Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

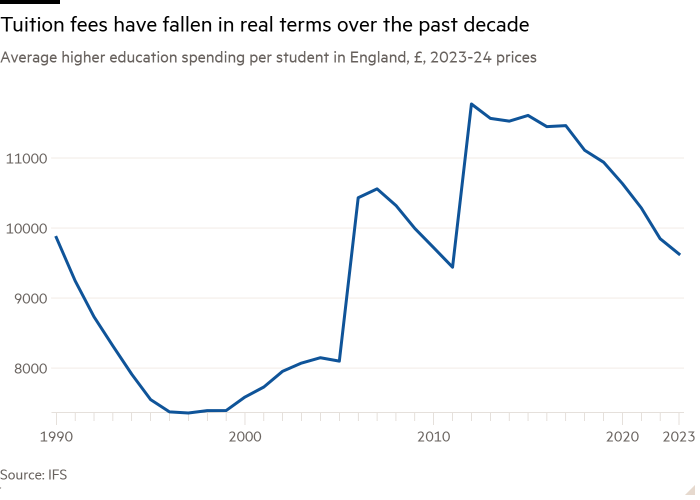

Top UK universities routinely win high marks in international rankings. But many of their less famous peers are flunking important financial tests. The recent decision to increase university tuition fees in line with inflation next year will not, by itself, make much difference.

It halts the erosion of the income from teaching domestic students. But costs are rising too. After taking account of the rise in employers’ national insurance announced in the Budget, the net increase averages a princely £45,000 per institution.

Advertisement

Many problems are down to overexpansion. The funding model introduced in 2012 created an incentive to maximise student recruitment without much pressure to provide value for money. There was also little reason to minimise taxpayers’ exposure to written-off student loans until the accounting rules changed in 2018. Universities sought to attract growing numbers of international students. Their share of total fee income rose 12 percentage points to 44 per cent in the six years to 2022-2023.

That helped bridge the funding gap caused by the domestic tuition fee freeze. But foreign student numbers have sharply fallen after new visa restrictions on their ability to bring in dependants were imposed in January. There is also growing competition from Canadian and Australian institutions.

The pain is unevenly distributed. Rating agency S&P Global Ratings reckons most universities’ credit quality will remain solid, though margins are being severely squeezed. At the institutions it monitors, it expects operating profits to average about 0.5 per cent of operating expenses in the next two years, down from almost 5 per cent over the past three years.

Best placed are research-intensive institutions, with famous brands that are a big draw for international students. Institutions such as Oxford, Cambridge and University College London only relied on domestic undergraduate tuition fees for about 5 per cent of their total income in 2023, according to rating agency Moody’s.

The finances of lower-ranked universities that focus on domestic students are also reasonably stable as they will benefit from the fee rise and not suffer much from international students staying away. The most vulnerable institutions are lower-tier universities that rely on international students, especially those drawn from countries such as Nigeria and India who are particularly affected by the recent visa changes.

Advertisement

Struggling institutions have been cutting jobs and considering mergers and partnerships. That might not be enough to stave off disaster. The universities that staked their future on recruiting growing numbers of international students are finding that bet is rapidly turning sour.

Good afternoon and welcome back to the State of Britain.

I’m Jennifer Williams, the FT’s northern England correspondent, covering for Peter while he takes a break.

Tuesday saw an esteemed gathering in Manchester’s Bridgewater Hall. A thousand people — including some very big names from the past 40 years of British politics — gathered to pay their respects to Sir Howard Bernstein, the late chief executive of Manchester council.

However Bernstein was no mere council chief executive. In the words of former chancellor George Osborne, Bernstein was the “single most important” public servant this country has seen in the past 30 years. Not just in local government, but full stop.

Advertisement

Bernstein’s story is about the transformation, one that is a long way from complete, of an urban economy that in the 1980s looked in danger of collapsing.

And as such, it contains lessons for a new generation of ministers now wanting to lever in private investment on a national scale.

Doing things differently

In recent years the phrase “we do things differently here” has come to be somewhat overused by those promoting Manchester’s story.

Advertisement

But Bernstein actually did do things differently, out of sheer necessity.

