed intellectual property rights for goods including antiperspirants, tuxedos and biofuels, were so broad as to be unenforceable.

Advertisement

Lawyers said the judgment, which overturned an earlier decision from the Court of Appeal, could make it harder for companies wanting to prevent others in different industries from using their brand names and logos.

Geoff Steward, partner at Addleshaw Goddard, said the ruling would require a “radical rethink” among brand owners who had long sought “the widest possible intellectual property protection”.

“Gone are the days of overreaching to gain wider trademark monopolies,” he said.

Peter Vaughan, chartered trademark attorney and associate professor at Nottingham Law School, described the ruling as “a victory for David over Goliath in many ways”.

Advertisement

“Some of the more aggressive [trademark] enforcement strategies of major brands are likely to have to stop to some degree,” he said.

Sky brought a High Court claim against US tech company SkyKick in 2016, alleging that it had infringed five of its trademarks. But the Seattle-based company challenged the validity of Sky’s trademarks, which covered products including shampoo, carbon monoxide detectors and slippers as well as the goods and services for which it is better known.

The High Court, in a series of judgments, found that Sky had to an extent applied for trademarks in “bad faith”, as they covered such a broad range of goods and services that the company could not have intended to use them all.

The case went to the Court of Appeal, which found in Sky’s favour in 2021. But in an unanimous judgment on Wednesday, the five Supreme Court judges found the “Court of Appeal was wrong to reverse” the initial finding.

Advertisement

The High Court had been “entitled to find that the Sky marks were applied for in bad faith to the extent that it did”, they found.

In an unusual move, the Supreme Court went ahead with its judgment even though Sky and SkyKick settled their dispute — which had been narrowed to a smaller number of goods and services — in September.

SkyKick said it had decided to rebrand following its acquisition by ConnectWise and that both it and Sky “determined that their respective interests would be best served by concluding these long running disputes.”

Sky said in a statement: “Sky, like many other businesses, historically filed a range of trade marks in accordance with relevant guidance available at the time.”

Advertisement

The Supreme Court judgment “concludes a lengthy legal process to clarify the correct application of the law. We acknowledge this clarification and will follow this moving forward.”

Kerry Russell, intellectual property expert at law firm Shakespeare Martineau, said the decision had “sent shockwaves throughout trademark law”.

Companies would need to “give careful consideration” about whether the types of products for which they file trademark applications “are really likely to be used by them” in the near future.

If offered a free trip into space, Samantha Harvey says she would like to be “brave enough” to say yes — but then adds that in truth she’d probably be too scared to go.

The question is not as random as it may seem: 49-year-old Harvey has just won the prestigious Booker Prize for fiction for her novel Orbital, a story set aboard the International Space Station as it circles the Earth, unfurling along the way observations and meditations about the “suspended jewel” below and the preoccupations of the six humans on board “up there”.

Whatever her own trepidations about taking to the heavens, Harvey’s finely executed imagination of the reality of life suspended in low Earth orbit was found by the Booker judges to be “extraordinary” and “beautiful”.

The book, which came out a year ago, has already proven a hit with readers. The £50,000 award is set to spur sales further. Harvey, who was longlisted for the prize 15 years ago for her novel The Wilderness, is the first British author to win the Booker since 2020 and the first woman since 2019.

Advertisement

“I can’t even begin to process it. It’s just beyond anything that I hoped or imagined,” she says in quiet, precise tones when we meet the next morning. On the table between us stands “Iris”, the gilded Booker Prize trophy, surrounded by a generously filled bowl of fruit, a largely exhausted cafetière of coffee and bags of untouched pastries. “I’m utterly overwhelmed by it,” she adds.

The International Space Station is ‘a symbol of an era that I think is passing, or has already passed, one of post-cold war reconciliation and hope’

In truth, Harvey says, the book is “more about Earth than about space”. She wanted to write something that felt “vaguely pastoral”, to find a way of writing about the Earth and its natural environment that captured a “feeling of connection but also a feeling of sorrow towards what we are doing to it”.

