Money

In Conversation With… William Marshall: Retirement Realities & Investment Insights

In this episode of In Conversation With…, Kimberley Dondo talks with William Marshall, CIO and Head of Wealth Investment at Hymans Robertson Investment Services. They dive into key topics like sequencing risk, debunking longevity myths, and how Hymans Robertson’s holistic approach supports clients in retirement. William also addresses how the Consumer Duty has shaped the focus on value for money, the balance between passive and active investing, and the role of factor investing in portfolio design. Tune in now:

EBAY is set to ban private sales of a popular product in the UK, citing increasing safety concerns.

The move will come into effect on October 31, with only “eligible business sellers” allowed to continue offering the item on the platform.

2

2

The clampdown focuses on e-bikes and their batteries, following a sharp rise in incidents involving battery fires.

The London Fire Brigade reported 155 e-bike fires so far this year, a jump of 78% compared to 2022.

E-bikes, equipped with electrically-assisted pedals and battery power, have surged in popularity, but their safety has come under scrutiny.

In one tragic case, a man died when a battery pack he was charging overheated and ignited, leading to a house fire.

Read more on banned items

The UK’s regulatory body recently classified e-bike battery packs as “dangerous products,” further intensifying calls for better consumer protection.

An eBay spokesperson said: “Consumer safety is a top priority for eBay,” adding that the firm would audit sellers to ensure they meet CE mark safety standards for listed products.

The charity Electrical Safety First has praised eBay’s decision but insists new laws are necessary to safeguard consumers across all online platforms.

A spokesperson said: “We are encouraged to see eBay take proactive steps in an attempt to reduce the risk of substandard batteries entering people’s homes, as they pose a serious risk of fire if they fail.

“Whilst this voluntary move is welcome, we continue to call for online marketplaces to be legally obligated to take reasonable steps to ensure products sold via their sites are safe.

“We hope the Product Regulation and Metrology Bill will mandate this.

“This legislation must also be used to prevent battery fires by introducing mandatory third-party certification for e-bikes, e-scooters and their batteries to stop poor quality products from entering the market.

“It should also introduce more robust standards for conversion kits and regulations for charging.“

The Product Regulation and Metrology Bill, currently progressing through Parliament, could eventually make these obligations law.

For now, eBay’s ban on private e-bike sales is seen as a crucial step toward reducing fire risks associated with the product.

Despite the impending restrictions, nearly 3,000 used e-bikes are still available on eBay, highlighting the challenge of managing the growing demand for these vehicles while ensuring safety.

Meanwhile, earlier this year a man was forced to flee through a bedroom window after a house erupted into flames when an e-bike battery exploded.

Leicestershire Fire and Rescue Service was able to confirm that a lithium battery in the ebike overheated and caused a severe fire.

The fire service reminded e-bike owners to use the correct charger, never leave the device unattended and allow the battery to cool before charging.

Elsewhere, in another tragic case, the grieving boyfriend of a model killed in a horror e-bike flat blaze told how he tried to battle through flames to save her.

The 21-year-old was forced to jump out of a window naked when smoke billowed through his flat in London.

A fireball erupted through their home when on New Year’s Day 2023 when a dodgy ebike battery exploded.

The dangers of e-bikes

Last year, 11 people lost their lives to fires involving e-bikes and e-scooters, with hundreds injured as a result of the fires caused by the lithium-ion batteries.

Other victims include Sofia Duarte, who died in London on New Year’s Day 2023 at the age of 21, when a converted e-bike caught fire during the night.

Sofia was unable to escape the building with the fire blocking her escape route.

Alda Simoes, a friend of Ms Duarte, said: “We are out of time to save our beautiful Sofia and everyone that has passed away like her.

“But we will do everything in our power to prevent others going through what Sofia’s mum, me, family and friends are going through.

“This problem is a public safety issue that needs action from all political parties to introduce new measures to tackle the increasingly problem of e-bike battery fires.

“The number of these fires caused by these batteries keeps rising and we urgently need intervention to protect the public.

“Change needs to happen. There are people dying, what are we waiting for? Sofia’s death must have a purpose. If nothing changes, her death will be in vain.

“I am urging the next Government and all political parties to please, help us create change.”

On March 21, fire crews were called to an exploding e-bike on a train platform in Sutton, London, with dramatic footage showing flaming battery cells being projected from the battery across the platform.

Fire crews in Wakefield, West Yorkshire, were called to a property fire on April 6 following a severe fire that resulted in one person being taken to hospital with serious injuries.

The cause was deemed to be a charging e-bike.

Five others suffered minor injuries.

Four children were among six people taken to hospital due to smoke inhalation following an e-bike fire near Croydon at the beginning of April that caused serious damage to their maisonette, destroying the staircase between the first and second floor

Do you have a money problem that needs sorting? Get in touch by emailing money-sm@news.co.uk.