His mission was the transformation of Manchester’s ailing post-industrial economic landscape. He thought the city needed to stand on its own two feet, rather than relying on endless fiscal transfers from London. That meant sidestepping obstacles, often imposed by the state itself, and convincing investors that the city was worth a punt.

Let’s start with the puzzle Bernstein had to solve.

To shamelessly steal a figure quoted by the Mancunian economist Mike Emmerich, who worked closely with Bernstein, between 1978 and 1981, the conurbation was losing 127 manufacturing jobs per working day. Manchester was haemorrhaging traditional industry.

Advertisement

After an initial period of trench warfare with Margaret Thatcher’s government, a conscious decision was taken to do something more productive. Bernstein and others sought to identify where the city’s economy went next — and how to get there.

Lessons for metro mayors

Opportunities were identified, some of which didn’t come off. But others did. Crucially, Manchester took its ability to think seriously. It had its own internal think-tank, run by Emmerich, specifically to analyse, research and understand what the economy looked like and where it might go.

As investors came to understand what Manchester was doing, the town hall became seen as a credible partner.

Advertisement

The importance of local reliable institutions is therefore one of the biggest takeaways, for me, from Bernstein’s story.

At present, new ministers are looking to metro mayors — who only exist, incidentally, due to Bernstein’s 2014 devolution deal with Osborne, one of his many local growth strategies — for answers to their economic questions. They want them to create localised growth plans and sell their areas to investors.

Whitehall can’t possibly know the needs of each local economy. But at the moment, there is not an abundance of that kind of expertise across English local government either (partly, it has to be said, as a result of policies enacted by Osborne).

So these institutions are going to have to either be rebuilt, or in some cases, built from scratch, if the sort of endeavours undertaken by Bernstein are to be replicated at scale.

Advertisement

The Productivity Institute’s Philip McCann, who has been researching how investors perceive risk outside of the south east, notes that reassuring investors about propositions beyond London is not just about mayors. It’s also about “the capabilities of the people who don’t appear in the news”.

In Manchester’s case, such people spent years coming up with ways to de-risk their city.

Public land was leveraged. The sovereign wealth of Abu Dhabi was tapped. New financial mechanisms were invented and taken to the Treasury, such as the rotating Housing Investment Fund, a recyclable loan facility for the property sector that in effect underwrote the new skyline you can see in the city centre today.

Some of those, including the HIF, have proved controversial. Even some of its supporters acknowledge that what the fund does is in effect pick winners, not something everyone is comfortable with. Abu Dhabi’s involvement in the city, meanwhile, has not been without controversy either; debates have raged over levels of transparency, where tax gets paid and what human rights records lurk in the background.

Advertisement

Always have a plan B

These were trade-offs Bernstein himself was entirely at ease with. Labour ministers in search of capital may have to weigh up similar questions, amply highlighted by the recent row over P&O, the ferry operator.

Bernstein was also rarely without a plan B. In 2008, his original aim to raise cash for an expanded tram network was thwarted: a proposed congestion charge was defeated by referendum. Central government had little intention of simply funding more trams. So Bernstein suggested a deal: give us the money and we will repay you through the increase in our tax returns.

The model worked, indicating that the traditional Treasury view of the value of such investments may be somewhat flawed.

Advertisement

Bernstein also leveraged the Greater Manchester Pension Fund, the area’s local government pension pot, which for a long time has allocated 5 per cent of its money to local investment propositions. There are signs, in the chancellor’s latest Mansion House address, that she is thinking along similar lines.

Nevertheless, you still end up circling back to the importance of local leadership and institutions. For even if such capital is freed up, a credible set of investable proposals, based on a clear-eyed, real-world understanding of the local economies and markets in question, will be needed.

One property investor told me this week that many local areas have a tendency to pop up at major symposia like the MIPIM property festival, touting shiny “pitchbooks”.

But once the surface is scratched, he said, they do not always stand up under scrutiny.

Advertisement

A final lesson from the Bernstein story relates not to Manchester, but to the hard wiring of central government. The level of imagination that has had to be applied to the city’s turnaround was not only necessary in order to convince private investors — it was necessary because central government had been continually placing its own bets in the south east.

