CryptoCurrency

2 Unstoppable Growth Stocks Each Up More Than 600% in 8 Years to Buy Now, According to Wall Street

When a company decides to split its stock, it doesn’t change any of the underlying fundamentals or value of the business. Nonetheless, it usually follows significant share-price appreciation, and it signals confidence from management that the future will see the stock continue to rise. As such, many investors flock to stocks when they announce forward stock splits as well as shortly after the splits occur.

This suggests investors may do well to take a look at companies that have the potential to be stock-split candidates. These companies still have plenty of upside left and a stock split could attract a lot more investor attention. Getting in before the stock split could work out nicely, even for long-term investors who are less concerned about timing a stock purchase. Even if these stocks never split their shares again, Wall Street still sees good upside for each.

Both Microsoft (NASDAQ: MSFT) and ASML Holdings (NASDAQ: ASML) have seen their share prices soar more than 600% over the past eight years. That’s the kind of price appreciation that often leads to stock splits, especially since neither stock was starting from a small base. Meanwhile, the average analyst on Wall Street still sees significant upside for both.

1. Microsoft: Up 622% from October 2016

Microsoft made an early bet on generative artificial intelligence (AI) leader OpenAI and sizably increased that bet in early 2023 with an extra $10 billion investment. As a result, Microsoft’s Azure cloud computing platform has become the first stop for developers looking to build on top of large language models like GPT-4o. Not only that, but Microsoft’s integrated generative AI capabilities across its various software platforms, including Github, Dynamics 365, Office 365, and the Power platform.

Its efforts have driven incredible results. Azure revenue climbed 30% in the fourth quarter. What’s more, management expects Azure results to accelerate in the second half of fiscal 2025 as its massive investments in new data center capacity come online.

Microsoft is also seeing strong uptake on its Copilot software, an AI-powered assistant that can help workers accomplish tasks more efficiently and effectively. Copilot customers for Microsoft 365 grew more than 60% sequentially in the fourth quarter. With over 400 million Office 365 users, Microsoft has a long runway for continued growth. Not to mention, the number of users continues to grow, as Microsoft dominates the workplace productivity software space.

The average price target among Wall Street analysts is $496, which implies about 19% upside for the tech giant’s stock. At its current price, shares trade around 32 times forward earnings estimates. Considering the growth drivers pushing Microsoft’s operating results and its competitive position, that high multiple is well worth paying for investors looking at growth stocks. Even at its massive size, Microsoft is growing quickly.

While shares have backed off of their all-time high price, they still trade well above $400. A split at this price is a reasonable maneuver for the third-highest-priced Dow component.

2. ASML Holdings: Up 694% from October 2016

ASML has also been a beneficiary of the booming demand for artificial intelligence. Its extreme ultraviolet (EUV) lithography machines are essential hardware for printing the most advanced semiconductors in the market. ASML is the only company supplying those machines.

As companies like Microsoft and other hyper scalers build out massive data centers full of silicon, ASML stands to see the benefits over the long run. It’s important to note that chip manufacturers, known as foundries, can’t just expand their operations overnight. There are long lead times for ASML’s massive machines: Not only do they need to take delivery and install them, they also need the space in the first place.

As such, ASML’s management has called 2024 a transition year. It expects flat revenue and gross margin contraction as it ramps up production of its newest machinery for delivery in 2025. But 2025 should be a big year for the company. It expects 30 billion to 40 billion euros ($33.2 billion to $44.2 billion) in revenue, an increase of 27% from 2023 at its midpoint.

In the long term, ASML should see strong growth from unit sales and even better growth from ongoing servicing of its existing install base. In 2022, management forecast 44 billion euros to 60 billion euros ($48.1 billion to $65.6 billion) by 2030 with gross margin expanding to as much as 60% from about 51.5% today. Considering those forecasts preceded the boom in demand for AI chips, investors should expect revenue closer to the high end of that forecast.

The average price target among Wall Street analysts is $1,127, which implies about 33% upside for the stock. With shares trading at about 26 times 2025 earnings estimates, the shares look inexpensive relative to their earnings growth over the next few years. With strong forthcoming sales and expanding margins, analysts expect earnings growth above 20% for the next five years. That makes the stock extremely attractive at this price.

