CryptoCurrency

What’s the Best Spot for My Short-Term Savings?

I’m holding $300,000 in cash that I plan to put into a new home. With the market as it is, I’m putting off that purchase for six to nine months. I’m 66 years old, single and plan to retire within the next 12 months. What should I do with the cash until I purchase?

-Judi

When it comes to determining where to house your short-term savings, factors to consider include risk, access, goals and what will give you peace of mind.

These factors are going to determine where you store your cash. And ultimately, understanding your unique needs and preferences, specifically your goals, will bring calm and clarity to your decision. You can use this tool to get matched with a financial advisor who might meet your needs.

How to Evaluate Short-Term Savings Vehicles

There are several factors to consider when eyeing short-term funds.

Term and type. Short-term investment and savings should be easily converted to cash within three to 12 months (or less) without losing principal value. They may have the opportunity for a small risk-free gain.

Risk. You want funds to retain the value of principal or earn a risk-free return.

Yes, there is an opportunity for short-term gains across various investment opportunities. But if you must assume risk for these gains, you may absorb the shock of sudden loss. Given your short time horizon, it is best to avoid unnecessary risk.

Access. Ease of access contributes to your storage decision. Short-term events require liquidity and expediency. It shouldn’t take more than a few days to liquidate and transfer cash to your goal. Nimble access requires a flexible financial institution location.

Goal. Assigning a goal to your funds is an essential factor. A goal begins with a series of functional and emotional questions. These may include these:

-

What are these funds for?

-

What event, experience or expense am I preparing for?

-

What positive outcome do I want to experience?

The answers to these questions will bring a sense of serenity to your process and decision.

Consider matching with a financial advisor to speak about your own personal finance strategy with a fiduciary.

What Are Your Options for Short-Term Savings?

Banks and credit unions.

Banks and credit unions have several advantages. FDIC insurance covers $250,000 of bank deposits per individual, per bank and account ownership. Depending on the account ownership, you can have more than $250,000 of coverage at one bank.

Credit unions insure $250,000 per depositor through the National Credit Union Association. An FDIC overview and calculator are available here. An NCUA calculator is here.

You can spread the deposit amounts across multiple institutions if your funds are too high to meet the FDIC insurance range at one institution. That strategy, however, adds a layer of personal management complexity.

Insurance is not the only benefit banks and credit unions offer. Banks and credit unions offer liquidity and access.

Cash does not require liquidation. Cash is cash when held in a savings account, which provides the quickest form of access, liquidity and transferability. Banks and credit unions tend to offer robust online platforms with electronic capabilities. Brokerage options will give the same.

Larger banks and credit unions offer multiservice platforms that allow clients to efficiently use their funds and access expertise across divisions such as mortgage, loans, brokerages, trusts and banking. If you think you’ll need any of these services during a short-term time horizon, banks and credit unions may look more appealing.

A potential drawback is low interest rates on your funds. Several reputable and insured online banking platforms, however, offer attractive savings account interest rates.

Brokerage money market mutual fund account. The brokerage money market at your investment institution offers liquidity. Your cash is grouped with other savers’ cash in mutual funds that invest in short-term government securities that pay interest rates net of fees, similar to savings accounts.

Brokerage money market accounts are not insured and are regulated by the Securities and Exchange Commission (SEC). Another general plus for brokerage money markets is their liquidity and access. Cash is available the next day in your account and is easily electronically transferable to external accounts.

Brokerage stock market. The stock market giveth and taketh. For the market to “give” gains, investors must “give” the market time. That’s not the same thing as “timing” the market. This refers to “time in” the market.

For short-term goals, the market may not be your best bet. The time horizon may “taketh” quickly through a market shock where your principal value dramatically declines.

Comparatively, if the invested funds are for a long-term goal, there is time in the market for a principal amount to recover and compound.

Treasury I Bonds. Americans are experiencing inflationary times and feeling the higher prices in their grocery carts, gas tanks, wallets and lifestyles. One upside is Treasury I Bonds, which adjust their interest rate payout to changes in the Consumer Price Index-Urban (CPI-U).

When the inflation rate is high, the interest rate on I Bonds reflects the increase and is attractive. The current rate is around 9.62%, much higher than any savings account rate at a bank, credit union or brokerage.

There are caveats. You must purchase directly from the government at Treasurydirect.gov, you can buy up to $10,000 annually (an allowance of an additional $5,000 if paying with a tax refund) and you must hold the bond for 12 months.

