CryptoCurrency

2 Top Electric Vehicle (EV) Stocks to Buy in October

Want to add massive long-term growth potential to your portfolio? Check out electric car stocks.

Many EV makers have seen their sales skyrocket in recent years. Yet their stock prices haven’t always followed suit, creating several compelling buying opportunities over the years. This month looks like an especially great time to jump in.

If you want to buy into the world’s adoption of EVs — a story that is truly a multi-decade growth opportunity — then these two stocks are for you. One you’ve likely heard of. But the other is a diamond in the rough.

Don’t be shy about buying shares in Tesla

Perhaps the most popular EV maker in the world is Tesla (NASDAQ: TSLA). Its boisterous CEO, Elon Musk, is constantly making the news. And with nearly $100 billion in sales, Tesla dominates the EV industry of several major markets, the U.S. included.

You’re likely already familiar with the company’s lineup. Tesla offers premium models like the Roadster, Model X, Cybertruck, and the Model S. But it also offers a few mass-market vehicles. These are typically vehicles under the $50,000 price mark, a common benchmark for gleaning whether a car or truck will be accessible to the masses.

While Tesla does have exposure to other markets like energy generation and storage, more than 90% of its revenue is still tied to its EV business. And while its luxury models helped put it on the map, it really was its two mass-market models — the Model Y and Model 3 — that helped Tesla’s sales grow by more than 1,000% over the past decade. After all, the volumes that can be achieved through a $50,000 car are perhaps an order of magnitude higher than what can be achieved with a $100,000 car.

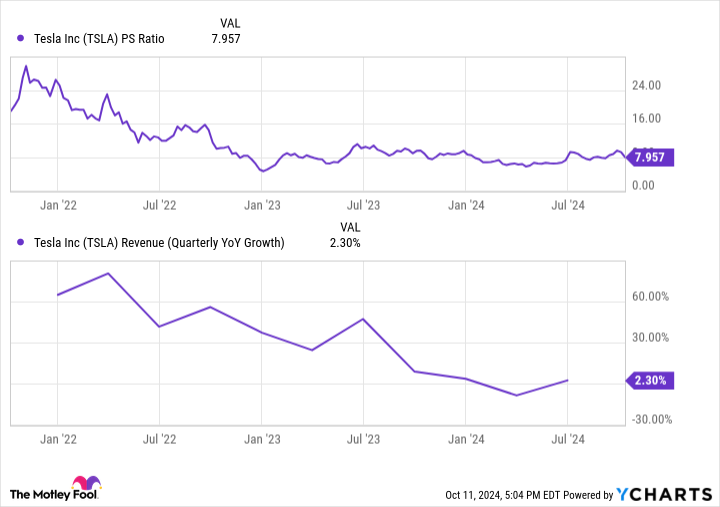

Due to weaker-than-expected sales growth this year for the EV industry, the stocks of most EV producers have suffered. Tesla hasn’t been immune to these pressures, but its valuation still doesn’t look like an obvious bargain. Shares currently trade at 7.9 times sales — roughly what they traded for nearly two years ago, when quarterly sales growth was around 30%.

But a bet on Tesla today isn’t about the near term — it’s about the multidecade growth trajectory for EVs in general. The IEA forecasts EV demand to grow by double digits for decades to come. And Tesla has what most EV start-ups only dream of: access to capital.

So while the stock isn’t as big of a bargain as the next stock on this list, Tesla is still a reasonable investment for those looking to bet on EV companies with the best chance of riding the long-term EV adoption wave.

This EV stock looks like a hidden gem

Want to invest in the next Tesla? Look no further than Rivian (NASDAQ: RIVN). The EV maker might not have the brand-name recognition of Tesla right now, but in the coming years, that could change quickly.

The company expects to release its first mass-market vehicles — the R2, R3, and R3X — beginning in 2026. And if Tesla is any indication, sales could quickly rise by 1,000% more in the years that follow.

Despite this impending sales ramp, Rivian shares trade at a steep discount to Tesla on a price-to-sales basis. What’s going on?

As a smaller competitor with a sales base of just $5 billion, the market is understandably skeptical that Rivian can execute on its sales ramp. While Tesla is a success story, there have been many more bankruptcies in the EV space than successes. Rivian not only needs to raise billions in additional capital to support its launch plans, but also to scale up manufacturing capabilities greater than any other time in its history. And then, of course, it needs to produce cars that people love at a price point they can afford.