For that she needed an angle, which is what took her to space and the ISS. While she’s no “space nerd” — Harvey’s previous books have roamed very much in earthly terrain, from the impact of Alzheimer’s, filial duty, insomnia and the searing consequences of a love triangle — she says that she has always been interested in the perspective on Earth that space offers.

The ISS proved a perfect observation deck. Her fictional version of the space station is populated with its six humans — four men, two women; four western and Japanese astronauts, two Russian cosmonauts — who circle our planet, observing the “magnificent seemingly unbreakable majesty of the natural environment that is the planet Earth and also the enormous human impact we are having on it”. The book — at 136 pages, it is second-shortest to ever win the Booker — tracks them, and our planet, through a “normal” 24-hour day, which in the world of the ISS involves 16 orbits of Earth with 16 sunrises and 16 sunsets.

Advertisement

Threaded through the novel is a gathering typhoon whose progress towards its ultimate devastating impact in south-east Asia is observed in beguiling prose. “It’s the plot,” says Harvey almost teasingly, addressing one of the observations about Orbital that the story does not follow a narrative form or contain the conflict central in much conventional storytelling.

To imagine all this required deep dives into the Nasa and European Space Agency archives, and many hours on the ISS live feed. It helped that she worked on the book through lockdown. (Tellingly “almost nothing” of the Russian space programme is accessible.) “I love research,” says Harvey. “It opens a creative door.” Do enough research and you get the point “to feel confident enough to make things up”.

The result is a startling and acutely presented contrast between the cosmic and the quotidian. There are beautiful descriptive passages of the world below, looping weather systems, continents blurring — “Asia come and gone” — as the space station whizzes along at 17,500mph. The creation of our galaxy — “some cosmic clumping thumping clashing banging Wild West Shoot-out of rock and gas”— is given lyrical treatment. Meanwhile, up there are the daily routines and realities — bland dinners, uncleared dishes, recycled urine and everything velcroed into place — and thoughts about “home”.

Space is “the one remaining wilderness”, says Harvey. And yet few novelists engage with it, leaving it more to the writers of sci-fi or memoir-penning astronauts. She believes that space offers “a really strange place in the human psyche”, caught between the now “humdrum” of routine missions and rocket launches, and the “mythical” that lends itself to sci-fi. Yet we fail to grasp the reality that space has been a natural lived environment for humans for the last quarter of a century on the ISS.

The space station, which was launched in 1998, is one of the few places where Russia and the west are co-operating in a meaningful way. “It’s a symbol of an era that I think is passing, or maybe has already passed, one of post-cold war reconciliation and hope,” says. In Orbital she writes about the growing cracks in the shell of the ageing ISS. Meanwhile, Moscow has previously threatened to quit the project.

Advertisement

Harvey adds that the ISS also belongs to a passing era in human exploration of space, where the next phases will be about establishing a staging post on the Moon to support future missions to Mars. That will involve a shift away from a focus on “our planet”, circling and looking down on Earth, to looking “out”. As such, Harvey sees the ISS freighted with a deep sense of nostalgia.

The next chapter in space exploration is also set to have new authors. While the likes of Elon Musk and Jeff Bezos find no place in Orbital, there is a telling line when one of the characters ponders a media inquiry about “how we are writing the future of humanity”. The answer: “With the gilded pens of billionaires, I guess.”

Harvey worries about the shift to discovery driven by wealthy individuals rather than states. “I think we have an opportunity with space exploration to do things radically differently and we are not taking that opportunity. We are just repeating the same paradigm,” she says. “It is exploitative, the new frontier: whoever gets there first claims it.”

Meanwhile, “we are filling up low Earth orbit with junk that we have no way of disposing of. We’ve entirely trashed the field of space around our planet.”

As for her own life beyond Orbital, Harvey is just getting to grips with the relentless promotional schedule that awaits all Booker winners. Somewhat wistfully, she says that there is a love story of sorts that she began working on a while back and is “still taking shape in her mind” and that she is “desperate” to get back to writing.