These limitations do not fit with short-term goals that have a horizon of fewer than 12 months, are more significant than $10,000, and require liquidity and ease of user access. I Bonds are most useful when a person has $10,000 outside of an emergency fund, a short-term goal and the spare time to clip the inflation interest paid.

A financial advisor can help you evaluate your options based on your goals.

What to Do Next

Consider your needs, then review the savings vehicles described above to determine which one best meets your criteria.

The bottom line is that your needs are principal preservation, low-risk capacity and the ability to make a large purchase within 12 months. You also need liquid, accessible and transferrable funds.

Your secondary goals are to earn interest and achieve insurance protection. You may consider an online bank or credit union outside your primary institution if your funds exceed the FDIC insurance limits.

Tips for Growing and Protecting Your Assets

-

If you have questions specific to your investing and retirement situation, a financial advisor can help. Finding a qualified financial advisor doesn’t have to be hard. SmartAsset’s free tool matches you with up to three financial advisors who serve your area, and you can interview your advisor matches at no cost to decide which one is right for you. If you’re ready to find an advisor who can help you achieve your financial goals, get started now.

-

Keep an emergency fund on hand in case you run into unexpected expenses. An emergency fund should be liquid — in an account that isn’t at risk of significant fluctuation like the stock market. The tradeoff is that the value of liquid cash can be eroded by inflation. But a high-interest account allows you to earn compound interest. Compare savings accounts from these banks.

-

Are you a financial advisor looking to grow your business? SmartAsset AMP helps advisors connect with leads and offers marketing automation solutions so you can spend more time making conversions. Learn more about SmartAsset AMP.

Photo credit: Madilyn Heinke, ©iStock.com/Extreme Media, ©iStock.com/shironosov

The post Ask An Advisor: Where Should I Stash Short-Term Savings? appeared first on SmartAsset Blog.

Super Micro Computer (NASDAQ: SMCI) split its shares this month and now they are trading at one-tenth of what they were before the split. For investors, that means a lower share price, and perhaps the ability to own more full shares. Stock splits can sometimes have positive effects on the share price even though they don’t fundamentally change anything about a company’s prospects or improve its earnings numbers.

With shares of Super Micro Computer, also known as just Supermicro, down more than 50% in just the past six months, could the recent split provide the stock a boost, and potentially help stop its tailspin?

Why a stock split may not help Supermicro

A stock split doesn’t solve any problems for a business. Regardless of whether Supermicro stock is trading at $450 or $45, investors can buy fractional shares if they want to invest in it but don’t have the funds necessary to acquire entire shares of the company. And that’s why stock splits normally shouldn’t lead to a rally in the share price; they don’t change valuation multiples to make the stock a better buy.

Some investors may believe that because a stock is priced lower, it’s cheaper and a better buy, but that is a mistake. When talking about valuation, you should always look at per-share earnings and revenue multiples, which take into context the share price. And stock splits don’t change those multiples.

Stock splits can become positive catalysts if a stock rises significantly in value and then a company opts to do a split. In Supermicro’s case, however, the stock has been crashing of late, and its stock split comes at a time when there’s a lot of negativity and bearishness around the business, which is why a split may not have a positive effect on its share price.

Supermicro’s problems have nothing to do with its share price

For Supermicro, there are much larger concerns for investors than its share price being too high. The company’s margins have been under pressure and the Department of Justice (DOJ) is reportedly looking into the company after a short report in August alleged the company was involved in questionable accounting practices. Management has denied any wrongdoing and the DOJ investigation may not necessarily lead to anything substantive and consequential for the business and its investors.

The bigger issue, however, is that the company’s earnings may not grow at a high rate if Supermicro’s margins don’t improve. In its most recent earnings report, for the quarter ended June 30, the company’s gross margin was just 11%, down from an already fairly low rate of 17% a year ago. Low margins can negate much of the benefit the tech company will get from generating strong server sales and growing its operations, and that’s the biggest reason I’d be concerned about the stock right now.

Is Supermicro stock a buy?

I don’t believe a stock split is going to save Supermicro stock nor do I think the DOJ probe is going to cripple it. Short reports are often biased and meritless and while they can temporarily send a stock lower, they rarely uncover disastrous findings auditors, analysts, and investors have all missed.