At a panel event the day after Bernstein’s memorial, Lord Jim O’Neill, a long-standing proponent of further investment into northern cities, argued that the chancellor’s increased borrowing headroom must now be used to invest in the sort of transport infrastructure that has not traditionally been a Treasury favourite.

It comes down, he concluded, to “how you measure value”: the Treasury needs to start valuing the impact of potential investments to long term growth. Precisely the approach taken by Bernstein.

Britain in charts

What really matters, of course, is whether Bernstein’s approach worked.

First, the good news.

Advertisement

Over the past couple of decades, Greater Manchester’s productivity has improved. All that work, all that cajoling of investment, all those innovations are starting to show up in the data.

This is not to be underestimated. What looks like a modest productivity improvement on this week’s chart reflects what has in reality been a monumental change in the face and economy of a city.

Anyone involved in this enterprise would also point you back to those job losses I cited at the start. The mountain to climb was huge.

And yet. The fact remains, Greater Manchester is still miles behind London; it is a long way from being able to stand on its own two feet.

Advertisement

To quote researchers from the Resolution Foundation’s Economy 2030 Inquiry, Greater Manchester remains 35 per cent less productive than London, “a demonstrably larger gap than between France’s second city, Lyon, and Paris, which stands at just 20 per cent”.

Widening this conundrum out to regional cities in general, you can see other places are even further behind. That’s how hard this stuff is.

Bernstein, of course, is no longer around to help close the gap. But he started the job — and it will now be for a new generation of civic leaders, thinkers, investors and ministers to finish it.

A MAP has revealed Britain’s cheapest postcodes where homes cost as little as £80,000.

Homebuyers in dual-income households now face paying nearly four times their total income to purchase an average property, according to Zoopla.

9

Workington Harbourwith with the Lake District in the distance, where the average house price is £222,200Credit: Getty

9

Advertisement

The marina in PlymouthCredit: PA

9

Croydon is the most affordable place to live in London, according to ZooplaCredit: Getty

The property website claimed households, where both partners work full-time, typically pay 3.8 times their annual household income to buy a home.

Single buyers in Britain typically face paying 7.6 times their annual income to purchase a home.

Advertisement

Zoopla analysed house price-to-earnings ratios to identify the most affordable areas across the UK’s nations and regions, using data based on a two-earner household with an average local salary.

The online property marketplace found that in Cumnock in East Ayrshire, Scotland, and Shildon in County Durham in the North East of England, the average house price is 1.1 times typical household earnings.

The most affordable location in London was still above the national average affordability ratio for a two-earner household.

Zoopla identified Croydon as the most affordable area in London, with homes costing approximately 4.7 times local incomes.

Advertisement

Izabella Lubowiecka, a senior property researcher at Zoopla, said: “London remains the least affordable area for home-buyers.

“Those in London looking to get more for their money may want to consider buying in one of the South East and East of England’s commuter belt, where there are many towns that are more affordable than London.

“The same is true in markets around many regional cities and we see buyers seeking value for money.”

NAEA (National Association of Estate Agents) Propertymark president Toby Leek said: “Affordability for many is a real issue and, as purse strings remain tightened despite easing factors such as slight drops in inflation, prospective and current home-owners will be looking to enter the market with caution, but also, in some cases, further flexibility in where they nest themselves.

Advertisement

The Sun’s James Flanders explains how to find the best deal on your mortgage

“As many people no longer have the restriction of basing themselves from a static office full-time, they are able to look elsewhere to actually step onto the housing ladder for the first time or find their next, more affordable dream home.”

The report was released alongside research commissioned by Santander UK, which found that nearly three-quarters (73%) of potential first-time buyers would consider relocating to new towns.

This contrasts with 57% of “second steppers” planning to move from their first home and 41% of those looking to downsize in later life.

Among those unwilling to move, several expressed concerns about housing quality.

Advertisement

However, others stated that the availability of healthcare facilities and green spaces would make them more likely to consider relocating.

According to a survey of over 4,000 people in September, 47% of prospective first-time buyers cited affordability as a major hurdle.

Graham Sellar, head of business development – mortgages, at Santander, said: “New towns have incredible potential but, to maximise the impact they can have, they must be built with the people who will call them home in mind.