Plus, you can join our Sun Money Chats and Tips Facebook group to share your tips and stories

Scottish Widows has launched a flexible income protection product to help bridge the gender protection gap.

The product has been designed to be simple and easy to understand for established protection advisers, holistic advisers and those who may be new to advising in this area.

Research by Scottish Widows found that just 8% of people in the UK have cover in place if their income stopped suddenly.

Meanwhile, 42% of UK adults worry that their household wouldn’t cope if they were unable to work.

The data also revealed a gender protection gap with 29% of surveyed women saying they could not afford protection compared with 23% of men.

Over a quarter (29%) of women surveyed said they would expect to rely on a partner’s income if they could not work.

Scottish Widows’s intention with its new product is to build financial resilience for clients against financial shocks in their moment of need and enable a greater number of advisers to incorporate income protection into their recommendations.

The launch enhances the suite of products available through the recently digitised Scottish Widows Protect platform and via the UnderwriteMe Protection Platform portal; the product will be available on other protection portals in the coming weeks.

These latest developments provide advisers with a streamlined application process, an accelerated underwriting journey, and a better client experience.

As part of the launch, Scottish Widows has joined the Income Protection Task Force (IPTF), formalising its long-term commitment to open dialogue on ways to extend income protection across the country.

Product benefits

- Fracture and hospitalisation cover – included as standard with no extra charge.

- Rehabilitation/Proportionate benefit – a top-up payment to help clients resume work.

- Partnership benefits- clients can benefit from a range of partnerships available through Scottish Widows Protect:

- ‘Clinic in a Pocket’ (included in cover) to receive a GP sick note quickly and access to a GP 24/7

- A dedicated personal nurse service in partnership with Red Arc.

- Immediate income payment – received whilst the claim is still being assessed, provided a GP note is supplied and once the deferred period has passed.

- Mental health underwriting – Scottish Widows won’t decline an income protection application for mental health without an underwriting review conducted by a real person, rather than AI. We also ask the customer if they’re doing anything to improve their condition, for example improved nutrition, sleep or exercise. Where customers are proactively taking steps to improve their mental health we can provide better underwriting rates.

- Price lock promise – guarantees the quote for up to 12 months, subject to underwriting terms being imposed.

- Reduced earnings with our minimum benefit guarantee, even if your client’s earnings have reduced, as long as their monthly claim payment is more than £1,500, we won’t pay them less than this.

Scottish Widows protection director Rose St Louis said: “Life doesn’t always go in a straight line and an unexpected adverse health event can have a significant impact on our ability to remain financially stable.

“This is where products like income protection can come to the rescue and have a meaningful impact in reducing income ‘troughs’ if you’re unable to work due to illness or disability.

“Launching income protection is part of our effort to help customers feel prepared, no matter what life throws at them.

“Our research shows women are less likely to have protection, and we want to be part of the solution towards closing the gender protection gap while also making it easy for established protection writers, as well as those new to protection, to write this type of business.”