The company can put a lot of concerns to rest by simply posting strong earnings numbers and showing that it can grow both its top and bottom lines at high rates. But it still has to prove that it can do that.

Unless you’re comfortable with the risk that comes with owning Supermicro stock today, the safest option is to take a wait-and-see approach right now. The biggest question mark around the business remains its ability to grow its earnings, because if it can’t do that, it’s going to be hard to justify buying the AI stock.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

-

Amazon: if you invested $1,000 when we doubled down in 2010, you’d have $21,266!*

-

Apple: if you invested $1,000 when we doubled down in 2008, you’d have $43,047!*

-

Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $389,794!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of October 7, 2024

David Jagielski has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Will Super Micro Computer’s Stock Split Help Rally Its Shares? was originally published by The Motley Fool

An HBO documentary says Peter Todd is the Bitcoin creator known as Satoshi Nakamoto. He denies it

Who created Bitcoin? Is it finally known? Perhaps not.

“Money Electric: The Bitcoin Mystery,” a new HBO (WBD) documentary that premiered on Tuesday, claims that former Bitcoin developer Peter Todd is Satoshi Nakamoto, who created Bitcoin. Hours before the documentary’s release, the 39-year-old Canadian software designer involved in the early years of developing Bitcoin denied the claim, saying that he was not the creator of Bitcoin.

Tesla stock sinks 7% after Elon Musk’s robotaxi reveal disappoints investors

Tesla (TSLA) stock fell during morning trading on Friday, after its highly-anticipated robotaxi reveal failed to impress investors.

The electric vehicle maker’s shares were down around 7.5% on Friday morning after being down about 6% during pre-market trading. Its shares closed down almost 1% Thursday before the event. Read More

The CEO of disgraced crypto firm FTX actually announced his prison stint on LinkedIn

Ryan Salame, the former co-CEO of FTX Digital Markets, has been seeking a two-month delay for the start of his prison sentence due to alleged injuries from a dog. However, it appears he has come to terms with his situation. In a recent LinkedIn post, he announced his new role as an inmate at FCI Cumberland.

The next Nvidia? Data center stocks could be a goldmine, strategist says

Tejas Dessai, director of research at Global X, breaks down what companies to invest in for the next phase of AI expansion

10 cities where low mortgage rates have homeowners locked in ‘golden handcuffs’

Despite signs that the “lock-in” effect is beginning to fade, many homeowners that snagged rock-bottom mortgage rates during the pandemic are still waiting on rates to fall again before making a move.

Nvidia (NASDAQ: NVDA) has been one of the best-performing stocks on the market over the past two years, and the catalysts that drove it higher are still present. But after its strong run-up, is Nvidia stock still a smart buy at its current level, or would those who hold shares be advised to sell and take some profits?

There are valid arguments for both views.

The sell argument: How long will this demand wave last?

Nvidia’s rise has been directly tied to the artificial intelligence (AI) arms race. Its primary products are graphics processing units (GPUs) — parallel processors that excel at handling large and complex computing tasks that are easily broken down into many smaller ones that can be handled independently and simultaneously. Connect GPUs in clusters and you end up with a computing platform that can process certain types of incredibly complex workloads at blistering speeds — and these are just the sorts of workloads that AI systems create.

As AI companies and cloud computing providers rushed to get in front of the emerging demand for processing power, Nvidia’s sales went through the roof. In the past couple of years, quarterly revenues have often tripled on a year-over-year basis. However, its stellar growth is starting to slow slightly due to tougher annualized comparisons. This growth slowdown makes sense, but the bigger question is, can Nvidia maintain its overall sales at these levels?

Because companies are buying these GPUs to rapidly build their AI computing capacity, there is going to be a time when the demand will be satisfied. At that point, Nvidia’s sales may crater, as companies will only be buying replacement GPUs or making gradual capacity increases. This could be a huge problem for Nvidia, as its revenue levels in its latest quarters are far above where they have been in the past.

This also highlights the cyclical nature of the chip business. Nvidia has gone through multiple boom-and-bust cycles in its life as a company. If AI-related demand wanes, investors could be in a rough spot.

But has Nvidia built up enough of a sales base to compensate for that cyclicality?

The buy argument: New technology will spur further demand past 2025

GPUs don’t last forever. They generally need to be replaced after about three to five years, which means that if the companies that have been building out their computing infrastructure recently want to maintain that processing power over the long term, they will have to regularly fork out massive chunks of money on new hardware.

