CryptoCurrency

Foxconn building Nvidia superchip facility in Mexico, execs say

By Yimou Lee

TAIPEI (Reuters) -Foxconn is building in Mexico the world’s largest manufacturing facility for bundling Nvidia’s GB200 superchips, a key component of the U.S. firm’s next-generation Blackwell family computing platform, senior executives at the Taiwanese company said on Tuesday.

Foxconn, the world’s largest contract electronics manufacturer and known as Apple’s biggest iPhone assembler, has been benefiting from the artificial intelligence boom as it assembles servers used to process AI work.

“We’re building the largest GB200 production facility on the planet,” said Benjamin Ting, Foxconn senior vice president for the cloud enterprise solutions business group.

Nvidia said in August that it had started shipping Blackwell samples to its partners and customers after tweaking its design, and expected several billion dollars in revenue from these chips in the fourth quarter.

Ting said the partnership between his company and Nvidia was very important and everyone was asking for Nvidia’s Blackwell platform.

“The demand is awfully huge,” Ting said at the company’s annual tech day in Taipei, standing next to Nvidia’s vice president for AI and robotics, Deepu Talla.

Speaking to reporters later, Foxconn Chairman Young Liu said the plant was being build in Mexico, and that the capacity there would be “very, very enormous”. He did not elaborate.

Foxconn already has a large manufacturing presence in Mexico and has invested more than $500 million to date in the state of Chihuahua.

Liu said the company’s supply chain was ready for the AI revolution, adding its manufacturing capabilities include the “advanced liquid cooling and heat dissipation technologies necessary to complement the GB200 server’s infrastructure.”

He said that the company’s outlook in the current quarter was strong, though did not give details. On Saturday, Foxconn posted its highest-ever revenue for the third quarter on strong demand for AI servers.

Foxconn’s other focus is ambitious plans to diversify away from its role of building consumer electronics for Apple, hoping to use its tech know-how to offer EV contract manufacturing and also produce vehicles using models built by Foxtron brand.

Asked about fierce competition in the global electric vehicle market amid slowing demand, Liu said Foxconn was committed to the sector.

“It is the right direction and we will continue to work hard towards that,” he said, adding that with the EVs, the “engine barrier” no longer exists in car manufacturing.

Automakers “don’t need to make the whole car themselves anymore”, he said.

(Reporting by Yimou Lee; Writing by Ben Blanchard; Editing by Christopher Cushing, Tom Hogue and Kim Coghill)

Consumer prices in the US rose by 2.4% in September, above market expectations but still in a negative trend compared to the past few years.

Georgia’s political opposition wants to use blockchain technology to develop civil society and the country’s business landscape.

CryptoCurrency

Super Micro Computer stock continues wild ride as investors weigh AI hype against alleged DOJ probe

Super Micro Computer (SMCI) stock fell 2.5% Thursday after rallying as much as 9% the day before, continuing its rollercoaster ride of a week as investors swing between optimism over the company’s strong financials and cautiousness over its regulatory risks.

Super Micro is reportedly being investigated by the Department of Justice over allegations of shady business practices outlined in a scathing report by short seller firm Hindenburg Research in late August. That has pressured the stock, which has hovered under $50 per share since then.

This week, SMCI climbed on positive reports from the AI server maker. Super Micro surged 16% Monday after the company released numbers showing strong demand for its products. The stock was up 12% on Thursday from the prior week.

Super Micro makes servers using Nvidia’s (NVDA) AI chips for data centers that power artificial intelligence software. The company said it’s shipping servers containing over 100,000 Nvidia GPUs per quarter “for some of the largest AI factories ever built.”

Then on Tuesday, shares of SMCI fell 5% after a promising premarket rally that saw the stock jump as much as 7%. Daniel Newman, CEO of the Futurum Group, said investors’ euphoria over the company’s shipment data faded against the backdrop of Super Micro’s regulatory risk.

“I think one piece of good news hardly undoes multiple months of significant financial and regulatory scrutiny around a company like this,” Newman said.

The Hindenburg report in August accused Super Micro of shoddy accounting, undisclosed relationships between its CEO and companies it does business with, and violations of US export bans. For example, Hindenburg said Super Micro has shipped servers to sanctioned Russian firms through shell companies, some of which were likely used by its military for its war against Ukraine.

The day after Hindenburg released its report, Super Micro shares dropped 20%. The company also delayed filing its annual 10-K report to the US Securities and Exchange Commission. Super Micro’s woes continued with a Wall Street Journal report of an alleged DOJ probe, which sent shares tumbling in late September.