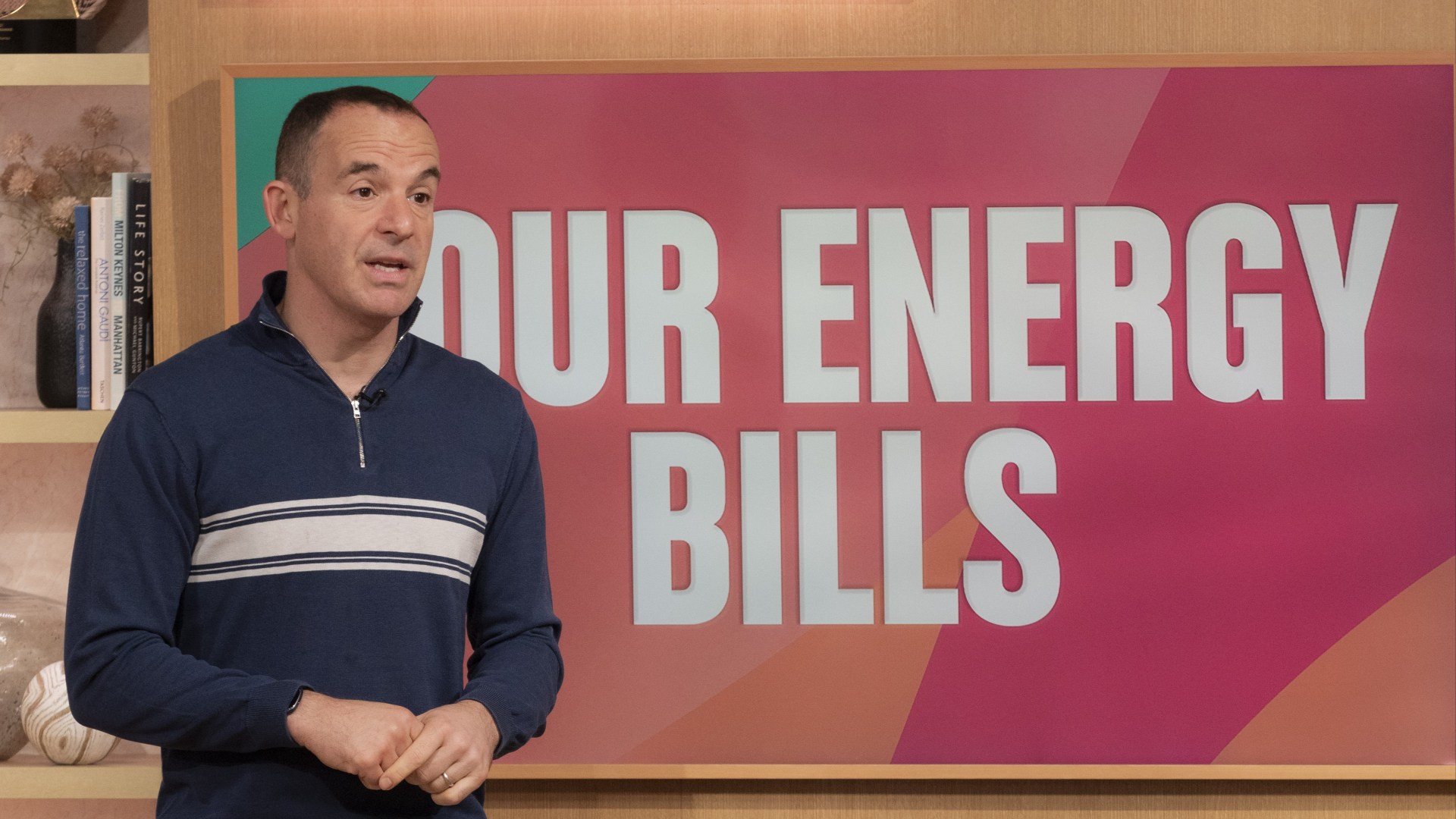

Money

Martin Lewis issues warning for 28million households to ‘act ASAP’ and save on energy bills as suppliers pull deals

MARTIN Lewis has issued a warning to millions of households who could slash their energy bills.

Last week, the energy price cap jumped from £1,568 to £1,717 a year.

1

This means that bills have risen by 10%, and the average household bill is up by more than £12 a month, or £149 a year.

However, Martin Lewis said: “Last week, the energy pants price cap, which dictates the rate eight in 10 homes in Eng, Scotland and Wales pay, rose by 10%

“Yet, for now, the deals you can compare and switch to are far cheaper.

“That’s why last week I called the current cap a pants cap, as, stay on it, and you’ll miss out on savings.”

Around 28million households are on standard variable tariffs, which are affected by the price cap, according to Ofgem.

However, there are several fixed energy deals that beat these tariffs.

The founder of MoneySavingExpert.com said: “A fix gives you peace of mind that the rate won’t change for a set time.

“Currently, a host of one-year fixes hugely undercut the price cap.

“Yet world turmoil has hit oil prices, and there’s potential knock-on to energy prices, so we’ve already seen three of last week’s cheapest fixes pulled and replaced with more expensive ones.”

EDF Energy also pulled the cheapest fixed deal on the market on Monday.

Those who signed up for the Essentials Fixed 1Yr Oct25v3 tariff were promised savings of £163 a year.

As a result, Martin added: “So for the short term, the mood music seems to say fixing ASAP is the safest route.”

The cheapest fixed deal available right now can still save the average household £162 a year.

How do fixed deals work?

Fixed deals work to protect customers from bill hikes if Ofgem were to increase the price cap in the future.

Customers on their supplier’s standard variable tariff see their energy prices change every three months, as these are tied to Ofgem’s price cap.

However, those who lock into a fixed energy deal are charged the same gas and electricity rates throughout the contract’s term.

Of course, doing so carries a slight risk of you paying more than those on the standard variable tariff if Ofgem’s energy price cap were to fall within your deal’s term.

The price cap is reviewed every three months in Oct, Jan, April and July, and can go up or down depending on what’s happening in the wholesale energy market.

Since October 1, those on the standard variable tariff (SVT) have had their rates capped by Ofgem at the following levels:

- 5.48p per kilowatt hour (p/kWh) for gas

- 22.36p per kWh for electricity

- A standing charge of 31.66p per day for gas

- A standing charge of 60.99p per day for electricity

- For a typical household that uses an average of 11,500kWh of gas and 2,700kWh of electricity every year, these rates will cap bills at roughly £1,717 .

As this is only an estimate for a typical household, if you use more energy, you’ll pay more.

But if you’re offered a fix that’s cheaper than October’s price cap, it’s always worth considering.

How can I check future price cap predictions?