We’re two years into the AI build-out already, and many companies are still scaling up their AI computing power, so 2025 will be another year of strong demand. That gets investors to 2026, at which point the natural replacement cycle starts for the GPUs that were purchased at the start of the generative AI era. But there could also be more reasons for companies to upgrade.

First, the semiconductor chips within these Nvidia GPUs are produced by Taiwan Semiconductor Manufacturing (NYSE: TSM). Taiwan Semi is always innovating on the process node front, allowing chip designers like Nvidia to create denser, higher-performance chips.

TSMC expects that its chips built using its next-generation N2 process node will be 25% to 30% more power efficient than prior-generation chips when configured at the same speeds. Energy costs are a huge operating expense for server farms, so some customers may choose to upgrade for that reason, regardless of whether they need more computing power or not. The N2 manufacturing lines aren’t expected to start production until 2025, which likely means Nvidia GPUs built on them won’t make their way to its customers in quantity until 2026.

Meanwhile, Nvidia is just launching its Blackwell architecture GPUs, which will replace the Hopper architecture upon which it has built its current top-of-the-line chips, and the improvements are astounding. Blackwell’s architecture is four times faster than Hopper’s, allowing AI companies to create more complex models faster.

The combination of all these factors points to demand remaining strong well past 2026. In other words, the market probably isn’t peaking any time soon. This is key, as Nvidia’s forward price-to-earnings ratio has already reached levels that are starting to look reasonable, at least relative to how fast it’s growing.

Trading at 45 times forward earnings, Nvidia stock is far from cheap, but it’s putting up strong growth, so this valuation is acceptable.

Investors’ decisions about whether to buy or sell Nvidia stock today should be based on how they expect the company’s business to be faring in 2026 and beyond. There are enough catalysts out there that Nvidia’s growth should last far beyond 2026, and with the upgrade cycle, it should be able to maintain its newfound revenue levels.

As a result, I think Nvidia’s buy case is greater than its sell case today.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

-

Amazon: if you invested $1,000 when we doubled down in 2010, you’d have $21,266!*

-

Apple: if you invested $1,000 when we doubled down in 2008, you’d have $43,047!*

-

Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $389,794!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of October 7, 2024

Keithen Drury has positions in Taiwan Semiconductor Manufacturing. The Motley Fool has positions in and recommends Nvidia and Taiwan Semiconductor Manufacturing. The Motley Fool has a disclosure policy.

Should You Buy or Sell Nvidia Stock? was originally published by The Motley Fool

Bitcoin bulls enjoy more weekend BTC price gains as market cap signals point to a classic bull run comeback.

CryptoCurrency

The Newest Artificial Intelligence Stock Has Arrived — and It Claims to Make Chips That Are 20x Faster Than Nvidia

The artificial intelligence chipmaker Nvidia (NASDAQ: NVDA) has amassed close to a $3.2 trillion market cap, making it one of the world’s largest chipmakers. It now consumes more than 6% of the broader benchmark S&P 500 index. Over the last five years, Nvidia has grown annual revenue by 458% and the stock is up an incredible 2,009%. Given the potential for AI to disrupt life as we know it, it’s understandable that investors are so excited about the stock.

But the lure of these kinds of gains is naturally going to attract competition. Now, one of Nvidia’s competitors is planning an initial public offering (IPO) and claiming to manufacture chips that can vastly outperform Nvidia at a fraction of the price. Let’s take a look.

20x better than Nvidia?

Last week, the AI chipmaker Cerebras filed its registration statement with the Securities and Exchange Commission (SEC) with the intent to go public. In a press release from 2021, Cerebras said it had a valuation of $4 billion after a $250 million series F financing round. The company is targeting a $1 billion IPO at a $7 billion to $8 billion valuation.

In its registration statement, Cerebras cites Nvidia as a competitor, as well as other large AI companies such as Advanced Micro Devices, Intel, Microsoft, and Alphabet. Here is a description of what Cerebras does:

We design processors for AI training and inference. We build AI systems to power, cool, and feed the processors data. We develop software to link these systems together into industry-leading supercomputers that are simple to use, even for the most complicated AI work, using familiar ML frameworks like PyTorch. Customers use our supercomputers to train industry-leading models. We use these supercomputers to run inference at speeds unobtainable on alternative commercial technologies.