Super Micro CEO Charles Liang said the Hindenburg report contained “false or inaccurate statements” and “misleading presentations of information that we have previously shared publicly.” Liang said the company’s delayed 10-K filing would not affect the company’s fourth quarter financial results, adding that Super Micro would address Hindenburg’s allegations “in due course.”

Super Micro’s stock climb this week displays the tension between its potential as a key player in the AI boom and its regulatory hurdles.

“This is a high-risk reward,” Newman said. “If they get absolved of all of this, there’s a very good chance it’s going to see a pretty nice move to the upside.” Of the Wall Street analysts tracked by Bloomberg who are covering the stock, seven have a Buy rating on the stock, while 11 maintain a Hold rating. Only one analyst recommends selling the stock.

Analysts see shares rising to $66 over the next 12 months.

The company reported mixed results in its last earnings report. Super Micro’s most recent quarterly revenue of $5.3 billion for the three months ended June 30 barely missed Wall Street’s expectations, but was 143% higher than the prior year. On the other hand, Super Micro earnings per share for the company’s fiscal fourth quarter of $0.63 were far lower than analysts’ consensus forecast of $0.83, according to Bloomberg data.

Argus Research analyst Jim Kelleher told investors in a note on Oct. 3 to buy the dip, noting that Super Micro “has been growing sales and earnings much more rapidly than the Tech industry in recent years.” Wall Street expects Super Micro to report revenues of $6.5 billion for the period ended Sept. 30, up 206% from the previous year. The company has not yet confirmed a date for its next earnings release.

“At this point, we are assuming that any accounting irregularities should they exist are minor and can be addressed while requiring re-issued financial documents,” Kelleher said, adding that Super Micro’s recent 10-for-1 stock split on Oct. 1 “broadens the potential investor pool and should be a long-term positive.”

Despite his long-term optimism, Kelleher lowered his 12-month price target for the stock from $100 to $70.

Laura Bratton is a reporter for Yahoo Finance.

Click here for the latest stock market news and in-depth analysis, including events that move stocks

Read the latest financial and business news from Yahoo Finance

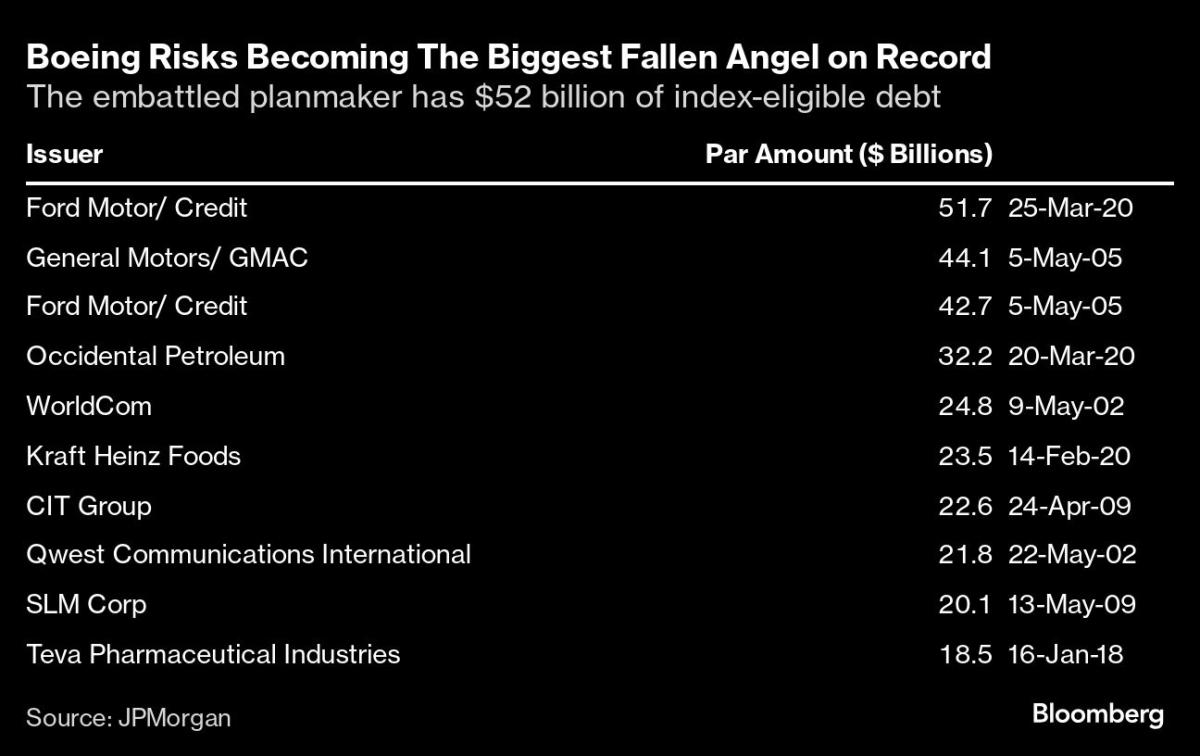

(Bloomberg) — If cut to junk status, Boeing Co. will be the biggest US corporate borrower to ever be stripped of its investment-grade ratings, flooding the high-yield bond market with a record volume of new bonds to absorb.