EDF Energy has launches a brand new Ofgem price cap prediction tool on its website.

The energy company updates the tool with new information about changes to the cap on energy prices every Tuesday.

It also includes advice on how this affects your energy tariff choices.

You can find out more by visiting edfenergy.com/gas-and-electricity/price-cap-predictions.

Which suppliers are offering the best-fixed deals?

Outfox the Market is currently offering the cheapest deal on the open market right now.

Its Fix’d Dual Oct24 v5.0 tariff costs a typical household £1,555 a year.

This means it is £162 cheaper than Ofgem’s October price cap.

It comes with a £25 exit fee per fuel or £50 if you lock in with a dual fuel tariff.

British Gas‘ The Fixed Tariff v5 tariff matches the Outfox the Market deal, but it comes with a £50 exit dee per fuel.

Octopus Energy’s 12M Fixed October 2024 v1 costs £1,566 a year – £151 less than Ofgem’s October price cap.

This deal also comes with no exit fees, so customers can ditch and switch suppliers at any time.

Remember to always compare prices before switching, as energy tariffs vary widely, and costs differ depending on where you live.

Outfox the Market, Ovo Energy and British Gas fixes are available to those with or without a smart meter.

What are the alternatives?

Customers unwilling to commit to long-term fixed energy deals may want to consider flexible tariffs.

Kara Gammell, personal finance expert at comparison site Money Supermarket Group, says: “These will almost always be at or below the price cap.”

For example, E.ON Next‘s Pledge variable tariff offers a fixed discount of around three per cent on the price cap rates for 12 months.

It will save the average household around £50 a year but comes with a £50 exit fee if you switch before the year ends.

The deal is available to both new and existing customers.

EDF Energy’s Ensure Tracker works in a similar way and offers a £50 discount off the price cap’s standing charges for 12 months.

For a bigger reward but at a higher risk, Octopus Energy offers two variable tariffs which track wholesale gas and electricity costs.

Customers on the Octopus Tracker see their prices change daily, but unit rates have remained consistently lower than the price cap in recent months.

The Agile Octopus tariff works similarly to the Octopus Tracker, but the main difference is that the former’s prices change every half hour.

Remember that those wishing to switch to any of these tracker tariffs must have a smart meter.

What energy bill help is available?

THERE’S a number of different ways to get help paying your energy bills if you’re struggling to get by.

If you fall into debt, you can always approach your supplier to see if they can put you on a repayment plan before putting you on a prepayment meter.

This involves paying off what you owe in instalments over a set period.

If your supplier offers you a repayment plan you don’t think you can afford, speak to them again to see if you can negotiate a better deal.

Several energy firms have grant schemes available to customers struggling to cover their bills.

But eligibility criteria varies depending on the supplier and the amount you can get depends on your financial circumstances.

For example, British Gas or Scottish Gas customers struggling to pay their energy bills can get grants worth up to £2,000.

British Gas also offers help via its British Gas Energy Trust and Individuals Family Fund.

You don’t need to be a British Gas customer to apply for the second fund.

EDF, E.ON, Octopus Energy and Scottish Power all offer grants to struggling customers too.

Thousands of vulnerable households are missing out on extra help and protections by not signing up to the Priority Services Register (PSR).

The service helps support vulnerable households, such as those who are elderly or ill, and some of the perks include being given advance warning of blackouts, free gas safety checks and extra support if you’re struggling.

Get in touch with your energy firm to see if you can apply.

If there’s one thing that consistently worries the financial advice sector, it’s the looming capacity crunch.

The statistics are well known: a recent Investec survey found 49% of financial advisers and planners intended to retire within the next five years, while 35% aimed to retire by age 50. And this is only the latest in a long line of such findings.

So, why aren’t these numbers being replaced? Again, it’s a familiar story: in some cases, young people see financial advice as not relevant to them, as something “stuffy and old-fashioned”, in the words of the LIBF’s John Somerville.

These initiatives are a great starting point, but they should act as a spur for a much bigger push

Others may feel, incorrectly, that they lack the necessary skills. Or they are put off by the routes to qualification, seeing them as arduous and expensive. Or the advice firms themselves are reluctant to invest in new talent.

But the overwhelming problem is a lack of awareness. According to the CII’s Claire Bishop, “Often, it’s just not something that’s on the radar of people at school, university or college.” The same is true for careers advisers.

This is despite the opportunities financial advice offers in terms of role diversity, opportunity, location, salary and self-employment. It is a sector that suits a wide range of talent and abilities; as Bishop puts it: “There’s an assumption that it’s all about maths. And it’s not. It’s about helping people and understanding people.”

All of the schemes agree that collaboration is vital

And, while no one would describe it as an easy profession, research last year by Dynamic Planner revealed that nine in 10 advisers under 30 would recommend financial advice as a career. There aren’t many other professions that could make that claim.