ASML shares are well off their all-time high, but shares trade around $850 each. That’s plenty high enough to justify a stock split, but as shares climb above $1,000 and remain there, it could push the company to split its stock and bring the price back down to the triple-digit territory.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

-

Amazon: if you invested $1,000 when we doubled down in 2010, you’d have $21,266!*

-

Apple: if you invested $1,000 when we doubled down in 2008, you’d have $43,047!*

-

Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $389,794!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of October 7, 2024

Adam Levy has positions in Microsoft. The Motley Fool has positions in and recommends ASML and Microsoft. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Possible Stock Splits in 2025: 2 Unstoppable Growth Stocks Each Up More Than 600% in 8 Years to Buy Now, According to Wall Street was originally published by The Motley Fool

The artificial intelligence (AI) revolution is driving unprecedented demand for energy-intensive data centers. The International Energy Agency projects that data centers may account for up to one-third of the anticipated increase in U.S. electricity demand through 2026.

Major tech companies, like Microsoft, Amazon, and Alphabet, are racing to secure clean energy power sources, such as nuclear energy, to meet their mounting energy needs. One under-the-radar company with established renewable infrastructure is uniquely positioned to capitalize on this accelerating trend.

TeraWulf (NASDAQ: WULF) operates Bitcoin (CRYPTO: BTC) mining facilities powered by approximately 95% zero-carbon energy sources, primarily hydroelectric power. The company’s revenue surged 130% year over year to $35.6 million in the second quarter of 2024, driven by an 80% increase in operational mining capacity and higher Bitcoin prices.

Moreover, TeraWulf has significantly strengthened its financial position by eliminating its debt ahead of schedule. This clean balance sheet positions TeraWulf to fund its ambitious expansion plans in both cryptocurrency mining and AI infrastructure.

TeraWulf is leveraging its existing clean energy infrastructure to enter the high-performance computing and AI market. The company has already completed a 2.5 megawatt (MW) proof-of-concept project designed for next-generation graphics processing unit (GPU) technology.

Additionally, construction is underway on a 20 MW colocation facility engineered to support AI workloads. The facility includes advanced features, like liquid cooling and redundant power systems typical of premium data centers. It is scheduled to kick off operations in Q1 2025, according to the company.

TeraWulf recently secured $425 million through a convertible note offering at a reasonable 2.75% interest rate, reflecting strong institutional investor confidence. The company plans to use these funds for strategic acquisitions and the expansion of data center infrastructure to support its AI computing initiatives.

Furthermore, TeraWulf’s board recently authorized a $200 million share repurchase program through December 2025, signaling management’s belief that the stock may be undervalued despite rising approximately 165% year to date.

TeraWulf’s clean energy resources give it a unique edge in the rapidly growing AI infrastructure market. Major tech companies are actively seeking sustainable power sources for their energy-intensive AI operations, making TeraWulf’s zero-carbon data centers particularly attractive.

I want to become financially independent. My core strategy is to grow my passive income so that it will eventually cover my recurring expenses. To reach that goal, I’m taking a multipronged approach that includes investing in dividend stocks, exchange-traded funds (ETFs), and real estate.

I’m loading up on several dividend ETFs to grow my passive income, including JPMorgan Nasdaq Equity Premium ETF (NASDAQ: JEPQ), SPDR Portfolio High Yield Bond ETF (NYSEMKT: SPHY), and iShares Core U.S. Aggregate Bond ETF (NYSEMKT: AGG). Here’s why I like this trio for passive income.

JPMorgan Nasdaq Equity Premium ETF takes a unique approach to generating income. The fund writes out-of-the-money call options on the Nasdaq-100 Index. That strategy generates options premium income each month that the ETF distributes to investors.

That income has really added up over the past year. The ETF’s dividend yield over the last 12 months is 9.5%. That’s a higher yield than U.S. high-yield junk bonds (7.9%) and the U.S. 10-year Treasury bond (4.4%). However, the payments do ebb and flow based on the options premium income the fund generates, which fluctuates with volatility.

In addition to income, this fund offers price appreciation potential. The ETF also holds a portfolio of stocks the managers select based on data science and fundamental research. The fund’s price rises as that equity portfolio’s value increases. Because of that, the fund offers the best of both worlds: high income and upside potential.