Cerebras’ pitch is that bigger is better. That’s because the company has designed a chip that is the size of a full silicon wafer, and the largest ever sold. The company believes that the size advantage leads to less time moving data. Furthermore, Cerebras has a flexible business model in which clients can buy Cerebras products to have at their facilities or through a consumption-based subscription through the company’s cloud infrastructure.

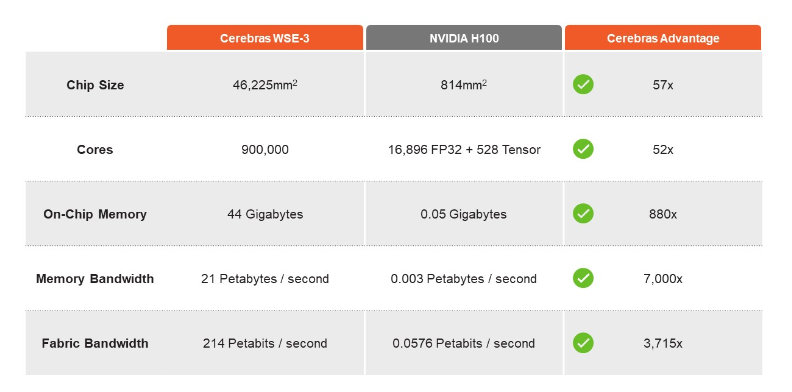

Cerebras clearly wants investors to compare, or at least associate, the company with Nvidia. Nvidia is mentioned 12 times in the registration statement. Cerebras also provides a side-by-side comparison of its Wafer-Scale Engine-3 chip versus Nvidia’s H100 graphics processing unit (GPU), which is considered the most powerful GPU on the market.

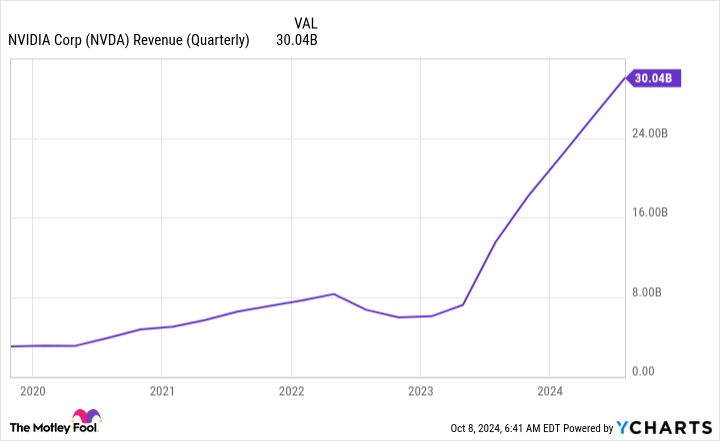

Cerebras CEO Andrew Feldman publicly said the company’s inference offering is 20 times faster than Nvidia’s at a fraction of the price. In 2023, Cerebras generated about $78.7 million of revenue, up 220% year over year. Through the first half of 2024, Cerebras has grown revenue to $136.4 million. The company still hasn’t earned a profit, having reported a nearly $67 million loss through the first half of 2024. These numbers also pale in comparison to Nvidia, which recently reported second-quarter revenue of $30 billion and a profit of roughly $16.6 billion.

Will Cerebras make a splash?

With big publicity from news publications and claims of being 20 times faster than Nvidia, I think it’s safe to say that Cerebras already has and will continue to make a splash.

Depending on the excitement investment bankers can drum up during the company’s road show and market conditions, I wouldn’t be surprised to see Cerebras go public at a higher valuation than expected. AI has been all the buzz and the IPO market has been flat for a few years now, so there could be pent-up demand on Wall Street.

Will Cerebras overtake Nvidia? Only time will tell. Its product offerings are impressive, but it still has a ways to go to get its financial profile in line with Nvidia. Furthermore, there may be some advantages to Nvidia having smaller chips and it remains to be seen whether Cerebras can compete with Nvidia’s software language CUDA — although the company does say that its software program “eliminates the need for low-level programming in CUDA.”