So, it’s time the sector pulled together and did more to promote itself. If financial advice is so rewarding, why don’t more people know about it? And, if everyone in the profession is agreed that we have a problem, why not collaborate more on the solutions?

Fortunately, there are plenty of initiatives out there that are doing just that. This month’s cover feature highlights four of them: CII’s virtual work-experience programme with Springpod; the New Talent Alliance; The Verve Foundation’s ‘We Are Change’ initiative; and Future Financial Adviser.

In some cases, young people see financial advice as not relevant to them, as something stuffy and old-fashioned

All of these are promoting opportunities to young people and assisting them on their journey. All of them are helping to push financial advice into the spotlight. And all of them agree that collaboration is vital.

However, we need to do more. These initiatives are a great starting point, but they should act as a spur for a much bigger push.

So, if you know of a project that is addressing the adviser gap, or you have any thoughts that aren’t addressed in our feature, we’d love to hear from you!

Tom Browne is editor of Money Marketing. Contact him at: tom.browne@moneymarketing.co.uk

This article featured in the October 2024 edition of Money Marketing.

If you would like to subscribe to the monthly magazine, please click here.

Good morning and welcome to your Morning Briefing for Wednesday 9 October 2024. To get this in your inbox every morning click here.

#ICYMI: The news from MMI London

‘Selling your advice firm should be the the last option’

Advisers are ‘flip flopping’ due to the upcoming Budget

FOS and FCA should work together on simplified advice

‘Money is an emotional lightning rod,’ says TFP Financial Planning director

Chancellor Reeves ‘wrapping herself in a straight jacket’ ahead of Budget

Shouting about advice

If there’s one thing that consistently worries the financial advice sector, it’s the looming capacity crunch.

The statistics are well known: a recent Investec survey found 49% of financial advisers and planners intended to retire within the next five years, while 35% aimed to retire by age 50. And this is only the latest in a long line of such findings.

So, why aren’t these numbers being replaced? Again, it’s a familiar story: in some cases, young people see financial advice as not relevant to them, as something “stuffy and old-fashioned”, in the words of the LIBF’s John Somerville.

In Conversation With… Hymans Robertson’s William Marshall

In this episode of In Conversation With…, Kimberley Dondo talks with William Marshall, CIO and head of wealth investment at Hymans Robertson Investment Services.

They dive into key topics like sequencing risk, debunking longevity myths, and how Hymans Robertson’s holistic approach supports clients in retirement. William also addresses how the Consumer Duty has shaped the focus on value for money, the balance between passive and active investing, and the role of factor investing in portfolio design. Tune in now:

Scottish Widows income protection

Scottish Widows has launched a flexible income protection product to help bridge the gender protection gap.

The product has been designed to be simple and easy to understand for established protection advisers, holistic advisers and those who may be new to advising in this area.

Quote Of The Day

A move like this could stoke fear amongst public sector workers that the government is coming for their pensions.

– Graham Crossley, NHS pension specialist at Quilter, comments on reports that the Chancellor is considering cutting the amount that can be taken tax-free from pensions to £100,000

Stat Attack

New research from Pay.UK reveals a gap between how much people say they understand about money and the reality.

It shows:

78%

of UK adults consider themselves financially literate.

71%

However, almost three quarters of respondents don’t know how a savings account works.

19%

Among those who view themselves as financially literate, a fifth run out of money every month.

41%

This figure climbs to 41% for those who don’t consider themselves literate.

27%

Of the respondents who feel confident in their ability to manage finances, over a quarter find themselves running out of money up to every two months.

28%

of UK adults save regularly with a plan for rainy days.

6%

don’t save at all.

35%

of Brits use a manual approach to manage their finances (such as notebooks and spreadsheets)

30%

Have taken the initiative to learn about financial terms like pensions and taxes outside of school.

86%

of UK adults feel personal finance education should be on the national curriculum.

29%

of respondents could not define what a savings account is,

35%

struggled to explain what an Isa is.

Source: Pay.UK

In Other News

Progeny has appointed Phillip Liu to the role of director of data and digital.

A newly created role, the director of data and digital will lead an increasingly data-driven approach and provide strategic leadership to Progeny’s data team.

With over 20 years in data leadership, Liu is an experienced transformational data change leader and was previously at Atlanta Group as director of data.

He has also held leadership roles for Yorkshire Building Society, General Electric and International Personal Finance.

In his new role at Progeny, Liu will have responsibility for overseeing, building on and enhancing the group’s data capability, to help inform and support Progeny’s continued growth.

He will also act as data protection officer, overseeing all aspects of data stewardship, data quality and data protection.

KPMG US chief cites urgent need to halt slide in accounting ranks (Financial Times)

Chinese stocks tumble as stimulus skepticism keeps bulls at bay (Bloomberg)

India cenbank holds rates, shifts stance to ‘neutral’ signalling rate cuts ahead (Reuters)

Did You See?