“Our research shows just how important it is to create lively communities with green spaces as well as easy access to healthcare when it comes to appealing to more home-buyers.”

Here are the most affordable locations in each nation or region, according to Zoopla, based on a two-income household, with the postal town followed by the average house value, the estimated annual household income and the house value-to-earnings ratio:

Advertisement

East Midlands, Gainsborough, £170,000 – £70,500, 2.4

East of England, Wisbech, £209,800 – £70,900, 3.0

South East, Dover, £250,000 – £79,300, 3.2

South West, Plymouth, £222,200 – £68,300, 3.3

Wales, Ferndale, £101,600 – £67,700, 1.5

West Midlands, Stoke-On-Trent, £139,200 – £62,100, 2.2

Yorkshire and the Humber, Hull, £119,800 – £62,200, 1.9

London, Croydon, £417,800 – £84,800, 4.7

North East, Shildon, £73,200 – £65,800, 1.1

North West, Workington, £123,700 – £76,900, 1.6

Scotland, Cumnock, £80,300 – £75,800, 1.1

Source: Zoopla

How to buy your first home

Getting on the property ladder can feel like a daunting task but there are schemes out there to help first-time buyers have their own home.

Lifetime ISA – This is a Government scheme that gives anyone aged 18 to 39 the chance to save tax-free and get a bonus of up to £32,000 towards their first home.

You can save up to £4,000 a year and the Government will add 25% on top.

Shared ownership – Co-owning with a housing association means you can buy a part of the property and pay rent on the remaining amount.

Advertisement

You can buy anything from 25% to 75% of the property but you’re restricted to specific ones.

Mortgage guarantee scheme – Available for first-time buyers and those who’ve owned a property before who have a minimum 5% deposit.

It can be used to buy any type of home so long as you don’t pay more than £600,000 for it.

By providing a guarantee that the government will cover some of a lender’s losses if a borrower can’t afford to repay their mortgage and the home is repossessed – more lenders are prepared to lend up to 95%.

Advertisement

First-Time Buyer Tips

IF you’re looking to take your first step onto the property ladder, why not sign up to our new first-time buyer newsletter.

Buying your first home can be scary and confusing, but our five-part series will cover everything you need to know.

From ways to boost your chances of getting a top-rate mortgage to preparing for your move, The Sun’s new first-time buyer newsletter has got you covered.

Advertisement

9

An aerial view of a rural countryside under a bright sky in New Cumnock, ScotlandCredit: Getty

9

The average annual income in Stoke-on-Trent is £62,100Credit: Getty

9

The average house price in Gainsborough, Lincolnshire, is £170,000Credit: Getty

9

Advertisement

A view of houses in Ferndale in the Rhondda ValleyCredit: Getty

9

Residents in Wisbech are paying an estimated 3 times more than their annual income on propertiesCredit: Getty

9

The average house price in Dover is around £250,000Credit: Getty

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Angry eruptions in elections around the world are changing leaders. And many of those leaders are coming in with radical offers to the voters. But can anger change an economic outcome for the better? And will it? Today on the show, Katie Martin hosts a live forum at the Kilkenomics Festival in Kilkenny, Ireland and discusses the topic with Leah Downey, a political theorist, and Eric Lonergan, a money manager. Also, we go long turkeys and short orange politicians.

ROYAL Mail is to make a major change to fees within days as shoppers face a surcharge this Christmas.

The service has revealed that business account customers will be asked to pay an additional peak surcharge of 5p for letters and 10p for parcels.

1

Royal Mail is to make a major change to fees within daysCredit: Getty

This will come into force on November 18 and end on January 10, 2025 – the peak time for Christmas deliveries.

Advertisement

While the surcharge won’t be charged to directly to consumers, there are concerns that they will end up footing the bill anyway as businesses look to up their prices to cover the extra cost.

Sarah Coles, personal finance analyst at Hargreaves Lansdown, said: “At a time when rising prices have eaten into profits, some companies will feel they have no alternative but to pass the costs on.

“It means shoppers being clobbered with extra delivery charges at a horribly expensive time of year.”

The same surcharge was added to letters and parcels for the first time last year.