“I feel that I can access a room in myself through writing that I cannot access in any other way,” she says. “And I kind of need to go back to that room quite often. At the same time, it’s the Booker Prize!”

Orbital by Samantha Harvey, Jonathan Cape £14.99, 136 pages

Advertisement

Frederick Studemann is the FT’s literary editor

Join our online book group on Facebook at FT Books Café and subscribe to our podcast Life & Art wherever you listen

THE government is set to announce huge plans to create “pension megafunds” in a bid to boost both savers’ retirement pots and investment in the UK.

Chancellor Rachel Reeves will outline the plans to move around £800billion of pension savings into larger so-called “megafunds” in her first annual “Mansion House” speech this evening.

1

Ms Reeves is hoping the cash will be used to invest in infrastructure

Local government pension schemes, which manage around £400billion of that cash, will be forced to split into eight megafunds.

Advertisement

Eventually, the plan is to then group all other defined contribution (DC) schemes – what most workers save into – into a number of other big funds.

DC schemes are where you and your employer both put money into a scheme and the cash is invested to grow your pot over time.

The plan is to set a minimum amount these funds can have in them – currently touted as somewhere between £25billion and £50billion.

The government is also consulting on allowing fund managers – who manage where all this cash is invested – to move savers from schemes which are under-performing into schemes that will deliver them better value.

Advertisement

The megafund set-up is similar to the pension systems in other countries like Australia and Canada, where pension cash is pooled into huge so-called “superfunds” and invested on behalf of larger groups of savers.

Ms Reeves said the reforms are the biggest change to the pensions market “in decades” that will “boost people’s savings in retirement” and “drive economic growth”.

The government added: “Consolidating the assets into a handful of megafunds run by professional fund managers will allow them to invest more in assets like infrastructure, supporting economic growth and local investment.”

What do the changes mean for your money?

Currently, most workers in the UK are automatically enrolled into their workplace pension scheme.

Advertisement

These are usually DC schemes. The other type of pensions in the UK are “defined benefit” schemes, where workers receive a guaranteed income in retirement based on their years of service.

But “megafunds” will pool a number of workplace pension schemes together to create giant pots of money to invest.

The aim is that by having much larger amounts to invest, the cash returns on those investments will be far higher than having lots of smaller pots.

For example, if you returned 5% on £1,000 in a year, you would earn £50, but if you returned 5% on £100,000 over a year, you would earn £5,000, and so on.

Advertisement

This should mean savers should end up with much larger pots of money by the time they retire.

Having more cash also means investment managers can take more risk with their investments with the aim of achieving higher returns.

Looking at the bigger picture, the government is hoping that these larger pension funds can be used to invest in infrastructure projects, which will ultimately benefit everyone.

Currently, most DC pensions in the UK are too small to invest in any meaningful capacity in infrastructure projects, such as roads, railways or building developments.

Advertisement

But government analysis has found pension funds worth between £25billion and £50billion can achieve much greater “productive investment levels”.

For example, it found Canada’s pension schemes invest around four times more in infrastructure than the UK currently does, while Australia’s pension schemes invest around three times more.

By combining UK schemes, the government estimates it could unlock a whopping £80billion to invest in the country’s infrastructure.

Jon Greer, head of retirement policy at wealth manager Quilter, said that by pooling resources into larger funds, savers will access “high-yield investments that smaller schemes often miss”.

Advertisement

“Drawing inspiration from successful models in Australia and Canada, this approach has the potential to deliver stable returns while supporting meaningful long-term projects,” he added.

However, some pensions industry experts have expressed concern that the government’s main focus is on investing in the UK rather than achieving returns for savers.

Tom Selby, director of public policy at AJ Bell, warned: “Conflating a government goal of driving investment in the UK and people’s retirement outcomes brings a danger because the risks are all taken with members’ money.