While everything sounds great, there is likely still a “show me” component to this story. After all, the bulk of Cerebras’ revenue comes from one customer. Nvidia also has a leading market share in the AI chip space and relationships with many large clients. Who’s to say Nvidia couldn’t use its size — and likely resource — advantage to develop a similar large wafer chip? There’s a lot left to play out, but this could be one of the more interesting developments for market watchers to pay attention to.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

-

Amazon: if you invested $1,000 when we doubled down in 2010, you’d have $21,266!*

-

Apple: if you invested $1,000 when we doubled down in 2008, you’d have $43,047!*

-

Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $389,794!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of October 7, 2024

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Bram Berkowitz has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices, Alphabet, Microsoft, and Nvidia. The Motley Fool recommends Intel and recommends the following options: long January 2026 $395 calls on Microsoft, short January 2026 $405 calls on Microsoft, and short November 2024 $24 calls on Intel. The Motley Fool has a disclosure policy.

The Newest Artificial Intelligence Stock Has Arrived — and It Claims to Make Chips That Are 20x Faster Than Nvidia was originally published by The Motley Fool

On some levels, Advanced Micro Devices (NASDAQ: AMD) looks increasingly like a competitor to Nvidia in the artificial intelligence (AI) accelerator market. While almost everyone perceives Nvidia as the dominant player in this market, AMD raised some eyebrows by winning a contract from Oracle.

Still, for all these accolades, AMD is barely profitable, and its revenue growth rate remains mired in the single digits. Also, despite the Oracle contract, AMD is not yet in Nvidia’s league regarding AI accelerators.

Nonetheless, one AMD metric has shown a dramatic improvement. As that figure continues to grow, the semiconductor stock could take its place as a full-fledged Nvidia competitor in the AI accelerator market.

Where investors should look

The important figure is not so much data center revenue as it is data center revenue as a percentage of total revenue. Here’s why: In the second quarter of 2024, AMD’s revenue of $5.8 billion grew by only 9% yearly. But this figure is deceiving. Gaming revenue dropped 59%, while embedded revenue fell 41%.

However, data center revenue, the segment designing AI accelerators, was up 115%! This is significant because Nvidia’s data center revenue was 88% of the company’s total in the latest quarter. Three years ago, it was not Nvidia’s largest revenue source. Now, the same pattern seems to have appeared in AMD’s financials.

In Q2, the data center was 49% of AMD’s revenue, up from only 25% one year ago. Assuming it is going to follow in Nvidia’s footsteps, AMD’s data center revenue appears on track to continue growing rapidly.

Furthermore, the chip industry is cyclical, meaning the gaming and embedded segments are unlikely to experience revenue declines comparable to the ones over the last year. Both factors should mean that AMD’s overall revenue — and, by extension, net income — are likely to experience dramatic surges, helping to draw more investors into AMD.

Ultimately, market leadership for AMD is unlikely anytime soon. However, as long as the data center segment continues to grow as a percentage of the company’s revenue, it should take its stock dramatically higher.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

-

Amazon: if you invested $1,000 when we doubled down in 2010, you’d have $21,266!*

-

Apple: if you invested $1,000 when we doubled down in 2008, you’d have $43,047!*

-

Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $389,794!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of October 7, 2024

Will Healy has positions in Advanced Micro Devices. The Motley Fool has positions in and recommends Advanced Micro Devices, Nvidia, and Oracle. The Motley Fool has a disclosure policy.

Every AMD Stock Investor Should Keep an Eye on This Number was originally published by The Motley Fool

-

Technology4 weeks ago

Technology4 weeks agoWould-be reality TV contestants ‘not looking real’

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoHyperelastic gel is one of the stretchiest materials known to science

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoHow to unsnarl a tangle of threads, according to physics

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoMaxwell’s demon charges quantum batteries inside of a quantum computer

-

Science & Environment3 weeks ago

Science & Environment3 weeks ago‘Running of the bulls’ festival crowds move like charged particles

-

Womens Workouts3 weeks ago

Womens Workouts3 weeks ago3 Day Full Body Women’s Dumbbell Only Workout

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoLiquid crystals could improve quantum communication devices

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoQuantum ‘supersolid’ matter stirred using magnets

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoSunlight-trapping device can generate temperatures over 1000°C

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoWhy this is a golden age for life to thrive across the universe

-

News4 weeks ago

the pick of new debut fiction

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoHow to wrap your mind around the real multiverse

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoITER: Is the world’s biggest fusion experiment dead after new delay to 2035?