Due to these concerns, Rivian shares have fallen by roughly 55% in 2024, versus a much lesser 12% decline for Tesla shares. This has created a great buying opportunity this month for investors willing to take on extra risk in exchange for the high potential returns involved in identifying the next big EV brand.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

-

Amazon: if you invested $1,000 when we doubled down in 2010, you’d have $21,266!*

-

Apple: if you invested $1,000 when we doubled down in 2008, you’d have $43,047!*

-

Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $389,794!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of October 7, 2024

Ryan Vanzo has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Tesla. The Motley Fool has a disclosure policy.

2 Top Electric Vehicle (EV) Stocks to Buy in October was originally published by The Motley Fool

It’s no secret that tech stocks have been powering the market gains over the past few years, and software stocks were among the biggest drivers of this growth.

Multiple factors are propelling the software industry forward, such as the rapid advancement of AI technology, high demand for IT solutions, and the ongoing expansion of the global digital economy.

Wedbush tech expert Daniel Ives has been watching the tech industry, and his take on it points to continued strength supported by AI and cloud expansion.

“Solid enterprise spending, digital advertising rebound, and the AI Revolution will drive tech stocks higher into year-end in our view,” Ives opined. “We believe 70% of global workloads will be on the cloud by the end of 2025, up from less than 50% today.”

Keeping that in mind, Ives goes on to add that the time has come to hit buy on two software stocks. They may not be household names, but according to the TipRanks data, both stocks are Buy-rated – and Ives sees significantly more upside to each than the consensus on the Street. Let’s take a closer look.

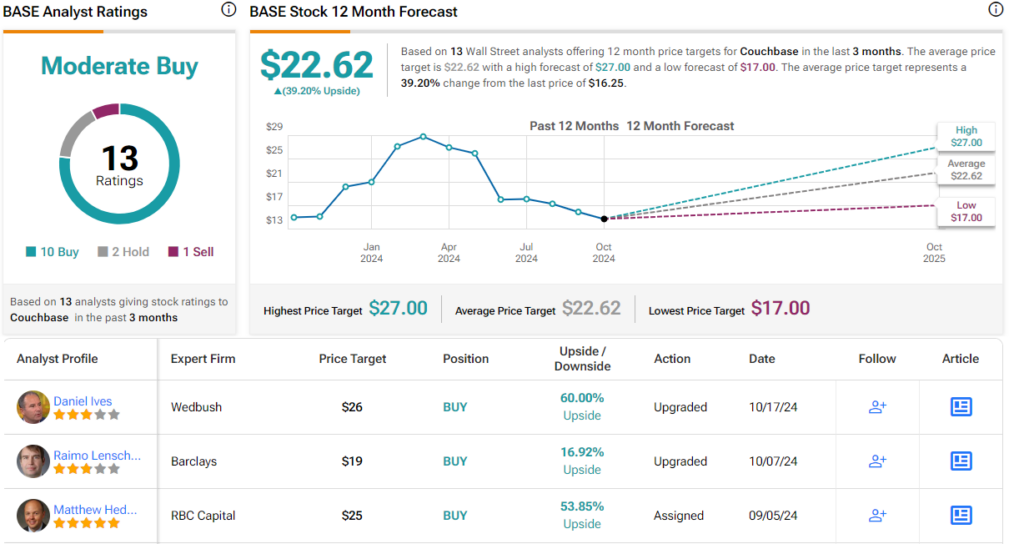

Couchbase (BASE)

We’ll start with Couchbase, a modern database platform provider that offers users and developers everything they need to support a wide range of applications – from cloud, to edge, to AI. Couchbase bills itself as a one-stop-shop for data developers and architects, making its services available through its powerful database-as-a-service platform, Capella. Organizations using the service can quickly create applications and services that deliver premium customer experiences, giving top-end performance at affordable prices.

The Capella platform brings the popular as-a-service subscription model to the database industry. The company can support database services for a wide range of AI applications, including the latest gen-AI tech, as well as database search, mobile access, and analytic functions. Customers can also choose self-managed services through Couchbase’s servers, with on-premises management for both multicloud and community apps.

Couchbase’s database service has found success in a wide range of fields, including the gaming, healthcare, entertainment, retail, travel, and utility sectors. The company’s customer base includes such major names as Verizon, UPS, Walmart, Cisco, Comcast, GE, and PayPal.

Turning to the financial results, we see that Couchbase reported its fiscal 2Q25 figures at the start of last month. The top line of $51.6 million was up almost 20% year-over-year and came in just over the forecast, beating expectations by nearly a half-million dollars. At the bottom line, the company ran a net loss of 6 cents per share in non-GAAP measures, but that was 3 cents per share better than had been anticipated.