“If it goes well, everyone can celebrate – but it’s clearly possible that it will go the other way, so there needs to be some caution in this push to use other people’s money to drive economic growth.”

Advertisement

How do pensions make money?

DEFINED contribution pension cash is pooled together to make money for savers.

Schemes are managed by investment firms, such as Hargreaves Lansdown or Fidelity, and fund managers at those firms decide where to invest savers’ cash to earn as much money as possible.

Over a long period, these returns from investments gradually increase the size of the pot – and as the pot size increases, the amount it can return also increases, as the return is calculated on a larger amount of money.

Advertisement

This is known as “compound interest”.

We have previously revealed how over 40 years, you could save a total of £109,671, while only paying in £40,000 of your own money because of compound interest.

The larger the amount of money is that’s invested, the higher the returns can be in cash-terms for savers.

The past doesn’t predict the future. But if a company has been paying dividends for a long time, that can give investors confidence in its ability to continue doing so. It demonstrates that the company can weather a lot of adversity and innovate and launch new products to meet changing demand. Those are key characteristics investors will want to see when considering long-term investments.

Three stocks that have not only been around for a century but have also been paying dividends for that long are Coca-Cola (NYSE: KO), Eli Lilly (NYSE: LLY), and Abbott Laboratories (NYSE: ABT). Here’s why these can be some of the safest stocks you can add to your portfolio today.

Start Your Mornings Smarter! Wake up with Breakfast news in your inbox every market day. Sign Up For Free »

Coca-Cola has an iconic brand that’s known all around the world. It’s a top Warren Buffett holding, and a big reason for that is its strong brand power. Its products are found in millions of households, across hundreds of countries. While the company is known for its Coke products, it has evolved over the years and now has more than 200 brands, branching out beyond just soft drinks and into coffee, tea, and water.

Advertisement

The company has created no-sugar products to meet changing customer demand, and it has also expanded via acquisitions. Coca-Cola may not be the growth machine it once was, but it’s still a reliable business to invest in. It has generated $10.4 billion in profit over the past four quarters on sales of $46.4 billion, for a profit margin of 22%.

Coca-Cola has paid a dividend going back to 1893. Today, it’s part of an exclusive club of Dividend Kings, which have increased their dividend payments for more than 50 straight years. Its dividend yields 3%, and if your priority is to generate a safe and recurring dividend, Coca-Cola may be an ideal stock to put into your portfolio right now.

Eli Lilly is a hot growth stock to buy, as investors are bullish on its prospects in the weight loss market. The company has an incredibly promising product in tirzepatide, which regulators have approved for diabetes treatment (Mounjaro) and weight loss (Zepbound). At its peak, tirzepatide may be the best-selling drug ever, with some analysts projecting that its annual revenue will eventually top more than $50 billion.

To put into perspective just how massive that is, consider that Eli Lilly generated $34 billion in sales last year — from all of its products. With so much excitement surrounding Eli Lilly’s potential, it’s little wonder that the healthcare stock has risen by more than 200% in just the past three years.

Advertisement

But that’s just part of the equation for investors, as Eli Lilly is also a fantastic dividend stock to own. It has been making dividend payments to its shareholders since 1885. While the stock’s yield looks unimpressive at just 0.6%, it would have been even lower if not for its generous increases in recent years — the company has doubled its dividend since 2019. In November 2021, the stock was trading at around $250. At that price point, the current dividend would yield 2.1% and be higher than the S&P 500 average of 1.2%. However, investors would probably much rather have the stock’s incredible gains over the past few years instead.

Given Eli Lilly’s fantastic growth prospects plus its growing dividend, this is another great income stock you can buy and hold for years.

Rounding out this list of top income stocks is Abbott Laboratories. What’s great about this stock is the diversity that it offers investors. Abbott is a testing company, a pharma business, and a medical device maker, all rolled into one. It also generates a significant portion of its revenue from nutritional products, including its leading brand, Ensure.

