Donald Trump said earlier this year that if he were to be re-elected, “incomes will skyrocket, inflation will vanish completely, jobs will come roaring back, and the middle class will prosper like never before”.

The majority of US voters have bought into that pitch, but many economists do not.

Instead, they warn that his plans to enact sweeping tariffs and deport millions of immigrants risk will do the exact opposite of what the president-elect claims — reigniting inflationary pressures when the worst bout for a generation has yet to be fully tamed.

While stock markets were boosted by Trump’s pledge to lower taxes for the wealthy and corporations, others think those moves will store up issues for years to come, expanding the already-large government deficit.

“These kinds of policies — deportation, incursions on Fed independence, tariffs on an unprecedented level — they all inject additional uncertainty into the economic environment,” said David Wilcox, a former Federal Reserve staffer who now works at the Peterson Institute for International Economics.

“There’s not much these days that unites businesspeople, households and policymakers,” said Wilcox. “But there is one concept that does unite just about everybody, and that is that uncertainty is really damaging economically.”

The economists who support Trump’s economic agenda — figures such as Stephen Moore, Arthur Laffer and Larry Kudlow — believe his tax cuts will boost demand. Their impact on growth will raise tax revenues, shrinking the country’s gargantuan deficit in the process.

Others think the lower levies could provide a short-term boost to growth too.

Advertisement

“Trump’s victory will ensure a lower tax environment that should boost sentiment and spending in the near term,” said James Knightley, economist at ING Bank. “However, promised tariffs, immigration controls and higher borrowing costs will increasingly become headwinds through his presidential term.”

While inflation is not fully under control, the president-elect will take the helm at a time when the world’s largest economy is, by most metrics, in rude health.

Jobs are plentiful, lay-offs are low and consumers continue to spend, despite a surge in US interest rates, which — until recently — left borrowing costs at a 23-year high. Once rampant, recession fears have faded as inflation has fallen from above 7 per cent to close in on the Fed’s 2 per cent target, suggesting a much-anticipated soft landing is within reach.

“The economy is still pretty solid,” said Karen Dynan, a former senior Fed staffer now at Harvard University. “We’re getting much closer to normal inflation conditions [and] nothing suggests the labour market is in a worrisome spot.”

Advertisement

Republicans captured control of the Senate on Tuesday and have made inroads in several House of Representatives races that will need to swing to Democrats if they are to win the lower chamber of Congress.

If Republicans are victorious there too, Trump would have much more leeway to push through even the most unorthodox parts of his economic agenda.

Trump’s plan centres on sweeping tariffs that he claims will not only bolster US manufacturing, create jobs and lower prices, but will also hand the country a powerful bargaining tool in negotiations with allies and adversaries.

Calling such levies the “greatest thing ever invented”, Trump has floated the idea of across-the-board tariffs of up to 20 per cent on all imports as well as 60 per cent tariffs on Chinese goods.

Şebnem Kalemli-Özcan, an economist at Brown University, predicts that unemployment could also rise as businesses are forced to cut back in the face of higher costs borne from tariffs and higher wages resulting from changes in immigration policy.

“These policies are pushed as policies that will create more jobs for Americans, but the effect is going to be the exact opposite,” said Kalemli-Özcan.

The US central bank, which began lowering borrowing costs in September, would potentially be forced to reverse course should price pressures re-emerge.

During Trump’s first presidency, the Fed responded to an intensifying trade war between the US and China by lowering interest rates by 0.75 percentage points, in what it likened to taking out insurance against the possibility of a significant blow to growth.

Advertisement

But with the embers of inflation not yet fully snuffed out, the policy response could look different from in 2019, when inflation was below the Fed’s 2 per cent target.

The tariffs and immigration restrictions Trump put in place during his first term did not generate significant inflation, but they were of a far smaller scale than what the president-elect has proposed for his next four years in office.

In his first term, Trump repeatedly attacked the Fed and its chair, Jay Powell, for not lowering interest rates earlier and more aggressively. This time, he has floated more direct interference with the central bank, including advocating for having a greater say over monetary policy decisions.

The Fed has “a lot of legal and institutional safeguards” to protect its status as an independent institution, says Vincent Reinhart, a former Fed official who is now chief economist at Dreyfus and Mellon. That includes extended term limits for governors, whose appointments require Congressional approval.

Advertisement

Powell’s term as chair ends in May 2026, and before that there is only one other vacancy on the board of governors that year. The next opening would not come up until 2030, when Christopher Waller’s term expires.