Believe it or not, we’ll soon be turning our attention to 2025 – and it might be a year for advisers to take particular notice of, says Nucleus’s Laura Barnes.

If estimates from The Centre of Economics and Business Research are correct, women will hold 60% of the UK’s wealth from next year. That’s a hefty amount.

As women’s wealth grows, the hope would be they increasingly look to seek professional advice on how best to manage it.

Of course, some will have been responsible for their own wealth creation and may already be benefitting from the peace of mind that comes with advice.

Money

A little-known benefit paid out £3,500 when my partner died – it’s not means tested and takes minutes to apply

WHEN Isabella Day’s partner Ford unexpectedly died in August, she was forced to navigate running a small business and a household budget alone while grieving.

The 51-year-old goldsmith, from Devon, had worked with Ford Hallam selling hand-made gold jewellery at a store in Dartmouth and through website isabelladay.co.uk for years.

1

Ford was also a skilled craftsman and could restore items such as swords, and he was the only non-native artist to have been adopted into Japan’s ancient decorative metalworking tradition.

He was 61 when he died due to complications arising from an auto immune disease, leaving Isabella stunned and heartbroken.

She told The Sun: “It was a massive shock when he died. We were engaged, due to be married in October but instead of planning a wedding, I had to plan a funeral.”

The pair had lived together as a blended family with Isabella’s two sons 16 and 25 and one of Ford’s sons, 22.

Ford had no life insurance or pension when he died, so the drop in income left Isabella’s finances and business under huge pressure, too.

Two of their sons are in full-time education and so aren’t able to contribute to the family budget, and this month the 25-year-old has just moved into his own flat.

“I was struggling emotionally and grieving but I was now also solely responsible for the business that I had with Ford,” Isabella said.

“You can’t just scale up a skilled craft business when someone else’s output is no longer there.”

Feeling desperate for help, Isabella went to Citizen’s Advice in September to see if there was any financial support she could access.

The organisation told her about the Bereavement Support Allowance.

The benefit gives lump sum payments of up to £3,500 after a partner has died, as well as ongoing payments up to £350 for 18 months.

Within days of applying, she received the payment.

“I was really surprised to find out about it, but the whole thing has been amazing – it was so easy to apply, I did it in about 20 minutes,” she said.

“And it was facts that you can manage while you are grieving, I didn’t need to go into the details of the death or anything traumatic.”

The Bereavement Support Allowance is not mean-tested and it’s available even if you are not married to your partner – though you will have had to have been living together.

You will need to be under state pension age and your partner’s National Insurance contributions will need to be up to date for you to qualify.

Isabella added: “I just wish I had known about it sooner. In hospital they give you a booklet when your partner dies, but there was no mention of this benefit.

“It’s a lot of money and made a significant difference to us.

“I think a lot of women could benefit from knowing about this support, especially small business owners. There needs to be greater awareness of it.”

What is the Bereavement Support Allowance?

If your partner dies when you are under State Pension age you could claim for the Bereavement Support Payment.

The benefit isn’t means-tested so it doesn’t matter what your income is, if you have any savings or if you’re working.

The benefit is available if you were married, but you can also claim if you and your partner were living together, and you look after a child which you get Child Benefit for.

If you have children under the or you’re pregnant, you can get a lump sum payment of £3,500, as well as monthly payments of £350 for up to 18 months.

If you don’t have children and are married, you can still get support. You’ll be entitled to a lump sum payment of £2,500, plus monthly payments of £100 for up to 18 months.

You’ll be asked for your National Insurance number as well as your partners as part of the application.

You usually need to make a claim within 21 months of your partner’s death – and in most situations you’ll need to claim within three months of death to get the full amount of payments.

You can apply for the Bereavement Support Payment by filling in a form from the gov website or calling the Bereavement Service helpline on 0800 151 2012.

If you need more help, you can contact Citizens Advice in England on 0800 144 8848. You can also talk online or find your nearest Citizens Advice at citizensadvice.org.uk.

Where to get support for bereavement

There is lots of help and available if you are experiencing grief after the death of a loved one.

NHS therapy and counselling services – NHS talking therapies services are for people in England aged 18 or over. You can speak to your GP about talking therapies or get in touch with the talking therapies service directly without going to your GP.

At a loss – Find bereavement services and counselling across the UK

Child Bereavement UK – Offers support if you are bereaved after losing a child. Or if you’re a child or young person who is grieving after losing someone.

The Good Grief Trust – a charity run by bereaved people, helping all those experiencing grief in the UK.

Samaritans – if you’re struggling you can call Samaritans any time on 116 123 to talk about anything.