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoNerve fibres in the brain could generate quantum entanglement

-

Science & Environment2 weeks ago

Science & Environment2 weeks agoX-rays reveal half-billion-year-old insect ancestor

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoQuantum forces used to automatically assemble tiny device

-

News3 weeks ago

News3 weeks agoOur millionaire neighbour blocks us from using public footpath & screams at us in street.. it’s like living in a WARZONE – WordupNews

-

Technology2 weeks ago

Technology2 weeks agoIs sharing your smartphone PIN part of a healthy relationship?

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoA slight curve helps rocks make the biggest splash

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoPhysicists are grappling with their own reproducibility crisis

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoLaser helps turn an electron into a coil of mass and charge

-

Business2 weeks ago

Eurosceptic Andrej Babiš eyes return to power in Czech Republic

-

News3 weeks ago

News3 weeks agoYou’re a Hypocrite, And So Am I

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoTime travel sci-fi novel is a rip-roaringly good thought experiment

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoNuclear fusion experiment overcomes two key operating hurdles

-

News4 weeks ago

News4 weeks ago▶️ Hamas in the West Bank: Rising Support and Deadly Attacks You Might Not Know About

-

Sport3 weeks ago

Sport3 weeks agoJoshua vs Dubois: Chris Eubank Jr says ‘AJ’ could beat Tyson Fury and any other heavyweight in the world

-

Science & Environment4 weeks ago

Science & Environment4 weeks agoCaroline Ellison aims to duck prison sentence for role in FTX collapse

-

News3 weeks ago

News3 weeks ago▶️ Media Bias: How They Spin Attack on Hezbollah and Ignore the Reality

-

Business2 weeks ago

Should London’s tax exiles head for Spain, Italy . . . or Wales?

-

Football2 weeks ago

Football2 weeks agoFootball Focus: Martin Keown on Liverpool’s Alisson Becker

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoA new kind of experiment at the Large Hadron Collider could unravel quantum reality

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoRethinking space and time could let us do away with dark matter

-

News4 weeks ago

News4 weeks agoNew investigation ordered into ‘doorstep murder’ of Alistair Wilson

-

News3 weeks ago

The Project Censored Newsletter – May 2024

-

Technology2 weeks ago

Technology2 weeks agoQuantum computers may work better when they ignore causality

-

Technology2 weeks ago

Technology2 weeks ago‘From a toaster to a server’: UK startup promises 5x ‘speed up without changing a line of code’ as it plans to take on Nvidia, AMD in the generative AI battlefield

-

MMA2 weeks ago

MMA2 weeks agoConor McGregor challenges ‘woeful’ Belal Muhammad, tells Ilia Topuria it’s ‘on sight’

-

Sport2 weeks ago

Sport2 weeks agoWatch UFC star deliver ‘one of the most brutal knockouts ever’ that left opponent laid spark out on the canvas

-

News3 weeks ago

Israel strikes Lebanese targets as Hizbollah chief warns of ‘red lines’ crossed

-

Technology4 weeks ago

Technology4 weeks agoThe ‘superfood’ taking over fields in northern India

-

Technology2 weeks ago

Technology2 weeks agoGet ready for Meta Connect

-

Business2 weeks ago

Ukraine faces its darkest hour

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoUK spurns European invitation to join ITER nuclear fusion project

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoA tale of two mysteries: ghostly neutrinos and the proton decay puzzle

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoFuture of fusion: How the UK’s JET reactor paved the way for ITER

-

News3 weeks ago

News3 weeks agoWhy Is Everyone Excited About These Smart Insoles?

-

Health & fitness2 weeks ago

Health & fitness2 weeks agoThe 7 lifestyle habits you can stop now for a slimmer face by next week

-

Health & fitness4 weeks ago

Health & fitness4 weeks agoThe secret to a six pack – and how to keep your washboard abs in 2022

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoWhy we need to invoke philosophy to judge bizarre concepts in science

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoCardano founder to meet Argentina president Javier Milei

-

Politics3 weeks ago

UK consumer confidence falls sharply amid fears of ‘painful’ budget | Economics

-

MMA3 weeks ago

MMA3 weeks agoRankings Show: Is Umar Nurmagomedov a lock to become UFC champion?