Still, any indication that the Fed’s independence is being eroded could have severe financial market consequences — a growing fear given the enormous deficits the country is set to run during Trump’s second term.

The US president-elect’s vow to extend tax cuts on the wealthy that are set to expire in 2025, as well as reducing the corporate tax rate for domestic producers and exempting certain forms of pay from income tax, would add a further $5.8tn to the deficit over the next decade, according to the Penn Wharton Budget Model at the University of Pennsylvania.

Advertisement

“The conversation we need to have as a nation is about getting fiscal policy on to a sustainable trajectory. The first step in addressing that problem is not to enact an aggressive programme of additional spending or aggressive tax cuts,” said Wilcox, who is also the director of US economic research at Bloomberg Economics.

“Trump has made it clear that he has no concern whatsoever for fiscal sustainability.”

Your guide to what the 2024 US election means for Washington and the world

Voters have chosen Donald Trump as their 47th president in the 2024 US election after a heated campaign against Kamala Harris.

FT readers have been debating the pros and cons of both candidates for weeks in the comments sections below articles, and now the winner has been decided we want to know what you think about the outcome.

Advertisement

How do you feel now the election is over? Are you happy with the winner? How do you see the outlook for the US? What does it mean for you and your family? Perhaps you live outside the US — tell us what the result means for you.

We will be updating this story with comments and excerpts from our readers across FT.com. Share your thoughts in the comments section below.

Stock markets around the world have been digesting the impact of a Trump administration.

The prospect of looser regulation lifted US bank stocks, with Frankfurt-listed shares in Goldman Sachs, JPMorgan and Morgan Stanley up between 8 and 9 per cent in early European trading. Futures on the S&P 500 and Nasdaq 100 indices climbed 2.4 and 1.8 per cent respectively, while those linked to the small-cap Russell 2000 rose about 5 per cent.

Shares in Tesla, whose chief executive Elon Musk became one of Trump’s most vociferous backers, rose 12 per cent in pre-market trading.

European defence stocks have surged on the prospect of rising spending on defence by European governments. Carmakers took a hit, with auto stocks slumping on fears of new tariffs. Renewable power stocks dropped on fears that Trump could block US wind projects, with Denmark’s Ørsted down 14 per cent in early trading.

Advertisement

Tariff fears hit Chinese markets, with Hong Kong’s Hang Seng index down 2.2 per cent.

Here is a fun fact to start things off: 65.9 percent of American homes are owned by their occupants. If you are one of these homeowners, you already know that life can throw unexpected surprises your way.

From a burst pipe in the basement to a tree crashing through the roof, the unexpected often means scrambling to cover costs.

Repairing a burst pipe will cost around $500 on average. Roof repairs can cost up to $8,000. There is just a lot of money that needs to be spent if you are a homeowner with such bad luck.

Thankfully, that is where your homeowner’s insurance policy steps in, but only if you know how to navigate the process.

Advertisement

What to Know Before You Submit a Claim to Insurance

Let us start at the beginning – before disaster strikes.

You have probably spent a decent amount of time and money picking the best homeowners insurance coverage to protect your property. However, do you know exactly what your policy covers?

According to Hippo, in general, home insurance usually covers damage to the home’s structure and personal property within it. However, such insurance policies vary widely, so take a moment to review yours. Whether it is fire damage, theft or a leaky roof, make sure you know what potential risks your policy accounts for.

It is a bit like knowing the fine print on a concert ticket. Sure, you have got a seat, but are you allowed to bring snacks? It helps to be clear on the details before you actually need them. Knowing your homeowner’s insurance covers a specific incident means you can move quickly when the time comes to submit a claim.

Advertisement

Now, the national average cost of home insurance in the US is $2,285 per year. This is strictly for a policy with a $300,000 dwelling limit. Punch in the numbers in a calculator and it evens out to about $190 per month.

How to Submit a Claim After an Incident

Now, let us fast-forward to the moment when something actually happens. Say you wake up to a flooded basement, and it is time to jump into action.

First things first, do not panic. Most insurance companies have systems in place to handle situations just like this. You will want to notify your insurer right away. Contacting them quickly ensures that the process starts sooner, and they can advise you on the immediate steps to take.

Gathering the necessary documents is a crucial part of submitting an insurance claim. You will need your homeowner’s policy information, receipts for any damaged items and any photos or videos you can take of the damage.

Advertisement

Providing detailed evidence can help support your claim and smooth out the process with the insurance company.