Ripple challenges SEC’s ruling on institutional XRP sales, claiming the Howey test was misapplied.

BTC price trajectory appears all but destined for six figures in the mid term — despite nearly eight months of Bitcoin market consolidation.

2024 is turning out to be a solid year for the global semiconductor industry, driven by multiple catalysts. These include the booming demand for chips that can manage artificial intelligence (AI) workloads, a turnaround in the smartphone market’s fortunes, and a recovery in the personal computer (PC) market.

These factors explain why the global semiconductor industry’s revenue is expected to jump 16% in 2024 to $611.2 billion, according to World Semiconductor Trade Statistics (WSTS). That points toward a nice turnaround from last year, when the semiconductor industry’s revenue fell 8%. Even better, the semiconductor space is expected to keep growing in 2025 as well, with WSTS projecting a 12.5% increase in the industry’s earnings to $687.4 billion next year.

More specifically, WSTS predicts a whopping 25% increase in the memory market’s revenue in 2025 to $204.3 billion. As it turns out, memory is expected to be the fastest-growing semiconductor segment next year as well, following an estimated jump of almost 77% in this segment’s revenue in 2024.

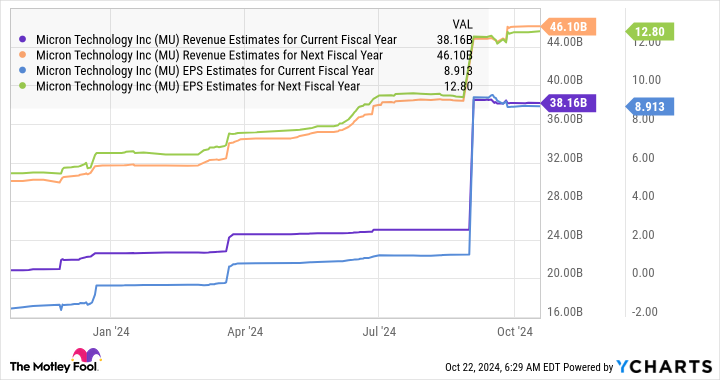

There’s one company that could help investors tap this fast-growing niche of the semiconductor market next year: Micron Technology (NASDAQ: MU). Let’s look at the reasons why buying this semiconductor stock could turn out to be a smart move right now.

WSTS isn’t the only forecaster expecting the memory market to surge higher next year. Market research firm TrendForce estimates that the sales of dynamic random access memory (DRAM) could jump 51% in 2025, while the NAND flash storage market could clock 29% growth. Both these markets are expected to reach record highs next year.

The growth in these memory markets will be driven by a combination of strong demand and improved pricing. TrendForce is forecasting a 35% year-over-year increase in DRAM prices next year, driven by the increasing demand for high-bandwidth memory (HBM) that’s used in AI processors, as well as the growth in DRAM deployed in servers. Meanwhile, the growing demand for enterprise-class solid-state drives (SSDs) and the growth in smartphone storage will be tailwinds for the NAND flash market.

These positive trends explain why Micron is set to begin its new fiscal year on a bright note. The company’s revenue in fiscal 2024 (which ended on Aug. 29) increased 61% year over year to $25.1 billion. The company posted a non-GAAP (generally accepted accounting principles) profit of $1.30 per share, compared to a loss of $4.45 per share in fiscal 2023, driven by a big jump in its operating margin on account of recovering memory prices.

Cardano Foundation chief technology officer Giorgio Zinetti told Cointelegraph that centralized authority is good for speed, but decentralized governance would give long-term sustainability.

Tech pioneer Intel (INTC) has seemingly missed out on the artificial intelligence boom — and part of it can reportedly be traced back to a decision not to buy the chipmaker at the center of it all almost two decades ago.

Intel’s former chief executive Paul Otellini wanted to buy Nvidia in 2005 when the chipmaker was mostly known for making computer graphics chips, which some executives thought had potential for data centers, The New York Times (NYT) reported, citing unnamed people familiar with the matter. However, Intel’s board did not approve of the $20 billion acquisition — which would’ve been the company’s most expensive yet — and Otellini dropped the effort, according to The New York Times.

Instead, the board was reportedly more interested in an in-house graphics project called Larrabee, which was led by now-chief executive Pat Gelsinger.