SPDR Portfolio High Yield Bond ETF provides exposure to the high-yield (junk) bond market. These bonds have sub-investment-grade bond ratings because the companies issuing this debt have weaker financial profiles. That puts these bonds at high risk of default.

This fund holds a large basket of these bonds (over 1,900) diversified across sectors, issuers, and maturity. That diversification helps reduce the default risk. If an issuer defaults on its bond, it won’t have a major impact on the ETF. Meanwhile, even if a severe market downturn negatively impacted financially weaker companies, the overall diversification of the fund should help mute the impact on ETF investors.

Investors get paid well to assume the higher risk profile of these bonds. The fund has a distribution yield currently above 7%. While the monthly distribution payments fluctuate based on interest payments received, the fund offers a relatively steady passive income stream.

The iShares Core U.S. Aggregate Bond ETF focuses on the other side of the bond market: investment-grade bonds. These bonds have a lower risk of defaulting, making them ideal for those seeking a very low-risk income stream.

CryptoCurrency

Could Buying This Weight Loss Stock Be Like Investing in Novo Nordisk At The Dawn of The GLP-1 Revolution?

One of the biggest sensations fueling the healthcare space right now is the medication class of glucagon-like peptide-1 (GLP-1) agonists. Even if you aren’t familiar with the term “GLP-1,” you’ve probably heard of Ozempic and Wegovy. Both medications are GLP-1 agonists, used to treat diabetes and obesity, respectively.

These treatments have become blockbuster drugs for their maker, Novo Nordisk, and have helped fuel generous gains for investors in the stock. While Novo Nordisk currently dominates the GLP-1 industry, a number of other players are looking to enter the space.

One leading entrant is Viking Therapeutics (NASDAQ: VKTX). Below, I’ll break down where Viking stands in its pursuit of the weight loss market, and assess whether buying the stock could be like investing in Novo Nordisk at the beginning of the Ozempic revolution.

Viking has several drug candidates in its pipeline. But the one that investors seem most honed in on is VK2735 — a dual GLP-1 and GIP receptor agonist focused on treating obesity. As a dual agonist, VK2735 could wind up being a more optimal treatment for obesity and diabetes than single-pathway GLP-1 medicines such as Ozempic or Wegovy.

In late October, Viking announced that it will be meeting with the Food and Drug Administration (FDA) during the fourth quarter, about the proper steps and protocols to move VK2735 into a phase 3 clinical trial.

Given the information above, you might think buying Viking stock now — prior to phase 3 trials — is a lucrative opportunity. However, there is quite a bit to consider besides anecdotal updates about VK2735.

So far in 2024, shares of Viking have rocketed by a whopping 323% — putting its market cap right around $8.8 billion. Considering that the company doesn’t generate revenue, it’s hard to justify this valuation.

On the bright side, I think Viking is in a pretty solid financial position.

At the end of the third quarter, it boasted $930 million of cash and equivalents on its balance sheet. Furthermore, the company has spent roughly $105 million in operating expenses through the first nine months of the year. This implies an annual run rate of approximately $140 million in spending on research and development (R&D) and other administrative expenses, suggesting that Viking has ample liquidity to continue funding its operations.

I see Viking Therapeutics as largely a speculative opportunity. While data from its clinical trials so far have been encouraging, there are still plenty of unknowns surrounding the phase 3 study.

The prices of Bitcoin and other digital assets were significantly lower during the 2022 collapse of FTX compared to current market prices.