Most Read from Bloomberg

On Tuesday, S&P Global Ratings said it’s considering downgrading the planemaker to junk as strikes at its manufacturing sites persist, hurting production. Last month, Moody’s Ratings said it’s considering a similar move. Fitch Ratings has highlighted the growing risks but not yet announced a review.

Downgrades to junk from two of Boeing’s three major credit graders would leave much of its $52 billion of outstanding long-term debt ineligible for inclusion in investment-grade indexes. If that happens, Boeing would become the biggest ever fallen angel — industry parlance for a company that’s lost its investment-grade ratings — by index-eligible debt, according to JPMorgan Chase & Co. analysts.

“Boeing has worn out its welcome in the investment-grade index,” said Bill Zox, a portfolio manager at Brandywine Global Investment Management. “But the high-yield index would be honored to welcome Boeing and its many coupon step-ups.”

A spokesperson for Boeing declined to comment for this story.

‘Idiosyncratic Credit Situation’

JPMorgan isn’t taking a view on the likelihood of Boeing transitioning to junk or what such a transition would mean for its credit fundamentals, strategists led by Eric Beinstein and Nathaniel Rosenbaum wrote in a Thursday note.

There could be a relatively seamless transition, the strategists wrote. Credit spreads are tight trading conditions are relatively liquid trading in both the high-grade and high-yield markets, the strategists wrote. Much of of Boeing’s debt has a coupon step-up feature — where the interest rate increases by 0.25 percentage point for each step below investment-grade that each ratings firm downgrades by, which could make it more palatable to some investors, including insurers.

“Usually downgrades from high-grade to high-yield are clustered together around economic downturns or crisis,” the analysts wrote. “This is an idiosyncratic credit situation, should a downgrade occur. No other large fallen angel has ever transitioned at such tight spreads.”

The corporate bond market has swelled in recent years, so even if Boeing has more debt than other borrowers have had historically, it takes up a smaller part of the investment-grade universe. The company makes up just 0.7% of Bloomberg’s US corporate investment-grade bond index. When Ford Motor Co. and General Motors Co. were downgraded in 2005, they took up 8.3% and 3% of the high-grade market respectively, according to JPMorgan.

But there are also reasons for the transition to potentially result in big price moves for the company’s debt. Boeing’s $52 billion debt load is big by junk issuer standards. And it has a relatively high proportion of longer-dated debt, while most high-yield investors focus on shorter- and intermediate-term securities to help manage credit risk.

High-grade and high-yield funds, which pool together bonds according to factors like credit quality and maturity to pay regular returns to investors, could also be impacted. More passive fund investors have piled into the high-grade market over the years, which would mean a higher volume of “forced sellers” if Boeing is downgraded, according to JPMorgan.

“I would expect a fair amount of index-related selling as the debt changes hands between the investment-grade and high-yield markets,” said Scott Kimball, chief investment officer at Loop Capital Asset Management. “It wouldn’t surprise me if things got ugly as high-yield investors aren’t as beholden to benchmarks, generally.”

Since active high-yield managers are not going be “forced buyers,” they will have a greater degree of price-setting power, according to Kimball.

“The liquidity transfer costs are real,” he said. “High-yield buyers, being less index-focused, are the ones setting the price. It’s the opposite of upgrades where passive money is more prevalent.”

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.

The “Peter Todd is Satoshi” claim isn’t the first time a misguided theory has appeared in crypto. Here’s 10 more ideas that turned out wrong.

The app chain promises faster and cheaper transactions and cross-chain interoperability, according to Uniswap.

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoHyperelastic gel is one of the stretchiest materials known to science

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoHow to unsnarl a tangle of threads, according to physics

-

Technology3 weeks ago

Technology3 weeks agoWould-be reality TV contestants ‘not looking real’

-

Womens Workouts3 weeks ago

Womens Workouts3 weeks ago3 Day Full Body Women’s Dumbbell Only Workout

-

Science & Environment3 weeks ago

Science & Environment3 weeks ago‘Running of the bulls’ festival crowds move like charged particles

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoMaxwell’s demon charges quantum batteries inside of a quantum computer

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoLiquid crystals could improve quantum communication devices

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoQuantum ‘supersolid’ matter stirred using magnets

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoSunlight-trapping device can generate temperatures over 1000°C

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoITER: Is the world’s biggest fusion experiment dead after new delay to 2035?