Essential Steps on Submitting a Claim to Insurance

Every insurance company has its way of handling claims, but the general process remains consistent. Here is how to navigate the waters:

Contact Your Insurance Company

You have spotted the damage; now it is time to alert your insurer. Calling or submitting a report online will initiate the claims process.

They will assign an adjuster to evaluate the situation and, if needed, guide you on what to do next. Remember, the sooner you inform them, the faster you can move forward.

Advertisement

Meet the Adjuster

Your insurance company will send an adjuster to assess the damage. They will inspect your property and gather information about what happened. Do not worry; these folks are here to help. Be prepared to provide them with all the necessary documents you have collected.

Discuss Your Coverage Options

This is where knowing yourhomeowners insurance policy pays off. Be ready to discuss what your policy covers with the adjuster. You will want to know how the claim will affect your coverage and whether your payments or premiums might change.

Review and Settle the Claim

Once the adjuster has gathered all the information, your insurance company will offer a settlement. If you are satisfied, they will process the payment, and you can get back to repairing your home.

If not, do not hesitate to negotiate. After all, it is your property, and you deserve a fair settlement.

Advertisement

Preparing for Future Claims: What Homeowners Should Keep in Mind

Sure, no one likes to think about future disasters, but being prepared is always smart.

When reviewing your homeowner’s insurance policies, make a habit of checking the coverage options regularly. Life changes, and so should your insurance. Maybe you have upgraded the kitchen, added a home office or turned your garage into a mini gym. Your homeowner’s insurance coverage should reflect these updates to ensure you are protected.

One trick is to treat your homeowner’s policy like a financial safety net. You would not want to realize there is a hole in it when you need it the most. Understanding what homeowners insurance covers and knowing how to submit a claim to insurance will keep you ahead of any potential risks.

Navigating the Insurance Coverage Process Without Stress

Insurance claims can sometimes feel like an uphill battle, but knowing how to submit a claim to insurance can make all the difference. The key is in the details – gathering the right documents, understanding the process and communicating effectively with your insurance company.

Advertisement

This way, you will not feel lost when you are knee-deep in water or staring at a missing roof.

Stay organized and keep all your insurance documents in one place, whether it is a physical folder or a digital one. When the time comes to submit a claim, you will not be hunting for your homeowner’s policy in a panic. Trust us on this – your future self will thank you for the foresight.

How to Handle the Insurance Company During the Claims Process

If dealing with the insurance company feels intimidating, just remember they are not the enemy. Sure, they might have a business to run, but they are also there to help you through a tough situation.

Approach the process calmly, ask questions, and get clarification if something is not clear. If at any point you feel overwhelmed, consider hiring a public adjuster.

Advertisement

Also, do not forget – being honest and transparent is essential. The more straightforward and detailed you are about what happened, the easier it will be for the insurance company to process your claim.

Your Home, Your Peace of Mind

The bottom line? Submitting an insurance claim does not have to be an arduous process. Knowing how to submit a claim to insurance can help you navigate it with confidence.

Keep your homeowners insurance policy updated, know exactly what your homeowners insurance covers and always be prepared to provide the necessary documents. Your home is one of your biggest investments, and having the right homeowners insurance coverage ensures you are protected when things go wrong.

This week, York will welcome creative industry leaders from around the world as the city celebrates ten years of being a UNESCO City of Media Arts.

York is one of 26 cities globally to have won the City of Media Arts designation and the only city in the UK to hold the title.

The tenth anniversary coincides with the 14th annual Aesthetica Short Film Festival, which showcases and brings together the world’s independent film, VR and gaming industry.

In addition, the city will mark this milestone with York’s first-ever UNESCO EXPO, bringing together leading media arts cities from across Europe, including Braga (Portugal), Linz (Austria), and Oulu (Finland) to explore how UNESCO designation has driven cultural investment and sparked creative opportunities.

Advertisement

The festival, taking place in venues across the city from 6-10 November, will see attendees and participants from over 60 countries arrive in York, with industry leaders from world-famous organisations like the New York Times, Aardman and Ridley Scott Associates sharing their expertise through workshops and panel discussions.

Claire Foale, Interim Director of City Development, said:

“On behalf of the council, I’d like to warmly welcome delegates from across the world to York – a city that blends a rich sense of history with a forward-looking and innovative spirit, making it one of the UK’s most exciting places for creative investment.