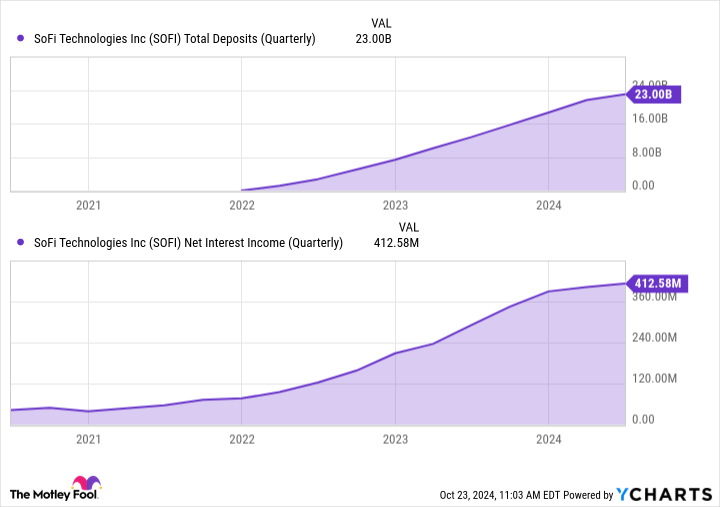

SoFi Technologies (NASDAQ: SOFI) has done an excellent job expanding its customer base and growing revenue. However, it has contended with sluggish loan growth in the high-interest rate environment, leading to investor skepticism about its short-term prospects. As a result, the stock remains 62% below its all-time high price in 2021.

However, the company has found multiple levers for growth and is seeing encouraging progress in its nonconsumer business. If you’re considering buying SoFi today, here’s what you should know.

In its early days, SoFi focused on helping people refinance their student loan debt. Then in 2020, the pandemic and policies around student loan forbearance forced SoFi to reevaluate its business. One area that helped drive its ongoing growth was personal lending. From 2020 to 2023, SoFi’s personal loan originations grew from $2.6 billion to $13.8 billion.

The higher-interest rate environment of the past couple of years has been a double-edged sword for SoFi. On one hand, consumers have had to grapple with higher interest rates, which could make it harder for them to pay down their debts.

In the second quarter, SoFi charged off $151.8 million in personal loans, giving it a charge-off ratio of 3.84% on its $15.9 billion personal loan portfolio. This is up from 2.94% one year ago and is one metric that investors have kept a close eye on. Charge-offs have risen across the banking sector over the past couple of years, which many attribute to normalizing conditions rather than systemic weakness across the consumer.

Additionally, SoFi projects that its lending segment revenue will decline 5% to 8% compared to last year. CEO Anthony Noto told investors during the first quarter that the fintech is taking “a more conservative approach in light of macroeconomic uncertainty.”

Conversely, higher interest rates have helped SoFi grow its net interest income significantly. One big reason for this was its 2022 acquisition of Golden Pacific Bancorp, which enabled SoFi to hold deposits and thus, more loans on its books. Since acquiring the bank, its total deposits have grown to nearly $23 billion, thanks to its high-yielding savings accounts offering an annual yield of up to 4.5%.

Last year, SoFi brought in almost $1.3 billion in net interest income, up over 400% from 2021. This solid growth continued through the first half of this year, with its net interest income increasing 55% to $815 million.

CryptoCurrency

U.S. Banks Sitting on $750 billion In Losses On Real Estate Debt Related Securities-Which Sectors Are Most Exposed?

Benzinga and Yahoo Finance LLC may earn commission or revenue on some items through the links below.

The 2008 financial crisis exposed numerous flaws in America’s financial system, such as the inherent danger of America’s largest banks being overleveraged. Significant dangers remain despite a slate of reforms designed to keep banks on sound financial footing going forward. A recent article in Cryptopolitan magazine revealed that American banks’ potential loss exposure on real estate-related securities skyrocketed to $750 billion in Q3 2024.

Don’t Miss:

This is raising concerns for many reasons. First, the estimated $750 billion is roughly seven times more than banks held in 2008. Second, many unrealized losses are concentrated in portfolios that are crucial to bank profits. The most at-risk portfolios are:

· AFS-Available for sale

· HTM-Held to maturity

One deeply troubling aspect of the potential $750 billion in losses is that so much is tied to residential mortgage-backed securities (RMBS). Banks loaded up on these when interest rates were lower. The easy credit made it easier for banks to acquire larger debt tranches and the underlying assets were also easier to sell. Making such heavy investments in RMBS now threatens to boomerang back on banks and investors in a big way.

Many of those HTM portfolio loans are approaching maturity dates and high interest rates are slowing sales down in the AFS portfolios. That’s why the potential losses are beginning to stack up. Increased financing costs are consuming massive chunks of what used to be profit and Investors are wary of buying RMBS in the current environment.

This decreases the value of bank-held RMBS while increasing the potential losses on the underlying assets. Being upside down on large AFS or HTM portfolios has taken banks down. In 2023, unrealized losses on First Republic Bank’s commercial loan portfolios were a major contributor to the bank’s eventual collapse and takeover by JP Morgan Chase.