Advertisement

The 5p peak surcharge is applied to Royal Mail 24 and Royal Mail 48 large letters, Royal Mail Tracked 24 and Royal Mail Tracked 48 letterboxable products sent by business account holders.

While the following products will be hit with a 10p peak surcharge:

Royal Mail 24

Royal Mail 48 Parcels

Royal Mail Tracked 24

Royal Mail Tracked 48 Parcels

Royal Mail Tracked Returns

Royal Mail Special Delivery Guaranteed by 9am, 1pm and end of the day Sunday

Special Delivery Guaranteed Returns

A Royal Mail spokesperson said: “The peak surcharge only applies to business customers for the Christmas period and was introduced last year.

“It applies an additional charge to certain business parcel products for a limited period to reflect the increased demand and capacity needed to handle increased volumes.

eBay Parcel Surprise: Rare Stamps Galore!

“Other parcel carriers apply a similar surcharge. Christmas is our busiest time of the year and we invest in around 16,000 additional staff, more vehicles and temporary sites to increase our capacity to handle double the normal volumes of parcels.”

Advertisement

It comes after Royal Mail upped the price of first-class stamps by 30p to £1.65 at the start of October.

First class stamp prices increased by 10p to £1.35 in April and by 10p to 85p for second class.

Royal Mail said it had tried to keep price increases as low as possible in the face of declining letter volumes, and inflationary pressures.

Regulator Ofcom, which has been consulting on the future of the universal postal service since January, said it is now focusing efforts on changes to the second class service while keeping first class deliveries six days a week.

Under the plans being considered, second class deliveries would not be made on Saturdays and would only be on alternate weekdays, but delivery times would remain unchanged at up to three working days.

Ofcom said no decision had been made and it continues to review the changes, with aims to publish a consultation in early 2025 and make a decision in the summer of next year.

Royal Mail said letter volumes have fallen from 20billion in 2004/5 to around 6.7billion a year in 2023/4, so the average household now receives four letters a week, compared to 14 a decade ago.

The business said the move would make letters more secure.

Anyone who still has these old-style stamps and uses them may have to pay a surcharge.

How to save money on Christmas deliveries

Advertisement

CHRISTMAS is all about giving, but unfortunately, it does come at a price – especially if you prefer to shop online.

Senior Consumer Reporter Olivia Marshall shares five ways you can save money on Christmas deliveries to help you protect the pennies this festive season.

Order early

Many retailers offer discounts on shipping costs if you place your orders well in advance.

Advertisement

This can also help you avoid the higher costs associated with last-minute express deliveries.

Free shipping offers

Look out for retailers that offer free shipping promotions, especially during the festive season.

Some stores provide free delivery if you meet a minimum purchase amount.

Advertisement

Click and collect

Opt for click and collect services where you can pick up your purchases from a local store or designated collection point.

This can often be a free service and can save you on delivery fees.

Combine orders

Advertisement

If you are buying from the same retailer, try to combine your purchases into a single order.

This can help you meet free shipping thresholds or reduce the number of delivery charges you need to pay.

Use discount codes

Search for discount codes or vouchers that can be applied to your delivery costs.

Advertisement

Websites and browser extensions dedicated to finding and applying discounts can be particularly helpful.

By planning ahead and taking advantage of these strategies, you can reduce the cost of your Christmas deliveries.

Do you have a money problem that needs sorting? Get in touch by emailing money-sm@news.co.uk.

Your guide to what the 2024 US election means for Washington and the world

Donald Trump has nominated vocal vaccine sceptic and former Democrat Robert F Kennedy Jr as head of the US Department of Health and Human Services, the latest in a series of controversial picks for top cabinet jobs.

The appointment will put Kennedy, who sowed doubts about Covid-19 vaccines and has been critical of the pharmaceutical industry, in charge of a department with a $1.8tn budget with wide-ranging influence over drug regulation and public health.

Advertisement

Trump said in a statement on Thursday that he was “thrilled” to appoint Kennedy to the role. “For too long, Americans have been crushed by the industrial food complex and drug companies who have engaged in deception, misinformation, and disinformation when it comes to Public Health,” the president-elect wrote in social media post.