“We’re delighted to have supported this year’s festival through the UK Shared Prosperity Fund, enabling Aesthetica to make cutting-edge culture accessible and open for all to enjoy.

Advertisement

“We’re encouraging residents and visitors alike to get involved with the festival and enjoy the world-class talent and creativity on show in our city this week.”

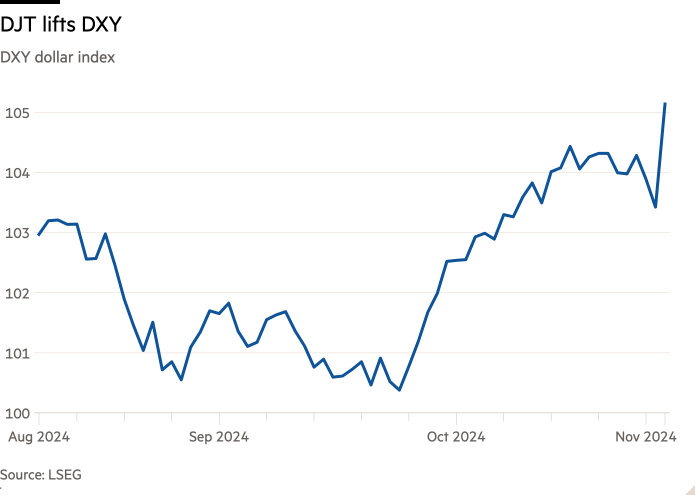

Well, that’s that. Donald Trump will once again be president of the US — and this time fuelled with a desire for “retribution”, a greater popular mandate and at the head of a party now moulded in his image.

That means investors have to contemplate the possibility of a far more radical second term, with many more outlandish policies suddenly becoming at the very least possible. Greenland just got put back into play.

The main “Trump trade” has been to buy the dollar, on the view that Trump’s economic policies will be highly inflationary. This will force the Federal Reserve to shelve its plans for interest rate cuts and buoy the greenback. Higher tariffs dampen overseas purchases and also lift exchange rates, all things being equal.

As Kit Juckes of Société Générale said this morning:

Advertisement

President Trump would like a weaker dollar, but he isn’t going to get his way if he wants to run accommodative fiscal policy at a time when real GDP growth has averaged almost 3% for the last 5 years (and despite how things looked a few months ago, isn’t showing much sign of slowing at all). Throw in trade tariffs at a time when the unemployment rate is only at 4.1%, and he won’t get a weaker dollar, any more than Ronald Reagan was able to, in the first half of the 1980s.

However, this has always felt a little like a myopic, short-term trade, given Trump’s long-standing view that the dollar’s strength is hurting America. Along with the supposed magic of tariffs it is the closest he has to a firm, constant economic conviction.

So we have a big currency problem because the depth of the currency now in terms of strong dollar/weak yen, weak yuan, is massive. And I used to fight them, you know, they wanted it weak all the time. . . . . That’s a tremendous burden on our companies that try and sell tractors and other things to other places outside of this country. It’s a tremendous burden . . . I think you’re going to see some very bad things happen in a little while. I’ve been talking to manufacturers, they say we cannot get, nobody wants to buy our product because it’s too expensive.

Sure, Scott Bessent — a possible pick for a Republican administration Treasury Secretary — has insisted that Trump wants the dollar to keep its reserve status. Indeed, Trump has vowed 100 per cent tariffs on countries that shun the dollar in international trade.

But Republican vice-president candidate JD Vance seems to have Trump’s ear, and he has repeatedly argued that the negatives of the US currency’s reserve status outweigh the positives. Here he is questioning Fed chair Jay Powell last year:

Advertisement

This isn’t a policy he has flip-flopped on either. As Vance told Politico earlier this year: “‘Devaluing’ of course is a scary word, but what it really means is American exports become cheaper.”

Investors have generally discounted this rhetoric, on the view that presidents can jawbone currencies as much as they like but markets will do what markets will do. However, Trump now looks set to have won re-election with popular mandate and a Republican majority in at least the Senate, opening the possibility for more forceful action.

So here is FTAV’s guide on how the US can devalue the dollar if he really really wanted to.

Severe fiscal retrenchment (no, really!)

Reining in America’s yawning budget deficit would probably be the most orthodox of the radical options available to the Trump administration. It would weigh on economic growth, dampen inflation, send interest rates downward and thus weigh on the dollar.