See Also: Commercial real estate has historically outperformed the stock market, and this platform allows individuals to invest in commercial real estate with as little as $5,000 offering a 12% target yield with a bonus 1% return boost today!

Banks may have been able to carry these balances in years past, but one of the major reforms instituted after 2008 is making that much more difficult. U.S. banks must submit to periodic “stress tests” where their liquidity is weighed against outstanding debt and liabilities. If those numbers are out of line, the bank could be forced to close or make major markdowns.

-

Technology1 month ago

Technology1 month agoIs sharing your smartphone PIN part of a healthy relationship?

-

Science & Environment1 month ago

Science & Environment1 month agoHow to unsnarl a tangle of threads, according to physics

-

Science & Environment1 month ago

Science & Environment1 month agoHyperelastic gel is one of the stretchiest materials known to science

-

Science & Environment1 month ago

Science & Environment1 month ago‘Running of the bulls’ festival crowds move like charged particles

-

Science & Environment1 month ago

Science & Environment1 month agoMaxwell’s demon charges quantum batteries inside of a quantum computer

-

Technology1 month ago

Technology1 month agoWould-be reality TV contestants ‘not looking real’

-

Science & Environment1 month ago

Science & Environment1 month agoX-rays reveal half-billion-year-old insect ancestor

-

Science & Environment1 month ago

Science & Environment1 month agoSunlight-trapping device can generate temperatures over 1000°C

-

Technology4 weeks ago

Technology4 weeks agoUkraine is using AI to manage the removal of Russian landmines

-

Science & Environment1 month ago

Science & Environment1 month agoLiquid crystals could improve quantum communication devices

-

Science & Environment1 month ago

Science & Environment1 month agoQuantum ‘supersolid’ matter stirred using magnets

-

TV4 weeks ago

TV4 weeks agoসারাদেশে দিনব্যাপী বৃষ্টির পূর্বাভাস; সমুদ্রবন্দরে ৩ নম্বর সংকেত | Weather Today | Jamuna TV

-

Sport3 weeks ago

Sport3 weeks agoBoxing: World champion Nick Ball set for Liverpool homecoming against Ronny Rios

-

Science & Environment1 month ago

Science & Environment1 month agoLaser helps turn an electron into a coil of mass and charge

-

Science & Environment1 month ago

Science & Environment1 month agoPhysicists have worked out how to melt any material

-

Technology3 weeks ago

Technology3 weeks agoSamsung Passkeys will work with Samsung’s smart home devices

-

News3 weeks ago

News3 weeks agoMassive blasts in Beirut after renewed Israeli air strikes

-

Football4 weeks ago

Football4 weeks agoRangers & Celtic ready for first SWPL derby showdown

-

Science & Environment1 month ago

Science & Environment1 month agoA new kind of experiment at the Large Hadron Collider could unravel quantum reality

-

News3 weeks ago

News3 weeks ago‘Blacks for Trump’ and Pennsylvania progressives play for undecided voters

-

News3 weeks ago

News3 weeks ago▶ Hamas Spent $1B on Tunnels Instead of Investing in a Future for Gaza’s People

-

News3 weeks ago

News3 weeks agoNavigating the News Void: Opportunities for Revitalization

-

Football3 weeks ago

Football3 weeks agoWhy does Prince William support Aston Villa?

-

Business3 weeks ago

Business3 weeks agoWhen to tip and when not to tip

-

MMA3 weeks ago

MMA3 weeks ago‘Uncrowned queen’ Kayla Harrison tastes blood, wants UFC title run

-

Womens Workouts1 month ago

Womens Workouts1 month ago3 Day Full Body Women’s Dumbbell Only Workout

-

MMA4 weeks ago

MMA4 weeks agoDana White’s Contender Series 74 recap, analysis, winner grades

-

MMA3 weeks ago

MMA3 weeks agoPereira vs. Rountree prediction: Champ chases legend status

-

Sport3 weeks ago

Sport3 weeks agoAaron Ramsdale: Southampton goalkeeper left Arsenal for more game time

-

Technology4 weeks ago

Technology4 weeks agoMicrophone made of atom-thick graphene could be used in smartphones

-

Technology3 weeks ago

Technology3 weeks agoGmail gets redesigned summary cards with more data & features