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoMeet the world's first female male model | 7.30

-

Womens Workouts3 weeks ago

Womens Workouts3 weeks ago3 Day Full Body Toning Workout for Women

-

Technology3 weeks ago

Technology3 weeks agoRobo-tuna reveals how foldable fins help the speedy fish manoeuvre

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoPhysicists have worked out how to melt any material

-

Womens Workouts3 weeks ago

Womens Workouts3 weeks agoEverything a Beginner Needs to Know About Squatting

-

TV3 weeks ago

TV3 weeks agoCNN TÜRK – 🔴 Canlı Yayın ᴴᴰ – Canlı TV izle

-

News3 weeks ago

News3 weeks agoFour dead & 18 injured in horror mass shooting with victims ‘caught in crossfire’ as cops hunt multiple gunmen

-

Servers computers2 weeks ago

Servers computers2 weeks agoWhat are the benefits of Blade servers compared to rack servers?

-

Technology2 weeks ago

Technology2 weeks agoThe best robot vacuum cleaners of 2024

-

Technology2 weeks ago

Technology2 weeks agoMicrophone made of atom-thick graphene could be used in smartphones

-

News3 weeks ago

News3 weeks agoChurch same-sex split affecting bishop appointments

-

Politics4 weeks ago

Politics4 weeks agoTrump says he will meet with Indian Prime Minister Narendra Modi next week

-

Sport3 weeks ago

Sport3 weeks agoUFC Edmonton fight card revealed, including Brandon Moreno vs. Amir Albazi headliner

-

Health & fitness4 weeks ago

Health & fitness4 weeks agoThe maps that could hold the secret to curing cancer

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoBeing in two places at once could make a quantum battery charge faster

-

News4 weeks ago

News4 weeks agoHow FedEx CEO Raj Subramaniam Is Adapting to a Post-Pandemic Economy

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoTiny magnet could help measure gravity on the quantum scale

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoDecentraland X account hacked, phishing scam targets MANA airdrop

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoDZ Bank partners with Boerse Stuttgart for crypto trading

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoLow users, sex predators kill Korean metaverses, 3AC sues Terra: Asia Express

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoBlockdaemon mulls 2026 IPO: Report

-

Business3 weeks ago

Thames Water seeks extension on debt terms to avoid renationalisation

-

Politics3 weeks ago

‘Appalling’ rows over Sue Gray must stop, senior ministers say | Sue Gray

-

Womens Workouts3 weeks ago

Womens Workouts3 weeks agoBest Exercises if You Want to Build a Great Physique

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoCNN TÜRK – 🔴 Canlı Yayın ᴴᴰ – Canlı TV izle

-

Technology2 weeks ago

Technology2 weeks agoUniversity examiners fail to spot ChatGPT answers in real-world test

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoEthereum is a 'contrarian bet' into 2025, says Bitwise exec

-

Technology3 weeks ago

Technology3 weeks agoiPhone 15 Pro Max Camera Review: Depth and Reach

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoHow one theory ties together everything we know about the universe

-

News3 weeks ago

News3 weeks agoBrian Tyree Henry on voicing young Megatron, his love for villain roles

-

Business4 weeks ago

JPMorgan in talks to take over Apple credit card from Goldman Sachs

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoQuantum time travel: The experiment to ‘send a particle into the past’

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoMost accurate clock ever can tick for 40 billion years without error

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoBitcoin miners steamrolled after electricity thefts, exchange ‘closure’ scam: Asia Express

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoDorsey’s ‘marketplace of algorithms’ could fix social media… so why hasn’t it?

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoBitcoin bulls target $64K BTC price hurdle as US stocks eye new record

-

News3 weeks ago

Brian Tyree Henry on voicing young Megatron, his love for villain roles

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoCoinbase’s cbBTC surges to third-largest wrapped BTC token in just one week

-

Politics2 weeks ago

Politics2 weeks agoHope, finally? Keir Starmer’s first conference in power – podcast | News

-

News2 weeks ago

News2 weeks agoUS Newspapers Diluting Democratic Discourse with Political Bias

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoLouisiana takes first crypto payment over Bitcoin Lightning

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoHow do you recycle a nuclear fusion reactor? We’re about to find out

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoRedStone integrates first oracle price feeds on TON blockchain

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks ago‘No matter how bad it gets, there’s a lot going on with NFTs’: 24 Hours of Art, NFT Creator

-

Business3 weeks ago

How Labour donor’s largesse tarnished government’s squeaky clean image

-

Travel3 weeks ago

Travel3 weeks agoDelta signs codeshare agreement with SAS

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoCrypto scammers orchestrate massive hack on X but barely made $8K

You must be logged in to post a comment Login