Almost two decades later, Nvidia (NVDA) has become the second-most valuable public company in the world and continuously exceeds Wall Street’s high expectations. Intel, on the other hand, has seen its shares fall around 53% so far this year and is now worth less than $100 billion — around 30 times less than Nvidia’s $3.4 trillion market cap.

In August, Intel shares fell 27% after it missed revenue expectations with its second-quarter earnings and announced layoffs. The company missed profit expectations partly due to its decision to “more quickly ramp” its Core Ultra artificial intelligence CPUs, or core processing units, that can handle AI applications, Gelsinger said on the company’s earnings call.

And Nvidia wasn’t the only AI darling Intel missed out on.

Over a decade after passing on Nvidia, Intel made another strategic miss by reportedly deciding not to buy a stake in OpenAI, which had not yet kicked off the current AI hype with the release of ChatGPT in November 2022.

Former Intel chief executive Bob Swan didn’t think OpenAI’s generative AI models would come to market soon enough for the investment to be worth it, Reuters reported, citing unnamed people familiar with the matter. The AI startup had been interested in Intel, sources told Reuters (TRI), so it could depend less on Nvidia and build its own infrastructure.

-

Technology1 month ago

Technology1 month agoIs sharing your smartphone PIN part of a healthy relationship?

-

Science & Environment1 month ago

Science & Environment1 month agoHow to unsnarl a tangle of threads, according to physics

-

Science & Environment1 month ago

Science & Environment1 month agoHyperelastic gel is one of the stretchiest materials known to science

-

Science & Environment1 month ago

Science & Environment1 month ago‘Running of the bulls’ festival crowds move like charged particles

-

Science & Environment1 month ago

Science & Environment1 month agoMaxwell’s demon charges quantum batteries inside of a quantum computer

-

Technology1 month ago

Technology1 month agoWould-be reality TV contestants ‘not looking real’

-

Science & Environment1 month ago

Science & Environment1 month agoX-rays reveal half-billion-year-old insect ancestor

-

Science & Environment1 month ago

Science & Environment1 month agoSunlight-trapping device can generate temperatures over 1000°C

-

Technology4 weeks ago

Technology4 weeks agoUkraine is using AI to manage the removal of Russian landmines

-

Science & Environment1 month ago

Science & Environment1 month agoLiquid crystals could improve quantum communication devices

-

Science & Environment1 month ago

Science & Environment1 month agoQuantum ‘supersolid’ matter stirred using magnets

-

Science & Environment1 month ago

Science & Environment1 month agoLaser helps turn an electron into a coil of mass and charge

-

TV3 weeks ago

TV3 weeks agoসারাদেশে দিনব্যাপী বৃষ্টির পূর্বাভাস; সমুদ্রবন্দরে ৩ নম্বর সংকেত | Weather Today | Jamuna TV

-

Technology3 weeks ago

Technology3 weeks agoSamsung Passkeys will work with Samsung’s smart home devices

-

News3 weeks ago

News3 weeks agoMassive blasts in Beirut after renewed Israeli air strikes

-

Sport3 weeks ago

Sport3 weeks agoBoxing: World champion Nick Ball set for Liverpool homecoming against Ronny Rios

-

Science & Environment1 month ago

Science & Environment1 month agoPhysicists have worked out how to melt any material

-

Science & Environment1 month ago

Science & Environment1 month agoA new kind of experiment at the Large Hadron Collider could unravel quantum reality

-

Football4 weeks ago

Football4 weeks agoRangers & Celtic ready for first SWPL derby showdown

-

News3 weeks ago

News3 weeks agoNavigating the News Void: Opportunities for Revitalization

-

News3 weeks ago

News3 weeks ago▶ Hamas Spent $1B on Tunnels Instead of Investing in a Future for Gaza’s People

-

News3 weeks ago

News3 weeks ago‘Blacks for Trump’ and Pennsylvania progressives play for undecided voters

-

MMA3 weeks ago

MMA3 weeks ago‘Uncrowned queen’ Kayla Harrison tastes blood, wants UFC title run

-

Womens Workouts1 month ago

Womens Workouts1 month ago3 Day Full Body Women’s Dumbbell Only Workout

-

Football3 weeks ago

Football3 weeks agoWhy does Prince William support Aston Villa?