-

Sport3 weeks ago

Sport3 weeks agoWales fall to second loss of WXV against Italy

-

Science & Environment1 month ago

Science & Environment1 month agoWhy this is a golden age for life to thrive across the universe

-

Technology1 month ago

Technology1 month agoRussia is building ground-based kamikaze robots out of old hoverboards

-

Business4 weeks ago

DoJ accuses Donald Trump of ‘private criminal effort’ to overturn 2020 election

-

Technology3 weeks ago

Technology3 weeks agoMusk faces SEC questions over X takeover

-

Sport3 weeks ago

Sport3 weeks agoMan City ask for Premier League season to be DELAYED as Pep Guardiola escalates fixture pile-up row

-

Science & Environment1 month ago

Science & Environment1 month agoA slight curve helps rocks make the biggest splash

-

Science & Environment1 month ago

Science & Environment1 month agoQuantum forces used to automatically assemble tiny device

-

Science & Environment1 month ago

Science & Environment1 month agoITER: Is the world’s biggest fusion experiment dead after new delay to 2035?

-

Science & Environment1 month ago

Science & Environment1 month agoNuclear fusion experiment overcomes two key operating hurdles

-

News1 month ago

News1 month ago▶️ Hamas in the West Bank: Rising Support and Deadly Attacks You Might Not Know About

-

Technology1 month ago

Technology1 month agoMeta has a major opportunity to win the AI hardware race

-

Technology1 month ago

Technology1 month agoWhy Machines Learn: A clever primer makes sense of what makes AI possible

-

Technology4 weeks ago

Technology4 weeks agoEpic Games CEO Tim Sweeney renews blast at ‘gatekeeper’ platform owners

-

News3 weeks ago

News3 weeks agoWoman who died of cancer ‘was misdiagnosed on phone call with GP’

-

Technology3 weeks ago

Technology3 weeks agoMicrosoft just dropped Drasi, and it could change how we handle big data

-

Sport4 weeks ago

Sport4 weeks agoSturm Graz: How Austrians ended Red Bull’s title dominance

-

Money3 weeks ago

Money3 weeks agoWetherspoons issues update on closures – see the full list of five still at risk and 26 gone for good

-

MMA3 weeks ago

MMA3 weeks agoKetlen Vieira vs. Kayla Harrison pick, start time, odds: UFC 307

-

Technology4 weeks ago

Technology4 weeks agoThis AI video generator can melt, crush, blow up, or turn anything into cake

-

News3 weeks ago

News3 weeks agoFamily plans to honor hurricane victim using logs from fallen tree that killed him

-

Sport3 weeks ago

Sport3 weeks ago2024 ICC Women’s T20 World Cup: Pakistan beat Sri Lanka

-

Entertainment3 weeks ago

Entertainment3 weeks agoNew documentary explores actor Christopher Reeve’s life and legacy

-

Science & Environment1 month ago

Science & Environment1 month agoNerve fibres in the brain could generate quantum entanglement

-

MMA4 weeks ago

MMA4 weeks agoJulianna Peña trashes Raquel Pennington’s behavior as champ

-

Business3 weeks ago

Sterling slides after Bailey says BoE could be ‘a bit more aggressive’ on rates

-

Sport4 weeks ago

Sport4 weeks agoChina Open: Carlos Alcaraz recovers to beat Jannik Sinner in dramatic final

-

Business3 weeks ago

The search for Japan’s ‘lost’ art

-

MMA3 weeks ago

MMA3 weeks ago‘I was fighting on automatic pilot’ at UFC 306

-

Business4 weeks ago

Business4 weeks agoChancellor Rachel Reeves says she needs to raise £20bn. How might she do it?