-

News4 weeks ago

the pick of new debut fiction

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoHow to wrap your mind around the real multiverse

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoWhy this is a golden age for life to thrive across the universe

-

News3 weeks ago

News3 weeks agoOur millionaire neighbour blocks us from using public footpath & screams at us in street.. it’s like living in a WARZONE – WordupNews

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoQuantum forces used to automatically assemble tiny device

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoNerve fibres in the brain could generate quantum entanglement

-

Science & Environment2 weeks ago

Science & Environment2 weeks agoX-rays reveal half-billion-year-old insect ancestor

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoPhysicists are grappling with their own reproducibility crisis

-

Business2 weeks ago

Eurosceptic Andrej Babiš eyes return to power in Czech Republic

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoTime travel sci-fi novel is a rip-roaringly good thought experiment

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoLaser helps turn an electron into a coil of mass and charge

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoNuclear fusion experiment overcomes two key operating hurdles

-

News4 weeks ago

News4 weeks ago▶️ Hamas in the West Bank: Rising Support and Deadly Attacks You Might Not Know About

-

Technology2 weeks ago

Technology2 weeks agoIs sharing your smartphone PIN part of a healthy relationship?

-

News3 weeks ago

News3 weeks agoYou’re a Hypocrite, And So Am I

-

Sport3 weeks ago

Sport3 weeks agoJoshua vs Dubois: Chris Eubank Jr says ‘AJ’ could beat Tyson Fury and any other heavyweight in the world

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoA slight curve helps rocks make the biggest splash

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoCaroline Ellison aims to duck prison sentence for role in FTX collapse

-

News3 weeks ago

News3 weeks ago▶️ Media Bias: How They Spin Attack on Hezbollah and Ignore the Reality

-

Technology2 weeks ago

Technology2 weeks ago‘From a toaster to a server’: UK startup promises 5x ‘speed up without changing a line of code’ as it plans to take on Nvidia, AMD in the generative AI battlefield

-

Football2 weeks ago

Football2 weeks agoFootball Focus: Martin Keown on Liverpool’s Alisson Becker

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoRethinking space and time could let us do away with dark matter

-

News4 weeks ago

News4 weeks agoNew investigation ordered into ‘doorstep murder’ of Alistair Wilson

-

News3 weeks ago

The Project Censored Newsletter – May 2024

-

Technology2 weeks ago

Technology2 weeks agoQuantum computers may work better when they ignore causality

-

Business2 weeks ago

Should London’s tax exiles head for Spain, Italy . . . or Wales?

-

MMA2 weeks ago

MMA2 weeks agoConor McGregor challenges ‘woeful’ Belal Muhammad, tells Ilia Topuria it’s ‘on sight’

-

Sport2 weeks ago

Sport2 weeks agoWatch UFC star deliver ‘one of the most brutal knockouts ever’ that left opponent laid spark out on the canvas

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoA new kind of experiment at the Large Hadron Collider could unravel quantum reality

-

News3 weeks ago

Israel strikes Lebanese targets as Hizbollah chief warns of ‘red lines’ crossed

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoFuture of fusion: How the UK’s JET reactor paved the way for ITER

-

Technology2 weeks ago

Technology2 weeks agoGet ready for Meta Connect

-

Business1 week ago

Ukraine faces its darkest hour

-

Health & fitness3 weeks ago

Health & fitness3 weeks agoThe secret to a six pack – and how to keep your washboard abs in 2022

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoUK spurns European invitation to join ITER nuclear fusion project

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoWhy we need to invoke philosophy to judge bizarre concepts in science

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoA tale of two mysteries: ghostly neutrinos and the proton decay puzzle

-

Health & fitness2 weeks ago

Health & fitness2 weeks agoThe 7 lifestyle habits you can stop now for a slimmer face by next week

-

Technology3 weeks ago

Technology3 weeks agoThe ‘superfood’ taking over fields in northern India

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoCardano founder to meet Argentina president Javier Milei

-

Politics3 weeks ago

UK consumer confidence falls sharply amid fears of ‘painful’ budget | Economics

-

MMA3 weeks ago

MMA3 weeks agoRankings Show: Is Umar Nurmagomedov a lock to become UFC champion?

-

News3 weeks ago

News3 weeks agoWhy Is Everyone Excited About These Smart Insoles?