-

MMA3 weeks ago

MMA3 weeks agoPereira vs. Rountree prediction: Champ chases legend status

-

Business3 weeks ago

Business3 weeks agoWhen to tip and when not to tip

-

Sport3 weeks ago

Sport3 weeks agoAaron Ramsdale: Southampton goalkeeper left Arsenal for more game time

-

Technology4 weeks ago

Technology4 weeks agoMicrophone made of atom-thick graphene could be used in smartphones

-

MMA4 weeks ago

MMA4 weeks agoDana White’s Contender Series 74 recap, analysis, winner grades

-

Technology3 weeks ago

Technology3 weeks agoGmail gets redesigned summary cards with more data & features

-

Sport3 weeks ago

Sport3 weeks agoWales fall to second loss of WXV against Italy

-

Science & Environment1 month ago

Science & Environment1 month agoWhy this is a golden age for life to thrive across the universe

-

Technology4 weeks ago

Technology4 weeks agoRussia is building ground-based kamikaze robots out of old hoverboards

-

Business4 weeks ago

DoJ accuses Donald Trump of ‘private criminal effort’ to overturn 2020 election

-

Technology3 weeks ago

Technology3 weeks agoMusk faces SEC questions over X takeover

-

Sport3 weeks ago

Sport3 weeks agoMan City ask for Premier League season to be DELAYED as Pep Guardiola escalates fixture pile-up row

-

Technology4 weeks ago

Technology4 weeks agoEpic Games CEO Tim Sweeney renews blast at ‘gatekeeper’ platform owners

-

News3 weeks ago

News3 weeks agoWoman who died of cancer ‘was misdiagnosed on phone call with GP’

-

MMA3 weeks ago

MMA3 weeks agoKetlen Vieira vs. Kayla Harrison pick, start time, odds: UFC 307

-

Science & Environment1 month ago

Science & Environment1 month agoQuantum forces used to automatically assemble tiny device

-

Science & Environment1 month ago

Science & Environment1 month agoITER: Is the world’s biggest fusion experiment dead after new delay to 2035?

-

Science & Environment1 month ago

Science & Environment1 month agoA slight curve helps rocks make the biggest splash

-

News1 month ago

News1 month ago▶️ Hamas in the West Bank: Rising Support and Deadly Attacks You Might Not Know About

-

Technology1 month ago

Technology1 month agoMeta has a major opportunity to win the AI hardware race

-

Technology1 month ago

Technology1 month agoWhy Machines Learn: A clever primer makes sense of what makes AI possible

-

Science & Environment1 month ago

Science & Environment1 month agoNerve fibres in the brain could generate quantum entanglement

-

Science & Environment1 month ago

Science & Environment1 month agoNuclear fusion experiment overcomes two key operating hurdles

-

Technology4 weeks ago

Technology4 weeks agoThis AI video generator can melt, crush, blow up, or turn anything into cake

-

Technology3 weeks ago

Technology3 weeks agoMicrosoft just dropped Drasi, and it could change how we handle big data

-

Sport4 weeks ago

Sport4 weeks agoSturm Graz: How Austrians ended Red Bull’s title dominance

-

Money3 weeks ago

Money3 weeks agoWetherspoons issues update on closures – see the full list of five still at risk and 26 gone for good

-

News3 weeks ago

News3 weeks agoFamily plans to honor hurricane victim using logs from fallen tree that killed him

-

Sport3 weeks ago

Sport3 weeks ago2024 ICC Women’s T20 World Cup: Pakistan beat Sri Lanka

-

Entertainment3 weeks ago

Entertainment3 weeks agoNew documentary explores actor Christopher Reeve’s life and legacy

-

MMA4 weeks ago

MMA4 weeks agoJulianna Peña trashes Raquel Pennington’s behavior as champ

-

Business3 weeks ago

Sterling slides after Bailey says BoE could be ‘a bit more aggressive’ on rates

-

MMA3 weeks ago

MMA3 weeks ago‘I was fighting on automatic pilot’ at UFC 306

-

Sport4 weeks ago

Sport4 weeks agoChina Open: Carlos Alcaraz recovers to beat Jannik Sinner in dramatic final

-

Technology3 weeks ago

Technology3 weeks agoThe best budget robot vacuums for 2024

-

Sport3 weeks ago

Sport3 weeks agoCoco Gauff stages superb comeback to reach China Open final

-

Science & Environment1 month ago

Science & Environment1 month agoTime travel sci-fi novel is a rip-roaringly good thought experiment

-

Science & Environment1 month ago

Science & Environment1 month agoHow to wrap your mind around the real multiverse

-

News1 month ago

News1 month ago▶️ Media Bias: How They Spin Attack on Hezbollah and Ignore the Reality

-

Business4 weeks ago

Business4 weeks agoChancellor Rachel Reeves says she needs to raise £20bn. How might she do it?