Advertisement

As Barclays’ FX analysts Lefteris Farmakis and Themistoklis Fiotakis wrote in a September report on how Trump might engineer a dollar debasement:

Prima facie fiscal retrenchment is not about the dollar. If anything, it is the ‘responsible’ economic policy that the Fed, IMF and most international organisations deem necessary for the US following eight years of extraordinarily loose fiscal policy and mounting government debt.

However, fiscal tightening has direct implications for the dollar via slower economic growth, lower interest rates, and less favourable capital flows. Accordingly, it deserves to be included in the list of weak dollar policy options.

And various Trump hangers-on — like Vivek Ramaswamy and Elon Musk — have advocated for swingeing cuts to the size of the US government. The scale of what they’ve advocated would probably produce a swift recession.

However, nothing about Trump’s business career, his first term or his latest presidential election campaign indicate that he is suddenly about to become a paragon of fiscal rectitude.

Advertisement

When the Committee for a Responsible Federal Budget scored the policy proposals of Kamala Harris and Trump, it found that the latter would probably increase US government debt by $7.75tn by 2035 — twice what Harris’s budget would do.

So if we want realistic crazytown options, this is probably not it.

Tariffs and taxes and subsidies, oh my

Another more obvious way to affect the dollar’s value is to address America’s current account balance by fiddling around with levies on imports, subsidies for exports or even taxing overseas investments.

Tariffs have naturally received most of the attention, given Trump’s frequently-stated love for them (although he still doesn’t seem to grasp who actually pays them)

Here’s what Chris Marsh and Jens Nordvig of Exante Data wrote earlier this week on possible outcomes and scenarios:

Advertisement

Goods balance: imports. Lowering imports through tariffs intended to reduce demand for foreign traded goods while improving the competitiveness of domestic producers who may be able to fill the demand. Crucially, such a tariff is like a tax on US consumers, contributing to government revenues while reducing real incomes — this lowers domestic demand while increasing saving, thus current account adjustment. Foreign economies may try to lower their nominal exchange rate against USD to raise domestic currency incomes of exporters to offset some loss of export volumes, so having second or third round effects globally.

Goods balance: exports. Alternatively, boosting exports through subsidies to domestic producers to lower the price to foreigners of US output. This will contribute to higher fiscal deficit in the US which may be offset by higher private saving. So the impact on the current account is ambiguous. Alternatively, de-regulation of closed sectors (such as in energy) opens up competitive US markets to foreign consumers with less fiscal impact — raising domestic incomes and saving.

Service balance: Though net services run a surplus, efforts to improve net tourism or financial services through tax incentives is possible.

Primary income balance: a tax on foreign investment income (Treasury coupons) would generate fiscal revenue and contribute to a lowering external balance assuming no retaliation on US investment income abroad.

Such analysis is inevitably partial equilibrium as, to work out the ultimate impact on the current account and therefore currency of such actions, it is necessary to work through the final impact on incomes and expenditures of US residents as well as foreigners. For example, a tariff on imports will initially lower US real incomes. But this could trigger wage claims to offset lost income, require tighter monetary policy as a result, driving a stronger dollar alongside restored real incomes.

Advertisement

Tl;dr the impact isn’t as clear-cut as you might think, given the first, second and third derivatives of the various measures. Of course, that might not be enough to deter a Trump administration keener on action than analysis.

Occupy the Fed

Trump has never been a big fan of the Federal Reserve, frequently railing against its interest rate increases in his first term and making it clear that he’d replace Jay Powell when his term as chair ends in 2026. And if Trump really wants to debase the dollar, then occupying the Fed is an obvious way to do so.

The low-key way would simply be to gradually pack the Federal Reserve’s board with vaguely-credible (so they can get confirmed) but ultra-dovish members that will toe Trump’s low-interest-rate line.

Although controversial, this isn’t actually enormously different from what several presidents have done in the past. The point would be to ensure that interest rates stay lower than they really should, and that even a moderate erosion of the Fed’s independence and credibility would might spook international investors and dampen demand for US assets.

Advertisement

However, Trump could go far beyond what any of his predecessors have done. Given the US Supreme Court’s leanings, it might also be possible for Trump to actively eject sitting governors before their term ends, quickly stamping his mark on the institution.

As JPMorgan’s Michael Feroli has observed:

. . . There is some uncertainty as to whether the president can remove a Fed governor from their position as chair or vice chair. However, most legal scholars believe that even the current Supreme Court — which is often seen as favorably inclined toward executive authority — would respect the “for cause” limitation on the president’s authority to remove a sitting governor.