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoMeet the world's first female male model | 7.30

-

News3 weeks ago

News3 weeks agoFour dead & 18 injured in horror mass shooting with victims ‘caught in crossfire’ as cops hunt multiple gunmen

-

Womens Workouts3 weeks ago

Womens Workouts3 weeks ago3 Day Full Body Toning Workout for Women

-

Technology2 weeks ago

Technology2 weeks agoRobo-tuna reveals how foldable fins help the speedy fish manoeuvre

-

Health & fitness3 weeks ago

Health & fitness3 weeks agoThe maps that could hold the secret to curing cancer

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoBeing in two places at once could make a quantum battery charge faster

-

News4 weeks ago

News4 weeks agoHow FedEx CEO Raj Subramaniam Is Adapting to a Post-Pandemic Economy

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoLow users, sex predators kill Korean metaverses, 3AC sues Terra: Asia Express

-

Womens Workouts3 weeks ago

Womens Workouts3 weeks agoBest Exercises if You Want to Build a Great Physique

-

Womens Workouts3 weeks ago

Womens Workouts3 weeks agoEverything a Beginner Needs to Know About Squatting

-

TV3 weeks ago

TV3 weeks agoCNN TÜRK – 🔴 Canlı Yayın ᴴᴰ – Canlı TV izle

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoCNN TÜRK – 🔴 Canlı Yayın ᴴᴰ – Canlı TV izle

-

Servers computers2 weeks ago

Servers computers2 weeks agoWhat are the benefits of Blade servers compared to rack servers?

-

Technology2 weeks ago

Technology2 weeks agoThe best robot vacuum cleaners of 2024

-

News3 weeks ago

News3 weeks agoChurch same-sex split affecting bishop appointments

-

Sport3 weeks ago

Sport3 weeks agoUFC Edmonton fight card revealed, including Brandon Moreno vs. Amir Albazi headliner

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoEthereum is a 'contrarian bet' into 2025, says Bitwise exec

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoHow one theory ties together everything we know about the universe

-

Business3 weeks ago

JPMorgan in talks to take over Apple credit card from Goldman Sachs

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoQuantum time travel: The experiment to ‘send a particle into the past’

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoTiny magnet could help measure gravity on the quantum scale

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoMost accurate clock ever can tick for 40 billion years without error

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoDecentraland X account hacked, phishing scam targets MANA airdrop

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoBitcoin miners steamrolled after electricity thefts, exchange ‘closure’ scam: Asia Express

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoDorsey’s ‘marketplace of algorithms’ could fix social media… so why hasn’t it?

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoDZ Bank partners with Boerse Stuttgart for crypto trading

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoBitcoin bulls target $64K BTC price hurdle as US stocks eye new record

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoBlockdaemon mulls 2026 IPO: Report

-

Business3 weeks ago

Thames Water seeks extension on debt terms to avoid renationalisation

-

Politics3 weeks ago

‘Appalling’ rows over Sue Gray must stop, senior ministers say | Sue Gray

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoCoinbase’s cbBTC surges to third-largest wrapped BTC token in just one week

-

News2 weeks ago

News2 weeks agoUS Newspapers Diluting Democratic Discourse with Political Bias

-

Politics3 weeks ago

Politics3 weeks agoTrump says he will meet with Indian Prime Minister Narendra Modi next week

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoPhysicists have worked out how to melt any material

-

Technology3 weeks ago

Technology3 weeks agoiPhone 15 Pro Max Camera Review: Depth and Reach

-

News3 weeks ago

News3 weeks agoBrian Tyree Henry on voicing young Megatron, his love for villain roles

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoHow do you recycle a nuclear fusion reactor? We’re about to find out

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoRedStone integrates first oracle price feeds on TON blockchain

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks ago‘No matter how bad it gets, there’s a lot going on with NFTs’: 24 Hours of Art, NFT Creator

-

Business3 weeks ago

How Labour donor’s largesse tarnished government’s squeaky clean image

-

News3 weeks ago

Brian Tyree Henry on voicing young Megatron, his love for villain roles

-

Travel2 weeks ago

Travel2 weeks agoDelta signs codeshare agreement with SAS

-

Politics2 weeks ago

Politics2 weeks agoHope, finally? Keir Starmer’s first conference in power – podcast | News

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoLouisiana takes first crypto payment over Bitcoin Lightning

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoCrypto scammers orchestrate massive hack on X but barely made $8K

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoTelegram bot Banana Gun’s users drained of over $1.9M

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoSEC asks court for four months to produce documents for Coinbase

You must be logged in to post a comment Login