Advertisement

That diversification gives Abbott plenty of ways to grow, diversify, and adapt to changing market conditions. When there was a big need for testing when concerns about COVID were rampant, that area of its business was soaring. When its nutritional segment struggled due to a recall of baby formula products, the company was able to weather the storm. Over the past nine months, it has reported positive growth in all of its segments besides diagnostics, which are down against stronger comparable numbers from a year ago due to COVID testing sales.

Abbott is experiencing some excellent growth in its medical device segment. Demand for its continuous glucose monitors (which help people with diabetes stay on top of their glucose levels) is particularly strong. For the period ending Sept. 30, those products brought in $1.6 billion in revenue, which increased at a rate of more than 19% year over year.

The company has been paying a dividend since 1924, and like Coca-Cola, it is a Dividend King. Abbott’s strong diversification and modest payout ratio of 66% make it highly probable that there will be more dividend hikes in store for investors who buy and hold the stock.

Before you buy stock in Eli Lilly, consider this:

Advertisement

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Eli Lilly wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $908,737!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. TheStock Advisorservice has more than quadrupled the return of S&P 500 since 2002*.

David Jagielski has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Abbott Laboratories. The Motley Fool has a disclosure policy.

(Bloomberg) — ASML Holding NV (ASML), the Dutch maker of advanced chip-making machines that are critical to global supply chains, reaffirmed its long-term revenue outlook as it bets on an artificial intelligence-driven boom in semiconductor demand.

Most Read from Bloomberg

The Dutch firm projected that sales in 2030 will range from €44 billion ($46 billion) to €60 billion, in line with its previous forecast, according to a statement issued as part of the company’s investor day on Thursday.

Advertisement

The outlook is meant to reassure investors after the company’s order intake significantly missed analysts’ estimates in the third quarter, sparking a selloff in its shares and those of other chip-related businesses. Chipmakers such as Nvidia Corp. have enjoyed a boom in demand for their AI chips. But sales to other key buyers, including automakers and mobile phone and PC manufacturers, have remained mired in a prolonged slump.

“A few weeks ago, we had a bit of a conservative view for 2025,” Chief Executive Officer Christophe Fouquet said at the investor day. “In many ways, this is related to the change of the market. But when it comes to 2030, we are still very, very bullish.”

ASML expects growing AI demand will help boost global chip sales to over $1 trillion by 2030, which it said represents an annual growth rate in the semiconductor market of about 9%.

ASML is the only company in the world that makes the kind of lithography machines that help semiconductor companies in turn produce the advanced chips powering everything from Apple Inc.’s smartphones to Nvidia’s AI accelerators. As such, it is often viewed as a bellwether for the broader industry and an early indicator of global semiconductor demand.

Manufacturing more cutting-edge AI chips will mean more of ASML’s advanced extreme ultraviolet lithography machines will be needed by semiconductor makers. The company foresees double-digit growth in EUV spending annually through 2030 for both advanced logic and DRAM.

Advertisement

The company forecast a gross margin of between approximately 56% and 60% in 2030.

ASML shares rose as much as 5.9% in Amsterdam on Thursday, the biggest intraday gain since July 31. They were up 5% to €659.10 at 1:18 p.m.

While ASML in October cut its sales outlook for next year, it said on Thursday it will maintain its spending priorities. ASML currently has an ongoing €12 billion buyback through 2025 of which only 14% has been repurchased.

“We confirm our capital allocation strategy, and expect to continue to return significant amounts of cash to our shareholders through a combination of growing dividends and share buybacks,” ASML Chief Financial Officer Roger Dassen said in the statement.