-

Womens Workouts2 weeks ago

Womens Workouts2 weeks ago3 Day Full Body Women’s Dumbbell Only Workout

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoHow to unsnarl a tangle of threads, according to physics

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoHyperelastic gel is one of the stretchiest materials known to science

-

Technology3 weeks ago

Technology3 weeks agoWould-be reality TV contestants ‘not looking real’

-

Science & Environment3 weeks ago

Science & Environment3 weeks ago‘Running of the bulls’ festival crowds move like charged particles

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoMaxwell’s demon charges quantum batteries inside of a quantum computer

-

News2 weeks ago

News2 weeks agoOur millionaire neighbour blocks us from using public footpath & screams at us in street.. it’s like living in a WARZONE – WordupNews

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoSunlight-trapping device can generate temperatures over 1000°C

-

News3 weeks ago

the pick of new debut fiction

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoHow to wrap your mind around the real multiverse

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoQuantum ‘supersolid’ matter stirred using magnets

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoLiquid crystals could improve quantum communication devices

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoITER: Is the world’s biggest fusion experiment dead after new delay to 2035?

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoQuantum forces used to automatically assemble tiny device

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoPhysicists are grappling with their own reproducibility crisis

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoWhy this is a golden age for life to thrive across the universe

-

News3 weeks ago

News3 weeks agoYou’re a Hypocrite, And So Am I

-

Sport3 weeks ago

Sport3 weeks agoJoshua vs Dubois: Chris Eubank Jr says ‘AJ’ could beat Tyson Fury and any other heavyweight in the world

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoTime travel sci-fi novel is a rip-roaringly good thought experiment

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoLaser helps turn an electron into a coil of mass and charge

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoCaroline Ellison aims to duck prison sentence for role in FTX collapse

-

Business2 weeks ago

Eurosceptic Andrej Babiš eyes return to power in Czech Republic

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoNuclear fusion experiment overcomes two key operating hurdles

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoNerve fibres in the brain could generate quantum entanglement

-

Technology2 weeks ago

Technology2 weeks ago‘From a toaster to a server’: UK startup promises 5x ‘speed up without changing a line of code’ as it plans to take on Nvidia, AMD in the generative AI battlefield

-

Football2 weeks ago

Football2 weeks agoFootball Focus: Martin Keown on Liverpool’s Alisson Becker

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoRethinking space and time could let us do away with dark matter

-

News3 weeks ago

News3 weeks ago▶️ Hamas in the West Bank: Rising Support and Deadly Attacks You Might Not Know About

-

Science & Environment2 weeks ago

Science & Environment2 weeks agoX-rays reveal half-billion-year-old insect ancestor

-

MMA2 weeks ago

MMA2 weeks agoConor McGregor challenges ‘woeful’ Belal Muhammad, tells Ilia Topuria it’s ‘on sight’

-

News3 weeks ago

News3 weeks ago▶️ Media Bias: How They Spin Attack on Hezbollah and Ignore the Reality

-

Business2 weeks ago

Should London’s tax exiles head for Spain, Italy . . . or Wales?

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoA slight curve helps rocks make the biggest splash

-

News3 weeks ago

News3 weeks agoNew investigation ordered into ‘doorstep murder’ of Alistair Wilson

-

News3 weeks ago

Israel strikes Lebanese targets as Hizbollah chief warns of ‘red lines’ crossed

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoA new kind of experiment at the Large Hadron Collider could unravel quantum reality

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoFuture of fusion: How the UK’s JET reactor paved the way for ITER

-

Technology2 weeks ago

Technology2 weeks agoQuantum computers may work better when they ignore causality

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoUK spurns European invitation to join ITER nuclear fusion project

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoWhy we need to invoke philosophy to judge bizarre concepts in science

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoCardano founder to meet Argentina president Javier Milei

-

News2 weeks ago

News2 weeks agoWhy Is Everyone Excited About These Smart Insoles?

-

Science & Environment2 weeks ago

Science & Environment2 weeks agoMeet the world's first female male model | 7.30

-

Technology2 weeks ago

Technology2 weeks agoGet ready for Meta Connect

-

Health & fitness2 weeks ago

Health & fitness2 weeks agoThe 7 lifestyle habits you can stop now for a slimmer face by next week

-

Health & fitness3 weeks ago

Health & fitness3 weeks agoThe maps that could hold the secret to curing cancer

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoLow users, sex predators kill Korean metaverses, 3AC sues Terra: Asia Express

-

News3 weeks ago

The Project Censored Newsletter – May 2024

-

Politics3 weeks ago

UK consumer confidence falls sharply amid fears of ‘painful’ budget | Economics

-

Womens Workouts3 weeks ago

Womens Workouts3 weeks agoBest Exercises if You Want to Build a Great Physique

-

Womens Workouts3 weeks ago

Womens Workouts3 weeks agoEverything a Beginner Needs to Know About Squatting

-

News2 weeks ago

News2 weeks agoFour dead & 18 injured in horror mass shooting with victims ‘caught in crossfire’ as cops hunt multiple gunmen