As head of HHS, with oversight of agencies such as the Food and Drug Administration and the Centers for Disease Control and Protection, Trump said Kennedy would “restore these Agencies to the traditions of Gold Standard Scientific Research, and beacons of Transparency, to end the Chronic Disease epidemic, and to Make America Great and Healthy Again!”

STATE pensioners are eligible to claim up to £350 in cash to help cover the cost of energy bills this winter.

The Suffolk Community Foundation has launched the 14th year of its annual Surviving Winter appeal, which is in response to winter fuel payments being slashed.

1

A charity that helps vulnerable older people to “survive winter” said its grants and advice were needed more than everCredit: Alamy

However, in July, the government said it would only be made to those on low incomes who received certain benefits.

Chancellor Rachel Reeve’s decision to means-test the up to £300 cash boost has meant around 10million elderly people can no longer get the support.

Now only those receiving pension credit will receive the handout.

The Suffolk charity said it’s campaign has become even more relevant this year because ninety per cent of pensioners are estimated to lose the winter fuel payment.

Advertisement

It added that the government’s policy change also means the organisation cannot rely on those who do not need the payment to consider donating it to help others.

According to the appeal’s website, the campaign has raised more than £1.5 million so far, and the charity is appealing to anyone who feels able to donate to consider doing so.

£175 could be used to help someone pay for gas or electricity, whereas £350 could provide 500 litres of heating oil.

Cabinet Minister grilled on Winter Fuel Payments

It adds that the fund has provided a lifeline for many thousands of people by helping them to stay safe and healthy in their own homes as the weather turns colder.

Advertisement

How can I apply for the scheme?

You may apply for support if you are over the age of 66 and are not on pension credit.

You must also live in Suffolk, have maximum savings of £5,000 and a maximum income of £20,000, or £24,000 if you’re a couple.

Three charity partners are working with Suffolk Community Foundation to manage the applications and payments; East Suffolk Citizens Advice, Sudbury and South Suffolk Citizens Advice and Gatehouse Caring.

Individuals wishing to apply should get in contact with the office of the district or borough they live in.

It is means-tested, so you must have no more than £6,000 in savings for a household of one person or no more than £8,000 for a household of two or more people.

You must have a weekly income of no more than £323 per week for a household of one person or no more than £442 per week for a household of two or more people.

To apply you can call 0808 808 00 00 or you can speak to one of your healthcare team, like a district nurse or Macmillan nurse, care professional or benefits adviser who can fill in the form with you online.

The British Legion has also set up a Cost of Living grant, which can be applied for here using the Lightning Reach portal.

You can also find out what grants may be available to you using Turn2Us’s grant search on the charity website.

There is a huge range of grants available for different people – including those who are bereaved, disabled, unemployed, redundant, ill, a carer, veteran, young person or old person.

Advertisement

How has the Household Support Fund evolved?

The Household Support Fund was first launched in October 2021 to help Brits pay their way through winter amid the cost of living crisis.

Councils up and down the country got a slice of the £421million funding available to dish out to Brits in need.

It was then extended in the 2022 Spring Budget and for a second time in October 2022 to help those on the lowest incomes with the rising cost of living.

You may also be eligible for up to £500 worth of cost of living payments from the government’s Household Support Fund (HSF) which is worth £421 million in total.

It’s available to support those who are struggling to afford household basics including food, energy, wider essentials, and exceptional costs.

Advertisement

The fund has been split up between councils in England who are in charge of distributing their allocation.

It was set up in 2021, however, it has been extended by the UK government a number of times.

How much you are eligible for is usually based on what benefits you already receive and your financial circumstances.

To be eligible for help, you usually have to be in receipt of a council tax reduction or show proof of being in financial difficulty.

Advertisement

Each council has a different application process – so you’ll have to ask your local authority or find out via your council’s website.

To find out how to contact your local authority, use the gov.uk authority tool checker.

In the last round of funding, some residents received their share automatically, while others had to apply.

For example, Haringey London Council is issuing automatic payments to eligible residents, as well as a support fund which can be applied to.

Advertisement

It is also issuing payments to schools, which means they can distribute free school vouchers.

Do you have a money problem that needs sorting? Get in touch by emailing money-sm@news.co.uk.

You must be logged in to post a comment Login