Advertisement

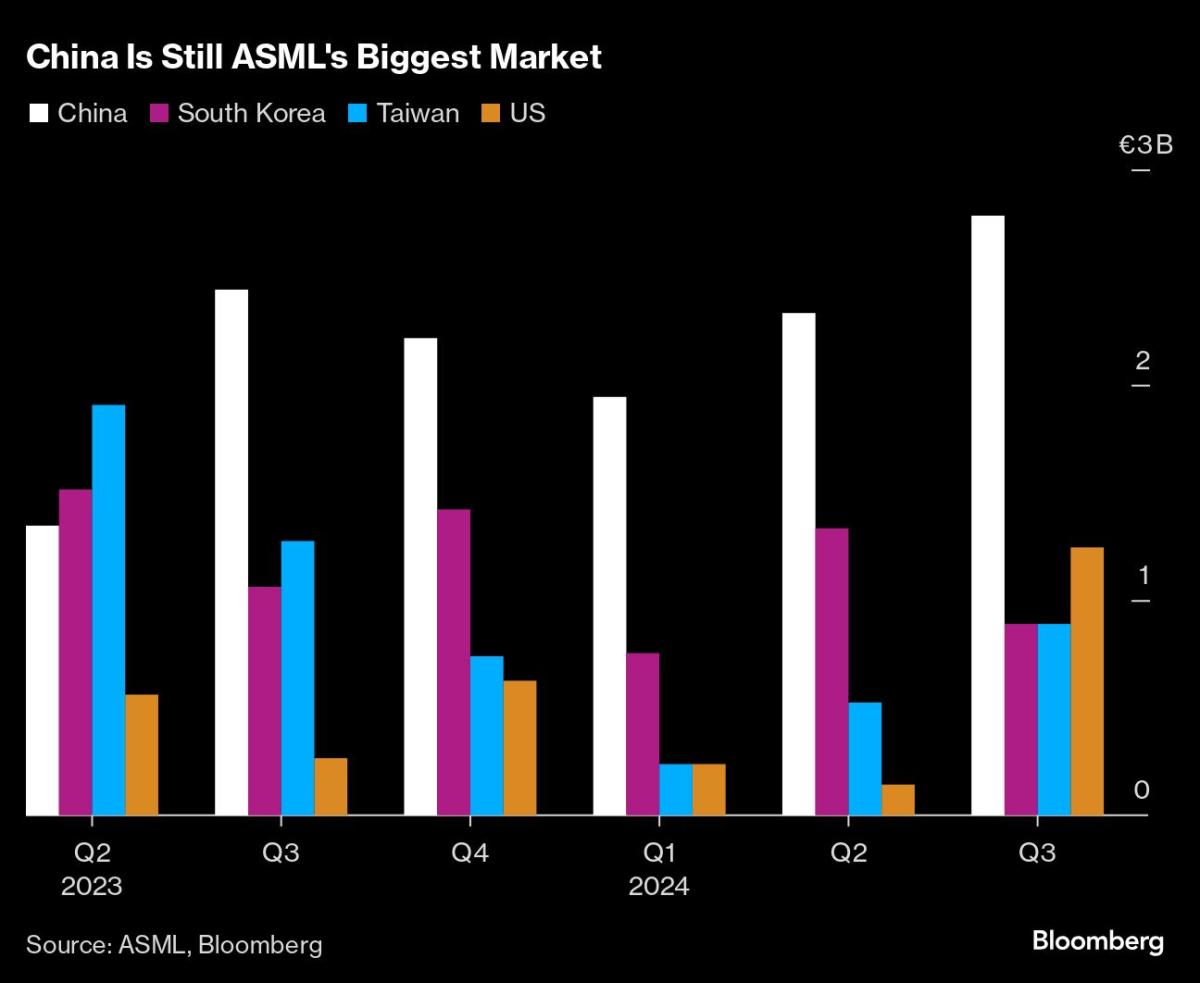

Also weighing on ASML’s prospects is the US government’s ongoing effort to limit China’s rise in the semiconductor sector, through repeated rounds of export controls that have targeted the sale of advanced artificial intelligence chips and chipmaking equipment. The Dutch government has struggled to find a middle ground between its US ally and ASML’s biggest market.

Due to the US pressure, ASML has never been able to sell its EUV machines to the Asian nation and was restricted from shipping its second most-advanced tools from this year.