-

Womens Workouts2 weeks ago

Womens Workouts2 weeks ago3 Day Full Body Toning Workout for Women

-

Technology2 weeks ago

Technology2 weeks agoRobo-tuna reveals how foldable fins help the speedy fish manoeuvre

-

Sport1 week ago

Sport1 week agoWatch UFC star deliver ‘one of the most brutal knockouts ever’ that left opponent laid spark out on the canvas

-

Sport3 weeks ago

Sport3 weeks agoUFC Edmonton fight card revealed, including Brandon Moreno vs. Amir Albazi headliner

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoEthereum is a 'contrarian bet' into 2025, says Bitwise exec

-

Health & fitness3 weeks ago

Health & fitness3 weeks agoThe secret to a six pack – and how to keep your washboard abs in 2022

-

Business3 weeks ago

JPMorgan in talks to take over Apple credit card from Goldman Sachs

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoQuantum time travel: The experiment to ‘send a particle into the past’

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoBeing in two places at once could make a quantum battery charge faster

-

Technology3 weeks ago

Technology3 weeks agoThe ‘superfood’ taking over fields in northern India

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoA tale of two mysteries: ghostly neutrinos and the proton decay puzzle

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoBitcoin miners steamrolled after electricity thefts, exchange ‘closure’ scam: Asia Express

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoDorsey’s ‘marketplace of algorithms’ could fix social media… so why hasn’t it?

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoDZ Bank partners with Boerse Stuttgart for crypto trading

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoBitcoin bulls target $64K BTC price hurdle as US stocks eye new record

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoBlockdaemon mulls 2026 IPO: Report

-

TV2 weeks ago

TV2 weeks agoCNN TÜRK – 🔴 Canlı Yayın ᴴᴰ – Canlı TV izle

-

Science & Environment2 weeks ago

Science & Environment2 weeks agoCNN TÜRK – 🔴 Canlı Yayın ᴴᴰ – Canlı TV izle

-

Servers computers2 weeks ago

Servers computers2 weeks agoWhat are the benefits of Blade servers compared to rack servers?

-

News2 weeks ago

News2 weeks agoUS Newspapers Diluting Democratic Discourse with Political Bias

-

Technology2 weeks ago

Technology2 weeks agoThe best robot vacuum cleaners of 2024

-

News3 weeks ago

News3 weeks agoChurch same-sex split affecting bishop appointments

-

Politics3 weeks ago

Politics3 weeks agoTrump says he will meet with Indian Prime Minister Narendra Modi next week

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoHow one theory ties together everything we know about the universe

-

News3 weeks ago

News3 weeks agoBrian Tyree Henry on voicing young Megatron, his love for villain roles

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoTiny magnet could help measure gravity on the quantum scale

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoHow do you recycle a nuclear fusion reactor? We’re about to find out

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoDecentraland X account hacked, phishing scam targets MANA airdrop

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoRedStone integrates first oracle price feeds on TON blockchain

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks ago‘No matter how bad it gets, there’s a lot going on with NFTs’: 24 Hours of Art, NFT Creator

-

Business3 weeks ago

Thames Water seeks extension on debt terms to avoid renationalisation

-

Business3 weeks ago

How Labour donor’s largesse tarnished government’s squeaky clean image

-

Politics3 weeks ago

‘Appalling’ rows over Sue Gray must stop, senior ministers say | Sue Gray

-

News3 weeks ago

Brian Tyree Henry on voicing young Megatron, his love for villain roles

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoCoinbase’s cbBTC surges to third-largest wrapped BTC token in just one week

-

MMA3 weeks ago

MMA3 weeks agoRankings Show: Is Umar Nurmagomedov a lock to become UFC champion?

-

Travel2 weeks ago

Travel2 weeks agoDelta signs codeshare agreement with SAS

-

Politics2 weeks ago

Politics2 weeks agoHope, finally? Keir Starmer’s first conference in power – podcast | News

-

Business1 week ago

Ukraine faces its darkest hour

-

Technology3 weeks ago

Technology3 weeks agoiPhone 15 Pro Max Camera Review: Depth and Reach

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoCrypto scammers orchestrate massive hack on X but barely made $8K

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoSEC asks court for four months to produce documents for Coinbase

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks ago‘Silly’ to shade Ethereum, the ‘Microsoft of blockchains’ — Bitwise exec

-

Womens Workouts3 weeks ago

Womens Workouts3 weeks agoHow Heat Affects Your Body During Exercise

-

Womens Workouts3 weeks ago

Womens Workouts3 weeks agoKeep Your Goals on Track This Season

-

Technology2 weeks ago

Technology2 weeks agoIs sharing your smartphone PIN part of a healthy relationship?

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoPhysicists have worked out how to melt any material

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoSingle atoms captured morphing into quantum waves in startling image

You must be logged in to post a comment Login