The administration and its potentates on the Fed board could then supercharge any damage inflicted on the dollar by halting the central bank’s balance sheet shrinkage and restarting a quantitative easing programme to contain the inevitable hit on long-term bonds.

As Farmakis and Fiotakis at Barclays wrote:

Advertisement

A scenario in which the Fed ends up accommodating yet more fiscal expansion in the absence of a negative output gap — per Trump’s proposed policies — could end up stoking inflation (and putting the stability of expectations at risk). This, in turn, would likely weigh on the dollar, but also keep borrowing costs elevated for much longer, in classic fiscal dominance fashion. What is more, any attempt by the Fed to contain long-term yields via a fresh round of QE would probably only serve to weaken the dollar even more severely.

Of course, all this isn’t costless either. Aggressive monetary easing would probably stir up inflation a bit, and even Trump can’t be blind to the fact that inflation is a major reason why he will soon be back in the White House.

But the Fed is almost certainly in for a bumpy ride, and the idea that Trump will be afraid of more radical action seems . . . optimistic.

A Mar-a-Lago Accord

The favoured approach by the dwindling number of American multilateralists would be something like the Plaza Accord of 1985, when the US browbeat its major trading partners into helping engineer a dollar devaluation.

This worked wonders at the time, with the DXY dollar index nearly halving from its 1985 peak by the end of the decade.

Advertisement

Naturally, analysts have dubbed a potential sequel “Mar-a-Lago Accord”, after Trump’s Florida abode. Marsh and Nordvig think this is the most viable solution:

The set-up is similar to today in that there is a wide fiscal deficit (so low US saving) with the potential for trading partners to acknowledge the need for nominal exchange rate adjustment under pressure of tariffs.

Such coordinated policy includes a fiscal consolidation by the US (raising domestic saving) associated with a managed appreciation of the currencies of trading partners. Today, this could include measures by China to improve transfers to households and support domestic demand.

Unlike the above, this approach has the benefit of being general equilibrium and simultaneously working on spending and income decisions in the US and trading partners, intended to switch spending patterns while sustaining overall demand.

The problem of course is that this is not the 1980s, when almost every country was suffering from a long and persistent bout of inflation that the strength of the dollar was clearly exacerbating.

And as you can see from the chart above, the dollar’s strength versus its main international peers was far more extreme and out of sync with the economic fundamentals in the 1980s than it is today. Most analysts today reckon the dollar is pretty fairly valued, given the strength of the US economy.

Advertisement

Moreover, a crucial component of the Plaza Accord was the US agreeing to get its fiscal house in order — which Trump is unlikely to do. Nor are China, Europe, Japan or other countries likely to be receptive to an engineered dollar devaluation, given how crucial trade is to their economies. They might be more willing to swallow the tariffs, Barclays notes:

In the 1980s, manufacturing accounted for as large a share of the US economy as in Germany and Japan today, while in China, it is as large today as Japan’s and Germany’s in the 1980s. Absent the inflationary cost and given domestic deleveraging policies in Europe and China, the bar is arguably higher for them to agree to coordinated dollar depreciation. Indicatively, trade has been a key source of growth in the eurozone in the past two years

Direct, aggressive and unilateral FX intervention

Now we’re cooking with gas.

The US actually has something called the Exchange Stabilization Fund, controlled by the US Treasury Secretary, who has “considerable discretion” in the use of its $211bn of assets to intervene in exchange rates.

The problem is that the ESF is puny compared to the size of the FX markets. Japan alone has $1.3tn of foreign currency reserves. The ESF could issue government bonds and use the extra firepower to buy foreign currencies, but this debt would naturally fall on the sovereign balance sheet, and thus face the old Congressional debt ceiling issue.

Advertisement

However, if the Trump administration enjoys de facto control over the House and installs a bevy of supine Federal Reserve governors, you could see many possible levers that they might push and pull. After all, engineering a currency devaluation is a lot easier than an appreciation — it just requires you to issue enough currency. A Fed brought to heel could do so.

This is obviously not without many complications — practical, political, legal and technical — but for Trump the optical benefit might also be to build a “sovereign wealth fund” in the process.

The Swiss National Bank’s assets ballooned from SFr85bn at the end 2007 to over SFr1tn by the end of 2021 — invested in everything from gold and German bonds to US equities — as it fought the Swiss franc’s appreciation.

Could this happen? These days, what can’t happen? ¯_ (ツ)_/¯

You must be logged in to post a comment Login