China accounted for €2.79 billion of sales in the third quarter, nearly half of ASML’s total. The company expects China sales to account for about 20% of total revenue next year. US pressure on ASML to further restrict sales of semiconductor technology to Beijing will likely grow, Fouquet said in an interview with Bloomberg in October.

Fouquet, who took the helm at ASML in April, told investors in October that he expects a slow chip market recovery to extend “well into 2025.” Still, next year and 2026 will be growth years for the industry and ASML overall, he said.

Disney (DIS) on Thursday reported fiscal fourth quarter earnings per share and revenue that topped Wall Street estimates as its direct-to-consumer business built on recent momentum and swung to a profit.

The company reported Q4 adjusted earnings of $1.14 per share, above the $1.10 analysts polled by Bloomberg had expected and higher than the $0.82 Disney reported in the prior-year period.

Revenue came in at $22.57 billion, exceeding consensus expectations for $22.47 billion and higher than the $21.24 billion reported in the year-ago period.

Advertisement

The stock rose over 5% in premarket trading immediately following the results.

Disney’s direct-to-consumer (DTC) streaming business, which includes Disney+, Hulu, and ESPN+, posted operating income of $321 million for the three months ending Sept. 28, compared to a loss of $387 million in the prior-year period.

Analysts polled by Bloomberg had expected DTC operating income to come in around $203 million after the company reached its first quarter of streaming profitability in its Q3 results.

Achieving consistent profits in streaming is critical for Disney and other media giants as more consumers shift to DTC services over traditional pay-TV packages.

Advertisement

In mid-October, the company hiked the price of its various subscription plans, highlighting a trend that has gained traction over the past year as media companies attempt to boost margins on direct-to-consumer (DTC) offerings in the face of greater linear television declines.

Disney said Thursday that it expects DTC operating income of approximately $875 million in fiscal 2025.

The entertainment giant’s results come as it searches for a successor to current CEO Bob Iger to help it navigate a changing industry. A recent report from the Wall Street Journal said the pool of candidates is expanding as the executive is set to leave Disney for a second time by the end of 2026.

Last month, Disney said it plans to announce its next CEO in early 2026, with current Disney board member and former Morgan Stanley (MS) CEO James Gorman leading the charge. He will serve as the company’s new chairman of the board, effective Jan. 2, 2025.

Advertisement

Among the investor concerns Iger’s successor will inherit is a potential slowdown in Disney’s theme parks business.

Revenue for the parks division came in slightly ahead of estimates, rising 1% year over year to reach $8.24 billion.

Operating income, however, fell short of expectations of $2.31 billion to hit $1.66 billion in the quarter, a 6% drop compared to the prior year.

This was primarily driven by weak results overseas with international operating income plummeting 32% year over year. The company cited a decline in attendance and a decrease in guest spending amid the Paris Olympics and a typhoon in Shanghai.

Advertisement

(L to R) Chief executive officer and chairman of The Walt Disney Company Bob Iger and Mickey Mouse look on before ringing the opening bell at the New York Stock Exchange (NYSE), November 27, 2017 in New York City. Disney is marking the company’s 60th anniversary as a listed company on the NYSE. (Drew Angerer/Getty Images) ·Drew Angerer via Getty Images

In one bright spot, domestic operating income rose 5% compared to the prior-year period, reversing the declines seen in the third quarter. The company estimated that Hurricanes Helene and Milton will register a hit of about $130 million for the current quarter, while the Disney cruise line pre-launches will tack on an additional $90 million.

Disney said it expects “high single-digit” adjusted EPS growth in 2025, beating estimates of a 4% uptick, and that earnings growth should reach double digits in 2026 and continue through 2027.

In 2025, the company is also targeting $3 billion in stock repurchases and “dividend growth that tracks our earnings growth.”

Alexandra Canal is a Senior Reporter at Yahoo Finance. Follow her on X @allie_canal, LinkedIn, and email her at alexandra.canal@yahoofinance.com.

You must be logged in to post a comment Login