-

Technology3 weeks ago

Technology3 weeks agoTexas is suing TikTok for allegedly violating its new child privacy law

-

Business3 weeks ago

The search for Japan’s ‘lost’ art

-

Business4 weeks ago

Bank of England warns of ‘future stress’ from hedge fund bets against US Treasuries

-

News3 weeks ago

News3 weeks agoGerman Car Company Declares Bankruptcy – 200 Employees Lose Their Jobs

-

MMA3 weeks ago

MMA3 weeks agoKayla Harrison gets involved in nasty war of words with Julianna Pena and Ketlen Vieira

-

MMA3 weeks ago

MMA3 weeks agoUFC 307 preview show: Will Alex Pereira’s wild ride continue, or does Khalil Rountree shock the world?

-

Business3 weeks ago

Head of UK Competition Appeal Tribunal to step down after rebuke for serious misconduct

-

MMA3 weeks ago

MMA3 weeks agoPereira vs. Rountree preview show live stream

-

Technology3 weeks ago

Technology3 weeks agoThe best shows on Max (formerly HBO Max) right now

-

Technology3 weeks ago

Technology3 weeks agoIf you’ve ever considered smart glasses, this Amazon deal is for you

-

Business4 weeks ago

Business4 weeks agoStocks Tumble in Japan After Party’s Election of New Prime Minister

-

Sport4 weeks ago

Sport4 weeks agoWorld’s sexiest referee Claudia Romani shows off incredible figure in animal print bikini on South Beach

-

Science & Environment4 weeks ago

Science & Environment4 weeks agoMarkets watch for dangers of further escalation

-

Technology3 weeks ago

Technology3 weeks agoJ.B. Hunt and UP.Labs launch venture lab to build logistics startups

-

News3 weeks ago

News3 weeks agoCornell is about to deport a student over Palestine activism

-

News3 weeks ago

News3 weeks agoHull KR 10-8 Warrington Wolves – Robins reach first Super League Grand Final

-

Technology3 weeks ago

Technology3 weeks agoOpenAI secured more billions, but there’s still capital left for other startups

-

Health & fitness3 weeks ago

Health & fitness3 weeks agoNHS surgeon who couldn’t find his scalpel cut patient’s chest open with the penknife he used to slice up his lunch

-

Business3 weeks ago

Business3 weeks agoStark difference in UK and Ireland’s budgets

-

MMA4 weeks ago

MMA4 weeks agoAlex Pereira faces ‘trap game’ vs. Khalil Rountree

-

Football4 weeks ago

Football4 weeks agoSimo Valakari: New St Johnstone boss says Scotland special in his heart

-

Technology3 weeks ago

Technology3 weeks agoCheck, Remote, and Gusto discuss the future of work at Disrupt 2024

-

Politics3 weeks ago

Rosie Duffield’s savage departure raises difficult questions for Keir Starmer. He’d be foolish to ignore them | Gaby Hinsliff

-

Money3 weeks ago

Money3 weeks agoPub selling Britain’s ‘CHEAPEST’ pints for just £2.60 – but you’ll have to follow super-strict rules to get in

-

TV3 weeks ago

TV3 weeks agoLove Island star sparks feud rumours as one Islander is missing from glam girls’ night

-

News1 month ago

News1 month agoOur millionaire neighbour blocks us from using public footpath & screams at us in street.. it’s like living in a WARZONE – WordupNews

-

News1 month ago

the pick of new debut fiction

-

News4 weeks ago

News4 weeks agoRwanda restricts funeral sizes following outbreak

-

Technology3 weeks ago

Technology3 weeks agoApple iPhone 16 Plus vs Samsung Galaxy S24+

-

News3 weeks ago

News3 weeks agoBalancing India and China Is the Challenge for Sri Lanka’s Dissanayake

-

MMA4 weeks ago

MMA4 weeks agoHow to watch Salt Lake City title fights, lineup, odds, more

-

Business4 weeks ago

how UniCredit built its Commerzbank stake

-

News4 weeks ago

News4 weeks agoLiverpool secure win over Bologna on a night that shows this format might work

-

TV4 weeks ago

TV4 weeks agoPhillip Schofield accidentally sets his camp on FIRE after using emergency radio to Channel 5 crew

-

Business3 weeks ago

Business3 weeks agoWater companies ‘failing to address customers’ concerns’

You must be logged in to post a comment Login