-

Technology3 weeks ago

Technology3 weeks agoTexas is suing TikTok for allegedly violating its new child privacy law

-

Technology3 weeks ago

Technology3 weeks agoThe best budget robot vacuums for 2024

-

Sport3 weeks ago

Sport3 weeks agoCoco Gauff stages superb comeback to reach China Open final

-

Science & Environment1 month ago

Science & Environment1 month agoTime travel sci-fi novel is a rip-roaringly good thought experiment

-

Science & Environment1 month ago

Science & Environment1 month agoHow to wrap your mind around the real multiverse

-

News1 month ago

News1 month ago▶️ Media Bias: How They Spin Attack on Hezbollah and Ignore the Reality

-

Technology3 weeks ago

Technology3 weeks agoIf you’ve ever considered smart glasses, this Amazon deal is for you

-

Business4 weeks ago

Bank of England warns of ‘future stress’ from hedge fund bets against US Treasuries

-

News3 weeks ago

News3 weeks agoCornell is about to deport a student over Palestine activism

-

News3 weeks ago

News3 weeks agoGerman Car Company Declares Bankruptcy – 200 Employees Lose Their Jobs

-

MMA3 weeks ago

MMA3 weeks agoKayla Harrison gets involved in nasty war of words with Julianna Pena and Ketlen Vieira

-

News3 weeks ago

News3 weeks agoHull KR 10-8 Warrington Wolves – Robins reach first Super League Grand Final

-

MMA3 weeks ago

MMA3 weeks agoUFC 307 preview show: Will Alex Pereira’s wild ride continue, or does Khalil Rountree shock the world?

-

Business3 weeks ago

Head of UK Competition Appeal Tribunal to step down after rebuke for serious misconduct

-

MMA3 weeks ago

MMA3 weeks agoPereira vs. Rountree preview show live stream

-

Technology3 weeks ago

Technology3 weeks agoThe best shows on Max (formerly HBO Max) right now

-

Business4 weeks ago

Business4 weeks agoStocks Tumble in Japan After Party’s Election of New Prime Minister

-

Sport4 weeks ago

Sport4 weeks agoWorld’s sexiest referee Claudia Romani shows off incredible figure in animal print bikini on South Beach

-

Science & Environment4 weeks ago

Science & Environment4 weeks agoMarkets watch for dangers of further escalation

-

Football4 weeks ago

Football4 weeks agoSimo Valakari: New St Johnstone boss says Scotland special in his heart

-

Technology4 weeks ago

Technology4 weeks agoJ.B. Hunt and UP.Labs launch venture lab to build logistics startups

-

Technology3 weeks ago

Technology3 weeks agoCheck, Remote, and Gusto discuss the future of work at Disrupt 2024

-

Technology3 weeks ago

Technology3 weeks agoOpenAI secured more billions, but there’s still capital left for other startups

-

Health & fitness3 weeks ago

Health & fitness3 weeks agoNHS surgeon who couldn’t find his scalpel cut patient’s chest open with the penknife he used to slice up his lunch

-

Business3 weeks ago

Business3 weeks agoStark difference in UK and Ireland’s budgets

-

News1 month ago

News1 month agoOur millionaire neighbour blocks us from using public footpath & screams at us in street.. it’s like living in a WARZONE – WordupNews

-

News4 weeks ago

News4 weeks agoRwanda restricts funeral sizes following outbreak

-

MMA4 weeks ago

MMA4 weeks agoAlex Pereira faces ‘trap game’ vs. Khalil Rountree

-

Politics3 weeks ago

Rosie Duffield’s savage departure raises difficult questions for Keir Starmer. He’d be foolish to ignore them | Gaby Hinsliff

-

Money3 weeks ago

Money3 weeks agoPub selling Britain’s ‘CHEAPEST’ pints for just £2.60 – but you’ll have to follow super-strict rules to get in

-

TV3 weeks ago

TV3 weeks agoLove Island star sparks feud rumours as one Islander is missing from glam girls’ night

-

News4 weeks ago

News4 weeks agoLiverpool secure win over Bologna on a night that shows this format might work

-

Technology3 weeks ago

Technology3 weeks agoApple iPhone 16 Plus vs Samsung Galaxy S24+

-

News3 weeks ago

News3 weeks agoBalancing India and China Is the Challenge for Sri Lanka’s Dissanayake

-

MMA3 weeks ago

MMA3 weeks ago‘Dirt decision’: Conor McGregor, pros react to Jose Aldo’s razor-thin loss at UFC 307

-

News1 month ago

the pick of new debut fiction

-

MMA4 weeks ago

MMA4 weeks agoHow to watch Salt Lake City title fights, lineup, odds, more

-

Business4 weeks ago

how UniCredit built its Commerzbank stake

-

Business4 weeks ago

Top shale boss says US ‘unusually vulnerable’ to Middle East oil shock

You must be logged in to post a comment Login